PAKISTAN MARKET MONITORING BULLETIN

|

|

|

- Rosalyn Morris

- 5 years ago

- Views:

Transcription

indicates that 3.")

1 T H E U N I T E D N A T I O N S W O R L D F O O D P R O G R A M M E PAKISTAN MARKET MONITORING BULLETIN J A N U A R Y - A P R I L Highlights Approximately 5.6 million people in the flood affected areas are food insecure Flood Recovery Assessment (FRA) indicates that 3.6 million people are in need of recovery food assistance International wheat flour prices in 2011 are well above prices in 2009 and 2010 but remained below highs seen in 2008 Domestic cereal output in 2010/2011 declined by 4.7 million tonnes due to floodrelated crop loss Domestic cereal supply should satisfy national requirements through April 2012 INSIDE THIS ISSUE: HOUSEHOLD FOOD SECURITY AND OUTLOOK (Page 1) INTERNATIONAL WHEAT AND RICE MARKET SITUA- TIONS (Page 2) FLOODS IMPACT ON DOMES- TIC PRODUCTION AND AVAILABILITY (Page 2) DOMESTIC STAPLE FOOD PRICES (Page 3) WAGE RATES AND CON- SUMER PURCHASE POWER (Page 5) Vulnerability Analysis and Mapping Unit, World Food Programme, Islamabad, Pakistan. Ph: Lower wheat opening stocks in May 2011 and reduced wheat production may lead to import requirements in 2011/2012 marketing year Wholesale wheat prices remain high compared to previous years but have stabilized between November 2010 and April 2011 In April 2011 the average retail wheat flour price remains at Sept 2010 highs Wheat flour prices in February 2011 in KPK markets remained 14 to 22%higher than pre flood averages Consumer purchasing power has deteriorated further since the floods HOUSEHOLD FOOD SECURITY AND OUTLOOK Approximately 5.6 million people in the flood affected areas are food insecure As of end of January, relief assistance ended in most parts of the country, outside of certain pockets in Sindh. At the peak of the emergency WFP was feeding over 7 million floodaffected people. The Flood Recovery Assessment (FRA) indicates that 5.6 million people in the flood affected areas are food insecure, with 3 million newly food insecure as a result of the floods. The prevalence of food insecurity is highest in the flood affected areas of Balochistan and Sindh (~50%) but the largest number of food insecure is in Sindh (2.4 million) and Punjab (1.8 million) Deterioration in food security status is a result of asset loss and shifting livelihoods (from farming to wage labour activities) resulting in lost purchasing power and more difficulty in accessing food. Among the people affected by the floods, the most vulnerable to food insecurity appear to be farmers, many of which are now unable to cultivate but instead rely on daily wage labour activities to provide food for their households. Overall, at least 80% of the newly food insecure were farmers before the floods. FRA indicates that 3.6 million people are in need of recovery food assistance Medium to longer-term food assistance will be required in flood affected areas to help those who were not able to fully recover their livelihoods after the floods. FRA estimates that 3.6 million people are in need of recovery food assistance for the foreseeable future.

2 PAGE 2 INTERNATIONAL WHEAT AND RICE MARKETS International wheat prices in 2011 are well above prices in 2009 and 2010 but still below highs seen in 2008 In addition, about 1.5 million tonnes of private and public wheat stocks are estimated to have been damaged or lost by the flood waters 2 FAO Rice Market Monitor January FAO Rice Market Monitor January Source : Government of Pakistan Domestic cereal supply should satisfy national requirements through April 2012 In the first four months of 2011, International wheat prices remained well above the prices observed in 2009 and 2010 but well below the price spikes in The average US wheat export price (US No 2 Hard Red winter) was 359 USD per tone in April, 25 percent below its peak in March 2008 but 79 percent higher than a year earlier. Concerns about a slowdown in imports because of political instability in a number of major wheat importing countries weighed on prices but worries over dry conditions in major winter wheat producing areas of United States and a rally in maize markets limited the price decline 1. 1Globle information and early warning system on food and agriculture (GIEWS country brief) FLOODS IMPACT ON DOMESTIC PRODUCTION AND AVAILABILITY Domestic cereal output in 2010/2011 declined by 4.7 million tonnes due to flood-related crop loss The 2010 monsoon floods damaged almost all the standing cereal crops of the Kharif season (rice, maize, sorghum and millet). Total cereal supply losses in 2010/11 (May/April) due to the floods are estimated at 4.7 million tonnes. Paddy production losses were officially estimated at about 2.4 million tonnes 2, which is almost one-third of national production. As a result, 2010 paddy production was forecasted at 6.3 million tonnes 3 compared to 10.1 million tonnes 4 in Total coarse grain (maize, sorghum and millet etc.) losses are estimated at 0.8 million tonnes. Wheat is the country's main staple food, accounting for 35 percent of the total dietary energy supply in Pakistan. From May 2010 to April 2012, the wheat supply is expected to satisfy national requirements (estimated at 25 million tones for this period) thanks to high beginning stocks (4.3 million tonnes in May 2010) and good pre-flood production (with 23.8 million tonnes harvested before the floods 5 ) and as expecting good rabi crop. Rice is a secondary cereal as far as consumption is concerned but is a substantial export earner. Pakistan typically exports between 40 and 60 percent of its domestic production and is the world's third largest rice exporter, with an estimated 2.9 and 3.5 million tonnes exported in 2009 and 2010 respectively. For the 2010/2011 marketing year, the combined impacts of flood-related crop loss and continued emphasis on rice exports (conservatively estimated to be 1.8 million tonnes) is likely to result in a decrease in domestic rice availability. Increased wheat consumption, however, can likely compensate for this shortfall. 5 Source : Government of Pakistan, Rice data in the chart is calculated by authors (WFP/VAM) based on FAOSAT data and forecast data Lower wheat opening stocks in May 2011 and reduced wheat production may lead to import requirements in 2011/2012 marketing year Because of the floods, winter season (Rabi) wheat production for the 2010/2011 marketing year could be reduced compared to 2009/2010 (a wheat planting survey is needed to provide a better estimate). The recovery of agriculture sector in the flood affected areas will take at least five years 7. 7 based on the preliminary analysis by UN MDG assessment team DOMESTIC STAPLE FOOD PRICES Wholesale wheat prices remain high compared to previous years but have stabilized between November 2010 and April 2011 Wheat import parity prices in Multan or Rahim Yar Khan have increased to 833 USD per tonne in April 2011, but

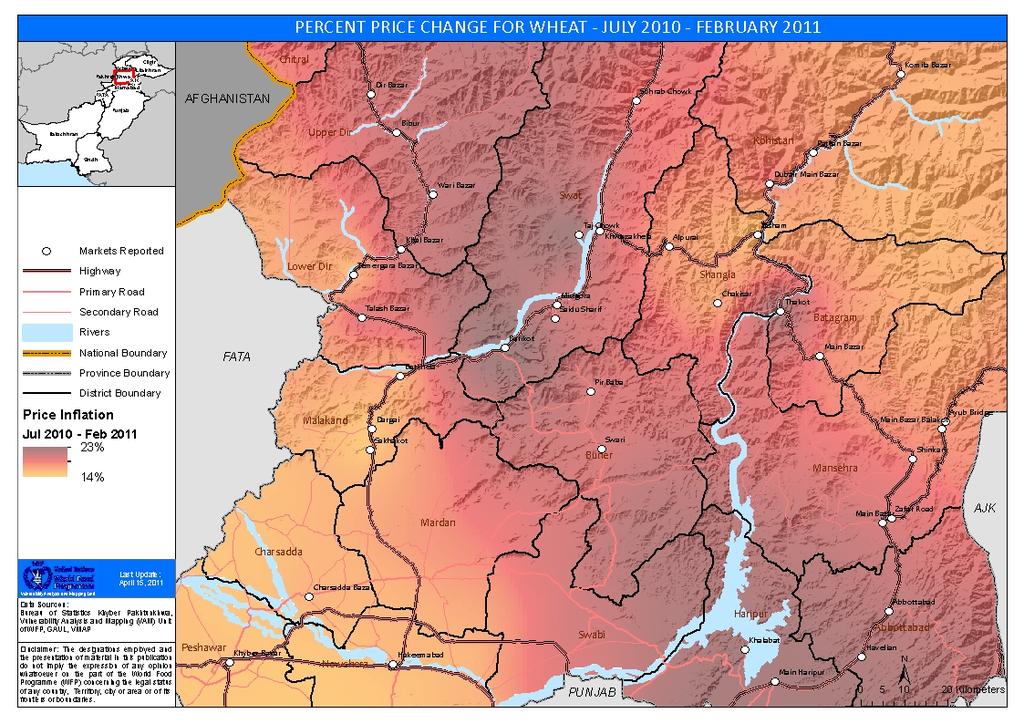

3 PAGE 3 wheat wholesale prices remained much lower at 327 USD per tonne. Wholesale wheat prices still remain very high compared to previous years, however, wheat prices have stabilized between November 2010 (Rs.25.2/KG) and April 2011 (Rs.26.4/KG). In April 2011 the average retail wheat flour price remains at Sept 2010 highs The average wheat flour retail price in the main Punjab markets has increased since 2006, reaching its highest level at Rs.30/kg in April Price has remained at current levels since September 2010 Overall, in 2011, average retail wheat flour prices in major non Punjab markets was only a few rupees higher than in main Punjab markets, suggesting relatively good integration between the main markets in Pakistan (this might however not to be the case with less accessible markets in Pakistan, especially in less accessible markets in wheat deficit areas). In April 2011, wheat retail prices ranged from 29 Rs/kg in Multan, Sialkot of Punjab Province to 32 Rs/kg in Sukkur. Wheat flour prices in February 2011 in KPK markets remained 14 to 22%higher than pre flood averages District level wheat flour prices in February 2011 are 14-22% higher than pre flood prices throughout the Swat Valley region of KP. Highest increases in prices are seen in Markets along the Swat River Prices have remained stable since November In non-punjab markets, especially during the 2008 foodprice crisis, the average wheat retail price was more responsive to international prices; between March and October 2008 prices remained more than doubled, peaking at 33 Rs/ kg in October Since then, prices have declined slightly but remained significantly higher than pre-food-price crisis levels. Retail wheat flour prices in the main non-punjab markets 10.3 percent increased between April 2010 (29 Rs/kg) and April 2011 (32 Rs/KG) Price increases in Punjab markets are comparable.

4 PAGE 4

.")

however, qualitative findings suggest the increase in wages may be having")

5 PAGE 5 WAGE RATES AND CONSUMER PURCHASE POWER Consumer purchasing power has deteriorated further since the floods Wages play an important role in the household economy in Pakistan, especially in urban areas where they account for almost half of the household income (compared to one quarter in rural areas). Wage rates increased sharply in the immediate aftermath of floods, but stabilized thereafter in most areas. FRA findings from November show continued modest improvements in daily wages for unskilled workers (between 5 and 20 percent) however, qualitative findings suggest the increase in wages may be having little effect as the number of days worked has declined. The ToT between daily wage rates and IRRI-6 rice prices have also deteriorated since In March 2011, daily wage labourers could purchase 7.6 KGs of IRRI-6 in Multan, 9 KGs in Karachi, 6.8 KGs in Peshawar, 11 KGs in Quetta and 8.8 KGs in Lahore. Short-lived increase in purchasing power during the floods Probably as a result of reduced labour supply during the floods, wage rates temporarily increased between June and November Given comparatively larger increases in food prices, however, this has still resulted in a reduction of purchasing power. Since 2006, and especially during the 2008 food price crisis, the amount of wheat flour or rice that could be purchased with one day of wages (Terms of Trade ToT- between daily wage labour and retail wheat flour and rice prices) has decreased significantly.