PLP SHAHDOL EXECUTIVE SUMMARY

|

|

|

- Amy Morrison

- 5 years ago

- Views:

Transcription

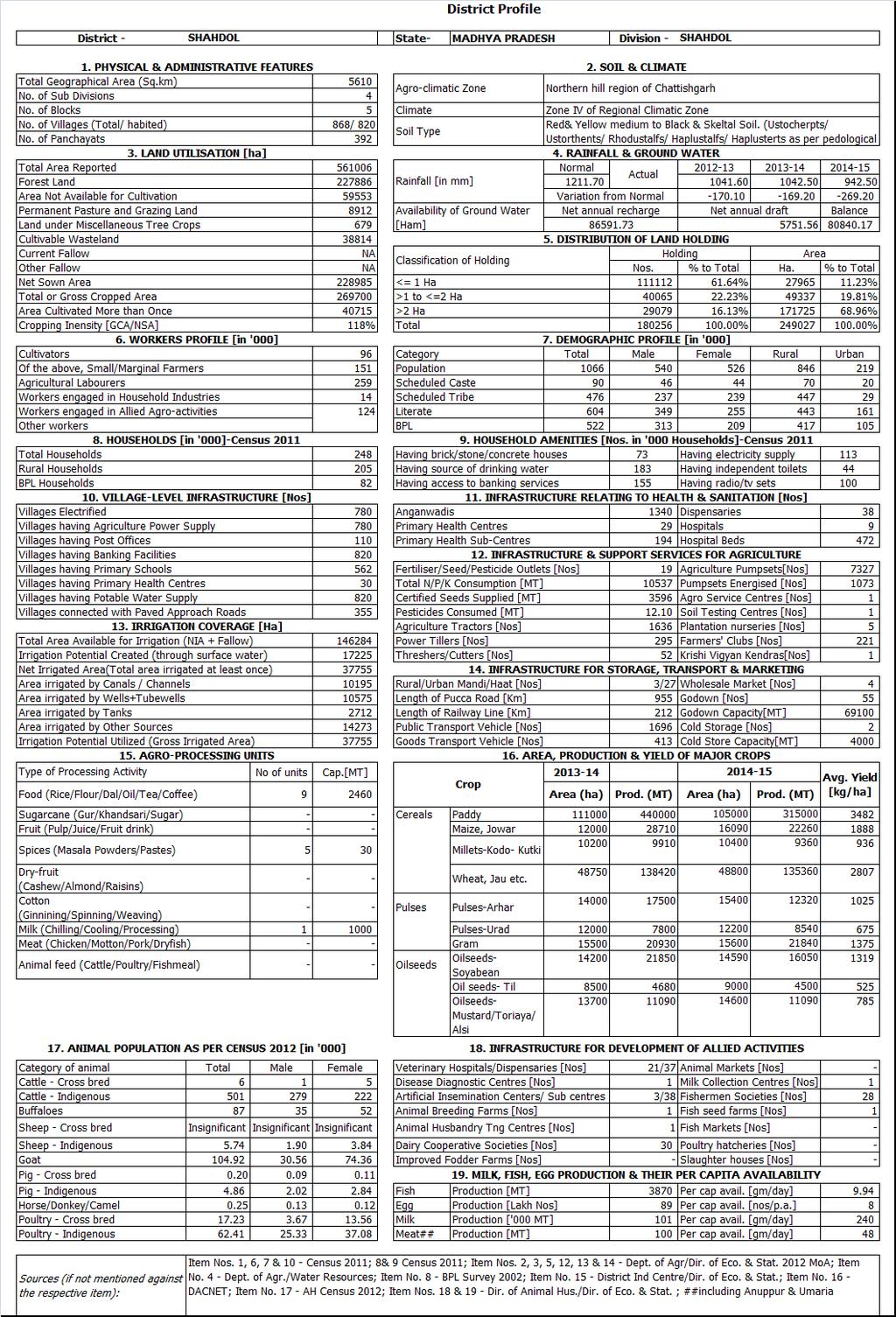

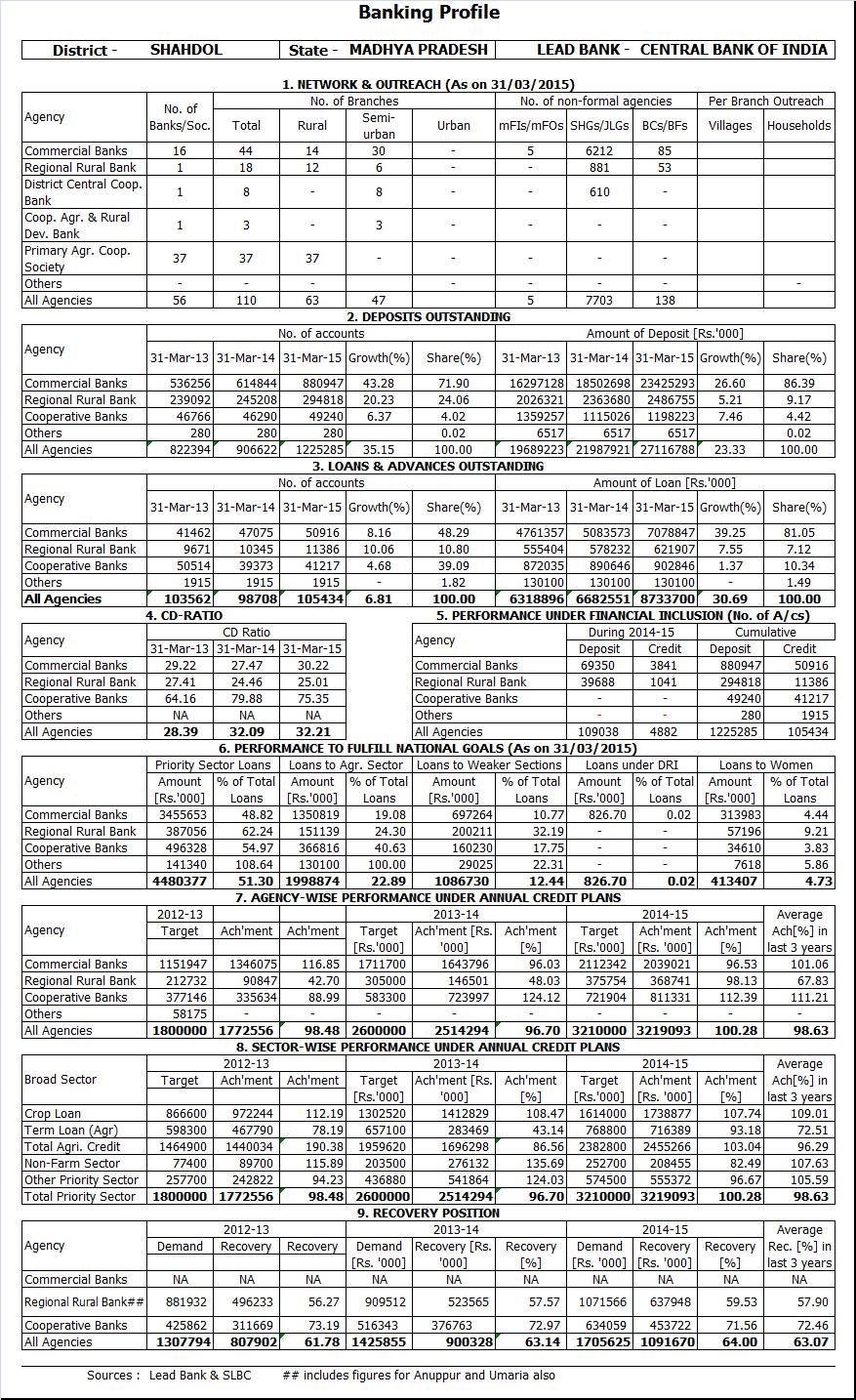

1 I) General EXECUTIVE SUMMARY a) The Theme of the PLP is Accelerating the pace of Capital Formation in agriculture and allied sector. b) Shahdol district is situated in the eastern part of Madhya Pradesh. It has five blocks with a total geographical area of 5610 sq. km. constituting 1.82% of the total area of the State. The average rainfall of the district is mm per annum which precipitates in about 60 to 80 days. The district population (2011 Census) is lakh with 8.46 lakh in rural areas. The population below poverty line is 49.06%. The Gross Domestic Product (GDP) of the district during was i.e. 2.40% of the state GDP. The total irrigated area as a percentage to net sown area is 14.33%. As on , there were 7916 Micro Industries/ Small industries and 02 Mega Industries providing employment to persons in the district. The district is classified as tribal district and is also among Left Wing Extremist (LWE) district. c) Ground Level Credit Flow (GLC): Total GLC of the district under priority sector which was crore during , increased to crore during and further to crore during The agricultural loans issued during the last three years were crore, crore and crore respectively. The disbursements under NFS (including OPS) during the above period were crore, and crore respectively. The share of agriculture in GLC which stood at 67.46% in has increased to 76.27% during The Agriculture Term Loan constituted 29.18% of the total agriculture lending during This share has decreased by 3.31% since d) Highlights of banking benchmarks: The district has 73 bank branches with 44 branches of Commercial Banks, 18 branches of Gramin Bank, 08 branches of DCCB, 03 branches of DARDB and 37 PACS. The performance of banks in achieving the parameters stipulated by RBI during was satisfactory, except CD ratio parameter. The CD ratio of 32.21%, PSA advances of 51.30%, Agricultural Advances of 22.89% were achieved as against the stipulation of 65%, 40% and 18% respectively. Submission of LBRs by banks needs to be improved. Achievement under ACP at crore formed % of the target. The performance under Financial Inclusion was also satisfactory, as the targets regarding coverage of villages through USB, appointment of BCs, number of transactions of BCs, accounts under PMJDY etc., were achieved. During the year 04 new banks viz.- IDBI, UCO Bank, Bank of India, Bank of Maharashtra have entered in to the district. e) Sectoral assessment of potential: (i) The potential, under Priority Sector, in each sector / sub sector for that could be tapped with institutional credit has been assessed at crore as against for the year showing 31% growth over previous year. The potential under various sectors include crop loans crore, investment credit for agriculture comprising various sectors viz., Water Resources, Land Development, Farm Mechanisation, Forestry, Dairy Development, Poultry, Sheep/goat/piggery, Fisheries, Storage Godowns & Market Yards and Other activities at crore, MSME crore. In tune with revision in priority sector guidelines by RBI, credit potential for Education 9.18 crore, Housing crore, Renewal Energy 0.96 crore, loans to SHG etc crore and Social Infrastructure crore have been assessed in addition to traditional sector. This has lead an increase of crore over previous year. f) Agriculture credit projection ( crore) which includes Farm credit, Agriculture infrastructure and Ancillary activities forms 67.95% of the total credit projection. The share of crop loan and agriculture term loan in Agriculture credit is 70.90% and 29.10% 1

2 and 48.18% and 19.77% in total credit projection. MSME & remaining sector i.e.- Education, Housing, Renewal Energy, loans to SHG etc. and Social Infrastructure in credit potentials for is 16.26% and 15.79% respectively. The potential has been assessed keeping in view the GoI/GoMP s priorities, revised Priority sector guideline, existing/likely improvements in infrastructure, past GLC, revision in SoF/Unit Cost and various subsidy schemes of GoI/GoMP. g) Some of the major constraints envisaged in achieving the potential assessed are inadequate extension support, inadequate irrigation facility, lack of assured and quality power supply in rural areas, lack of post harvest facilities for horticulture crops, absence of milk routes in a major portion of the district, average roads and communication network, etc., in rural areas. Forward and backward linkages such as quality planting material, post harvest facilities, organised marketing facilities for Plantation, Horticulture and floriculture crops could trigger exploitation of latent potential for Plantation & Horticulture sector in the district. II. Thrust areas and Developmental Initiatives of NABARD a) In order to realise the theme envisaged in the document, viz., Accelerating the pace of Capital Formation in Agriculture and Allied sector, a few pilot Area Based Schemes have been identified. The sectors identified are Forestry- Eucalyptus plantation and Animal Husbandry- Dairy Development. Tentative banking plans have been prepared for these activities. An estimated amount of lakh is expected to be financed by banks under these models.. b) NABARD had also identified a few thrust areas for viz., JLG/SHG financing, improving dairy development, Producer Organizations, etc. To promote the above areas, NABARD has also initiated several developmental activities in the form of support to Self Help/JLG Promoting Institutions, conduct of workshops, seminars, training camps, support to farmers clubs, FPOs, Natural Resource Management through Watershed, loan based training for NFS development, etc. III.Infrastructure a) Infrastructure Indicators comparison indicates that the district is fairly developed in comparison to state average in Electricity, Water supply, Education, healthcare, and transportation and lags behind in other components viz. Irrigation, communication, urbanisation etc. Infrastructure facilities act as catalysts in the development. Under RIDF, 37 projects with an outlay of crore and loan component of crore was sanctioned by NABARD for the district covering mainly rural roads and bridges, minor irrigation projects, primary health centres, ITI projects, etc. b) In order to improve the credit off-take in the district, the State Govt may consider improving the various critical infrastructure identified in the district viz., setting up of soil-testing laboratories in each block, Building infrastructure for Medical / Engineering college, lining of canals, Solar /Electrification Nal-Jal Yojana in non electrified villages strengthening the existing extension network, technology transfer, improving irrigation, popularisation of improved agricultural implements and machinery through demonstrations in farmers' fields, popularizing high density cropping systems, improving animal health care, activating/increasing the milk routes, establishment of poultry/fish hatcheries, establishment of fish markets, improving road network, uninterrupted power supply to the industries, etc. 2

3 IV.Conclusion: In order to achieve the overall credit potential assessed and in particular to enhance the capital formation in Agriculture in the district, there is a need to have a coordinated approach by all the stakeholders, viz., banks, Govt. Departments and NGOs. The LBRs/SAMIS submission, regular monitoring of achievements vis-à-vis the targets in DLCC/BLBC meetings assume greater importance. The implementation of SHG, JLG, RuPay enabled KCC and Financial Inclusion drive for bank linkage, insurance cover and pension scheme will ultimately result in achieving the various objectives of inclusive growth in the rural areas of the district. 3

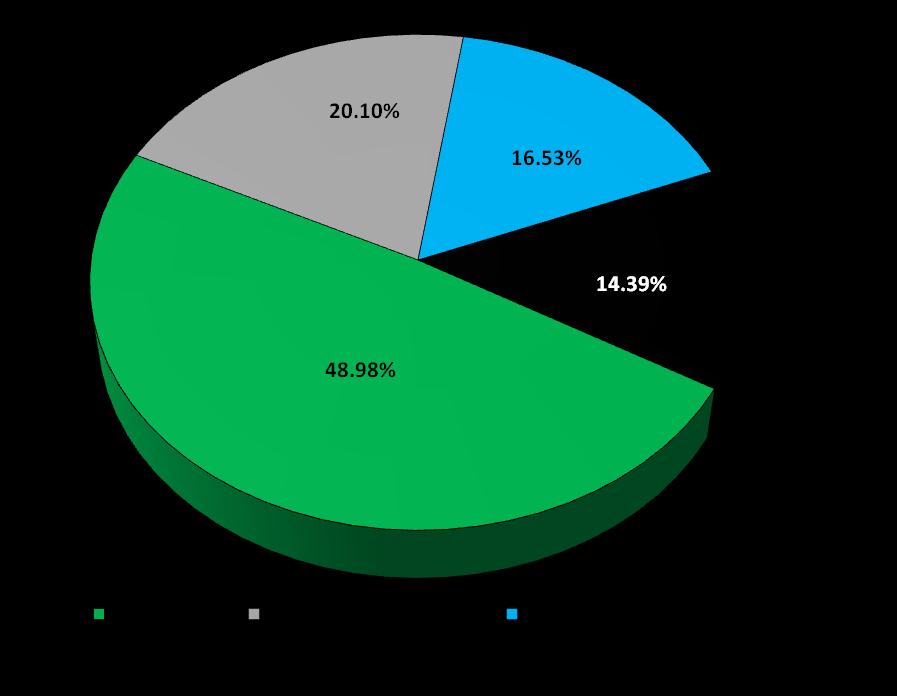

4 Sr. No. A i Appendix A to Annexure 1 Broad Sector wise PLP projections ( Lakh) PLP projections for Particulars Farm Credit Crop Production, Maintenance and Marketing ii Term investment for Agriculture and Allied Activities Subtotal B Agriculture Infrastructure C Ancillary Activities I Total Credit Potential for Agriculture (A+B+C) II Micro Small and Medium Enterprises III Export Credit 0.00 IV Education V Housing VI Renewable Energy VII Others VIII Social Infrastructure Involving bank credit Total priority Sector (I to VIII)

5 Appendix B to Annexure 1 Summary of Sector/Sub Sector wise PLP projections ( Lakh) Sr. PLP projections Sector No I Credit Potential for Agriculture A. Farm Credit i Crop Production, Maintenance and Marketing ii Water Resources iii Farm Mechanisation iv Plantation and Horticulture v Forestry and Waste Land Development vi Animal Husbandry Dairy Development vii Animal Husbandry Poultry Development viii Animal Husbandry Sheep, Goat and Piggery Development ix Fisheries Development x Other Activities Sub Total B. Agriculture Infrastructure i Construction of Storage Facilities ii Land Development, Soil conservation, watershed Development iii Others Sub Total C. Ancillary Activities i Food & Agro processing ii Others Sub Total Total Agriculture (A+B+C) II. Micro, Small and Medium Enterprises MSME - Manufacturing i MSME Investment credit ii MSME working capital Sub Total MSME - service i MSME Investment credit ii MSME working capital Sub Total Total MSME III Export Credit 0.00 IV Education V Housing VI Renewable Energy VII Others (loans to SHG/JLG, PMJDY etc.) VIII Social Infrastructure Involving bank credit Total priority Sector (I to VIII)

6 BROAD SECTOR-WISE PLP PROJECTIONS DISTRICT MAP OF 6

7 7

8 9