CL King Best Ideas Conference

|

|

|

- Cameron Walker

- 5 years ago

- Views:

Transcription

1 Leadership in Surface Modification and Drug Delivery Phil Ankeny, Senior Vice President and CFO CL King Best Ideas Conference The Omni Berkshire Place Hotel September 19, 2007

2 Safe Harbor Statement Some of the comments made today will be forwardlooking and are made under the Private Securities Litigation Reform Act of Actual results may differ and factors that may cause such results to differ are identified beginning on page 14 of the Company s fiscal 2006 Form 10-K annual report and in the MD&A section of the Company s Forms 10-Q filed after the 10- K.

3 Investment Highlights Demonstrated leadership and expertise in the development of surface modification and drug delivery technologies Unique opportunity to exploit convergence of drugs and medical devices; expanding to include polymer based drug delivery Partner of choice for the world's most renowned ophthalmology, cardiology, pharmaceutical, and biotechnology companies Broad portfolio of proprietary platforms enables development, manufacture, and commercialization of breakthrough products Making progress moving up product development value chain Consistent track record of execution driven by a strong, sustainable business model

4 Focus: Business Units Surface Modification Drug Delivery In Vitro Hydrophilic Tech. Regenerative Tech. Drug Delivery Ophthalmology In Vitro Tech. Orthopedics Brookwood Pharma.

5 Focus: Applications & End Markets Surface Modification Drug Delivery In Vitro Applications: Hydrophilic Biocompatible Hemocompatible Prohealing Cell Encapsulation End Markets: Cardiovascular Ophthalmology Orthopedics Diabetes

6 Focus: Applications & End Markets Surface Modification Drug Delivery In Vitro Applications: Hydrophilic Biocompatible Hemocompatible Prohealing Cell Encapsulation Applications: Site Specific Drug Eluting Stents Ophthalmic Implants Systemic Injections Implants End Markets: Cardiovascular Ophthalmology Orthopedics Diabetes End Markets: Cardiovascular Ophthalmology Orthopedics Oncology Diabetes Central Nervous System Pain

7 Focus: Applications & End Markets Surface Modification Drug Delivery In Vitro Applications: Hydrophilic Biocompatible Hemocompatible Prohealing Cell Encapsulation End Markets: Cardiovascular Neurology Orthopedics Diabetes Applications: Site Specific Drug Eluting Stents Ophthalmic Implants Systemic Injections Implants End Markets: Cardiovascular Ophthalmology Orthopedics Oncology Diabetes Central Nervous System Pain Applications: Components for Diagnostic Test Kits Stabilization Antigens Substrates Microarrays Cell Culture Labware End Markets: In Vitro Diagnostics Genomics Cell Culture

8 SurModics Customer Base Today 89 Licensed Customers Novocell

9 Business Model Revenue by Type $69.9M FY06 Revenue by Business Segment 3Q07 Royalties and License Fees $53.0M 76% In Vitro $5.1M (29%) Drug Delivery $5.8M (32%) Product Sales $11.2M 16% R & D $5.7M 8% Hydrophilic and Other $6.9M (39%) Operating Results 3Q07 Revenue $17.8M Operating Margin 42% Net Margin 31%

10 Growth Drivers Convergence of drugs and devices Climbing the value chain Multiple ways to participate in DES market Growing pipeline New markets Put the balance sheet to work

11 Convergence of Drugs and Devices Drug Device Polymer Convergence catapults drugs, devices and polymers into new and unexpected applications Major convergence trends are present in orthopedics, ophthalmology, cardiovascular, biomaterials, and regenerative medicine, among others SurModics is positioned at the forefront of this trend, having partnered in the first wave of convergence with the Cypher DES, and participating in numerous subsequent waves in a wide range of applications

12 Multiple Combinations for Polymer Based Drug Delivery Polymer Only Polymer / Device Polymer / Drug Polymer / Device / Drug Eureka In Situ Matrix Hydrophilic Coating Microparticles I-vation Implant Eureka Implant Finale Prohealing Coating Drug Delivery Implant Ophthalmic Implant Drug Eluting Stent Wound Spacer Device Drug Polymer

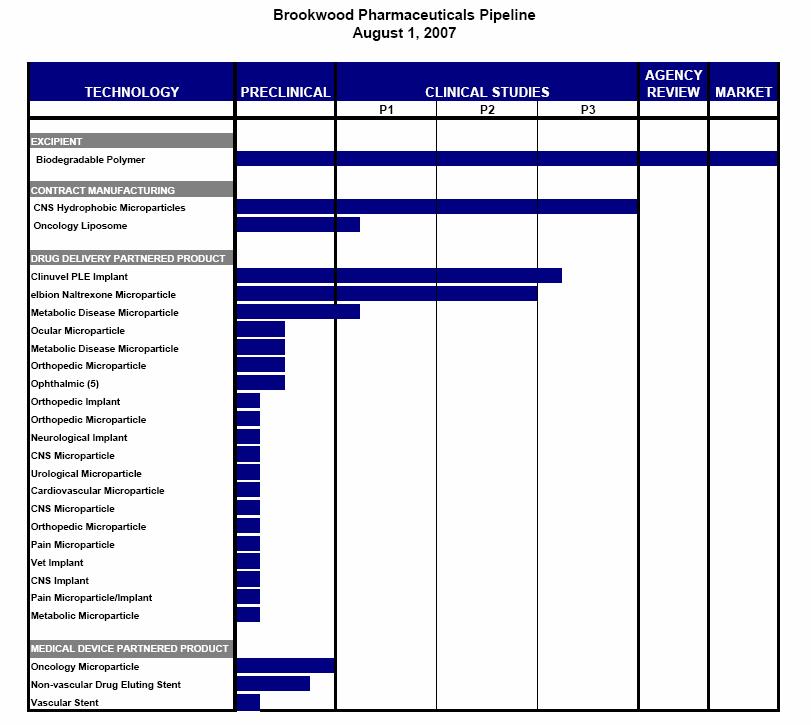

13 Brookwood Pharmaceuticals July 2007 Acquisition of Brookwood Pharmaceuticals A drug delivery business that provides polymer based technologies to companies developing improved pharmaceutical products Strength is injectable microparticles and implant technology, both based on biodegradable polymers, to provide sustained and systemic drug delivery ~30 customers, including pharma, biotech and medical device cos. $12.7 million revenue in calendar year 2006 Paid $40 million in cash at closing and up to an additional $22 million on achievement of specified milestones Anticipated Acquisition Benefits: Broader technology offerings to customers Revenue, market and customer expansion and diversification Enhances pipeline of potential revenue generating opportunities Improved Capabilities: Enhances product manufacturing capabilities Bolsters capabilities to support key projects with Merck and other customers

14 Brookwood Pharmaceuticals

15 Growth Drivers Convergence of drugs and devices Climbing the value chain Multiple ways to participate in DES market Growing pipeline New markets Put the balance sheet to work

16 Ophthalmology $11B ophthalmology market Retinal disease AMD (age-related macular degeneration) DR/DME (diabetic retinopathy, macular edema) Addressable market expected to reach multi-billion dollar level over next 5 years January Acquisition of InnoRx, Inc. Drug delivery company developing novel therapies for ocular diseases

17 Anatomy of the Eye RETINA MACULA CORNEA LENS TARGET: Back of Eye Diseases VITREOUS

18 Value Proposition Site-specific controlled release offers significant advantages over multiple injections Improved therapeutic outcomes Increased compliance reducing number of injections Reduced side effects High SITE SPECIFIC CONTROLLED RELEASE Toxic Tissue Drug Level Therapeutic Window Low MULTIPLE INJECTIONS Ineffective Elapsed Time

19 Agreement License agreement covering I-vation implant in combination with TA and other Merck drugs facilitates SurModics drive to climb the value chain $20 million up front license fee Up to $288 million in development milestones R&D revenue, including funding of clinical trial activities Manufacturing revenue for clinical and commercial supply Royalties

20 Multiple Paid Development Partners Clinical Applications Back of the Eye AMD DME DR Posterior uveitis Front of the Eye Glaucoma Cataracts Potential Customer Projects SurModics Polymers Durable Bravo Encore Biodegradable PolyActive SynBiosys Cameo Eureka Therapeutic Agents Multiple drugs and bioactive agents being evaluated Drug Delivery Platforms Intravitreal Implant Subretinal Implant Working with other top 10 pharma/biotech companies

21 BioFx Laboratories August 2007 Acquisition of BioFx Laboratories A leading manufacturer of substrates, a critical component of diagnostic test kits used to detect and signal that a certain reaction has taken place Offers both colorimetric and chemiluminescent substrates, as well as other products for use in in vitro diagnostic assays $3.5 million revenue in calendar year 2006 Paid $11.3 million in cash at closing and up to an additional $11.4 million in cash on achievement of specified revenue targets Anticipated Acquisition Benefits: Broadens product portfolio in In Vitro diagnostics Expands customer base and creates cross selling opportunities Increases revenue diversification Improved Capabilities: Additional technology and management expertise in In Vitro business Offers customers more complete product development solution

22 Growth Drivers Convergence of drugs and devices Climbing the value chain Multiple ways to participate in DES market Growing pipeline New markets Put the balance sheet to work

23 Multiple Ways to Participate in DES Market $4.5 Billion Worldwide Market Drug Delivery Polymers Durable Biodegradable Stent Delivery Systems Hydrophilic coatings Anti-Thrombotic Coatings Heparin Biodegradable polymers Prohealing

24 FINALE Prohealing Technology Lack of endothelial cells on DES without FINALE coating DES shows endothelial cell overgrowth with a FINALE prohealing coating

25 Growth Drivers Convergence of drugs and devices Climbing the value chain Multiple ways to participate in DES market Growing pipeline New markets Put the balance sheet to work

26 Growing Pipeline Feeds Near- and Long-Term Growth (Excluding Brookwood Pharmaceuticals Pipeline) 6/30/07 Products on the Market Licensed Products Not Yet Launched Major Non- Licensed Projects 74 6/30/

27 Licenses Signed by Customers of SurModics Q1-Q

28 Growth Drivers Multiple ways to participate in DES market Growing pipeline Convergence of drugs and devices Climbing the value chain New markets Put the balance sheet to work

29 Donaldson Partnership: Extracellular Matrix and Nanofibers Natural Collagen Surface Synthetic Nanofibers

30 Donaldson Partnership Synthetic extracellular matrix (ECM) products for cell culture Large addressable markets Research ~ $100 million High Throughput Screening (HTS) ~ $500 million No FDA approval process Distribution partner Initial products launched in April 2007

31 Orthopedics Trauma wound spacer Military and civilian applications High rate of infection in extremity war wounds (as high as 40%) No FDA cleared pre-made bead product available in the U.S. Use in theater currently requires time and supplies to create beads in a tactical situation FDA path under investigation Other pipeline products in development

32 Growth Drivers Multiple ways to participate in DES market Growing pipeline Convergence of drugs and devices Climbing the value chain New markets Put the balance sheet to work

33 Strong Balance Sheet $94.1 million in cash and investments as of June 30, 2007 Does not include $20 million from Merck, or funding of recent acquisitions Up from $73.3 million at end of FY06 No debt Putting the balance sheet to work Technology in-licensing and acquisition Strategic investments M&A Share repurchase

34 Business Development Over $110 Million of Capital Committed InnoRx acquisition Brookwood Pharmaceuticals acquisition BioFx Laboratories acquisition Abbott Diagnostics purchase of future royalties under SurModics patents OctoPlus (2 transactions strategic investments and polymer licensed-in) Paragon IP investment Novocell investment ThermopeutiX investment InnoCore biodegradable polymers Intralytix biodegradable polymers

35 Corporate Goals Launch 20 new products by our customers Execute 18 new licenses with our customers Generate $5.0M in commercial R&D in Q2-Q4 FY2007

36 Cardiovascular Sign a customer license for a new drug eluting device Secure a paid development program with a third party for Eureka Secure a paid development program with a customer for Prohealing

37 Ophthalmology Sign our first customer license using SurModics implant technology Initiate Phase II clinical trial for I-vation TA Develop a new platform other than I-vation TA for sustained drug delivery Secure multiple paid programs with customers for drug delivery, including at least one for delivery of a large molecule (currently at 6)

38 Orthopedics Partner with a major orthopedic company

39 In Vitro Technologies Launch by Corning Life Sciences of the first cell culture labware product developed with Donaldson and Corning

40 3 rd Quarter FY2007 Results (000's) 3Q07 3Q06 Growth Revenue: Royalties and license fees $13,416 $13,948-4% Product sales 2,947 2,659 11% Research & development 1,399 1,532-9% Total Revenue 17,762 18,139-2% Cost of Sales 1, % Operating Expenses 9,027 7,785 16% Operating Income 7,518 9,463-21% Investment Income * 1,201 1,102 9% Income Taxes (3,132) (4,207) -26% Net Income $5,587 $6,358-12% EPS $0.31 $0.34-9% * 2Q06 results include a non-cash impairment loss on the Company s investment in Novocell.

41 Successful Track Record Revenue Operating Margin $ in millions % 50% 40% 30% 20% 10% 9.7% 17.9% 33.3% 36.3% 29.2% 47.7% 58.3% 59.7% 54.7% 0 0% * 2005** 2006*** * Excludes $16.5M asset impairment charge and non-cash equity compensation expense ** Excludes $30.3M IPR&D charge, $2.5M asset impairment charge and non-cash equity compensation expense ***Excludes non-cash equity compensation expense and a $4.7M non-cash impairment loss on the Company s investment in Novocell

42 Successful Track Record Operating Cash Flow Diluted EPS $ in millions $1.50 $1.30 $1.10 $0.90 $ $0.50 $0.30 $ * * ** 2005*** 2006**** * As adjusted ** Excludes $16.5M asset impairment charge and non-cash equity compensation expense *** Excludes $30.3M IPR&D charge, $2.5M asset impairment charge and non-cash equity compensation expense **** Excludes non-cash equity compensation expense and a $4.7M non-cash impairment loss on the Company s investment in Novocell

43 Investment Highlights Demonstrated leadership and expertise in the development of surface modification and drug delivery technologies Unique opportunity to exploit convergence of drugs and medical devices; expanding to include polymer based drug delivery Partner of choice for the world's most renowned ophthalmology, cardiology, pharmaceutical, and biotechnology companies Broad portfolio of proprietary platforms enables development, manufacture, and commercialization of breakthrough products Making progress moving up product development value chain Consistent track record of execution driven by a strong, sustainable business model

44