MARTINSON AG. Jan. 12, 2018 WHEAT

|

|

|

- Gwenda Bradley

- 6 years ago

- Views:

Transcription

1 MARTINSON AG Jan. 12, 2018 WHEAT Wheat started the week by opening lower in the overnight session and proceeded to trade mixed throughout the day with strength in Mpls and modest losses in the winter wheat contracts. Early pressure was due to weather forecasts calling for the Southern Plains to see a slight warm up in temps, which will be accompanied by chances for rain. But the losses were kept in check by reports of freeze damage to the soft red winter wheat crop. Long term weather forecasts are calling for the cold temps to return, which will likely add to crop stress. In export news, Morocco bought 315 TMT of US soft red wheat overnight. On Tuesday, wheat traded with gains throughout the session as traders worked a little weather premium back into the market. Light trading was due to technical buying. Position squaring ahead of Friday s report was also noted as early estimates indicate little change in wheat s supply and demand estimates, but winter wheat acreage is expected to drop 4.5% (likely closer to 8 to 9%). If that is realized, it would be the 5th straight year of declining acreage. In export news, Japan was in tendering for 56,981 MT of US wheat in their weekly tender. Wheat traded with gains for most of the session on Wednesday. Expectations for lower planted winter wheat acreage helped give the market strength. Additional support came from weather forecasts calling for another round of extreme cold temps for the Southern Plains. After a few days of melting any snow cover, this round of freezing temps will likely result in more crop damage. In export news, Taiwan bought 73,625 MT of wheat overnight. Thursday s session saw wheat trading lower overnight, with most contracts trading in a tight two cent trading range. Early selling pressure came from this morning s disappointing export sales estimate, which was below expectations. Pressure also came from reports of rain in parts of KS, but so far amounts and coverage have been disappointing. Losses were kept in check by this morning s Drought Monitor map as the South saw a 5% increase in area in some sort of drought while the High Plains increased 1.2%. Position squaring ahead of Fridays USDA report was also evident. Friday s USDA reports were not as friendly wheat as expected. The Winter Wheat Seedings report was bearish as it estimated virtually unchanged acres for 2018 (decrease of 4.5% was expected). The Quarterly Grain Stocks estimate was neutral wheat as stocks were 10% lower than last year. But wheat s Supply and Demand estimate was negative, increasing the US ending stocks estimate to 989 MB, 33 MB more than expected. Mar MW support is at $5.95 and resistance is at $6.65 Last week s wheat export shipments pace was estimated at 8.6 MB and sales were at 2.6 MB. After 31 weeks, wheat shipments were at 56% of USDA s expectations while sales were at 74% of expectations (vs the 5-year average of 76%). With 21 weeks left in wheat s export marketing year, shipments need to average 20.6 MB and sales need to average 12.2 MB to make USDA s projection of 975 MB. For the week, Mar MW was at $ down 14.0 cents, Mar Chicago was at $4.205 down cents, and Mar KC was at $ down cents.

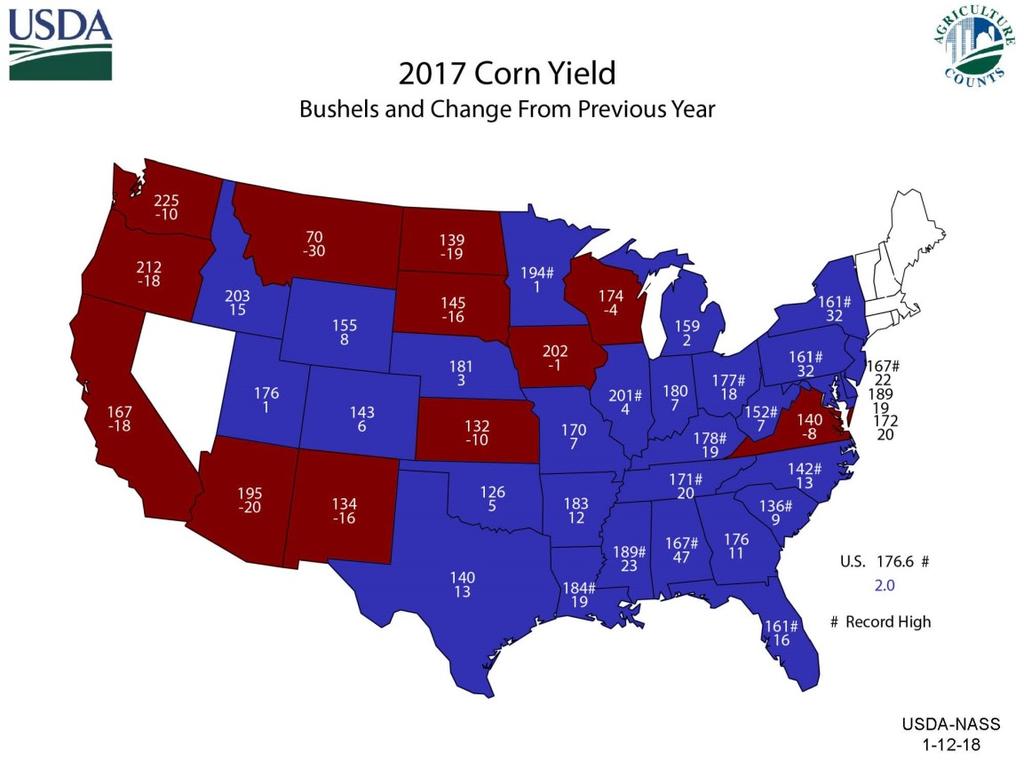

2 CORN Corn began the week by opening lower in the overnight session, and then maintained those losses throughout the day. Position squaring ahead of Friday s USDA Final Crop Production estimate was the main driver as most expect USDA to increase corn s production estimate and decrease corn s demand picture. Corn s export sales pace is in line with the 5-year average, but corn shipments are not keeping pace. Early session losses were kept in check by reports Mexico was in and bought 102 TMT of corn overnight. But that news was overshadowed by reports that US DDG exports were slightly off Oct s pace (with Mexico the main destination) and that US ethanol exports were also off Oct s pace (with Brazil the main destination). On Tuesday, corn traded with small gains in the overnight session. Early support came from technical buying as corn traded within a quarter of a cent of its recent low. Slow farmer selling added support as recent cold wintery weather has resulted in poor shipping conditions, which in turn has led to improving basis levels. Producers should be patient marketing corn at this time. Basis levels have seen a strong improvement and producers could look at locking in basis levels now, but hold off on futures. Corn traded mainly steady throughout the session on Wednesday. Corn s trading range continues to be tight as the spread between high and low was two cents. Losses were kept in check by a stronger wheat complex, while gains were limited by a weaker soybean market. Last week s ethanol production was estimated at 996,000 barrels per day, down close to 36,000 barrels per day. Ethanol stocks also saw an increase, now estimated at million barrels, up 100,000 barrels. On Thursday, corn had another uneventful day lacking in fresh news, closing just slightly lower. The Rosario Grains Exchange lowered their estimate of Argentina s corn crop to 39.9 MMT (previous estimate was 41.5 MMT and USDA s last estimate was 42.0 MMT) due to the dry conditions there. As for Brazil s CONAB s total corn estimate is at 92.3 MMT, up 0.1 MMT (vs USDA s last estimate of 95.0 MMT). Friday s USDA reports were slightly negative corn. The Quarterly Grain Stocks estimate was neutral corn as it showed only a 1% increase in corn stocks from last year. But corn s Supply and Demand estimate was negative, putting ending stocks at BB, 55 MB higher than expected. Mar corn support is at $3.465 and resistance is at $3.57. Last week s corn export shipments pace was estimated at 33.4 MB and sales were at 17.2 MB. After 18 weeks, corn shipments were at 23% of USDA s expectations while sales were at 55% of expectations (vs the 5-year average of 59%). With 34 weeks left in corn s export marketing year, shipments need to average 43.4 MB and sales need to average 25.2 MB to make USDA s projections of BB. For the week, Mar corn was at $ down 5.0 cents.

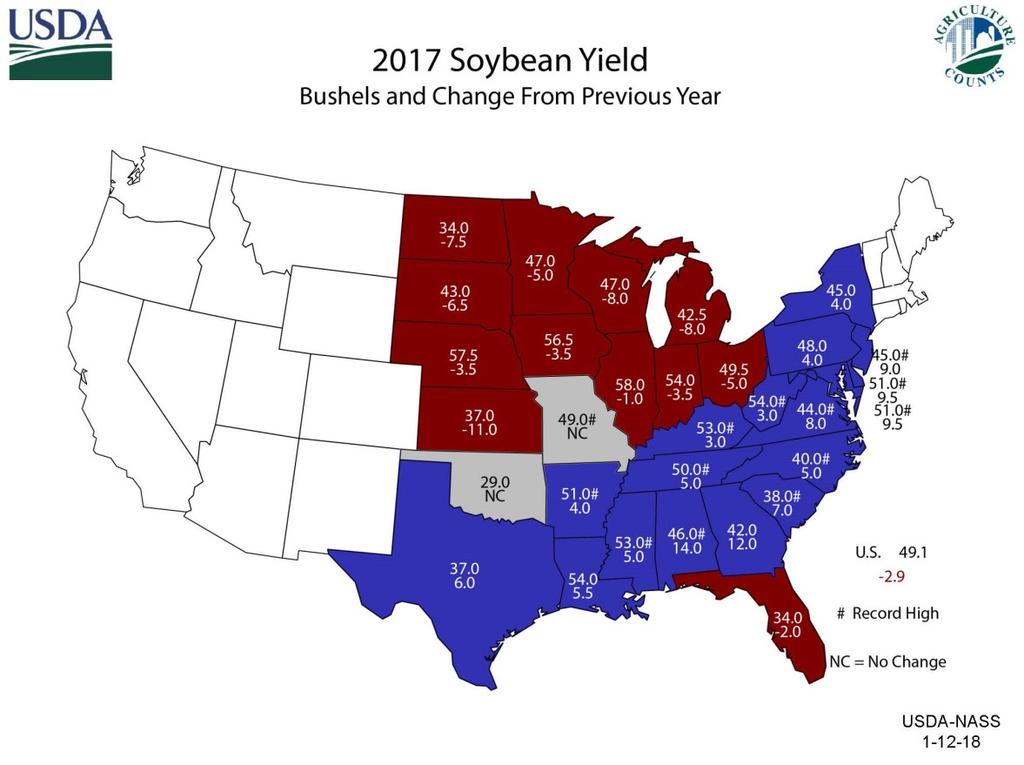

3 SOYBEAN Soybeans started the week by opening lower in the overnight session and then traded with modest losses to start the day session. By midsession the selling intensified to push most contracts to post double digit losses with selling tied to pressure from reports of decent rains over the weekend in Argentina and from wetter forecasts. Even with the weekend rains, officials are estimating 50% of Argentina is in some sort of drought. Soybeans were able to trim session losses from two separate export sales: Egypt bought 120 TMT of soybeans and an unknown destination bought 132 TMT of soybeans. On Tuesday, soybeans closed lower on forecasts of rain in Argentina, although the forecasts do not show considerable rainfall. Meanwhile, rains in the Mato Grosso region of Brazil may delay harvest there. Position squaring ahead of Friday s USDA report was also seen as most traders are looking for USDA to increase production and decrease demand, especially soybean exports since sales are running over 12% behind average. In Wednesday s session, soybeans closed lower on position squaring ahead of Friday s USDA reports. Light selling was tied to pressure from weather forecasts for Argentina, which are calling for rain. That has traders thinking that the drought scare might be less than expected. However, long term forecasts continue to call for hot dry conditions. In export news, an unknown destination bought 65 TMT of 2017 soybeans overnight and 195 TMT of 2018 soybeans. On Thursday, soybeans closed lower again, with Mar soybeans hitting lows not seen since August, as the trade assumes tomorrow s USDA report will be negative. USDA reported a sale of 132,000 MT of soybeans to an unknown destination. The Rosario Grains Exchange lowered their estimate of Argentina s soybean crop to 52.0 MMT (previous estimate was 54.5 MMT and USDA s last estimate was 57.0 MMT) due to the dry conditions there. Meanwhile, Brazil s AgRural raised their soybean crop estimate to MMT (vs their prior estimate of and USDA s last estimate of MMT). CONAB s latest estimate is MMT (vs MMT previously). In true fashion, the trade was expecting USDA s soybean numbers to be bearish, but instead they were friendly. The Quarterly Grains stocks estimate showed 9% higher soybean stocks that last year, but that was less than expected by the trade. And that was followed up with a small than expected ending stocks estimate (now estimated at 470 MB vs the average trade estimate of 474 MB) in soybeans Supply and Demand estimate. Mar soybean support is at $9.50 and resistance is at $10.27 Last week s soybean export shipments pace was estimated at 43.5 MB and sales were at 22.3 MB. After 18 weeks, soybean shipments were at 49% of USDA s expectations while sales were at 69% of expectations (vs the 5-year average of 81%). With 34 weeks left in soybean s export marketing year, shipments need to average 33.4 MB and sales need to average 20.4 MB to make USDA s projections of BB. For the week, Mar soybeans were at $9.605, down cents.

4 CATTLE Live cattle started the week off with major losses and then spent the rest of the week trading back and forth with modest changes. Monday s triple digit losses started the cattle market off on the wrong foot and just could not completely dig its way out of that hole. The lack of a cash trade and technical selling pushed the cattle lower on the opening Monday and with no one willing to step in front of the train, the selloff accelerated throughout the session. A stronger boxed beef market helped to limit the losses. Reports of cash trading at $120 helped cattle push higher on Tuesday, as did technical buying once cattle traded to support. But the recovery performance was not convincing enough to bring in new buyers. Heavy selling dominated the cattle market on Wednesday with pressure once again coming from a disappointing cash market. Reports had only 401 of the 711 head of cattle offered on the FCE Auction selling, and at $119, $1 lower than earlier in the week and $3 lower than last week. Thursday s session found willing buyers due to a better than expected export pace for beef. Light support was also due to weather forecasts calling for another round of frigid temps for the Southern Plains, which will once again decrease cattle performance and slow movement. Technically cattle are not in a good place, but fundamentally live cattle have a chance to see better days (due to lower than expected first quarter production estimates). Feeder cattle have not faired as well as the live cattle as feeder cattle posted losses in every session this week. Selling pressure did spill over from the lower fat cattle market, but selling was also tied to a firmer grain complex. Last week s warmer temps were enough to entice country movement of cattle. The large runs were enough to pull cash bids down $5 to $7 in just a few days time. Cattle movement should remain heavy over the next 3 to 4 weeks as backgrounders start to unload calves. For the week, Feb live cattle was at $ down $1.575 while Jan feeders were at $ down $2.275.

5 CANOLA/SUNFLOWER Canola started the week off under pressure and traded with losses for three out of the four session this week. Most of the pressure spilled over from a weaker US soybean complex and stronger Canadian dollar. Improving weather conditions in Argentina added some selling pressure as hit and miss showers in the central and southern regions of Argentina have helped to alleviate dry conditions. Late in the week selling was tied to an increase in farmer selling as producers started to sell product ahead of USDA s Final Crop Production report, which was expected to be negative to the oilseed market. Losses were limited by continued strong demand for canola. harvested acres: 2.0 million (+18%), yield: 1558 lbs (-15%), production: 3.1 billion lbs (+1%). For all sunflowers USDA estimated the following: planted acres: 1.4 million (-12%), harvested acres: 1.3 million (-13%), yield: 1613 lbs (-7%), and production: 2.17 billion lbs (-12%). Thursday s cash canola bids in Velva were at $17.59 and sunflower bids in Fargo were at $ For the week, Mar canola was down $5.20 at $ Canadian. In the Jan Final Crop Production report, USDA estimated the following for canola: planted acres: 2.08 million (+22%), RECOMMENDATIONS Corn 2016 Corn 2017 % Sold Sold Date % Sold Sold Date 10% $4.08 Dec 5/26/16 15% $3.95 Dec 4/13/17 20% $4.38 Dec 6/15/16 10% $4.05 Dec 6/7/17 20% $3.65 Mar 1/17/17 25% $3.85 Jul 6/7/17 75% 25% Soybeans 2016 Soybeans % $9.28 Nov 3/29/16 10% $10.15 Nov 11/22/16 15% $9.95 Nov 4/20/16 25% $9.33 Nov 10/12/17 20% $11.38 Nov 6/15/16 40% $10.20 Mar 12/6/17 25% $10.70 Mar 1/17/17 25% $10.20 Mar 12/6/17 100% 75% Wheat 2016 Wheat % $5.05 Dec MW 9/23/16 15% $5.65 Sept MW 5/1/17 20% $5.89 Mar MW 1/17/17 10% $6.05 Sept MW 6/7/17 15% $5.65 July MW 5/1/17 10% $6.35 Sept MW 6/14/17 20% $6.05 Sept MW 6/7/17 10% $6.35 Sept MW 6/14/17 75% 35%

$0.27 $0.24 Pinto $0.27 $0.21 Dry Peas: Sm. Green/Yellow $0.11 $0.12 Lentil $0.25 $0.")

6 CROP INSURANCE Upcoming Farmer Meetings: Jan 22 - Bismarck, ND Jan 23 - Dickinson, ND Feb 6 - Jamestown, ND Feb 6 - New Rockford, ND (rescheduled) Feb 8 - Fargo, ND Feb 19 - Roseau, MN Feb 20 - East Grand Forks, MN For more details, see The markets, as well as our office, will be closed Monday, January 15, for the Martin Luther King Day holiday. Dry Bean and Dry Pea Harvest Prices Released: If you have RP coverage and the harvest price is lower than the projected (spring) price, you can be over your guarantee and still possibly have a revenue loss. Crop Proj. Price Harvest Price Dry Beans: Black $0.26 $0.26 Dark Red Kidney $0.36 $0.34 Pea (Navy) $0.27 $0.24 Pinto $0.27 $0.21 Dry Peas: Sm. Green/Yellow $0.11 $0.12 Lentil $0.25 $0.25 Small Kabuli $0.22 $0.32 Large Kabuli $0.30 $0.34 The markets will reopen at 7:00 pm This material has been prepared by a sales or trading employee or agent of Martinson Ag Risk Management LLC. and is, or is in the nature of, a solicitation. This material is not a research report prepared by Martinson Ag Risk Management s Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that Martinson Ag Risk Management believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

7 Summary of January 12, 2018 USDA Crop Estimates Average Trade Estimate Change from Estimate USDA Previous Change from Previous Last Year USDA Jan USDA 2017/18 US Production (million bushels) CORN Production 14,604 14, , ,148 Yield (bu/acre) SOYBEANS Production 4,392 4,427 (35) 4,425 (33) 4,296 Yield (bu/acre) (0.4) 49.5 (0.4) 52.0 USDA 2017/18 US Ending Stocks (million bushels) Corn 2,477 2, , ,295 Soybeans (4) Wheat ,181 USDA 2017/18 World Ending Stocks (million tonnes) Corn Soybeans (0.5) Wheat (0.4) USDA 2018/19 Winter Wheat Seedings (million acres) All Winter Wheat Hard Red Winter Soft Red Winter White Winter

8

MARTINSON AG. April 20, 2018 WHEAT

MARTINSON AG April 20, 2018 WHEAT Wheat began the week by starting the overnight session mostly lower. By the close all of the wheat exchanges were posting double digit losses with most of the pressure

MARTINSON AG April 20, 2018 WHEAT Wheat began the week by starting the overnight session mostly lower. By the close all of the wheat exchanges were posting double digit losses with most of the pressure

Signs align for corn profit hopes Short crop in Brazil could be fix the market needs By Bryce Knorr, senior grain market analyst

Signs align for corn profit hopes Short crop in Brazil could be fix the market needs By Bryce Knorr, senior grain market analyst Corn growers enjoyed an outbreak of optimism last week at Commodity Classic

Signs align for corn profit hopes Short crop in Brazil could be fix the market needs By Bryce Knorr, senior grain market analyst Corn growers enjoyed an outbreak of optimism last week at Commodity Classic

KSU Agriculture Today Radio Notes

KSU Agriculture Today Radio Notes Daniel O Brien, Extension Agricultural Economist, Kansas State University For Radio Program to be aired 10:00-10:15 a.m., Friday, November 17, 2017 I. Grain Futures Closes,

KSU Agriculture Today Radio Notes Daniel O Brien, Extension Agricultural Economist, Kansas State University For Radio Program to be aired 10:00-10:15 a.m., Friday, November 17, 2017 I. Grain Futures Closes,

Santa Claus rally could help corn Be ready to sell brief rallies when they come By Bryce Knorr, senior grain market analyst

Santa Claus rally could help corn Be ready to sell brief rallies when they come By Bryce Knorr, senior grain market analyst Rallies are always possible in corn, even in down markets. Trouble is, they don

Santa Claus rally could help corn Be ready to sell brief rallies when they come By Bryce Knorr, senior grain market analyst Rallies are always possible in corn, even in down markets. Trouble is, they don

DAILY SOY COMPLEX COMMENTARY 12/20/17

Wednesday December 20, 2017 150 S. Wacker Dr., Suite 2350 Chicago, IL 60606 800-621-1414 or 312-277-0102 info@zaner.com www.zaner.com DAILY SOY COMPLEX COMMENTARY Soybean sales announcements the last three

Wednesday December 20, 2017 150 S. Wacker Dr., Suite 2350 Chicago, IL 60606 800-621-1414 or 312-277-0102 info@zaner.com www.zaner.com DAILY SOY COMPLEX COMMENTARY Soybean sales announcements the last three

Analysis of the October 2010 USDA Crop Production & WASDE Reports

Analysis of the October 2010 USDA Crop Production & WASDE Reports Daniel O Brien Extension Agricultural Economist, K State Research and Extension October 11, 2010 Summary of October 8 th 2010 Crop Production

Analysis of the October 2010 USDA Crop Production & WASDE Reports Daniel O Brien Extension Agricultural Economist, K State Research and Extension October 11, 2010 Summary of October 8 th 2010 Crop Production

October 20, 1998 Ames, Iowa Econ. Info U.S., WORLD CROP ESTIMATES TIGHTEN SOYBEAN SUPPLY- DEMAND:

October 20, 1998 Ames, Iowa Econ. Info. 1752 U.S., WORLD CROP ESTIMATES TIGHTEN SOYBEAN SUPPLY- DEMAND: USDA's domestic and world crop estimates show a less burdensome world supply-demand balance for soybeans

October 20, 1998 Ames, Iowa Econ. Info. 1752 U.S., WORLD CROP ESTIMATES TIGHTEN SOYBEAN SUPPLY- DEMAND: USDA's domestic and world crop estimates show a less burdensome world supply-demand balance for soybeans

SOYBEANS: LARGE SUPPLIES CONFIRMED, BUT WHAT ABOUT 2005 PRODUCTION?

SOYBEANS: LARGE SUPPLIES CONFIRMED, BUT WHAT ABOUT 2005 PRODUCTION? JANUARY 2005 Darrel Good 2005 NO. 2 Summary USDA s January reports confirmed a record large 2004 U.S. crop, prospects for large year-ending

SOYBEANS: LARGE SUPPLIES CONFIRMED, BUT WHAT ABOUT 2005 PRODUCTION? JANUARY 2005 Darrel Good 2005 NO. 2 Summary USDA s January reports confirmed a record large 2004 U.S. crop, prospects for large year-ending

Daily Market Highlights

Daily Market Highlights Click below to see the Daily Commentary PDF version http://www.aghost.net/images/e0176001/dailymarketcommentary.pdf Wednesday, November 2, 2016 Hogs: Today's Markets: Dec 16 LEAN

Daily Market Highlights Click below to see the Daily Commentary PDF version http://www.aghost.net/images/e0176001/dailymarketcommentary.pdf Wednesday, November 2, 2016 Hogs: Today's Markets: Dec 16 LEAN

SOUTH AMERICAN SOYBEAN CROP ESTIMATE INCREASED

April 14, 2000 Ames, Iowa Econ. Info. 1787 SOUTH AMERICAN SOYBEAN CROP ESTIMATE INCREASED USDA s World Agricultural Outlook Board raised its estimate of combined Brazilian and Argentine soybean production

April 14, 2000 Ames, Iowa Econ. Info. 1787 SOUTH AMERICAN SOYBEAN CROP ESTIMATE INCREASED USDA s World Agricultural Outlook Board raised its estimate of combined Brazilian and Argentine soybean production

Crops Marketing and Management Update

Crops Marketing and Management Update Department of Agricultural Economics Princeton REC Dr. Todd D. Davis Assistant Extension Professor -- Crop Economics Marketing & Management Vol. 2016 (3) March 9,

Crops Marketing and Management Update Department of Agricultural Economics Princeton REC Dr. Todd D. Davis Assistant Extension Professor -- Crop Economics Marketing & Management Vol. 2016 (3) March 9,

Ending stocks can adjust due to a variety of factors from changes in production as well as adjustments to beginning stocks and demand.

1 2 3 Wire services such as Reuters and Bloomberg offer a survey of analysts expectations for high-profile USDA reports. These surveys hold interest because they help clarify what constitutes a shock or

1 2 3 Wire services such as Reuters and Bloomberg offer a survey of analysts expectations for high-profile USDA reports. These surveys hold interest because they help clarify what constitutes a shock or

April 9, Dear Subscriber:

April 9, 2014 Dear Subscriber: We will be adding material to this shell letter after the report is released on April 9, 2014 at 11:00 a.m CST. Be sure to click back on the link often for the latest information.

April 9, 2014 Dear Subscriber: We will be adding material to this shell letter after the report is released on April 9, 2014 at 11:00 a.m CST. Be sure to click back on the link often for the latest information.

CORN: DECLINING WORLD GRAIN STOCKS OFFERS POTENTIAL FOR HIGHER PRICES

CORN: DECLINING WORLD GRAIN STOCKS OFFERS POTENTIAL FOR HIGHER PRICES OCTOBER 2000 Darrel Good Summary The 2000 U.S. corn crop is now estimated at 10.192 billion bushels, 755 million (8 percent) larger

CORN: DECLINING WORLD GRAIN STOCKS OFFERS POTENTIAL FOR HIGHER PRICES OCTOBER 2000 Darrel Good Summary The 2000 U.S. corn crop is now estimated at 10.192 billion bushels, 755 million (8 percent) larger

Learn more at MarginManager.com May As always, if you have questions, please feel free to contact me.

Learn more at MarginManager.com May 17 This Issue Feature Article Pages -6 Optimize Your Capital... Margin Watch Reports Pages 73 Hog....7 Dairy...8 Beef....9 Corn.... 11 Soybean...1 Wheat...13 Dear Ag

Learn more at MarginManager.com May 17 This Issue Feature Article Pages -6 Optimize Your Capital... Margin Watch Reports Pages 73 Hog....7 Dairy...8 Beef....9 Corn.... 11 Soybean...1 Wheat...13 Dear Ag

Feed Grain Outlook June 2, 2014 Volume 23, Number 33

June 2, Today s Newsletter Market Situation Crop Progress 1 Corn Use 2 Outside Markets 3 Marketing Strategies Corn Marketing Plan 5 Upcoming Reports/Events 6 Market Situation Crop Progress. This afternoon

June 2, Today s Newsletter Market Situation Crop Progress 1 Corn Use 2 Outside Markets 3 Marketing Strategies Corn Marketing Plan 5 Upcoming Reports/Events 6 Market Situation Crop Progress. This afternoon

January 12, USDA World Supply and Demand Estimates

January 12, 2017 - USDA World Supply and Demand Estimates Corn This month s U.S. corn outlook is for lower production, reduced feed and residual use, increased corn used to produce ethanol, and smaller

January 12, 2017 - USDA World Supply and Demand Estimates Corn This month s U.S. corn outlook is for lower production, reduced feed and residual use, increased corn used to produce ethanol, and smaller

Contact: Dante Manocchio Richardson International

The following information was presented at the 2015 Cereals & Oilseeds Workshop on Feb 25, 2015 and should not be copied or reproduced without permission from the author. Contact: Dante Manocchio Richardson

The following information was presented at the 2015 Cereals & Oilseeds Workshop on Feb 25, 2015 and should not be copied or reproduced without permission from the author. Contact: Dante Manocchio Richardson

US Imported Beef Market A Weekly Update

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 47 November 24, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 47 November 24, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com

Decision enabling cash market analysis & price outlook. Report Summary Last closing USD (+16.00) per MT as on October 11, 2013

per MT as on October 11, 2013") Decision enabling cash market analysis & price outlook For the week beginning Oct 15, 213 Argentina Soy Oil 1 Month Forward Fundamental Summary Report Summary Last closing USD 93. (+16.) per MT as on October

Decision enabling cash market analysis & price outlook For the week beginning Oct 15, 213 Argentina Soy Oil 1 Month Forward Fundamental Summary Report Summary Last closing USD 93. (+16.) per MT as on October

Commodity Market Outlook

Commodity Market Outlook Jim Hilker Professor and MSU Extension Economist Department of Agricultural, Food, and Resource Economics Michigan State University Market Outlook Reports For September 6, 2017

Commodity Market Outlook Jim Hilker Professor and MSU Extension Economist Department of Agricultural, Food, and Resource Economics Michigan State University Market Outlook Reports For September 6, 2017

Hog:Corn Ratio What can we learn from the old school?

October 16, 2006 Ames, Iowa Econ. Info. 1944 Hog:Corn Ratio What can we learn from the old school? Economists have studied the hog to corn ratio for over 100 years. This ratio is simply the live hog price

October 16, 2006 Ames, Iowa Econ. Info. 1944 Hog:Corn Ratio What can we learn from the old school? Economists have studied the hog to corn ratio for over 100 years. This ratio is simply the live hog price

Situation and Outlook of the Canadian Livestock Industry

Situation and Outlook of the Canadian Livestock Industry 2011 USDA Agricultural Outlook Forum Tyler Fulton February 25, 2011 tyler@hamsmarketing.ca Lost in Translation Canadian Livestock Industry - Outline

Situation and Outlook of the Canadian Livestock Industry 2011 USDA Agricultural Outlook Forum Tyler Fulton February 25, 2011 tyler@hamsmarketing.ca Lost in Translation Canadian Livestock Industry - Outline

November 18, 1996 Ames, Iowa Econ. Info. 1706

November 18, 1996 Ames, Iowa Econ. Info. 1706 LEAN HOG CARCASS BASIS The new Lean Hog futures contract differs from its predecessor in several ways. It is traded on carcass weight and price rather than

November 18, 1996 Ames, Iowa Econ. Info. 1706 LEAN HOG CARCASS BASIS The new Lean Hog futures contract differs from its predecessor in several ways. It is traded on carcass weight and price rather than

Hog Producers Near the End of Losses

Hog Producers Near the End of Losses January 2003 Chris Hurt Last year was another tough one for many hog producers unless they had contracts that kept the prices they received much above the average spot

Hog Producers Near the End of Losses January 2003 Chris Hurt Last year was another tough one for many hog producers unless they had contracts that kept the prices they received much above the average spot

Grain Market Outlook for

Grain Market Outlook for 2017-2018 KSU Ag Econ 520 Fall 2017 Manhattan, Kansas DANIEL O BRIEN EXTENSION AGRICULTURAL ECONOMIST Topics to be discussed.. 1) Grain Market Analysis & Outlook Corn & Grain Sorghum

Grain Market Outlook for 2017-2018 KSU Ag Econ 520 Fall 2017 Manhattan, Kansas DANIEL O BRIEN EXTENSION AGRICULTURAL ECONOMIST Topics to be discussed.. 1) Grain Market Analysis & Outlook Corn & Grain Sorghum

2017 Crop Market Outlook

2017 Crop Market Outlook Presented at the Row Crop Short Course Jackson County Agriculture Conference Center March 2, 2017 Adam N. Rabinowitz, PhD Assistant Professor and Extension Specialist Agricultural

2017 Crop Market Outlook Presented at the Row Crop Short Course Jackson County Agriculture Conference Center March 2, 2017 Adam N. Rabinowitz, PhD Assistant Professor and Extension Specialist Agricultural

Field Pea and Lentil Marketing Strategies

EC-1295 Field Pea and Lentil Marketing Strategies George Flaskerud Professor and Extension Crops Economist Department of Agribusiness and Applied Economics The United States is a small but growing producer

EC-1295 Field Pea and Lentil Marketing Strategies George Flaskerud Professor and Extension Crops Economist Department of Agribusiness and Applied Economics The United States is a small but growing producer

TOC INDEX. Basis Levels in Cattle Markets. Alberta Agriculture Market Specialists. Introduction. What is Basis? How to Calculate Basis

TOC INDEX Basis Levels in Cattle Markets Feeder Associations of Alberta Ltd. Alberta Agriculture Market Specialists Introduction Basis levels are an effective tool to use for monitoring feeder and fed

TOC INDEX Basis Levels in Cattle Markets Feeder Associations of Alberta Ltd. Alberta Agriculture Market Specialists Introduction Basis levels are an effective tool to use for monitoring feeder and fed

Agri-Service Industry Report

Agri-Service Industry Report December 2016 Dan Hassler 2017 U.S. Industry Outlook A little better or a little worse is the quickest way to sum up the expectations for the agricultural equipment industry

Agri-Service Industry Report December 2016 Dan Hassler 2017 U.S. Industry Outlook A little better or a little worse is the quickest way to sum up the expectations for the agricultural equipment industry

Drought Marketing 9/17/2012

9/17/2012 Drought Marketing Edward Usset, Grain Marketing Specialist University of Minnesota Center for Farm Financial Management email: usset001@umn.edu Center for Farm Financial Management: www.cffm.umn.edu

9/17/2012 Drought Marketing Edward Usset, Grain Marketing Specialist University of Minnesota Center for Farm Financial Management email: usset001@umn.edu Center for Farm Financial Management: www.cffm.umn.edu

THE HIGHTOWER REPORT

Futures Analysis & Forecasting HightowerReport.com Strategies for the March 31st USDA Prospective Plantings Report Large Grain Supply May Not Be Enough! Several years ago, the amount of food consumed inside

Futures Analysis & Forecasting HightowerReport.com Strategies for the March 31st USDA Prospective Plantings Report Large Grain Supply May Not Be Enough! Several years ago, the amount of food consumed inside

Analysis & Comments. Livestock Marketing Information Center State Extension Services in Cooperation with USDA. National Hay Situation and Outlook

Analysis & Comments Livestock Marketing Information Center State Extension Services in Cooperation with USDA April 2, 2015 Letter #12 www.lmic.info National Hay Situation and Outlook The 2014 calendar

Analysis & Comments Livestock Marketing Information Center State Extension Services in Cooperation with USDA April 2, 2015 Letter #12 www.lmic.info National Hay Situation and Outlook The 2014 calendar

Soy Canada SOYBEAN PROCESSING WORKSHOP PRESENTATION NOVEMBER 16, 2017 BRANDON, MANITOBA

Soy Canada SOYBEAN PROCESSING WORKSHOP PRESENTATION NOVEMBER 16, 2017 BRANDON, MANITOBA Overview 1) Soy Canada & Mandate 2) Soybean Sector Update & Trends 3) Growth in Western Canada 4) Commodity Soybean

Soy Canada SOYBEAN PROCESSING WORKSHOP PRESENTATION NOVEMBER 16, 2017 BRANDON, MANITOBA Overview 1) Soy Canada & Mandate 2) Soybean Sector Update & Trends 3) Growth in Western Canada 4) Commodity Soybean

Cattle Market Situation and Outlook

Cattle Market Situation and Outlook Rebuilding the Cow Herd Series March 28, 2007 Falls City, TX Coordinated by: Dennis Hale-Karnes CEA Ag & Charlie Pfluger-Wilson CEA Ag Prepared and presented by: Larry

Cattle Market Situation and Outlook Rebuilding the Cow Herd Series March 28, 2007 Falls City, TX Coordinated by: Dennis Hale-Karnes CEA Ag & Charlie Pfluger-Wilson CEA Ag Prepared and presented by: Larry

Iowa Farm Outlook. February 2018 Ames, Iowa Econ. Info Betting on the Come in the Fed Cattle Market

Iowa Farm Outlook 0BDepartment of Economics February 2018 Ames, Iowa Econ. Info. 2094 Betting on the Come in the Fed Cattle Market Prices feedlot managers are bidding for feeder cattle suggest that feedlot

Iowa Farm Outlook 0BDepartment of Economics February 2018 Ames, Iowa Econ. Info. 2094 Betting on the Come in the Fed Cattle Market Prices feedlot managers are bidding for feeder cattle suggest that feedlot

FNB Agri-Weekly 17 March 2006

An Authorised Financial Services Provider FNB Agri-Weekly Web www.fnb.co.za e-mail:pmakube@fnb.co.za Beef market trends (Graph 1) International: Beef prices continued to drift lower due to improved volumes

An Authorised Financial Services Provider FNB Agri-Weekly Web www.fnb.co.za e-mail:pmakube@fnb.co.za Beef market trends (Graph 1) International: Beef prices continued to drift lower due to improved volumes

United Nations Conference on Trade and Development

United Nations Conference on Trade and Development 1th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 25-26 April 218, Geneva Assessing the recent past and prospects for grains and oilseeds markets

United Nations Conference on Trade and Development 1th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 25-26 April 218, Geneva Assessing the recent past and prospects for grains and oilseeds markets

SOYBEANS: FOCUS ON SOUTH AMERICAN AND U.S. SUPPLY AND CHINESE DEMAND

SOYBEANS: FOCUS ON SOUTH AMERICAN AND U.S. SUPPLY AND CHINESE DEMAND APRIL 2002 Darrel Good 2002-NO.4 Summary Soybean prices during the first half of the 2001-02 marketing year were well below the prices

SOYBEANS: FOCUS ON SOUTH AMERICAN AND U.S. SUPPLY AND CHINESE DEMAND APRIL 2002 Darrel Good 2002-NO.4 Summary Soybean prices during the first half of the 2001-02 marketing year were well below the prices

Iowa Farm Outlook. May 2015 Ames, Iowa Econ. Info Several Factors Supporting, Pressuring Fed Cattle Prices

Iowa Farm Outlook 0BDepartment of Economics May 2015 Ames, Iowa Econ. Info. 2061 Several Factors Supporting, Pressuring Fed Cattle Prices All market classes of beef cattle are at record high levels for

Iowa Farm Outlook 0BDepartment of Economics May 2015 Ames, Iowa Econ. Info. 2061 Several Factors Supporting, Pressuring Fed Cattle Prices All market classes of beef cattle are at record high levels for

Iowa Farm Outlook. December 2015 Ames, Iowa Econ. Info Replacement Quality Heifer Prices Supported by Latest Data

Iowa Farm Outlook 0BDepartment of Economics December 2015 Ames, Iowa Econ. Info. 2068 Replacement Quality Heifer Prices Supported by Latest Data Beef cow herd expansion started briskly in 2014 with a 2.1%

Iowa Farm Outlook 0BDepartment of Economics December 2015 Ames, Iowa Econ. Info. 2068 Replacement Quality Heifer Prices Supported by Latest Data Beef cow herd expansion started briskly in 2014 with a 2.1%

The weather models continue to paint an optimistic picture for the new season. The South African maize belt could

22 September 2017 South African Agricultural Commodities Weekly Wrap The weaker domestic currency, coupled with higher Chicago grains and oilseed prices led to widespread gains in the South African agricultural

22 September 2017 South African Agricultural Commodities Weekly Wrap The weaker domestic currency, coupled with higher Chicago grains and oilseed prices led to widespread gains in the South African agricultural

Iowa Farm Outlook. Big Supply, Strong Dollar Pressure Hog Prices. January 2016 Ames, Iowa Econ. Info. 2069

Iowa Farm Outlook 0BDepartment of Economics January 2016 Ames, Iowa Econ. Info. 2069 Big Supply, Strong Dollar Pressure Hog Prices After holding between $60 and $75 per cwt for much of the fall, nearby

Iowa Farm Outlook 0BDepartment of Economics January 2016 Ames, Iowa Econ. Info. 2069 Big Supply, Strong Dollar Pressure Hog Prices After holding between $60 and $75 per cwt for much of the fall, nearby

Commodity Outlook: September 2017 West Central Illinois: July 2017

Commodity Outlook: September 2017 West Central Illinois: July 2017 William George Senior Agriculture Economist U.S. Department of Agriculture Foreign Agriculture Service Office of Global Analysis Commodity

Commodity Outlook: September 2017 West Central Illinois: July 2017 William George Senior Agriculture Economist U.S. Department of Agriculture Foreign Agriculture Service Office of Global Analysis Commodity

World Agricultural Outlook Board Interagency Commodity Estimates Committee Forecasts. Lockup Briefing April 9, 2014

World Agricultural Outlook Board Interagency Commodity Estimates Committee Forecasts Lockup Briefing World Wheat Production Country or Region Million Tons World 656.5 712.5 8.5 United States 61.7 58.0-6.0

World Agricultural Outlook Board Interagency Commodity Estimates Committee Forecasts Lockup Briefing World Wheat Production Country or Region Million Tons World 656.5 712.5 8.5 United States 61.7 58.0-6.0

US Imported Beef Market A Weekly Update

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 33 August 16, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com 800-526-4612

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 33 August 16, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com 800-526-4612

or

Cutting edge research, state of the art reports, conference calls, seminars and trading have made American Restaurant Association Inc. the premier food commodity economics company since 1996. 941-379-2228

Cutting edge research, state of the art reports, conference calls, seminars and trading have made American Restaurant Association Inc. the premier food commodity economics company since 1996. 941-379-2228

Despite Slowing Herd Expansion-- Can Domestic, Export Beef Demand Keep Pace?

Despite Slowing Herd Expansion-- Can Domestic, Export Beef Demand Keep Pace? Presented by Mike Sands MBS Research Forecasting Agricultural and Biofuels Interplay The Jacobsen--Chicago May 23, 2018 1 Livestock

Despite Slowing Herd Expansion-- Can Domestic, Export Beef Demand Keep Pace? Presented by Mike Sands MBS Research Forecasting Agricultural and Biofuels Interplay The Jacobsen--Chicago May 23, 2018 1 Livestock

Wheat Year in Review (International): Low 2007/08 Stocks and Higher Prices Drive Outlook

: Low 2007/08 Stocks and Higher Prices Drive Outlook") United States Department of Agriculture WHS-2008-01 May 2008 A Report from the Economic Research Service Wheat Year in Review (International): Low 2007/08 Stocks and Higher Prices Drive Outlook www.ers.usda.gov

United States Department of Agriculture WHS-2008-01 May 2008 A Report from the Economic Research Service Wheat Year in Review (International): Low 2007/08 Stocks and Higher Prices Drive Outlook www.ers.usda.gov

In its final estimates for the 2017 summer crop production season, the Crop Estimates Committee (CEC) lifted maize

lifted maize") 29 September 2017 South African Agricultural Commodities Weekly Wrap This was a data-packed week for grain and oilseed markets with releases that include production estimates update, producer deliveries

29 September 2017 South African Agricultural Commodities Weekly Wrap This was a data-packed week for grain and oilseed markets with releases that include production estimates update, producer deliveries

Iowa Farm Outlook. December 2017 Ames, Iowa Econ. Info Stretch Run for Meat Markets

Iowa Farm Outlook 0BDepartment of Economics December 2017 Ames, Iowa Econ. Info. 2092 Stretch Run for Meat Markets The holiday season is an important test for meat sales and demand. Retailers and foodservice

Iowa Farm Outlook 0BDepartment of Economics December 2017 Ames, Iowa Econ. Info. 2092 Stretch Run for Meat Markets The holiday season is an important test for meat sales and demand. Retailers and foodservice

Agri-Service Industry Report

Years Since Presidential Election 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 Billions Agri-Service Industry Report November 2016 Dan Hassler Farm Income and Presidential Elections

Years Since Presidential Election 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 Billions Agri-Service Industry Report November 2016 Dan Hassler Farm Income and Presidential Elections

Agriculture Commodity Markets & Trends

Agriculture Commodity Markets & Trends Agenda Short History of Agriculture Commodities US & World Supply and Demand Commodity Prices Continuous Charts What is Contango and Backwardation Barge, Truck and

Agriculture Commodity Markets & Trends Agenda Short History of Agriculture Commodities US & World Supply and Demand Commodity Prices Continuous Charts What is Contango and Backwardation Barge, Truck and

Economic Research Service Situation and Outlook Report

Economic Research Service Situation and Outlook Report WHS-18d April 12, 2018 Next release is May 14, 2018 Wheat Outlook Jennifer K. Bond, coordinator Olga Liefert In this report: - Domestic Outlook -

Economic Research Service Situation and Outlook Report WHS-18d April 12, 2018 Next release is May 14, 2018 Wheat Outlook Jennifer K. Bond, coordinator Olga Liefert In this report: - Domestic Outlook -

2018 ETHANOL MARKET OUTLOOK

Moe Agostino (Chief Commodity Strategist) & Abhinesh Gopal (Commodity Research Analyst), supported by the Commodity Research Team February 16 th, 2018 Highlights 2018 ETHANOL MARKET OUTLOOK Ethanol demand

Moe Agostino (Chief Commodity Strategist) & Abhinesh Gopal (Commodity Research Analyst), supported by the Commodity Research Team February 16 th, 2018 Highlights 2018 ETHANOL MARKET OUTLOOK Ethanol demand

Iowa Farm Outlook. February 2016 Ames, Iowa Econ. Info Cattle Inventory Report Affirms What Happened in 2015 and What May Happen in 2016

Iowa Farm Outlook 0BDepartment of Economics February 2016 Ames, Iowa Econ. Info. 2070 Cattle Inventory Report Affirms What Happened in 2015 and What May Happen in 2016 Curious about how fast the beef cow

Iowa Farm Outlook 0BDepartment of Economics February 2016 Ames, Iowa Econ. Info. 2070 Cattle Inventory Report Affirms What Happened in 2015 and What May Happen in 2016 Curious about how fast the beef cow

Tennessee Market Highlights

Tennessee Market Highlights September 29, 2017 Number: 39 Trends for the Week Compared to a Week Ago Slaughter Cows $4 to $6 lower Slaughter Bulls $5 to $6 lower Feeder Steers $2 to $7 lower Feeder Heifers

Tennessee Market Highlights September 29, 2017 Number: 39 Trends for the Week Compared to a Week Ago Slaughter Cows $4 to $6 lower Slaughter Bulls $5 to $6 lower Feeder Steers $2 to $7 lower Feeder Heifers

U.S. Agriculture: Commodity Situation and Outlook

U.S. Agriculture: Commodity Situation and Outlook H. Scott Stiles Instructor - Economics University of Arkansas Division of Agriculture Farm Policy Education 2013 U.S. Crop Outlook Overview: Preliminary

U.S. Agriculture: Commodity Situation and Outlook H. Scott Stiles Instructor - Economics University of Arkansas Division of Agriculture Farm Policy Education 2013 U.S. Crop Outlook Overview: Preliminary

US Imported Beef Market A Weekly Update

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 44 November 3, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com 800-526-4612

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 44 November 3, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com 800-526-4612

3/25/2017. What to do today? Cattle & Beef Markets: Commodity Outlook

3/25/27 Cattle & Beef Markets: Commodity Outlook Stephen R. Koontz Professor & extension economist Department of Agricultural & Resource Economics Colorado State University Stephen.Koontz@ColoState.Edu

3/25/27 Cattle & Beef Markets: Commodity Outlook Stephen R. Koontz Professor & extension economist Department of Agricultural & Resource Economics Colorado State University Stephen.Koontz@ColoState.Edu

Iowa Farm Outlook. February 2015 Ames, Iowa Econ. Info Takeaways from the January Cattle Inventory Report

Iowa Farm Outlook 0BDepartment of Economics February 2015 Ames, Iowa Econ. Info. 2058 Takeaways from the January Cattle Inventory Report USDA has released the much anticipated inventory of the U.S. cattle

Iowa Farm Outlook 0BDepartment of Economics February 2015 Ames, Iowa Econ. Info. 2058 Takeaways from the January Cattle Inventory Report USDA has released the much anticipated inventory of the U.S. cattle

PRX Grain Market Overview

PRX The ProExporter Network Grain, Oilseed & Biofuel Fundamentals Updated 4/1/18 PRX Grain Market Overview US Major Grains Crop Years 217/18 & 218/19 with USDA Apr 1, 218 WASDE PRX_Overview, SDU, Apr-1-18

PRX The ProExporter Network Grain, Oilseed & Biofuel Fundamentals Updated 4/1/18 PRX Grain Market Overview US Major Grains Crop Years 217/18 & 218/19 with USDA Apr 1, 218 WASDE PRX_Overview, SDU, Apr-1-18

Ukraine Winter Wheat: Sowing Progress (All years include estimated area for Crimea.)

") Sept 7 Sept 14 Sept 21 Sept 28 Oct 5 Oct 12 Oct 19 Oct 26 Nov 2 Nov 9 Nov 16 Million hectares 1,000 hectares 8,000 7,000 6,000 Ukraine Winter Wheat: Sowing Progress (All years include estimated area for

Sept 7 Sept 14 Sept 21 Sept 28 Oct 5 Oct 12 Oct 19 Oct 26 Nov 2 Nov 9 Nov 16 Million hectares 1,000 hectares 8,000 7,000 6,000 Ukraine Winter Wheat: Sowing Progress (All years include estimated area for

Livestock and Feedgrain Outlook

Livestock and Feedgrain Outlook 2017 Range Beef Cow Symposium James G. Robb Director, LMIC Website: www.lmic.info November 28-30, 2017 28 US Land Grant Universities: USDA Data Sources -- NASS, AMS, FAS,

Livestock and Feedgrain Outlook 2017 Range Beef Cow Symposium James G. Robb Director, LMIC Website: www.lmic.info November 28-30, 2017 28 US Land Grant Universities: USDA Data Sources -- NASS, AMS, FAS,

February 10, Tickets are 30 dollars and include a continential breakfast, Beef House lunch, and 25th anniversery hat.

February 10, 2014 WE WILL BE UPDATING AND ADDING MATERIAL THROUGHOUT THE DAY ON FEBRUARY 10 TO THIS LETTER BEGINNING AT 11:00 AM CST. PLEASE CHECK BACK OFTEN FOR THE LATEST INFORMATION! Tickets for the

February 10, 2014 WE WILL BE UPDATING AND ADDING MATERIAL THROUGHOUT THE DAY ON FEBRUARY 10 TO THIS LETTER BEGINNING AT 11:00 AM CST. PLEASE CHECK BACK OFTEN FOR THE LATEST INFORMATION! Tickets for the

World Sorghum Grain Producers

World Sorghum Grain Producers Million Metric Tons 18 16 14 12 12 10 8 6 7 7 6 6 4 4 4 3 2 2 2 2 0 14 MY 2014/15 MY 2015/16 MY 2016/17 Grain Sorghum Exporters Million Metric Tons 10 9 8 7 6 5 4 3 2 1 0

World Sorghum Grain Producers Million Metric Tons 18 16 14 12 12 10 8 6 7 7 6 6 4 4 4 3 2 2 2 2 0 14 MY 2014/15 MY 2015/16 MY 2016/17 Grain Sorghum Exporters Million Metric Tons 10 9 8 7 6 5 4 3 2 1 0

World Agricultural Outlook Board Interagency Commodity Estimates Committee Forecasts. Lockup Briefing July 11, 2014

World Agricultural Outlook Board Interagency Commodity Estimates Committee Forecasts Lockup Briefing World Wheat Production Country or Region estimate 2014/15 forecast June 11 Million Tons Percent Percent

World Agricultural Outlook Board Interagency Commodity Estimates Committee Forecasts Lockup Briefing World Wheat Production Country or Region estimate 2014/15 forecast June 11 Million Tons Percent Percent

Ammonia costs spike sharply higher Nitrogen prices disrupt calm in fertilizer market By Bryce Knorr, grain market analyst

Ammonia costs spike sharply higher Nitrogen prices disrupt calm in fertilizer market By Bryce Knorr, grain market analyst Ammonia joined other forms of nitrogen in the parade of higher costs, with contracts

Ammonia costs spike sharply higher Nitrogen prices disrupt calm in fertilizer market By Bryce Knorr, grain market analyst Ammonia joined other forms of nitrogen in the parade of higher costs, with contracts

Fundamental Analysis for Grain

Fundamental Analysis for Grain By Dr. Robert Wisner University Professor Emeritus Iowa State University Texas A & M University Master Marketers Conference, Amarillo, Texas, January 13, 2010 The process

Fundamental Analysis for Grain By Dr. Robert Wisner University Professor Emeritus Iowa State University Texas A & M University Master Marketers Conference, Amarillo, Texas, January 13, 2010 The process

World Wheat Supply and Demand. Crop Quality Seminars 2013 Ian Flagg

World Wheat Supply and Demand Crop Quality Seminars 2013 Ian Flagg Beginning Stocks 250 200 Exporter beginning stocks down 35% from 5-year average 199 199 174 150 125 100 83 122 50 0 27 14 14 32 48 38

World Wheat Supply and Demand Crop Quality Seminars 2013 Ian Flagg Beginning Stocks 250 200 Exporter beginning stocks down 35% from 5-year average 199 199 174 150 125 100 83 122 50 0 27 14 14 32 48 38

Soybean Supply and Demand Forecast

Soybean Supply and Demand Forecast U.S. soybean planted acreage is expected to increase 5.7 million acres over the forecast period. U.S. soybean yields are expected to increase 2.2 bushels per acre or

Soybean Supply and Demand Forecast U.S. soybean planted acreage is expected to increase 5.7 million acres over the forecast period. U.S. soybean yields are expected to increase 2.2 bushels per acre or

Global Agricultural Supply and Demand: Factors contributing to recent increases in food commodity prices

Global Agricultural Supply and Demand: Factors contributing to recent increases in food commodity prices Ron Trostle Economic Research Service U.S. Department of Agriculture Agricultural Markets and Food

Global Agricultural Supply and Demand: Factors contributing to recent increases in food commodity prices Ron Trostle Economic Research Service U.S. Department of Agriculture Agricultural Markets and Food

Cattle Market Outlook

Cattle Market Outlook Winter C. Wilson Gray District Economist Twin Falls R & E Center wgray@uidaho.edu http://web.cals.uidaho.edu/idahoagbiz/ Thank You! Topics: Markets and Aspects of Domestic Consumer

Cattle Market Outlook Winter C. Wilson Gray District Economist Twin Falls R & E Center wgray@uidaho.edu http://web.cals.uidaho.edu/idahoagbiz/ Thank You! Topics: Markets and Aspects of Domestic Consumer

Dairy Outlook. June By Jim Dunn Professor of Agricultural Economics, Penn State University. Market Psychology

Dairy Outlook June 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology Cheese prices have been rising this past month, rising 16 cents/lb. in a fairly steady climb.

Dairy Outlook June 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology Cheese prices have been rising this past month, rising 16 cents/lb. in a fairly steady climb.

South Africa s maize crop is generally in good condition across the country. The areas that started the season on a

20 April 2018 South African Agricultural Commodities Weekly Wrap The weather remains a key focus in the local agricultural market but could have a different impact on crops than the past couple of weeks.

20 April 2018 South African Agricultural Commodities Weekly Wrap The weather remains a key focus in the local agricultural market but could have a different impact on crops than the past couple of weeks.

2017 Tennessee Agricultural Outlook. Aaron Smith Crop Economist University of Tennessee Extension

2017 Tennessee Agricultural Outlook Aaron Smith Crop Economist University of Tennessee Extension Overview Review of the Tennessee Agricultural Economy Crops Livestock 2017 Estimated Net Returns Principle

2017 Tennessee Agricultural Outlook Aaron Smith Crop Economist University of Tennessee Extension Overview Review of the Tennessee Agricultural Economy Crops Livestock 2017 Estimated Net Returns Principle

Veal Price Forecast. October 2015

Veal Price Forecast October 2015 VEAL PRICE FORECAST OCTOBER 2015 Veal Light Production Veal prices in 2015 have been stronger than anticipated and are expected to continue to show year-over-year increases

Veal Price Forecast October 2015 VEAL PRICE FORECAST OCTOBER 2015 Veal Light Production Veal prices in 2015 have been stronger than anticipated and are expected to continue to show year-over-year increases

Beef Outlook Webinar July 27, 2009

2009-10 Beef Outlook Webinar July 27, 2009 David Maloni Principal American Restaurant Association Inc. 888-423-4411 www.americanrestaurantassociation.com David.Maloni@AmericanRestaurantAssociation.com

2009-10 Beef Outlook Webinar July 27, 2009 David Maloni Principal American Restaurant Association Inc. 888-423-4411 www.americanrestaurantassociation.com David.Maloni@AmericanRestaurantAssociation.com

Week Ending August 11, 2017

Week Ending August 11, 2017 **Graphs represent data for the week ending August 4, 2017** DIESEL Diesel Fuel $/Gallon 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 BEEF Market

Week Ending August 11, 2017 **Graphs represent data for the week ending August 4, 2017** DIESEL Diesel Fuel $/Gallon 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 BEEF Market

Jason Henderson Vice President and Branch Executive Federal Reserve Bank of Kansas City Omaha Branch April 25, 2012

Jason Henderson Vice President and Branch Executive April 25, 2012 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or

Jason Henderson Vice President and Branch Executive April 25, 2012 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Brazil Post: Brasilia

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Brazil Post: Brasilia

Wheat Pricing Guide. David Kenyon and Katie Lucas

Wheat Pricing Guide David Kenyon and Katie Lucas 5.00 4.50 Dollars per bushel 4.00 3.50 3.00 2.50 2.00 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 Year David Kenyon is Professor and Katie Lucas

Wheat Pricing Guide David Kenyon and Katie Lucas 5.00 4.50 Dollars per bushel 4.00 3.50 3.00 2.50 2.00 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 Year David Kenyon is Professor and Katie Lucas

OUTLOOK FOR US AGRICULTURE

Agricultural Outlook Forum 216 OUTLOOK FOR US AGRICULTURE Robert Johansson Chief Economist 25 February 216 Fig 2 Main themes for 216 1. The macroeconomy is weighing on trade, but there are reasons for

Agricultural Outlook Forum 216 OUTLOOK FOR US AGRICULTURE Robert Johansson Chief Economist 25 February 216 Fig 2 Main themes for 216 1. The macroeconomy is weighing on trade, but there are reasons for

Clearing the Clutter:

Clearing the Clutter: Getting rid of market noise and focusing on your bottom-line ANGIE SETZER VICE PRESIDENT OF GRAIN CITIZENS LLC CHARLOTTE, MI My market watching face. .unless soybeans are having a

Clearing the Clutter: Getting rid of market noise and focusing on your bottom-line ANGIE SETZER VICE PRESIDENT OF GRAIN CITIZENS LLC CHARLOTTE, MI My market watching face. .unless soybeans are having a

FRIEDBERG S F O C U S O N F U T U R E S. Wheat: crop problems galore. Inside

FRIEDBERG S F O C U S O N F U T U R E S Friedberg Mercantile Group Ltd. Volume 18, No. 10 November 19, 2015 Wheat: crop problems galore Northern Hemisphere winter wheat crops for the upcoming 2016-17 marketing

FRIEDBERG S F O C U S O N F U T U R E S Friedberg Mercantile Group Ltd. Volume 18, No. 10 November 19, 2015 Wheat: crop problems galore Northern Hemisphere winter wheat crops for the upcoming 2016-17 marketing

HOG PRODUCERS SHOW LITTLE SIGN OF RETREAT

HOG PRODUCERS SHOW LITTLE SIGN OF RETREAT APRIL 2007 Chris Hurt 2007 NO. 2 Hog producers reported in the latest USDA update that they increased the size of the breeding herd by 1 percent. This means pork

HOG PRODUCERS SHOW LITTLE SIGN OF RETREAT APRIL 2007 Chris Hurt 2007 NO. 2 Hog producers reported in the latest USDA update that they increased the size of the breeding herd by 1 percent. This means pork

Tennessee Market Highlights

Tennessee Market Highlights September 22, 2017 Number: 38 Trends for the Week Compared to a Week Ago Slaughter Cows $2 to $3 lower Slaughter Bulls $4 to $7 lower Feeder Steers less than 600 lbs. $3 to

Tennessee Market Highlights September 22, 2017 Number: 38 Trends for the Week Compared to a Week Ago Slaughter Cows $2 to $3 lower Slaughter Bulls $4 to $7 lower Feeder Steers less than 600 lbs. $3 to

MONTHLY MARKET PROFILE: 12/10/04 Nevil C. Speer, PhD, Western Kentucky University

MONTHLY MARKET PROFILE: 12/10/04 Nevil C. Speer, PhD, Western Kentucky University The market seems like a heavyweight match with packers and feeders standing toe-to-toe slugging it out. Negotiations are

MONTHLY MARKET PROFILE: 12/10/04 Nevil C. Speer, PhD, Western Kentucky University The market seems like a heavyweight match with packers and feeders standing toe-to-toe slugging it out. Negotiations are

Weekly Mature U.S. Beef Cow Slaughter

Louisiana Cattle Market Update Friday, July 9 th, 2010 Ross Pruitt, Department of Agricultural Economics and Agribusiness Louisiana State University AgCenter In two weeks, USDA NASS will release the July

Louisiana Cattle Market Update Friday, July 9 th, 2010 Ross Pruitt, Department of Agricultural Economics and Agribusiness Louisiana State University AgCenter In two weeks, USDA NASS will release the July

Beef Cattle Outlook Dr. Curt Lacy Extension Economist-Livestock

Beef Cattle Outlook Dr. Curt Lacy Extension Economist-Livestock Current Situation $ Per Cwt. 190 180 170 160 150 140 130 120 110 100 90 MED. & LRG. #1 & 2 STEER CALF PRICES 500-600 Pounds, Georgia, Weekly

Beef Cattle Outlook Dr. Curt Lacy Extension Economist-Livestock Current Situation $ Per Cwt. 190 180 170 160 150 140 130 120 110 100 90 MED. & LRG. #1 & 2 STEER CALF PRICES 500-600 Pounds, Georgia, Weekly

ICF Propane Inventory Update and Winter 2014/15 Supply Assessment

ICF Propane Inventory Update and Winter 2014/15 Supply Assessment October 30, 2014 Michael Sloan Principal ICF International 703-218-2753 Michael.Sloan@icfi.com Andrew Duval Research Assistant ICF International

ICF Propane Inventory Update and Winter 2014/15 Supply Assessment October 30, 2014 Michael Sloan Principal ICF International 703-218-2753 Michael.Sloan@icfi.com Andrew Duval Research Assistant ICF International

Louisiana Cattle Market Update FRIDAY, MARCH 30 TH, Ground Beef Prices

Louisiana Cattle Market Update FRIDAY, MARCH 30 TH, 2012 Ross Pruitt, Department of Agricultural Economics and Agribusiness LSU AgCenter Ground Beef Prices The full impact on demand of recent news stories

Louisiana Cattle Market Update FRIDAY, MARCH 30 TH, 2012 Ross Pruitt, Department of Agricultural Economics and Agribusiness LSU AgCenter Ground Beef Prices The full impact on demand of recent news stories

The Agricultural Risk Consulting Group 4546 South 86th St Suite D Lincoln NE Toll Free

Global View June 5 2009 It has been an interesting spring in the markets. Spot crude market has gone from just over $30 in January to $69 this week. The DJIA hit a low around 6,500 before rebounding back

Global View June 5 2009 It has been an interesting spring in the markets. Spot crude market has gone from just over $30 in January to $69 this week. The DJIA hit a low around 6,500 before rebounding back

Who Will Own the Grain? Elevators Eye Improved Prospects

November Who Will Own the Grain? Elevators Eye Improved Prospects Key Points: n Opportunities from significant futures market carry, weak harvest basis, and low transportation rates point to improved margins

November Who Will Own the Grain? Elevators Eye Improved Prospects Key Points: n Opportunities from significant futures market carry, weak harvest basis, and low transportation rates point to improved margins

Iowa Farm Outlook. Livestock Price and Profitability Outlook

Iowa Farm Outlook Department of Economics November, 2010 Ames, Iowa Econ. Info. 2007 Livestock Price and Profitability Outlook The holiday season is fast coming, marking the end of a year of variable livestock

Iowa Farm Outlook Department of Economics November, 2010 Ames, Iowa Econ. Info. 2007 Livestock Price and Profitability Outlook The holiday season is fast coming, marking the end of a year of variable livestock

Wheat Outlook. U.S. 2017/18 all-wheat area planted projected to be smallest on record. Figure 1: U.S. wheat planted area by class

Economic Research Service Situation and Outlook WHS-17d April 13, 2017 Wheat Chart Gallery will be updated on April 13, 2017. The next release is May 12, 2017. -------------- Approved by the World Agricultural

Economic Research Service Situation and Outlook WHS-17d April 13, 2017 Wheat Chart Gallery will be updated on April 13, 2017. The next release is May 12, 2017. -------------- Approved by the World Agricultural

Potential Forecasted Economic Impact of Commercializing Agrisure Duracade 5307 in U.S. Corn Prior to Chinese Import Approval

Potential Forecasted Economic Impact of Commercializing Agrisure Duracade 5307 in U.S. Corn Prior to Chinese Import Approval Author: Max Fisher, Director of Economics and Government Relations National

Potential Forecasted Economic Impact of Commercializing Agrisure Duracade 5307 in U.S. Corn Prior to Chinese Import Approval Author: Max Fisher, Director of Economics and Government Relations National

Iowa Farm Outlook. More Beef Expansion Ahead. March 2018 Ames, Iowa Econ. Info. 2095

Iowa Farm Outlook 0BDepartment of Economics March 2018 Ames, Iowa Econ. Info. 2095 More Beef Expansion Ahead The numbers in USDA s recently released annual Cattle inventory report confirm that beef herd

Iowa Farm Outlook 0BDepartment of Economics March 2018 Ames, Iowa Econ. Info. 2095 More Beef Expansion Ahead The numbers in USDA s recently released annual Cattle inventory report confirm that beef herd

What tools can we use to help us decide when to enter and when to exit a hedge? (Or, or for that matter, when to enter and exit any trade.

Motivation for Fundamental and Technical Analysis What tools can we use to help us decide when to enter and when to exit a hedge? (Or, or for that matter, when to enter and exit any trade.) So, how do

Motivation for Fundamental and Technical Analysis What tools can we use to help us decide when to enter and when to exit a hedge? (Or, or for that matter, when to enter and exit any trade.) So, how do

Agriculture: farm income recovers

Agriculture: farm income recovers Farm earnings rose substantially last year, breaking a four-year slide. The index of prices received by farmers averaged a record 209 (1967=100). That was 14 percent over

Agriculture: farm income recovers Farm earnings rose substantially last year, breaking a four-year slide. The index of prices received by farmers averaged a record 209 (1967=100). That was 14 percent over