Investor Roadshow New York Northcoast Research. March 18, 2015

|

|

|

- Sydney Page

- 5 years ago

- Views:

Transcription

1 Investor Roadshow New York Northcoast Research March 18,

2 Safe Harbor Statement The information provided in this presentation (both written and oral) relating to future events are subject to risks and uncertainties, such as competition; changing market and economic conditions; currency fluctuations; changes in laws and regulations, including tax laws, and other factors discussed in the company s SEC filings. These documents contain and identify important factors that could cause actual results to differ materially from those contained in our projections or forwardlooking statements. 2

3 3

Managed Solutions Contingent Workforce Outsourcing (CWO) Executive Coaching and Development Global")

4 Portfolio of Solutions Commercial Staffing Office Services Light Industrial Electronic Assembly Marketing Contact Center Educational Services Professional & Technical Staffing Science Engineering IT Finance Law Healthcare Creative Services Revenue 69% 21% 61% of GP 23% of GP 11% 16% of GP Outsourcing & Consulting Recruitment Solutions Recruitment Process Outsourcing (RPO) Project Solutions Business Process Outsourcing (BPO) Managed Solutions Contingent Workforce Outsourcing (CWO) Executive Coaching and Development Global Consulting 4

5 Kelly s Strategy: 2015 Pursue High-Margin PT Aggressively Grow OCG Maintain Commercial Core Capture Perm Placement Control Expenses 5

Realigned PT recruiters by niche (vs.")

6 2014 Investment Scorecard U.S. Local PT Model Created national recruiting centers led by specialty recruiters (vs. ops leaders) Realigned PT recruiters by niche (vs. geography) Hired additional niche PT sales resources Completed customized training and new performance standards for all PT recruiters/sales staff Talent Supply Chain Expanded IC/Statement of Work solution to meet increased demand for projectbased work Developed supply chain analytics to provide market insight to customers Closed the gap in our ability to design truly global solutions across 50+ countries U.S. Large Account Model Completed transition of targeted large accounts into centralized model Increased number of specialty recruiters Implemented aggressive performance requirements for recruiters Aligned recruiting and sales verticals to drive rapid PT growth Technology Updates Improved billing process for large accounts using OCG Completed Phase 1 of revamped frontoffice system Put non-critical updates on hold to control expenses 6

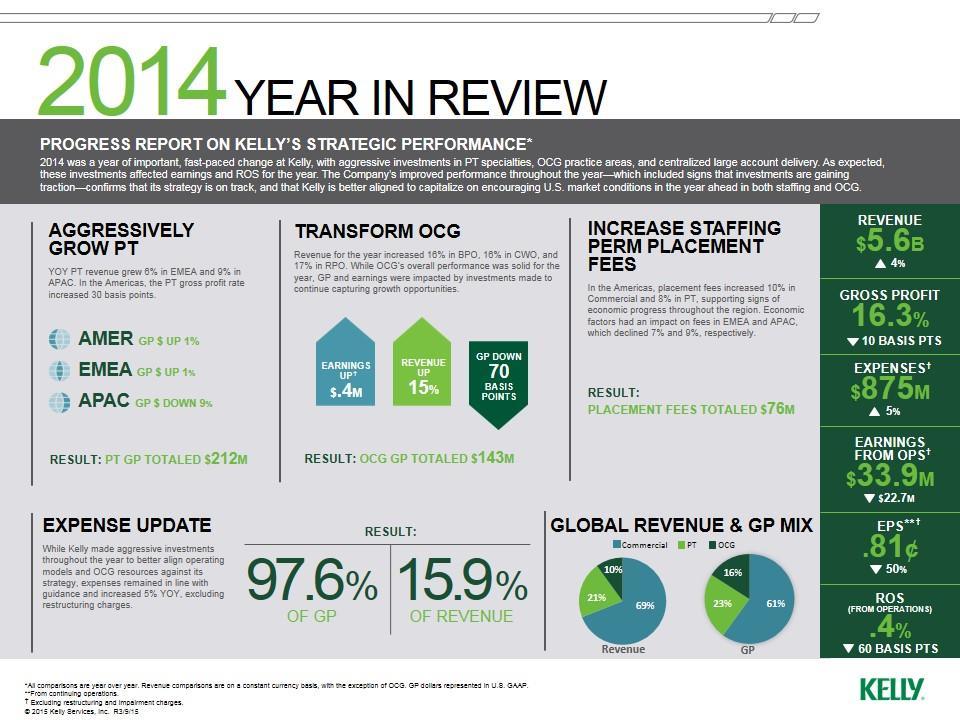

7 2014 Restructuring Plan Streamlined U.S. Operations by closing 52 U.S. branches Simplified management structure at all levels Optimized large account delivery structure Simplified world headquarters operations Continued to align OCG more efficiently against ROI = $35M taken out of 2015 cost base 7

8 Local Account PT Growth Strategy Focus on markets where we re most likely to succeed Use niche-specific sales teams to win higher-margin PT business Use national network of specialty recruiters to create higherskilled talent pipelines in IT, Engineering, Science, Finance - Strong communities of product-dedicated recruiters - Proven expert leaders for all specialties - Proactive vs. reactive recruiting approach - Clear process for attracting and retaining top PT talent - Aggressive metrics for tracking recruiter performance 8

9 Large Account PT Growth Strategy Optimize our centralized model More than $1B revenue now centralized Streamlined processes and service delivery Efficiencies of scale, improved productivity Leverage relationships with established Kelly clients - Visibility into higher-margin PT opportunities - Recruiting and sales verticals aligned to drive PT growth Diversify PT portfolio across numerous large accounts - Reduces exposure to volatility Increase PT fill rates in vendor-neutral accounts - Higher number of PT orders flowing to Kelly through OCG-managed programs 9

10 OCG Growth Strategy Expand talent supply chain solutions - Meet growing need for Independent Contractors/Statement of Work o Meet increased demand for project-based solutions - Deliver supply chain analytics o Provide customers market insights into labor supply & demand - Apply our global supply chain expertise o Provide solutions customized to the regulatory requirements of 50+ countries Leverage opportunities within existing large accounts - Large companies looking for holistic talent management solutions Apply a talent supply chain management approach - Creates opportunities across entire spectrum of workforce solutions 10

PROCUREMENT Full Time Employees Alumni, Retirees and Interns 2012 2015 Kelly Services, Inc.")

11 Talent Supply Chain Management CORPORATE STRATEGIC PLAN Temporary Staff OPERATIONS Independent Contractors / Freelancers HUMAN RESOURCES WORKFORCE ANALYTICS STRATEGIC WORKFORCE PLANNING Talent Supply Chain Management Service Providers (SOW) PROCUREMENT Full Time Employees Alumni, Retirees and Interns Kelly Services, Inc. 11

12 Q1 **

13 Q1 **

14 OCG Growth (in millions) OCG Earnings from Operations $12 $10 $9.7 $8 $6 $6.0 $6.6 $4 $4.0 $3.2 $3.6 $2 $- $(2) $(4) $0.8 $1.7 $1.8 $1.2 $0.5 $0.9 $0.0 -$0.8 -$0.2 -$2.4 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 *Excluding Restructuring & Impairment Charges. 14

15 OCG Growth (in millions) $45.0 OCG Gross Profit 42.3 $40.0 $35.0 $34.8 $36.5 $35.8 $30.0 $29.2 $32.6 $32.9 $25.0 $27.7 $20.0 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 15

16 2015 Outlook Revenue up 6% - 8% YOY in constant currency Gross Profit relatively flat SG&A up 4% - 5% YOY Annual tax rate expected to be in the low 20% range, assuming renewal of Work Opportunity Credits; If WOC is not renewed, our rate is expected to be 20 percentage points higher 16

17 Q Outlook Revenue up 6% - 7% YOY in constant currency Gross Profit slightly down YOY and flat sequentially SG&A up 3% - 4% YOY 17

18 Operations Summary: Q Kelly Services Sales $ 1,425 GP $ 233 Expenses $ 224 Profit $ 9 ROS 0.6% Americas EMEA APAC OCG Sales $ 927 GP $ 137 Expenses $ 114 Profit $ 23 Sales $ 249 GP $ 39 Expenses $ 36 Profit $ 3 Sales $ 103 GP $ 15 Expenses $ 13 Profit $ 2 Sales $ 165 GP $ 42 Expenses $ 33 Profit $ 10 ROS 2.5% ROS 1.1% ROS 2.1% ROS 5.8% (in $millions USD; excluding restructuring) 18

19 Revenue by Quarter (in billions) $1.8 $1.6 $ $ $ $0.8 $0.6 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q

26.")

20 Constant Currency Revenue Growth by Segment 30% 25% (Q4 2014) 26.9% 20% 15% 10% 9.3% 9.7% 11.9% 5% 5.7% 2.7% 0% -5% Total -0.2% Americas -2.4% EMEA APAC OCG Commercial PT Commercial PT Commercial PT 20

21 Staffing Fee Income by Quarter (in millions) $30 $26 $26 $25 $20 $15 $23 $21 $23 $21 $19 $20 $18 $10 $5 $0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q

22 Gross Profit Rate by Quarter 20% 18% 16% 15.8% 15.8% 16.0% 16.1% 16.5% 16.3% 16.8% 16.2% 16.5% 16.1% 16.4% 16.7% 16.7% 16.2% 16.1% 16.3% 14% 12% 10% 8% 6% 4% 2% 0% Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q

23 Expense by Quarter (in millions) $250 $200 $197 $212 $208 $222 $214 $224 $150 $176 $100 $50 $0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q *Excluding Restructuring, Impairment & Certain Litigation Charges. 23

24 Return on Sales by Quarter (in millions) 2.0% 1.8% 1.8% 1.6% 1.4% 1.2% 1.5% 1.3% 1.0% 0.8% 0.8% 0.6% 0.4% 0.2% 0.5% 0.4% 0.5% 0.7% 0.4% 0.6% 0.0% Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q *Excluding Restructuring, Impairment & Certain Litigation Charges. 24

25 Comparison of Gross Profit & Expense: Fourth Quarter (in millions; in constant currency) $300 $7.8 $9.0 $250 $231.5 $239.3 $221.6 $230.6 $200 $150 $100 $50 $ *Excluding Restructuring Gross Profit Expense*

26 Cash Flows: as of December 28, 2014 (in millions) Net Income/(Loss) $ 23.7 $ 58.9 Other Cash (used in)/from Operating Activities (93.7) 56.4 Capital Expenditures (21.7) (20.0) Free Cash Flow $ (91.7) $ 95.3 Borrowing 63.9 (35.8) Available Cash Flow $ (27.8) $ 59.5 Dividends (7.6) (7.6) Other (5.2) (1.1) Cash (used in)/provided by $ (40.6) $ 50.8 Effect of Exchange Rates (2.0) (1.4) Net Change in Cash $ (42.6) $ 49.4 Cash at Period End $ 83.1 $

27 Balance Sheet: at December 28, 2014 (in millions) Cash $ 83.1 $ Accounts Receivable 1, ,023.1 Other Current Assets Total Current Assets $ 1,288.2 $ 1,236.5 Long Term Assets Total Assets $ 1,917.9 $ 1,798.6 Short Term Debt $ 91.9 $ 28.3 Other Current Liabilities Total Current Liabilities $ $ Other Long Term Liabilities Equity Total Liabilities and Equity $ 1,917.9 $ 1,798.6 Working Capital $ $ Net Cash $ (8.8) $ 97.4 Debt-to-Total Capital 9.9% 3.3% 27

28 Kelly Services: Company Contacts George Corona Executive Vice President & Chief Operating Officer Olivier Thirot Senior Vice President, Chief Accounting Officer & Controller James Polehna Vice President, Investor Relations & Corporate Secretary kellyservices.com 28