|

|

|

- Johnathan Brown

- 5 years ago

- Views:

Transcription

1

2 More Things To Keep You Up at Night Will Low Prices/Low Returns allow the investment in agriculture to continue? (Consolidation) Black Sea Competition Brazil/Argentina Issues The China Syndrome GMO/Sustainability/Traceability Strongest El Nino in 50 to 100 years Presentation title 00/00/00002

3 Wake Up Call!

4 High Prices = Big Margins Every level spent too much Low Prices = Narrow Margins Life is Changing Presentation title 00/00/00004

5 The Next Trend Change? U.S. farm equipment sales -50%+ Excess export capacity Cheap rail & ocean freight Mergers/Consolidations CWB/Cofco/Glencore Layoffs (Monsanto) UPDATE 1-Monsanto slashing 2,600 jobs, buying back shares as sales fall Carey Gillam Wednesday, 7 Oct :57 AM ET Reuters

6

7 French farmers stage 1,000-strong tractor protest in Paris (AP, Sep 3)

8 Brazil Farm Client Comment NO MONEY, NO CREDIT, NO RAIN! Presentation title 00/00/00008

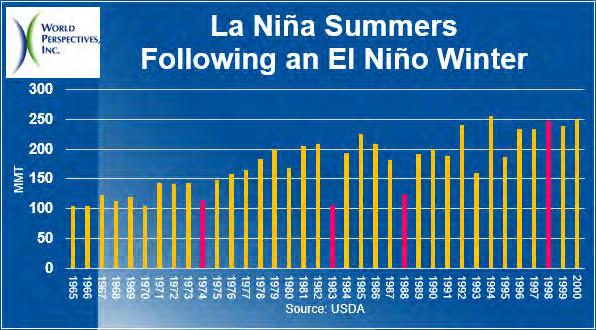

9 The Next Trend Change? Net farm returns now negative around the world Corn shows greatest losses Corn most expensive crop to produce Should see shift away from corn Marginal acres go out of production Double cropped acres decline World balance sheets eventually tighten even with good weather

10 Black Sea Competition Improved crop production practices Improved interior and port infrastructure Prices dependent on governmental decisions Currency valuations Export taxes Production heavily dependent on weather No sanctity of contracts

11 Russia/Ukraine Wheat Production 70,000 60,000 Source:USDA 50,000 40,000 30,000 20,000 10,000 0 Wheat Wheat

12 Russia/Ukraine Wheat Exports Source:USDA Wheat Wheat

13 Russia/Ukraine Corn Production 35,000 30,000 Source:USDA 25,000 20,000 15,000 10,000 5,000 0 Corn Corn

14 Russia/Ukraine Corn Exports Source:USDA Corn Corn

15 Brazil Corn Production & Exports 90,000 80,000 70,000 60,000 50,000 40,000 30,000 20,000 10, / / / / / / / / / / / / / / / /2016 Corn Corn

16 Brazil/Argentina Issues Economic chaos Possible impeachments/major political changes Currency devaluations Brazil land values have plummeted as much as 50% to 60% Input costs remain very high Farm income in the red Sharp reduction in corn acres (cost) Will plant soybeans Clearing new farmland has stopped

17 Argentina Election Macri wins! Currency devaluations Reduced export taxes? Corn from 23% to ), wheat from 20% to 0, soybeans -5% Special deals for 3 to 4 months Need tax revenue More corn acres now? More wheat acres next year? Control Inflation?

18 The China Syndrome New Farm Subsidy Program Coming? Domestic corn prices too high DDG s, Barley, Sorghum outside the TRQ s Big reserve supplies while imports continue Potential Impact? Decouple farm payments from production Lower domestic prices Use domestic reserve Reduce imports of feed grains

19 1 Presentation title 00/00/0000 9

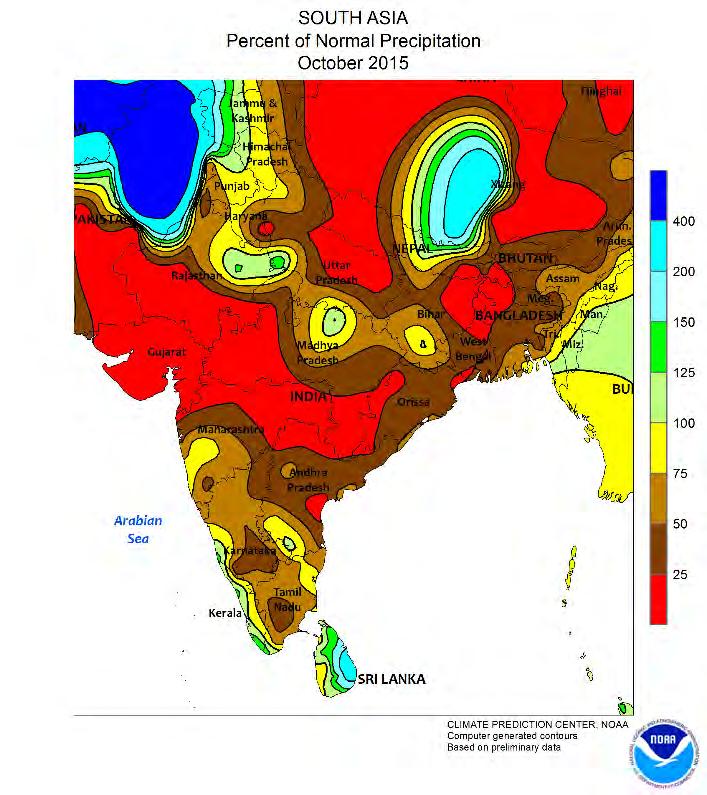

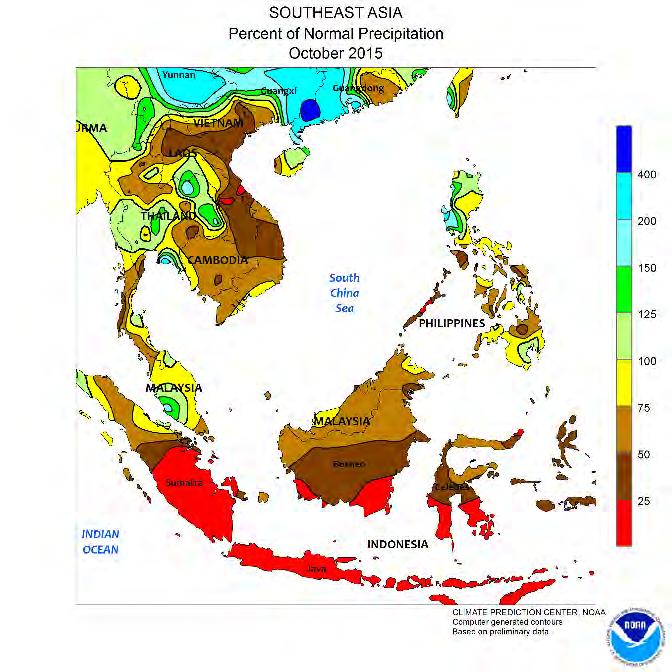

20 The China Syndrome Cofco teams up with Chinese fund to create global grains trader Exclusive: China's COFCO in talks to raise stake in grain trader Nidera China's COFCO to pay $1.5 billion for stake in Noble's agribusiness The Chinese Want Their Own Cargill The next potential target: Glencore (Viterra)?

21 The China Syndrome China now accounts for 65% of world soybean exports

22 The China Syndrome The Cofco Problem: Unlimited resources (STE?) Willing to work on very narrow margins? Currency controls? Structural change in world grain trade?

23 Biotech Crop Adoption Global Crops - Corn - Soybeans - Cotton - Canola - Squash - Papaya - Alfalfa - Sugar beet - Sweet Pepper - Tomato - Poplar

24 Source:USDA 2 12/14/2015 4

25 Bloomberg News 2 Presentation title 00/00/0000 5

26 Strongest El Nino in 50 to 100 Years Mild North America winter (yahoo!) Finally some rain for California (not a drought buster) Too much rain in southern Brazil & too dry central & north Argentina should be good but now dry Too dry in eastern Australia Too dry in Southeast Asia (reduced palm oil production) Below normal Indian monsoon (impact on ground nut and pulse crops?) Some predicting rapid collapse of El Nino by spring and that could mean 2016 Corn Belt drought?

27

28

29

30 What does it all mean? Planted area & crop inputs will be reduced that will impact production Margins at every level will stay very tight in this low price environment Demand will continue to expand, especially with low prices, cheap freight and, in many areas, low interest rates Asia, Southeast Asia, China are the critical markets that s where population and incomes continue to rise We are still only a production problem away from a return to higher prices led by corn first, wheat second and the soy complex third 12/14/

31 What are possible price ranges? 12/14/

? Can we have 4 record world crops?")

32 Wheat bouncing along the bottom at $4.70 to $5.00 (CBOT futures)? Can we have 4 record world crops? 3 12/14/2015 2

33 Corn bouncing along the bottom at $3.50 to $3.80 (CBOT futures)? Smaller world planted area Another record yield? 3 12/14/2015 3

34 Soybeans more downside risk to $8.00 (CBOT Futures)? Record world supplies More planted area Demand always underestimated 3 12/14/2015 4

35 What is Driving the Price Bus? Fundamentals still rule the long term Supply/Demand Currency valuations Weather & crop production Smaller role in periods of adequate supplies (like today) Funds still play a major short term role Big % of open interest even during this bear market Big swings in positions long or short Technical traders with very short time horizons Larger role in periods of little fresh fundamental news (like today) World geo-political risks Russian drought & contract cancelations Changes in domestic/export policies (China) Unpredictable events with significant consequences (China abandons 1 child policy?) 12/14/

36