Outlook Presentation Updated

|

|

|

- Frederick Fowler

- 5 years ago

- Views:

Transcription

1 Outlook Presentation Updated Darrell Holaday Advanced Market Concepts/Country Futures Wamego KS

2 How Did This Happen?

3

4

5

6

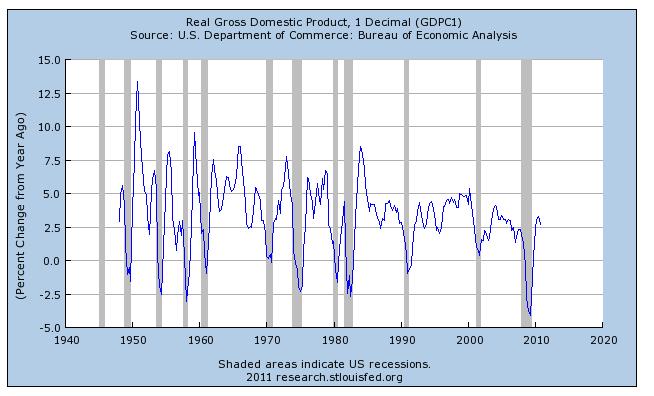

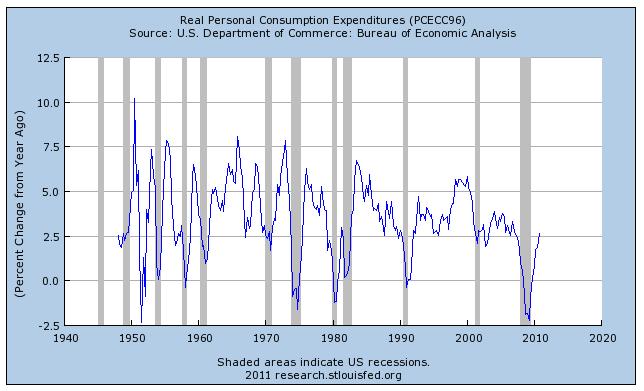

7 Is the Recession Over?? GDP improved

8 Is the Recession Over?? GDP improved Consumer Expenditures Increased

9

10

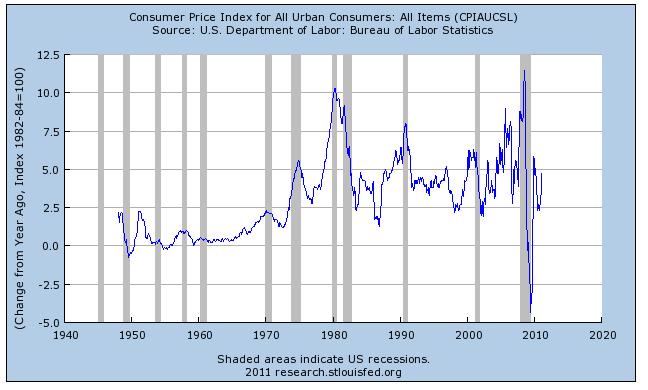

11 Is the Recession Over?? GDP improved Consumer Expenditures Increased Inflation under control?? Food and Energy

12

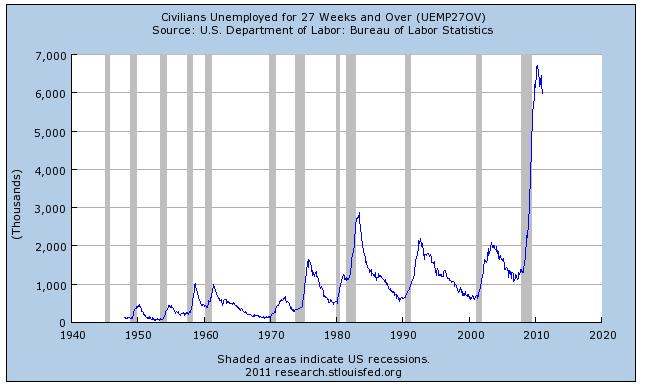

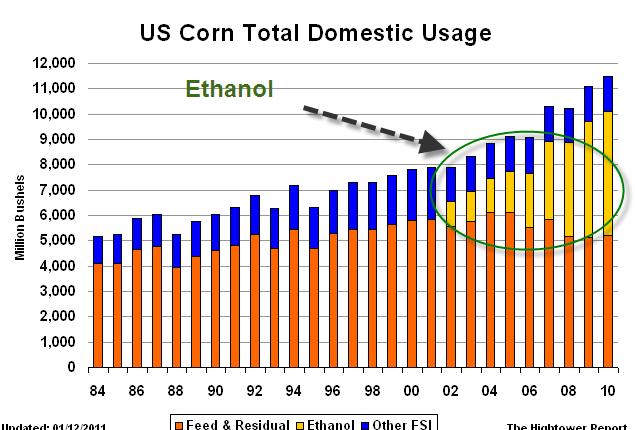

13 Is the Recession Over?? GDP improved Consumer Expenditures Increased Inflation under control?? Food and Energy What about Employment? How do you explain 9%?

14

15 Is the Recession Over?? Debt issues still haunting this economy Public and Private Explosion in Asian Economies

16 Why are Food Commodities so much higher? Corn Yield in 2010 was the flame The drought in Russia was the spark Asian economies growing at 6-10% annual rates. US Exports benefiting from other problems. US and World Consumers are going to see a much larger piece of their income pie going to food and energy. Ultimately this is negative for GDP growth.

17 This was the flame that changed everything!

18

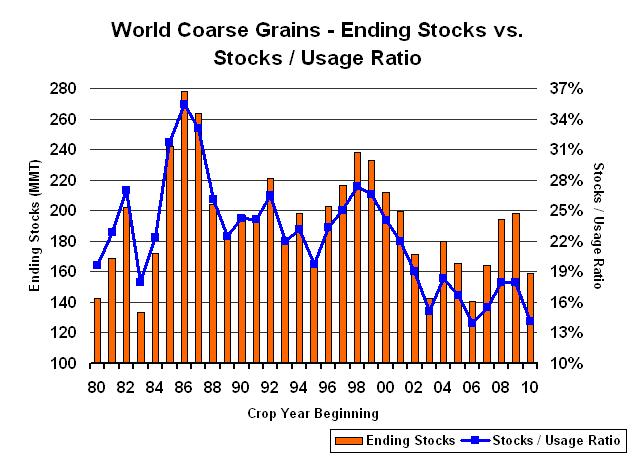

19 40 Percentage Change in US Exports Wheat Soybeans Corn Beef Pork

20 Corn/ Feed Grains Corn is still the backbone of the strength Yields disappointing Down 5%-7 from Trend and Expectations Still a lot of questions as to why Energy drives corn Has been true since US Govt Initiative in Ethanol Tax Credits Important but the Mandate is much more IMPORTANT. How would mandate work without Tax Credits. What is the impact of Ethanol on the price of corn?

21 2000 US Corn Use 2010 US Corn Use Ethanol 7% FSI 13% FSI 9% Feed 40% Exports 20% Feed 60% Ethanol 35% Exports 16%

22

23

24 Corn Used For Ethanol (US) (Bushels) Sep Oct Nov Dec Jan Feb Mar Apr May June July Aug

25

26 Corn / Feed Grains Price has not seemed to trim use of corn domestically (or internationally). Somebody has to stop. The markets job is to make someone lose money using corn. It cannot live with ending stock to use ratio at 5%. Who will stop first?? Did the Japanese Earthquake Trim Use?? Tremendous pressure to increase acres to 93 million with at 160 bushel yield. Acreage fight will be more interesting than any year in the past.

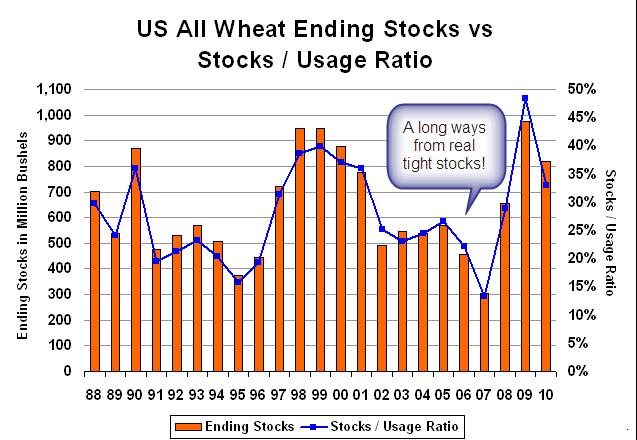

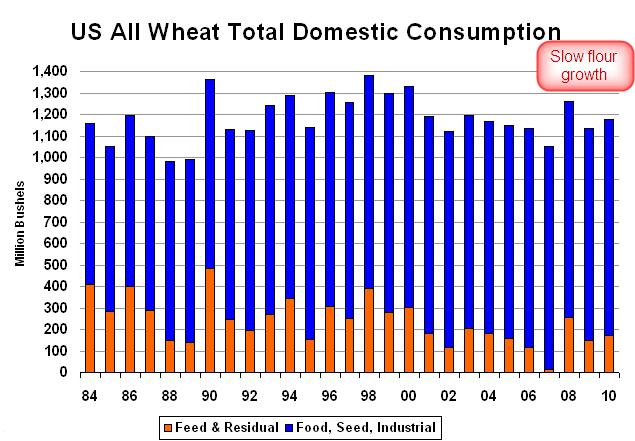

27

28 How is this at a tight stock situation?

29

30

31

32

33 What I Like Tied To Energy and Overall demand for energy is still growing. We have not rationed supplies. Stocks for the current crop year have to increase. The fight for acreage will be fierce. Corn Inventory in strong hands. There will be much more concern about prospective yields after last year. Corn What I dislike A lot of feed wheat in the world. Japan s purchases will be reduced in the short run. Tax credits may be on their last leg. How do we exist with no tax credits and a mandatory blending level? Cattle and ethanol use may both decline at the same time.

34 Wheat Fundamentally this market is generally the weakest of the sector. The Russian drought changed the world psychology Started a small avalanche of production problems The problems in Russia and Australia have pushed business to the US. Also had Canadian and EU Problems this year USSOUTHERN PLAINS GETTING ATTENTION!!

35 MMT World Wheat Production

36 MMt World Wheat Ending Stocks /94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11

37

38

39

40

41 130 China Wheat Production and Imports China Prod Chin Imports

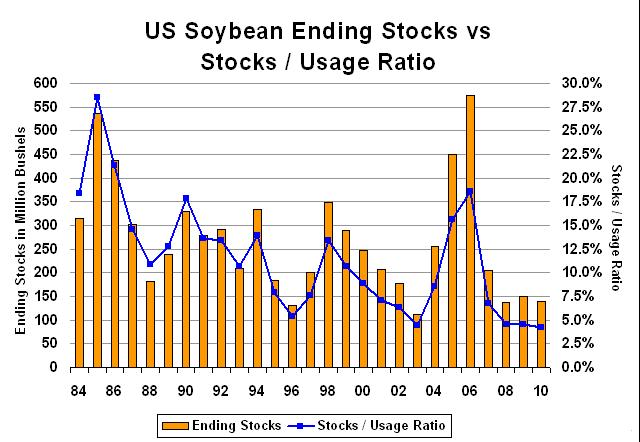

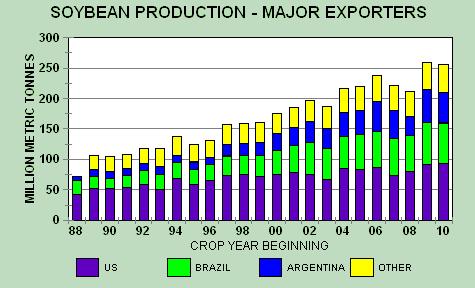

42

43

44

45

46

47

48 What I Like Bullish Psychology Weather problems in the world. US and China, Russia. Will be another fight for acreage that may trim some wheat acres from the high expectations. Wheat is a competitive feed in many parts of the world. CORN Wheat What I dislike US and World Stocks still in reasonable shape if yields come through without big acreage increase. Still a lot of wheat in the US. Australia will fill the boat with wheat acres. Could be a false price signal and will attract too many acres Basis and the possible contract changes

49 Soybeans Overall long term growth in demand remains strong. Still a growing protein market and China consumption reflects this fact. We are beginning to see the growth in yield capability. Started in 2009 New Genetics will promote additional yield gains. South American production will slow US exports, but Argentine crop stunted. China carries the big stick in this market.

50 Soybeans Overall long term growth in demand remains strong. Still a growing protein market and China consumption reflects this fact. We are beginning to see the growth in yield capability. Started in 2009 New Genetics will promote additional yield gains. South American production will slow US exports, but Argentine crop stunted. China carries the big stick in this market.

51

52 28.0% % of World Use of Soybeans by China 26.0% 24.0% 22.0% 20.0% 18.0% 16.0% 14.0% 12.0% 10.0% 2002/ / / / / / / / /11

53

54

55 280 World Soybean Use (mmt) / / / / / / / / /11

56 80 World Oilseed Ending Stocks (mmt) / / / / / / / / /11

57 400 Total World Oilseed Use / / / / / / / / /11

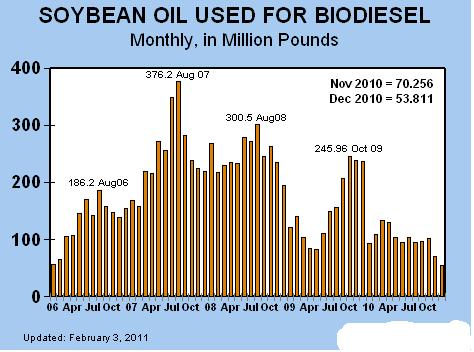

58

59

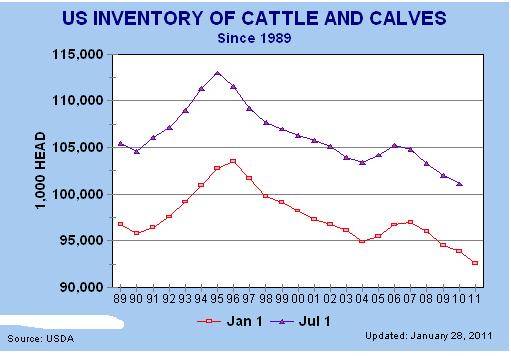

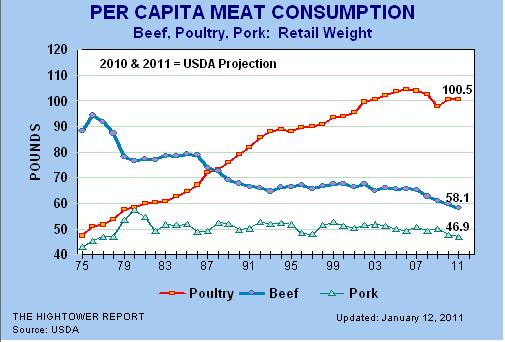

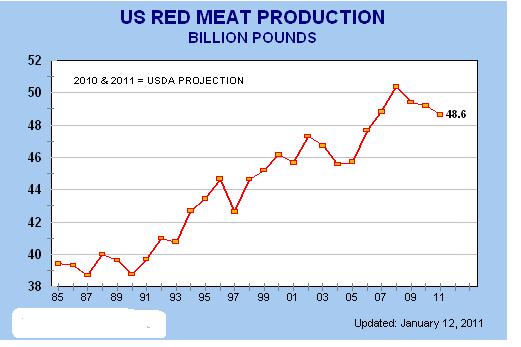

60

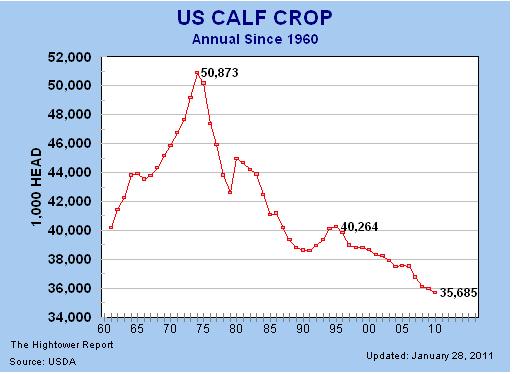

61

62

63

64

65 What I Like Market cannot deal with ending stock number near 100 million bus in the US Chinese Consumption Argentina crop has questions and a long way to go. Macro Psychology of inflation still dominates Soyoil Demand still strong despite biodiesel. The industry cannot let acres slip like they did the last time US corn acres jumped up over 93 million (2007) Soybeans What I dislike CHINA, but no sign of trouble yet. If inflation play disappears, soybean values will retreat. There is no pullback in South American production. Price will eventually destroy some market.

66 Crop Insurance and Marketing RMA offers very Puts and Calls Don t Exclude the Harvest Option Consider selling Puts? Consider selling Calls? Crop Insurance allows for more aggressive forward pricing.

67 Meats Inventories Have declined significantly in US and Much of the World Beef Demand Exploding in Asia (Until Earthquake). Poultry Increasing supplies gradually Can t Build Beef Consumption if Supplies Shrinking But World supplies of protein Very Tight Good Demand in Asia extremely positive Beef and Pork Exports the big story

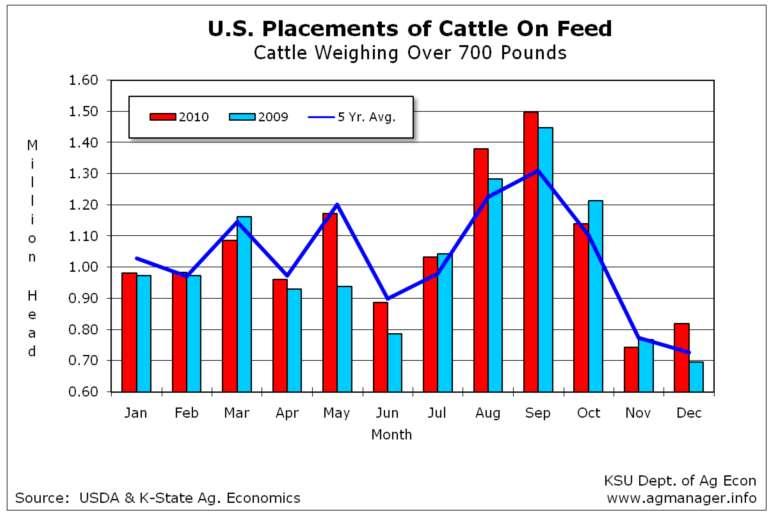

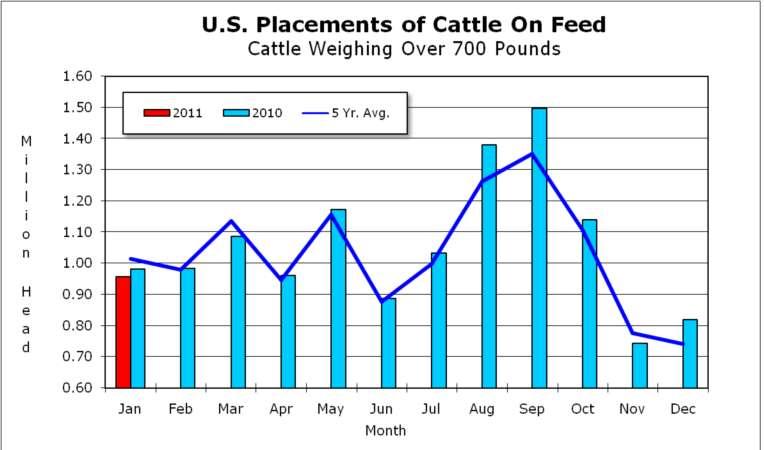

68 Cattle Corn Price and Overall Economy (Unemployment driving near term psychology Cattle have been marketed very orderly and that has been critical. Calf supplies continuing to shrink and COF numbers declining should eventually decline Numbers do not indicate any herd building The lack of grass is the number one impediment to herd rebuilding Corn is the next problem THE LACK OF GRASS IS THE LIMITING FACTOR FOR COW HERD EXPANSION!!

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85 Meats Cont d Poultry product still grow 2-3% this year. Will gain US market share in the US versus pork and beef Cattle and Hog futures have built in steep premium to cash anticipating substantial drop in supplies.