UK and European Organic Markets and Policies

|

|

|

- Joella McDowell

- 5 years ago

- Views:

Transcription

1 UK and European Organic Markets and Policies Nic Lampkin, Executive Director Susanne Padel, Senior Researcher Organic Research Centre, Elm Farm

2 In the media spotlight 2008/9... Shoppers lose their taste for organic food - The Guardian Organic sales set to slip Mintel Hard-up shoppers abandon organic and fair trade goods The Times

3 ... and now Is it all over for organic food? The Guardian, Sep 2011 Conventional farmers are shunning organic Farmers Guardian, Aug 2011 Premiums vanish for organic meat/ organic land area falls South East Farmer, Sep 2011 Has anything changed?... well, yes Is it is as bad as the headlines suggest? (lies, damned lies and statistics!)

4 UK organic market development Total Organic Grocery Products including Baby - 4 weekly m Source: Kantar Worldpanel

5 Total Organic Market (inc. Baby) Rolling 52 week periods Y-on-Y Change % 12- Jul Aug Sep Oct Decline is slowing down 01- Nov Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Oct Nov Dec Jan Source: Kantar Worldpanel

6 Organic Growth - m - 52 w/e Dec v. year ago Baby Food Yoghurt Fresh Beef Butter Cider Wine Herbal Tea Herbs+Spices Beer+Lager Peanut Butter Meat Extract Packet Soup Prepared Peas&Beans Fresh Sausages Total Ice Cream Fresh Pork Instant Coffee Childrens Biscuits Ambient Cooking Sauces Chilled Prepared Chilled Fruit Juice+Drink Vegetables Chilled Vegetarian Fresh Poultry Chocolate Confectionery Breakfast Cereals Total Bread Fresh Lamb Total Cheese Seasonal Biscuits Hens Eggs Total Milk Chilled Ready Meals Fruit Source: Kantar Worldpanel

7 Year-on-Year Expenditure Trends - % Change Organic Waitrose Total Grocers Morrisons Sainsbury's Tesco Asda w/e 23 Jan 11 6 Source: Kantar Worldpanel

8 Year-on-Year Expenditure Trends - % Change Organic Own Label Waitrose Sainsbury's Total Grocers Tesco Asda w/e 23 Jan Morrisons -28 Source: Kantar Worldpanel

9 Total Organics- Spend by Frequency Group 62% of Organic buyers account for only 12% of spend 8% of Organic buyers represent 54% of money spent on Organics % Homes Buying % Spend Occasions 7-12 Occasions 2-6 Occasions 1 Occasion 52 w/e Jan Source: Kantar Worldpanel

10 Two broad segments of organic consumers Regular/committed >80 % of sales Well educated Health aware Middle income levels Believe in organic product quality Seek other attributes Environment Animal welfare Social Missionary zeal Occasional < 2% of sales More price & convenience sensitive Cooking skills? More sceptical about some claims Little knowledge

11 Penetration % Organic Top Markets by Household Penetration Vegetables 61 Fruit 35 Yoghurt Total Milk Chocolate Confectionery 15 Total Cheese Chilled Prepared Frt+Veg Total Organic Market Household Penetration = 86% Baby Food Hens Eggs Total Bread Dry Pasta Fresh Beef Home Baking 52 w/e 24 Jan w/e 23 Jan 11 Source: Kantar Worldpanel

12 UK organic sector development Land area (thousand ha) Retail value ( million) No of holdings '00 '01 '02 '03 '04 '05 '06 ' Source: Defra, 2011

13 Different trends in UK nations - kha fully organic N Ireland Scotland Wales England

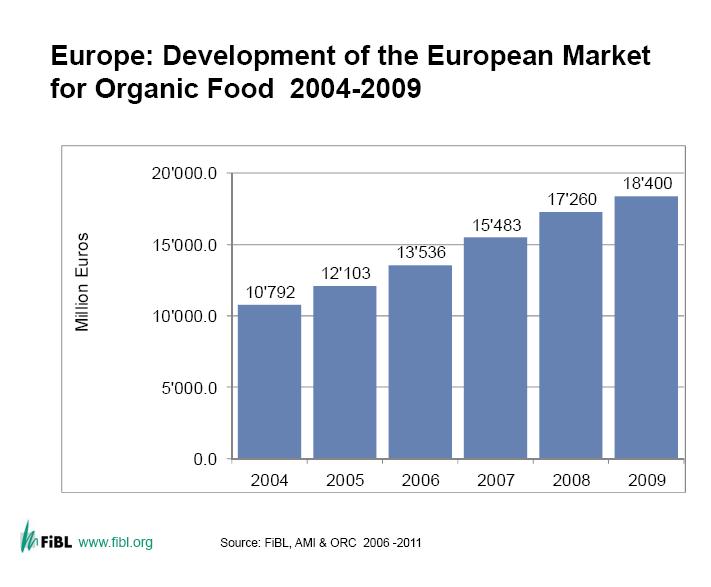

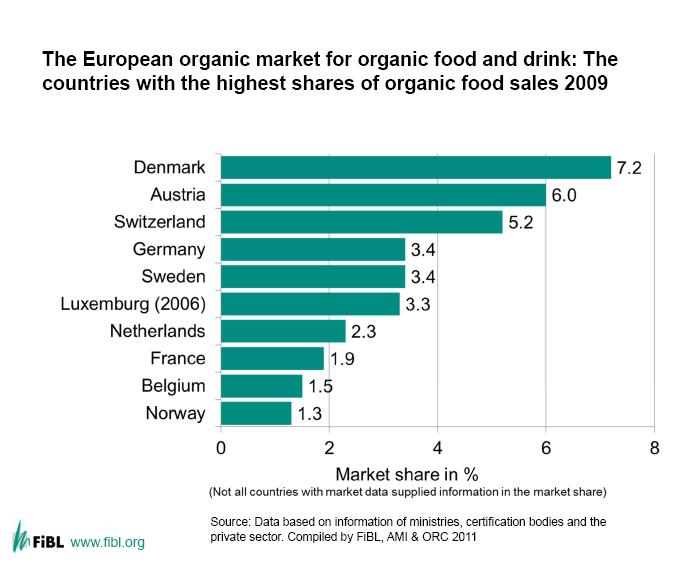

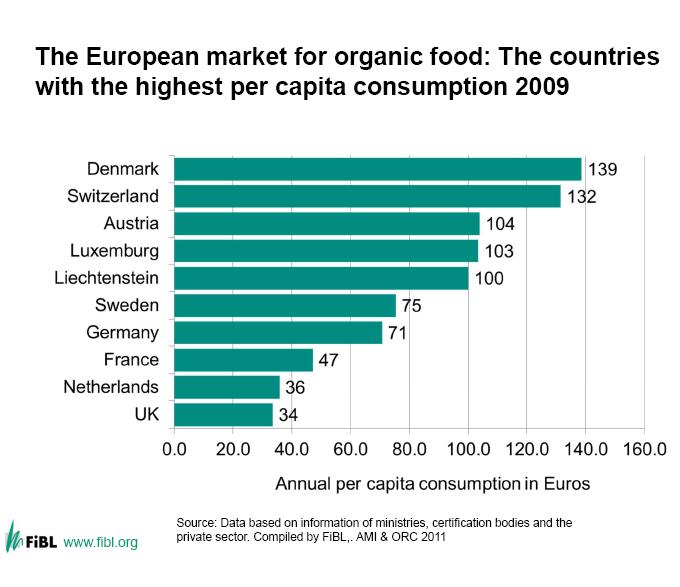

14 and in conversion N Ireland Scotland Wales England

15 Source: Defra, 2011

16 Sheep numbers increased by 11% to ca. 1 million in 2010 Source: Defra, 2011

17 Sector trends Arable: Good yields and quality this year, wheat/barley prices ca. 230/t post harvest, a reduction on prices earlier in the year while conventional prices are up Horticulture: Remains challenging following recession and a serious reduction in sales Dairy: UK production and sales fell slightly, but increasing exports, with June price 29ppl (27.5ppl 12 months previously) Poultry and pigs: Tough times, sales -20% For most sectors, profitability still comparable with non-organic

18 A closer look at beef...

19 ...and lamb

20 What s the real situation? For beef, supply shortages are now a real threat, potentially leading to retail unavailability For lamb, high conventional prices have created a floor to organic prices, with many lambs sold as conventional, but Supermarkets still charging significant premiums for organic lamb, and Spring shortages an issue

21 European organic area

22 European organic land area density in different countries, 2009

23

24

25

26

27 UK market trends compared to other countries

28 Why is the UK different? Perception of elitism and political disengagement (new CAP opportunities?) Lack of recognition of environmental and other public good benefits Competition from other initiatives (natural, local, fair-trade, low carbon), but Only organic has clearly defined standards and a European regulation Organic is often used in combination with the above, but consumers appear unaware

29 Need better communication Mintel: Consumers may review spending on premium organic foods if they do not fully understand the benefits, but a growing trend of people seeking ways to make a difference What is needed is a unified voice from the organic industry, extolling the virtues of their products. Justin King, chief executive of Sainsbury's: customers were increasingly concerned with animal welfare and husbandry standards but organic food producers had not done a good job in communicating what it stood for. EU-funded promotion campaign response

30 The Organic Research Centre

31 The Organic Research Centre Key Messages There are lots of reasons to love organic, discover yours Organic is better for nature Organic is better for animal welfare Organic costs more and it s worth it Organic contains less pesticides and nasties = natural & great tasting food Maybe next time I go shopping, I ll chose organic

32 The Organic Research Centre

33 The Organic Research Centre UK policy support Conversion and maintenance payments restored in Scotland, rescued in Wales, but low level of payment compared with EU Rural development funding used for marketing initiatives and vocational training Some research funding (but more from EU) No UK government match-funding for promotion campaign Action plans now only in Scotland (new)

34 The Organic Research Centre Organic farming scheme payments ( /ha) Arable Grass Veg Fruit England C M Wales C M Scotland C M N Ireland C M Austria C M Germany C M France C M

35 The Organic Research Centre CAP reform from 2014 an opportunity for renewal? additional payment (30% of annual national ceiling) for farmers following agricultural practices beneficial for climate/environment: crop diversification, maintenance of permanent pastures and ecological focus areas (7%). organic farming will automatically benefit from this additional payment new specific rural development measure for organic farming (Article 43) max. payment rates as for other agri-environment ( /ha:600 annual, 900 perennial, 450 other)

36 The Organic Research Centre Conclusion Recession and political environment have created challenging market conditions and low farmer interest in conversion in UK. UK situation is in marked contrast to other EU countries Some evidence that UK organic market may be stabilising, possibly even recovering (but current economic prospects poor) CAP reform proposal could herald renewal of interest in organic farming, especially if market also recovering

37 The Organic Research Centre Further information on markets, financial performance and policy support

38 The Organic Research Centre Thank you for listening!