PLP GUNA EXECUTIVE SUMMARY

|

|

|

- Holly Marshall

- 5 years ago

- Views:

Transcription

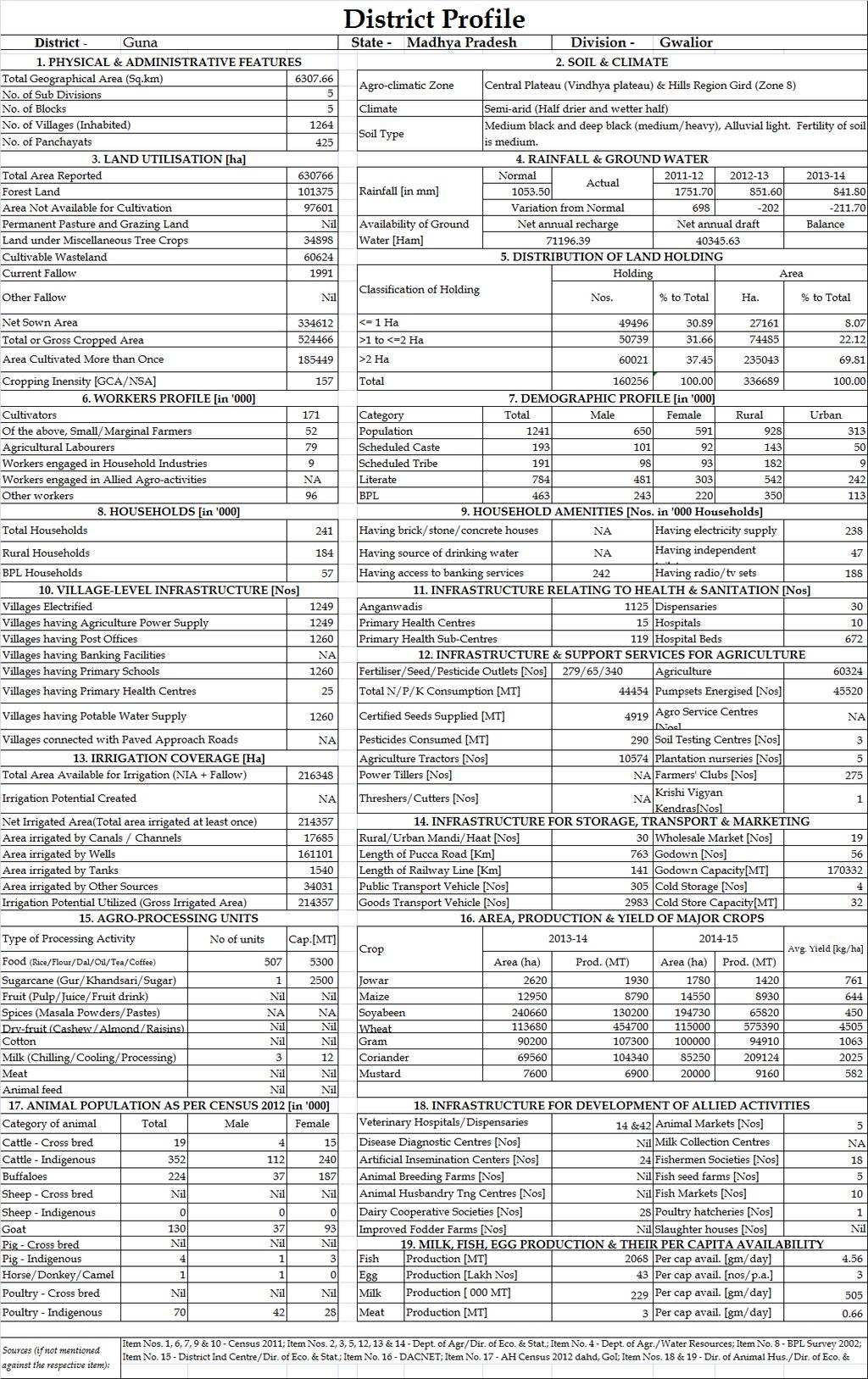

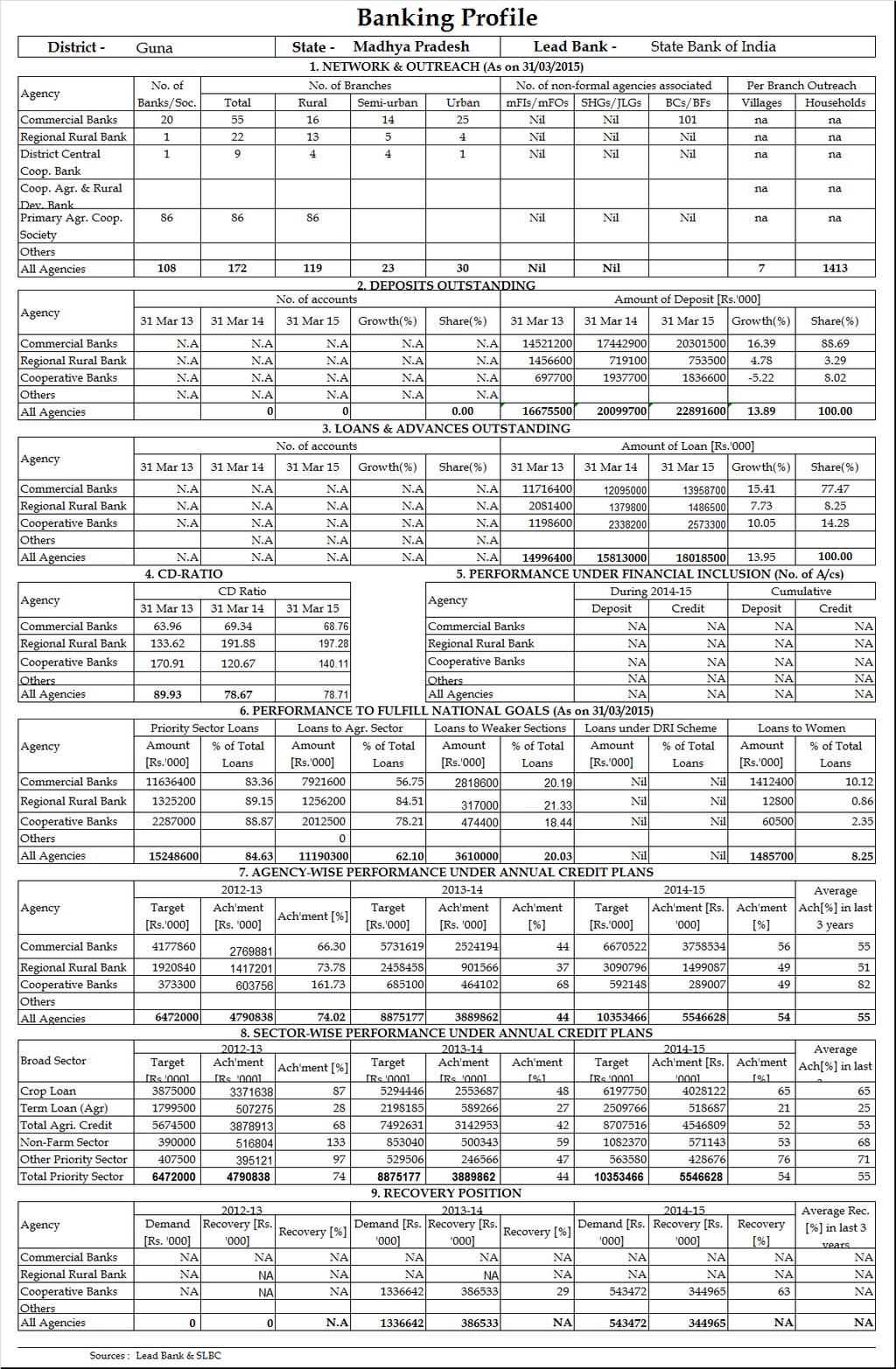

1 EXECUTIVE SUMMARY a) Theme of the PLP is Accelerating the pace of Capital Formation in agriculture and allied sector. b) Guna district is situated in the North West part of Madhya Pradesh. It has 05 blocks with a total geographical area of 6308 sq. km. constituting 2.05% of the total area of the State. The average rainfall of the district is mm per annum which precipitates in about 70 days. The district population (2011 Census) is lakh with 9.28 lakh in rural areas. The no. of households below poverty line is %. The Gross Domestic Product (GDP) of the district during was 2.5% of the state GDP. The total irrigated area as a percentage to net sown area is 64.06%. As on , there were 6390 micro and small enterprises providing employment to people are operational in the District. c) Ground Level Credit Flow (GLC): Total GLC of the district under priority sector which was crore during , decreased to crore during but increase to crore during The agricultural loans issued during the last three years were, , crore and crore respectively. The disbursements under NFS (incl. OPS) during the above period were crore, crore and crore respectively. The share of agriculture in GLC which stood at 80.96% in has decreased to 80.79% during & increased to 80.97% in The GLC flow was 53.57% of the targets set under District Credit Plan during the year Sector wise achievement for the same period was under Agriculture, MSME & Other Priority Sector. d) Highlights of banking benchmarks: The district has 55 branches of Commercial Banks, 22 branches of Gramin Bank, 09 branches of DCCB, and 86 PACS. The performance of banks in achieving the parameters stipulated by RBI was satisfactory under Priority Sector Advances such as CD ratio of 78.71%, PSA advances of 84.63%, Agricultural Advances of 62.10%, as against the stipulation of 60%, 40% and 18% respectively. Achievement under ACP at crore formed 53.57% of the target. e) Sectoral assessment of potential: (i) The potential, under Priority Sector, for each sector / sub sector for that could be tapped with institutional credit has been assessed and presented in Annexure I. The potential has been assessed at crore as against crore for the year showing 14.12% growth over previous year. The potential for crop loan has been assessed at crore as against crore for the year showing % growth over previous year. The potential under various sectors include Agriculture crore, MSME crore, Education 6.07 crore, Housing crore, Social Infrastructure 4.78 crore, Renewal Energy 1.0 crore and Others 7.85 crore. The shares of Agriculture, MSME, Export credit, Education, Housing, Renewal Energy, Others and Social Infrastructure are be %, %,0.20%, 0.41%, 2.29 %,0.07 %, 0.53 % and 0.31 % respectively. The potential has been assessed keeping in view the GoI/GoMP s priorities, existing/likely improvements in infrastructure, past GLC, revision in SoF/Unit Cost and various subsidy schemes of GoI/GoMP. f) Some of the major constraints envisaged in achieving the potential assessed are inadequate infrastructure, non availability of agriculture inputs in time and reluctance of bankers to extend agriculture term loans etc. Implementation of Vision 2018 document of GoMP would go a long way in realizing the potentials assessed. 1

2 I. Thrust areas and Developmental Initiatives of NABARD a) In order to realise the theme envisaged in the document, viz., Accelerating the pace of Capital Formation in Agriculture and Allied sector, a few Area Based Schemes have been identified. The sectors identified are Dairy and Micro warehousing. Tentative banking plans have been prepared for these activities. An estimated amount of lakh is expected to be financed by banks under these models. The models indicated are only pilots and it is expected that more such schemes will be prepared by banks. b) NABARD had also identified a few thrust areas for viz., JLG/SHG financing, micro warehousing, improving dairy development, Producer Organizations, etc. To promote the above areas, NABARD has also initiated several developmental activities in the form of support to Self Help/JLG Promoting Institutions, conduct of workshops, seminars, training camps, support to farmers clubs, FPOs. To promote the above areas, NABARD has also initiated several developmental activities in the form of support to Self Help/JLG Promoting Institutions, Farmers Producers Organisations through its Producer Organisation Development Fund and PRODUCE Fund established though the GOI Union Budget III. Infrastructure a) The district fares fairly well under some of the infrastructure indicators such as Electricity, Irrigation, watersupply and Education where the ranking of the district is better than the State average. However, certain other like indicators communication and health are lower than the State average. Incidence of poverty is higher than State average. Infrastructure facilities act as catalysts for development. Under RIDF, 81 projects with a cumulative loan component of crore was sanctioned by NABARD for the district covering mainly Irrigation, Road, Bridges & Health projects. b) In order to improve the credit off-take in the district, the State Govt may consider improving the various critical infrastructure identified in the district viz., setting up of soil-testing laboratories in each block, strengthening the existing extension network, technology transfer, improving irrigation, popularisation of improved agricultural implements and machinery through demonstrations in farmers' fields, popularizing high density cropping systems, improving animal health care, activating/increasing the milk routes, establishment of poultry/fish hatcheries, establishment of fish markets, improving road network, uninterrupted power supply to the industries, etc. c) There are certain critical infrastructure requirements which can be supported through private investment in the district viz., setting up of warehouses, micro warehouses, cold storages/cold chains, etc. Banks have to play an active role in financing such investments. IV Conclusion: In order to achieve the overall credit potential assessed and in particular to enhance the capital formation in Agriculture in the district, there is a need to have a coordinated approach by all the stakeholders, viz., banks, Govt. Departments and NGOs. The reporting system by banks through LBRs, regular monitoring of achievements vis-à-vis the targets in DLCC/BLBC meetings assume greater importance. The implementation of SHG, JLG, RuPay enabled KCC and Financial Inclusion drive will ultimately result in achieving the various objectives of inclusive growth in the rural areas of the district 2

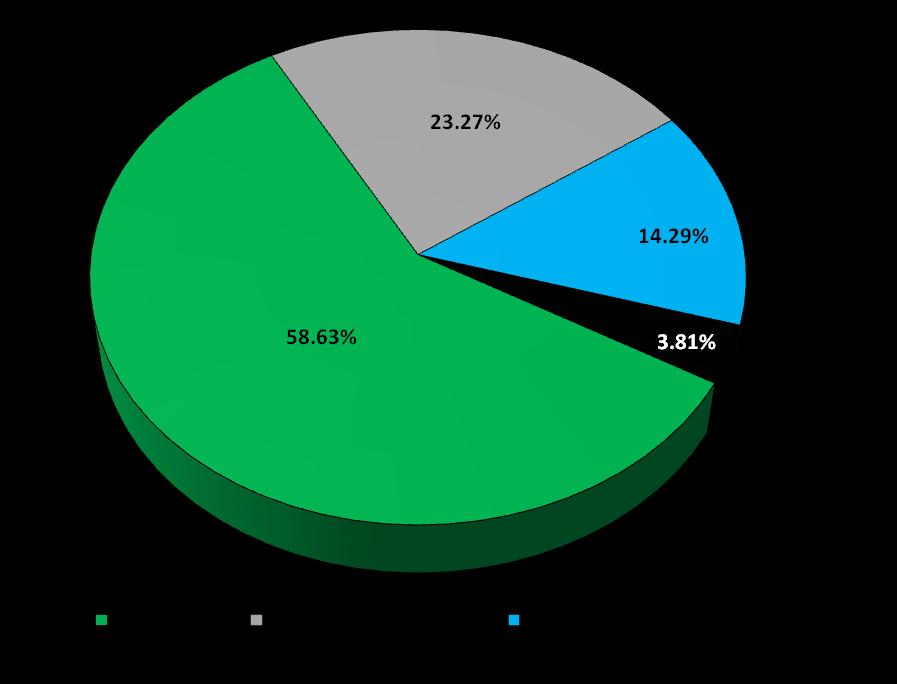

3 Appendix A to Annexure 1 Broad Sector wise PLP projections Sr No Particulars PLP projections A Farm Credit i Crop production, maintenance and marketing ii Term loan for agriculture and allied activities Sub total B Agriculture Infrastructure C Ancillary Activities I Credit potential for agriculture II Micro small and medium enterprise III Export credit IV Education V Housing VI Renewable Energy VII Others(SHG/JLG) VIII Social Infrastructure involving bank credit Total priority sector ( I to VIII)

4 Appendix B to Annexure 1 Summary of Sector/Sub Sector wise PLP projections ( lakh) Sr No Particulars PLP projections I Credit potential for agriculture A Farm credit i Crop production, maintenance and marketing ii Water resources iii Farm mechanization iv Plantation and horticulture v Forestry and Wasteland Development vi Animal Husbandry-Dairy vii Animal Husbandry-Poultry viii Animal Husbandry-Sheep, goat, piggery ix Fisheries x Others-Bullock, Bullock cart Sub Total B Agriculture Infrastructure i Construction of storage facilities (warehouse, cold storage) ii Land Development, soil conservation, watershed development iii Others( Tissue culture, Seed production, bio pesticide/fertilizer, vermin compost) Sub total C Ancilliary activites i Food and agro processing ii Others ( Loans to agriclinincs/agri business center) Sub total Total agriculture II Micro, small and medium enterprise i MSME-Working capital ii MSME-Investment credit Total MSME III Export credit IV Education V Housing VI Renewable Energy VII Others ( Loans to SHG/JLG, PMJDY) VIII Social Infrastructure involving bank credit Total Priority Sector

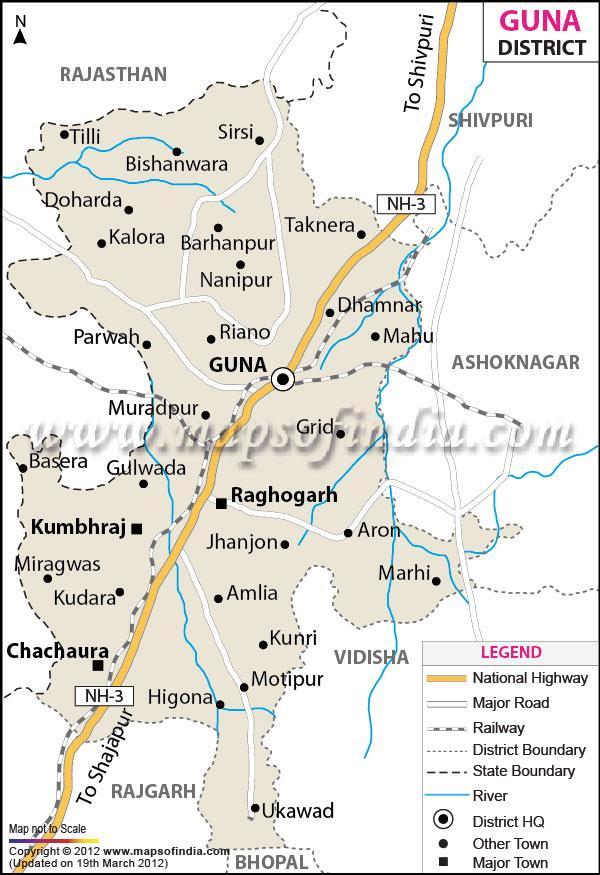

5 BROAD SECTOR-WISE PLP PROJECTIONS DISTRICT MAP OF 5

6 6

7 8