Sobi Update and Perspective Jefferies Healthcare Conference

|

|

|

- Phebe Ross

- 5 years ago

- Views:

Transcription

1 Sobi Update and Perspective Jefferies Healthcare Conference Geoffrey McDonough CEO London 19 November 2014

2 Forward Looking Statements In order to utilize the Safe Harbor provisions of the United States Private Securities Litigation Reform Act of 1995, Swedish Orphan Biovitrum is providing the following cautionary statement. This presentation contains forward-looking statements with respect to the financial condition, results of operations and businesses of Swedish Orphan Biovitrum. By their nature, forwardlooking statements and forecasts involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results and developments to differ materially from that expressed or implied by these forward-looking statements. These factors include, among other things, the loss or expiration of patents, marketing exclusivity or trade marks; exchange rate fluctuations; the risk that R&D will not yield new products that achieve commercial success; the impact of competition, price controls and price reductions; taxation risks; the risk of substantial product liability claims; the impact of any failure by third parties to supply materials or services; the risk of delay to new product launches; the difficulties of obtaining and maintaining governmental approvals for products; the risk of failure to observe ongoing regulatory oversight; the risk that new products do not perform as we expect; and the risk of environmental liabilities.

3 An international specialty healthcare company dedicated to rare diseases. Our key therapeutic areas are Inflammation and Genetic diseases, with a growing focus on Haemophilia. We deliver products to specialist physicians and their patients through our integrated and focused team approach to sales and marketing, medical affairs and patient access. We leverage our world-class capabilities in protein biochemistry and biologics manufacturing to develop next generation biological products. 3

Outstanding shares: 272.")

4 Quick Facts Market Cap: $3.48 Billion USD (SEK 23.2 Billion) Share: 12 November 2014: SEK week range: SEK Listing: NASDAQ OMX (STO:SOBI) Outstanding shares: M International Presence 550 employees Sales and marketing organization which covers about 20 countries in Europe Growing organizations in US, Russia, Middle East Ownership Summary: 9% 4% 3% 1% Sweden United States 19% United Kingdom 64% Luxemburg Switzerland Rest of World 4 USD 1 = SEK (average rate for the period)

5 Building Our Future 1. Diverse, growing, and profitable base business focused on rare diseases 2. Near-term first-to-market longacting haemophilia factors with exclusive USD 3.7 B in Sobi territories 3. Pipeline of early stage rare disease biologics 5

6 Building a Leading Rare Disease Company EBITA Short-term Mediumterm Long-term Early Programmes Haemophilia Haemophilia royalties Genetics & Metabolism Inflammation Partner Products ReFacto TIME 6

7 Highlights YTD 2014 Financial YTD 2014 (YTD 2013) MSEK Total revenues: SEK 1,902 M (1,566) An increase of 21% An increase of 18% at constant exchange rates Product revenues: SEK 1,414 M (1,110) An increase of 27% 1,900 1, , ,902 1,121 Gross Margin: 59% (59) EBITA: SEK -82 M (146) Adj. EBITA: SEK 243 M (146) excluding Kiobrina write-off CF from operations: SEK 232 M (181) -100 YTD YTD-14 Total revenues Gross profit EBITA EBITA excluding Kiobrina write-downs Cash flow from operating activities 7

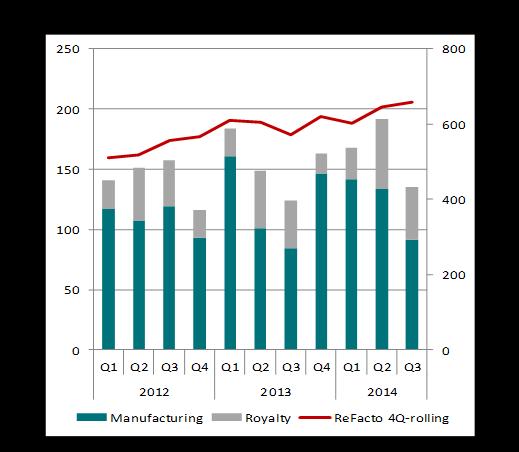

8 Revenue Trajectory: Driven by Product Sales MSEK 700 Total Revenue Total revenue driven by double digit growth in product sales ReFacto continues to meet our expectations for single digit growth 300 Product Revenue 200 ReFacto Revenue

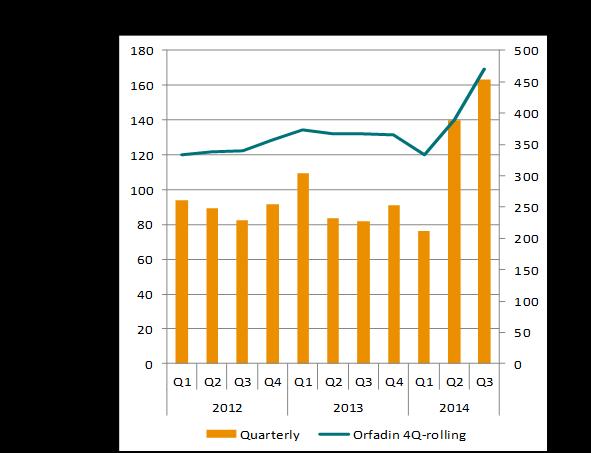

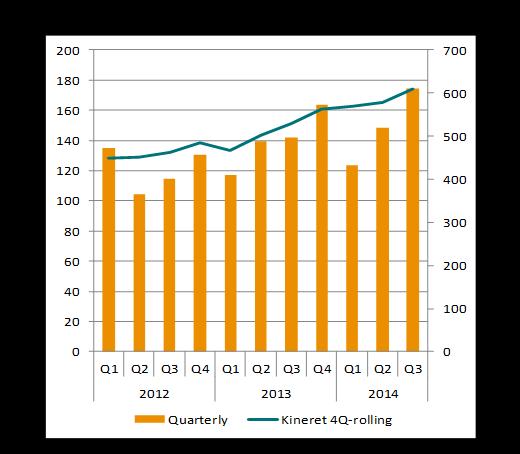

9 YTD Revenue by Business Line Early Stage Development Programmes Haemophilia SEK 19 M USD 3 M +12% Inflammation SEK 446 M USD 67 M Genetics & Metabolism SEK 465 M USD 70 M +37% 9 USD 1 = SEK (average rate for the period) Percentage increases at constant exchange rates Partner Products SEK 484 M USD 72 M ReFacto AF SEK 488 M USD 73 M +7% +30%

10 Operating Portfolio Momentum 10

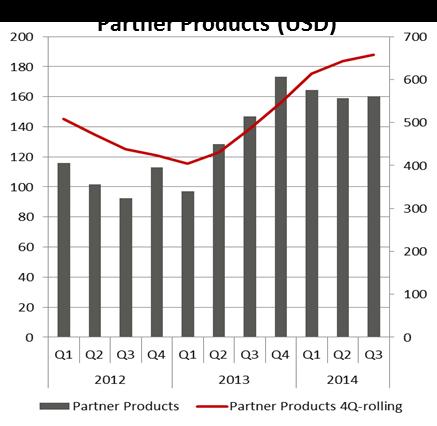

11 Partner Products Annual Growth Trend MSEK 407 Revenue YTD 2014 Excluding co-promotion revenues 11

12 Q1-12 Q2-12 Q3-12 Q4-12 Q1-13 Q2-13 Q3-13 Q4-13 Q1-14 Q2-14 Q3-14 SEK M Cash and Net Debt % End of quarter cash position: SEK 611 M % Net debt SEK 206 M % 20% Expected one-time cost in Q4 for Multiferon SEK 25 to 30 M, with limited cash impact % 0% Expected larger payments in Q4 XTEN payment Q4, USD 7M Elocta opt-in Q4, USD 10 M Net debt Net debt / Equity 12

13 Outlook 2014 (Unchanged) Revenues MSEK 2,300 to 2,500 Gross Margin 58-60% Operating costs Operating costs are expected to increase as the company continues to prepare for the planned launch of the Haemophilia programmes The outlook was first published in the 2013 Q4 report on 20 February

14 Significant events after the reporting period Biogen Idec filed a marketing authorisation application for Elocta in Europe Decided to discontinue the production of Multiferon Placed the phase 1 study of SOBI002 on clinical hold Decided not to pursue an additional indication for Kepivance 14

Positive KIDS-A-LONG data Q1 2014 Approved in the US European file validated October 2014 European launch expected 2H 2015 Potential future hemophilia candidate")

15 Building a Leading European Haemophilia Platform Haemophilia Factor IX Fc (Alprolix in the US) Approved in Canada Approved in US Paediatric studies underway in Europe European launch expected 2H 2016 Factor VIII Fc (Eloctate in the US) Positive KIDS-A-LONG data Q Approved in the US European file validated October 2014 European launch expected 2H 2015 Potential future hemophilia candidate (XTEN) added to partnership with Biogen Idec 15

16 Expected Long Acting FVIII EU timeline EU MAA filing Possible EMA approval Sobi opt-in Sobi Elocta launch in EU (Sobi territory)

17 Expected Long Acting FVIII EU timeline EU MAA filing Possible EMA approval Sobi opt-in Sobi Elocta launch in EU (Sobi territory) Competitors First potential long-acting FVIII competitors* 17 * Based on publically announced data

18 Haemophilia A in Sobi Territory Size of Market in Sobi Territories* $ 3,3 Billion 18 *Source: MRB, 2011, includes all patients (mild, moderate, severe)

19 Haemophilia A in Sobi Territory Recombinant Market in Europe* Plasma:Recombinant in European Market* 11% 17% 46% Baxter Bayer 43% Recombinant 26% Pfizer CSL Behring 57% Plasma 19 *Source: MRB, 2011, includes all patients (mild, moderate, severe)

20 Fewer than 100 Haemophilia Reference Centres 20

21 Sobi Launch Team on Track Headcount Anticipated EU Approval Elocta Q Preparation has been ongoing for two years On track to reach launch readiness in 2015 with fully dedicated organization Sequential build of Market Access, Medical Affairs, and Commercial teams 0 H H H H

22 Sobi/Biogen Collaboration Financial Flows for Eloctate/Elocta Programme Contractual Milestones BIIB first commercial sale EMA filing/ Sobi Opt-in EMA approval Sobi first commercial sale After Sobi s share of development cost is paid back Royalties 17% 12% 7% Sobi royalty to BIIB Base rate cross royalty 2% BIIB royalty to Sobi

23 Building Our Future 1. Diverse, growing, and profitable base business focused on rare diseases 2. Near-term first-to-market longacting haemophilia factors with exclusive USD 3.7 B in Sobi territories 3. Pipeline of early stage rare disease biologics 23

24 Strategic Priorities 1. Near-term focus on growth in our base business, with sustainable positive cash flow from operations. 2. Medium-term investments to ensure successful commercialisation of our haemophilia programmes. 3. Long-term growth will come organically and through acquisitions. 24