AF AgInflation Index and Farm Inputs Outlook. Clarke Willis Chief Executive, Anglia Farmers Limited

|

|

|

- Alison Gibbs

- 5 years ago

- Views:

Transcription

1

2

3 AF AgInflation Index and Farm Inputs Outlook Clarke Willis Chief Executive, Anglia Farmers Limited

4 Agenda AF AgInflation Index Latest Results Grain Prices v Cost of Production Single Farm Payment and Euro Volatility Farm Inputs Outlook

5 AF AgInflation Index AF launched their AgInflation Index in 2006 and it is compiled by Jim Alston. It is intended to reflect the changing expenditure of farming and is a weighted average of 9 cost centres and 132 cost items. Weightings within cost centre and between them are based on real farm expenditure. This time last year 6 months to February 2011 was 8.4% 12 months to September 2011 was 13%

6 AF AgInflation within each category for the 6 months to February 2012 Inflation within group Weighted contribution to overall inflation Seed Fertiliser Agrochemicals Animal feed & meds Contract & hire Machinery inc depreciation Fuel Labour Rent, interest, property Index Oct06=100

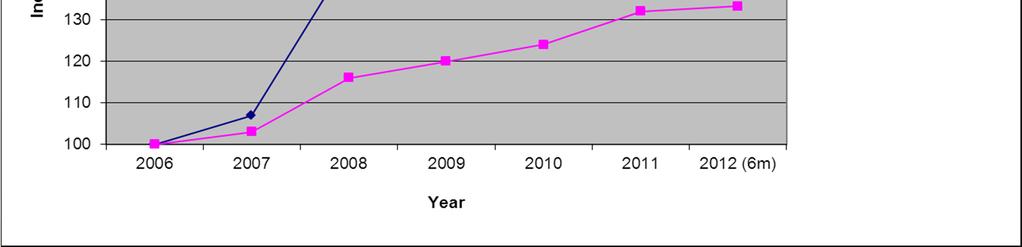

7 AF AgInflation v Retail Price Index AgInflation for period Index Oct06 =100 RPI Oct06=100 RPI inflation Overall 1.53% % All food Cereals & OSR 1.88% % Bread & magarine Potatoes 1.12% % Potatoes Sugar Beet 1.22% % Gran sugar Dairy 2.15% % Milk Beef & Lamb % Mince & lamb

8 AF AgInflation Index v RPI Total Food

9 A Closer Look at Grain Price v Cost of Growing

10 Single Farm Payments and Euro Volatility The continued uncertainty caused by the Eurozone crisis has direct implications for farmers and the value of their single farm payment. Over the last 12 months the EUR/GBP exchange rate has fluctuated by more than 10%, with a peak of 0.91 and a low of 0.82 (currently 0.84). This volatility is set to continue with analysts predicting a make-orbreak year for the single currency project. The Eurozone economy appears to be heading for a recession, adding more uncertainty to how the Euro will perform in coming months.

11 Single Farm Payments and Euro Volatility As the Euro continues to weaken against GBP, the value of your single farm payment is reduced. EUR/GBP Daily 0.91 Exch an g e R ate Feb-11 May-11 Aug-11 Date Nov-11 Feb-12

12 How You Could be Affected Illustration: You receive a single farm payment of 100,000. If the currency exchange was made at the top of the market, at a rate of 0.91 you would receive 91,000. If the currency exchange was made at the bottom of the market, at a rate of 0.83 you would receive 83,000. That equates to a difference of 8,000 in the amount received, due to fluctuating exchange rates over the past 12 months. You can protect yourself against this risk by electing to receive your payment in EUR instead of GBP and fixing your exchange rate in advance.

13 How to Protect Yourself Set up a forward contract where you can lock in a favourable exchange rate now to protect yourself against any further fluctuations between now and when the subsidy is paid. Plan your budget for the next year, knowing what you will receive, eliminating uncertainty and risk. Six month window to make the currency exchange: protects you in the event of any delay in payment

14 Inputs Market Review Fertiliser Agrochemicals Energy

15 Fertiliser Outlook

16 Urea Outlook month ahead: prices to remain stable-to-firm 3-6 months: new supply from Algeria and elsewhere will provide competition for existing producers 12 months: peak Indian demand Q3/Q4, but doubts over global demand growing to absorb new supply, limiting price escalation during second half of 2012?

17

18 Phosphate Prices fallen the result of strong fundamentals (supply v demand) by 60-70: prices started to tail-off at year end 2011 and are expected to remain soft for the next 18 to 24 months reduced supply will help slow the price slide, but unless it continues throughout the year, the market will still be long

19 Potash Demand for potash in developing economies has increased: Prices and demand will increase further as farmers improve the productivity of arable land Supply & demand is finely balanced allowing the market to push through material price increases Canadian producers have increased contract prices from $470/t (late 2011) to $530/t (start 2012) Price rises forecast to $575/t (2014)

20 Agrochemical Outlook

21 AgChem headlines High level of autumn cropping especially after beet/potatoes Mild autumn forward crops with significant levels of disease UK varieties bred for yield requirement for robust disease control Drive for yield new SDHI chemistry offers improved disease control/yield if used at correct rates crop prices make growing for yield attractive Potentially a very high demand year

22 UK the cheapest market in Europe? FARM BRIEF 26 Jan 2012

23 UK AgChem cheapest? So what? Increased potential for exports from UK distribution can disrupt other EU markets volatile exchange rates increase the risk manufacturers manage this risk with availability to the possible detriment of UK farmers Lower manufacturer profitability from the UK high demand years; increased production diverted to more profitable markets (e.g. Crystal 2011) low margin products withdrawn from UK (e.g. chlormequat 2012)

24 AgChem drivers High demand (total area and rate of use)? variety mix disease susceptibility crop output prices encourage spend forward crops carrying disease through a mild winter Finite product availability inventory control a key driver for manufacturers enabling price rises at farm gate to be realised? Availability of preferred products? Consolidation of AgChem supply chain (Agrii)

25 AgChem outlook General drive for inflationary rises c.5-7%? not all will stick depending on competition and demand Some key product price adjustments Bravo (chlorothalonil) - 10%+ - generic registrations Amistar (azoxystrobin) -? - generic registrations chlormequat - 20% - European pricing Mocap - 25% - global demand/pricing Goltix (metamitron) - 40% - global demand/pricing New fungicide chemistry

26 Energy Outlook Fuel & Electricity An uncertain future!

27 Energy Outlook Liquid Fuel Supplier consolidation in gas oil market AF dedicated vehicles Direct delivery from Thames Weekly / monthly prices using PLATTS Telematics

28