Transatlantic Trade and Investment Partnership (TTIP):

|

|

|

- Imogen Hall

- 6 years ago

- Views:

Transcription

, marketing (7,100),")

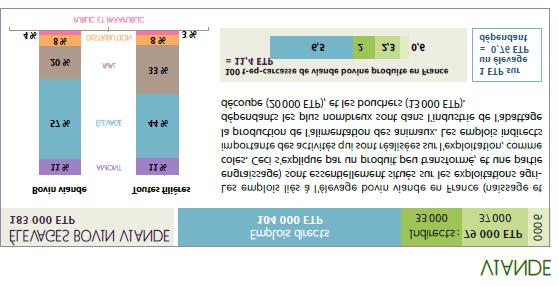

1 Ref. Ares(2016) /01/2016 Transatlantic Trade and Investment Partnership (TTIP): Almost 50,000 under threat in the French bovine meat sector Introduction: Employment in the French bovine meat sector, the leading beef producer in Europe In 2015, the French bovine meat sector provided 259,800, shared between various sectors, including livestock farming (138,000), marketing (7,100), processing (29,700) and distribution (85,000). As well as fulfilling their main objective - feeding the population - these workers also make a significant contribution to the development and dynamism of rural areas, generate economic activities (tourism, etc.) and are key stakeholders in France s cultural influence. French Elevage Eleveurs Effectifs ETP Mise en marché animaux Commerçants en bestiaux Coopératives d'éleveurs Transformation (entreprises privées et coopératives) Abatteurs English Livestock farming Livestock farmers Workers Full-time Marketing of animals Livestock traders Cooperatives of livestock farmers Processing (private companies and cooperatives) Slaughterers

2 Transformateurs découpe et élaboration Commerçants en gros de viande (chevillards) Commercialisation viande Hypermarchés et supermarchés rayon tradition/libre-service Restaurateurs (collectivités ou privés) Boucheries et triperies traditionnelles (artisans) Consommation Consommateurs Processing, cutting and production Wholesale meat traders Sale of meat Hypermarkets and supermarkets (traditional/self-service sections) Restaurant owners (private or community caterers) Traditional butchers and tripe shops (artisans) Consumption Consumers In its study Jobs connected to French livestock farming, the Scientific Interest Group GIS Elevage Demain (Livestock farming tomorrow) offers an in-depth analysis of the which depend directly on livestock farming in France: these represent 183,000 full-time, involving 236,300 workers (see diagram on the following page).

3 183,000 full-time are dependent on French beef farming ( Jobs connected to French livestock farming study, scientific interest group GIS Elevage demain, 2015) 183,000 full-time depend on French beef farming Total number of full-time in these sectors: 339,000 Animal feed: 7,700 full-time Manufacturers of compound animal feed, supplements, byproducts, transport, etc. Sector total: 22,000 full-time Public and para-public services 7,300 full-time Administration, research, education Sector total: 21,900 fulltime Other goods and services: 13,500 full-time Equipment, buildings, animal health, genetics and performance, etc. Sector total: 59,700 full-time Collection, processing and wholesale: 34,600 full-time Slaughter, cutting, livestock traders, wholesale meat traders, producer organisations, storage, by-product management, industry suppliers, animal transport Sector total: 171,200 full-time [Central circle] Bovine meat farming: 104,000 full-time Sector total: 203,000 full-time Distribution: 15,900 full-time Artisan butchers and delicatessens, supermarket butchers, transport of end products Sector total: 64,300 full-time

4 I - Before TTIP : companies in jeopardy, struggling for competitiveness 1 - French beef producers in serious difficulty Economically, workers in the French bovine meat sector are on the brink: closures of suckler farms and slaughterhouses have increased over the last 5 years throughout the country. In 2013, the annual pre-tax profits of beef farmers hovered between 10,000 and 15,000 net and 26.5% of these farms had annual pre-tax profits of below 10, Profitability relies heavily on the sale of loin The consumption of beef is radically different between Europe and USA: although demand for minced beef is high in USA, the sale of prime cuts (such as loin steak) remains lukewarm. However, these cuts are particularly popular in Europe, especially in France, making them by far the most profitable products for French producers. Nevertheless, the European market for loin from suckling cattle is particularly narrow: according to the French Livestock Institute (L Institut de l Elevage), it is estimated to only represent 400,000 tonnes (Source: Eurostat). 3 - Current American exports to the EU directly target the loin market. This difference in habits regarding the consumption of beef on either side of the Atlantic has inevitably led to American producers exporting their loin to the European Union. As of today, imports of beef from USA - notably as part of the Hilton and the High quality beef» (HQB) quota 1 - are made up of 75% loin 2. The European market - and more specifically the French market - is all the more attractive to Americans since their production methods give them a major competitive advantage over French producers. The reasons for this competitiveness gulf between European and American loin are mainly structural: whilst European beef farms are, in the large majority of cases, family businesses with an average of 61 LU (Livestock Units) per farm, mainly grass-fed as part of long production cycles, in the USA 2/3 of American cows are fed using industrial methods in feedlots (see note attached Transatlantic Trade and Investment Partnership: Towards a new model of bovine meat production in Europe? ) 1 Issued from the 2009 Memorandum of Understanding (MoU) between the EU and the US. 2 Estimate from French Livestock Institute (L Institut de l Elevage Français)

5 II - After-TTIP according to estimates carried out by the sector: around 50,000 workers in the French bovine meat sector will be forced out of business due to competition from America. 1 - The American price, soon to become the benchmark on the European market? Although imports of American beef is currently limited and the price of this meat is relatively high due to its rarity, a large-scale opening of the European beef market through TTIP (and future free-trade agreements currently being negotiated with the EU s other American partners) could have a significant destabilising effect on prices in this market. Indeed, according to our estimates:! Given the duty free quota on beef already agreed with Canada (65,000 tonnes) and because USA produces 10 times more and exports 25 times more beef to the EU, a particularly high quota could be granted to them, in accordance with the opening of 300,000 tonnes to be potentially handed over to exporters from third countries as part of the 2008 WTO project.! Because the European market for loin from suckling cattle is estimated at 400,000 tonnes, it could be dictated by the American price if it is inundated with American imports. In the event of USA being granted a large duty free quota as part of TTIP, we have estimated this price at 8.60/kg cwe (carcass weight equivalent) 3 (wholesale price estimated as sold in Europe). By way of a comparison, the current standard price of 1 kg of loin produced and sold in Europe is 13.70/kg. 2 - A drop in earnings which French producers simply cannot absorb, with an impact on the entire supply chain leading to a large-scale destruction of 4. According to the same estimation, such downward pressure on prices in the European loin market would trigger a drop of 9.6% in the price of young bull paid to French producers, causing a 30% to 60% fall in operating profits of farms which specialise in bovine meat production. Given farms current earnings (over 25% of beef production farms have pre-tax operating profits below 10,000), between 25,000 and 30,000 directly associated full-time in this sector would be in grave danger (out of a total of 104,000 such full-time in France). According to the study Jobs connected to French livestock farming by GIS Elevage Demain (Livestock farming tomorrow) June 2015, since 0.76 indirect full-time (slaughter and cutting, butchery, etc.) depend on each of these full-time beef farming, a total of between 44,000 and 53,000 full-time in the French beef industry could be lost due to American competition. And this number could grow yet further, taking into account other resulting from livestock farming (i.e. generated by household spending in direct and indirect sectors) and/or created by a leverage effect within the sector, which this study does not examine. APPENDICES 3 Estimate based on wholesale price in 2013 in USA ( 4.40/kg cwe (carcass weight equivalent), source: USDA) to which was added the standard premium applied to hormone-free beef, transport costs to the EU and wholesaler s margin was chosen because it falls between (when the price of loin sold in the EU increased to 6.50) and when prices exploded in USA due to temporary shortages. 4 Estimated using a counterfactual analysis of the consequences of the TTIP and CETA in 2009 on profits of farms specialising in beef production over the last 5 years.

6 APPENDICES 1 - Estimate of the potential impact of TTIP and CETA on the French beef sector: Proposed methodology. Step 1 (Nov 2014): impact analysis of the opening of duty free quotas on the prices of French young bull, using case studies of French farms specialising in beef production (database: Réseaux d élevage (Livestock farming networks)). Working on the assumption that CETA + TTIP will lead to an opening of quotas totalling around 200,000 tonnes. Région Case study System of production Pays de la Grass-fed and concentra tes Pays de la Intensive Pays de la Semi intensiv e Poitou- Charentes Race Parthenaise Pays de la AOC Maine -Anjou Pays de la Collective farming group (GAEC) Auvergne Extensive Farming Limousine Number of LU Of which: suckling cattle Agricultural land (hectares) Labour Unit 1,2 1,2 1,2 2,0 1,2 2,2 1,8 1,5 Share of adult cattle in turnover 75% 73% 71% 71% 69% 69% 60% 69% (%) 2013 profits Turnover ( 1,000) before impact Operating profits ( 1,000) % operating profits/turnover 11% 13% 14% 15% 14% 17% 16% 24% TTIP+CETA impact on operating profits % -55% -50% -46% -46% -40% -37% -27% 2012 profits before impact Share of adult bovines in turnover (%) Operating profits ( 1,000) % operating profits/turnover TTIP+CETA impact on operating profits % 68% 68% 67% 65% 66% 67% Turnover ( 1,000) % 14% 14% 11% 13% 16% 22% Limousin -124% -58% -61% -77% -62% -52% -37% Semiintensive Limousine Source: Inosys Réseaux d élevage - Idele data, 2014 See details of this estimate in the annexed document titled Estimate of the impact of TTIP and CETA on the earnings of French beef farmers.

7 Step 2: Estimated losses of direct (beef meat breeders / farmers) caused by an unsubsidised drop in turnover from beef production: - Estimated drop in unsubsidised farm turnover (database = Comptes de l Agriculture de la Nation (National Agriculture Accounts)) - Estimate of lost as a result: % of fall in price of juvenile beef Change in the unsubsidized turnover of the beef production industry (year N) = Number of full-time destroyed by the agreement Average farm operating profits (year N-1)

8 2 Etude «Les emplois liés à l élevage français», GIS Elevage demain, Juin 2015 Notice méthodologique et résultat concernant la filière viande bovine.

9

10

11

12

13 3 Study: Estimate of the impact of TTIP and CETA on the earnings of French beef farmers, IDELE for INTERBEV, 2014 Estimate of the impact of TTIP and CETA on the earnings of French beef farmers This analysis consists of 2 stages: 1. Impact of TTIP and CETA on the prices of European young bull carcasses paid to the producer; 2. Impact of the drop in prices of European young bull carcasses on the earnings of French beef farmers. Part 1 Impact on the domestic price using 2013 data This model only takes into account North American exports of loin to Europe - North America is a net exporter of loin, while European imports consist largely of this type of cut: in North America, the management of the carcass balance ( équilibre carcasse ) is less focused on the quality cuts from the rear of the carcass since demand for minced meat is much higher. It is estimated that USA and Canada will fill their quotas with a minimum of 75% loin. - The price of American loin will set the benchmark price for loin on the European market, due to: o The size of quotas currently expected (over 100,000 tonnes 5 /year for USA alone, since a duty free quota of 67,500 tonnes/year is already granted to Canada). A duty free quota of 200,000 tonnes/year filled with 75% North American loin would equate to half of the European production of loin from suckling livestock, and a quota of 400,000 tonnes/year would correspond to the entirety of annual production in Europe (source: estimates from GEB-Institut de l Elevage according to data from BDNI-Normabev Eurostat, AMI) 6. According to American exporters, exports outside of the established quotas are not profitable. o The possible application of a first come, first served rule with regard to quotas, which could encourage competition between wholesale importers and a squeezing of their margins. According to data on 2013, the arrival of such volumes of American loin in Europe would lead to a reduction of almost 10% in the price of young bull paid to the producer: - European loin is sold at a wholesale price of 13.70/kg cwe (carcass weight equivalent) before the impact: o The average price of a young bull carcass in the wholesale market in Hamburg: 4.00/kg (carcass equivalent weight) (Source: AMI) o Loin represents 9% of the weight of the carcass but 31% of its price in Europe (Source: UECBV). - American loin would be sold at 8.60/kg cwe (carcass weight equivalent) in Europe: o Choice 7 loin is sold at an average wholesale price of USD 3.24/kg (carcass equivalent weight) (Source: USDA) 5 Tonnages are given as carcass equivalent weight 6 Currently, the price of imports does not set the benchmark price on the European market due to tariff and non-tariff protections limiting the imported volumes of fresh meat which could substitute European loin in various areas of the market: small Hilton quotas, GATT quotas on frozen products only, customs duties of 20% on Hilton and GATT quotas, High Quality Beef quota is too small to lead to a large-scale implementation of hormone-free supply chains, and prohibitive customs duties outside of quotas. 7 Meat from carcasses classified as Choice (premium quality) currently make up the majority of the volume exported to the EU.

14 CONFIDENTIAL o o o For the carcass of an animal reared without hormones, the loin will represent 75% of the value in the EU. 75% of the NHTC 8 premium paid to the livestock farmer (USD 200 per animal, source: US press and surveys) is attributable to the loin (9% of the carcass), equating to an extra cost of 3.07/kg (carcass equivalent weight) per loin. The TTIP quotas, like the CETA and the High Quality Beef quotas, would be duty free quotas. The cost of transatlantic transport and the wholesaler margin are estimated at respectively 5% (Source: OECD) and 10% (Source: INSEE, commercial margin of wholesale meat traders) of the price of the product, amounting to a surcharge of approximately 1.10/kg (carcass equivalent weight) per loin. - European loin would therefore be sold at 9.40/kg cwe (carcass weight equivalent) with TTIP and CETA quotas: o European loin would retain an added value of around 10% compared to loin imported from third countries (as is currently the case, source: AMI/pricing in Hamburg). - Only taking into account this drop in the price of loin, the average price of a young bull carcass on the wholesale market in Hamburg would therefore decrease from 4.00 to 3.60/kg, equivalent to a 9.6% fall. - Working on the assumption that this 9.6% decrease will be passed on to all of the links in the supply chain in the same way, the price of young bull paid to the producer would also fall by 9.6%. Part 2 Impact on the profits of farms in 2013 It is estimated that this decrease would be the same for prices in all categories of adult cattle and in all countries in Europe. The impact of the 9.6% fall in prices of adult cattle on beef meat farms has been estimated using case studies from the Livestock Farming Networks (Réseaux d élevage). We based our estimates exclusively on the breeders and fatteners systems, due to the lack of models for the price of lean meat. Moreover, we selected case studies representing systems specialised in beef production 9. According to data on 2013, with everything else remaining equal, a fall of 9.6% in the price of adult cattle would lead to a drop in farms operating profits (pre-tax operating profits, with Agricultural Social Insurance payments (MSA) deducted) of between 27% and 66%, depending on the type of farm. The discrepancy in the impact between different types of farm can be explained by: - The varying economic efficiency of different case studies, measured here by the relationship between the operating profit and the turnover - The varying share of the turnover which comes from meat products, and therefore the impact of the fall in the price of adult cattle is felt to a greater or lesser extent. Model for data from 2012 For 2012, the same model gives: - A fall in the price of adult cattle of 12.4% paid to the producer - A fall in earnings of between 37% and 124%. 8 Non-Hormone Treated Cattle. Name of the hormone-free rearing programme applied to European supply chains. The EU is the only region to apply the NHTC premium: cuts which are not sent to the EU and are sold on the conventional market do not benefit from their non-hormone treated origin. 9 Where over 60% of their turnover comes from the sale of adult bovines.

15 CONFIDENTIAL Région Case study System of production Pays de la Grass-fed and concentra tes Pays de la Intensive Pays de la Semi intensiv e Poitou- Charentes Race Parthenaise Pays de la AOC Maine -Anjou Pays de la Collective farming group (GAEC) Auvergne Extensive Farming Limousine Number of LU Of which: suckling cattle Agricultural land (hectares) Labour Unit 1,2 1,2 1,2 2,0 1,2 2,2 1,8 1,5 Share of adult cattle in turnover 75% 73% 71% 71% 69% 69% 60% 69% (%) 2013 profits Turnover ( 1,000) before impact Operating profits ( 1,000) % operating profits/turnover 11% 13% 14% 15% 14% 17% 16% 24% TTIP+CETA impact on operating profits % -55% -50% -46% -46% -40% -37% -27% 2012 profits before impact Share of adult bovines in turnover (%) Operating profits ( 1,000) % operating profits/turnover TTIP+CETA impact on operating profits % 68% 68% 67% 65% 66% 67% Turnover ( 1,000) % 14% 14% 11% 13% 16% 22% Limousin -124% -58% -61% -77% -62% -52% -37% Semiintensive Limousine Summary of Estimates and Data from Part Source Exchange rate /USD Banque de France Price of CHOICE loin (cwt/usd) USDA Price of CHOICE carcass (cwt/usd) USDA Type of meat 100% Choice 100% Choice Estimations Level of NHTC premium (USD/animal) Interviews/Bibliography % of loin in exports to EU 75% 75% Estimations Transport cost 5% 5% OECD Wholesaler margin 10% 10% INSEE Customs duties 0% 0% Estimations Price of young bull carcass in Hamburg before impact ( /kg) AMI Price to the producer of young bull in Europe before impact European Commission ( /kg carcass equivalent weight) Premium for EU-origin meat on the European market 10% 10% Estimations/AMI

CETA and Transatlantic Trade and Investment Partnership (TTIP) - What are the consequences for the French beef sector?

- What are the consequences for the French beef sector?") Ref. Ares(2015)2247606 Ares(2015)412940-02/02/2015 29/05/2015 CETA and Transatlantic Trade and Investment Partnership (TTIP) - What are the consequences for the French beef sector? French beef producers

Ref. Ares(2015)2247606 Ares(2015)412940-02/02/2015 29/05/2015 CETA and Transatlantic Trade and Investment Partnership (TTIP) - What are the consequences for the French beef sector? French beef producers

AN AHDB PAPER ON THE IMPACT OF CHANGES IN COUPLED PAYMENTS TO THE UK CATTLE AND SHEEP SECTORS

AN AHDB PAPER ON THE IMPACT OF CHANGES IN COUPLED PAYMENTS TO THE UK CATTLE AND SHEEP SECTORS Executive Summary This paper, from the Agriculture and Horticulture Development Board (AHDB), examines the

AN AHDB PAPER ON THE IMPACT OF CHANGES IN COUPLED PAYMENTS TO THE UK CATTLE AND SHEEP SECTORS Executive Summary This paper, from the Agriculture and Horticulture Development Board (AHDB), examines the

French beef industry chain at the turning point. Philippe Chotteau Head Economics Dpt Institut de l Elevage

French beef industry chain at the turning point Philippe Chotteau Head Economics Dpt Institut de l Elevage 1 Plan French Beef balance & 2015 forecast Main beef systems profitability Impacts of the new

French beef industry chain at the turning point Philippe Chotteau Head Economics Dpt Institut de l Elevage 1 Plan French Beef balance & 2015 forecast Main beef systems profitability Impacts of the new

INTERNATIONAL MEAT COUNCIL. Inventory of Domestic Policies and Trade Measures and Information on Bilateral, Plurilateral or Multilateral Commitments

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED 26 April 1989 Arrangement Regarding Bovine Meat Original : French INTERNATIONAL MEAT COUNCIL Inventory of Domestic Policies and Trade Measures and Information

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED 26 April 1989 Arrangement Regarding Bovine Meat Original : French INTERNATIONAL MEAT COUNCIL Inventory of Domestic Policies and Trade Measures and Information

Prices and margins formation in beef industry

Prices and margins formation in beef industry Methods and results of the French Observatory on prices and margins formation of food products Presentation to The Meat Market Observatory EC, Brussels, 2016,

Prices and margins formation in beef industry Methods and results of the French Observatory on prices and margins formation of food products Presentation to The Meat Market Observatory EC, Brussels, 2016,

Some aspects of beef marketing in Portugal

Some aspects of beef marketing in Portugal Roquete C., Fernandes L. in Belhadj T. (ed.), Boutonnet J.P. (ed.), Di Giulio A. (ed.). Filière des viandes rouges dans les pays méditerranéens Zaragoza : CIHEAM

Some aspects of beef marketing in Portugal Roquete C., Fernandes L. in Belhadj T. (ed.), Boutonnet J.P. (ed.), Di Giulio A. (ed.). Filière des viandes rouges dans les pays méditerranéens Zaragoza : CIHEAM

MEAT INDUSTRY KEY INFO IN POINTS

MEAT INDUSTRY 10 KEY INFO IN POINTS 1 FRANCE: EUROPE S LARGEST CATTLE HERD France has over 19 million cattle, more than any other European country. With nearly 3.7 million dairy cattle and over 4 million

MEAT INDUSTRY 10 KEY INFO IN POINTS 1 FRANCE: EUROPE S LARGEST CATTLE HERD France has over 19 million cattle, more than any other European country. With nearly 3.7 million dairy cattle and over 4 million

France s strategy for a more profitable beef & sheep industry

France s strategy for a more profitable beef & sheep industry L. Griffon 1, A. Bonnot 1 1 Institut de l Elevage, 149 rue de Bercy, 75595 Paris Cedex 12, France Abstract France has developed genetic programs

France s strategy for a more profitable beef & sheep industry L. Griffon 1, A. Bonnot 1 1 Institut de l Elevage, 149 rue de Bercy, 75595 Paris Cedex 12, France Abstract France has developed genetic programs

Beef and veal producers Committed to a green economy

Beef and veal producers Committed to a green economy Working for a green econo The beef and veal sector counts more than 500,000 beef producers in the EU28 and contributes to sustainable development. Production

Beef and veal producers Committed to a green economy Working for a green econo The beef and veal sector counts more than 500,000 beef producers in the EU28 and contributes to sustainable development. Production

BEEF PRODUCTION SYSTEM GUIDELINES. Animal & Grassland Research & Innovation Programme

BEEF PRODUCTION SYSTEM GUIDELINES Animal & Grassland Research & Innovation Programme INTRODUCTION 03 Under 16 Month Bull Beef (Suckler) (High Concentrate) 04 Under 16 Month Bull Beef (Suckler) 06 Under

BEEF PRODUCTION SYSTEM GUIDELINES Animal & Grassland Research & Innovation Programme INTRODUCTION 03 Under 16 Month Bull Beef (Suckler) (High Concentrate) 04 Under 16 Month Bull Beef (Suckler) 06 Under

UNDER 16 MONTH BULL BEEF (SUCKLER)

") UNDER 16 MONTH BULL BEEF (SUCKLER) 1. SYSTEM DESCRIPTION (HIGH CONCENTRATE) Production of young bulls from the suckler herd which are slaughtered before they reach 16 months of age. These young bulls are

UNDER 16 MONTH BULL BEEF (SUCKLER) 1. SYSTEM DESCRIPTION (HIGH CONCENTRATE) Production of young bulls from the suckler herd which are slaughtered before they reach 16 months of age. These young bulls are

IMPLEMENTATION OF THE CAP REFORM ON LEAN BEEF FARMING SYSTEMS

IMPLEMENTATION OF THE CAP REFORM ON LEAN BEEF FARMING SYSTEMS F. Bécherel - French Livestock Institute, France Slide number 1 EU COW CALF ENTERPRISES : MAIN COUNTRIES Countries Total Farms Germany Spain

IMPLEMENTATION OF THE CAP REFORM ON LEAN BEEF FARMING SYSTEMS F. Bécherel - French Livestock Institute, France Slide number 1 EU COW CALF ENTERPRISES : MAIN COUNTRIES Countries Total Farms Germany Spain

Glossary of terms used in agri benchmark

Whole farm Assumptions Harvest years / agricultural years They usually comprise two calendar years, e.g. July 2000 - June 2001. TIPI-CAL year The model calculates on a calendar year basis (January December).

Whole farm Assumptions Harvest years / agricultural years They usually comprise two calendar years, e.g. July 2000 - June 2001. TIPI-CAL year The model calculates on a calendar year basis (January December).

Meat Trade Sector COCERAL AGM

EUROPEAN LIVESTOCK AND MEAT TRADES UNION UECBV Meat Trade Sector COCERAL AGM Jean-Luc Mériaux Secretary General 1 What is the UECBV? Global/EU meat market: Meat industry Single Market and EU integration.

EUROPEAN LIVESTOCK AND MEAT TRADES UNION UECBV Meat Trade Sector COCERAL AGM Jean-Luc Mériaux Secretary General 1 What is the UECBV? Global/EU meat market: Meat industry Single Market and EU integration.

Case Studies presentations Argentina Pampean Beef Meat

Case Studies presentations Argentina Pampean Beef Meat Marcelo Champredonde (INTA) Claire Cerdan (CIRAD) Delphine Vitrolles (Univ. Lyon 2/CIRAD) and François Casabianca (INRA) Case presentation Argentine

Case Studies presentations Argentina Pampean Beef Meat Marcelo Champredonde (INTA) Claire Cerdan (CIRAD) Delphine Vitrolles (Univ. Lyon 2/CIRAD) and François Casabianca (INRA) Case presentation Argentine

Beef production, supply and quality from farm to fork in Europe

INNOVATION IN LIVESTOCK PRODUCTION: FROM IDEAS TO PRACTICE Beef production, supply and quality from farm to fork in Europe Kees de Roest and Claudio Montanari EAAP, 1 September 2015 Research Center for

INNOVATION IN LIVESTOCK PRODUCTION: FROM IDEAS TO PRACTICE Beef production, supply and quality from farm to fork in Europe Kees de Roest and Claudio Montanari EAAP, 1 September 2015 Research Center for

Prices and margins formation in pork industry

Prices and margins formation in pork industry Methods and results of the French Observatory on prices and margins formation of food products Presentation to The Meat Market Observatory EC, Brussels, 2016,

Prices and margins formation in pork industry Methods and results of the French Observatory on prices and margins formation of food products Presentation to The Meat Market Observatory EC, Brussels, 2016,

New Zealand. New Zealand Cattle and Beef Semi-Annual Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 3/15/2012 GAIN Report Number:

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 3/15/2012 GAIN Report Number:

TRACEABILITY OF BEEF PRODUCTION AND INDUSTRY IN FRANCE Unique identification number, passport, movements, slaughtering number

TRACEABILITY OF BEEF PRODUCTION AND INDUSTRY IN FRANCE Unique identification number, passport, movements, slaughtering number L. Marguin B. Balvay INSTITUT DE L ELEVAGE 23 rue Baldassini F- 69364 LYON

TRACEABILITY OF BEEF PRODUCTION AND INDUSTRY IN FRANCE Unique identification number, passport, movements, slaughtering number L. Marguin B. Balvay INSTITUT DE L ELEVAGE 23 rue Baldassini F- 69364 LYON

Latest developments of beef production in the EU. Mark Topliff Senior Analyst AHDB Market Intelligence Brisbane June 2010

Latest developments of beef production in the EU Mark Topliff Senior Analyst AHDB Market Intelligence Brisbane June 2010 Overview of EU cattle sector Background Over 24 million dairy cows and over 12 million

Latest developments of beef production in the EU Mark Topliff Senior Analyst AHDB Market Intelligence Brisbane June 2010 Overview of EU cattle sector Background Over 24 million dairy cows and over 12 million

3rd Cattle Network EAAP Workshop

3rd Cattle Network EAAP Workshop Profitability and sustainability of beef farming: Adaptation and conformation of EU beef systems to CAP regulations Friday 24 AUGUST 2007 DUBLIN, Ireland Organized by the

3rd Cattle Network EAAP Workshop Profitability and sustainability of beef farming: Adaptation and conformation of EU beef systems to CAP regulations Friday 24 AUGUST 2007 DUBLIN, Ireland Organized by the

CCA - Responding to NFU Cattle Industry Report 1 of 5

Canadian Cattlemen s Association Responding to the National Farmers Union Report The Farm Crisis and the Cattle Sector: Toward a New Analysis and New Solutions On November 19, 2008 the National Farmers

Canadian Cattlemen s Association Responding to the National Farmers Union Report The Farm Crisis and the Cattle Sector: Toward a New Analysis and New Solutions On November 19, 2008 the National Farmers

GENERAL AGREEMENT ON TARIFFS AND TRADE

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED IMC/ INV/24 3 June 1986 Arrangement Regarding Bovine Meet Original: English INTERNATIONAL MEAT COUNCIL Inventory of Domestic Policies and Trade Measures

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED IMC/ INV/24 3 June 1986 Arrangement Regarding Bovine Meet Original: English INTERNATIONAL MEAT COUNCIL Inventory of Domestic Policies and Trade Measures

INTERNATIONAL MEAT COUNCIL. Inventory of Domestic Policies and Trade Measures and Information on Bilateral. Plurilateral or Multilateral Commitments

GENERAL AGREEMENT ON TARIFFS AND TRADE Arrangement Regarding Bovine Meat RESTRICTED IMC/INV/15/Rev.8 17 June 1993 Special Distribution Original: French INTERNATIONAL MEAT COUNCIL Inventory of Domestic

GENERAL AGREEMENT ON TARIFFS AND TRADE Arrangement Regarding Bovine Meat RESTRICTED IMC/INV/15/Rev.8 17 June 1993 Special Distribution Original: French INTERNATIONAL MEAT COUNCIL Inventory of Domestic

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 2/27/2013 GAIN Report Number:

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 2/27/2013 GAIN Report Number:

Beef and Sheep Network

Beef and Sheep Network Claus Deblitz A new dimension for the analysis of the beef sector Working Paper 1/2011 Part 1 1 A global network for the exchange of information, knowledge and expertise generating

Beef and Sheep Network Claus Deblitz A new dimension for the analysis of the beef sector Working Paper 1/2011 Part 1 1 A global network for the exchange of information, knowledge and expertise generating

Competition in the Global Beef Industry. Clint Peck, Director, Beef Quality Assurance Montana State University

Competition in the Global Beef Industry Clint Peck, Director, Beef Quality Assurance Montana State University The competition is TOUGH 10 Largest Cattle Populations India Brazil China USA EU Argentina

Competition in the Global Beef Industry Clint Peck, Director, Beef Quality Assurance Montana State University The competition is TOUGH 10 Largest Cattle Populations India Brazil China USA EU Argentina

AGRICULTURAL TRADE AND ITS IMPORTANCE

AGRICULTURAL TRADE AND ITS IMPORTANCE 1. SOME HISTORICAL REFLECTIONS Since the founding of the Common Agricultural Policy (CAP) in 1959, one of the objectives was to increase productivity and the volume

AGRICULTURAL TRADE AND ITS IMPORTANCE 1. SOME HISTORICAL REFLECTIONS Since the founding of the Common Agricultural Policy (CAP) in 1959, one of the objectives was to increase productivity and the volume

Argentinean Beef Market Summary 1

Argentinean Beef Market Summary 1 1. According to article 18, section a) of Law N 25,156, the Comisión Nacional de Defensa de la Competencia (CNDC), Argentina s competition authority, has the power to

Argentinean Beef Market Summary 1 1. According to article 18, section a) of Law N 25,156, the Comisión Nacional de Defensa de la Competencia (CNDC), Argentina s competition authority, has the power to

STOCKTAKE REPORT 2015

STOCKTAKE REPORT 2015 This document includes costings for English cattle and sheep enterprises in the year ending 31 March 2015 CONTENTS Welcome... 1 Glossary of abbreviations... 1 Cost and price changes

STOCKTAKE REPORT 2015 This document includes costings for English cattle and sheep enterprises in the year ending 31 March 2015 CONTENTS Welcome... 1 Glossary of abbreviations... 1 Cost and price changes

Comments about the Beef & Sheep meat forecast

Comments about the Beef & Sheep meat forecast AGMEMOD Workshop 26th February 2015 Philippe Chotteau Head Economics Dpt 1 Institut de l Elevage: a specialized R&D organization GENETICS HUSBANDRY & ENVIRONMENT

Comments about the Beef & Sheep meat forecast AGMEMOD Workshop 26th February 2015 Philippe Chotteau Head Economics Dpt 1 Institut de l Elevage: a specialized R&D organization GENETICS HUSBANDRY & ENVIRONMENT

Selecting a Beef System by Pearse Kelly

Section 3 23 16 Selecting a Beef System by Pearse Kelly Introduction If the aim is to maximise profits per hectare, it is important to have as few systems as possible, know the targets achievable for them,

Section 3 23 16 Selecting a Beef System by Pearse Kelly Introduction If the aim is to maximise profits per hectare, it is important to have as few systems as possible, know the targets achievable for them,

Documentation of statistics for Slaughter Animals and Meat Production 2017 Month 06

Documentation of statistics for Slaughter Animals and Meat Production 2017 Month 06 1 / 14 1 Introduction (S.0) The purpose of these statistics are to show changes in the size and value of total production

Documentation of statistics for Slaughter Animals and Meat Production 2017 Month 06 1 / 14 1 Introduction (S.0) The purpose of these statistics are to show changes in the size and value of total production

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR AGRICULTURE AND RURAL DEVELOPMENT

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR AGRICULTURE AND RURAL DEVELOPMENT Directorate L. Economic analysis, perspectives and evaluations L.3. Microeconomic analysis of EU agricultural holdings Brussels,

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR AGRICULTURE AND RURAL DEVELOPMENT Directorate L. Economic analysis, perspectives and evaluations L.3. Microeconomic analysis of EU agricultural holdings Brussels,

Graph 1.0 Consumption of Carcase Meat & Offal in Wales Source: Defra, National Statistics

Market Bulletin Information Changes in Carcase Meat & Offal Consumption The Family Food Survey for 27 was published recently by the Office of National Statistics. This report looks at how the consumption

Market Bulletin Information Changes in Carcase Meat & Offal Consumption The Family Food Survey for 27 was published recently by the Office of National Statistics. This report looks at how the consumption

The New Zealand Agricultural Story. Successes, Challenges and Opportunities from a hungry world

The New Zealand Agricultural Story. Successes, Challenges and Opportunities from a hungry world Mike Petersen, New Zealand s Special Agricultural Trade Envoy First, a little about New Zealand Population

The New Zealand Agricultural Story. Successes, Challenges and Opportunities from a hungry world Mike Petersen, New Zealand s Special Agricultural Trade Envoy First, a little about New Zealand Population

CURRENT ACTIVITIES IN THE SOUTH AFRICAN BEEF INDUSTRY. 15 October 2014 GERHARD SCHUTTE CEO : RED MEAT PRODUCERS ORGANISATION

CURRENT ACTIVITIES IN THE SOUTH AFRICAN BEEF INDUSTRY 15 October 2014 GERHARD SCHUTTE CEO : RED MEAT PRODUCERS ORGANISATION SWOT ANALYSIS FOR THE SOUTH AFRICAN BEEF INDUSTRY Weaknesses Threats Opportunities

CURRENT ACTIVITIES IN THE SOUTH AFRICAN BEEF INDUSTRY 15 October 2014 GERHARD SCHUTTE CEO : RED MEAT PRODUCERS ORGANISATION SWOT ANALYSIS FOR THE SOUTH AFRICAN BEEF INDUSTRY Weaknesses Threats Opportunities

Employment in the EU based on Farmed Norwegian Salmon Short version

Employment in the EU based on Farmed Norwegian Salmon Short version SINTEF Fisheries and Aquaculture SINTEF Technology and Society Fafo Institute for Labour and Social Research June 2005 Introduction SINTEF

Employment in the EU based on Farmed Norwegian Salmon Short version SINTEF Fisheries and Aquaculture SINTEF Technology and Society Fafo Institute for Labour and Social Research June 2005 Introduction SINTEF

Dual purpose breed, a more sustainable choice?

58th Annual Meeting of the European Association for Animal Production Dublin Session 23 : Free communications on Livestock Farming Systems Abstract 1404 C.Gaillard, ENESAD Dijon, France F.Casabianca, INRA-LRDE,

58th Annual Meeting of the European Association for Animal Production Dublin Session 23 : Free communications on Livestock Farming Systems Abstract 1404 C.Gaillard, ENESAD Dijon, France F.Casabianca, INRA-LRDE,

Beef Industry. Reality. Cow Numbers England 759, ,000 6% Scotland 471, ,000 7% Northern Ireland 269, ,000 9%

Beef Industry Reality Gavin Hill Beef Specialist and Assistant Regional Manager SAC Consulting Breeding herds Cow Numbers 2011 Cow Numbers 2014 England 759,000 710,000 6% Scotland 471,000 437,000 7% Northern

Beef Industry Reality Gavin Hill Beef Specialist and Assistant Regional Manager SAC Consulting Breeding herds Cow Numbers 2011 Cow Numbers 2014 England 759,000 710,000 6% Scotland 471,000 437,000 7% Northern

EU Milk Margin Estimate up to 2015

Ref. Ares(2016)5774609-05/10/2016 EU Agricultural and Farm Economics Briefs No 13 September 2016 EU Milk Margin Estimate up to 2015 An overview of estimates of of production and gross margins of milk production

Ref. Ares(2016)5774609-05/10/2016 EU Agricultural and Farm Economics Briefs No 13 September 2016 EU Milk Margin Estimate up to 2015 An overview of estimates of of production and gross margins of milk production

US Imported Beef Market A Weekly Update

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 48 December 1, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com 800-526-4612

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 48 December 1, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com 800-526-4612

US Imported Beef Market A Weekly Update

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVIII, Issue 42 October 26, 2018 Prepared by: Steiner Consulting Group SteinerConsulting.com

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVIII, Issue 42 October 26, 2018 Prepared by: Steiner Consulting Group SteinerConsulting.com

Intention to package of measures for phosphate reduction

Intention to package of measures for phosphate reduction During the last few weeks, the dairy sector has in cooperation with other parties composed a package of measures aimed at substantially reducing

Intention to package of measures for phosphate reduction During the last few weeks, the dairy sector has in cooperation with other parties composed a package of measures aimed at substantially reducing

IRISH CATTLE BREEDING FEDERATION

IRISH CATTLE BREEDING FEDERATION Information system technology for integrated animal identification, traceability and breeding the example of the Irish cattle sector. Brian Wickham (PhD) Chief Executive,

IRISH CATTLE BREEDING FEDERATION Information system technology for integrated animal identification, traceability and breeding the example of the Irish cattle sector. Brian Wickham (PhD) Chief Executive,

Developing Value Chains in Southern Africa

Developing Value Chains in Southern Africa John Purchase GBI Conference 18 April 2013 Agribusiness & Value Chains Hot Topic McKinsey & Company Lions on the Move: The Progress & Potential of African economies

Developing Value Chains in Southern Africa John Purchase GBI Conference 18 April 2013 Agribusiness & Value Chains Hot Topic McKinsey & Company Lions on the Move: The Progress & Potential of African economies

GENERAL AGREEMENT ON TARIFFS AND TRADE

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED IMC/INV/11/Rev.2 27 November 1986 Arrangement Regarding Bovine Meat Original: English INTERNATIONAL MEAT COUNCIL Inventory of Domestic Policies and Trade

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED IMC/INV/11/Rev.2 27 November 1986 Arrangement Regarding Bovine Meat Original: English INTERNATIONAL MEAT COUNCIL Inventory of Domestic Policies and Trade

DORSET COUNTY FARMS ECONOMIC IMPACT ASSESSMENT

Appendix 2 Dorset County Farms Economic Impact Assessment DORSET COUNTY FARMS ECONOMIC IMPACT ASSESSMENT February 2018 Anne Gray, 6 th February 2018 Policy and Research Dorset County Council County Hall

Appendix 2 Dorset County Farms Economic Impact Assessment DORSET COUNTY FARMS ECONOMIC IMPACT ASSESSMENT February 2018 Anne Gray, 6 th February 2018 Policy and Research Dorset County Council County Hall

In summary: Global market for cattle and beef is grossly distorted to the disadvantage of US cattle producers.

The global market place for cattle and beef trade is one of the most heavily distorted sectors of the world s economic activity. These global distortions have seriously harmed U.S. cattle producers by

The global market place for cattle and beef trade is one of the most heavily distorted sectors of the world s economic activity. These global distortions have seriously harmed U.S. cattle producers by

WTO Commitments and Support to Agriculture: Experience from Canada

WTO Commitments and Support to Agriculture: Experience from Canada Lars Brink Workshop WTO Commitments and Support to Russian Agriculture: Issues and Possible Solutions Food and Agriculture Organization

WTO Commitments and Support to Agriculture: Experience from Canada Lars Brink Workshop WTO Commitments and Support to Russian Agriculture: Issues and Possible Solutions Food and Agriculture Organization

Knowledge Growth Balance STATISTICS pigmeat

Knowledge Growth Balance pigmeat AGRICULTURE & FOOD Table of Content STRUCTURE OF PIG PRODUCERS AND PIG HERD IN DENMARK Pig Producers in Denmark 3 Structure of Pig Herd in Denmark 5 PIG POPULATION AND

Knowledge Growth Balance pigmeat AGRICULTURE & FOOD Table of Content STRUCTURE OF PIG PRODUCERS AND PIG HERD IN DENMARK Pig Producers in Denmark 3 Structure of Pig Herd in Denmark 5 PIG POPULATION AND

Argentina and Uruguay

MARKET SUPPLIER SNAPSHOT BEEF Argentina and Uruguay Argentina and Uruguay are major beef producers and exporters with a traditional and strong farming history. The Argentinean beef industry has started

MARKET SUPPLIER SNAPSHOT BEEF Argentina and Uruguay Argentina and Uruguay are major beef producers and exporters with a traditional and strong farming history. The Argentinean beef industry has started

Study on Livestock scenarios for Belgium in 2050 Full report

Study on Livestock scenarios for Belgium in 2050 Full report Authors: Anton Riera, Clémentine Antier, Philippe Baret Version: 4 th of February 2019 1 This study was conducted independently by UCLouvain

Study on Livestock scenarios for Belgium in 2050 Full report Authors: Anton Riera, Clémentine Antier, Philippe Baret Version: 4 th of February 2019 1 This study was conducted independently by UCLouvain

Cooperl Arc Atlantique: The European pig specialist

//22 Jun 2011 From starting out as a small cooperative, Cooperl Arc Atlantique has managed to build a vast pork and meat empire in the West of France, to become a leader in expertise and know-how, from

//22 Jun 2011 From starting out as a small cooperative, Cooperl Arc Atlantique has managed to build a vast pork and meat empire in the West of France, to become a leader in expertise and know-how, from

Analysis of the Impact of Decoupling on Agriculture in the UK

Analysis of the Impact of Decoupling on Agriculture in the UK Joan Moss, Seamus McErlean, Philip Kostov and Myles Patton Department of Agricultural and Food Economics Queen s University Belfast Patrick

Analysis of the Impact of Decoupling on Agriculture in the UK Joan Moss, Seamus McErlean, Philip Kostov and Myles Patton Department of Agricultural and Food Economics Queen s University Belfast Patrick

National Farmers Union. Comments on the. Saskatchewan Meat Inspection Review

National Farmers Union Comments on the Saskatchewan Meat Inspection Review December 9, 2005 Introduction National Farmers Union Comments on the Saskatchewan Meat Inspection Review December 9, 2005 The

National Farmers Union Comments on the Saskatchewan Meat Inspection Review December 9, 2005 Introduction National Farmers Union Comments on the Saskatchewan Meat Inspection Review December 9, 2005 The

Montpellier, 13 Juillet, 2011

Systèmes d information et approches pour l évaluation de la performance environnementale des filières d élevage au niveau mondial Montpellier, 13 Juillet, 2011 La problématique Évaluation basés sur des

Systèmes d information et approches pour l évaluation de la performance environnementale des filières d élevage au niveau mondial Montpellier, 13 Juillet, 2011 La problématique Évaluation basés sur des

Information based on FADN data 2013

Ref. Ares(2016)4773682-25/08/2016 EU Agricultural and Farm Economics Briefs No 12 August 2016 FARM ECONOMY OVERVIEW: BEEF SECTOR Information based on FADN data 2013 This brief provides an overview of production

Ref. Ares(2016)4773682-25/08/2016 EU Agricultural and Farm Economics Briefs No 12 August 2016 FARM ECONOMY OVERVIEW: BEEF SECTOR Information based on FADN data 2013 This brief provides an overview of production

The real value of English red meat Economic analysis

The real value of English red meat Economic analysis Final report March 2012 Kevin Marsh Evelina Bertranou Heini Suominen Disclaimer In keeping with our values of integrity and excellence, Matrix has taken

The real value of English red meat Economic analysis Final report March 2012 Kevin Marsh Evelina Bertranou Heini Suominen Disclaimer In keeping with our values of integrity and excellence, Matrix has taken

Overview. Background. Beef and Sheep Outlook Situation and Outlook for Cattle. Cattle Sheep. Inputs Outputs Margins Take Home Messages

Beef and Sheep Outlook 212 James Breen 1, Kevin Hanrahan 2 & Anne Kinsella 2 1 School of Agriculture and Food Science, UCD 2 Agricultural Economics & Farm Surveys Dept. Teagasc Outlook 212 19 th January

Beef and Sheep Outlook 212 James Breen 1, Kevin Hanrahan 2 & Anne Kinsella 2 1 School of Agriculture and Food Science, UCD 2 Agricultural Economics & Farm Surveys Dept. Teagasc Outlook 212 19 th January

Florida Beef Cattle Short Course

Florida Beef Cattle Short Course Competition in the Global Beef Industry Clint Peck, director Beef Quality Assurance, Montana State Univ. The competition is TOUGH 10 Largest Cattle Populations India

Florida Beef Cattle Short Course Competition in the Global Beef Industry Clint Peck, director Beef Quality Assurance, Montana State Univ. The competition is TOUGH 10 Largest Cattle Populations India

Evaluation of CAP measures for the sheep and goat sector

Ref. Ares(2011)1350301-13/12/2011 10 Boulevard de Bonne Nouvelle - 75010 Paris In collaboration with COGEA (Roma) And the Institut de l Elevage, QMS, MLCS, Speed, Incatema, Board Bia Evaluation of CAP

Ref. Ares(2011)1350301-13/12/2011 10 Boulevard de Bonne Nouvelle - 75010 Paris In collaboration with COGEA (Roma) And the Institut de l Elevage, QMS, MLCS, Speed, Incatema, Board Bia Evaluation of CAP

The milk package and the prospects for the dairy sector

The milk package and the prospects for the dairy sector Answers to five questions in the light of the French experience Vincent CHATELLIER INRA, SMART-LERECO (France) European Parliament Commission Agriculture

The milk package and the prospects for the dairy sector Answers to five questions in the light of the French experience Vincent CHATELLIER INRA, SMART-LERECO (France) European Parliament Commission Agriculture

European beef farming systems classification

3rd Cattle Network EAAP Workshop Friday 24 AUGUST 2007 DUBLIN, Ireland European beef farming systems classification P. Sarzeaud (1) - F. Becherel (2) - C. Perrot (3) Livestock Institute - France Slide

3rd Cattle Network EAAP Workshop Friday 24 AUGUST 2007 DUBLIN, Ireland European beef farming systems classification P. Sarzeaud (1) - F. Becherel (2) - C. Perrot (3) Livestock Institute - France Slide

BULGARIA: ESTIMATES OF SUPPORT TO AGRICULTURE. Tel : (33-1) Fax : (33-1) DEFINITION AND SOURCES

Fax : (33-1) DEFINITION AND SOURCES") BULGARIA: ESTIMATES OF SUPPORT TO AGRICULTURE Contact person: Catherine Moreddu Email: catherine.moreddu@oecd.org Tel : (33-1) 45 24 95 57 Fax : (33-1) 44 30 61 01 DEFINITION AND SOURCES Country Total

BULGARIA: ESTIMATES OF SUPPORT TO AGRICULTURE Contact person: Catherine Moreddu Email: catherine.moreddu@oecd.org Tel : (33-1) 45 24 95 57 Fax : (33-1) 44 30 61 01 DEFINITION AND SOURCES Country Total

US Imported Beef Market A Weekly Update

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVIII, Issue 9 March 9, 2018 Prepared by: Steiner Consulting Group SteinerConsulting.com 800-526-4612

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVIII, Issue 9 March 9, 2018 Prepared by: Steiner Consulting Group SteinerConsulting.com 800-526-4612

% of Reference Price 190% Avg Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec. Male Calves Dairy Type Male Calves Beef Type

EU Canada Chile Chile EU Canada Trade Tonnes cw in Tonnes cwe In Tonnes cwe Russia (up to Aug) Japan Mexico (up to Aug) South Korea Russia (up to Aug) Japan Mexico (up to Aug) South Korea Qty in 1 Tonnes

EU Canada Chile Chile EU Canada Trade Tonnes cw in Tonnes cwe In Tonnes cwe Russia (up to Aug) Japan Mexico (up to Aug) South Korea Russia (up to Aug) Japan Mexico (up to Aug) South Korea Qty in 1 Tonnes

ANNEX 5: Animals and Animal products

ANNEX 5: Animals and Animal products In general, the calculation of the values of animals is the quantity multiplied by average prices. For cattle, pigs and other animals the calculation of the value is:

ANNEX 5: Animals and Animal products In general, the calculation of the values of animals is the quantity multiplied by average prices. For cattle, pigs and other animals the calculation of the value is:

% of Reference Price 190% Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Beef & Veal Production (E28 Slaughtering) - Tonnes

- Tonnes") Iran EU Iran EU Trade Japan Japan South Korea Tonnes cw in Tonnes cwe South Korea Qty in 1 Tonnes World Trade -8.4% Production Production & Stocks -1.8% -4.2% -4.2% -.6% EU Uruguay Paraguay Iran EU Paraguay

Iran EU Iran EU Trade Japan Japan South Korea Tonnes cw in Tonnes cwe South Korea Qty in 1 Tonnes World Trade -8.4% Production Production & Stocks -1.8% -4.2% -4.2% -.6% EU Uruguay Paraguay Iran EU Paraguay

Meat Traceability in Japan

Center for Agricultural and Rural Development (CARD) November 2003 Roxanne Clemens Review Paper (IAR 9:4:4-5) November 2003 Center for Agricultural and Rural Development Iowa State University Ames, Iowa

Center for Agricultural and Rural Development (CARD) November 2003 Roxanne Clemens Review Paper (IAR 9:4:4-5) November 2003 Center for Agricultural and Rural Development Iowa State University Ames, Iowa

PLEASURE WITH A CLEAR CONSCIENCE beef from the grasslands of the Baltic States Estonia, Latvia and Lithuania.

PLEASURE WITH A CLEAR CONSCIENCE beef from the grasslands of the Baltic States Estonia, Latvia and Lithuania. Version from 30.05.2018 1 INDEX OF CONTENT overview 4...INITIAL POSITION OBJECTIVE Philosophy

PLEASURE WITH A CLEAR CONSCIENCE beef from the grasslands of the Baltic States Estonia, Latvia and Lithuania. Version from 30.05.2018 1 INDEX OF CONTENT overview 4...INITIAL POSITION OBJECTIVE Philosophy

EU beef sector report DG AGRI L3, 4 April 2011

EU beef sector report 2010 DG AGRI L3, 4 April 2011 Structure of this presentation 1. Methodology 2. Beef production costs and margins 3. Income indicators 4. Summary and Conclusions 1. Methodology What

EU beef sector report 2010 DG AGRI L3, 4 April 2011 Structure of this presentation 1. Methodology 2. Beef production costs and margins 3. Income indicators 4. Summary and Conclusions 1. Methodology What

Pampa Gaucho da Campanha Meridional Meat

Pampa Gaucho da Campanha Meridional Meat Claire Cerdan (CIRAD) Delphine Vitrolles (Uni. Lyon 2/CIRAD) Luiz Otavio Pimentel (UFSC) - John Wilkinson (UFFRJ) Carne do Pampa Gaúcho da Campanha Meridional IP

Pampa Gaucho da Campanha Meridional Meat Claire Cerdan (CIRAD) Delphine Vitrolles (Uni. Lyon 2/CIRAD) Luiz Otavio Pimentel (UFSC) - John Wilkinson (UFFRJ) Carne do Pampa Gaúcho da Campanha Meridional IP

agrodok Beef production

agrodok Beef production 55 agrodok Beef production 55 Agromisa Foundation and CTA, Wageningen 2016 All rights reserved. No part of this book may be reproduced in any form, by print, photocopy, microfilm

agrodok Beef production 55 agrodok Beef production 55 Agromisa Foundation and CTA, Wageningen 2016 All rights reserved. No part of this book may be reproduced in any form, by print, photocopy, microfilm

% of Reference Price 190% Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Beef & Veal Production (E28 Slaughtering) - Tonnes

- Tonnes") Trade Prices Production Production & Stocks DG AGRI DASHBOARD: BEEF AND VEAL Last update: 5.1.217 Carcasse Live Animals 3.2% 1.7% -6.3% -4.2% -1.8% -7.3% 4.2% /1 kg Tonnes cw /head /kg 16.5% 1.5% -1.6%

Trade Prices Production Production & Stocks DG AGRI DASHBOARD: BEEF AND VEAL Last update: 5.1.217 Carcasse Live Animals 3.2% 1.7% -6.3% -4.2% -1.8% -7.3% 4.2% /1 kg Tonnes cw /head /kg 16.5% 1.5% -1.6%

GENERAL AGREEMENT ON TARIFFS AND TRADE

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED 3 November 1986 International Dairy Arrangement Original: English INTERNATIONAL DAIRY PRODUCTS COUNCIL Reply to Questinnaire 5 Regarding Information on

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED 3 November 1986 International Dairy Arrangement Original: English INTERNATIONAL DAIRY PRODUCTS COUNCIL Reply to Questinnaire 5 Regarding Information on

% of Reference Price 190% Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Beef & Veal Production (E28 Slaughtering) - Tonnes

- Tonnes") EU Trade Japan South Korea Russia (up to Mar) Chile (up to Mar) EU Chile (up to Mar) in Tonnes cwe Japan South Korea Russia (up to Mar) Tonnes cw Qty in 1 Tonnes World Trade China + H. Kong China + H.

EU Trade Japan South Korea Russia (up to Mar) Chile (up to Mar) EU Chile (up to Mar) in Tonnes cwe Japan South Korea Russia (up to Mar) Tonnes cw Qty in 1 Tonnes World Trade China + H. Kong China + H.

US Imported Beef Market A Weekly Update

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVIII, Issue 48 December 7, 2018 Prepared by: Steiner Consulting Group SteinerConsulting.com

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVIII, Issue 48 December 7, 2018 Prepared by: Steiner Consulting Group SteinerConsulting.com

EU Milk Margin Estimate up to 2016

EU Agricultural and Farm Economics Briefs No 16 December 217 EU Milk Margin Estimate up to 216 An overview of estimates of of production and gross margins of milk production in the EU Contents Need for

EU Agricultural and Farm Economics Briefs No 16 December 217 EU Milk Margin Estimate up to 216 An overview of estimates of of production and gross margins of milk production in the EU Contents Need for

EU milk margin index estimate up to 2018

EU Agricultural and Farm Economics Briefs No 17 December 2018 EU milk margin index estimate up to 2018 An overview of estimates of of production and gross margin indexes of milk production in the EU Contents

EU Agricultural and Farm Economics Briefs No 17 December 2018 EU milk margin index estimate up to 2018 An overview of estimates of of production and gross margin indexes of milk production in the EU Contents

COSTS UP, PRICES UP BREXIT S IMPACT ON CONSUMER BUSINESSES AND THEIR CUSTOMERS

COSTS UP, PRICES UP BREXIT S IMPACT ON CONSUMER BUSINESSES AND THEIR CUSTOMERS AUTHORS Duncan Brewer, Partner Lisa Quest, Partner Rachel Gregory, Associate INTRODUCTION Brexit outcomes remain uncertain

COSTS UP, PRICES UP BREXIT S IMPACT ON CONSUMER BUSINESSES AND THEIR CUSTOMERS AUTHORS Duncan Brewer, Partner Lisa Quest, Partner Rachel Gregory, Associate INTRODUCTION Brexit outcomes remain uncertain

BEEF CATTLE FARMS IN LESS-FAVOURED AREAS

BEEF CATTLE FARMS IN LESS-FAVOURED AREAS Multi-performances, drivers of sustainability over the last 25 years Veysset P., Mosnier C., Lherm M. INRA Clermont-Theix, UMRH, 63122 St Genès-Champanelle VEYSSET

BEEF CATTLE FARMS IN LESS-FAVOURED AREAS Multi-performances, drivers of sustainability over the last 25 years Veysset P., Mosnier C., Lherm M. INRA Clermont-Theix, UMRH, 63122 St Genès-Champanelle VEYSSET

Chapter 5 International trade

Chapter 5 International trade International trade consists of buying and selling of exports and imports between countries. Why do we trade? The reason countries do not produce all their own goods to satisfy

Chapter 5 International trade International trade consists of buying and selling of exports and imports between countries. Why do we trade? The reason countries do not produce all their own goods to satisfy

US Imported Beef Market A Weekly Update

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVIII, Issue 43 November 2, 2018 Prepared by: Steiner Consulting Group SteinerConsulting.com

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVIII, Issue 43 November 2, 2018 Prepared by: Steiner Consulting Group SteinerConsulting.com

Farm Credit Canada Annual Report

16 17 2016-17 Annual Report Annual Report 2016-17 19 Agriculture industry overview FCC advances the business of agriculture by lending money to all agriculture sectors, including primary producers, agribusinesses

16 17 2016-17 Annual Report Annual Report 2016-17 19 Agriculture industry overview FCC advances the business of agriculture by lending money to all agriculture sectors, including primary producers, agribusinesses

% of Reference Price 190% Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Beef & Veal Production (E28 Slaughtering) - Tonnes

- Tonnes") EU Trade South Korea Malaysia (up to Sep) EU Japan Japan South Korea Malaysia (up to Sep) in Tonnes cwe Russia (up to Oct) Mexico (up to Sep) Russia (up to Oct) Mexico (up to Sep) Tonnes cw Qty in 1 Tonnes

EU Trade South Korea Malaysia (up to Sep) EU Japan Japan South Korea Malaysia (up to Sep) in Tonnes cwe Russia (up to Oct) Mexico (up to Sep) Russia (up to Oct) Mexico (up to Sep) Tonnes cw Qty in 1 Tonnes

US ranchers face a big challenge in the years

Evaluating Strategies for Ranching in the 21st Century: Ranching in the Ethanol Era By James Mintert US ranchers face a big challenge in the years ahead. Feed grain prices have increased dramatically in

Evaluating Strategies for Ranching in the 21st Century: Ranching in the Ethanol Era By James Mintert US ranchers face a big challenge in the years ahead. Feed grain prices have increased dramatically in

Canfax Research Services A Division of the Canadian Cattlemen s Association

Canfax Research Services A Division of the Canadian Cattlemen s Association Publication Sponsored By: Focus on Productivity COW/CALF PRODUCTIVITY The feedlot and packing sectors have been very successful

Canfax Research Services A Division of the Canadian Cattlemen s Association Publication Sponsored By: Focus on Productivity COW/CALF PRODUCTIVITY The feedlot and packing sectors have been very successful

Table 5 - Bovine general overview in the EU-27 (2012)

") 18 2. The veal and young cattle market chain This chapter describes the main characteristics and trends of the veal and young cattle market chain. First, general data in all the EU-27 Member States are

18 2. The veal and young cattle market chain This chapter describes the main characteristics and trends of the veal and young cattle market chain. First, general data in all the EU-27 Member States are

rerc Irish Agriculture and Food Development Authority

RERC Working Paper Series 99-WP-RE-02 The Rural Economy Research Centre Working Paper Series Working Paper 99-WP-RE-02 Development of a Strategic Approach for a Single EU Beef Market Direct Payments and

RERC Working Paper Series 99-WP-RE-02 The Rural Economy Research Centre Working Paper Series Working Paper 99-WP-RE-02 Development of a Strategic Approach for a Single EU Beef Market Direct Payments and

EXPORT OPPORTUNITIES FOR IRISH ORGANIC BEEF PRESENTED BY JOHN PURCELL GOOD HERDSMEN LTD.

EXPORT OPPORTUNITIES FOR IRISH ORGANIC BEEF PRESENTED BY JOHN PURCELL GOOD HERDSMEN LTD. INTRODUCTION: Good Herdsmen established in 1989 by Josef Finke. Opened Ireland s first independent organic meat

EXPORT OPPORTUNITIES FOR IRISH ORGANIC BEEF PRESENTED BY JOHN PURCELL GOOD HERDSMEN LTD. INTRODUCTION: Good Herdsmen established in 1989 by Josef Finke. Opened Ireland s first independent organic meat

Irish Agriculture 20 th June 2018 Trevor Donnellan: Teagasc

Irish Agriculture 20 th June 2018 Trevor Donnellan: Teagasc trevor.donnellan@teagasc.ie Current position What does Brexit mean? Implications of Brexit? RICS Rural Conference, Cirencester, June 20 th 2018

Irish Agriculture 20 th June 2018 Trevor Donnellan: Teagasc trevor.donnellan@teagasc.ie Current position What does Brexit mean? Implications of Brexit? RICS Rural Conference, Cirencester, June 20 th 2018

A293. Production, Finance and External Business Environment. Formulas and Key words

A293 Production, Finance and External Business Environment Formulas and Key words Formulas Fixed costs costs that do not change when the business changes the amount it produces Variable costs costs that

A293 Production, Finance and External Business Environment Formulas and Key words Formulas Fixed costs costs that do not change when the business changes the amount it produces Variable costs costs that

European Union. >US$35,000/year. In million In million households In million households

MARKET SNAPSHOT BEEF European Union The European Union (EU) contains one of the largest pools of wealthy consumers (households earning in excess of US$,/year) in the world. While a lucrative market, the

MARKET SNAPSHOT BEEF European Union The European Union (EU) contains one of the largest pools of wealthy consumers (households earning in excess of US$,/year) in the world. While a lucrative market, the

EXECUTIVE SUMMARY

EXECUTIVE SUMMARY Herlambang, Tedy. Came Fattening and Slaughter Houses Business in Indonesia: Players, Volume, Consumption, Investment and Forecast (Supervised by E. GumbiraSa'id, Soeksmono B. Martakoesoemo

EXECUTIVE SUMMARY Herlambang, Tedy. Came Fattening and Slaughter Houses Business in Indonesia: Players, Volume, Consumption, Investment and Forecast (Supervised by E. GumbiraSa'id, Soeksmono B. Martakoesoemo

Brief for Market Research and Strategic Plan for the Promotion of Argentine Beef in China and Hong Kong 1.

1 Brief for Market Research and Strategic Plan for the Promotion of Argentine Beef in China and Hong Kong 1. General objective The aim is to carry out a Market Research study for Argentine Chilled and

1 Brief for Market Research and Strategic Plan for the Promotion of Argentine Beef in China and Hong Kong 1. General objective The aim is to carry out a Market Research study for Argentine Chilled and

Proceedings, Range Beef Cow Symposium November 29, 30 and December 1, 2011 Mitchell NE. Global Beef Marketing Opportunities

Proceedings, Range Beef Cow Symposium November 29, 30 and December 1, 2011 Mitchell NE Global Beef Marketing Opportunities Paul Clayton U.S. Meat Export Federation, Denver CO Introduction Over the last

Proceedings, Range Beef Cow Symposium November 29, 30 and December 1, 2011 Mitchell NE Global Beef Marketing Opportunities Paul Clayton U.S. Meat Export Federation, Denver CO Introduction Over the last

3rd Cattle Network EAAP Workshop

3rd Cattle Network EAAP Workshop Profitability and sustainability of beef farming: Adaptation and conformation of EU beef systems to CAP regulations Friday 24 AUGUST 2007 DUBLIN, Ireland Organized by the

3rd Cattle Network EAAP Workshop Profitability and sustainability of beef farming: Adaptation and conformation of EU beef systems to CAP regulations Friday 24 AUGUST 2007 DUBLIN, Ireland Organized by the

SWEDISH FARMING, BEEF PRODUCTION AND CHAROLAIS. - An overview Sofia Persson and Lennart Nilsson The Swedish Charolais Association

SWEDISH FARMING, BEEF PRODUCTION AND CHAROLAIS - An overview 2018 Sofia Persson and Lennart Nilsson The Association Short about Sweden - 21 counties - 290 municipalities - 2523 parishes - 87 % lives in

SWEDISH FARMING, BEEF PRODUCTION AND CHAROLAIS - An overview 2018 Sofia Persson and Lennart Nilsson The Association Short about Sweden - 21 counties - 290 municipalities - 2523 parishes - 87 % lives in

Australian beef production in a global market- How do we compare?

Australian beef production in a global market- How do we compare? Lloyd Davies, Agricultural Economist Agribusiness Today 2012 Profitable Beef in a Challenging Future Outline of talk What agri-benchmark

Australian beef production in a global market- How do we compare? Lloyd Davies, Agricultural Economist Agribusiness Today 2012 Profitable Beef in a Challenging Future Outline of talk What agri-benchmark