MARKETING WITH COWEN AND COMPANY. Germain Lamonde Chairman, President & CEO June 30, 2016

|

|

|

- Tabitha Francis

- 5 years ago

- Views:

Transcription

1 MARKETING WITH COWEN AND COMPANY Germain Lamonde Chairman, President & CEO June 30, 2016

2 FORWARD-LOOKING STATEMENTS Certain statements in this presentation, or given in response to your questions, may constitute forward-looking statements within the meaning of the Securities Act of The Private Securities Litigation Reform Act of 1995 provides safe-harbors for such forward-looking statements and we intend that any forward-looking statements made today be subject to the safe harbors. We caution you that any forward-looking statements are just predictions. They are not guarantees of future performance and involve risks and uncertainties. Actual results may differ materially from those projected in forward-looking statements and we invite you to review the company s most recent filings with the Securities and Exchange Commission or Canadian securities commissions for a discussion of the factors at risk. These forward-looking statements speak only as of the date of this presentation and, unless required by law or applicable regulations, we will not be reviewing or updating the material that is contained herein. For a reconciliation of adjusted EBITDA to net earnings, refer to the Q press release or the Non-IFRS Measures section on EXFO s website. All amounts in millions of US dollars, except otherwise noted. 2

3 EXFO BY NUMBERS LEADER WIRELESS LEADERSHIP 30% $222M IN PORTABLE OPTICAL TESTING OF TOTAL BOOKINGS IN FY 2015 FY 2015 SALES. GLOBAL NO.2 IN PORTABLE TELECOM T&M SHAREHOLDER VALUE DIVERSIFIED GLOBAL $25.5M CASH RETURNED TO SHAREHOLDERS VIA SHARE REPURCHASE PLANS GEOGRAPHICAL SALES FOR FY EMPLOYEES IN 25 COUNTRIES 3

4 LEADER IN PORTABLE TEST MULTI -TECHNOLOGY PLATFORMS WORLD NO. 1 IN OPTICAL TEST SIMPLIFICATION & AUTOMATION 4

Test")

5 TESTFLOW: FIELD TEST AUTOMATION Drives efficiency of network operator processes; M&P pushed out to platforms via Cloud Ensures compliancy, right the first time, test consistency and test result integrity (no cheating) Test results automatically stored in EXFO Xtract Ideal for FTTA, FTTH, small cell, DAS rollouts Runs on all FTB test platforms and modules 5

6 LEADER IN SERVICE ASSURANCE FULL END-TO-END SOLUTION PORTFOLIO CONVERGED & VIRTUALIZED IP SERVICES OVER 100 DEPLOYMENTS WORLDWIDE 6

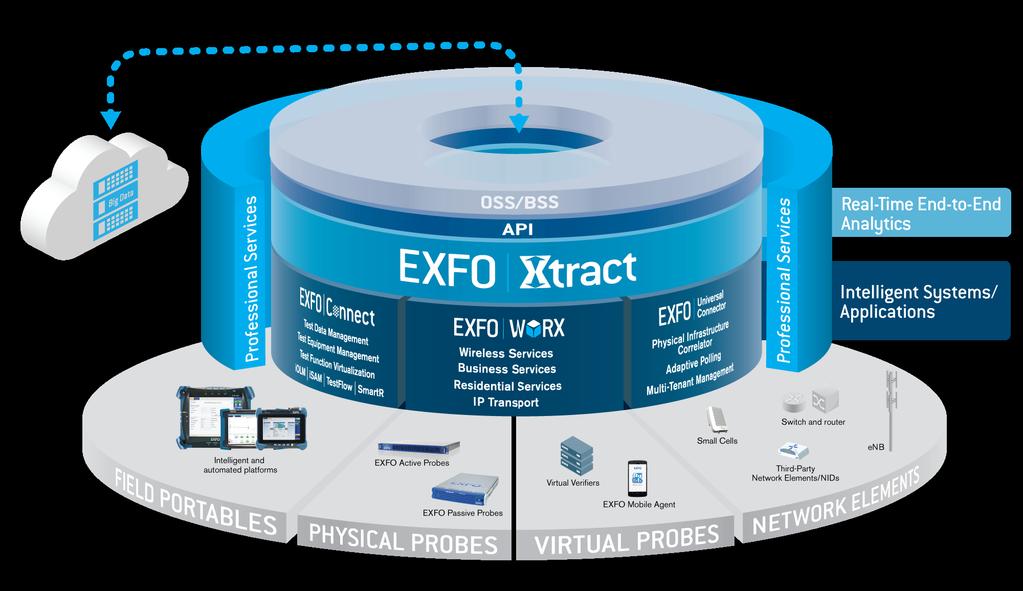

7 EXFO BLUEPRINT 7

")

8 CONSUMER AND BUSINESS TRENDS COMMUNICATION SERVICES VIDEO AUGMENTED REALITY CONNECTED CARS HEALTHCARE INTERNET OF THINGS MOBILITY BROADBAND CLOUD By B mobile subscribers 7.7B mobile broadband subscribers 28B connected devices 10X mobile data traffic growth (from 2015) Source: Ericsson Mobility Report, November

9 MAJOR OPPORTUNITIES FOR EXFO FIBER EVERYWHERE FIELD AUTOMATION QoE + E2E VISIBILITY High-Speed, NFV, Cloud, Data Centers rich in the core deeper in access to-the-home to-the-antenna Operational efficiency Deploy services faster Reduce time-torevenue QoE and retention Reduce service costs Prioritize and predict Simplify operations NFV + H/W co-exist Service complexity Operational cost QoE and retention TEST ORCHESTRATION AND PERFORMANCE INTELLIGENCE SOLUTIONS World No.1 in portable test Consistent share gains Frost & Sullivan Market Leadership Award for 2015 Major new offerings EXFO Connect penetration iolm, FIP, etc. TestFlow process automation Wins at tier-1 MNO more to come Active/Passive + analytics Both NFV + HW-centric NFV driving active SA Xtract: Major wins & funnel NFV ready for deployment 100G+ growth (labs & field) Web-scale + data centers Driving active/analytics opportunities 9

10 GROWTH STRATEGY TOP-LINE DRIVEN: BOLSTER SALES AND GROSS MARGIN TRANSFORM Into a solutions partner. Customers seeking E2E solutions to enhance network performance and service experience quality. INCREASE Wireless presence. Bookings to wireless customers reached 30-32% of total bookings in FY EXPAND Share of wallet with tier-1 network operators. Top-15 operators account for lion s share of capital spending. ACCELERATE Penetration of data center, Cloud and web-scale operator markets. Web-scale operators spending at a faster rate than network operators. 10

TOTAL TAM")

11 TELECOM MARKET PHYSICAL (Optical & Access) PROTOCOL (Wireless, T&D, SA, Analytics) TOTAL TAM $815 M $4.3 B $5.1 B SAM $495 M $2.4 B $2.9 B Market growth rate 0-5% 10-15% Single-digit Sales FY 2015 $144.1 M $80.6 M $224.7 M * Gross margin profile 55-60% 70-75% 63%-65% Major competitors *Excludes losses on FX contracts. Viavi, Anritsu Viavi, IXIA, Netscout PROTOCOL TO DRIVE REVENUE AND EARNINGS GROWTH 11

12 PHYSICAL-LAYER SOLUTIONS PORTABLE OPTICAL No. 1 player with >34% market share Market dominance in OTDR testing Key differentiator: iolm software Market leader in dispersion testing Unmatched product breadth & depth COPPER ACCESS Most advanced product portfolio for high-speed copper links MaxTester secured contract wins with several tier-1 operators Supports pair bonding, vectoring and G.fast (up to 1 Gbit/s) 12

SERVICE ASSURANCE & ANALYTICS")

13 PROTOCOL-LAYER SOLUTIONS TRANSPORT AND DATACOM Multi-service analyzers for SONET/SDH, OTN and Ethernet rates from 10M to 100G Comprehensive portfolio for wireless backhaul and fronthaul Pioneered new standard for Ethernet testing (EtherSam) SERVICE ASSURANCE & ANALYTICS SOFTWARE Probe-based systems targeted at medium to large network operators E2E solutions with fully integrated active/passive monitoring and infrastructure polling to assure SLAs Real-time analytics for unmatched network performance and service experience visibility WIRELESS Network simulators: Large-scale emulation of IMS, WebRTC subscriber sessions to test routers, gateways and session border controllers 13

14 Q HIGHLIGHTS Sales increased 5.4% YoY to $60.9 M Bookings slightly up 0.8% YoY to $59.7 M Gross margin 1 reached 60.8% Adjusted EBITDA 2 improved 18.8% YoY to $5.3 M Cash position of $46.3 M and no debt 1 Gross margin before depreciation and amortization is a non-ifrs measure and represents sales less cost of sales, excluding depreciation and amortization. 2 Adjusted EBITDA represents net earnings before interest, income taxes, depreciation and amortization, stock-based compensation costs and foreign exchange gain. 14

15 STRONG VALUE PROPOSITION WHY INVEST? History of market-share gains Captured market share in growth and downward markets Well positioned for key growth drivers 3G, 4G/LTE, wireless backhaul, small cells, DAS, RRH, FTTx, 100G Balancing sales growth and profitability Raised adjusted EBITDA target of $20 M by $2 M for FY 2016 Solid balance sheet Cash position of $46.3 M and no debt as at May 31, 2016 Experienced and disciplined management team Averaging >15 years of experience in sales, marketing, R&D, manufacturing, finance, HR 1 Adjusted EBITDA represents net earnings before interest, income taxes, depreciation and amortization, stock-based compensation costs and foreign exchange gain or loss. 15