Specialty Pharmacy 101

|

|

|

- Dulcie Thomas

- 5 years ago

- Views:

Transcription

1

2 Specialty Pharmacy 101 The Landscape of Specialty Pharmacy Services DATE: October 27, 2011 NAME: TITLE: Clinical Pharmacist, Serve You

3 Agenda Define specialty pharmacy Examine market trends and current challenges Review pipeline highlights Discuss specialty management

4 Why is it Important to focus on Specialty Pharmacy? Fastest growing segment of pharmaceutical spending > The biologics share of the pharmaceutical market is expected to increase to 25-30% in 2013 > Hundreds of drugs in the biotechnology pipeline with manufacturers spending 25% of R&D on biologics > In 2010, more than half of FDA approvals were specialty drugs Changing pharmacy environment for payers > 1-3% of a health plan population take specialty drugs which represents ~25% of the plan s pharmacy spend > The actual spend for a health plan may even be as high as 50% when considering specialty drugs received under the medical benefit > Annual year-over-year specialty drug trend is 12-17%

5 Defining Specialty Pharmacy There is no universally accepted definition or industry standard URAC, an independent nonprofit organization, defines it as a high touch, comprehensive care system of pharmacological care wherein patients with chronic illnesses and complex disease states receive expert therapy management and support tailored to their individual needs

6 What is a specialty drug? Specialty drugs are typically large, unstable, protein-based molecules, produced through a biotechnology process and have the following characteristics: High cost (CMS defines as > or = $600/month) Prescribed for complex or chronic medical conditions targeting underlying disease pathology Require specialized patient training and coordination of care prior to initiation and/or during therapy Have unique patient compliance and safety monitoring requirements Require special handling, shipping and/or storage Have potential for significant waste due to high cost of drug

7 These drugs have the potential to: What is a specialty drug? Decrease or reverse the progression of chronic illness and may also mitigate the adverse consequences of chronic disease Increase life expectancy Improve quality of life Enhance workplace productivity Minimize the burden of disease Reduce health care spending Limit the overall cost of disease Each PBM has its own criteria for defining and including drugs on their specialty lists.

8 General Categories of Specialty Drugs Definition SELF-ADMINISTERED DRUGS CLINIC/OFFICE ADMINISTERED INFUSIONS AND INJECTIONS CLINIC/OFFICE ADMINISTERED CHEMOTHERAPY Multiple sclerosis Rheumatoid arthritis Psoriasis Hepatitis C Vaccines Immune disorders Rheumatoid arthritis Asthma Cancer Neutropenia Anemia

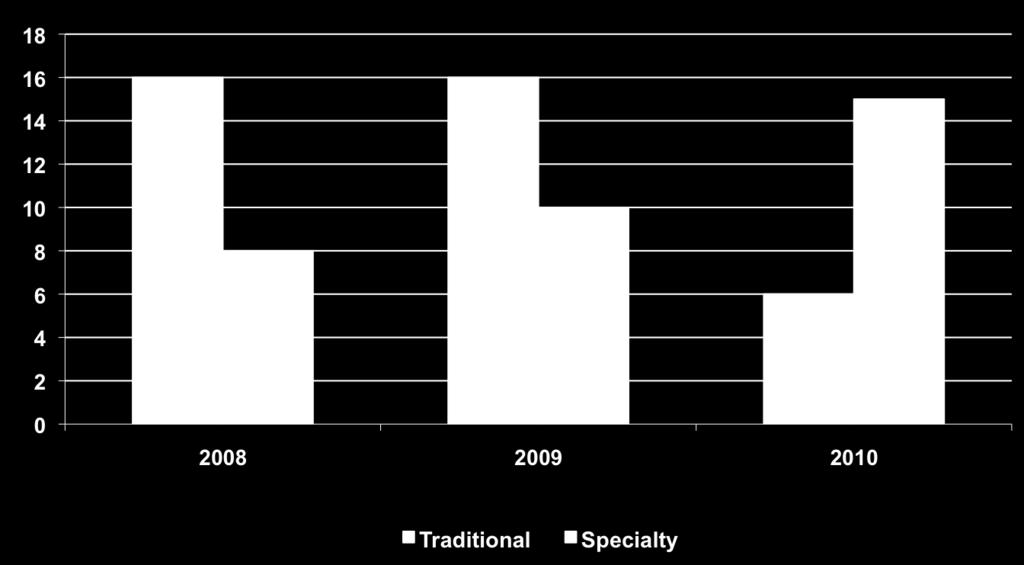

9 Trends Specialty Market Trends Traditional Conditions Shifting to Specialty New Oral Drugs for RA, MS and Hepatitis C SPECIALTY MARKET GROWTH Manufacturers Focusing on Specialty Development for Rare Diseases and Cancer

10 Current Challenges Cost of specialty medications and double digit growth trajectory Associated costs of administering specialty drugs and effect on total drug spend Breadth and depth of pipeline of new specialty drugs

11 Trends and Drivers of Spend The specialty trend continues a double digit growth rate with the annual growth trajectory estimated at 17-20%. The trend is driven by increased utilization and increased unit cost. Unit cost growth is the most significant driver of specialty drug trend Medco Drug Trend Report

12 Spend by Therapeutic Category Multiple sclerosis (MS), rheumatoid arthritis (RA) and other autoimmune conditions, and cancer represent the largest contributors to specialty trend representing 67% of total specialty drug spending in 2009, with each of these classes growing at a rate from 18% to 34%. Serve You Specialty Claims by Therapeutic Category (2009) 2% 4% 26% 1% 36% Autoimmune Conditions MS Oncology Other Hepatitis C Pulmonary Hypertension Growth Hormone 10% 21%

13 FDA New Drug Approvals

14 Trends Recent Specialty Drug Approvals Drug Manufacturer Indication Route Gilenya Novartis Multiple Sclerosis PO Egrifta Theratechnologies Lipodystrophy SQ Xgeva Amgen Bone Metastases SQ Makena KV Pharmaceuticals Prevent Preterm Birth IM Benlysta HGS/GSK Lupus IV Xalkori Pfizer Lung Cancer PO Incivek Vertex Hepatitis C PO Victrelis Merck Hepatitis C PO

15 Pipeline PIPELINE DATA AS OF 2008 Type Number Total number of biotechnology drugs 633 Oncology agents Oral chemotherapy agents Infectious diseases 162 Autoimmune disorders 59 Source: FMCP Specialty Initiative Report (PhRMA)

16 Near-Term Specialty Pipeline Highlights Inflammatory conditions: > Oral biologics will compete with injectables > More therapies for gout and lupus > Biobetters on the horizon Multiple sclerosis: > More oral disease-modifying drugs > May see combination use of MS drugs Cancer: > Cancer treated as a chronic condition > Role of pharmacogenomics Hepatitis C: > Oral protease inhibitors are potential blockbusters > HCV-related disease burden is projected to increase severalfold over the next 20 years

17 Long Term Challenges & Trends Impact of health care reform Availability of biosimilars > Specifics of what constitutes therapeutic equivalency will have to come from the FDA > Savings estimates are smaller than that of generics, e.g. 20 to 30% of brand costs Demonstration of value of specialty services

18 Management of Specialty Drugs Specialty drugs require unique management practices for patients, health plans, and employers. The following services are necessary to achieve these objectives: Medication management Patient management Cost management Distribution

19 Specialty Drug Delivery Channel Specialty pharmaceuticals may flow through a variety of distribution channels according to: > Their administration requirements > Benefit design > Risk Evaluation and Mitigation Strategies (REMS) A number of drugs are used in a limited number of patients and have high manufacturing costs; thus, these manufacturers depend on centralized distribution points e.g. limited distribution

20 Specialty Pharmacy Service Levels Generally classified into three levels: Baseline or core level services High touch or advanced care management services Home infusion or home training Drugs can be tied to different levels of service. For example: orals = core services RA/MS drugs = high touch services IVIG/factor products = home infusion/training

21 Core Services Cost management Insurance billing and coordination of benefits 30 day fill Utilization management 24/7 access

22 Core Services: Cost Management Specialty pharmacy providers utilize the following strategies to manage costs: Volume purchasing Rebates: while not available for all specialty drugs, in some well-used classes such as growth hormones, rheumatoid arthritis, manufacturers are providing rebates similar to those seen on the traditional drug side Intelligent benefit design: Shift of coverage from the medical to the pharmacy benefit, appropriate cost-sharing/member affordability Mail order: e.g. retail lock-out 30 day fill

23 Two primary questions to consider: Intelligent Benefit Design 1. Should specialty drugs be part of the medical or pharmacy benefit? 2. What is the appropriate level of member cost-sharing?

24 Specialty Prescription Abandonment Gleason et al examined abandonment of specialty prescriptions at the pharmacy for patients newly initiating a biologic for the treatment of MS or TNF blocker for treatment of RA or other conditions. Out-of-Pocket (OOP) Expense Multiple Sclerosis (N=2,791) Unadjusted Abandonment Rate Odds Ratio from Logistic Regression TNF Blocker (N=7,313) Unadjusted Abandonment Rate Odds Ratio from Logistic Regression $0 - $ Reference Group 4.7 Reference Group $101 - $ * $151 - $ * $201 - $ * $251 - $ * * $351 - $ * * >$ * * Increasing OOP costs were associated with increased prescription abandonment. Gleason et al. JMCP. 2009(15)8

25 Abandonment of Oral Anti-Cancer Drugs In a 2011 study, researchers used a nationally representative pharmacy claims database and identified 10,508 patients with Medicare and commercial insurance for whom oral anti-cancer therapy was initiated between 2007 and Key findings include: 10% of patients abandoned their anticancer medicine, and another quarter had some delay in initiating another oncolytic. Pharmacy plan design (cost-sharing amount) and complexity of patients' drug therapy (prescription activity) were significant drivers of abandonment > Claims with cost sharing greater than $500 were four times more likely to be abandoned than claims with cost sharing of $100 or less > Patients with five or more prescription claims processed within in the previous month had 50% higher likelihood of abandonment than patients with no other prescription activity Decision makers should be aware of the impact of benefit structure on adherence and access to specialty drugs.

26 What are plans doing now? The Pharmacy Benefit Management Institute recently released its Prescription Drug Benefit Cost and Plan Design Report. The 2011 survey was completed by 274 employers representing 5.2 million members. Key results include: Plans using a 4-tier design increased from 17% to 25% between 2010 and Specialty copays increased by 37% in The average specialty copay grew from $61 in 2010 to $84 in 2011 Nearly 1 in 4 employers now place specialty drugs on the 4 th tier. Reduced coverage of specialty drugs on the medical side is on the rise as 24% of employers now restrict coverage of specialty drugs under the medical benefit, up from 12% in Accessed 20 October 2011

27 Core Services: 30 day fill It is industry standard to dispense a 30 day supply of specialty drugs, even via mail. Some specialty pharmacies are evaluating a split-fill program for those highly toxic (oncology) drugs in which the discontinuation rate is very high or a starter pack quantity limit (7 to 14 days) for any newly prescribed specialty drug therapy

28 Core Services: Insurance Billing and Coordination of Benefits Specialty pharmacy providers ensure: plan eligibility and coordination of benefits is seamless all avenues of reimbursement are considered for each member (e.g. manufacturer co-pay assistance programs, disease foundations)

29 Core Services: Utilization Management Utilization management tools are similar to those employed in the traditional pharmacy benefit plan design but may vary by disease state: Formulary management Prior authorization Step therapy (traditional step therapy is not usually employed; however, elements of step criteria are included as appropriate in prior authorizations) Quantity limits

30 Core Services: 24/7 access Specialty pharmacies provide 24/7 availability of clinical pharmacy or nursing staff to answer any drug therapy or disease-related questions.

31 High Touch Services: New Rx For any new specialty Rx received, the following activities are typically undertaken: 1. Assessment of patient s education needs and compliance risk 2. Confirmation of dose and medical necessity (e.g. prior authorization) 3. Enrollment in health management programs, as applicable 4. Coordination of injection training and/or home healthcare as needed 5. Discussion of patient concerns and preferences

32 High Touch Services: Medication Adherence Programs Medication adherence programs are a key strategy for managing the specialty pharmacy benefit and ensuring positive patient outcomes. Programs offer in-depth personal support for every patient with an increased focus in disease states with highest prescription volume and known to have severe side effects (e.g. MS, RA, PAH, psoriasis, hepatitis C) Specialty pharmacy providers can provide individual and aggregate adherence data and outcome reporting Programs typically include two components: 1. Refill reminders conducted by Patient Care Coordinators to confirm patient s medication regimen 2. Compliance monitoring conducted by Clinician (nurse or pharmacist) to promote compliance, assess for efficacy/safety, and coordinate care with patient s physicians.

33 High Touch Services: Disease Management Disease management programs focus on improving member health and controlling client expenditures across the entire spectrum of healthcare services. Programs address disease prevention, education, treatment, and long-term management of high-prevalence, chronic diseases. Individualized care plans are developed with ongoing case management A variety of approaches are typically employed, such as risk assessment, wellness and prevention education, drug utilization evaluation, clinical interventions, and outcomes assessment.

34 Other Specialty Pharmacy Services Specialty pharmacy providers may also provide some of the following services: Education materials (print materials, mailings, web-based materials) Administration of Risk Evaluation and Mitigation Strategies (REMS) Conformity with prescribing protocols/guidelines, genetic testing as appropriate Integration and coordination with the medical benefit

35 High cost, high complexity, high touch Takeaways > Specialty drugs are expensive and rapidly getting more so. > Specialty drugs require unique management practices for patients, health plans, and employers. > Effective disease therapy management can help a patient get maximum benefit from a prescribed medication. Biosimilar versions of some specialty drugs are in the future and may have lower costs.

36 Thank You! Clinical Pharmacist Serve You