Agenda. What is EMV. Chip vs Mag Stripe. Benefits of EMV. Timeframes & Liability Shift. Costs. Things to consider. Questions

|

|

|

- Barrie Hart

- 6 years ago

- Views:

Transcription

1 EMV Chip Cards

2 Agenda What is EMV Chip vs Mag Stripe Benefits of EMV Timeframes & Liability Shift Costs Things to consider Questions 2

3 What is EMV EMV was named for the developers Europay, MasterCard and Visa. Embedded microprocessor chip that encrypts transaction data. Dynamic chip that changes verification values for each transaction. This is static on the magstripe. A set of specifications developed to define requirements to ensure interoperability between chip-based Credit, Debit and Prepaid cards and POS and ATM terminals. 3

4 EMV Chip Cards 1. Card Type: Contact (chip) contactless (tap or wave), Dual interface (both contact and contactless) 2. Card Authentication Method (CAM) Protects against counterfeit cards. EMV supports two methods Online authentication takes place between the chip and issuer host using dynamic cryptogram Offline authentication takes place between chip and terminal using static data 3. Cardholder Verification Method (CVM) Authenticates the cardholder. EMV supports four methods Online PIN- The PIN is stored at the issuer s processor, it is encrypted in POS terminal and sent to issuer s processor to verify Offline PIN- The PIN is stored in the chip and is sent from the POS terminal back to the card to validate Signature-Cardholders signature on the receipt is compared to signature on the card No CVM-No verification method is used. Typically low value transactions at unattended terminals 4. Authorization Transaction authorization Online-Transaction information is sent to issuer processor along with a transaction specific cryptogram and issuer processor authorizes or declines Offline-Card and terminal communicate and use issuer defined risk parameter 4

or swiped if terminal is not chip enabled Authentication can be offline or online enabled by computer chip in the card Issuer can")

5 Swipe vs Chip- How are they different? Magnetic Stripe EMV Chip Cards are swiped and read at POS terminal Authentication takes place between POS terminal & merchant acquirer Verification takes place through PIN or signature Authorization comes from processor or host processor Cards are Dipped (Contact) or waved (Contactless) or swiped if terminal is not chip enabled Authentication can be offline or online enabled by computer chip in the card Issuer can choose verification methods offline or online PIN, signature, no CVM Authorization comes from processor or host processor 5

6 What are the benefits of EMV? Increase security Liability shift Reduction in Card Present fraud, resulting from counterfeit transactions. Provides interoperability with the global payments infrastructure consumers with EMV chip payment cards can use their card on any EMV-compatible payment terminal anywhere inside or outside the U.S. 6

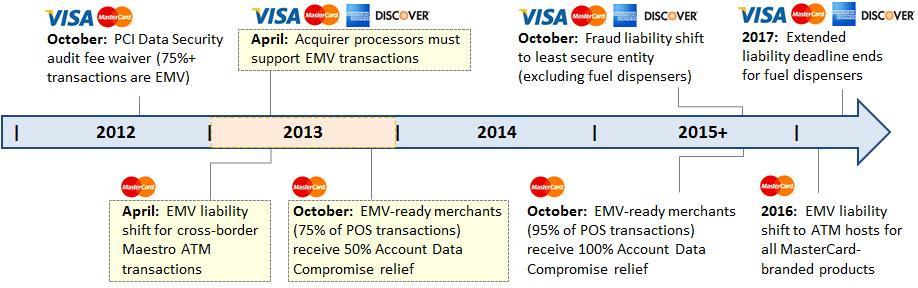

7 What are the timeframes? October 1, 2015 U.S. liability shift becomes effective for all card associations. The participant that does not support chip transactions will be held financially liable for any card present counterfeit fraud losses. Automated fuel dispensers (AFD) receive a two year grace period before the liability shift becomes effective for all card associations. (October 1, 2017) October 1, 2016 MasterCard ATM owners and operators will be financially liable for fraud that takes place at a non-emv enabled ATM, if the card is EMVcapable October 1, 2017 VISA ATM owners and operators will be financially liable for fraud that takes place at a non-emv enabled ATM if the card is EMVcapable. 7

8 What are the timeframes? Credit The TBS credit platform is chip capable today. VISA recommends implementation closer to the Liability shift which is October 1, The implementation process can be as little as 6 months or up to 8 months depending on standard vs custom programs. Debit Today the debit networks are working together toward a solution to the Durbin Amendment. Until the details and technical requirements to support EMV and the U.S. common AIDs (Application Identifier) is resolved, debit EMV does not have an implementation date yet. 8

9 What does all this mean? There is no mandate that says your credit union must use chip enabled cards; however, there is a liability shift that will take place starting October 1, 2015 The liability shift is on card present counterfeit fraud transactions. A non enabled merchant will be liable for fraud that occurs on a chip card used on a terminal that is not chip enabled. Magnetic stripes will continue to be on all cards for merchants & issuers to use if one or the other is not chip enabled. Card Present fraud will decrease as EMV is implemented. Card Not Present (CNP) fraud will likely increase 9

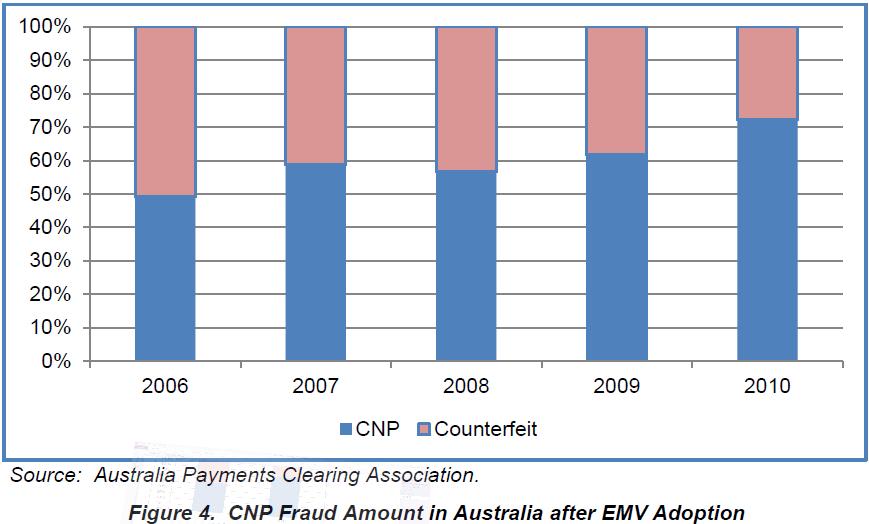

10 Fraud After Adoption 10

11 Global Adoption 11

12 Things to consider Goals Costs Increase Acceptance Worldwide Prepare for the Liability Shift An Emerging Technology Leader Implementation Fees Set Up Fees Monthly Recurring Fees Roll Out Plastic Education 12

13 13

14 14

15 15

16 16

17 Merchant and Card Issuer Readiness EMV in USA: Assessment of Merchant and Card Issuer Readiness 17

18 Merchant and Card Issuer Readiness U.S. to reach global parity in EMV by 2018 Industry ready to convert 1.2 Billion EMV Payment Cards and 8 Million POS terminals for EMV transition. By the end of 2015, it is forecasted that 166 million EMV credit cards will be in circulation in the U.S. (29% of the total), and 105 million EMV debit and prepaid cards (17% of the total). 18

19 The U.S. migration to secure chip-based EMV payments requires new activities and collaboration 19

20 Multiple Form Factors, Multiple Communications Links 20

21 21

22 Visa, MasterCard Agree on Common AID for EMV Debit Routing BY DAVID HEUN JUL 1, :15pm ET EMV Migration Forum: Use Single Code for Debit Transactions Visa and MasterCard have agreed to share their common application identifier technology, enabling EMV-chip based debit transactions to originate from a single application while allowing merchants a choice of networks for routing. The agreement is a major step toward resolving a longstanding dispute within the payments industry over how to adapt EMV payment technology to U.S. regulation. The licensing agreement between the two major card brands provides for "a multi-access common AID that all others can adopt" and supports the single-code recommendation of the EMV Migration Forum, says Stephanie Ericksen, Visa's head of authentication product integration. The agreement comes less than a week after the Secure Remote Payments Council, representing independent debit networks, announced what it considered a major concession in agreeing to allow Visa and MasterCard applications on their debit cards after earlier committing to Discover's common AID. The debate over EMV debit routing has raged for more than a year as debit networks preparing for EMV smart cards in the U.S. deal with Durbin amendment requirements that call for at least two network options. The U.S. is the only country with multiple debit networks and federal mandates for routing. "We are pleased to be able to offer a cost-effective option for acquirers and issuers for merchant routing choice through a single common AID," says Carolyn Balfany, MasterCard's senior vice president and group head of U.S. product delivery. 22

23 Visa s Counterfeit Liability Shift Policies Visa s Counterfeit Liability Shift Policies VISA BULLETIN 9 August 2011 Visa intends to institute a liability shift in the U.S. for domestic and cross-border counterfeit transactions effective 1 October Visa s global POS counterfeit liability shift policies are designed to encourage EMV chip card issuance and acceptance in participating geographical regions, effectively creating a more secure environment for transactions within and between each participating Visa region. Note: The liability shift encourages chip transactions because any chip-on-chip transaction (i.e., a chip card read by a chip terminal) provides dynamic authentication data, which helps to better protect all parties. With this type of liability shift, the party that is the cause of a chip-onchip transaction not occurring (i.e., either the issuer or the merchant s acquirer) will be financially liable for any resulting card-present counterfeit fraud losses. When a transaction occurs using chip technology, any liability for counterfeit fraud, though unlikely, would follow current Visa Operating Regulations. The policy assigns liability for counterfeit fraud to the party that has not made the investment in EMV chip cards (issuers) or terminals (merchants acquirers). The policy encourages wider deployment of EMV cards and terminals. EMV chip implementation is accelerating globally. Today, excluding the U.S., 44 percent of all cards are EMV chip cards, and 74 percent of all terminals are EMV chip-capable, with 62 percent of cross-border trans October, 2015 Fraud Liability Shift. MasterCard liability hierarchy takes effect. The party that has made investment in the most secure EMV options is protected from financial liability for card-present fraud losses for both counterfeit and lost, stolen and non-receipt fraud on this date. October, 2015 Account Data Compromise Relief: On this date, if at least 95% of MasterCard transactions originate from EMV-compliant POS terminals, the merchant is relieved of 100% of account data compromise penalties. 23

24 Specification Bulletins EMVCo technology Publicati on Date Septemb er 2014 Septemb er 2014 Septemb er 2014 Septemb er 2014 August 2014 August 2014 Versi on 1st Editi on 1st Editi on 1st Editi on 1st Editi on 1st Editi on 2nd Editi on Description SB-148: Clarification on Terminal Support of Multiple Application Version Numbers per AID (Spec Change) SB-147: Clarification on the Format of Exponent Data Elements (Spec Change) SB-146: Entry Point Final Combination Selection (Spec Change) SB-145: Clarification on the Format of ICC Public Key Exponent (Spec Change) SB-142: User Interaction Parameters for Installation of Contactless Mobile Payment Applications (Spec Change) SB-119: Clarifies Group Member CREL & FCI contactless characteristic declarations, clarifies length of Base AID (Spec Change) Download Download Download Download Download Download Download 24

25 Worldwide EMV Card and Terminal Deployment The statistics below show worldwide EMV deployment figures as of Q The figures represent the latest statistics from American Express, Discover, JCB, MasterCard, UnionPay, and Visa, as reported by their member financial institutions globally. 25

26 26

27 27

28 Questions???? Please contact 28

29 Thank You 29

Is Your Organization Ready for the EMV Challenge?

Is Your Organization Ready for the EMV Challenge? Suzanne Galvin Director of Product Management Elan Financial Services Jeff Green Director of the Emerging Technologies Advisory Service Mercator Advisory

Is Your Organization Ready for the EMV Challenge? Suzanne Galvin Director of Product Management Elan Financial Services Jeff Green Director of the Emerging Technologies Advisory Service Mercator Advisory

EMV Chip Cards. Table of Contents GENERAL BACKGROUND GENERAL FAQ FREQUENTLY ASKED QUESTIONS GENERAL BACKGROUND...1 GENERAL FAQ MERCHANT FAQ...

EMV Chip Cards FREQUENTLY ASKED QUESTIONS Table of Contents GENERAL BACKGROUND...1 GENERAL FAQ...1 4 MERCHANT FAQ...5 PROCESSOR/ATM PROCESSOR FAQ... 6 ISSUER FAQ... 6 U.S.-SPECIFIC FAQ...7 8 GENERAL BACKGROUND

EMV Chip Cards FREQUENTLY ASKED QUESTIONS Table of Contents GENERAL BACKGROUND...1 GENERAL FAQ...1 4 MERCHANT FAQ...5 PROCESSOR/ATM PROCESSOR FAQ... 6 ISSUER FAQ... 6 U.S.-SPECIFIC FAQ...7 8 GENERAL BACKGROUND

EMV is coming. Here s how to stay ahead of the trend. Presented by CO-OP Financial Services

EMV is coming. Here s how to stay ahead of the trend. Presented by CO-OP Financial Services October 25, 2012 Agenda What EMV is and how it works U.S. and global adoption Impact to the payments ecosystem

EMV is coming. Here s how to stay ahead of the trend. Presented by CO-OP Financial Services October 25, 2012 Agenda What EMV is and how it works U.S. and global adoption Impact to the payments ecosystem

EMV: Facts at a Glance

EMV: Facts at a Glance 1. What is EMV? EMV is an open-standard set of specifications for smart card payments and acceptance devices. The EMV specifications were developed to define a set of requirements

EMV: Facts at a Glance 1. What is EMV? EMV is an open-standard set of specifications for smart card payments and acceptance devices. The EMV specifications were developed to define a set of requirements

EMV is coming. But it s ever changing.

EMV is coming. But it s ever changing. March 26, 2013 Presented By MICHELLETHORNTON Senior Product Manager CO-OP Financial Services RYANZILKER B2B Marketing Manager CO-OP Financial Services Today s Agenda

EMV is coming. But it s ever changing. March 26, 2013 Presented By MICHELLETHORNTON Senior Product Manager CO-OP Financial Services RYANZILKER B2B Marketing Manager CO-OP Financial Services Today s Agenda

EMV and Educational Institutions:

October 2014 EMV and Educational Institutions: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks,

October 2014 EMV and Educational Institutions: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks,

ATM Webinar Questions and Answers May, 2014

May, 2014 Debit Network Alliance LLC (DNA) is a Delaware Limited Liability Company currently comprised of 10 U.S. Debit Networks and open to all U.S. Debit Networks. The goal of this collaborative effort

May, 2014 Debit Network Alliance LLC (DNA) is a Delaware Limited Liability Company currently comprised of 10 U.S. Debit Networks and open to all U.S. Debit Networks. The goal of this collaborative effort

Understanding the 2015 U.S. Fraud Liability Shifts

Understanding the 2015 U.S. Fraud Liability Shifts Version 1.0 May 2015 Some U.S. payment networks are implementing EMV fraud liability shifts effective October 2015. With these liability shifts fast approaching,

Understanding the 2015 U.S. Fraud Liability Shifts Version 1.0 May 2015 Some U.S. payment networks are implementing EMV fraud liability shifts effective October 2015. With these liability shifts fast approaching,

EMV Migration. What You Need to Know about the Technology, the Security Protection it Provides, and When to Implement

EMV Migration What You Need to Know about the Technology, the Security Protection it Provides, and When to Implement According to a 2016 TSYS study identifying consumer payment preferences, 40 percent

EMV Migration What You Need to Know about the Technology, the Security Protection it Provides, and When to Implement According to a 2016 TSYS study identifying consumer payment preferences, 40 percent

Card Payment acceptance at Common Use positions at airports

Card Payment acceptance at Common Use s at airports Business requirements Version 1, published in June 2016 Preamble Common Use (CU) touchpoints (self-service s such as self-service kiosks or bag drops,

Card Payment acceptance at Common Use s at airports Business requirements Version 1, published in June 2016 Preamble Common Use (CU) touchpoints (self-service s such as self-service kiosks or bag drops,

Top 5 Facts Merchants Need To Know About EMV

Top 5 Facts Merchants Need To Know About EMV June, 2015 Lindsay Breathitt, Product Marketing Steve Cole, Product Management Why EMV, Why Now Agenda U.S. market update EMV Top 5 EMV facts Understanding

Top 5 Facts Merchants Need To Know About EMV June, 2015 Lindsay Breathitt, Product Marketing Steve Cole, Product Management Why EMV, Why Now Agenda U.S. market update EMV Top 5 EMV facts Understanding

E M V O V E R V I E W. July 2014

E M V O V E R V I E W July 2014 A G E N D A EMV Overview EMV Industry Announcements EMV Transaction Differences, What to Expect Solution Decisions Market Certification Considerations Questions 2 E M V

E M V O V E R V I E W July 2014 A G E N D A EMV Overview EMV Industry Announcements EMV Transaction Differences, What to Expect Solution Decisions Market Certification Considerations Questions 2 E M V

EMV Just the Facts. Ozarks Association of Government Accountants

EMV Just the Facts Ozarks Association of Government Accountants Speakers and Housekeeping EMV: Just the Facts Presentation Brad Hench Regional Sales Manager US Bank Elavon 45 minute presentation 10 minute

EMV Just the Facts Ozarks Association of Government Accountants Speakers and Housekeeping EMV: Just the Facts Presentation Brad Hench Regional Sales Manager US Bank Elavon 45 minute presentation 10 minute

EMV: Frequently Asked Questions for Merchants

EMV: Frequently Asked Questions for Merchants The information in this document is offered on an as is basis, without warranty of any kind, either expressed, implied or statutory, including but not limited

EMV: Frequently Asked Questions for Merchants The information in this document is offered on an as is basis, without warranty of any kind, either expressed, implied or statutory, including but not limited

Card Payments Roadmap in the United States: How Will EMV Impact the Future Payments Infrastructure?

Card Payments Roadmap in the United States: How Will EMV Impact the Future Payments Infrastructure? A Smart Card Alliance Payments Council White Paper Publication/Update Date: January 2013 Publication

Card Payments Roadmap in the United States: How Will EMV Impact the Future Payments Infrastructure? A Smart Card Alliance Payments Council White Paper Publication/Update Date: January 2013 Publication

PayPass M/Chip Requirements. 3 July 2013

PayPass M/Chip Requirements 3 July 2013 Notices Following are policies pertaining to proprietary rights, trademarks, translations, and details about the availability of additional information online. Proprietary

PayPass M/Chip Requirements 3 July 2013 Notices Following are policies pertaining to proprietary rights, trademarks, translations, and details about the availability of additional information online. Proprietary

EMV Adoption in the U.S.

EMV Adoption in the U.S. What you need to know about the outcome of EMV adoption in other countries and the implications for adoption in the U.S. Table of Contents Introduction [3] What is EMV? [4] The

EMV Adoption in the U.S. What you need to know about the outcome of EMV adoption in other countries and the implications for adoption in the U.S. Table of Contents Introduction [3] What is EMV? [4] The

EMV, PCI, Tokenization, Encryption What You Should Know for Presented by: The Bryan Cave Payments Team

EMV, PCI, Tokenization, Encryption What You Should Know for 2015 Presented by: The Bryan Cave Payments Team Agenda Overview of Secured Payments Judie Rinearson (NY) EMV Courtney Stout (DC) End to End Encryption

EMV, PCI, Tokenization, Encryption What You Should Know for 2015 Presented by: The Bryan Cave Payments Team Agenda Overview of Secured Payments Judie Rinearson (NY) EMV Courtney Stout (DC) End to End Encryption

EMV: The Journey Begins October 1st

221 NORTH LASALLE ST. CHICAGO, IL 60601 312-873-3300 INFO@WCAPRA.COM EMV: The Journey Begins October 1st An Examination of the History, Impact, Best Practices, Pitfalls of EMV Implementations, and What

221 NORTH LASALLE ST. CHICAGO, IL 60601 312-873-3300 INFO@WCAPRA.COM EMV: The Journey Begins October 1st An Examination of the History, Impact, Best Practices, Pitfalls of EMV Implementations, and What

Cards on the table! Bernd Filsinger Payment Technology Services Lead Client Support Services, Europe region

Cards on the table! Bernd Filsinger Payment Technology Services Lead Client Support Services, Europe region Notice of confidentiality This presentation is furnished to you solely in your capacity as a

Cards on the table! Bernd Filsinger Payment Technology Services Lead Client Support Services, Europe region Notice of confidentiality This presentation is furnished to you solely in your capacity as a

EMV & Fraud POS Fraud Mitigation Tips for Merchants First Data Corporation. All Rights Reserved.

EMV & Fraud POS Fraud Mitigation Tips for Merchants EMV Information Merchants may see an increase in Card-Not-Present Fraud as a result of the new EMV standards. Help protect your business from fraud risk

EMV & Fraud POS Fraud Mitigation Tips for Merchants EMV Information Merchants may see an increase in Card-Not-Present Fraud as a result of the new EMV standards. Help protect your business from fraud risk

Technology Developments in Card-Based Payments WACHA Payments 2013

Technology Developments in Card-Based Payments WACHA Payments 2013 April 9, 2013 The information contained on these slides is considered the Confidential & Proprietary Information of Two Sparrows Consulting,

Technology Developments in Card-Based Payments WACHA Payments 2013 April 9, 2013 The information contained on these slides is considered the Confidential & Proprietary Information of Two Sparrows Consulting,

Pinless Transaction Clarifications

Pinless Transaction Clarifications April, 2017 Agenda Definition Level Set Application Selection Overview and Scenario Explanation EMV No CVM PIN Bypass Debit Expansion Programs PINless POS Product Signature

Pinless Transaction Clarifications April, 2017 Agenda Definition Level Set Application Selection Overview and Scenario Explanation EMV No CVM PIN Bypass Debit Expansion Programs PINless POS Product Signature

EMV: Coming Soon to a Card Near You

Julie Conroy EMV: Coming Soon to a Card Near You Page 2 This presentation is the work of its author who is solely responsible for its contents. First Data Corporation and its subsidiaries and affiliates

Julie Conroy EMV: Coming Soon to a Card Near You Page 2 This presentation is the work of its author who is solely responsible for its contents. First Data Corporation and its subsidiaries and affiliates

U.S. Bank. U.S. Bank Chip Card FAQs for Program Administrators. In this guide you will fnd: Explaining Chip Card Technology (EMV)

") U.S. Bank U.S. Bank Chip Card FAQs for Program Administrators Here are some frequently asked questions Program Administrators have about the replacement of U.S. Bank commercial cards with new chip-enabled

U.S. Bank U.S. Bank Chip Card FAQs for Program Administrators Here are some frequently asked questions Program Administrators have about the replacement of U.S. Bank commercial cards with new chip-enabled

EMV IN THE U.S. HOW FAR HAVE WE COME AND WHERE ARE WE GOING? Andy Brown

EMV IN THE U.S. HOW FAR HAVE WE COME AND WHERE ARE WE GOING? Andy Brown andy.brown@ncr.com MAC is an organization comprised of members from Banks, Acquirers, ISOs, Card Associations, Law Enforcement and

EMV IN THE U.S. HOW FAR HAVE WE COME AND WHERE ARE WE GOING? Andy Brown andy.brown@ncr.com MAC is an organization comprised of members from Banks, Acquirers, ISOs, Card Associations, Law Enforcement and

The Changing Landscape of Card Acceptance

The Changing Landscape of Card Acceptance Troy Byram Vice-President Sr. E-Receivables Consultant February 6, 2015 Agenda EMV (Chip and Pin) PCI Compliance and Data Security New Regulations for Municipalities

The Changing Landscape of Card Acceptance Troy Byram Vice-President Sr. E-Receivables Consultant February 6, 2015 Agenda EMV (Chip and Pin) PCI Compliance and Data Security New Regulations for Municipalities

A Guide to. US EMV Migration

A Guide to US EMV Migration Table of Contents What is EMV?... 3 EMV: A Global Standard... 4 Fraud Prevention... 5 Mobile & Contactless... 6 U.S. EMV Deadlines... 7 Maestro Liability Shift... 8 U.S. EMV

A Guide to US EMV Migration Table of Contents What is EMV?... 3 EMV: A Global Standard... 4 Fraud Prevention... 5 Mobile & Contactless... 6 U.S. EMV Deadlines... 7 Maestro Liability Shift... 8 U.S. EMV

Optimizing Transaction Speed at the POS

Optimizing Transaction Speed at the POS Version 3.0 Date: October 2017 U.S. Payments Forum 2017 Page 1 About the U.S. Payments Forum The U.S. Payments Forum, formerly the EMV Migration Forum, is a cross-industry

Optimizing Transaction Speed at the POS Version 3.0 Date: October 2017 U.S. Payments Forum 2017 Page 1 About the U.S. Payments Forum The U.S. Payments Forum, formerly the EMV Migration Forum, is a cross-industry

Visa Minimum U.S. Online Only Terminal Configuration

Visa Minimum U.S. Online Only Terminal Configuration Intended Audience This document is intended for U.S. merchants, acquirers, processors and terminal providers who are planning deployments of EMV chip

Visa Minimum U.S. Online Only Terminal Configuration Intended Audience This document is intended for U.S. merchants, acquirers, processors and terminal providers who are planning deployments of EMV chip

Tokenization April Tokenization. Gregory H. Soule, CPA, CISA, CISSP, CFE Senior Manager. Andrews Hooper Pavlik PLC

ization Gregory H. Soule, CPA, CISA, CISSP, CFE Senior Manager Andrews Hooper Pavlik PLC 1 Agenda and Implementation EMV, Encryption, ization Apple Pay Google Wallet Recent Trends Resources Agenda and

ization Gregory H. Soule, CPA, CISA, CISSP, CFE Senior Manager Andrews Hooper Pavlik PLC 1 Agenda and Implementation EMV, Encryption, ization Apple Pay Google Wallet Recent Trends Resources Agenda and

Canada EMV Test Card Set Summary

Canada EMV Test Card Set Summary.90 January, 2018 Powered by Disclaimer Information provided in this document describes capabilities available at the time of developing this document and information available

Canada EMV Test Card Set Summary.90 January, 2018 Powered by Disclaimer Information provided in this document describes capabilities available at the time of developing this document and information available

EMVCo: Operating Principles

EMVCo: Operating Principles This document provides an overview of EMVCo s operating principles, including its governance, operations and the role of EMV Specifications in the wider payments community.

EMVCo: Operating Principles This document provides an overview of EMVCo s operating principles, including its governance, operations and the role of EMV Specifications in the wider payments community.

The Future of Payment Security in Canada

The Future of Payment Security in Canada October 2017 1 Visa Canada Public The Future of Payment Security in Canada Notices Forward-Looking Statements This presentation contains forward-looking statements

The Future of Payment Security in Canada October 2017 1 Visa Canada Public The Future of Payment Security in Canada Notices Forward-Looking Statements This presentation contains forward-looking statements

EMV. When to Wait and When to Move

EMV When to Wait and When to Move Welcome CO-OP and TMG: Leaders in Innovation Michelle Thornton Senior Product Manager CO-OP Financial Services Brandon Kuehl Product Development Architect The Members

EMV When to Wait and When to Move Welcome CO-OP and TMG: Leaders in Innovation Michelle Thornton Senior Product Manager CO-OP Financial Services Brandon Kuehl Product Development Architect The Members

A Merc r ator r Adv d i v sory y Gr G oup Re R search h Br B ief S p S onsored d by J nu n a u ry

EMV ESSENTIALS FOR THE U.S. MERCHANT January 201 1 12 About Heartland Heartland, Inc. (NYSE: HPY), the fifth largest payments processor in the United States, delivers credit/ /debit/prepaidd card processing,

EMV ESSENTIALS FOR THE U.S. MERCHANT January 201 1 12 About Heartland Heartland, Inc. (NYSE: HPY), the fifth largest payments processor in the United States, delivers credit/ /debit/prepaidd card processing,

Tokenization: What, Why and How

Tokenization: What, Why and How 11/5/2015 UL Transaction Security 2011 Underwriters Laboratories Inc. We have EMV why do we need tokenization? From Magstripe Merchant Signature Issuer Magstripe Risk Management

Tokenization: What, Why and How 11/5/2015 UL Transaction Security 2011 Underwriters Laboratories Inc. We have EMV why do we need tokenization? From Magstripe Merchant Signature Issuer Magstripe Risk Management

Contactless Toolkit for Acquirers

MASTERCARD AND MAESTRO CONTACTLESS PAYMENTS Contactless Toolkit for Acquirers DECEMBER 2016 19.7% The Global Contactless Payment Market is poised to grow at a CAGR of around 19.7% over the next decade

MASTERCARD AND MAESTRO CONTACTLESS PAYMENTS Contactless Toolkit for Acquirers DECEMBER 2016 19.7% The Global Contactless Payment Market is poised to grow at a CAGR of around 19.7% over the next decade

USA EMV Test Card Set Summary

USA EMV Test Card Set Summary.80 January, 2018 Powered by Disclaimer Information provided in this document describes capabilities available at the time of developing this document and information available

USA EMV Test Card Set Summary.80 January, 2018 Powered by Disclaimer Information provided in this document describes capabilities available at the time of developing this document and information available

Seeds of Change in Debit

Seeds of Change in Debit The 2016 Debit Issuer Study MEDIA EXHIBITS Study Overview The Debit Issuer Study is the definitive assessment of U.S. debit market 2016 Debit Issuer Study is the 11th edition of

Seeds of Change in Debit The 2016 Debit Issuer Study MEDIA EXHIBITS Study Overview The Debit Issuer Study is the definitive assessment of U.S. debit market 2016 Debit Issuer Study is the 11th edition of

Acquirer JCB EMV Test Card Set Summary

Acquirer JCB EMV Test Card Set Summary July, 2017 Powered by Disclaimer Information provided in this document describes capabilities available at the time of developing this document and information available

Acquirer JCB EMV Test Card Set Summary July, 2017 Powered by Disclaimer Information provided in this document describes capabilities available at the time of developing this document and information available

EMV : One year later. Merchants take steps to adapt and address challenges in the year following the shift to EMV technology at the point of sale

EMV : One year later Merchants take steps to adapt and address challenges in the year following the shift to EMV technology at the point of sale EMV: ONE YEAR LATER A BANK OF AMERICA MERCHANT SERVICES

EMV : One year later Merchants take steps to adapt and address challenges in the year following the shift to EMV technology at the point of sale EMV: ONE YEAR LATER A BANK OF AMERICA MERCHANT SERVICES

Smart Cards and EMV Adoption in China

Smart Cards and EMV Adoption in China Opportunities and Obstacles Emerging Strategy www.emerging-strategy.com August, 2008 Table of Contents Background... 2 Global Drivers for EMV Migration... 3 Migration

Smart Cards and EMV Adoption in China Opportunities and Obstacles Emerging Strategy www.emerging-strategy.com August, 2008 Table of Contents Background... 2 Global Drivers for EMV Migration... 3 Migration

Protecting Your Future

Protecting Your Future with NCR Secure How to prepare for the EMV and Windows 7 Migration An NCR White Paper 02 1 Upcoming Major Changes and Trends The North American financial industry will go through

Protecting Your Future with NCR Secure How to prepare for the EMV and Windows 7 Migration An NCR White Paper 02 1 Upcoming Major Changes and Trends The North American financial industry will go through

Security enhancement on HSBC India Debit Card

Security enhancement on HSBC India Debit Card A Secure Debit Card HSBC India Debit Cards are more secure and enabled with the Chip and PIN technology. In addition to this you can restrict usage of the

Security enhancement on HSBC India Debit Card A Secure Debit Card HSBC India Debit Cards are more secure and enabled with the Chip and PIN technology. In addition to this you can restrict usage of the

I N T E R A C. The Faster, More Convenient Way. Small Value Purchases

I N T E R A C I S S U I N G F L A S H The Faster, More Convenient Way to Securely Accept Payment For Small Value Purchases Trade-mark of Interac Inc. (Everlink Payment Services Inc.) authorized user of

I N T E R A C I S S U I N G F L A S H The Faster, More Convenient Way to Securely Accept Payment For Small Value Purchases Trade-mark of Interac Inc. (Everlink Payment Services Inc.) authorized user of

Collis/B2 EMV & Contactless Offering

Collis/B2 EMV & Contactless Offering USA Migration Bruce Murray, B2PS Itai Sela, B2PS January 2012 Ensuring Trust in Technology 1 Overview Introduction to EMV and Contactless in the USA B2 Training Programs

Collis/B2 EMV & Contactless Offering USA Migration Bruce Murray, B2PS Itai Sela, B2PS January 2012 Ensuring Trust in Technology 1 Overview Introduction to EMV and Contactless in the USA B2 Training Programs

Securing Card Payments Challenges & Opportunities. Julie Hanson Senior Vice President, Card & Payment Products ICBA Bancard & TCM Bank, NA

Securing Card Payments Challenges & Opportunities Julie Hanson Senior Vice President, Card & Payment Products ICBA Bancard & TCM Bank, NA Agenda Securing Payments Landscape Chip Technology Tokenization

Securing Card Payments Challenges & Opportunities Julie Hanson Senior Vice President, Card & Payment Products ICBA Bancard & TCM Bank, NA Agenda Securing Payments Landscape Chip Technology Tokenization

Merchant Services What You Need to Know. Agenda 6/5/2017. Overview of Merchant Services. EMV, Tokenization/Encryption, and PCI (Oh My!

Merchant Services What You Need to Know Heather Nowak VP, CPP Senior Product Manager Agenda Overview of Merchant Services Why accept cards? What you need to know/consider Capabilities/Pricing/Contract

Merchant Services What You Need to Know Heather Nowak VP, CPP Senior Product Manager Agenda Overview of Merchant Services Why accept cards? What you need to know/consider Capabilities/Pricing/Contract

JTC Resource Bulletin. EMV and Credit Card Liability: What Courts Need to Know

JTC Resource Bulletin EMV and Credit Card Liability: What Courts Need to Know Adopted December 5, 2014 Abstract Nearly every country in the world uses the global standard called EMV (short for Europay,

JTC Resource Bulletin EMV and Credit Card Liability: What Courts Need to Know Adopted December 5, 2014 Abstract Nearly every country in the world uses the global standard called EMV (short for Europay,

Mobile Payment Platforms For The Artist

Mobile Payment Platforms For The Artist Navigating Square & PayPal On The Go Presented by Renee Ford of Renee Ford Metals Mobile Payment Options Available Square Accept Visa, MasterCard, Discover, and

Mobile Payment Platforms For The Artist Navigating Square & PayPal On The Go Presented by Renee Ford of Renee Ford Metals Mobile Payment Options Available Square Accept Visa, MasterCard, Discover, and

The Shared Electronic Banking Services Company (KNET) Knet securing E-payment for EGOV

Knet securing E-payment for EGOV") The Shared Electronic Banking Services Company (KNET) Knet securing E-payment for EGOV November 21, 2015 Knet 2 The Shared Electronic Banking Services Company (Knet) was established in 1992. Knet Established

The Shared Electronic Banking Services Company (KNET) Knet securing E-payment for EGOV November 21, 2015 Knet 2 The Shared Electronic Banking Services Company (Knet) was established in 1992. Knet Established

EMV 3-D Secure Press Kit Q&A

EMV 3-D Secure Press Kit Q&A 1. What is EMV 3-D Secure? EMV Three-Domain Secure (3DS) is a messaging protocol that enables frictionless consumer authentication and the ability for consumers to authenticate

EMV 3-D Secure Press Kit Q&A 1. What is EMV 3-D Secure? EMV Three-Domain Secure (3DS) is a messaging protocol that enables frictionless consumer authentication and the ability for consumers to authenticate

KNOW YOUR RUPAY DEBIT CARD

KNOW YOUR RUPAY DEBIT CARD ABSTRACT The objective of this document is to introduce the member banks to RuPay Debit Card program and to guide the issuing banks on the RuPay Debit Card features including

KNOW YOUR RUPAY DEBIT CARD ABSTRACT The objective of this document is to introduce the member banks to RuPay Debit Card program and to guide the issuing banks on the RuPay Debit Card features including

EMV ESSENTIALS EMV U.S. ISSUERS FOR AND MERCHANTS. Essentials for U.S. Issuers and Merchants A Mercator Advisory Group Whitepaper Sponsored by SHAZAM

EMV ESSENTIALS FOR U.S. ISSUERS AND MERCHANTS 2010 Mercator Advisory September 201 1 12 About SHAZAM Mission To provide and enhance the opportunity for SHAZAM-affiliated financial institutions to compete

EMV ESSENTIALS FOR U.S. ISSUERS AND MERCHANTS 2010 Mercator Advisory September 201 1 12 About SHAZAM Mission To provide and enhance the opportunity for SHAZAM-affiliated financial institutions to compete

EMV Migration for the US Parking Industry EMV and the Parking Industry

EMV and the Parking Industry May 2013 Contents Introduction 03 What is EMV 04 Why EMV Matters 06 to Parking Overcoming the 08 Challenges Case Study 10 Best Practice Tips for 11 EMV Migration About Creditcall

EMV and the Parking Industry May 2013 Contents Introduction 03 What is EMV 04 Why EMV Matters 06 to Parking Overcoming the 08 Challenges Case Study 10 Best Practice Tips for 11 EMV Migration About Creditcall

EMV * Contactless Specifications for Payment Systems

EMV * Contactless Specifications for Payment Systems Book A Architecture and General Requirements Version 2.6 March 2016 * EMV is a registered trademark or trademark of EMVCo LLC in the United States permitted

EMV * Contactless Specifications for Payment Systems Book A Architecture and General Requirements Version 2.6 March 2016 * EMV is a registered trademark or trademark of EMVCo LLC in the United States permitted

Point-of-Sale Terminals

Point-of-Sale Terminals The Right Hardware for the Job SIMPLE, SECURE PAYMENT PROCESSING Your customers can be anywhere. And no matter where they are, they expect you to process their payments easily and

Point-of-Sale Terminals The Right Hardware for the Job SIMPLE, SECURE PAYMENT PROCESSING Your customers can be anywhere. And no matter where they are, they expect you to process their payments easily and

Ensuring the Safety & Security of Payments. Faster Payments Symposium August 4, 2015

Ensuring the Safety & Security of Payments Faster Payments Symposium August 4, 2015 Problem Statement: The proliferation of live consumer account credentials Bank issues physical card Plastic at point

Ensuring the Safety & Security of Payments Faster Payments Symposium August 4, 2015 Problem Statement: The proliferation of live consumer account credentials Bank issues physical card Plastic at point

Horizontal Integration in the Payments Industry

Horizontal Integration in the Payments Industry Gerard Hartsink Senior Executive Vice President 2007 Payments Conference Santa Fe, 3 May 2007 Content European landscape Restructuring of functions Impact

Horizontal Integration in the Payments Industry Gerard Hartsink Senior Executive Vice President 2007 Payments Conference Santa Fe, 3 May 2007 Content European landscape Restructuring of functions Impact

EMV Testing and Certification White Paper: Current Global Payment Network Requirements for the U.S. Acquiring Community

AN EMV MIGRATION FORUM TESTING AND CERTIFICATION WORKING COMMITTEE WHITE PAPER EMV Testing and Certification White Paper: Current Global Payment Network Requirements for the U.S. Acquiring Community Version

AN EMV MIGRATION FORUM TESTING AND CERTIFICATION WORKING COMMITTEE WHITE PAPER EMV Testing and Certification White Paper: Current Global Payment Network Requirements for the U.S. Acquiring Community Version

Quick Guide. Token Service Provider

Quick Guide Token Service Provider 1 Introduction to Mobile Payments The mobile payments revolution is here! Driven by the development of near field communication (NFC) enabled smartphones, the launch

Quick Guide Token Service Provider 1 Introduction to Mobile Payments The mobile payments revolution is here! Driven by the development of near field communication (NFC) enabled smartphones, the launch

Euronet s Dynamic Currency Conversion Solution Increase Your Revenue as an Acquirer with a Value Added Service

Serving millions of people worldwide with electronic payment convenience. Euronet s Dynamic Currency Conversion Solution Increase Your Revenue as an Acquirer with a Value Added Service Copyright 2010 Euronet

Serving millions of people worldwide with electronic payment convenience. Euronet s Dynamic Currency Conversion Solution Increase Your Revenue as an Acquirer with a Value Added Service Copyright 2010 Euronet

CANADIAN PAYMENTS ASSOCIATION ASSOCIATION CANADIENNE DES PAIEMENTS RULE E4

CANADIAN PAYMENTS ASSOCIATION ASSOCIATION CANADIENNE DES PAIEMENTS RULE E4 EXCHANGE OF PIN-LESS POINT-OF-SERVICE DEBIT PAYMENT ITEMS FOR THE PURPOSE OF CLEARING AND SETTLEMENT 2016 CANADIAN PAYMENTS ASSOCIATION

CANADIAN PAYMENTS ASSOCIATION ASSOCIATION CANADIENNE DES PAIEMENTS RULE E4 EXCHANGE OF PIN-LESS POINT-OF-SERVICE DEBIT PAYMENT ITEMS FOR THE PURPOSE OF CLEARING AND SETTLEMENT 2016 CANADIAN PAYMENTS ASSOCIATION

Visa Digital Solutions. Rocio Beckham Community Issuers

Visa Digital Solutions Rocio Beckham Community Issuers Notice of Confidentiality This presentation is furnished to you solely in your capacity as a customer of Visa and/or participant in the Visa payments

Visa Digital Solutions Rocio Beckham Community Issuers Notice of Confidentiality This presentation is furnished to you solely in your capacity as a customer of Visa and/or participant in the Visa payments

MOBILE CHECKOUT SOLUTION

MOBILE CHECKOUT SOLUTION MONEXgroup in this report introduces the Mobile Checkout Solution for merchants who process payments on-the-go using their Smartphone devices. Mobile Checkout allows businesses

MOBILE CHECKOUT SOLUTION MONEXgroup in this report introduces the Mobile Checkout Solution for merchants who process payments on-the-go using their Smartphone devices. Mobile Checkout allows businesses

Helping merchants automate testing practices.

Helping merchants automate testing practices. Meet deadlines, facilitate certifications and overcome complexities. www.fisglobal.com As a merchant, you are in the middle of the shift from traditional cash

Helping merchants automate testing practices. Meet deadlines, facilitate certifications and overcome complexities. www.fisglobal.com As a merchant, you are in the middle of the shift from traditional cash

The Migration to EMV in the USA from a Founders Perspective. Philip Andreae Oberthur Technologies

The Migration to EMV in the USA from a Founders Perspective Philip Andreae Oberthur Technologies Chip Card Contact multisim Identity Card Passport SIM card Access Control Identity Dual Card Form Factors

The Migration to EMV in the USA from a Founders Perspective Philip Andreae Oberthur Technologies Chip Card Contact multisim Identity Card Passport SIM card Access Control Identity Dual Card Form Factors

HEADLINE INSIGHTS ON HERE EMV TRANSACTION SPEED PERFORMANCE OPTIMIZATION

HEADLINE INSIGHTS ON HERE EMV TRANSACTION SPEED Subhead & POS Here PERFORMANCE OPTIMIZATION EXECUTIVE SUMMARY It has been more than a year since the EMV liability shift came into effect in the U.S. and

HEADLINE INSIGHTS ON HERE EMV TRANSACTION SPEED Subhead & POS Here PERFORMANCE OPTIMIZATION EXECUTIVE SUMMARY It has been more than a year since the EMV liability shift came into effect in the U.S. and

FTFS. Fault Tolerant Financial Systems

FTFS Fault Tolerant Financial Systems Fault Tolerant Financial Systems - FTFS - is the modular solution designed to support Enterprises and Financial Institutions in channel management for POS, self service,

FTFS Fault Tolerant Financial Systems Fault Tolerant Financial Systems - FTFS - is the modular solution designed to support Enterprises and Financial Institutions in channel management for POS, self service,

payshield 9000 The hardware security module securing the world s payments

> payshield 9000 The hardware security module securing the world s payments www.thalesgroup.com/iss Information Systems Security Information Systems Security payshield 9000 Table of Contents Introduction

> payshield 9000 The hardware security module securing the world s payments www.thalesgroup.com/iss Information Systems Security Information Systems Security payshield 9000 Table of Contents Introduction

CONVEGO. Platforms and Applications

CONVEGO Platforms and Applications Team up with the leader in secure payment products G&D s product line for native payment products G&D has specialized in the, G&D s multi-application product The full

CONVEGO Platforms and Applications Team up with the leader in secure payment products G&D s product line for native payment products G&D has specialized in the, G&D s multi-application product The full

NAB EFTPOS User Guide. for Countertop & Mobile Terminals

NAB EFTPOS User Guide for Countertop & Mobile Terminals YOUR NAB EFTPOS TERMINAL 2 NAB EFTPOS User Guide TABLE OF CONTENTS Getting to know your NAB EFTPOS Ingenico terminal 5 Contactless Tap & Go 8 Sale

NAB EFTPOS User Guide for Countertop & Mobile Terminals YOUR NAB EFTPOS TERMINAL 2 NAB EFTPOS User Guide TABLE OF CONTENTS Getting to know your NAB EFTPOS Ingenico terminal 5 Contactless Tap & Go 8 Sale

The October 1 EMV Liability Shift: Everything You Need to Know

The October 1 EMV Liability Shift: Everything You Need to Know 2 3 4 6 7 Introduction The Basics Predicting the impact Technical considerations What to look for in a service provider The financial services,

The October 1 EMV Liability Shift: Everything You Need to Know 2 3 4 6 7 Introduction The Basics Predicting the impact Technical considerations What to look for in a service provider The financial services,

Merchant Trading Name: Merchant Identification Number: Terminal Identification Number: ANZ CONTACTLESS EFTPOS MERCHANT OPERATING GUIDE

Merchant Trading Name: Merchant Identification Number: Terminal Identification Number: ANZ CONTACTLESS EFTPOS MERCHANT OPERATING GUIDE Contents 1. Welcome 3 2. Merchant Operating Guide 3 3. Important Contact

Merchant Trading Name: Merchant Identification Number: Terminal Identification Number: ANZ CONTACTLESS EFTPOS MERCHANT OPERATING GUIDE Contents 1. Welcome 3 2. Merchant Operating Guide 3 3. Important Contact

Best Guide to EMV Information As compiled by Mark Dunn, Field Guide Enterprises, LLC Updated late September, 2015

Best Guide to EMV Information As compiled by Mark Dunn, Field Guide Enterprises, LLC Updated late September, 2015 RECENT ARTICLES ABOUT EMV The Latest EMV Card Tally PYMNTS.COM September 30, 2015 http://www.pymnts.com/news/2015/the-latest-emv-card-tally/

Best Guide to EMV Information As compiled by Mark Dunn, Field Guide Enterprises, LLC Updated late September, 2015 RECENT ARTICLES ABOUT EMV The Latest EMV Card Tally PYMNTS.COM September 30, 2015 http://www.pymnts.com/news/2015/the-latest-emv-card-tally/

PCI BLOG. P2PE, EMV, Tokenization, Oh My!

Page 1 of 8 PCI BLOG THE UNOFFICIAL PCI COMPLIANCE & IT SECURITY BLOG HOME PCI IN THE NEWS PCI TOOLS IT SEC. JOB BOARD DOCUMENTS CONTACT US FORUM P2PE, EMV, Tokenization, Oh My! June 14, 2016 PCI Blog

Page 1 of 8 PCI BLOG THE UNOFFICIAL PCI COMPLIANCE & IT SECURITY BLOG HOME PCI IN THE NEWS PCI TOOLS IT SEC. JOB BOARD DOCUMENTS CONTACT US FORUM P2PE, EMV, Tokenization, Oh My! June 14, 2016 PCI Blog

Aconite Smart Solutions

Aconite Smart Solutions PIN Management Services Contents PIN MANAGEMENT... 3 CURRENT CHALLENGES... 3 ACONITE PIN MANAGER SOLUTION... 4 OVERVIEW... 4 CENTRALISED PIN VAULT... 5 CUSTOMER PIN SELF SELECT

Aconite Smart Solutions PIN Management Services Contents PIN MANAGEMENT... 3 CURRENT CHALLENGES... 3 ACONITE PIN MANAGER SOLUTION... 4 OVERVIEW... 4 CENTRALISED PIN VAULT... 5 CUSTOMER PIN SELF SELECT

PIN Issuance & Management

PIN Issuance & Management From PIN selection to PIN verification Card issuers and merchants know they can put their trust in MagTek. Whether meeting the growing need for instant, in-branch card and PIN

PIN Issuance & Management From PIN selection to PIN verification Card issuers and merchants know they can put their trust in MagTek. Whether meeting the growing need for instant, in-branch card and PIN

Verifone MX 915/925 Payment Devices. with KWI 6.x POS Registers: What s New?

Verifone MX 915/925 Payment Devices with KWI 6.x POS Registers: What s New? Contents Overview... 3 Network and Power Requirements... 5 Network Requirements... 5 Power Requirements... 5 Place Your Order

Verifone MX 915/925 Payment Devices with KWI 6.x POS Registers: What s New? Contents Overview... 3 Network and Power Requirements... 5 Network Requirements... 5 Power Requirements... 5 Place Your Order

Gemalto Consulting Services. Take control of your smart card implementation

Gemalto Consulting Services Take control of your smart card implementation FINANCIAL SERVICES & RETAIL > SERVICE ENTERPRISE INTERNET CONTENT PROVIDERS PUBLIC SECTOR TELECOMMUNICATIONS TRANSPORT Gemalto

Gemalto Consulting Services Take control of your smart card implementation FINANCIAL SERVICES & RETAIL > SERVICE ENTERPRISE INTERNET CONTENT PROVIDERS PUBLIC SECTOR TELECOMMUNICATIONS TRANSPORT Gemalto

Quick Guide. Token Service Provider

Quick Guide Token Service Provider Introduction to Mobile Payments The mobile payments revolution is here! Driven by the development of near field communication (NFC) enabled smartphones, the launch of

Quick Guide Token Service Provider Introduction to Mobile Payments The mobile payments revolution is here! Driven by the development of near field communication (NFC) enabled smartphones, the launch of

NAB EFTPOS MOBILE. Terminal Guide

NAB EFTPOS MOBILE Terminal Guide YOUR NAB EFTPOS MOBILE TERMINAL 2 NAB EFTPOS Mobile Terminal Guide TABLE OF CONTENTS Getting to know your NAB EFTPOS terminal 6 Contactless Tap & Go 8 Understanding your

NAB EFTPOS MOBILE Terminal Guide YOUR NAB EFTPOS MOBILE TERMINAL 2 NAB EFTPOS Mobile Terminal Guide TABLE OF CONTENTS Getting to know your NAB EFTPOS terminal 6 Contactless Tap & Go 8 Understanding your

Maximize the use of your HSM 8000

MAximise_HSM.qxp 19/06/2009 17:11 Page 1 www.thalesgroup.com/iss Maximize the use of your HSM 8000 Information Systems Security Information Systems Security Maximize the use of your HSM 8000 Table of Contents

MAximise_HSM.qxp 19/06/2009 17:11 Page 1 www.thalesgroup.com/iss Maximize the use of your HSM 8000 Information Systems Security Information Systems Security Maximize the use of your HSM 8000 Table of Contents

A New Way to Pay. Euronet Pakistan. An Overview of Contactless Payment. Kathy Hatcher Product Manager, Card Associations Payment Solutions

Euronet Pakistan A Euronet Software Solutions White Paper A New Way to Pay An Overview of Contactless Payment Kathy Hatcher Product Manager, Card Associations Payment Solutions Euronet Pakistan 7th Floor,

Euronet Pakistan A Euronet Software Solutions White Paper A New Way to Pay An Overview of Contactless Payment Kathy Hatcher Product Manager, Card Associations Payment Solutions Euronet Pakistan 7th Floor,

Virtual Terminal User Guide

Virtual Terminal User Guide Table of Contents Introduction... 4 Features of Virtual Terminal... 4 Getting Started... 4 3.1 Logging in and Changing Your Password 4 3.2 Logging Out 5 3.3 Navigation Basics

Virtual Terminal User Guide Table of Contents Introduction... 4 Features of Virtual Terminal... 4 Getting Started... 4 3.1 Logging in and Changing Your Password 4 3.2 Logging Out 5 3.3 Navigation Basics

The ABC of EMV. There s a chip on my Barclaycard

The ABC of EMV There s a chip on my Barclaycard by Dave Birch Consult Hyperion No Change My new Barclaycard has a chip on it. So do lots of others,

The ABC of EMV There s a chip on my Barclaycard by Dave Birch Consult Hyperion No Change My new Barclaycard has a chip on it. So do lots of others,

Strategy to Accelerate Migration to e-payments in Malaysia

Strategy to Accelerate Migration to e-payments in Malaysia Nurul Ashikin Mohammad Bokhari Payment System Policy Department Bank Negara Malaysia 1 Global Payments Week 20 September 2016 Despite a highly

Strategy to Accelerate Migration to e-payments in Malaysia Nurul Ashikin Mohammad Bokhari Payment System Policy Department Bank Negara Malaysia 1 Global Payments Week 20 September 2016 Despite a highly

Threat Landscape: Skimming In a Changing Environment

Threat Landscape: Skimming In a Changing Environment Chris Forsythe, Sr. Risk Analyst, Visa, Payment Fraud Disruption & Intelligence Stoddard Lambertson, Director, Fraud & Breach Investigations 22 February

Threat Landscape: Skimming In a Changing Environment Chris Forsythe, Sr. Risk Analyst, Visa, Payment Fraud Disruption & Intelligence Stoddard Lambertson, Director, Fraud & Breach Investigations 22 February

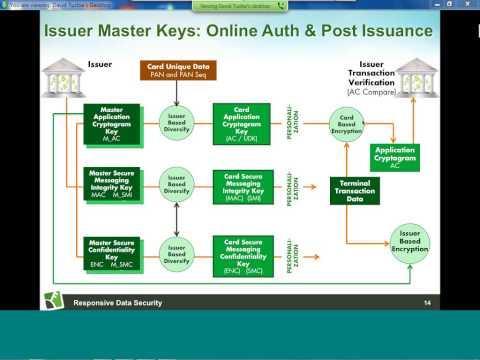

White Paper. EMV Key Management Explained

White Paper EMV Key Management Explained Introduction This white paper strides to provide an overview of key management related to migration from magnetic stripe to chip in the payment card industry. The

White Paper EMV Key Management Explained Introduction This white paper strides to provide an overview of key management related to migration from magnetic stripe to chip in the payment card industry. The

EMV Versions 1 & 2. Divided into 3 parts:

EMV Specification EMV Specifications May 94 - Version 1.0 EMV Part 1 Aug 94 - Version 1.0 EMV Part 2 Oct 94 - Version 1.0 EMV Part 3 Jun 95 - Version 2.0 EMV Jun 96 - Version 3.0 EMV 96 May 98 - Version

EMV Specification EMV Specifications May 94 - Version 1.0 EMV Part 1 Aug 94 - Version 1.0 EMV Part 2 Oct 94 - Version 1.0 EMV Part 3 Jun 95 - Version 2.0 EMV Jun 96 - Version 3.0 EMV 96 May 98 - Version

A Conversation with Visa on Consumer Debit Growth Connie Davis FIS Global Retail Payments Greg Borchardt Visa Consumer Debit Products

A Conversation with Visa on Consumer Debit Growth Connie Davis FIS Global Retail Payments Greg Borchardt Visa Consumer Debit Products May 2017 Visa Notice of Confidentiality This presentation is furnished

A Conversation with Visa on Consumer Debit Growth Connie Davis FIS Global Retail Payments Greg Borchardt Visa Consumer Debit Products May 2017 Visa Notice of Confidentiality This presentation is furnished

Payment Services. Issuing Processing. Product & Service Portfolio for Retailers

Payment Services Issuing Processing Product & Service Portfolio for Retailers New card business models generate profit for retailers Generate additional revenue and improve customer loyalty A payment card

Payment Services Issuing Processing Product & Service Portfolio for Retailers New card business models generate profit for retailers Generate additional revenue and improve customer loyalty A payment card

Topics. First Data and STAR Network overview. Competitive advantage. Fraud in emerging payments. Fraud innovation what s coming

Todd Clark Topics First Data and STAR Network overview Competitive advantage Fraud in emerging payments Fraud innovation what s coming 2 Introducing Todd Clark Background Entrepreneur Core Data Resources

Todd Clark Topics First Data and STAR Network overview Competitive advantage Fraud in emerging payments Fraud innovation what s coming 2 Introducing Todd Clark Background Entrepreneur Core Data Resources

International Processing for the Financial Industry

Payment Services International Processing for the Financial Industry State-of-the-art transaction processing and an unparalleled bandwidth of operational services to support banks and payment service providers

Payment Services International Processing for the Financial Industry State-of-the-art transaction processing and an unparalleled bandwidth of operational services to support banks and payment service providers

ECSG SEPA CARDS STANDARDISATION (SCS) VOLUME STANDARDS REQUIREMENTS

VOLUME STANDARDS REQUIREMENTS") ECSG001-17 01.03.2017 (Vol Ref. 8.7.00) SEPA CARDS STANDARDISATION (SCS) VOLUME STANDARDS REQUIREMENTS BOOK 7 CARDS PROCESSING FRAMEWORK Payments and Cash Withdrawals with Cards in SEPA Applicable Standards

ECSG001-17 01.03.2017 (Vol Ref. 8.7.00) SEPA CARDS STANDARDISATION (SCS) VOLUME STANDARDS REQUIREMENTS BOOK 7 CARDS PROCESSING FRAMEWORK Payments and Cash Withdrawals with Cards in SEPA Applicable Standards

Nayax 24 Raoul Wallenberg St., Building A1, 4th floor, Tel Aviv, 69719, Israel Tel:

Nayax 24 Raoul Wallenberg St., Building A1, 4th floor, Tel Aviv, 69719, Israel Tel: +972-3-7694380 info@nayax.com www.nayax.com Unattended Payment Solution Nayax specializes in the unattended market. Developing

Nayax 24 Raoul Wallenberg St., Building A1, 4th floor, Tel Aviv, 69719, Israel Tel: +972-3-7694380 info@nayax.com www.nayax.com Unattended Payment Solution Nayax specializes in the unattended market. Developing

Instant issuance in retail breaks new ground for banks

Use Case Instant issuance in retail breaks new ground for banks The most obvious consumer trend today is the expectation of immediacy. You can download movies and music, and shop online with instant results.

Use Case Instant issuance in retail breaks new ground for banks The most obvious consumer trend today is the expectation of immediacy. You can download movies and music, and shop online with instant results.

PRIME SM. A Next-Generation Solution for the World of Global Payments. Flexible Deployment Model. Reduce Cost of Ownership

Product Overview PRIME SM Reduce Cost of Ownership Speed-to-Market Risk Management Flexible Deployment Model A Next-Generation Solution for the World of Global Payments www.tsysprime.com PRIME Product

Product Overview PRIME SM Reduce Cost of Ownership Speed-to-Market Risk Management Flexible Deployment Model A Next-Generation Solution for the World of Global Payments www.tsysprime.com PRIME Product