The challenges of a semi-liberalized market and the Swiss way to handle. Kaltbach, 25th September 2017 Daniel Weilenmann

|

|

|

- Oliver Atkins

- 5 years ago

- Views:

Transcription

1 The challenges of a semi-liberalized market and the Swiss way to handle Kaltbach, 25th September 2017 Daniel Weilenmann Page 1

2 Content Overview Emmi Group The challenges of a semi-liberalized market 2

3 Emmi at a glance Net Sales 2016 CHF 3,259 million EBIT CHF 203 million EBIT margin 6.2 % Net profit 2016 CHF 140 million Net profit margin % Employees (full-time equivalents) 5779 Volume of milk processed in ,700 million kg 3

4 Three main product segments Cheese, fresh products and basic dairy products drive the portfolio Dairy products 31 % CHF 1,011 million Fresh products 25 % CHF 800 million Other products/services 5 % CHF 159 million Cheese 31 % CHF 1,015 million Powder/concentrates 3 % CHF 97 million Fresh cheese 5 % CHF 177 million Net sales Group 2016: CHF 3,259 million 4

5 Sales by region Business division Switzerland accounts for slightly more than half of sales Americas 27 % (CHF 866 million) Switzerland 53 % (CHF 1,741 million) Europe 16 % (CHF 519 million) Global Trade 4 % (CHF 133 million) Top 5, sales: Switzerland USA Spain Germany Tunisia Net sales Group 2016: CHF 3,259 million 5

6 Emmi's strategic pillars Strengthening of Swiss market International growth Cost management 6

7 Content Overview Emmi Group The challenges of a semi-liberalized market 7

8 Degree of market liberalization in Swiss agriculture Swiss producer prices in comparison to Germany (2015) Source: FOAG Dairy is the most liberalized sector of Swiss agriculture 8

-")

9 Reform of Swiss dairy market policy Market opening - Cheese (2007) - Processed agricultural products (2005) Reduction market & price support - From in average 35 to 8 Swiss cents per kg milk Increased direct payments - today CHF per farm Swiss cents per kg milk Abolition milk quota (2009) 9

10 Today s Swiss dairy market regulation milk price Cheese Liberalised market Cheese subsidy cheese subsidy border protection Dairy and fresh products Products with high/low border protection Products with no border protection Export of surplus milk to world market No more market support measures cheese dairy and fresh products milk quantity No milk quotas 10

11 Exports are needed Milk production mio kg milk Export 850 mio kg milk Import 450 mio kg milk Domestic use mio kg milk 11

12 Challenge Which milk producer / dairy has to deliver / produce for this segment? How can the sector avoid massive milk price pressure? 12

13 The Swiss solution target price A Protected and supported markets (border protection, cheese production subsidies) B Export and unprotected markets C Surplus (export to the world market) quantity of milk 13

14 Interprofession Milk ( Family «Milk producer» Family «Processors & Retail» -Dairy industry -Artisanal cheesemakers -Retailers Decisions Price recommendations Rules for segmentation Joint dairy strategy Lobbying 14

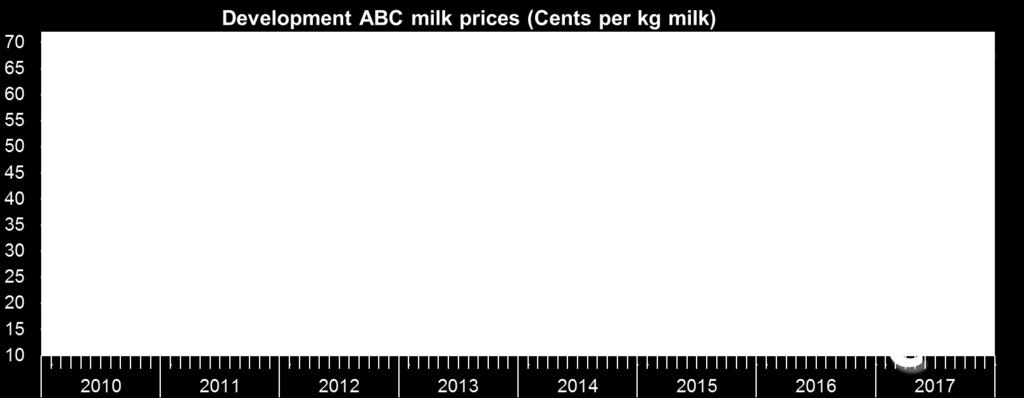

15 ABC milk prices 15

16 Defending a higher milk price level

17 Higher input costs lead to higher sales prices Significant price difference between Switzerland and neighbouring countries Germany UK Switzerland 0.62 euro 0.80 euro 17

18 Maintaining the competitive advantage of Swissness becomes harder Pressure through increasing imports 18

Feeding (based on roughage, less concentrates, GMO-free) Animal health (less antibiotics, no hormones) Family farms (average size Switzerland: 25 cows,")

19 How secure the higher Swiss milk price level? Added values of Swiss milk production! Why Swiss farmers will never be able to produce milk to world market conditions! Key factors Animal welfare (grazing) Feeding (based on roughage, less concentrates, GMO-free) Animal health (less antibiotics, no hormones) Family farms (average size Switzerland: 25 cows, average size Germany: 58 cows) 19

20 Favorable starting position Production intensity Average milk yield per dairy cow < litres/year (Germany: around 7,200 litres/ year) Lowest bacterial and cell counts worldwide (around half compared with Germany and Austria) Cattle feed Feed: 80% grass, hay & grass silage, 10% maize silage, 10% concentrated feed (around kg/year/cow) - EU: around 2,000-2,500 kg concentrated feed/year/cow 35% of milk without grass and maize silage (for traditional Swiss raw milk cheese) 100% GMO-free (cultivation forbidden in Switzerland, no imports) The world s strictest animal welfare regulations Regular access to open pasture a legal requirement in Switzerland; not in the EU Government programmes to encourage particularly animal-friendly indoor enclosures The same applies for additional, year-round access to open pasture (affects 80% of cows) Individually-run family businesses rather than large industrial concerns The average Swiss milk producer has 24 ha of production space and 23 cows. - Germany: 40 ha (old federal states) 200 ha (new federal states); 50 cows 20

21 Emmi sustainable milk 100% sustainable milk by 2020 Animal welfare Standards above national legislation Feeding Quality Dairy cows mainly fed on grass and hey Limited concentrates Certified soy GMO-free Top milk quality No performance-enhancing hormones Milk free of antibiotics Milk price Milk price above average 22

22 Conclusions The semi-liberalized market challenges the whole value chain Agreement on a private market regulation system secures a higher milk price level in Switzerland Added values and sustainability of Swiss milk production enable differentiation of Swiss milk 23

23 24