ATRESMEDIA

|

|

|

- Preston Carr

- 5 years ago

- Views:

Transcription

1 ATRESMEDIA Presentation to investors January

2 Advertising market in Spain 9M 15: A very positive year 9M 15 Gross Ad market Yoy growth 8% 7% 11% 5% 1% Total Ad market 6% Source: Infoadex 2

3 Advertising market in Spain TV: Clear leadership and upward trend Spanish Ad spending by medium Share 41.6% 42.0% +0.4pp 26.8% 21.9% +21.6pp 13.6% -13.2pp 10.8% 9.3% 9.1% 5.3% 1.3% +0.2pp -5.5pp e Source: Infoadex. 2015e: assuming growth rates at 9M15 3

4 Advertising market in Spain Total & TV market vs GDP is bouncing back Total & TV ad intensity (vs GDP) 0.94% Total Ad market All-time average= 0.73% TV Ad market 0.33% 0.44% All-time average= 0.29% 0.19% Source: Infoadex and Bank of Spain 4

5 Advertising market in Spain Spanish TV: Best cost-coverage mix Cost-coverage by medium In /1,000 impacts & % penetration % 67% 60% 88% % Coverage CPT Source: Internal estimates & EGM data 5

6 Spanish TV industry Key issues: Ad market recovery & industry changes 2016 key issues Ad market Macro outlook Ad market growth Industry changes More DTT channels New players: Pay TV & OTTs 6

7 Spanish TV industry: Main drivers Positive outlook for household consumption & GDP Household Consumption & GDP Yoy growth Consumption GDP 3.9% 1.4% 2.7% 4.1% 3.7% -0.5% -1.1% 1.0% -1.9% -2.1% Consensus e 2016e Source: Funcas (Dec 15). In nominal terms 7

8 Spanish TV industry: Ad market Recovery seems sustainable but the size of the market is still low in historical levels Gross TV Ad market In mill % yoy Gross TV Ad market 3,469 2,317 2,378 2,472 Average: 2,475 1,703 1,890 2,015 16% 10% 8% 9% 4% 11% 7% -11% -10% -6% -23% -19% e Source: Infoadex. 2015e: Consensus of analysts 8

9 Television industry: Ad market Spanish TV Ad market: Last 8 quarters in positive Gross TV Ad market Yoy growth FY14=+11% 22% 9M15=+8% 13% 12% 1% 6% 3% 8% 8% 3% -8% -10% -3% -14% -15% -15% -16% -18% FY11=-10% -21% FY13=-6% -24% FY12=-19% Q111 Q211 Q311 Q411 Q112 Q2 12 Q312 Q412 Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115 Q215 Q315 Source: Infoadex. 9

14% 14% 11% 10% 11% 10% 5% 6% 19% Weight Source: Internal")

10 Spanish TV industry: Ad market 9M 15: All the sectors in positive Ad spending by sectors % 9M 15 yoy 17% 6% 14% 11% 6% 8% 9% 10% 9M 15=+8% 1% Beauty, Hygiene & Cleaning Food Autos Telcos Retail Finance Culture Health Others (Beverages Energy Home Sports & leisure ) 14% 14% 11% 10% 11% 10% 5% 6% 19% Weight Source: Internal Estimates 10

11 Television industry: Prices and volumes Prices and volumes at very low levels TV Ad market In million + Market Prices & Volumes in index terms 3,469 2, ,703 1,890 2, TV ad market Nominal Prices Volumes e Source: TV Market: Infoadex. 2015e: Consensus of analysts Prices: Internal estimates. Conventional advertising. Volumes: Internal estimates. Commercial hours: 13h-25h. Conventional advertising excluding TVE. 11

12 Spanish TV industry: Audiences TV viewing remains at very high levels Average daily viewing In min Age groups >65 45 to 64 Ind 4+ (+7 days) Ind to 44 4 to to 24 Source: Kantar Media 12

13 Spanish TV industry Atresmedia has a key position in a wide FTA TV offer Commercial FTA TV landscape (2015) Channels Mkt share* Audience Power ratio 42.5% 26.8% 1.58x 43.4% 31.0% 1.40x Net TV 3.4% Veo TV 4.0% 2.1% 0.5x 13TV 2.0% Secuoya Real Madrid TV Kiss TV Source: Kantar Media, Infoadex * At 9M15 To be launched in Q

14 Spanish TV industry : Pay TV Pay TV position in Spain Pay TV sector in Spain 2015 Penetration % households with pay TV connection Pay TV 25% Audience % Total Individuals 4+ Pay TV 7% Ad market share % Total TV ad market Pay TV 4% Source: Kantar Media, Infoadex 14

15 Spanish TV industry : Pay TV Pay TV by platform type and player Pay TV sector % Total connections (5.4 mill) DTT 4% Others 4% Satellite 26% VOD 15% Others Gol T 10% 4% IPTV 44% Cable 22% TEF 71% Source: CMT (Data available for Q215) 15

16 Atresmedia: A leading communication group Solid and clear group structure OTHERS Market share 42% Market share 20% ADVERTISING Total Ad market share 19% 16

ATRESERIES (launched in 2016) Planeta-De Agostini: RTL: Shareh. La Sexta Treasury stock: Free-float: 41.7% 18.7% 4.1% 0.4% 35.")

17 Atresmedia: Market positioning TV & Radio as main source of revenues Atresmedia Cine Atresmedia Digital Atresmedia Diversification Others Onda Cero Europa FM Onda Melodía Radio 9% 2% 2014 Net Revenues 883m 89% TV ANTENA 3 LA SEXTA NEOX NOVA MEGA (launched in 2015) ATRESERIES (launched in 2016) Planeta-De Agostini: RTL: Shareh. La Sexta Treasury stock: Free-float: 41.7% 18.7% 4.1% 0.4% 35.2% Source: Infoadex & internal estimates 17

18 Atresmedia: Strategy Clear strategic approach Consolidating TV leading position Regaining #2 position Monetizing digital developments Consolidating business model 18

19 Atresmedia Television: Strategy Unique TV offer 19

20 Atresmedia Television: Positioning Balanced and varied TV offer Age 4-12 Male Female 20

Source: Kantar Media.")

21 Atresmedia Television: TV audiences by core channel Antena 3: Stable audience ratings Total Individuals 24h Commercial Target 24h Source: Kantar Media. Total Individuals (4y+) Source: Kantar Media. Commercial Target (16-54 y) 21

Source: Kantar Media.")

22 Atresmedia Television: TV audiences by second channel La Sexta: The best growth story Total Individuals 24h Commercial Target 24h Source: Kantar Media. Total Individuals (4y+) Source: Kantar Media. Commercial Target (16-54 y) 22

23 Atresmedia Television: TV group audiences Atresmedia TV: Solid ratings despite losing 3 channels as of May 2014 Total Individuals 24h Commercial Target 24h Source: Kantar Media. Total Individuals (4y+) Source: Kantar Media. Commercial Target (16-54 y) 23

24 Atresmedia Television: TV group audiences Atresmedia TV: closing the gap with MSE quarter after quarter Total Individuals 24h Commercial Target 24h Source: Kantar Media. Total Individuals (4y+) Source: Kantar Media. Commercial Target (16-54 y) 24

25 Atresmedia: 2015 guidance in costs Cost increases mostly explained by one offs & programming costs Cost increases by concept Updated guidance Original guidance +1.5% +2.0% One-offs Sports overlap +0.5% +2.0% +1.0% Mega Prog Variable costs % OPEX 2015 one-offs Variable costs & programming 2015 OPEX 25

26 Atresmedia Radio: Positioning & Strategy Atresmedia Radio: 20% market share #3 radio player in Spain 4.5 million listeners 20% market share # 2 talk radio 2.3 mill listeners # 3 music radio 2.1 mill listeners New music radio 230k listeners Source: EGM 2015 yearly average Market Share: Infoadex & internal estimates 26

27 Atresmedia Radio: Audiences Atresmedia Radio: 4.5 million listeners Thousand of listeners 4,123 4,738 4,812 4,981 4,552 2,492 1,548 2,623 2,598 2,649 2,009 2,045 2,077 2,368 1, rd 11 3rd 12 3rd 13 3rd 14 3rd 15 Source: EGM Surveys Monday to Friday (.000) ( Moving average). 27

28 Atresmedia Digital: Positioning & Strategy Exploring any possible source of audience & revenues 28

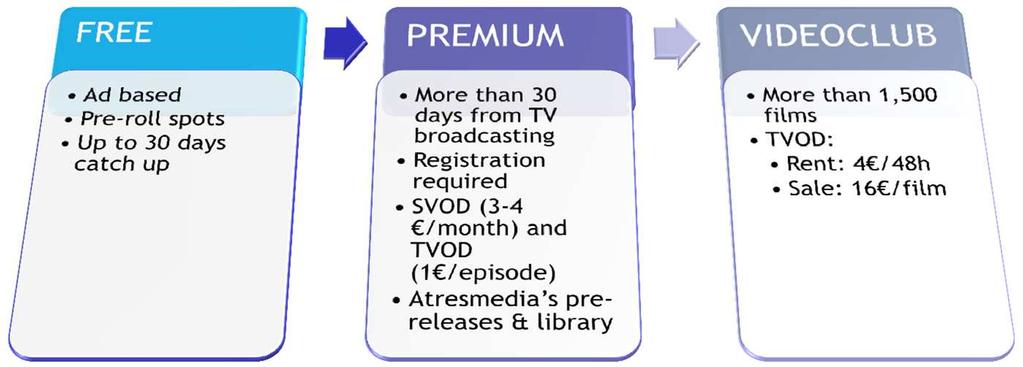

29 Atresmedia Digital: Atresplayer Atresplayer: Atresmedia s OTT offer 29

30 Atresmedia Diversification: Positioning & Strategy Developing new non ad-based media initiatives 30

")

5 mill subscribers 20% 33% 4 mill 100 %")

31 Atresmedia Diversification: International International: More than 31 mill subscribers ytd (Antena 3 s premium content channel) 16.5 mill subscribers (Celebrity & Life-style channel) 9.5 mill subscribers (Atresmedia s best-series channel) 5 mill subscribers 20% 33% 4 mill 100 % 47% 2 mill 35% 15% 50% 25 mill 31

32 Atresmedia Diversification: Media for Equity MEDIA FOR EQUITY: Exploring new business models Automotion Classified & Social Fashion & Accesories Travel Media For Equity Health Sports Leisure Education Technology Others 32

& EBITDA Margin 2013 1,703 2014 1,890 All")

33 Medium term goals: TV & Radio Television and Radio s EBITDA margin on track Market Gross Ad revenues ( mill) & EBITDA Margin , ,890 All time average 2, All time average % 25% 15% 21% 22% 7% EBITDA Margin EBITDA Margin Source: Kantar Media & Atresmedia s financial results 33

34 Medium term goals: Other revenues Other non-ad based revenues to double Other revenues than TV & Radio advertising as % of Total Revenues x2 45% 10% 55% 67% 5% 33% 2017e: 100 mill 2014: 50 mill Diversification Others (Films & Digital) 34

Dividend policy 185 150 mill")

35 Medium term goals: Financials Debt at target level and dividend policy according to plan Total Net Debt Target ( mill) Dividend policy mill Payout ratio 80% 136 Long term target 100 mill 2014 dividend: 0.20 / sh 100% payout ratio 35

36 Back up Back up: 9M 15 Financial Results 36

37 Atresmedia 9M 15 Results in mill: P&L 9M 15 9M 14 YoY Net Revenues % OPEX % EBITDA % EBITDA Margin 17.1% 13.5% EBIT % EBIT Margin 14.8% 11.5% Net profit Net profit Margin 9.9% 7.5% +47.1% Source: Atresmedia s financial statements 37

38 Atresmedia Television 9M 15 Results in mill: P&L 9M 15 9M 14 YoY Total Net Rev % OPEX % EBITDA EBITDA Margin 16.2% 12.6% +43.2% EBIT EBIT Margin 14.5% 10.8% +49.8% Source: Atresmedia`s financial statements 38

39 Atresmedia Radio 9M 15 Results in mill: P&L 9M 15 9M 14 YoY Net Revenues % OPEX % EBITDA EBITDA Margin 22.2% 15.2% EBIT EBIT Margin 20.1% 12.8% +59.5% +70.2% Source: Atresmedia s financial statements 39

40 Atresmedia: Others Division Financials Net revenues split mill 9M 15 9M 14 Net Revenues EBITDA Events 18% Films 32% Others * 50% Source: Atresmedia s financial statements Contribution to consolidated group *Others ( Internet, Editorial ) 40

41 Additional information Investor Relations Department Phone: Web: Legal Notice The information contained in this presentation has not been independently verified and is, in any case, subject to negotiation, changes and modifications. None of the Company, its shareholders or any of their respective affiliates shall be liable for the accuracy or completeness of the information or statements included in this presentation, and in no event may its content be construed as any type of explicit or implicit representation or warranty made by the Company, its shareholders or any other such person. Likewise, none of the Company, its shareholders or any of their respective affiliates shall be liable in any respect whatsoever (whether in negligence or otherwise) for any loss or damage that may arise from the use of this presentation or of any content therein or otherwise arising in connection with the information contained in this presentation. You may not copy or distribute this presentation to any person. The Company does not undertake to publish any possible modifications or revisions of the information, data or statements contained herein should there be any change in the strategy or intentions of the Company, or occurrence of unforeseeable facts or events that affect the Company s strategy or intentions. This presentation may contain forward-looking statements with respect to the business, investments, financial condition, results of operations, dividends, strategy, plans and objectives of the Company. By their nature, forward-looking statements involve risk and uncertainty because they reflect the Company s current expectations and assumptions as to future events and circumstances that may not prove accurate. A number of factors, including political, economic and regulatory developments in Spain and the European Union, could cause actual results and developments to differ materially from those expressed or implied in any forward-looking statements contained herein. The information contained in this presentation does not constitute an offer or invitation to purchase or subscribe for any ordinary shares, and neither it nor any part of it shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. 41