Benchmarking Report Share, Compare, Validate SAMPLE. Year: 2017 Your Organization Date

|

|

|

- May Skinner

- 6 years ago

- Views:

Transcription

1 Benchmarking Report Share, Compare, Validate Year: 2017 Your Organization Date

2 Benchmarking Tier 1: Your Organization Benchmarking Tier 2: Services Benchmarking Tier 3: Services $1B to $5B Benchmarking Tier 4: Services & Staff Size 1 to 5 Benchmarking Tier 5: Universe Terms and Conditions This report contains confidential data and is for the exclusive use of your organization. Distribution to other companies is strictly prohibited. By accepting this document you are consenting to be bound by an agreement between your organization and the Institute of lntemal Auditors (The IIA). Unauthorized reproduction or distribution of this document, or any portion of it, may result in severe civil or criminal penalties. Your suggestions for improvement are always welcome and can be submitted via to AIS@theiia.org. Thank you for your continued participation in the Audit Intelligence Suite Benchmarking Report.

3 Table Of Contents Section 1: Demographic Information Page 1 Respondents by Tier Group... Page 2 Demographic Information: Financial... Page 3 Respondents by Expense Class... Page 4 Demographic Information: Employees... Page 5 Respondents by Industry... Page 6 Organizational Demographics... Page 7 Organizational Demographics... Page 8 Sarbanes-Oxley... Page 9 Section 2: Summary Information Page 10 Summary Information (Tier 1)... Page 11 Summary Information (Tier 2)... Page 12 Summary Information (Tier 3)... Page 13 Summary Information (Tier 4)... Page 14 Summary Information (Tier 5)... Page 15 Revenues and Assets Per Auditor... Page 16 Expenses and Employees Per Auditor... Page 17 Section 3: Internal Audit Costs Page 18 Summary of Audit Costs... Page 19 Salary and Bonuses as % of Total Audit Costs (Excl. Benefits & Costs)... Page 20 Salary and Bonuses as % of Total Audit Costs (Incl. Benefits & Costs)... Page 21 Benefits as a Percentage of Total Audit Costs... Page 22 Travel and Training as % of Total Audit Costs (Excl. Benefits & Costs)... Page 23 Travel and Training as % of Total Audit Costs (Incl. Benefits & Costs)... Page 24 Total Costs per Auditor... Page 25 Total Costs per Auditor (with and without Travel)... Page 26 Travel and Training Costs per Auditor... Page 27 Section 4: Internal Audit Staffing Page 28 Internal Audit Staff Profile... Page 29 Change in Internal Audit Staff Size... Page 30 Summary of Professional Audit Staff by Function... Page 31 General and IT Auditors as a Percentage of Total Auditors... Page 32 Fraud and ESH Auditors as a Percentage of Total Auditors... Page 33 Other Compliance Auditors as a Percentage of Total... Page 34 Presence of Dedicated IT Audit Group... Page 35 Level of Education Sought for Auditors... Page 36 Level of Education Sought for Auditors Continued... Page 37 Internal Audit Experience of Auditors... Page 38 Relevant Non-Internal Audit Experience of Auditors... Page 39 Industry Experience of Auditors... Page 40 Staff with Professional Designation as Percent of Total Staff... Page 41 Percent of Staff with Professional Designations... Page 42 Professional Designation Mix... Page 43 CIA Designation... Page 44 Internal Audit Hiring Practices... Page 45 Staff Turnover... Page 46 Training Hours... Page 47 Section 5: Sourcing Page 48 Sourced Staff Profile... Page 49 Costs of Purchased Services... Page 50 Level of Sourcing... Page 51 What Internal Audit Activities are Sourced... Page 52 Percentage of Audit Areas Sourced... Page 53 Sourced Hours and Fees... Page 54 Fees For Purchased Services... Page 55 Future Reliance on Sourcing... Page 56

4 Section 6: External Audit Page 57 External Audit... Page 58 Total IA Hours Spent on External Audit... Page 59 External Audit Fees as Percentage of Total Revenues, Assets, and Expenses... Page 60 Section 7: Internal Audit Oversight Page 61 Section 7.1: Internal Audit Oversight - Chief Audit Executive Page 62 CAE Administrative Reporting Line... Page 63 CAE Functional Reporting Line... Page 64 Title of Chief Audit Executive... Page 65 Responsibilities of Chief Audit Executive... Page 66 Section 7.2: Internal Audit Oversight - Audit Committee Page 67 Audit Committee... Page 68 Audit Committee Chair... Page 69 Audit Committee Chair... Page 70 Private Sessions with Audit Committee... Page 71 Presence of Audit Committee Charter... Page 72 Responsibilities of Audit Committee... Page 73 Information Shared with Audit Committee... Page 74 Professional Development of Audit Committee Provided by Internal Audit... Page 75 Evaluations of Audit Committee and Charter... Page 76 Expertise Present on Audit Committee... Page 77 Section 8.2: Risk Assessments Page 89 Presence of Formal Risk Assessment Process for Internal Audit... Page 90 Frequency of Internal Audit Risk Assessment... Page 91 Factors Influencing Risk Assessment... Page 92 Presence of Engagement Level Risk Assessments... Page 93 Engagement Level Risk Assessments... Page 94 Section 9: Audit Implementation / Life Cycles / Reporting Page 95 Allocation of Audit Staff Time... Page 96 Audit Life Cycle... Page 97 Audit Life Cycle - Reporting... Page 98 Tools and Techniques Utilized on Audits... Page 99 Audit Engagement Reporting... Page 100 Section 9.1: Observations and Follow-Up Audits Page 101 Audit Follow-Up Activities... Page 102 Days Outstanding for Open Items... Page 103 Opinion Activities... Page 104 Section 10: Performance Management Page 105 Presence of Formal Quality Assurance and Improvement Program... Page 106 Section 10.1: Internal Quality Assessments Page 107 Frequency of Internal Quality Assessments... Page 108 Internal Quality Assessments... Page 109 Section 8: Risk Assessment and Audit Planning Page 78 Section 10.2: External Quality Assessments Page 110 Completion of External Quality Assessment... Page 111 Section 8.1: Audit Planning Page 79 Obstacles of External Quality Assessment... Page 112 Audit Performance... Page 80 Performance of External Quality Assessments... Page 113 Percent of Audits Planned Actually Performed... Page 81 Results of External Quality Assessment Shared With... Page 114 Number of Unplanned Audits... Page 82 Audits Per Auditor... Page 83 Allocation of Audit Plan... Page 84 Percent of Total Hours for Unallocated Time... Page 85 Percent of Management Requests Completed... Page 86 Type of Audit Plan... Page 87 Years Covered By Audit Plan... Page 88 Section 11: Subscribers By Industry Group Page 115

5 Section 1: Demographic Information

6 Respondents by Tier Group Respondents Your Organization 1 Services 34 Services $1B to $5B 11 Services & Staff Size 1 to 5 10 Universe 333 Page 2

7 Demographic Information: Financial Page 3

8 Respondents by Expense Class Page 4

9 Demographic Information: Employees Page 5

10 Respondents by Industry Value Aerospace and Defense 1% Agriculture, Forestry, and Fisheries 2% Chemical/Drug 2% Communications/Telecommunications 4% Engineering/Construction 2% Education 3% Energy, Oil & Gas, and Mining 10% Financial Services/Banking/Insurance 36% Government 11% Healthcare 6% Manufacturing 17% Real Estate 2% Services 10% Technology 6% Transportation 4% Utilities 10% Wholesale/Retail 8% Page 6

11 Organizational Demographics Page 7

12 Organizational Demographics Page 8

13 Sarbanes-Oxley Page 9

14 Section 2: Summary Information

15 Summary Information(Your Organization) Under $500 Million Revenues Revenues Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Revenues EA Fees AS % of Revenues $500 Million - $1 Billion $1 Billion - $5 Billion $5 Billion - $15 Billion $5,000,000,000 1, $325,000 $50, % 0.001% $15 Billion - $25 Billion Over $25 Billion Assets Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Assets EA Fees AS % of Assets Under $500 Million $500 Million - $1 Billion $1 Billion - $5 Billion $5 Billion - $15 Billion $5,000,000,000 1, $325,000 $50, % 0.001% $15 Billion - $25 Billion Over $25 Billion Assets Under $500 Million Expenses Expenses Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Expenses EA Fees AS % of Expenses $500 Million - $1 Billion $1 Billion - $5 Billion $4,000,000,000 1, $325,000 $50, % % $5 Billion - $15 Billion $15 Billion - $25 Billion Over $25 Billion Page 11

16 Summary Information(Services) Revenues Revenues Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Revenues EA Fees AS % of Revenues Under $500 Million $294,201,808 1, $699,016 $256, % % $500 Million - $1 Billion $746,316,333 2, $1,871,387 $3,087, % % $1 Billion - $5 Billion $2,880,191,000 13, $2,337,601 $3,144, % % $5 Billion - $15 Billion $8,231,548,634 78, $3,522,967 $3,536, % % $15 Billion - $25 Billion $19,276,615, , $5,055,094 $2,100, % % Over $25 Billion $38,419,430, , $12,763,622 $6,854, % % Assets Assets Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Assets EA Fees AS % of Assets Under $500 Million $278,916,779 1, $612,098 $179, % % $500 Million - $1 Billion $684,000,000 1, $714,500 $1,175, % % $1 Billion - $5 Billion $2,069,503,578 6, $1,357,583 $942, % % $5 Billion - $15 Billion $8,771,526,815 52, $3,065,224 $4,033, % % $15 Billion - $25 Billion $20,931,983, , $6,222,067 $2,502, % % Over $25 Billion $715,580,800, , $9,539,689 $8,129, % % Expenses Expenses Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Expenses EA Fees AS % of Expenses Under $500 Million $260,654,903 1, $699,016 $256, % % $500 Million - $1 Billion $747,450,250 2, $2,078,290 $2,702, % % $1 Billion - $5 Billion $2,768,044,272 21, $2,323,873 $3,633, % % $5 Billion - $15 Billion $7,435,941,769 76, $3,847,955 $2,732, % % $15 Billion - $25 Billion $19,158,678, , $5,055,094 $2,100, % % Over $25 Billion $35,950,780, , $12,763,622 $6,854, % % Page 12

17 Summary Information(Services $1B to $5B) Under $500 Million Revenues Revenues Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Revenues EA Fees AS % of Revenues $500 Million - $1 Billion $1 Billion - $5 Billion $2,880,191,000 13, $2,337,601 $3,144, % % $5 Billion - $15 Billion $15 Billion - $25 Billion Over $25 Billion Assets Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Assets EA Fees AS % of Assets Under $500 Million $500 Million - $1 Billion $1 Billion - $5 Billion $2,297,139,500 10, $1,762,117 $1,341, % % $5 Billion - $15 Billion $9,012,638,000 13, $2,906,190 $4,586, % % $15 Billion - $25 Billion Assets Over $25 Billion $3,400,000,000,000 27, $1,228,000 Under $500 Million Expenses Expenses Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Expenses EA Fees AS % of Expenses $500 Million - $1 Billion $793,200,000 4, $2,699,000 $1,547, % 0.195% $1 Billion - $5 Billion $2,550,648,700 14, $2,301,461 $3,343, % % $5 Billion - $15 Billion $15 Billion - $25 Billion Over $25 Billion Page 13

18 Revenues Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Revenues EA Fees AS % of Revenues Under $500 Million $280,434,608 1, $544,484 $287, % % $500 Million - $1 Billion $978,137,000 1, $353,979 $500, % % $1 Billion - $5 Billion $2,383,794,000 14, $1,109,964 $600, % % $5 Billion - $15 Billion $15 Billion - $25 Billion Over $25 Billion Summary Information(Services & Staff Size 1 to 5) Revenues Assets Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Assets EA Fees AS % of Assets Under $500 Million $278,916,779 1, $612,098 $179, % % $500 Million - $1 Billion $500,000, $431,000 $350, % 0.07% $1 Billion - $5 Billion $1,224,514,666 1, $555,268 $584, % % $5 Billion - $15 Billion $15 Billion - $25 Billion Assets Over $25 Billion $3,400,000,000,000 27, $1,228,000 Expenses Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Expenses EA Fees AS % of Expenses Under $500 Million $257,992,525 1, $544,484 $287, % % $500 Million - $1 Billion $922,392,000 1, $353,979 $500, % % $1 Billion - $5 Billion $2,128,565,500 14, $1,109,964 $600, % % $5 Billion - $15 Billion $15 Billion - $25 Billion Over $25 Billion Expenses Page 14

19 Summary Information(Universe) Revenues Revenues Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Revenues EA Fees AS % of Revenues Under $500 Million $253,991,343 1, $897,878 $384, % % $500 Million - $1 Billion $756,414,645 2, $1,604,150 $993, % 0.155% $1 Billion - $5 Billion $2,433,081,368 6, $2,000,834 $1,862, % 0.081% $5 Billion - $15 Billion $8,242,660,398 23, $3,798,189 $3,170, % 0.038% $15 Billion - $25 Billion $18,901,697,736 63, $10,686,439 $5,295, % % Over $25 Billion $64,085,203, , $23,978,729 $15,238, % % Assets Assets Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Assets EA Fees AS % of Assets Under $500 Million $263,813,129 1, $773,614 $401, % % $500 Million - $1 Billion $789,932,888 2, $750,641 $882, % % $1 Billion - $5 Billion $2,823,013,038 6, $1,279,195 $1,135, % 0.046% $5 Billion - $15 Billion $8,585,556,130 21, $2,464,798 $2,388, % % $15 Billion - $25 Billion $19,111,714,833 36, $3,720,241 $4,056, % % Over $25 Billion $288,323,400,046 40, $12,434,859 $7,427, % % Expenses Expenses Total Employees Audit Staff Count Internal Audit Costs Total External Audit Fees IA Costs AS % of Expenses EA Fees AS % of Expenses Under $500 Million $232,226,687 1, $1,249,415 $561, % % $500 Million - $1 Billion $761,762,754 2, $2,127,415 $1,081, % % $1 Billion - $5 Billion $2,549,703,699 10, $2,166,050 $2,085, % % $5 Billion - $15 Billion $8,333,181,230 28, $5,557,691 $3,875, % % $15 Billion - $25 Billion $18,352,084,463 71, $9,788,562 $5,204, % % Over $25 Billion $60,780,502, , $25,582,953 $16,720, % % Page 15

20 Revenues and Assets Per Auditor Page 16

21 Expenses and Employees Per Auditor Page 17

22 Section 3: Internal Audit Costs

23 Salary Bonuses Employee Benefits Travel Training Purchased Services Allocated or Overhead Costs Outsourced Project Work Your Organization $230,000 $20,000 $60,000 $10,000 $5,000 $0 $0 $0 $325,000 Services $1,969,440 $191,039 $481,036 $232,442 $31,710 $367,160 $131,551 $87,070 $3,483,708 Services $1B to $5B Services & Staff Size 1 to 5 Summary of Audit Costs $1,445,869 $162,280 $223,529 $121,947 $16,622 $218,705 $83,760 $80,118 $2,337,601 $330,167 $39,293 $70,479 $42,324 $5,211 $124,640 $9,551 $16,866 $638,530 Universe $2,562,240 $305,248 $676,017 $185,413 $41,095 $351,602 $255,575 $125,709 $4,487,422 Total Page 19

24 Salary and Bonuses as % of Total Audit Costs (Excl. Benefits and Allocated Costs) Page 20

25 Salary and Bonuses as % of Total Audit Costs (Incl. Benefits and Allocated Costs) Page 21

26 Benefits as a Percentage of Total Audit Costs Page 22

27 Travel and Training as % of Total Audit Costs (Excl. Benefits and Allocated Costs) Page 23

28 Travel and Training as % of Total Audit Costs (Incl. Benefits and Allocated Costs) Page 24

29 Total Costs per Auditor Page 25

30 Total Costs per Auditor (with and without Travel) Page 26

31 Travel and Training Costs per Auditor Page 27

32 Section 4: Internal Audit Staffing

33 Internal Audit Staff Profile Chief Audit Executive Directors / Managers Seniors / Supervisors Staff Professional Staff Total Administration / Clerical Your Organization Services Services $1B to $5B Services & Staff Size 1 to 5 In-House Staff Profile Total Positions Universe Sourced Staff Profile Chief Audit Executive Directors / Managers Seniors / Supervisors Staff Professional Staff Total Administration / Clerical Your Organization Services Services $1B to $5B Services & Staff Size to 5 Universe Total Positions Chief Audit Executive Directors / Managers Seniors / Supervisors Staff Professional Staff Total Administration / Clerical Your Organization Services Services $1B to $5B Services & Staff Size 1 to 5 Overall Staff Profile Total Positions Universe Page 29

34 Change in Internal Audit Staff Size Page 30

35 General Internal Auditors Information technology (IT) auditors Fraud auditors Environment, Health, and Safety internal auditors Other compliance auditors Your Organization Services Services $1B to $5B Services & Staff Size 1 to 5 Summary of Professional Audit Staff by Function Universe Other Total Page 31

36 General and IT Auditors as a Percentage of Total Auditors Page 32

37 Fraud and ESH Auditors as a Percentage of Total Auditors Page 33

38 Other Compliance Auditors as a Percentage of Total Page 34

39 Presence of Dedicated IT Audit Group Page 35

40 Level of Education Sought for Auditors Page 36

41 Level of Education Sought for Auditors Continued Page 37

42 Internal Audit Experience of Auditors Page 38

43 Relevant Non-Internal Audit Experience of Auditors Page 39

44 Industry Experience of Auditors Page 40

45 Staff with Professional Designation as Percent of Total Staff Page 41

46 Percent of Staff with Professional Designations Page 42

47 Professional Designation Mix Internal Auditing (such as CIA, MIIA, PIIA) Information Systems Auditing (such as CISA, QiCA, CISM) Your Organization 100% 25% Government Auditing, Finance (such as CIPFA, CGAP, CGFM) Control Self-Assessment (such as CCSA) Public Accounting, Chartered Accountancy (such as CA, CPA, ACCA, ACA) Management, General Accounting (such as CMA, CIMA, CGA) Services 29% 27% 2% 67% 47% 16% Services $1B to $5B 25% 34% 50% 19% Services & Staff Size 1 to 5 57% 39% 67% 53% 40% Universe 33% 26% 18% 17% 41% 17% Your Organization Accounting - technician level (such as CAT, AAT) Fraud Examination (such as CFE) Financial Services Auditing (such as CFSA, CIDA, CBA) Fellowship (such as FCA, FCCA, FCMA) Certified Financial Analyst (such as CFA) Certification in Risk Management Assurance (CRMA) Other Certifications Services 6% 16% 15% 6% 15% 22% Services $1B to $5B 6% 14% 6% 13% 26% Services & Staff Size 1 to 5 38% 33% 35% 33% Universe 9% 19% 14% 15% 7% 19% 27% Page 43

48 CIA Designation Page 44

49 Internal Audit Hiring Practices Page 45

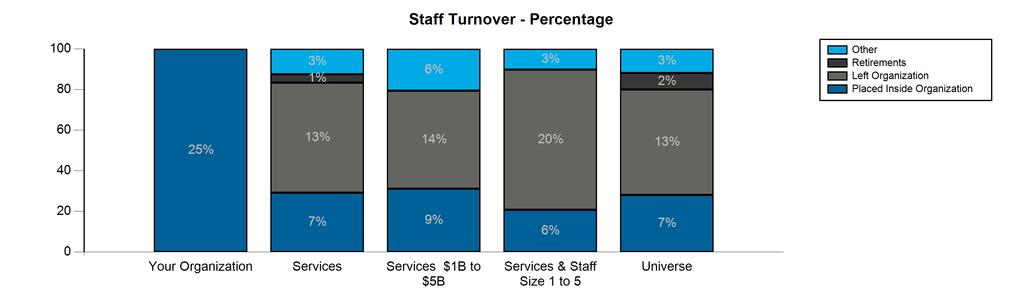

50 Staff Turnover Page 46

51 Training Hours Page 47

52 Section 5: Sourcing

53 Sourced Staff Profile Chief Audit Executive Directors / Managers Seniors / Supervisors Staff Professional Staff Total Administration / Clerical Your Organization Total Positions Services Services $1B to $5B Services & Staff Size 1 to 5 Sourced Staff Profile Universe Page 49

54 Costs of Purchased Services Page 50

55 Level of Sourcing Page 51

56 Your Organization General internal auditing What Internal Audit Activities are Sourced Information technology (IT) auditing Subject matter expertise Fraud auditing Other None Services 47% 47% 32% 6% 15% 29% Services $1B to $5B 64% 45% 55% 27% 36% Services & Staff Size 1 to 5 50% 40% 20% 30% Universe 38% 49% 42% 7% 11% 26% Page 52

57 Percentage of Audit Areas Sourced Page 53

58 Sourced Hours and Fees Page 54

59 Fees For Purchased Services Page 55

60 Future Reliance on Sourcing Page 56

61 Section 6: External Audit

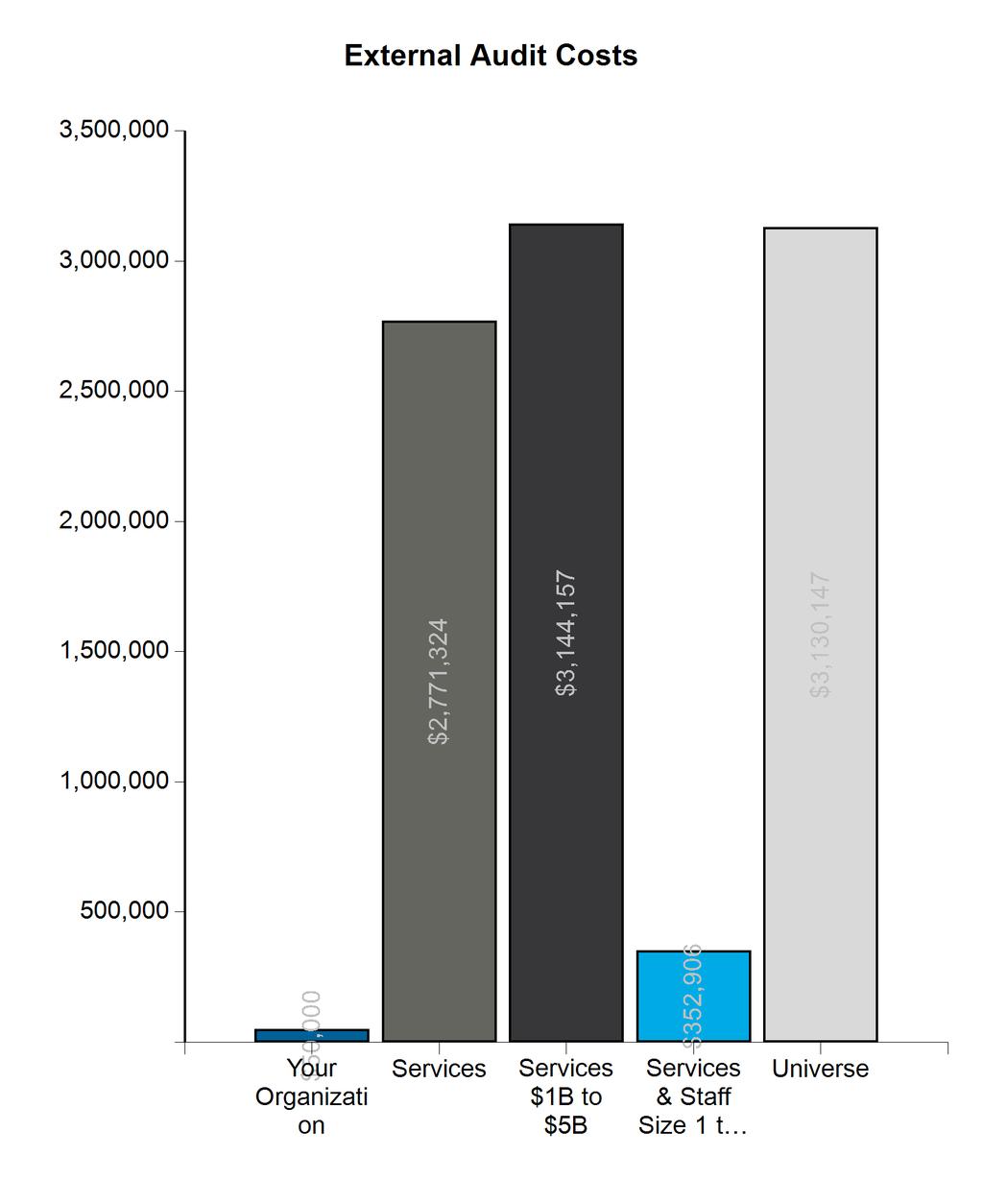

62 External Audit Page 58

63 Total IA Hours Spent on External Audit Page 59

64 External Audit Fees as Percentage of Total Revenues, Assets, and Expenses Page 60

65 Section 7: Internal Audit Oversight

66 Section 7.1: Internal Audit Oversight Chief Audit Executive

67 CAE Administrative Reporting Line Page 63

68 CAE Functional Reporting Line Page 64

69 Title of Chief Audit Executive Page 65

70 Your Organization General internal auditing IT auditing Fraud auditing Forensic investigations 100% 100% 100% Environment, Health, and Safety Compliance Risk management Ethics and business conduct Corporate social responsibility (sustainability) Services 100% 94% 68% 44% 15% 71% 56% 35% 15% 12% Services $1B to $5B Services & Staff Size 1 to 5 Responsibilities of Chief Audit Executive 100% 100% 73% 45% 18% 55% 36% 27% 100% 80% 50% 20% 60% 50% 30% Universe 99% 94% 73% 31% 14% 58% 48% 42% 17% 20% Other Page 66

71 Section 7.2: Internal Audit Oversight Audit Committee

72 Audit Committee Page 68

73 Audit Committee Chair Page 69

74 Audit Committee Meetings Page 70

75 Private Sessions with Audit Committee Page 71

76 Presence of Audit Committee Charter Page 72

77 Responsibilities of Audit Committee Selects the external auditor and reviews the audit fees and the engagement letter Reviews the external auditor's overall audit plan Reviews preliminary annual and interim financial statements Your Organization 100% 100% 100% Reviews results of engagements performed by external auditors, including management letter Approves the charter of the internal audit activity Reassesses and approves a new internal audit activity charter annually Services 94% 91% 88% 91% 88% 68% Services $1B to $5B 91% 91% 91% 82% 91% 73% Services & Staff Size 1 to 5 90% 80% 70% 90% 70% 30% Universe 86% 91% 89% 92% 91% 71% Your Organization Reviews and approves the internal audit activity's plans and resource requirements Directly communicates with the chief audit executive who regularly attends and participates in meetings Reviews evaluations of risk management control and governance processes as reported by the internal auditors Ensures that engagement results are given due consideration and receive distributions of communications Reviews policies on unethical and illegal procedures Reviews financial statements to be transmitted to regulatory agencies Services 94% 94% 88% 71% 53% 76% Services $1B to $5B 91% 91% 91% 64% 64% 73% Services & Staff Size 1 to 5 90% 90% 80% 70% 50% 50% Universe 92% 93% 92% 71% 63% 70% Your Organization Participates in the selection of accounting policies Reviews the impact of new or proposed legislation or regulations Reviews the organization's insurance program Considers evaluations of the effectiveness and efficiency of information systems Review performance of Chief Audit Executive Reviews proposed compensation Services 29% 56% 29% 68% 65% 29% Services $1B to $5B 36% 73% 36% 91% 73% 45% Services & Staff Size 1 to 5 20% 40% 30% 60% 40% 40% Universe 33% 60% 28% 64% 80% 35% Page 73

78 Information Shared with Audit Committee Your Organization Financial and resource budgets Financial variance analysis (actual versus budgeted expenses) Productivity measures Benchmark comparisons versus other companies Organizational structure Coordination of internal and external audit plans Services 82% 42% 48% 61% 82% 76% Services $1B to $5B 91% 55% 36% 55% 82% 73% Services & Staff Size 1 to 5 67% 11% 33% 33% 67% 67% Universe 78% 46% 62% 54% 79% 75% Risk assessment system Overall assessment of the corporate control environment Coverage of key organizational risks Fraud risks Assessment of fraud control environment Your Organization Services 64% 73% 76% 73% 48% Services $1B to $5B 45% 64% 64% 73% 55% Services & Staff Size 1 to 5 56% 56% 56% 67% 33% Universe 69% 72% 78% 61% 49% Your Organization Overall audit plan Percentage of audit plan completed Status of audits performed, outstanding issues, etc. ("Audit Dashboard") Results of monitoring programs concerning compliance with laws, codes of conduct, and ethics Significant findings from engagements Services 97% 88% 94% 70% 97% Services $1B to $5B 91% 82% 82% 73% 91% Services & Staff Size 1 to 5 100% 78% 89% 33% 100% Universe 99% 91% 96% 62% 98% Page 74

79 Professional Development of Audit Committee Provided by Internal Audit Page 75

80 Evaluations of Audit Committee and Charter Page 76

81 Financial Business management Your Organization 100% 100% Expertise Present on Audit Committee Legal Industry-specific knowledge Operational Information technology Fraud/forensics Internal/external audit Services 91% 91% 35% 76% 82% 38% 18% 47% Services $1B to $5B 91% 91% 36% 73% 91% 45% 18% 64% Services & Staff Size 1 to 5 90% 80% 40% 70% 70% 10% 10% 20% Universe 95% 91% 33% 77% 69% 32% 11% 53% Page 77

82 Section 8: Risk Assessment and Planning

83 Section 8.1: Audit Planning

84 Audit Performance Page 80

85 Percent of Audits Planned Actually Performed Page 81

86 Number of Unplanned Audits Page 82

87 Audits Per Auditor Page 83

88 Allocation of Audit Plan Page 84

89 Percent of Total Hours for Unallocated Time Page 85

90 Percent of Management Requests Completed Page 86

91 Type of Audit Plan Page 87

92 Years Covered By Audit Plan Page 88

93 Section 8.2: Risk Assessment

94 Presence of Formal Risk Assessment Process for Internal Audit Page 90

95 Frequency of Internal Audit Risk Assessment Page 91

96 Factors Influencing Risk Assessment Your Organization Degree of manual intervention / degree of automation Confidence in management Extent of major change (reorganization, new product line, etc.) Sensitivity (e.g., image, public relations, etc.) Employee turnover Services 71% 68% 88% 74% 62% Services $1B to $5B 55% 55% 73% 64% 45% Services & Staff Size 1 to 5 50% 70% 80% 80% 40% Universe 69% 62% 92% 69% 65% Fraud significance / potential Inherent risk Environmental factors Competitive pressures Complexity of activities Your Organization Services 82% 82% 56% 44% 79% Services $1B to $5B 73% 82% 36% 45% 73% Services & Staff Size 1 to 5 60% 70% 30% 20% 60% Universe 85% 85% 49% 37% 85% Control environment Time since last audit Continuous auditing - risk and controls assessments Degree of financial materiality Velocity Aggregation of risks Volume of transactions Your Organization Services 82% 85% 35% 91% 26% 68% 62% Services $1B to $5B 82% 82% 36% 82% 18% 64% 55% Services & Staff Size 1 to 5 70% 90% 20% 80% 10% 40% 50% Universe 89% 84% 34% 90% 29% 59% 67% Page 92

97 Presence of Engagement Level Risk Assessments Page 93

98 Engagement Level Risk Assessments Page 94

99 Section 9: Audit Implementation / Life Cycles / Reporting

100 Your Organization Assurance engagements Consulting engagements Fraud investigations Management requests Follow-up audits and activities External audit assistance Chargeable time -- other Non-chargeable time -- training 5% 5% 10% 10% 10% 10% 50% Non-chargeable time -- other Services 53% 5% 3% 5% 4% 5% 5% 3% 6% 10% Services $1B to $5B Services & Staff Size 1 to 5 Allocation of Audit Staff Time 53% 3% 4% 5% 4% 8% 3% 3% 5% 11% 59% 5% 4% 5% 2% 6% 3% 3% 7% 8% Universe 52% 5% 3% 5% 5% 4% 6% 4% 7% 10% Absences Page 96

101 Audit Life Cycle Page 97

102 Audit Life Cycle - Reporting Page 98

103 Tools and Techniques Utilized on Audits Analytical review Balanced scorecard or similar framework Benchmarking Computer-assisted audit techniques (CAAT) Your Organization 100% 100% Continuous auditing Services 85% 15% 53% 56% 21% Services $1B to $5B 73% 45% 55% 27% Services & Staff Size 1 to 5 90% 20% 60% 60% Universe 87% 17% 52% 66% 32% Control self-assessment Data mining Flowchart software Process modeling software Statistical sampling Your Organization Services 26% 59% 59% 9% 50% Services $1B to $5B 9% 82% 64% 45% Services & Staff Size 1 to 5 10% 50% 60% 20% Universe 35% 58% 59% 5% 57% Quality assessment review tools Total quality management techniques Six sigma methodologies Electronic workpaper software Your Organization Services 24% 9% 9% 56% Services $1B to $5B 18% 9% 9% 64% Services & Staff Size 1 to 5 10% 50% Universe 30% 8% 11% 67% Page 99

104 Highlight repeat findings in audit reports Rate observations and findings Audit Engagement Reporting Rank observations and findings based on likelihood and significance Include management action plans Your Organization 100% 100% Provide an overall "score" for the audit Provide an overall opinion on the audit Include positive findings Services 74% 68% 41% 94% 53% 68% 47% Services $1B to $5B 73% 82% 45% 91% 64% 82% 64% Services & Staff Size 1 to 5 50% 40% 20% 80% 30% 50% 30% Universe 79% 81% 55% 95% 41% 77% 58% Page 100

105 Section 9.1: Observations and Follow-Up Audits

106 Audit Follow-Up Activities Page 102

107 Days Outstanding for Open Items Page 103

108 Opinion Activities Page 104

109 Section 10: Performance Management

110 Presence of Formal Quality Assurance and Improvement Program Page 106

111 Section 10.1: Internal Quality Assessments

112 Frequency of Internal Quality Assessments Ongoing Reviews Periodic Reviews Your Organization 100% Services 54% 46% Services $1B to $5B 71% 29% Services & Staff Size 1 to 5 100% Universe 57% 43% Page 108

113 Internal Quality Assessments Engagement supervision Checklists Project budgets Timekeeping systems Your Organization 100% 100% 100% Tools Utilized for Internal Assessments Audit plan completion and summary reports Cost recoveries Interviews and surveys Benchmarking Services 84% 88% 68% 68% 96% 12% 68% 76% Services $1B to $5B 100% 100% 71% 71% 100% 14% 86% 86% Services & Staff Size 1 to 5 83% 67% 50% 50% 83% 67% 50% Universe 91% 89% 64% 64% 89% 14% 58% 64% Results of Internal Assessments Shared With Senior management Audit committee Board of directors External auditors Other appropriate persons outside the activity Your Organization 100% 100% 100% No one Services 72% 84% 20% 56% 24% 8% Services $1B to $5B 71% 86% 14% 57% 57% 14% Services & Staff Size 1 to 5 83% 83% 17% 67% 50% Universe 76% 87% 24% 40% 23% 8% Page 109

114 Section 10.2: External Quality Assessments

115 Completion of External Quality Assessment Page 111

116 Obstacles of External Quality Assessment Page 112

117 Performance of External Quality Assessments Page 113

118 Results of External Quality Assessment Shared With Senior management Audit committee Board of Directors External auditors Other appropriate persons outside the activity Your Organization 100% 100% No one Services 90% 95% 29% 71% 38% Services $1B to $5B 86% 86% 14% 86% 57% Services & Staff Size 1 to 5 100% 100% 50% 83% 33% Universe 91% 95% 34% 62% 32% Page 114

119 Section 11: Subscribers By Industry Group

120 Participants by Industry Group

121 Participants by Industry Group

122 Participants by Industry Group

123 Participants by Industry Group

124 Participants by Industry Group

125 Participants by Industry Group

126 Participants by Industry Group

127 Participants by Industry Group

128 Participants by Industry Group

129 Participants by Industry Group

130 Participants by Industry Group

131 Participants by Industry Group

132 Participants by Industry Group

133 Participants by Industry Group

134 Participants by Industry Group

135 Participants by Industry Group

136 Participants by Industry Group

137 Participants by Industry Group

138 Participants by Industry Group

139 Appendix A - Networking Directory

140 Appendix A - Networking Directory

141 Appendix A - Networking Directory

142 Appendix A - Networking Directory

143 Appendix A - Networking Directory

144 Appendix A - Networking Directory

145 Appendix A - Networking Directory

146 Appendix A - Networking Directory

Internal Audit & the Audit Committee

HCCA Audit & Compliance Committee Conference February 2008 Internal Audit & the Audit Committee Glen C. Mueller, CPA, CIA, CISA, CISM Scripps Health, San Diego, CA VP-Chief Audit & Compliance Executive

HCCA Audit & Compliance Committee Conference February 2008 Internal Audit & the Audit Committee Glen C. Mueller, CPA, CIA, CISA, CISM Scripps Health, San Diego, CA VP-Chief Audit & Compliance Executive

Texas Facilities Commission (TFC) Office of Internal Audit (OIA)

Office of Internal Audit (OIA)") Texas Facilities Commission (TFC) Office of Internal Audit (OIA) Audit Plan for Fiscal Year 2019 August 16, 2018 Amanda Jenami, CPA, CISA, CIA, CFE Chief Audit Executive Robert D. Thomas Chair, TFC Commission

Texas Facilities Commission (TFC) Office of Internal Audit (OIA) Audit Plan for Fiscal Year 2019 August 16, 2018 Amanda Jenami, CPA, CISA, CIA, CFE Chief Audit Executive Robert D. Thomas Chair, TFC Commission

Quality Assurance and Improvement Program (QAIP)

") Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

PULSE OF INTERNAL AUDIT. Navigating an Increasingly Volatile Risk Environment

PULSE OF INTERNAL AUDIT Navigating an Increasingly Volatile Risk Environment Survey Demographics Survey Conducted Oct. 2014 8th consecutive year 370 responses 63% Public/Private companies 84% CAEs and

PULSE OF INTERNAL AUDIT Navigating an Increasingly Volatile Risk Environment Survey Demographics Survey Conducted Oct. 2014 8th consecutive year 370 responses 63% Public/Private companies 84% CAEs and

DAVITA INC. AUDIT COMMITTEE CHARTER

DAVITA INC. AUDIT COMMITTEE CHARTER I. Audit Committee Purpose The Audit Committee (the Committee ) is appointed by the Board of Directors (the Board ) of (the Company ) to assist the Board in fulfilling

DAVITA INC. AUDIT COMMITTEE CHARTER I. Audit Committee Purpose The Audit Committee (the Committee ) is appointed by the Board of Directors (the Board ) of (the Company ) to assist the Board in fulfilling

Risky Business: Internal Audit Best Practices for Community Banks. Presented by: Angela Roberts & Leonard Wagers

Risky Business: Internal Audit Best Practices for Community Banks Presented by: Angela Roberts & Leonard Wagers Our Presenters Angela Roberts, CIA, Clark Schaefer Hackett Angela is an audit consultant

Risky Business: Internal Audit Best Practices for Community Banks Presented by: Angela Roberts & Leonard Wagers Our Presenters Angela Roberts, CIA, Clark Schaefer Hackett Angela is an audit consultant

Audit Committee Charter Matrix

Audit Matrix PURPOSE OF THIS TOOL: Preparing an audit committee charter is often referred to as a best practice and is required for many public companies. It is encouraged for most organizations and required

Audit Matrix PURPOSE OF THIS TOOL: Preparing an audit committee charter is often referred to as a best practice and is required for many public companies. It is encouraged for most organizations and required

Quality Assessment Review. Agenda. The Law Says 11/16/2015. Internal Audit Management November 19-20, 2015

Quality Assessment Review Internal Audit Management November 19-20, 2015 Flerida Rivera-Alsing MBA,CPA, CIA, CFE, CISA, CRMA, CIDA, LIFA Chief Audit Executive State Board of Administration of Florida Agenda

Quality Assessment Review Internal Audit Management November 19-20, 2015 Flerida Rivera-Alsing MBA,CPA, CIA, CFE, CISA, CRMA, CIDA, LIFA Chief Audit Executive State Board of Administration of Florida Agenda

Practice Guide. Developing the Internal Audit Strategic Plan

Practice Guide Developing the Internal Audit Strategic Plan JUly 2012 Table of Contents Executive Summary... 1 Introduction... 2 Strategic Plan Definition and Development... 2 Review of Strategic Plan...

Practice Guide Developing the Internal Audit Strategic Plan JUly 2012 Table of Contents Executive Summary... 1 Introduction... 2 Strategic Plan Definition and Development... 2 Review of Strategic Plan...

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER A. Purpose The purpose of the Audit Committee is to assist the Board of Directors (the Board ) oversight of: the quality and integrity of the Company s financial statements, financial

AUDIT COMMITTEE CHARTER A. Purpose The purpose of the Audit Committee is to assist the Board of Directors (the Board ) oversight of: the quality and integrity of the Company s financial statements, financial

Quality Assurance in Internal Audit. Standard on Internal Audit (SIA) 7

7") Quality Assurance in Internal Audit Standard on Internal Audit (SIA) 7 1 Agenda Introduction Expectations from Internal Audit Quality Assurance Framework Internal Quality Review External Quality Review

Quality Assurance in Internal Audit Standard on Internal Audit (SIA) 7 1 Agenda Introduction Expectations from Internal Audit Quality Assurance Framework Internal Quality Review External Quality Review

List of Key Performance Indicators

Internal Audit Quality: Developing a Quality Assurance and Improvement Program, First Edition. Sally-Anne Pitt. 2014 by John Wiley & Sons, Inc. Published 2014 by John Wiley & Sons, Inc. APPENDIX C List

Internal Audit Quality: Developing a Quality Assurance and Improvement Program, First Edition. Sally-Anne Pitt. 2014 by John Wiley & Sons, Inc. Published 2014 by John Wiley & Sons, Inc. APPENDIX C List

A-9: Audit Committee Effectiveness

A-9: Audit Committee Effectiveness Renée W. Jaenicke, CPA, CIA Renown Health 2011 AHIA Annual Conference www.ahia.org Renown Health and Internal Audit Our Journey Sources and Presentations Please ask questions

A-9: Audit Committee Effectiveness Renée W. Jaenicke, CPA, CIA Renown Health 2011 AHIA Annual Conference www.ahia.org Renown Health and Internal Audit Our Journey Sources and Presentations Please ask questions

Lake County School District. Quality Assurance & Improvement Program. Internal Self-Assessment for. The Internal Audit Department

Lake County School District Quality Assurance & Improvement Program Internal Self-Assessment for The Internal Audit Department Fiscal Year 2017 2018 Completed By: Thomas A. Mock, CIA Date: January 31,

Lake County School District Quality Assurance & Improvement Program Internal Self-Assessment for The Internal Audit Department Fiscal Year 2017 2018 Completed By: Thomas A. Mock, CIA Date: January 31,

FLORIDA STATE UNIVERSITY Office of Inspector General Services Report #17-06

FLORIDA STATE UNIVERSITY Office of Inspector General Services Report #17-06 Self-Assessment with External Independent Validation May 9, 2017 Sam McCall, PhD, CPA, CGMA, CGFM, CIA, CGAP, CIG, Chief Audit

FLORIDA STATE UNIVERSITY Office of Inspector General Services Report #17-06 Self-Assessment with External Independent Validation May 9, 2017 Sam McCall, PhD, CPA, CGMA, CGFM, CIA, CGAP, CIG, Chief Audit

Implementation Guide 1311

Implementation Guide 1311 Standard 1311 Internal Assessments Internal assessments must include: Ongoing monitoring of the performance of the internal audit activity. Periodic self-assessments or assessments

Implementation Guide 1311 Standard 1311 Internal Assessments Internal assessments must include: Ongoing monitoring of the performance of the internal audit activity. Periodic self-assessments or assessments

BIOSCRIP, INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

BIOSCRIP, INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS Statement of Purpose 1. Oversight Responsibility. The purpose of the Audit Committee of the Board of Directors of BioScrip, Inc.,

BIOSCRIP, INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS Statement of Purpose 1. Oversight Responsibility. The purpose of the Audit Committee of the Board of Directors of BioScrip, Inc.,

Why Internal Audit Matters

Why Internal Audit Matters Joseph Mauriello, CPA, CIA, CFE, CISA, CMA, CFSA, CRMA Director, Center for Internal Auditing Excellence The University of Texas at Dallas Financial Executives International

Why Internal Audit Matters Joseph Mauriello, CPA, CIA, CFE, CISA, CMA, CFSA, CRMA Director, Center for Internal Auditing Excellence The University of Texas at Dallas Financial Executives International

SUNEDISON, INC. AUDIT COMMITTEE CHARTER (Adopted October 29, 2008)

") SUNEDISON, INC. AUDIT COMMITTEE CHARTER (Adopted October 29, 2008) I. Purpose The primary purpose of the Audit Committee of the Board of Directors (the Committee ) is to assist the Board of Directors in

SUNEDISON, INC. AUDIT COMMITTEE CHARTER (Adopted October 29, 2008) I. Purpose The primary purpose of the Audit Committee of the Board of Directors (the Committee ) is to assist the Board of Directors in

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017)

") Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

GRANITE CONSTRUCTION INCORPORATED AUDIT/COMPLIANCE COMMITTEE CHARTER

GRANITE CONSTRUCTION INCORPORATED AUDIT/COMPLIANCE COMMITTEE CHARTER Purpose The Audit/Compliance Committee ( Committee ) is appointed by the Board of Directors and its purpose is to assist the Board in

GRANITE CONSTRUCTION INCORPORATED AUDIT/COMPLIANCE COMMITTEE CHARTER Purpose The Audit/Compliance Committee ( Committee ) is appointed by the Board of Directors and its purpose is to assist the Board in

Kentucky State University Office of Internal Audit

Draft for Discussion Only P&P Manual Section - Policy# I. Function and Responsibilities MISSION Mission Statement Definition of Internal Auditing PURPOSE, AUTHORITY, RESPONSIBILITY Audit Charter STANDARDS

Draft for Discussion Only P&P Manual Section - Policy# I. Function and Responsibilities MISSION Mission Statement Definition of Internal Auditing PURPOSE, AUTHORITY, RESPONSIBILITY Audit Charter STANDARDS

AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF THE TORONTO-DOMINION BANK CHARTER

AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF THE TORONTO-DOMINION BANK CHARTER ~ ~ Supervising the Quality and Integrity of the Bank's Financial Reporting ~ ~ Main Responsibilities: overseeing reliable,

AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF THE TORONTO-DOMINION BANK CHARTER ~ ~ Supervising the Quality and Integrity of the Bank's Financial Reporting ~ ~ Main Responsibilities: overseeing reliable,

POLARIS INDUSTRIES INC. BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER Revised January 26, 2017

POLARIS INDUSTRIES INC. BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER Revised January 26, 2017 I. INTRODUCTION AND PURPOSE The primary function of the Audit Committee (the Committee ) is to assist the Board

POLARIS INDUSTRIES INC. BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER Revised January 26, 2017 I. INTRODUCTION AND PURPOSE The primary function of the Audit Committee (the Committee ) is to assist the Board

CABOT OIL & GAS CORPORATION AUDIT COMMITTEE CHARTER

CABOT OIL & GAS CORPORATION AUDIT COMMITTEE CHARTER The Audit Committee is appointed by the Board of Directors to assist the Board of Directors in overseeing (1) the integrity of the financial statements

CABOT OIL & GAS CORPORATION AUDIT COMMITTEE CHARTER The Audit Committee is appointed by the Board of Directors to assist the Board of Directors in overseeing (1) the integrity of the financial statements

Brink's Modern Internal Auditing

Brink's Modern Internal Auditing A Common Body of Knowledge Seventh Edition ROBERT R. MOELLER WILEY John Wiley & Sons, Inc. Preface About the Author xix XXV PART ONE CHAPTER 1 FOUNDATIONS OF MODERN INTERNAL

Brink's Modern Internal Auditing A Common Body of Knowledge Seventh Edition ROBERT R. MOELLER WILEY John Wiley & Sons, Inc. Preface About the Author xix XXV PART ONE CHAPTER 1 FOUNDATIONS OF MODERN INTERNAL

See your auditor clearly. Transparency report: How we perform quality audit engagements

See your auditor clearly. Transparency report: How we perform quality audit engagements February 2014 Table of contents 1) A message from the CEO and Managing Partner Assurance 2 2) Quality control policies

See your auditor clearly. Transparency report: How we perform quality audit engagements February 2014 Table of contents 1) A message from the CEO and Managing Partner Assurance 2 2) Quality control policies

August 14, Dear Ms. Gula:

Department of Internal Audit North End Center, Suite 3200, Virginia Tech 300 Turner Street NW Blacksburg, Virginia 24061 Campus Mail Code: 0328 540-231-5883 Fax: 540-231-4681 www.ia.vt.edu August 14, 2013

Department of Internal Audit North End Center, Suite 3200, Virginia Tech 300 Turner Street NW Blacksburg, Virginia 24061 Campus Mail Code: 0328 540-231-5883 Fax: 540-231-4681 www.ia.vt.edu August 14, 2013

BEST BUY CO., INC. AUDIT COMMITTEE CHARTER

Approved September 2017 BEST BUY CO., INC. AUDIT COMMITTEE CHARTER Purpose The Audit Committee ("Committee") of Best Buy Co., Inc. (the "Company") is appointed by the Board of Directors ("Board") to assist

Approved September 2017 BEST BUY CO., INC. AUDIT COMMITTEE CHARTER Purpose The Audit Committee ("Committee") of Best Buy Co., Inc. (the "Company") is appointed by the Board of Directors ("Board") to assist

REVISED AUDIT PLAN FOR FY 2016 TEXAS FACILITIES COMMISSION

REVISED AUDIT PLAN FOR FY 2016 TEXAS FACILITIES COMMISSION Submitted by THE OFFICE OF INTERNAL AUDIT Amanda G. Jenami, CPA, CISA, CFE, CIA, CGAP, CCSA, MBA Jennifer Wu TABLE OF CONTENTS Introduction...1

REVISED AUDIT PLAN FOR FY 2016 TEXAS FACILITIES COMMISSION Submitted by THE OFFICE OF INTERNAL AUDIT Amanda G. Jenami, CPA, CISA, CFE, CIA, CGAP, CCSA, MBA Jennifer Wu TABLE OF CONTENTS Introduction...1

Independent Validation of the Internal Auditing Self-Assessment

Minnesota State Colleges & Universities Office of Internal Auditing Independent Validation of the Internal Auditing Self-Assessment Final Report March 7, 2007 Reference Number: 2007-03-004 INDEPENDENT

Minnesota State Colleges & Universities Office of Internal Auditing Independent Validation of the Internal Auditing Self-Assessment Final Report March 7, 2007 Reference Number: 2007-03-004 INDEPENDENT

EXTERNAL QUALITY ASSESSMENT OF ORANGE COUNTY S INTERNAL AUDIT DEPARTMENT

EXTERNAL QUALITY ASSESSMENT OF ORANGE COUNTY S INTERNAL AUDIT DEPARTMENT August 27, 2007 Office of Robert E. Byrd, CGFM County Auditor-Controller 4080 Lemon Street P.O. Box 1326 Riverside, CA 92502-1326

EXTERNAL QUALITY ASSESSMENT OF ORANGE COUNTY S INTERNAL AUDIT DEPARTMENT August 27, 2007 Office of Robert E. Byrd, CGFM County Auditor-Controller 4080 Lemon Street P.O. Box 1326 Riverside, CA 92502-1326

INTERNAL AUDIT : THE ROAD AHEAD. CIVIL ACCOUNTS DAY 1 st MARCH 2012

INTERNAL AUDIT : THE ROAD AHEAD CIVIL ACCOUNTS DAY 1 st MARCH 2012 MISSION STATEMENT Develop new paradigms of internal audit for improved transparency and accountability. STRUCTURE OF THE PRESENTATION

INTERNAL AUDIT : THE ROAD AHEAD CIVIL ACCOUNTS DAY 1 st MARCH 2012 MISSION STATEMENT Develop new paradigms of internal audit for improved transparency and accountability. STRUCTURE OF THE PRESENTATION

Internal Audit Appendix: IIA Standards

Accountability Modules Internal Audit Appendix: IIA Standards Return to Table of ontents The following section provides additional detailed steps to examine when evaluating an internal audit function.

Accountability Modules Internal Audit Appendix: IIA Standards Return to Table of ontents The following section provides additional detailed steps to examine when evaluating an internal audit function.

Implementation Guides

Implementation Guides Implementation Guides assist internal auditors in applying the Definition of Internal Auditing, the Code of Ethics, and the Standards and promoting good practices. Implementation

Implementation Guides Implementation Guides assist internal auditors in applying the Definition of Internal Auditing, the Code of Ethics, and the Standards and promoting good practices. Implementation

10/5/2016. Quality Assessment Review. Agenda. What s the purpose of a QAR? Internal Audit Manager Training October 3-4, 2016

Quality Assessment Review Internal Audit Manager Training October 3-4, 2016 Lori Clark CIGA, CCEP, CGAP Compliance & Audit Specialist State University System of Florida Agenda What s the purpose of a QAR?

Quality Assessment Review Internal Audit Manager Training October 3-4, 2016 Lori Clark CIGA, CCEP, CGAP Compliance & Audit Specialist State University System of Florida Agenda What s the purpose of a QAR?

Report on Quality AssuranceAssessment

. Escambia County School District Report on Quality AssuranceAssessment.......... of Internal Audit February 28, 2007 Report on Quality Assurance Assessment Escambia County School District Office of Internal

. Escambia County School District Report on Quality AssuranceAssessment.......... of Internal Audit February 28, 2007 Report on Quality Assurance Assessment Escambia County School District Office of Internal

BIG LOTS, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER

May 2010 BIG LOTS, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER The Audit Committee (the Committee ) is appointed by the Board of Directors (the Board ) of Big Lots, Inc. (the Company ) to assist

May 2010 BIG LOTS, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER The Audit Committee (the Committee ) is appointed by the Board of Directors (the Board ) of Big Lots, Inc. (the Company ) to assist

TRA Internal Audit Fiscal Year 2019 Audit Plan

TRA Internal Audit Fiscal Year 2019 Audit Plan Leslie Nagel, CPA, CEBS, CIA Chief Audit Executive Approved by TRA Audit Comittee April 10, 2018 Approved by TRA Board of Trustees April 11, 2018 TRA Internal

TRA Internal Audit Fiscal Year 2019 Audit Plan Leslie Nagel, CPA, CEBS, CIA Chief Audit Executive Approved by TRA Audit Comittee April 10, 2018 Approved by TRA Board of Trustees April 11, 2018 TRA Internal

Washington State University Office of Internal Audit FY 2015 Audit Plan

Washington State University Office of Internal Audit FY 2015 Audit Plan The purpose of the Audit Plan is to outline audits and other activities the WSU Office of Internal Audit will conduct during fiscal

Washington State University Office of Internal Audit FY 2015 Audit Plan The purpose of the Audit Plan is to outline audits and other activities the WSU Office of Internal Audit will conduct during fiscal

OFFICE OF INTERNAL AUDIT AUDIT MANUAL

OFFICE OF INTERNAL AUDIT AUDIT MANUAL Effective Date: October 31, 2006 Revised Date: October 27, 2016 Introduction The purpose of this manual is to outline the authority and scope of the internal audit

OFFICE OF INTERNAL AUDIT AUDIT MANUAL Effective Date: October 31, 2006 Revised Date: October 27, 2016 Introduction The purpose of this manual is to outline the authority and scope of the internal audit

BUSINESS RISK MANAGEMENT LTD. Proposal for External Quality Assessment of the Internal Audit function against world class best practice

BUSINESS RISK MANAGEMENT LTD Proposal for External Quality Assessment of the Internal Audit function against world class best practice 1. Summary The following proposal outlines the suggested approach

BUSINESS RISK MANAGEMENT LTD Proposal for External Quality Assessment of the Internal Audit function against world class best practice 1. Summary The following proposal outlines the suggested approach

Internal Audit Division FY 17 - Audit Plan Overview

Division FY 17 - Audit Plan Overview Our Value Proposition - Objective Insight and Catalyst for Positive Change delivers value-added services that are catalysts for positive institutional change in governance,

Division FY 17 - Audit Plan Overview Our Value Proposition - Objective Insight and Catalyst for Positive Change delivers value-added services that are catalysts for positive institutional change in governance,

MINDEN BANCORP, INC. AUDIT COMMITTEE CHARTER

MINDEN BANCORP, INC. AUDIT COMMITTEE CHARTER Purpose The Audit Committee (the Committee ) of Minden Bancorp, Inc. (the Company ) is appointed by the Board of Directors to assist the Board in fulfilling

MINDEN BANCORP, INC. AUDIT COMMITTEE CHARTER Purpose The Audit Committee (the Committee ) of Minden Bancorp, Inc. (the Company ) is appointed by the Board of Directors to assist the Board in fulfilling

Supervisory Committee Expectations of Internal Audit

Supervisory Committee Expectations of Internal Audit Alan N. Siegfried, MBA, CPA, CIA, CISA, CRMA, CCSA, CFSA, CGMA, CITP, CBA, CSP Theresa M. Grafenstine, CPA, CIA, CGAP, CISA, CGEIT, CRISC, CGMA June

Supervisory Committee Expectations of Internal Audit Alan N. Siegfried, MBA, CPA, CIA, CISA, CRMA, CCSA, CFSA, CGMA, CITP, CBA, CSP Theresa M. Grafenstine, CPA, CIA, CGAP, CISA, CGEIT, CRISC, CGMA June

Practice Advisory : Internal Audit Charter

Combined PAs Page 1 of 63 Practice Advisory 1000-1: Internal Audit Charter 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be

Combined PAs Page 1 of 63 Practice Advisory 1000-1: Internal Audit Charter 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be

CITIZENS, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER. Adopted November 5, the integrity of the Company s financial statements;

CITIZENS, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER Adopted November 5, 2014 A. Purpose The purpose of the Audit Committee is to assist the Board of Directors oversight of: the integrity of the

CITIZENS, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER Adopted November 5, 2014 A. Purpose The purpose of the Audit Committee is to assist the Board of Directors oversight of: the integrity of the

Hiring and Staff: An Effective Internal Department

2017 ACUIA Region 6 Conference Hiring and Staff: An Effective Internal Department Presented by: Lori Carmichael, CPA Rafael Guijarro, CPA Financial Institutions Group Michigan Texas Florida Insight. Oversight.

2017 ACUIA Region 6 Conference Hiring and Staff: An Effective Internal Department Presented by: Lori Carmichael, CPA Rafael Guijarro, CPA Financial Institutions Group Michigan Texas Florida Insight. Oversight.

Value-Added Internal Audit: Myth or Reality?

Value-Added Internal Audit: Myth or Reality? Istanbul 12 November 2013 Jean-Pierre Garitte, CIA, CCSA, CISA, CFE, RFA Past Chairman of the Board IIA Past President ECIIA Polling question #1 For how long

Value-Added Internal Audit: Myth or Reality? Istanbul 12 November 2013 Jean-Pierre Garitte, CIA, CCSA, CISA, CFE, RFA Past Chairman of the Board IIA Past President ECIIA Polling question #1 For how long

Southern Oregon University Internal Audit Plan Fiscal Year 2017

Southern Oregon University Internal Audit Plan Fiscal Year 2017 Prepared By Ryan Schnobrich Internal Auditor Office of the President 1 P a g e TABLE OF CONTENTS Description Page Cover Page 1 Table of Contents

Southern Oregon University Internal Audit Plan Fiscal Year 2017 Prepared By Ryan Schnobrich Internal Auditor Office of the President 1 P a g e TABLE OF CONTENTS Description Page Cover Page 1 Table of Contents

September 25-27, 2005 Baltimore Marriott Waterfront Baltimore, MD. WorldCom: What Went Wrong and Governance Lessons Learned

WorldCom: What Went Wrong and Governance Lessons Learned Moving Forward Aftermath Rise and Fall of WorldCom Identifying and Reporting the Fraud Auditors, Boards and Management Minimizing Fraud MCI - Moving

WorldCom: What Went Wrong and Governance Lessons Learned Moving Forward Aftermath Rise and Fall of WorldCom Identifying and Reporting the Fraud Auditors, Boards and Management Minimizing Fraud MCI - Moving

NEW YORK LIFE INSURANCE COMPANY AUDIT COMMITTEE MISSION STATEMENT

NEW YORK LIFE INSURANCE COMPANY AUDIT COMMITTEE MISSION STATEMENT I. MISSION AND FUNCTION OF THE AUDIT COMMITTEE A. The mission of the Audit Committee is to assist the Board of Directors (the Board of

NEW YORK LIFE INSURANCE COMPANY AUDIT COMMITTEE MISSION STATEMENT I. MISSION AND FUNCTION OF THE AUDIT COMMITTEE A. The mission of the Audit Committee is to assist the Board of Directors (the Board of

Canada. Internal Audit Charter 1+1. Canadian Nuclear Safety Commission. Office of Audit and Ethics. April 18, 2011

1+1 Commission canadienne de sorete nucleaire Canadian Nuclear Safety Commission Internal Audit Charter Canadian Nuclear Safety Commission Office of Audit and Ethics April 18, 2011 E-DOCS-#371 0602 v2

1+1 Commission canadienne de sorete nucleaire Canadian Nuclear Safety Commission Internal Audit Charter Canadian Nuclear Safety Commission Office of Audit and Ethics April 18, 2011 E-DOCS-#371 0602 v2

Changes to The IIA Standards: What Board Members and Executive Management Need to Know

Changes to The IIA Standards: What Board Members and Executive Management Need to Know Introduction The Institute of Internal Auditors (IIA) is the leading standard- and guidance-setting body for the global

Changes to The IIA Standards: What Board Members and Executive Management Need to Know Introduction The Institute of Internal Auditors (IIA) is the leading standard- and guidance-setting body for the global

Practice Advisory : Quality Assurance and Improvement Program

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

Implementation Guide 1000

Implementation Guide 1000 Standard 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter,

Implementation Guide 1000 Standard 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter,

Review of Duke Energy Florida, LLC Internal Audit Function

Review of Duke Energy Florida, LLC Internal Audit Function MAY 2017 B Y A U T H O R I T Y O F The Florida Public Service Commission Office of Auditing and Performance Analysis Review of Duke Energy Florida,

Review of Duke Energy Florida, LLC Internal Audit Function MAY 2017 B Y A U T H O R I T Y O F The Florida Public Service Commission Office of Auditing and Performance Analysis Review of Duke Energy Florida,

BOARD INTERNAL ORGANIZATION. Audit Committee

Audit Committee Board adoption: The Board amended, which serves as the District s Audit Committee charter. Purpose: The purpose of the Audit Committee is to provide structured, systematic oversight of

Audit Committee Board adoption: The Board amended, which serves as the District s Audit Committee charter. Purpose: The purpose of the Audit Committee is to provide structured, systematic oversight of

BancorpSouth, Inc. and. BancorpSouth Bank. Audit Committee Charter

BancorpSouth, Inc. and BancorpSouth Bank Audit Committee Charter I. Audit Committee Purpose BANCORPSOUTH, INC. AND BANCORPSOUTH BANK CHARTER OF THE AUDIT COMMITTEE OF THE BOARDS OF DIRECTORS The Audit

BancorpSouth, Inc. and BancorpSouth Bank Audit Committee Charter I. Audit Committee Purpose BANCORPSOUTH, INC. AND BANCORPSOUTH BANK CHARTER OF THE AUDIT COMMITTEE OF THE BOARDS OF DIRECTORS The Audit

NATIONAL CINEMEDIA, INC. AUDIT COMMITTEE CHARTER

January 24, 2018 NATIONAL CINEMEDIA, INC. AUDIT COMMITTEE CHARTER There will be a committee of the Board of Directors (the Board ) of National CineMedia, Inc. (the Corporation ) that will be called the

January 24, 2018 NATIONAL CINEMEDIA, INC. AUDIT COMMITTEE CHARTER There will be a committee of the Board of Directors (the Board ) of National CineMedia, Inc. (the Corporation ) that will be called the

1. Same Same. 3. Same. 4. Same. 1. Same. 2. Same.

Chief of Internal Audit: Role 1 and Responsibility Assessment Tool 2 Part of the IFC s Advanced Methodology for Financial Institutions I. Personal Qualification II. General Knowledge and Professional Skills

Chief of Internal Audit: Role 1 and Responsibility Assessment Tool 2 Part of the IFC s Advanced Methodology for Financial Institutions I. Personal Qualification II. General Knowledge and Professional Skills

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF ISRAMCO, INC.

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF ISRAMCO, INC. I. AUDIT COMMITTEE PURPOSE The Audit Committee of the Board of Directors of Isramco, Inc. (the Corporation ) is appointed by the

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF ISRAMCO, INC. I. AUDIT COMMITTEE PURPOSE The Audit Committee of the Board of Directors of Isramco, Inc. (the Corporation ) is appointed by the

Implementation Guide 2050

Implementation Guide 2050 Standard 2050 Coordination and Reliance The chief audit executive should share information, coordinate activities, and consider relying upon the work of other internal and external

Implementation Guide 2050 Standard 2050 Coordination and Reliance The chief audit executive should share information, coordinate activities, and consider relying upon the work of other internal and external

IIA 2015 Worldwide survey of 15,000 internal auditors

IIA 2015 Worldwide survey of 15,000 internal auditors Michael P. Cangemi CPA, retired CISA, CGMA retired Former CFO, CEO & Director; Audit Com Chair Senior Fellow Rutgers CA Lab Senior Advisor/Investor

IIA 2015 Worldwide survey of 15,000 internal auditors Michael P. Cangemi CPA, retired CISA, CGMA retired Former CFO, CEO & Director; Audit Com Chair Senior Fellow Rutgers CA Lab Senior Advisor/Investor

Implementation Guide 1200

Implementation Guide 1200 Standard 1200 Proficiency and Due Professional Care Engagements must be performed with proficiency and due professional care. Revised Standards Effective 1 January 2017 Getting

Implementation Guide 1200 Standard 1200 Proficiency and Due Professional Care Engagements must be performed with proficiency and due professional care. Revised Standards Effective 1 January 2017 Getting

Annual Report to the Audit Committee Internal Audit Division Work Plan and Activity

STAFF REPORT ACTION REQUIRED Annual Report to the Audit Committee Internal Audit Division Work Plan and Activity Date: May 31, 2014 To: From: Wards: Audit Committee Director, Internal Audit All SUMMARY

STAFF REPORT ACTION REQUIRED Annual Report to the Audit Committee Internal Audit Division Work Plan and Activity Date: May 31, 2014 To: From: Wards: Audit Committee Director, Internal Audit All SUMMARY

CREATING A FRAUD RISK ASSESSMENT AND IMPLEMENTING A CONTINUOUS MONITORING PROGRAM

CREATING A FRAUD RISK ASSESSMENT AND IMPLEMENTING A CONTINUOUS MONITORING PROGRAM Compliance professionals around the world are struggling with how to do more with less. In order to provide effective assurance

CREATING A FRAUD RISK ASSESSMENT AND IMPLEMENTING A CONTINUOUS MONITORING PROGRAM Compliance professionals around the world are struggling with how to do more with less. In order to provide effective assurance

Board Audit Committee Training Automation of Audit Function. Anthony Wanyoike TeamMate Consulting East, Central & West Africa

Board Audit Committee Training Automation of Audit Function Anthony Wanyoike TeamMate Consulting East, Central & West Africa Agenda 1. Automation of Audit Function Steps of developing automated Audit Operational

Board Audit Committee Training Automation of Audit Function Anthony Wanyoike TeamMate Consulting East, Central & West Africa Agenda 1. Automation of Audit Function Steps of developing automated Audit Operational

City of Edmonton EXTERNAL QUALITY ASSESSMENT OF THE OFFICE OF THE CITY AUDITOR. September 11, 2015

City of Edmonton EXTERNAL QUALITY ASSESSMENT OF THE OFFICE OF THE CITY AUDITOR September 11, 2015 PREPARED BY: MNP LLP 1500 640 5 th Ave SW Calgary, AB, T2P 3G4 MNP CONTACT: Maggie Kiel, CIA, MBA, ABCP,

City of Edmonton EXTERNAL QUALITY ASSESSMENT OF THE OFFICE OF THE CITY AUDITOR September 11, 2015 PREPARED BY: MNP LLP 1500 640 5 th Ave SW Calgary, AB, T2P 3G4 MNP CONTACT: Maggie Kiel, CIA, MBA, ABCP,

Audit Committee Charter

Audit Committee Charter Purpose The purpose of the Audit Committee (the "Committee") shall be as follows: 1. To oversee the accounting and financial reporting processes of the Company and audits of the

Audit Committee Charter Purpose The purpose of the Audit Committee (the "Committee") shall be as follows: 1. To oversee the accounting and financial reporting processes of the Company and audits of the

2010 Healthcare Internal Auditing Survey

Feature 2010 Healthcare Internal Auditing Survey Conducted by the Association of Healthcare Internal Auditors, Inc. and the Louisiana State University Center for Internal Auditing By Glenn E. Sumners,

Feature 2010 Healthcare Internal Auditing Survey Conducted by the Association of Healthcare Internal Auditors, Inc. and the Louisiana State University Center for Internal Auditing By Glenn E. Sumners,

STARWOOD HOTELS & RESORTS WORLDWIDE, INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

STARWOOD HOTELS & RESORTS WORLDWIDE, INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS Starwood Hotels & Resorts Worldwide, Inc. (the Company ) has determined that it is of the utmost importance

STARWOOD HOTELS & RESORTS WORLDWIDE, INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS Starwood Hotels & Resorts Worldwide, Inc. (the Company ) has determined that it is of the utmost importance

GTT COMMUNICATIONS, INC. AUDIT COMMITTEE CHARTER

GTT COMMUNICATIONS, INC. AUDIT COMMITTEE CHARTER This Audit Committee Charter (this Charter ) was adopted by the Board of Directors (the Board ) of GTT Communications, Inc., a Delaware corporation (the

GTT COMMUNICATIONS, INC. AUDIT COMMITTEE CHARTER This Audit Committee Charter (this Charter ) was adopted by the Board of Directors (the Board ) of GTT Communications, Inc., a Delaware corporation (the

Business Case and Proposal

Business Case and Proposal Formation of an Internal Audit Service for Cambridge City Council, Huntingdonshire District Council and South Cambridgeshire District Council 1.0 Executive Summary 1.1 Cambridge

Business Case and Proposal Formation of an Internal Audit Service for Cambridge City Council, Huntingdonshire District Council and South Cambridgeshire District Council 1.0 Executive Summary 1.1 Cambridge

CHARTER FEDERAL RESERVE BANK OF RICHMOND BOARD OF DIRECTORS AUDIT AND RISK COMMITTEE

CHARTER FEDERAL RESERVE BANK OF RICHMOND BOARD OF DIRECTORS AUDIT AND RISK COMMITTEE Purpose The Audit and Risk Committee (the Committee) is a committee of the Board of Directors (the Board). The Committee

CHARTER FEDERAL RESERVE BANK OF RICHMOND BOARD OF DIRECTORS AUDIT AND RISK COMMITTEE Purpose The Audit and Risk Committee (the Committee) is a committee of the Board of Directors (the Board). The Committee

The University of Texas at San Antonio 2014 External Quality Assessment of the Auditing and Consulting Services Office

www.pwc.com The University of Texas at San Antonio 2014 External Quality Assessment of the Auditing and Consulting Services Office July 9, 2014 Mr. Dick Dawson Chief Audit Executive The University of Texas

www.pwc.com The University of Texas at San Antonio 2014 External Quality Assessment of the Auditing and Consulting Services Office July 9, 2014 Mr. Dick Dawson Chief Audit Executive The University of Texas

AUDIT AND RISK COMMITTEE CHARTER

AUDIT AND RISK COMMITTEE CHARTER Contents Page A. Introduction 1 B. Statement of Policy 1 C. Perspective 1 D. Roles and Responsibilities 2 E. Membership 7 F. Meetings and Schedule of Activities 7 G. Reporting

AUDIT AND RISK COMMITTEE CHARTER Contents Page A. Introduction 1 B. Statement of Policy 1 C. Perspective 1 D. Roles and Responsibilities 2 E. Membership 7 F. Meetings and Schedule of Activities 7 G. Reporting

Assurance Dashboard. Audit added to review controls related to Audit Added Procurement. increased activity due to hurricane Irma 2017 CAT Travel and

1 Page Office of the Internal Auditor Overview of Audit Plan and Plan Changes The OIA continually follows development of risk and monitors delivery of projects listed in the Audit Plan. As we reassess

1 Page Office of the Internal Auditor Overview of Audit Plan and Plan Changes The OIA continually follows development of risk and monitors delivery of projects listed in the Audit Plan. As we reassess

External Quality Assessment of. The City Auditor s Office CITY OF CALGARY MARCH ISC: UNRESTRICTED AC Attachment

ISC: UNRESTRICTED Eternal Quality Assessment of The City Auditor s Office CITY OF CALGARY MARCH 2017 City of Calgary April 7, 2017 1 Table of Contents EXECUTIVE SUMMARY... 3 OPINION AS TO CONFORMANCE TO

ISC: UNRESTRICTED Eternal Quality Assessment of The City Auditor s Office CITY OF CALGARY MARCH 2017 City of Calgary April 7, 2017 1 Table of Contents EXECUTIVE SUMMARY... 3 OPINION AS TO CONFORMANCE TO

CHARTER OF THE AUDIT COMMITTEE NATIONWIDE MUTUAL INSURANCE COMPANY NATIONWIDE MUTUAL FIRE INSURANCE COMPANY NATIONWIDE CORPORATION

CHARTER OF THE AUDIT COMMITTEE NATIONWIDE MUTUAL INSURANCE COMPANY NATIONWIDE MUTUAL FIRE INSURANCE COMPANY NATIONWIDE CORPORATION ESTABLISHMENT The Audit Committees are committees of the Board of Directors

CHARTER OF THE AUDIT COMMITTEE NATIONWIDE MUTUAL INSURANCE COMPANY NATIONWIDE MUTUAL FIRE INSURANCE COMPANY NATIONWIDE CORPORATION ESTABLISHMENT The Audit Committees are committees of the Board of Directors

SMITH & NEPHEW PLC TERMS OF REFERENCE OF THE AUDIT COMMITTEE

SMITH & NEPHEW PLC TERMS OF REFERENCE OF THE AUDIT COMMITTEE MEMBERSHIP 1. Members of the Audit Committee shall be appointed by the Board subject to annual re-election by shareholders at the AGM on the

SMITH & NEPHEW PLC TERMS OF REFERENCE OF THE AUDIT COMMITTEE MEMBERSHIP 1. Members of the Audit Committee shall be appointed by the Board subject to annual re-election by shareholders at the AGM on the

EFFICIENT USE OF AUDIT COMMITTEES

AGENDA EFFICIENT USE OF AUDIT COMMITTEES BRENT YOUNG, CPA JERRY GAITHER, CPA Best practices related to: Audit Committee Process Internal Audit Risk Management 2 AUDIT COMMITTEE PROCESS AND PROCEDURES Audit

AGENDA EFFICIENT USE OF AUDIT COMMITTEES BRENT YOUNG, CPA JERRY GAITHER, CPA Best practices related to: Audit Committee Process Internal Audit Risk Management 2 AUDIT COMMITTEE PROCESS AND PROCEDURES Audit

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

Financial CIA-I. Certified Internal Auditor (CIA) Download Full Version :

Download Full Version :") Financial CIA-I Certified Internal Auditor (CIA) Download Full Version : http://killexams.com/pass4sure/exam-detail/cia-i QUESTION: 225 To identify those components of a telecommunications system that

Financial CIA-I Certified Internal Auditor (CIA) Download Full Version : http://killexams.com/pass4sure/exam-detail/cia-i QUESTION: 225 To identify those components of a telecommunications system that

Joint Report of PCC s Chief Finance Officer and Chief Constable s Director of Resources. Joint Audit Committee s Draft Annual Report for 2013/14

To: The Members of the Joint Audit Committee Meeting: 18 th September 2014 Joint Report of PCC s Chief Finance Officer and Chief Constable s Director of Resources Joint Audit Committee s Draft Annual Report

To: The Members of the Joint Audit Committee Meeting: 18 th September 2014 Joint Report of PCC s Chief Finance Officer and Chief Constable s Director of Resources Joint Audit Committee s Draft Annual Report

Regents of the University of Michigan Committee Charters Last updated June 17, 2010

Regents of the University of Michigan Committee Charters Last updated June 17, 2010 Personnel, Compensation and Governance Committee Charter The Personnel, Compensation and Governance Committee will review

Regents of the University of Michigan Committee Charters Last updated June 17, 2010 Personnel, Compensation and Governance Committee Charter The Personnel, Compensation and Governance Committee will review

The Internal Auditor s Duties Outside of Auditing

The Internal Auditor s Duties Outside of Auditing Dean Rohne, CPA, CIA dean.rohne@claconnect.com 1 1 Session Objectives Discuss the internal auditor s interaction with the supervisory committee and management

The Internal Auditor s Duties Outside of Auditing Dean Rohne, CPA, CIA dean.rohne@claconnect.com 1 1 Session Objectives Discuss the internal auditor s interaction with the supervisory committee and management

Periodic internal quality assessment Questions for discussion

Purpose, Authority, and Responsibility 1. Is the role of internal audit clearly defined in a document (a law, an act or a charter)? 2. Does this document also explain that we are not accountable for any

Purpose, Authority, and Responsibility 1. Is the role of internal audit clearly defined in a document (a law, an act or a charter)? 2. Does this document also explain that we are not accountable for any

Three Lines of Defense vs. Five Lines of Assurance

Three Lines of Defense vs. Five Lines of Assurance Elevating the Role of the Board and CEO in Risk Governance Tim Leech, Managing Director Risk Oversight Solutions Inc. Lauren Hanlon, Director Risk Oversight

Three Lines of Defense vs. Five Lines of Assurance Elevating the Role of the Board and CEO in Risk Governance Tim Leech, Managing Director Risk Oversight Solutions Inc. Lauren Hanlon, Director Risk Oversight

Institute of Internal Auditors 2018 IIA CHICAGO CHAPTER JOIN NTAC:4UC-11

2018 NORTH AMERICAN PULSE OF INTERNAL AUDIT THE INTERNAL AUDIT TRANSFORMATION IMPERATIVE JOHN WSZELAKI, CIA, CRMA, CFE DIRECTOR, AMERICAN CENTER FOR GOVERNMENT AUDITING THE INSTITUTE OF INTERNAL AUDITORS

2018 NORTH AMERICAN PULSE OF INTERNAL AUDIT THE INTERNAL AUDIT TRANSFORMATION IMPERATIVE JOHN WSZELAKI, CIA, CRMA, CFE DIRECTOR, AMERICAN CENTER FOR GOVERNMENT AUDITING THE INSTITUTE OF INTERNAL AUDITORS

Guidance Note: Corporate Governance - Board of Directors. January Ce document est aussi disponible en français.

Guidance Note: Corporate Governance - Board of Directors January 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance - Board of Directors (the Guidance

Guidance Note: Corporate Governance - Board of Directors January 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance - Board of Directors (the Guidance

Report. Quality Assessment of Internal Audit at <Organisation> Draft Report / Final Report

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

Internal Audit Mandate

1. Constitution 1.1. As a vital component of good Corporate Governance, an in-house and centralised Internal Audit function has been established by the Mr Price Group Board of Directors. 1.2. This function

1. Constitution 1.1. As a vital component of good Corporate Governance, an in-house and centralised Internal Audit function has been established by the Mr Price Group Board of Directors. 1.2. This function

Certificate in Establishing an Internal Audit Function

Certificate in Establishing an Internal Audit Function Who should attend? Recently appointed Chief Audit Executives (CAE s) or those about to be appointed or wishing to apply for this role CAE s appointed

Certificate in Establishing an Internal Audit Function Who should attend? Recently appointed Chief Audit Executives (CAE s) or those about to be appointed or wishing to apply for this role CAE s appointed

AUDIT COMMITTEE CHARTER APRIL 30, 2018

AUDIT COMMITTEE CHARTER APRIL 30, 2018 I. Purpose The Audit Committee ( Committee ) is appointed by the Board of Directors ( Board ) to assist the Board in its oversight responsibilities relating to: the

AUDIT COMMITTEE CHARTER APRIL 30, 2018 I. Purpose The Audit Committee ( Committee ) is appointed by the Board of Directors ( Board ) to assist the Board in its oversight responsibilities relating to: the

4. Organic documents. Please provide an English translation of the company s charter, by-laws and other organic documents.

Commitment to Good Corporate Governance 1. Ownership structure. Please provide a chart setting out the important shareholdings, holding companies, affiliates and subsidiaries of the company. If the company

Commitment to Good Corporate Governance 1. Ownership structure. Please provide a chart setting out the important shareholdings, holding companies, affiliates and subsidiaries of the company. If the company

CONTENTS. Acknowledgments... iv. 1: Introduction : Why have organizations chosen to seek compliance with the Standards?...2

IIA STANDARD 1312 - EXTERNAL QUALITY ASSESSMENTS: RESULTS, TOOLS, TECHNIQUES AND LESSONS LEARNED THE IIA RESEARCH FOUNDATION JULY 2007 Disclosure Copyright 2007 by The Institute of Internal Auditors Research

IIA STANDARD 1312 - EXTERNAL QUALITY ASSESSMENTS: RESULTS, TOOLS, TECHNIQUES AND LESSONS LEARNED THE IIA RESEARCH FOUNDATION JULY 2007 Disclosure Copyright 2007 by The Institute of Internal Auditors Research

9/15/2017. Automated Control Monitoring for Fraud, Waste and Abuse

Automated Control Monitoring for Fraud, Waste and Abuse 1 Join the session in the AGA app to join polls and ask question Agenda Introductions DOS OIG Criminal Analysis Division & Analytics Florida IG Audience

Automated Control Monitoring for Fraud, Waste and Abuse 1 Join the session in the AGA app to join polls and ask question Agenda Introductions DOS OIG Criminal Analysis Division & Analytics Florida IG Audience