Meeting Stakeholder Expectations for Assurance: Internal Audit s Role in a Group Effort

|

|

|

- Ashlie Williams

- 6 years ago

- Views:

Transcription

1 Meeting Stakeholder Expectations for Assurance: Internal Audit s Role in a Group Effort Urton Anderson The University of Texas at Austin 1

2 2

3 Agenda The IA Value Proposition The Demand for Assurance Assurance Mapping The Combined Assurance Approach Summary 3

4 The IA Value Proposition Thesis The fundamental value proposition for internal auditing is the role it plays in maintaining a system of effective organizational governance 4

5 What is organizational governance? The process through which (1) values and goals are established and communicated, (2) the accomplishment of goals is monitored, (3) accountability is ensured, and (4) values are preserved. 5

6 The Two Basic Responsibilities of the Governance Body of an Organization Governance Umbrella Board of Directors Strategic Direction Governance Oversight 6 Values Objectives Boundaries Accountability Values preservation

7 Key Components of Governance Oversight 7

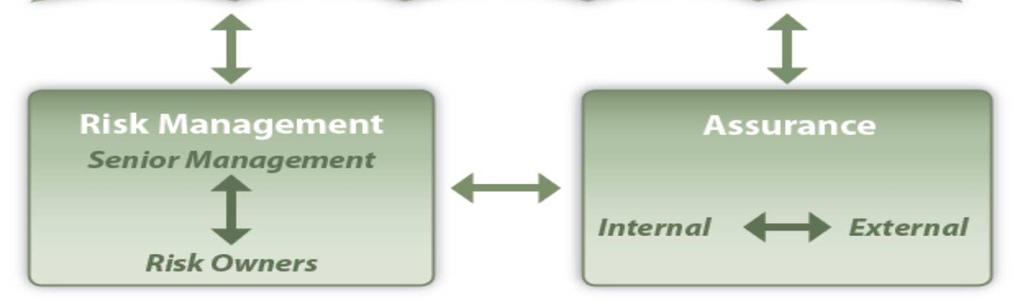

8 Governance Strategic Direction Set boundaries Set objectives Establish values Determine risk appetite Oversight Risk management Assurance 8

9 Depiction of Key Governance Elements 9

10 Internal Audit helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes. 10

11 IA Customers Auditee Audit Committee Senior Management Financial Management Vendors Regulators Suppliers External Auditors 11

12 What does the customer want? Audit Committee/Board Safeguarding Assets Compliance with Laws and Regulations Reliability of Data QUALITY OF INFORMATION Operating Management Effectiveness and Efficiency of Operations Achievement of Organizational Objectives CHANGE AGENT 12

13 The IA Value Proposition 13

14 ASSURANCE = Governance, Risk & Control Internal auditing provides assurance on the organization s governance, risk management, and control processes to help the organization achieve its strategic, operational, financial and compliance objectives. 14

15 OBJECTIVITY = Integrity, Accountability, & Independence With commitment to integrity and accountability, internal auditing provides value to governing bodies and senior management as an objective source of independent advice. 15

16 VALUE PROPOSITION OF INTERNAL AUDITING What STAKEHOLDERS should expect from your internal auditors 16

17 The Demand for Assurance Board Executive Management 17

18 Objectives Effectiveness and Efficiency of Operations Reliability of Financial Reporting and Safeguarding of Assets Compliance with Laws and Regulations 18

19 Responsibilities Effectiveness & Efficiency? Board s Executive Management 19

20 Responsibilities Effectiveness & Efficiency? Board s Reviewing and guiding corporate strategy, major plans of action, risk policy, annual budgets and business plans; setting performance objectives; monitoring implementation and corporate performance; and overseeing major capital expenditures, acquisitions and divestitures. OECD Principles of Corporate Governance, 2004 Executive Management (#1 of 8 responsibilities) 20

21 Responsibilities Reliability of Financial Reporting and Safeguarding of Assets? Board s Executive Management 21

22 Responsibilities Reliability of Financial Reporting and Safeguarding of Assets? Board s Ensuring the integrity of the corporation s accounting and financial reporting systems, including the independent audit OECD Principles of Corporate Governance, 2004 (#1 of 8 responsibilities) Executive Management SOX

23 Sky-rocketing Demand for Compliance Assurance Factors Increasing Complexity of the Legal and Regulatory Environment Technological Advancements Globalization Increased Interdependency of Organizations Demand for Accountability 23

24 The Board s Role in Compliance 24

25 Board s Role 2) (A) The organization s governing authority shall be knowledgeable about the content and operation of the compliance and ethics program and shall exercise reasonable oversight with respect to the implementation and effectiveness of the compliance and ethics program. Fed. Sent. Guidelines Chapter 8 25

26 Reasonable Oversight A director has a duty to attempt in good faith to assure that (1) a corporate information and reporting system exists, and (2) this reporting system is adequate to assure the board that appropriate information as to compliance with applicable laws will come to its attention in a timely manner as a matter of ordinary operations. In re Caremark International Inc. Derivative Litigation, 698 A.2d 959 (Del. Ch. 1996). 26

27 The Executive Management s Role in Compliance 27

28 Management s Responsibility To ensure that all operations are conducted in accordance with applicable law, regulations and policies, including internal policies. Compliance Programs are designed to establish a culture within a organization that promotes prevention, detection and resolution of instances of conduct that do not conform to federal and state law, as well as the organization s ethical and operations policies. 28

29 Assurance Mapping Web of Assurance 29

30 Practice Advisory Assurance Maps One of the key responsibilities of the board is to gain assurance that processes are operating within the parameters it has established to achieve the defined objectives. It is necessary to determine whether risk management processes are working effectively and whether key or businesscritical risks are being managed to an acceptable level. 30

31 Sources of Assurance Line management and employees (management provides assurance as a first line of defense over the risks and controls for which they are responsible.) Senior management Internal and external auditors Compliance Quality assurance Risk management Environmental auditors Workplace health and safety auditors Government performance auditors Financial reporting review teams External financial statement auditors Other external assurance providers, including surveys, specialist reviews (health and safety), etc. 31

32 Assurance Net (PWC) 32

33 3 Fundamental Classes of Assurance Providers 1. Those who report to management and/or are part of management (management assurance), including individuals who perform control self-assessments, quality auditors, environmental auditors, and other management- designated assurance personnel. 2. Those who report to the board, including internal audit, some cases compliance. 3. Those who report to external stakeholders (external audit assurance), which is a role traditionally fulfilled by the independent/statutory auditor. 33

34 Management Based Assurance Monitoring Function - Actions taken by management and others to assess the quality of internal control system performance over time 34

35 Assurance Continuum (Levels of Control in COSO) 35

36 Effective Monitoring 36

37 The Monitoring Function Supervisory Controls Investigation of unusual items Oversight Controls Customer surveys and complaint analysis Auditing Controls Traditional internal audit 37

38 Assurance Map 38

39 3 Lines of Defense Basel II - Basel Committee on Banking Supervision, UK, ECIIA Line 1 Line 2 Management oversight - management review, control selfassessment, and continuous monitoring mechanisms Staff functions Risk management, SOX review, compliance Line 3 Independent and objective assurance IA, EA, ISO, regulatory audits and other impendent reviews 39

40 Lines of Defense 40

41 How is assurance provided 41

42 COMBINED ASSURANCE King III Principle 3.5 The audit committee should ensure that a combined assurance model is applied to provide a coordinated approach to all assurance activities. 42

43 Combined Assurance Benefits Provides Board/Governance Body and senior management with assurance needed to carry out their responsibilities Reduce assurance fatigue 43

44 Implementing Step 1: Establishing the business case Step 2: Assurance reality check what risk, source of assurance, how Step 3: Risk mapping Step 4: Combined assurance design Step 5: Implement 44

")

45 Assurance Map (PWC) 45

46 Summary New approach to assurance required Increased demand for assurance Assurance fatigue Map of the organization s network of assurance Combined assurance approach New challenge for IA 46

47 CaE to CAE Responsibility of the CAE to understand the independent assurance requirements of the board and the organization, to clarify the role the internal audit activity fills and the level of assurance it provides. 47

48 Thank you! Contact Information: Urton Anderson McCombs School of Business The University of Texas at Austin (512) (messages until 8/1/12) (202) (until 7/31/12) 48

49 Agenda IPPF Code of Ethics Standards 49

2012 IIA Standards Update

2012 IIA Standards Update International Internal Audit Standards Board (IIASB) October 2012 1 Session Overview Why the Standards matter Standards-setting due process The key changes in 2012 Best practices

2012 IIA Standards Update International Internal Audit Standards Board (IIASB) October 2012 1 Session Overview Why the Standards matter Standards-setting due process The key changes in 2012 Best practices

The Red (Book) Rocks The Latest and Greatest Audit Standards

Rocks The Latest and Greatest Audit Standards") The Red (Book) Rocks The Latest and Greatest Audit Standards Presenter Toni Stephens Chief Audit Executive The University of Texas at Dallas Insert Logo Here Course Objectives Explain the development of

The Red (Book) Rocks The Latest and Greatest Audit Standards Presenter Toni Stephens Chief Audit Executive The University of Texas at Dallas Insert Logo Here Course Objectives Explain the development of

Changes To the Public Sector Internal Audit Standards April 2017

s To the Public Sector Internal Audit Standards April 2017 The Public Sector Internal Audit Standards (PSIAS) were updated in April 2017. The latest version of the document can be accessed on The Chartered

s To the Public Sector Internal Audit Standards April 2017 The Public Sector Internal Audit Standards (PSIAS) were updated in April 2017. The latest version of the document can be accessed on The Chartered

CHARTER OF THE SONOMA COUNTY INTERNAL AUDIT FUNCTION JANUARY 15, 2013

I. Introduction CHARTER OF THE JANUARY 15, 2013 ATTACHMENT B Fiscal Policy IA-1 A. The Institute of Internal Auditors (IIA) defines internal auditing as "an independent objective assurance and consulting

I. Introduction CHARTER OF THE JANUARY 15, 2013 ATTACHMENT B Fiscal Policy IA-1 A. The Institute of Internal Auditors (IIA) defines internal auditing as "an independent objective assurance and consulting

What We Will Cover Today

Standards for the Professional Practice of Internal Auditing The IIA Red Book The Basics of Internal Auditing September 8, 2014 Sam McCall, PhD, CPA, CGFM, CIA, CGAP, CIG Chief Audit Officer Florida State

Standards for the Professional Practice of Internal Auditing The IIA Red Book The Basics of Internal Auditing September 8, 2014 Sam McCall, PhD, CPA, CGFM, CIA, CGAP, CIG Chief Audit Officer Florida State

Implementation Guide 1000

Implementation Guide 1000 Standard 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter,

Implementation Guide 1000 Standard 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter,

IT Audit at Brown. A collaboration between the Information Technology and Internal Audit Teams

IT Audit at Brown A collaboration between the Information Technology and Internal Audit Teams Page 1 Agenda Objective Risk Management Overview Internal Audit at Brown IT Audit at Brown Frequently Asked

IT Audit at Brown A collaboration between the Information Technology and Internal Audit Teams Page 1 Agenda Objective Risk Management Overview Internal Audit at Brown IT Audit at Brown Frequently Asked

Implementation Guide 1200

Implementation Guide 1200 Standard 1200 Proficiency and Due Professional Care Engagements must be performed with proficiency and due professional care. Revised Standards Effective 1 January 2017 Getting

Implementation Guide 1200 Standard 1200 Proficiency and Due Professional Care Engagements must be performed with proficiency and due professional care. Revised Standards Effective 1 January 2017 Getting

This charter defines the purpose, authority and responsibility of News Corporation s (the Company ) Corporate Audit Department.

Corporate Audit Department.") CORPORATE AUDIT DEPARTMENT CHARTER PURPOSE This charter defines the purpose, authority and responsibility of News Corporation s (the Company ) Corporate Audit Department. The Institute of Internal Auditors

CORPORATE AUDIT DEPARTMENT CHARTER PURPOSE This charter defines the purpose, authority and responsibility of News Corporation s (the Company ) Corporate Audit Department. The Institute of Internal Auditors

The IPPF in How changes to The IIA s guidance framework can benefit internal auditors and SAIs

The IPPF in 2017 How changes to The IIA s guidance framework can benefit internal auditors and SAIs From the Previous IPPF To the New IPPF International Professional Practices Framework Launched July 2015

The IPPF in 2017 How changes to The IIA s guidance framework can benefit internal auditors and SAIs From the Previous IPPF To the New IPPF International Professional Practices Framework Launched July 2015

Implementation Guide 1312

Implementation Guide 1312 Standard 1312 External Assessments External assessments must be conducted at least once every five years by a qualified, independent assessor or assessment team from outside the

Implementation Guide 1312 Standard 1312 External Assessments External assessments must be conducted at least once every five years by a qualified, independent assessor or assessment team from outside the

Implementation Guide 2000

Implementation Guide 2000 Standard 2000 Managing the Internal Audit Activity The chief audit executive must effectively manage the internal audit activity to ensure it adds value to the organization. Interpretation:

Implementation Guide 2000 Standard 2000 Managing the Internal Audit Activity The chief audit executive must effectively manage the internal audit activity to ensure it adds value to the organization. Interpretation:

Report. Quality Assessment of Internal Audit at <Organisation> Draft Report / Final Report

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

Tools & Techniques II: Lead Auditor

About This Course Tools & Techniques II: Lead Auditor Course Description Learn the skills necessary to lead an audit team with confidence. This course provides an overview of the life cycle of an audit

About This Course Tools & Techniques II: Lead Auditor Course Description Learn the skills necessary to lead an audit team with confidence. This course provides an overview of the life cycle of an audit

Audit Standards 6/23/2017. Outline. Let s Refresh. Changes to the IIA Standards

Audit Standards Let s Refresh Outline Changes in the Standards Changes in the Yellowbook Standards Attribute/General Standards Performance/Fieldwork Standards Reporting Standards Key Differences Changes

Audit Standards Let s Refresh Outline Changes in the Standards Changes in the Yellowbook Standards Attribute/General Standards Performance/Fieldwork Standards Reporting Standards Key Differences Changes

PART 6 - INTERNAL CONTROL

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

AUDITING. Auditing PAGE 1

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

MISSISSIPPI STATE UNIVERSITY INTERNAL AUDIT CHARTER

MISSISSIPPI STATE UNIVERSITY INTERNAL AUDIT CHARTER I. The Charter The Office of Internal Audit was established by the President of Mississippi State University to assist the University in meeting its

MISSISSIPPI STATE UNIVERSITY INTERNAL AUDIT CHARTER I. The Charter The Office of Internal Audit was established by the President of Mississippi State University to assist the University in meeting its

Quality Assurance and Improvement Program (QAIP)

") Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

COMPLIANCE AT LARGER INSTITUTIONS. November 11 13, Robert F. Roach Chief Compliance Officer New York University

COMPLIANCE AT LARGER INSTITUTIONS November 11 13, 2009 Robert F. Roach Chief Compliance Officer New York University I. Introduction - What is Compliance? We re Watching You! In a University setting, the

COMPLIANCE AT LARGER INSTITUTIONS November 11 13, 2009 Robert F. Roach Chief Compliance Officer New York University I. Introduction - What is Compliance? We re Watching You! In a University setting, the

Quality Assessments what you need to know

Quality Assessments what you need to know Patty Miller, Partner Deloitte & Touche LLP Cavell Alexander, VP-Internal Audit Intermountain Healthcare Overview of requirements Scope of assessment Approaches

Quality Assessments what you need to know Patty Miller, Partner Deloitte & Touche LLP Cavell Alexander, VP-Internal Audit Intermountain Healthcare Overview of requirements Scope of assessment Approaches

Value-Added Internal Audit: Myth or Reality?

Value-Added Internal Audit: Myth or Reality? Istanbul 12 November 2013 Jean-Pierre Garitte, CIA, CCSA, CISA, CFE, RFA Past Chairman of the Board IIA Past President ECIIA Polling question #1 For how long

Value-Added Internal Audit: Myth or Reality? Istanbul 12 November 2013 Jean-Pierre Garitte, CIA, CCSA, CISA, CFE, RFA Past Chairman of the Board IIA Past President ECIIA Polling question #1 For how long

Policies, Procedures and Guidelines

Policies, Procedures and Guidelines Complete Policy Title: Internal Audit Department Policy Statement Policy Number (if applicable): Approved by: Audit Committee of the Board of Governors Date of Most

Policies, Procedures and Guidelines Complete Policy Title: Internal Audit Department Policy Statement Policy Number (if applicable): Approved by: Audit Committee of the Board of Governors Date of Most

August 14, Dear Ms. Gula:

Department of Internal Audit North End Center, Suite 3200, Virginia Tech 300 Turner Street NW Blacksburg, Virginia 24061 Campus Mail Code: 0328 540-231-5883 Fax: 540-231-4681 www.ia.vt.edu August 14, 2013

Department of Internal Audit North End Center, Suite 3200, Virginia Tech 300 Turner Street NW Blacksburg, Virginia 24061 Campus Mail Code: 0328 540-231-5883 Fax: 540-231-4681 www.ia.vt.edu August 14, 2013

Internal Oversight Division. Internal Audit Strategy

Internal Oversight Division Internal Audit Strategy 2018-2020 Date: January 24, 2018 page 2 TABLE OF CONTENTS LIST OF ACRONYMS 3 1. BACKGROUND 4 2. PURPOSE 4 3. WIPO STRATEGIC REALIGNMENT PROGRAM 5 (A)

Internal Oversight Division Internal Audit Strategy 2018-2020 Date: January 24, 2018 page 2 TABLE OF CONTENTS LIST OF ACRONYMS 3 1. BACKGROUND 4 2. PURPOSE 4 3. WIPO STRATEGIC REALIGNMENT PROGRAM 5 (A)

Implementation Guide 2050

Implementation Guide 2050 Standard 2050 Coordination and Reliance The chief audit executive should share information, coordinate activities, and consider relying upon the work of other internal and external

Implementation Guide 2050 Standard 2050 Coordination and Reliance The chief audit executive should share information, coordinate activities, and consider relying upon the work of other internal and external

IT Audit Process. Michael Romeu-Lugo MBA, CISA March 27, IT Audit Process. Prof. Mike Romeu

Michael Romeu-Lugo MBA, CISA March 27, 2017 1 Agenda Audit Planning PS 1203 / PG 2203 Evidence PS 1205 / PG 2205 References: ITAF 3 rd Edition Information Systems Auditing: Tools and Techniques Creating

Michael Romeu-Lugo MBA, CISA March 27, 2017 1 Agenda Audit Planning PS 1203 / PG 2203 Evidence PS 1205 / PG 2205 References: ITAF 3 rd Edition Information Systems Auditing: Tools and Techniques Creating

Advisory Services Governance, Risk & Compliance

Advisory Services Governance, Risk & Compliance Caribbean Association of Audit Committee Members Inc. 2010 Conference Caretakers of Integrity and Accountability: The Role of Internal Audit in Corporate

Advisory Services Governance, Risk & Compliance Caribbean Association of Audit Committee Members Inc. 2010 Conference Caretakers of Integrity and Accountability: The Role of Internal Audit in Corporate

Practice Advisory : Quality Assurance and Improvement Program

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

International Finance Corporation

International Finance Corporation Corporate Governance and Internal Audit Overview Bob Lamm Independent Senior Advisor Center for Corporate Governance Deloitte LLP Neil White Global IA Analytics Leader

International Finance Corporation Corporate Governance and Internal Audit Overview Bob Lamm Independent Senior Advisor Center for Corporate Governance Deloitte LLP Neil White Global IA Analytics Leader

INTERNATIONAL ORGANIZATION FOR MIGRATION. Keywords: internal audit, evaluation, investigation, inspection, monitoring, internal oversight

INTERNATIONAL ORGANIZATION FOR MIGRATION Document Title: Charter of the Office of the Inspector General (OIG) Document Type: Instruction Character: Compliance with this Instruction is mandatory Control

INTERNATIONAL ORGANIZATION FOR MIGRATION Document Title: Charter of the Office of the Inspector General (OIG) Document Type: Instruction Character: Compliance with this Instruction is mandatory Control

Session 7: Corporate Governance

Session 7: Corporate Governance New York Bankers Association-Community Bank Auditors Group 2016 Internal Audit Training-June 6-8, 2016 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

Session 7: Corporate Governance New York Bankers Association-Community Bank Auditors Group 2016 Internal Audit Training-June 6-8, 2016 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

King lll Principle Comments on application in 2016 Reference Chapter 1: Ethical leadership and corporate citizenship Principle 1.

Clicks Group Application of King III Principles 2016 APPLICATION OF King III PrincipleS 2016 This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King

Clicks Group Application of King III Principles 2016 APPLICATION OF King III PrincipleS 2016 This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King

INTERNAL AUDIT CHARTER

INTERNAL AUDIT CHARTER January 2018 1/5 A. Mission Statement AXA Internal Audit exists to help the Board and Executive Management protect the assets, reputation and sustainability of the organisation by

INTERNAL AUDIT CHARTER January 2018 1/5 A. Mission Statement AXA Internal Audit exists to help the Board and Executive Management protect the assets, reputation and sustainability of the organisation by

External Quality Assessment Are You Ready? Institute of Internal Auditors

External Quality Assessment Are You Ready? Institute of Internal Auditors Objectives Describe frameworks used to assess the quality of an IA activity Discuss benefits, challenges, and success factors related

External Quality Assessment Are You Ready? Institute of Internal Auditors Objectives Describe frameworks used to assess the quality of an IA activity Discuss benefits, challenges, and success factors related

CHARTER OF THE AUDIT COMMITTEE NATIONWIDE MUTUAL INSURANCE COMPANY NATIONWIDE MUTUAL FIRE INSURANCE COMPANY NATIONWIDE CORPORATION

CHARTER OF THE AUDIT COMMITTEE NATIONWIDE MUTUAL INSURANCE COMPANY NATIONWIDE MUTUAL FIRE INSURANCE COMPANY NATIONWIDE CORPORATION ESTABLISHMENT The Audit Committees are committees of the Board of Directors

CHARTER OF THE AUDIT COMMITTEE NATIONWIDE MUTUAL INSURANCE COMPANY NATIONWIDE MUTUAL FIRE INSURANCE COMPANY NATIONWIDE CORPORATION ESTABLISHMENT The Audit Committees are committees of the Board of Directors

Internal Audit Policy and Procedures Internal Audit Charter

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE

CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE AGRIUM INC. CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE TABLE OF CONTENTS Page 1. Introduction... 1 2. Overview of Responsibilities: The Board and the Chief Executive

CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE AGRIUM INC. CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE TABLE OF CONTENTS Page 1. Introduction... 1 2. Overview of Responsibilities: The Board and the Chief Executive

External Quality Assessment of the Internal Audit Activity at. County of Orange. April County of Orange Final Report: June 13,

Eternal Quality Assessment of the Internal Audit Activity at County of Orange April 2017 County of Orange Final Report: June 13, 2017 1 EXECUTIVE SUMMARY... 3 OPINION AS TO CONFORMANCE... 3 PART I MATTERS

Eternal Quality Assessment of the Internal Audit Activity at County of Orange April 2017 County of Orange Final Report: June 13, 2017 1 EXECUTIVE SUMMARY... 3 OPINION AS TO CONFORMANCE... 3 PART I MATTERS

LEVERAGING COSO ACROSS THE THREE LINES OF DEFENSE

Committee of Sponsoring Organizations of the Treadway Commission Governance and Internal Control LEVERAGING COSO ACROSS THE THREE LINES OF DEFENSE By The Institute of Internal Auditors Douglas J. Anderson

Committee of Sponsoring Organizations of the Treadway Commission Governance and Internal Control LEVERAGING COSO ACROSS THE THREE LINES OF DEFENSE By The Institute of Internal Auditors Douglas J. Anderson

Implementation Guides

Implementation Guides Implementation Guides assist internal auditors in applying the Definition of Internal Auditing, the Code of Ethics, and the Standards and promoting good practices. Implementation

Implementation Guides Implementation Guides assist internal auditors in applying the Definition of Internal Auditing, the Code of Ethics, and the Standards and promoting good practices. Implementation

Internal Audit Appendix: IIA Standards

Accountability Modules Internal Audit Appendix: IIA Standards Return to Table of ontents The following section provides additional detailed steps to examine when evaluating an internal audit function.

Accountability Modules Internal Audit Appendix: IIA Standards Return to Table of ontents The following section provides additional detailed steps to examine when evaluating an internal audit function.

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017)

") Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

King lll Principle Comments on application in 2013 Reference in 2013 Integrated Report

Application of King III Principles 2013 This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King III principles by the Clicks Group. The following

Application of King III Principles 2013 This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King III principles by the Clicks Group. The following

Bank of Botswana Internal Audit Charter March 18, 2013 INTERNAL AUDIT CHARTER BANK OF BOTSWANA

INTERNAL AUDIT CHARTER BANK OF BOTSWANA 1 CONTENTS PAGE 1. PURPOSE OF THE INTERNAL AUDIT CHARTER 3 2. PURPOSE OF THE INTERNAL AUDIT DIVISION 3 3. POLICY STATEMENTS 3 3.1 Establishment of the Internal Audit

INTERNAL AUDIT CHARTER BANK OF BOTSWANA 1 CONTENTS PAGE 1. PURPOSE OF THE INTERNAL AUDIT CHARTER 3 2. PURPOSE OF THE INTERNAL AUDIT DIVISION 3 3. POLICY STATEMENTS 3 3.1 Establishment of the Internal Audit

METUCHEN CAPACITORS INCORPORATED. Quality Manual P.O. BOX HIGHWAY 35, SUITE 2 HOLMDEL NJ USA

METUCHEN CAPACITORS INCORPORATED Quality Manual P.O. BOX 399 2139 HIGHWAY 35, SUITE 2 HOLMDEL NJ 07733 USA Copy Holder Copy Number : 1 This Quality Manual Covers the activities and functions performed

METUCHEN CAPACITORS INCORPORATED Quality Manual P.O. BOX 399 2139 HIGHWAY 35, SUITE 2 HOLMDEL NJ 07733 USA Copy Holder Copy Number : 1 This Quality Manual Covers the activities and functions performed

GoldSRD Audit 101 Table of Contents & Resource Listing

Au GoldSRD Audit 101 Table of Contents & Resource Listing I. IIA Standards II. GTAG I (Example Copy of the Contents of the GTAG Series) III. Example Audit Workprogram IV. Audit Test Workpaper Example V.

Au GoldSRD Audit 101 Table of Contents & Resource Listing I. IIA Standards II. GTAG I (Example Copy of the Contents of the GTAG Series) III. Example Audit Workprogram IV. Audit Test Workpaper Example V.

CORPORATE GOVERNANCE THEORY, SCOPE AND IMPORTANCE

CORPORATE GOVERNANCE THEORY, SCOPE AND IMPORTANCE What is on the agenda Corporate Governance: In Theory Brief history The concept Principles Corporate Governance: In Practice Corporate governance elements

CORPORATE GOVERNANCE THEORY, SCOPE AND IMPORTANCE What is on the agenda Corporate Governance: In Theory Brief history The concept Principles Corporate Governance: In Practice Corporate governance elements

LeiningerCPA, Ltd. RISK MANAGEMENT POLICY STATEMENT

LeiningerCPA, Ltd. RISK MANAGEMENT POLICY STATEMENT This policy provides an overview of the bank s risk management process and defines the broad responsibilities for overseeing corporate governance and

LeiningerCPA, Ltd. RISK MANAGEMENT POLICY STATEMENT This policy provides an overview of the bank s risk management process and defines the broad responsibilities for overseeing corporate governance and

Audit and Risk Committee Charter

Audit and Risk Committee Charter Pyrolyx AG (Company) Adopted by the Supervisory Board on 11 July 2017 3403640-v2\SYDDMS Audit and Risk Committee charter Contents 1 Purpose and authority 1 1.1 Purpose...

Audit and Risk Committee Charter Pyrolyx AG (Company) Adopted by the Supervisory Board on 11 July 2017 3403640-v2\SYDDMS Audit and Risk Committee charter Contents 1 Purpose and authority 1 1.1 Purpose...

University Students Council of the University of Western Ontario BY-LAW #4. AUTHORITY: Council RATIFIED BY: Council DAY MONTH YEAR BY-LAW #4

EFFECTIVE: DAY MONTH YEAR SUPERSEDES: NONE AUTHORITY: Council RATIFIED BY: Council DAY MONTH YEAR RELATED DOCUMENTS: By-Law #1 PAGE 1 of 9 of UNIVERSITY STUDENTS COUNCIL OF THE UNIVERSITY OF WESTERN ONTARIO

EFFECTIVE: DAY MONTH YEAR SUPERSEDES: NONE AUTHORITY: Council RATIFIED BY: Council DAY MONTH YEAR RELATED DOCUMENTS: By-Law #1 PAGE 1 of 9 of UNIVERSITY STUDENTS COUNCIL OF THE UNIVERSITY OF WESTERN ONTARIO

Practice Guide ASSESSING ORGANIZATIONAL GOVERNANCE IN THE PUBLIC SECTOR

Practice Guide ASSESSING ORGANIZATIONAL GOVERNANCE IN THE PUBLIC SECTOR OCTOBER 2014 Table of Contents Executive Summary... 1 Introduction... 1 Public Sector Characteristics... 4 Public Sector Structure...

Practice Guide ASSESSING ORGANIZATIONAL GOVERNANCE IN THE PUBLIC SECTOR OCTOBER 2014 Table of Contents Executive Summary... 1 Introduction... 1 Public Sector Characteristics... 4 Public Sector Structure...

Technical Services Document #: TS-0007 Internal Audit Procedure Version #: 01

1. Purpose The purpose of this procedure is to define the process used to manage the Internal Audits of the Quality Management System for Technical Services. 2. Scope This procedure applies to all Internal

1. Purpose The purpose of this procedure is to define the process used to manage the Internal Audits of the Quality Management System for Technical Services. 2. Scope This procedure applies to all Internal

Guidance Note: Corporate Governance - Audit Committee. March Ce document est aussi disponible en français.

Guidance Note: Corporate Governance - Audit Committee March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note )

Guidance Note: Corporate Governance - Audit Committee March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note )

IBL LTD AUDIT AND RISK COMMITTEE TERMS OF REFERENCE

IBL LTD AUDIT AND RISK COMMITTEE TERMS OF REFERENCE 1. Overall Purpose/Objectives 1.1 The Audit and Risk Committee, while assisting the Board in fulfilling its oversight responsibilities, will also be

IBL LTD AUDIT AND RISK COMMITTEE TERMS OF REFERENCE 1. Overall Purpose/Objectives 1.1 The Audit and Risk Committee, while assisting the Board in fulfilling its oversight responsibilities, will also be

Compliance and the Board of Directors

Adam J. Falcone, Esq., Partner Dianne K. Pledgie, Esq., Compliance Counsel Feldesman Tucker Leifer Fidell, LLP Compliance and the Board of Directors Speaker Name Title Organization Disclaimer: EDUCATIONAL

Adam J. Falcone, Esq., Partner Dianne K. Pledgie, Esq., Compliance Counsel Feldesman Tucker Leifer Fidell, LLP Compliance and the Board of Directors Speaker Name Title Organization Disclaimer: EDUCATIONAL

CHARTER INTERNAL OVERSIGHT OFFICE (IOO)

") CHARTER INTERNAL OVERSIGHT OFFICE (IOO) VISION The vision of IOO is - To be a high-performing internal oversight activity that meets the expectations of WMO stakeholders and adheres to the professional

CHARTER INTERNAL OVERSIGHT OFFICE (IOO) VISION The vision of IOO is - To be a high-performing internal oversight activity that meets the expectations of WMO stakeholders and adheres to the professional

How to plan an audit engagement

01 November 2017 How to plan an audit engagement Chartered Institute of Internal Auditors Planning audit projects, or engagements, well will ensure you deliver a quality assurance and consulting service

01 November 2017 How to plan an audit engagement Chartered Institute of Internal Auditors Planning audit projects, or engagements, well will ensure you deliver a quality assurance and consulting service

Corporate Governance and Financial Markets

Corporate Governance and Financial Markets World Congress of Accountants Istanbul, Turkey 14 November 2006 Jerry Edwards Senior Advisor on Accounting and Auditing Policy Financial Stability Forum Basel,

Corporate Governance and Financial Markets World Congress of Accountants Istanbul, Turkey 14 November 2006 Jerry Edwards Senior Advisor on Accounting and Auditing Policy Financial Stability Forum Basel,

Implementation Guide 1300

Implementation Guide 1300 Standard 1300 Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality assurance and improvement program that covers all aspects

Implementation Guide 1300 Standard 1300 Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality assurance and improvement program that covers all aspects

INTERNATIONAL STANDARD

INTERNATIONAL STANDARD ISO 19011 Second edition 2011-11-15 Guidelines for auditing management systems Lignes directrices pour l audit des systèmes de management Reference number ISO 19011:2011(E) ISO 2011

INTERNATIONAL STANDARD ISO 19011 Second edition 2011-11-15 Guidelines for auditing management systems Lignes directrices pour l audit des systèmes de management Reference number ISO 19011:2011(E) ISO 2011

RISK AND AUDIT COMMITTEE TERMS OF REFERENCE

RISK AND AUDIT COMMITTEE TERMS OF REFERENCE Brief description Defines the Terms of Reference for the Risk and Audit Committee. BHP Billiton Limited & BHP Billiton Plc BHP Billiton Limited & BHP Billiton

RISK AND AUDIT COMMITTEE TERMS OF REFERENCE Brief description Defines the Terms of Reference for the Risk and Audit Committee. BHP Billiton Limited & BHP Billiton Plc BHP Billiton Limited & BHP Billiton

The Three Lines of Defense Model: A framework for risk management and internal control. Office of the Inspector General Internal Audit services

The Three Lines of Defense Model: A framework for risk management and internal control Author: Daniel Ramirez León Date: December 2016 The Three Lines of Defense Model - A framework for risk management

The Three Lines of Defense Model: A framework for risk management and internal control Author: Daniel Ramirez León Date: December 2016 The Three Lines of Defense Model - A framework for risk management

External Quality Assessment of the Internal Audit Activity at the World Food Programme

External Quality Assessment of the Internal Audit Activity at the World Food Programme November 2016 Table of Contents Executive Summary... 3 Opinion as to conformance to the Standards... 3 Scope and methodology...

External Quality Assessment of the Internal Audit Activity at the World Food Programme November 2016 Table of Contents Executive Summary... 3 Opinion as to conformance to the Standards... 3 Scope and methodology...

UNITED ISD INTERNAL AUDIT DEPARTMENT QUALITY ASSESSMENT SELF-ASSESSMENT WITH INDEPENDENT EXTERNAL VALIDATION

UNITED ISD INTERNAL AUDIT DEPARTMENT QUALITY ASSESSMENT SELF-ASSESSMENT WITH INDEPENDENT EXTERNAL VALIDATION OCTOBER 2017 CONTENTS REPORT SECTION 1 Executive Summary Opinion as to Conformance with the

UNITED ISD INTERNAL AUDIT DEPARTMENT QUALITY ASSESSMENT SELF-ASSESSMENT WITH INDEPENDENT EXTERNAL VALIDATION OCTOBER 2017 CONTENTS REPORT SECTION 1 Executive Summary Opinion as to Conformance with the

RISK COMMITTEE BYLAW OF THE SUPERVISORY BOARD OF ING BANK ŚLĄSKI S.A.

RISK COMMITTEE BYLAW OF THE SUPERVISORY BOARD OF ING BANK ŚLĄSKI S.A. 1 The Risk Committee of the Supervisory Board of ING Bank Śląski S.A., hereinafter referred to as the Committee, shall perform consultation

RISK COMMITTEE BYLAW OF THE SUPERVISORY BOARD OF ING BANK ŚLĄSKI S.A. 1 The Risk Committee of the Supervisory Board of ING Bank Śląski S.A., hereinafter referred to as the Committee, shall perform consultation

Dexia Group Audit Charter

January 2013 Dexia Group Audit Charter The present Charter states the fundamental principles governing the internal audit function in the Dexia Group, describing its objectives, its role, responsibilities

January 2013 Dexia Group Audit Charter The present Charter states the fundamental principles governing the internal audit function in the Dexia Group, describing its objectives, its role, responsibilities

PRACTICE GUIDE. Formulating and Expressing Internal Audit Opinions

PRACTICE GUIDE Formulating and Expressing Internal Audit Opinions 2 of 23 Table of Contents 1. Executive Summary... 1 2. Introduction... 2 3. Planning the Expression of an Opinion... 3 3.1 Expressing an

PRACTICE GUIDE Formulating and Expressing Internal Audit Opinions 2 of 23 Table of Contents 1. Executive Summary... 1 2. Introduction... 2 3. Planning the Expression of an Opinion... 3 3.1 Expressing an

THE BOARD S ROLE IN AUDIT, CONTROL, & RISK OVERSIGHT

THE BOARD S ROLE IN AUDIT, CONTROL, & RISK OVERSIGHT Session 6 Key Functions Of The Board Reviewing and guiding corporate strategy and risk policy Monitoring effectiveness of the company s governance Monitoring

THE BOARD S ROLE IN AUDIT, CONTROL, & RISK OVERSIGHT Session 6 Key Functions Of The Board Reviewing and guiding corporate strategy and risk policy Monitoring effectiveness of the company s governance Monitoring

GOVERNANCE GUIDELINE DRAFT. Initial publication: April 2009 Updated: July Ligne directrice sur la conformité

GOVERNANCE GUIDELINE Initial publication: April 2009 Updated: July 2016 Ligne directrice sur la conformité Page 1 Autorité des marchés financiers Novembre 2007 TABLE OF CONTENTS Preamble... 2 Scope...

GOVERNANCE GUIDELINE Initial publication: April 2009 Updated: July 2016 Ligne directrice sur la conformité Page 1 Autorité des marchés financiers Novembre 2007 TABLE OF CONTENTS Preamble... 2 Scope...

Audit Project Process Overview 1/18/ Compliance and Audit Symposium. Agenda. How to Kick-start your. Audit Planning and Risk Assessment

2013 Compliance and Audit Symposium How to Kick-start your Audit Planning and Risk Assessment Jaime Jue, Associate Director, UC Berkeley David Meier, Manager Campus Audits, UC San Diego January 2013 Agenda

2013 Compliance and Audit Symposium How to Kick-start your Audit Planning and Risk Assessment Jaime Jue, Associate Director, UC Berkeley David Meier, Manager Campus Audits, UC San Diego January 2013 Agenda

Internal Audit Challenges & Opportunities Speaker: Laurie Shen, Director, Grant Thornton LLP

Internal Audit Challenges & Opportunities Speaker: Laurie Shen, Director, Grant Thornton LLP March 28, 2012-1 - Speaker Introduction Laurie Shen is a Director at Grant Thornton's Northeast Internal Audit

Internal Audit Challenges & Opportunities Speaker: Laurie Shen, Director, Grant Thornton LLP March 28, 2012-1 - Speaker Introduction Laurie Shen is a Director at Grant Thornton's Northeast Internal Audit

Assessment of the Design Effectiveness of Entity Level Controls. Office of the Chief Audit Executive

Assessment of the Design Effectiveness of Entity Level Controls Office of the Chief Audit Executive February 2017 Cette publication est également disponible en français. This publication is available in

Assessment of the Design Effectiveness of Entity Level Controls Office of the Chief Audit Executive February 2017 Cette publication est également disponible en français. This publication is available in

1. INTERNAL AUDIT CHARTER (PDF)

") 1. INTERNAL AUDIT CHARTER (PDF) The Internal Audit Charter spells out the purpose, authority, and responsibility of the Internal Audit function at the University of Swaziland. The Charter also provides

1. INTERNAL AUDIT CHARTER (PDF) The Internal Audit Charter spells out the purpose, authority, and responsibility of the Internal Audit function at the University of Swaziland. The Charter also provides

Internal Audit Performance

Internal Audit Performance A summary of the effectiveness of the internal audit functions reviewed during 2016/17 Chartered Institute of Internal Auditors April 2017 Contents Contents...2 Executive Summary...3

Internal Audit Performance A summary of the effectiveness of the internal audit functions reviewed during 2016/17 Chartered Institute of Internal Auditors April 2017 Contents Contents...2 Executive Summary...3

Accountability Framework

Bureau de la Directrice Director s Office Circular No. Circulaire n DIR 02/2015 Date: 02/02/2015 Accountability Framework Introduction 1. Strengthening accountability is an important part of improving

Bureau de la Directrice Director s Office Circular No. Circulaire n DIR 02/2015 Date: 02/02/2015 Accountability Framework Introduction 1. Strengthening accountability is an important part of improving

Chair all meetings of the Board of Directors and shareholders;

Executive Chairman A key responsibility of the Executive Chairman of the Board of Directors, in addition to his responsibilities as a senior member of the executive management team of the Corporation,

Executive Chairman A key responsibility of the Executive Chairman of the Board of Directors, in addition to his responsibilities as a senior member of the executive management team of the Corporation,

GRIFOLS STATUTES OF THE AUDIT COMMITTEE

GRIFOLS STATUTES OF THE AUDIT COMMITTEE GRIFOLS STATUTES OF THE AUDIT COMMITTEE Table of Contents 1. PURPOSE... 3 2. COMPOSITION... 3 3. FUNCTIONING... 3 4. FUNDING... 4 5. RESPONSIBILITIES... 4 A) In

GRIFOLS STATUTES OF THE AUDIT COMMITTEE GRIFOLS STATUTES OF THE AUDIT COMMITTEE Table of Contents 1. PURPOSE... 3 2. COMPOSITION... 3 3. FUNCTIONING... 3 4. FUNDING... 4 5. RESPONSIBILITIES... 4 A) In

SEMPRA ENERGY. Corporate Governance Guidelines. As adopted by the Board of Directors of Sempra Energy and amended through December 15, 2017

SEMPRA ENERGY Corporate Governance Guidelines As adopted by the Board of Directors of Sempra Energy and amended through December 15, 2017 I Role of the Board and Management 1.1 Board Oversight Sempra Energy

SEMPRA ENERGY Corporate Governance Guidelines As adopted by the Board of Directors of Sempra Energy and amended through December 15, 2017 I Role of the Board and Management 1.1 Board Oversight Sempra Energy

(Adopted by the Board of Directors on 13 May 2009 and amended on 24 September 2009, 13 September 2012 and 27 November 2013)

") Thomas Cook Group plc THE AUDIT COMMITTEE TERMS OF REFERENCE (Adopted by the Board of Directors on 13 May 2009 and amended on 24 September 2009, 13 September 2012 and 27 November 2013) Chairman and members

Thomas Cook Group plc THE AUDIT COMMITTEE TERMS OF REFERENCE (Adopted by the Board of Directors on 13 May 2009 and amended on 24 September 2009, 13 September 2012 and 27 November 2013) Chairman and members

4. Organic documents. Please provide an English translation of the company s charter, by-laws and other organic documents.

Commitment to Good Corporate Governance 1. Ownership structure. Please provide a chart setting out the important shareholdings, holding companies, affiliates and subsidiaries of the company. If the company

Commitment to Good Corporate Governance 1. Ownership structure. Please provide a chart setting out the important shareholdings, holding companies, affiliates and subsidiaries of the company. If the company

BOARD CHARTER TOURISM HOLDINGS LIMITED

BOARD CHARTER TOURISM HOLDINGS LIMITED INDEX Tourism Holdings Limited ( thl ) - Board Charter 2 1. Governance at thl 2 2. Role of the Board 3 3. Structure of the Board 4 4. Matters Relating to Directors

BOARD CHARTER TOURISM HOLDINGS LIMITED INDEX Tourism Holdings Limited ( thl ) - Board Charter 2 1. Governance at thl 2 2. Role of the Board 3 3. Structure of the Board 4 4. Matters Relating to Directors

OFFICE OF INTERNAL AUDITS APPALACHIAN STATE UNIVERSITY AUDIT MANUAL

OFFICE OF INTERNAL AUDITS APPALACHIAN STATE UNIVERSITY AUDIT MANUAL June, 2016 AUDIT MANUAL TABLE OF CONTENTS SECTION 100 THE INTERNAL AUDIT ACTIVITY 100.1: Audit Activity Charter 100.2: State Agency General

OFFICE OF INTERNAL AUDITS APPALACHIAN STATE UNIVERSITY AUDIT MANUAL June, 2016 AUDIT MANUAL TABLE OF CONTENTS SECTION 100 THE INTERNAL AUDIT ACTIVITY 100.1: Audit Activity Charter 100.2: State Agency General

Audit Committee Charter ISSUE DATE: 22 JUNE 2017 AUDIT COMMITTEE CHARTER. ISSUE DATE: 22 JUNE 2017 PAGE 01 OF 07

Audit Committee Charter ISSUE DATE: 22 JUNE 2017 AUDIT COMMITTEE CHARTER. ISSUE DATE: 22 JUNE 2017 PAGE 01 OF 07 Introduction The Audit Committee, appointed by the Board of the Company specified in item

Audit Committee Charter ISSUE DATE: 22 JUNE 2017 AUDIT COMMITTEE CHARTER. ISSUE DATE: 22 JUNE 2017 PAGE 01 OF 07 Introduction The Audit Committee, appointed by the Board of the Company specified in item

See your auditor clearly. Transparency report: How we perform quality audit engagements

See your auditor clearly. Transparency report: How we perform quality audit engagements February 2014 Table of contents 1) A message from the CEO and Managing Partner Assurance 2 2) Quality control policies

See your auditor clearly. Transparency report: How we perform quality audit engagements February 2014 Table of contents 1) A message from the CEO and Managing Partner Assurance 2 2) Quality control policies

NYSE: Corporate Governance Guide

NYSE: Corporate Governance Guide Italy Carlo Croff, Partner, and Enrico Giordano, Partner Chiomenti The key corporate governance provisions for Italian listed companies are found in: the Italian Civil

NYSE: Corporate Governance Guide Italy Carlo Croff, Partner, and Enrico Giordano, Partner Chiomenti The key corporate governance provisions for Italian listed companies are found in: the Italian Civil

Ethical leadership and corporate citizenship. Applied. Applied. Applied. Company s ethics are managed effectively.

CORPORATE GOVERNANCE- KING III COMPLIANCE Analysis of the application as at 24 June 2015 by Master Drilling Group Limited (the Company) of the 75 corporate governance principles as recommended by the King

CORPORATE GOVERNANCE- KING III COMPLIANCE Analysis of the application as at 24 June 2015 by Master Drilling Group Limited (the Company) of the 75 corporate governance principles as recommended by the King

1.1 Scope and purpose of the Manual Introduction Purpose Authority and responsibility... 2

April 20152016 Table of Contents 1 Introduction 1.1 Scope and purpose of the Manual... 1 2 Purpose, authority and responsibility of IAD 2.1 Introduction... 1 2.2 Purpose... 2 2.3 Authority and responsibility...

April 20152016 Table of Contents 1 Introduction 1.1 Scope and purpose of the Manual... 1 2 Purpose, authority and responsibility of IAD 2.1 Introduction... 1 2.2 Purpose... 2 2.3 Authority and responsibility...

KING III CHECKLIST. We do it better

KING III CHECKLIST 2016 We do it better 1 KING III CHECKLIST African Rainbow Minerals Limited (ARM or the Company) supports the principles and practices set out in the King Report on Governance for South

KING III CHECKLIST 2016 We do it better 1 KING III CHECKLIST African Rainbow Minerals Limited (ARM or the Company) supports the principles and practices set out in the King Report on Governance for South

IMMUNOGEN, INC. CORPORATE GOVERNANCE GUIDELINES OF THE BOARD OF DIRECTORS

IMMUNOGEN, INC. CORPORATE GOVERNANCE GUIDELINES OF THE BOARD OF DIRECTORS Introduction As part of the corporate governance policies, processes and procedures of ImmunoGen, Inc. ( ImmunoGen or the Company

IMMUNOGEN, INC. CORPORATE GOVERNANCE GUIDELINES OF THE BOARD OF DIRECTORS Introduction As part of the corporate governance policies, processes and procedures of ImmunoGen, Inc. ( ImmunoGen or the Company

IMPARTIALITY. Impartiality and objectivity of auditors are basic prerequisites for an effective and consistent audit.

International Organization for Standardization ISO 9001 Auditing Practices Group Guidance on: International Accreditation Forum 13 January 2016 IMPARTIALITY Impartiality and objectivity of auditors are

International Organization for Standardization ISO 9001 Auditing Practices Group Guidance on: International Accreditation Forum 13 January 2016 IMPARTIALITY Impartiality and objectivity of auditors are

DIAMOND OFFSHORE DRILLING, INC. Corporate Governance Guidelines

Revised 19 October 2009 DIAMOND OFFSHORE DRILLING, INC. Corporate Governance Guidelines Introduction The following Corporate Governance Guidelines ( Guidelines ) have been adopted by the Board of Directors

Revised 19 October 2009 DIAMOND OFFSHORE DRILLING, INC. Corporate Governance Guidelines Introduction The following Corporate Governance Guidelines ( Guidelines ) have been adopted by the Board of Directors

EUROPEAN CONFEDERATION OF INSTITUTES OF INTERNAL AUDITING (IVZW)

") EUROPEAN CONFEDERATION OF INSTITUTES OF INTERNAL AUDITING (IVZW) Marie-Hélène Laimay PRESIDENT Thijs Smit VICE PRESIDENT Head Office: c/o IIA Belgium Koningstraat 109-111, bus 5 - B-1000 Brussels (Belgium)

EUROPEAN CONFEDERATION OF INSTITUTES OF INTERNAL AUDITING (IVZW) Marie-Hélène Laimay PRESIDENT Thijs Smit VICE PRESIDENT Head Office: c/o IIA Belgium Koningstraat 109-111, bus 5 - B-1000 Brussels (Belgium)

Strengthening Control and integrity: A Checklist for government Managers

Forum: Analytics and Risk Management Tools for Making Better Decisions Strengthening Control and integrity: A Checklist for government Managers By James A. Bailey The next contribution is based on a Center

Forum: Analytics and Risk Management Tools for Making Better Decisions Strengthening Control and integrity: A Checklist for government Managers By James A. Bailey The next contribution is based on a Center

CITIZENS BANCORP CITIZENS BANK BOARD AUDIT COMMITTEE CHARTER

CITIZENS BANCORP CITIZENS BANK BOARD AUDIT COMMITTEE CHARTER SCOPE It is the responsibility of the Board of Directors of Citizens Bancorp and its subsidiary, Citizens Bank (the Company ) to ensure the

CITIZENS BANCORP CITIZENS BANK BOARD AUDIT COMMITTEE CHARTER SCOPE It is the responsibility of the Board of Directors of Citizens Bancorp and its subsidiary, Citizens Bank (the Company ) to ensure the

NEWMARK GROUP, INC. AUDIT COMMITTEE CHARTER. (as of December 2017)

") NEWMARK GROUP, INC. AUDIT COMMITTEE CHARTER (as of December 2017) Purpose The Audit Committee of Newmark Group, Inc. (the Company ) is appointed by the Board of Directors of the Company (the Board ) to

NEWMARK GROUP, INC. AUDIT COMMITTEE CHARTER (as of December 2017) Purpose The Audit Committee of Newmark Group, Inc. (the Company ) is appointed by the Board of Directors of the Company (the Board ) to

The City of Kawartha Lakes Public Library

The City of Kawartha Lakes Public Library Policy number: LIB2017-18 Policy name: Job description of the Chief Executive Officer/Library Director Developed by: CEO/Chief Librarian Date: June 2014 Adoption

The City of Kawartha Lakes Public Library Policy number: LIB2017-18 Policy name: Job description of the Chief Executive Officer/Library Director Developed by: CEO/Chief Librarian Date: June 2014 Adoption

Self Assessment Workbook

Self Assessment Workbook Corporate Governance Audit Committee January 2018 Ce document est aussi disponible en français. Applicability The Self Assessment Workbook: Corporate Governance Audit Committee

Self Assessment Workbook Corporate Governance Audit Committee January 2018 Ce document est aussi disponible en français. Applicability The Self Assessment Workbook: Corporate Governance Audit Committee

REPORT 2016/033 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/033 Advisory engagement on the Statement on Internal Control project at the United Nations Joint Staff Pension Fund 25 April 2016 Assignment No. VS2015/800/01 CONTENTS

INTERNAL AUDIT DIVISION REPORT 2016/033 Advisory engagement on the Statement on Internal Control project at the United Nations Joint Staff Pension Fund 25 April 2016 Assignment No. VS2015/800/01 CONTENTS

2013 COSO Internal Control Framework Update. September 5, 2013

2013 COSO Internal Control Framework Update September 5, 2013 Agenda 2013 COSO IC Framework Topic Minutes The update process 5 What is not changing / What is changing 5 The 17 principles and changes to

2013 COSO Internal Control Framework Update September 5, 2013 Agenda 2013 COSO IC Framework Topic Minutes The update process 5 What is not changing / What is changing 5 The 17 principles and changes to