Outline Economy Agriculture Inputs Weather Grains & Forage Corn Oilseeds Wheat Hay Management Strategies

|

|

|

- Shanon Hines

- 5 years ago

- Views:

Transcription

1 Navigating Market Risks in Volatile Times: Economic & Commodity Outlook Stephen R. Koontz Associate professor & extension economist Department of Agricultural & Resource Economics Colorado State University Greeley, CO January 24, 2012 Outline Economy Agriculture Inputs Weather Grains & Forage Corn Oilseeds Wheat Hay Management Strategies Resources Budgets Futures, Options, & Forward Contracts Crop Insurance Colorado, Kansas, & Nebraska extension Livestock Gross Margin Insurance Colorado, Kansas, & Nebraska extension Economic Outlook Summary Long slow economic recovery. Real estate problems Lending issues Deleveraging & Deflation Employment Chronic but improving unemployment Consumers Surprisingly strong 4 th quarter spending but what does the 1 st quarter bring? 1

2 Economic Outlook Summary (cont) Weekly S&P 500 Index Contract Business Record profitability & rapid improvement from recession low. But a wait and see attitude on any expansion. Government Lots of talk about austerity Net exports Risk, Capital, etc Daily Crude Oil Futures Contract Price 2

3 3

4 4

5 5

6 Weekly Baltic Dry Index 6

7 So What Does All This Mean? The vanilla forecast is things will get better because they are getting better. But there are still big undigested problems: Employment Real estate Government debt I am not willing to bet on the best guess. Input Market Outlook Summary Uncertainty & risk. Significantly higher fuel costs Fertilizer will follow higher. Chemical inputs will likely also. Seed availability or lack of. Supply industries operating under capacity & unwilling to take risk. Credit risk & broker risk Inflation unique to food & energy sectors. Weekly Crude Oil Contract Weekly Natural Gas Contract 7

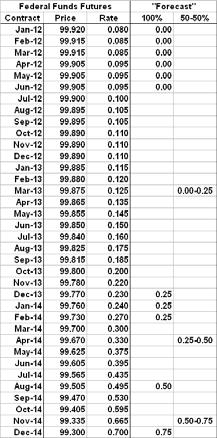

8 14-18% higher than previous year. 2-4% lower than previous year. 5-10% higher than previous year. Moderately higher than previous year. 8

9 Commodity Market Outlook Summary 6-8% higher than previous year. How long is this going to last? Corn Needs two enormous crops. Oilseeds Depends on acres, exports & South American weather. Wheat Only supported by corn & weather. Hay Impacted by drought and corn. Economy??? 9

10 10

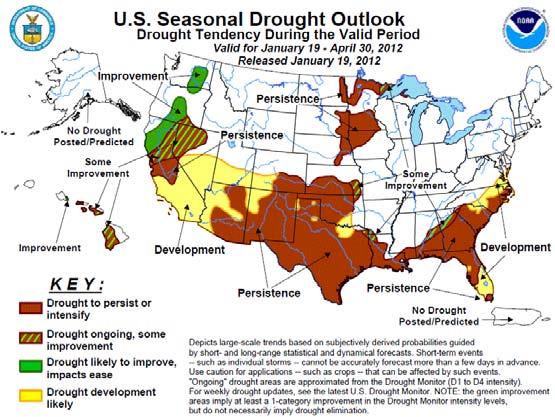

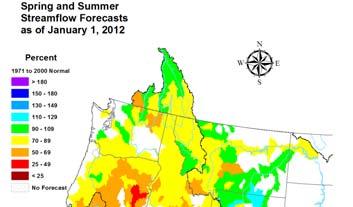

11 La Nina Not as strong as winter returning to normal summer

12 News: Dry & Not-Dry 12

13 The trading range for corn is $3.00-$4.50/bu. Except Weekly Corn Contract Corn Outlook World production of coarse grains level and consumption grows. Stocks are tight. Potential for much volatility until there are not one but two enormous crops. U.S. ethanol production is hitting blend wall. Tax credit elimination will not much impact corn price. U.S. needs to plant million acres in $5.00 $6.00/bu corn. But a forecasting challenge. $4.00/bu is as low as it could go 13

14 14

15 DEC 2012 Corn Contract DEC 2012 $5.56¼/bu. Market looking for a bottom. DEC 2013 corn mirrors DEC But, a 6 premium on

16 Weekly Soybeans Contract Oilseeds Outlook Economic issues that parallel corn and support world economy points. World production and consumption of oilseeds continues to grow at a strong rate. Weather problems in South America. Chinese demand grows. Will soybeans keep acres? (12.07/5.56 = 2.17) Oilseed market currently too low. 16

17 NOV 2012 Soybean Contract NOV 2012 $12.07½/bu. Looking for a bottom. NOV 2013 mirrors NOV However, is a 25 premium on

18 Weekly Wheat Contract Weekly KC Wheat Contract Wheat Outlook In 2007/08 the world and US stocks were at record lows. Thus, record high prices. World stocks have been rebuilt. U.S. stocks are substantial. No world weather problems. U.S. dollar is weak so exports have the potential to be good. KC wheat futures prices separated from U.S. cash wheat prices. That can change. 18

19 19

20 20

21 JUL 2012 KC Wheat Contract JUL $6.92¼/bu. And that is a 44 discount to JUL JUL 2012 Wheat Contract JUL $6.54¼/bu. And that is a 72 discount to JUL

22 Hay Outlook Excellent hay crop in northern U.S. Strong demand due to major drought in the southern U.S. Improving demand from dairy. Weak demand from beef. Interesting outlook for Colorado. 22

23 Mil. Tons U S ALL HAY SUPPLY & DISAPPEARANCE Crop Year Hay Supply Disap. Mil. Tons U S ALL HAY STOCKS May 1 (Beginning of Crop Year) Livestock Marketing Information Center G-NP-20 01/12/12 Livestock Marketing Information Center G-NP-21 01/12/12 Data Source: USDA-NASS, Compiled & Forecasts by LMIC Data Source: USDA-NASS, Compiled & Forecasts by LMIC U S ALL HAY STOCKS December DECEMBER 1 HAY STOCKS (1000 Tons) Mil. Tons Livestock Marketing Information Center G-NP-22 01/12/ to to to to 8401 VT 215 NH 49 MA 71 RI 8 CT 55 NJ 81 DE 13 MD 360 Data Source: USDA-NASS, Compiled & Forecasts by LMIC Livestock Marketing Information Center Data Source: USDA-NASS 1/17/

24 PERCENT CHANGE DECEMBER 1 HAY STOCKS ( ) 2011 ALL HAY ACRES (1000 Acres) -9% 780 5% 1% -11% -11% -13% -24% 35% -10% -32% 11% 14% 7% -9% -60% -13% -38% 3% VT 19% -19% 3% NH 23% -25% MA 13% -10% 0% RI 0% CT 22% -1% NJ -26% -25% 8% 21% DE -32% -16% 51% MD 16% -13% 4% 2% -24% -18% 26% -41% 15% -23% 11% -100% to -25% -25% to 0% 0% to 25% 25% to 100% VT 175 NH 53 MA 74 RI 9 CT 60 NJ 105 DE 15 MD to to to to to 3751 U.S. hay stocks down 11%. -16% 260 Livestock Marketing Information Center Data Source: USDA-NASS 1/17/2012 Livestock Marketing Information Center Data Source: USDA-NASS 1/17/2012 PERCENT CHANGE ALL HAY ACRES ( ) -7% -5% -1% -8% -6% -4% -6% 9% 1% -11% -10% U.S. hay acres down 7%. -3% -1% -8% -29% -6% -22% -4% -4% -3% 0% -5% -3% 1% -10% 0% 3% 3% -2% -9% -4% -10% -5% -4% 3% -17% -9% 3% -19% -4% -100% to -9% -9% to -5% -5% to -3% -3% to 2% 2% to 14% VT -10% NH -5% MA -4% RI 13% CT 2% NJ 0% DE 0% MD 2% Livestock Marketing Information Center Data Source: USDA-NASS 1/17/

25 Colorado Agricultural Outlook $8.5 billion forecasted livestock & crop revenue for 2011 & Record high & about 25% increase from Feed grain & forage producers benefit the most. Beef & dairy challenged but have seen strong demand & improved prices. But no water issues Outlook Summary Corn strong need a huge crop priced correct. Oilseeds strong most uncertainty too low. Wheat weak demand from feeding too high. Hay strong drought needs wait and see. Agriculture inflation strong but variable balance sheets. Economy strengthening and stronger world. When does hiring return to the U.S. economy? Deleveraging, deflation, & sluggish growth. Contact and Link Information Stephen.Koontz@ColoState.Edu 25