MIS 5208 Week 2 Fraud Detection & Prevention

|

|

|

- Anissa Roberts

- 6 years ago

- Views:

Transcription

1 MIS 5208 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP eferrara@temple.edu

2 Fraud Awareness & Internal Controls Awareness Internal Controls Understand Fraud Symptoms Behaviors Data sources Alert Fraudulent behaviors Operational & Control Environment Separation of Duties Account treatments Cybersecurity controls Assess Risk & Exposures Fraud Detection Identify Potential Data Sources for Fraud Detection

3 Risk Factors For Fraud Employee Relationships Attractive Assets Competitive Business Environment Internal Controls Management Environment Fraud Integration of duties

4 Fraud Exposure Fraud Risk Assessment Risk assessment is a sometimes and controversial issue We will have an entire section on risk assessment Examine the risks and exposures to identify process and system weakness Develop Categories of Risk External environment Legal Regulatory Governance Strategy Operational Information Human resources Financial Technology Determining Fraud Exposure Sources of risk Review existing risk assessments Review risk assessment process Business Impact Analysts Types and sources of fraud External environment Governance Legal Regulatory Operational Strategy

5 Risk Factors for Fraud Management Environment Unrealistic Financial Targets Unrealistic Performance Standards Corporate Culture Emphasizing Win At All Costs Evaluate: Company production figures for reasonableness, financial targets, and management s position on same. Competitive & Business Environment Misstatement of Inventory Positions Fraudulent Orders Off Balance Sheet Transactions Evaluate: Recalculate the value of of inventory ensuring it is correctly valued. Employee Relationships Nepotism Insider Trading Collusion Evaluate: Look for nepotism, matching employee and vendor addresses. Attractive Assets Intellectual Property Theft Insider Abuse of Privilege Customer Contact Center Fraud Evaluate: Monetize both physical and information assets for financially based risk assessment. Internal Controls Inadequate internal controls Inventory markdowns Trading Practices Evaluate: Computer systems have necessary corresponding controls, privileged user abuse protection, etc. Separation of Duties Related to Above Reduced Staff Fraud Opportunity Evaluate: Ensure necessary policies, procedures, guidelines and standards are in place.

6 Fraud Schemes A Data Driven Approach Control Weaknesses Approach Examine key controls Determine vulnerabilities System Process Key Fields Focus on data entry Which data can be changed? What is the impact?

7 Control Weakness Internal / External parties Example: Received quantity less than ordered quantity but payment made for full amount Key Fields Data manipulation Privileged user abuse Example: Create fictitious vendors, changing address and bank account.

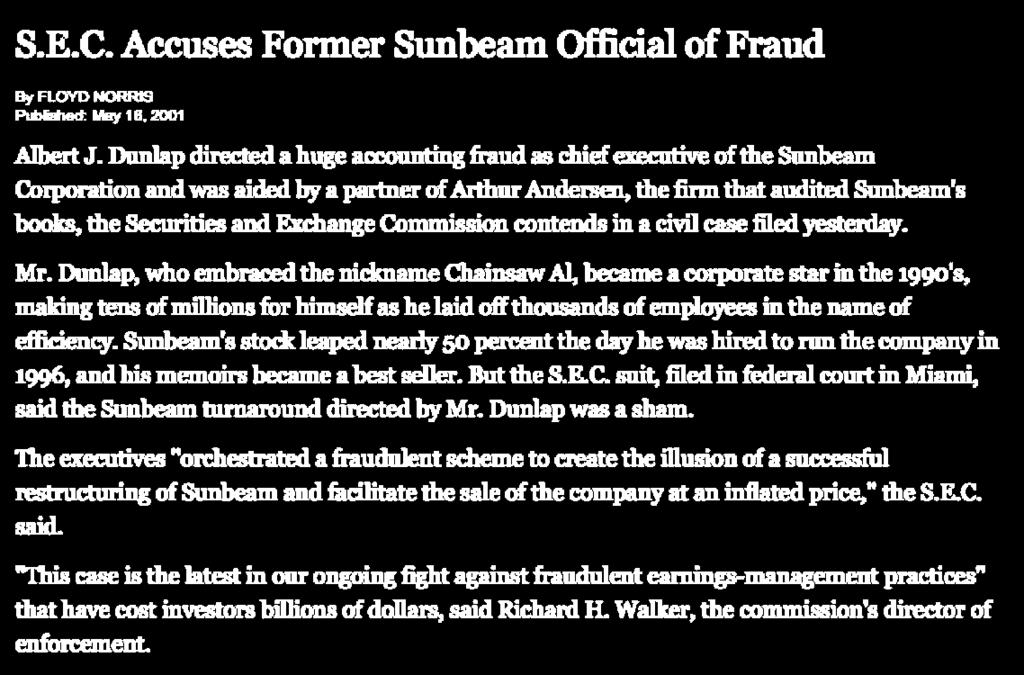

8 Case Study - Sunbeam

9 Fraud Exposure Identification Control Weakness Perpetrator Data Fields Data Analysis (Tests) Control Weakness Data of Interest

10 Key Data Vendor Name, Address, Bank Information Who Why Controls Test Clerks & Vendor Duplicate Payments, Fictitious Vendors & Payments Vendor creation, modification, Evaluate: Look for blanks in key fields, look for duplicates in vendor table. Unit Prices Clerk Direct Payments Vendor modification; system log files Evaluate: Look for disparities in unit price and contracted price. Quantities Contracting Officer, Vendor Kickbacks Invoice matching, on order quantity Evaluate: Look for disparities between ordered and delivered quantities. Transaction Amounts Clerk, vendor Overpayment to obtain funds or kickbacks, overcharges Invoice matching, contract amounts Evaluate: Look for disparities between contract and invoice amounts. Dates Clerk, vendor Backdate payment, due dates, backdate to obtain earlier payment Invoice matching, invoice and goods received date Evaluate: Look for transactions where invoice date is less than good receipt.

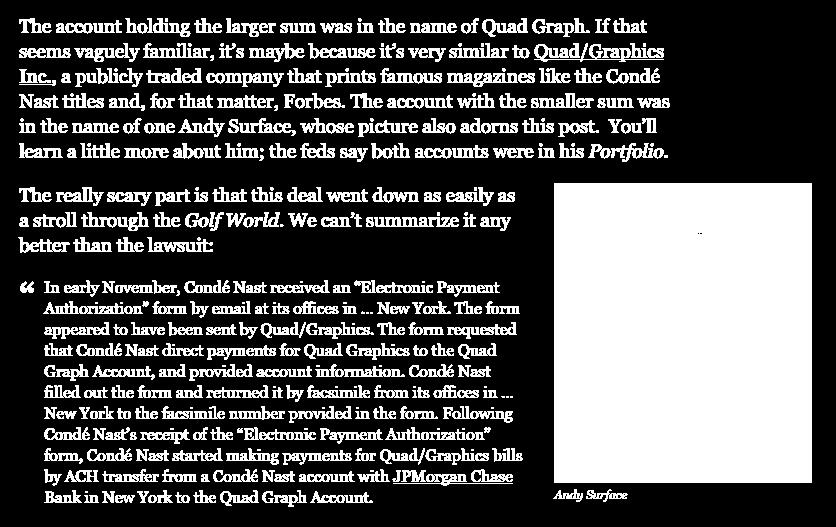

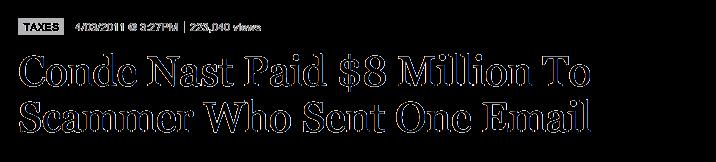

11 Case Study Conde Nast one- /print/

12 Fraud Standards

13 Investigating Fraud Which of these is true? An audit will: Detect all material errors and irregularities in the financial statements Discover all illegal acts committed by the client Ensure the financial health of the entity

14 Auditors Responsibilities Errors - Unintentional misstatements Mistakes in gathering or processing accounting data Incorrect accounting estimates Mistakes in the application of accounting principles Irregularities - Intentional misstatements, manipulation, falsification, or alteration of accounting records & supporting documents Misrepresentation or intentional omission of events, transactions, or other significant information Intentional misapplication of accounting principles

15 Software Accounting Standards SAS 1 and 22 Plan and perform the audit to provide reasonable assurance that financial statements are free of material misstatements caused by error or fraud. SAS 47 Audit risk, materiality and misstatements in financial statements SAS 54 Detection of illegal acts (AU Section 317) Section 301 of the Private Securities Litigation Reform Act Private Securities Litigation Reform Act of 1995 Section 10(a) of the Exchange Act Requires the inclusion of certain procedures in accordance with generally accepted accounting standards (GAAS). Audit procedures provide reasonable assurance of detecting illegal acts Audit procedures will identify related party transactions material to financial statements Evaluate of there is substantial doubt about the ability of the can stay in business. SAS 82 Auditor s responsibility related to fraud in a financial statement Provides guidance on what auditors should do to meet these responsibilities Describes: Fraudulent Financial Reporting Misappropriation of Assets

16 SAS 82 Requirements Consider the presence of fraud risk factors. - SAS No. 82 provides examples (detailed below) of risk factors an auditor may consider for fraud related to a) fraudulent financial reporting, and b) misappropriation of assets misstatements. An auditor should become familiar with these risk factors and be alert for their presence at the client s. Assess the risk of material misstatement of the financial statements due to fraud. SAS No. 82 requires an assessment as to the risk of material misstatement due to fraud. This assessment is separate from but may be performed in conjunction with other risk assessments (for example, control or inherent risk) made during the audit. SAS No. 82 also requires reevaluation of assessments if other conditions are identified during fieldwork. Develop a response. Based on assessments of risk, SAS No. 82 requires development of appropriate audit response. In some circumstances, an auditor s response may be that existing audit procedures are sufficient to obtain reasonable assurance that the financial statements are free of material misstatement due to fraud. In other circumstances, auditors may decide to extend planned audit procedures. Document certain items in work papers. SAS No. 82 requires auditors to document evidence of the performance of their assessment of risk of material misstatement due to fraud. Documentation should include risk factors identified as being present as well as the auditor s response to these risk factors. Communicate to management. If it is determined that there is evidence that a fraud may exist, an auditor should apprise the appropriate level of management, even if the matter may be considered inconsequential. SAS No. 82 also requires an auditor to communicate directly with the audit committee (or equivalent) if the matter involves fraud that would materially misstate the financial statements or fraud committed by senior management

17 Fraud Investigation

18 Fraud Types Billing - Cash Larceny Cash on Hand Check Tampering Corruption Financial Statement Fraud Non-Cash Payroll Register Disbursements Skimming

19 Fraud Analysis: Useful Information Issues Conflicts of interest Unknown relationships Abnormal patterns of activity Errors in key processes Control weaknesses Hindsight, insight, foresight Business Operations and Expense Areas Accounts payable Claims Damaged Goods Healthcare Insurance Loss Expense reimbursement General Ledger Travel and Entertainment

20 Vendor Attribute Capture Total number of vendors Vendors without: Addresses TAX ID Are they receiving payment? Electronic transfers Paper checks

21 Vendor Activity Assessment Number of Vendors Frequency of Use Number of Active Users Compared Against Total Vendors Unused Vendors can be source of internal abuse Vendor Identity Abuse

22 Name Mining Looking for Fictitious Vendors Fictitious Names Use their initials in the name of a vendor Anagrams Others Substitution Insertion and Omission Transposition Number Substitution

23 E mp lo y e e V e n d o r R e latio n s h ip s Employee and Vendor Name are Different Common Addresses Addresses that are different but are at the same geographic location: 201 College Avenue 669 West Chestnut Street Phone Number TAX ID Zip Codes

24 Proximity Analysis Mailbox Services Anonymous These mail drop have the appearance of a physical address Proximity location of vendor to actual employees Employee Addresses Vendor Addresses Proximity Analysis

25 Vendor Trending Analysis Accounts Payable Claims Payable Fraud Payment Acceleration Small initial amounts of fraud Amounts and frequency increases Test Phase Confidence Phase Greed Phase Trend Payments to Vendors Valley and Spike Payment Patterns Long periods of inactivity between periods of very high activity Unusually high periods of activity

26 Payment Trend Analysis Calendar By Day of Week By Day of Month By Month Checks created on weekends (Saturdays and Sundays) Date created Date posted Benford s Law The first digit should be a 1 (30% of the time)

27 Benford s Law McGinty, J. C. (2014). Accountants Increasingly Use Data Analysis to Catch Fraud - Auditors Wield Mathematical Weapons to Detect Cheating. The Wall Street Journal. (Web Site)

28 Check Sequence Analysis G/L Cash Receipts Identify Gaps in Check Sequences

29 Expense, Payroll, and Vacation Controls Analysis of Overtime Hours Reasonableness Consistent with role Holiday Hours Reasonableness Consistent with role Purchasing Cards Spending over approval limits Split transactions to avoid limit Collusion between subordinate and supervisor to avoid approval scrutiny Vacation Hours Reasonableness Consistent with role Large amounts of vacation outside of guidelines

30 Other Analysis Areas System Access Logs Maintenance Files Social Media The Price is Right Fraud Physical Investigations Surveillance

.")

31 Continuous Auditing Programmatic Auditing System Based Source: Cser, A. (2010).Market Overview: Fraud Management Solutions - Seven Tenets Of Effectively Combating Fraud Costs. Forrester Research.

32 Thank you.

Detecting Fraud Through Data Analytics

Detecting Fraud Through Data Analytics Jeremy Clopton, CPA, CFE, ACDA Managing Consultant jclopton@bkd.com 417.865.8701 July 24, 2013 To Receive CPE Credit Participate in entire webinar Answer polls when

Detecting Fraud Through Data Analytics Jeremy Clopton, CPA, CFE, ACDA Managing Consultant jclopton@bkd.com 417.865.8701 July 24, 2013 To Receive CPE Credit Participate in entire webinar Answer polls when

Week 3: Fraud, Procure to Pay Process Controls

Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Business Processes, ERP Systems & Controls Week 3: Fraud, Procure to Pay Process Controls Video: Record the Class Discussion v Something really new,

Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Business Processes, ERP Systems & Controls Week 3: Fraud, Procure to Pay Process Controls Video: Record the Class Discussion v Something really new,

Using Data Analytics as a Management Tool to Identify Organizational Risks

2013 CliftonLarsonAllen LLP Using Data Analytics as a Management Tool to Identify Organizational Risks Government Finance Officers Association of South Carolina October 13, 2014 cliftonlarsonallen.com

2013 CliftonLarsonAllen LLP Using Data Analytics as a Management Tool to Identify Organizational Risks Government Finance Officers Association of South Carolina October 13, 2014 cliftonlarsonallen.com

Managing Fraud Risks. Procurement & Contacting. John J. Hall, CPA (970)

") Managing Fraud Risks in Procurement & Contacting The IIA Los Angeles Chapter October 2, 2017 John J. Hall, CPA (970) 926-0355 John@JohnHallSpeaker.com 1 Four Categories 1. Theft 2. Results Manipulation

Managing Fraud Risks in Procurement & Contacting The IIA Los Angeles Chapter October 2, 2017 John J. Hall, CPA (970) 926-0355 John@JohnHallSpeaker.com 1 Four Categories 1. Theft 2. Results Manipulation

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

FRAUD SCHEMES. South Carolina HFMA Finance & Reimbursement Forum. November 13, 2012 WITH RELATED INTERNAL CONTROLS

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

OUTSMART FRAUD. Strategic Internal Controls to Prevent Business Fraud

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

The Role of Analytics in Auditing The Importance of What the Numbers Indicate and Lack to Indicate

The Role of Analytics in Auditing The Importance of What the Numbers Indicate and Lack to Indicate Vienna, November 18, 2013 Atanasko Atanasovski CFRR, consultant Analytic-enabled audits Cost effective

The Role of Analytics in Auditing The Importance of What the Numbers Indicate and Lack to Indicate Vienna, November 18, 2013 Atanasko Atanasovski CFRR, consultant Analytic-enabled audits Cost effective

AUDIT STATUS. Continuous Auditing Ideas and Priority Ranking Draft: 8/7/2012

Compliance Identify single day stays and subsequent re-admissions Identify inappropriate unbundling of lab tests Identify frequent use of high risk organizations Match OIG-excluded providers list with

Compliance Identify single day stays and subsequent re-admissions Identify inappropriate unbundling of lab tests Identify frequent use of high risk organizations Match OIG-excluded providers list with

716 West Ave Austin, TX USA

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a. AUDITING THEORY Risk Assessment and Response to Assessed Risks

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Detecting Fraud Through Vendor Audits

Detecting Fraud Through Vendor Audits Identifying and Selecting Audit Candidates 2017 Association of Certified Fraud Examiners, Inc. The Importance of Routinely Exercising Vendor Audit Rights There is

Detecting Fraud Through Vendor Audits Identifying and Selecting Audit Candidates 2017 Association of Certified Fraud Examiners, Inc. The Importance of Routinely Exercising Vendor Audit Rights There is

Common Frauds Found in Not-for- Profit Organizations

Common Frauds Found in Not-for- Profit Organizations NCACPA Not-for-Profit Conference May 19, 2015 Presented by Lynda M. Dennis CPA, CGFO, PhD Today s Session Overview 2014 Occupational Fraud Report Findings

Common Frauds Found in Not-for- Profit Organizations NCACPA Not-for-Profit Conference May 19, 2015 Presented by Lynda M. Dennis CPA, CGFO, PhD Today s Session Overview 2014 Occupational Fraud Report Findings

Fraud Risk Management

Fraud Risk Management Using Automated Continuous Monitoring Tools 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization use continuous and/or automated monitoring

Fraud Risk Management Using Automated Continuous Monitoring Tools 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization use continuous and/or automated monitoring

Post-Conference Auditing and Investigating Fraud Seminar

Post-Conference Auditing and Investigating Fraud Seminar Auditing Track Auditors Fraud Responsibilities 1 of 18 Introduction Differing roles one goal External auditor Internal auditor Fraud examiner 2

Post-Conference Auditing and Investigating Fraud Seminar Auditing Track Auditors Fraud Responsibilities 1 of 18 Introduction Differing roles one goal External auditor Internal auditor Fraud examiner 2

Consideration of Fraud in a Financial Statement Audit

Consideration of Fraud in a Financial Statement Audit 153 AU-C Section 240 Consideration of Fraud in a Financial Statement Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements

Consideration of Fraud in a Financial Statement Audit 153 AU-C Section 240 Consideration of Fraud in a Financial Statement Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements

OVERVIEW 4/19/10. Internal Controls and the Audit Process May 4, 2010 OVERVIEW. Definition and historical perspective of internal auditing

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

ACL ESSENTIALS. Get insight into your ERP process health, compliance & financial exposure SEGEREGATION OF DUTIES

ACL ESSENTIALS Get insight into your ERP process health, compliance & financial exposure SEGEREGATION OF DUTIES Page Analytic Name User creates a vendor and an invoice for this vendor SD Analytic 01 User

ACL ESSENTIALS Get insight into your ERP process health, compliance & financial exposure SEGEREGATION OF DUTIES Page Analytic Name User creates a vendor and an invoice for this vendor SD Analytic 01 User

Fraud and Fraud Detection

Fraud and Fraud Detection The Wiley Corporate F&A series provides information, tools, and insights to corporate professionals responsible for issues affecting the profitability of their company, from accounting

Fraud and Fraud Detection The Wiley Corporate F&A series provides information, tools, and insights to corporate professionals responsible for issues affecting the profitability of their company, from accounting

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young. Lessons on Audit Risk. Responding to fraud risk

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

INTERNAL CONTROL HANDBOOK

INTERNAL CONTROL HANDBOOK INTERNAL CONTROL HANDBOOK ILLINOIS STATE BOARD OF EDUCATION SCHOOL BUSINESS SERVICES DIVISION Revised July, 2017 Most Content remains the same as published in 1993 Prepared by

INTERNAL CONTROL HANDBOOK INTERNAL CONTROL HANDBOOK ILLINOIS STATE BOARD OF EDUCATION SCHOOL BUSINESS SERVICES DIVISION Revised July, 2017 Most Content remains the same as published in 1993 Prepared by

Fraud and the Small Business Owner

Fraud and the Small Business Owner Can you recognize it when you see it? National Society of Accountants Annual Meeting August 15, 2009 Erik H. Lindquist, CFE Presenter Definition The use of one s occupation

Fraud and the Small Business Owner Can you recognize it when you see it? National Society of Accountants Annual Meeting August 15, 2009 Erik H. Lindquist, CFE Presenter Definition The use of one s occupation

COPYRIGHTED MATERIAL. Index. Page references followed by f indicate an illustrated figure.

Index Page references followed by f indicate an illustrated figure. Abuse asset misappropriation, contrast, 206 207 expenses submission, 206 Abusive purchase scenario, 218 Access security databases, usage,

Index Page references followed by f indicate an illustrated figure. Abuse asset misappropriation, contrast, 206 207 expenses submission, 206 Abusive purchase scenario, 218 Access security databases, usage,

Using Transactional Analysis for

Using Transactional Analysis for Effective Fraud Detection Date: 15 th January 2009 Nishith Seth Seth Services.P. Ltd. www.sspl.net.in Cost Indirect costs: image, morale Fraud Issues & Impact Direct costs:

Using Transactional Analysis for Effective Fraud Detection Date: 15 th January 2009 Nishith Seth Seth Services.P. Ltd. www.sspl.net.in Cost Indirect costs: image, morale Fraud Issues & Impact Direct costs:

EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST

Page 128 of 174 EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST Recognizing Warning Signs and Preventing Problem Situations Why are consistent internal controls important? Management decisions, financial reports,

Page 128 of 174 EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST Recognizing Warning Signs and Preventing Problem Situations Why are consistent internal controls important? Management decisions, financial reports,

Fraud Risk Management

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Financial Statement Close Process

Financial Statement Close Process Process Control Objective Risk Control Considerations Segregation of Duties Accounting functions are properly segregated. Unauthorized and inaccurate transactions may

Financial Statement Close Process Process Control Objective Risk Control Considerations Segregation of Duties Accounting functions are properly segregated. Unauthorized and inaccurate transactions may

The Best of Crimes, the Worst of Crimes: Fraud Stories That Prove the Truth Is in the Transactions

Technology for Business Assurance The Best of Crimes, the Worst of Crimes: Fraud Stories That Prove the Truth Is in the Transactions Copyright 2009 ACL Services Ltd. Peter Millar Director, Technology Application

Technology for Business Assurance The Best of Crimes, the Worst of Crimes: Fraud Stories That Prove the Truth Is in the Transactions Copyright 2009 ACL Services Ltd. Peter Millar Director, Technology Application

FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A)

") Page 136 of 174 FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A) RECOGNIZING RISK FACTORS THAT SHOULD GET YOUR ATTENTION How to use the checklist: 1. Review this checklist towards

Page 136 of 174 FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A) RECOGNIZING RISK FACTORS THAT SHOULD GET YOUR ATTENTION How to use the checklist: 1. Review this checklist towards

Cash Reconciliations and Cash Handling

Cash Reconciliations and Cash Handling WASBO Accounting Conference March, 2016 Handling Cash Cash may be the most vulnerable asset in your LEA. How do you safeguard your cash? Timely reconciliation of

Cash Reconciliations and Cash Handling WASBO Accounting Conference March, 2016 Handling Cash Cash may be the most vulnerable asset in your LEA. How do you safeguard your cash? Timely reconciliation of

Leveraging Data Analytics to Expand Audit Coverage and Add Organizational Value

Leveraging Data Analytics to Expand Audit Coverage and Add Organizational Value Clint McPherson Managing Director, Dallas, TX Cindy Hart Manager, Dallas, TX Setting the Stage - Data Analysis Defined Data

Leveraging Data Analytics to Expand Audit Coverage and Add Organizational Value Clint McPherson Managing Director, Dallas, TX Cindy Hart Manager, Dallas, TX Setting the Stage - Data Analysis Defined Data

Managing Risk in Your P2P Process: 10 Ways that Automation Can Help Mitigate Risk

Managing Risk in Your P2P Process: 10 Ways that Automation Can Help Mitigate Risk Chris Doxey, CAPP, CCSA, CICA, CPC President, Doxey, Inc. chris@chrisdoxey.com 571-267-9107 Agenda Introduction to Risk

Managing Risk in Your P2P Process: 10 Ways that Automation Can Help Mitigate Risk Chris Doxey, CAPP, CCSA, CICA, CPC President, Doxey, Inc. chris@chrisdoxey.com 571-267-9107 Agenda Introduction to Risk

Due: Tuesday, May 1, 2007 by 5:45 p.m.

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

Eric Anderson, City Manager. Scottie Nix, Internal Auditor

City of Tacoma Internal Audit Office Memorandum TO: FROM: SUBJECT: Eric Anderson, City Manager Scottie Nix, Internal Auditor Improving SAP Roles Assignment and Monitoring at the City of Tacoma Follow Up

City of Tacoma Internal Audit Office Memorandum TO: FROM: SUBJECT: Eric Anderson, City Manager Scottie Nix, Internal Auditor Improving SAP Roles Assignment and Monitoring at the City of Tacoma Follow Up

Scope of this SA Effective Date Objective Definitions Sufficient Appropriate Audit Evidence... 6

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

International Standard on Auditing (Ireland) 500 Audit Evidence

500 Audit Evidence") International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

Chapter 7 Internal Controls

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

Contract and Procurement Fraud. Fraud in Procurement without Competition

Contract and Procurement Fraud Fraud in Procurement without Competition Sole-Source Awards Noncompetitive procurement process through the solicitation of only one source Procurement through sole-source

Contract and Procurement Fraud Fraud in Procurement without Competition Sole-Source Awards Noncompetitive procurement process through the solicitation of only one source Procurement through sole-source

Seattle Public Schools The Office of Internal Audit

Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2014 through Current Issue Date: June 21, 2016 Executive Summary Background Information The function is centralized

Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2014 through Current Issue Date: June 21, 2016 Executive Summary Background Information The function is centralized

Chapter 16. Auditing Operations and Completing the Audit. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 16 Auditing Operations and Completing the Audit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Auditing Operations Corporate earnings are considered as

Chapter 16 Auditing Operations and Completing the Audit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Auditing Operations Corporate earnings are considered as

Data Analytics: Where Do I Start?

Data Analytics: Where Do I Start? Ryan Merryman, CPA, CFF, CITP, CFE David Heneke, CPA, CISA Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered

Data Analytics: Where Do I Start? Ryan Merryman, CPA, CFF, CITP, CFE David Heneke, CPA, CISA Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered

ACL ESSENTIALS. Get insight into your ERP process health, compliance & financial exposure ACCOUNTS PAYABLE

ACL ESSENTIALS Get insight into your ERP process health, compliance & financial exposure ACCOUNTS PAYABLE Page Analytic Name Duplicate payments AP Analytic 01 Duplicate invoices AP Analytic 02 Duplicate

ACL ESSENTIALS Get insight into your ERP process health, compliance & financial exposure ACCOUNTS PAYABLE Page Analytic Name Duplicate payments AP Analytic 01 Duplicate invoices AP Analytic 02 Duplicate

FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom)

Foundations in Audit (United Kingdom)") Answers FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom) June 2012 Answers Section A QUESTIONS 1 10 MULTIPLE CHOICE Question Answer See Note Below 1 A 1 2 D 2 3 C 3 4 B 4

Answers FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom) June 2012 Answers Section A QUESTIONS 1 10 MULTIPLE CHOICE Question Answer See Note Below 1 A 1 2 D 2 3 C 3 4 B 4

Melinda J. DeCorte, CPA, CFE, CGFM, PMP

Melinda J. DeCorte, CPA, CFE, CGFM, PMP Melinda DeCorte has over 19 years of accounting, auditing and government financial management experience. She directs, manages and serves in a quality assurance

Melinda J. DeCorte, CPA, CFE, CGFM, PMP Melinda DeCorte has over 19 years of accounting, auditing and government financial management experience. She directs, manages and serves in a quality assurance

What does an external auditor look for in SAP R/3 during SOX 404 Audits? Ram Bapu, CISSP, CISM Sandra Keigwin, CISSP

What does an external auditor look for in SAP R/3 during SOX 404 Audits? Ram Bapu, CISSP, CISM Sandra Keigwin, CISSP What does an external auditor look for in SAP during SOX 404 Audits? Corporations have

What does an external auditor look for in SAP R/3 during SOX 404 Audits? Ram Bapu, CISSP, CISM Sandra Keigwin, CISSP What does an external auditor look for in SAP during SOX 404 Audits? Corporations have

Internal Control Evaluation

INTERNAL CONTROL EVALUATION Adapted from a checklist created by Jackie F. Breland, CPA (www.jackiebreland.com) Organization: Date Prepared or Updated: Prepared by: Introduction The purpose of this checklist

INTERNAL CONTROL EVALUATION Adapted from a checklist created by Jackie F. Breland, CPA (www.jackiebreland.com) Organization: Date Prepared or Updated: Prepared by: Introduction The purpose of this checklist

Internal Controls Dealerships Should Have but May Not Have Thought About

October 2017 Internal Controls Dealerships Should Have but May Not Have Thought About An article by Edmund J. Reinhard, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions. Lasting value. Internal

October 2017 Internal Controls Dealerships Should Have but May Not Have Thought About An article by Edmund J. Reinhard, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions. Lasting value. Internal

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a AUDITING THEORY PROFESSIONAL AND LEGAL RESPONSIBILITIES

Page 1 of 10 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs : PSA 240rev, 250 and 260 AUDITING THEORY PROFESSIONAL AND LEGAL RESPONSIBILITIES PSA 240(rev) The Auditor s Responsibility to

Page 1 of 10 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs : PSA 240rev, 250 and 260 AUDITING THEORY PROFESSIONAL AND LEGAL RESPONSIBILITIES PSA 240(rev) The Auditor s Responsibility to

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

Audit Evidence This section is effective for audits of financial statements for periods ending on or after December 15, 2012.

Audit Evidence 395 AU-C Section 500 Audit Evidence Source: SAS No. 122; SAS No. 128. See section 9500 for interpretations of this section. Effective for audits of financial statements for periods ending

Audit Evidence 395 AU-C Section 500 Audit Evidence Source: SAS No. 122; SAS No. 128. See section 9500 for interpretations of this section. Effective for audits of financial statements for periods ending

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable. Chapter 18

Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable. Chapter 18 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley

Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable. Chapter 18 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley

S12 - Guidelines for Planning an IS Audit Christopher Chung

S12 - Guidelines for Planning an IS Audit Christopher Chung IS Auditing Guidelines for Planning an IS Audit Session Objectives Agenda Information Systems Audit Planning and Scoping o Understanding Business

S12 - Guidelines for Planning an IS Audit Christopher Chung IS Auditing Guidelines for Planning an IS Audit Session Objectives Agenda Information Systems Audit Planning and Scoping o Understanding Business

Internal Audit Report

Internal Audit Report C u y a h o g a C o u n t y, O h i o D e p a r t m e n t o f I n t e r n a l A u d i t i n g Benford s Law Audit 2016 Cuyahoga County Fiscal Office Accounts Payable January 1, 2016

Internal Audit Report C u y a h o g a C o u n t y, O h i o D e p a r t m e n t o f I n t e r n a l A u d i t i n g Benford s Law Audit 2016 Cuyahoga County Fiscal Office Accounts Payable January 1, 2016

2/27/2017. Segregation of Duties/ Internal Controls. Objectives. Agenda

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Journal of Forensic & Investigative Accounting Volume 9: Issue 3, Special Issue, 2017

Cutting through the Numbers: How Data Mining Was Used to Uncover Multiple Frauds at a Hospital System Medical Center Dr. Bryan Cataldi Bryan Callahan Dr. James F. Sander Dr. Anne S. Kelly* Introduction

Cutting through the Numbers: How Data Mining Was Used to Uncover Multiple Frauds at a Hospital System Medical Center Dr. Bryan Cataldi Bryan Callahan Dr. James F. Sander Dr. Anne S. Kelly* Introduction

Loch Lomond and The Trossachs National Park Authority. Key Controls Report

Loch Lomond and The Trossachs National Park Authority Key Controls Report Prepared for Loch Lomond and The Trossachs Park Authority April 2015 Audit Scotland is a statutory body set up in April 2000 under

Loch Lomond and The Trossachs National Park Authority Key Controls Report Prepared for Loch Lomond and The Trossachs Park Authority April 2015 Audit Scotland is a statutory body set up in April 2000 under

Chapter 4. Risk Assessment. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 4 Risk Assessment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Audit Risk The risk that an auditor expresses an unqualified opinion on materially

Chapter 4 Risk Assessment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Audit Risk The risk that an auditor expresses an unqualified opinion on materially

Predictive Analysis Risk Analysis

Predictive Analysis Risk Analysis MARYLAND ASSOCIATION OF CPAS GOVERNMENT AND NOT-FOR-PROFIT CONFERENCE April 25, 2014 Overview Forensic Audit and Automated Oversight Data Analytics for Grant Oversight

Predictive Analysis Risk Analysis MARYLAND ASSOCIATION OF CPAS GOVERNMENT AND NOT-FOR-PROFIT CONFERENCE April 25, 2014 Overview Forensic Audit and Automated Oversight Data Analytics for Grant Oversight

Paper FAU (UK) Foundations in Audit (United Kingdom) FOUNDATIONS IN ACCOUNTANCY. Monday 18 June 2012

Foundations in Audit (United Kingdom) FOUNDATIONS IN ACCOUNTANCY. Monday 18 June 2012") FOUNDATIONS IN ACCOUNTANCY Foundations in Audit (United Kingdom) Monday 18 June 2012 Time allowed: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST be

FOUNDATIONS IN ACCOUNTANCY Foundations in Audit (United Kingdom) Monday 18 June 2012 Time allowed: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST be

Monterey County Office of Education

Monterey County Office of Education Extraordinary Audit of the King City Joint Union High School District April 28, 2010 Joel D. Montero Chief Executive Officer April 28, 2010 Nancy Kotowski, Superintendent

Monterey County Office of Education Extraordinary Audit of the King City Joint Union High School District April 28, 2010 Joel D. Montero Chief Executive Officer April 28, 2010 Nancy Kotowski, Superintendent

Butte County Office of Education

Butte County Office of Education Extraordinary Audit of the Blue Oak Charter School November 16, 2017 Michael H. Fine Chief Executive Officer Fiscal Crisis & Management Assistance Team November 16, 2017

Butte County Office of Education Extraordinary Audit of the Blue Oak Charter School November 16, 2017 Michael H. Fine Chief Executive Officer Fiscal Crisis & Management Assistance Team November 16, 2017

IAASB Main Agenda (March 2005) Page Agenda Item 12-C

Page Agenda Item 12-C") IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

Comprehensive List of Fraud Indicators

Comprehensive List of Fraud Indicators This document provides links to our contract audit resources. The scenarios are grouped by audit type, but the issues presented could be applicable to other audits

Comprehensive List of Fraud Indicators This document provides links to our contract audit resources. The scenarios are grouped by audit type, but the issues presented could be applicable to other audits

Energy Future Holdings (EFH)

") Energy Future Holdings (EFH) Inclusion of Data Analytics into the Internal Audit Lifecycle June 3, 2015 Starting Place Baseline Questions Pertaining to the utilization of data analytics in the internal

Energy Future Holdings (EFH) Inclusion of Data Analytics into the Internal Audit Lifecycle June 3, 2015 Starting Place Baseline Questions Pertaining to the utilization of data analytics in the internal

Internal Controls Integrating COSO

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

VERSION #1 WRITE ON YOUR SCANTRON!!!

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

PAYROLL CHECK-OFF AUDIT

PAYROLL CHECK-OFF AUDIT Prepared By: Craig Hametner, CPA, CIA, CMA, CFE City Auditor Randall Mahaffey, CIA, CGAP Senior Audit Analyst Steve Culpepper, CPA, CIA Audit Analyst Jed Johnson Audit Analyst Elizabeth

PAYROLL CHECK-OFF AUDIT Prepared By: Craig Hametner, CPA, CIA, CMA, CFE City Auditor Randall Mahaffey, CIA, CGAP Senior Audit Analyst Steve Culpepper, CPA, CIA Audit Analyst Jed Johnson Audit Analyst Elizabeth

Effective implementation of COSO s new anti-fraud guidance

Effective implementation of COSO s new anti-fraud guidance In September 2016, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) published a new Fraud Risk Management Guide (Anti-fraud

Effective implementation of COSO s new anti-fraud guidance In September 2016, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) published a new Fraud Risk Management Guide (Anti-fraud

Chapter 12: The Revenue Cycle

Chapter 12: The Revenue Cycle Syaiful Ali, SE., MIS., Ak. Introduction Revenue Cycles tend to be similar for all types of firms. Two subsystems perform the processing steps within the revenue cycle: The

Chapter 12: The Revenue Cycle Syaiful Ali, SE., MIS., Ak. Introduction Revenue Cycles tend to be similar for all types of firms. Two subsystems perform the processing steps within the revenue cycle: The

TACKLING HEALTH CARE FRAUD, WASTE, AND ABUSE WHERE DO YOU START?

TACKLING HEALTH CARE FRAUD, WASTE, AND ABUSE WHERE DO YOU START? William Gedman CPA, CIA Vice President Quality Audit, Fraud & Abuse UPMC Insurance Services Division Pittsburgh, PA Session Outline Elements

TACKLING HEALTH CARE FRAUD, WASTE, AND ABUSE WHERE DO YOU START? William Gedman CPA, CIA Vice President Quality Audit, Fraud & Abuse UPMC Insurance Services Division Pittsburgh, PA Session Outline Elements

Assurance Hand Note Professional Stage-Knowledge Level By: Shafique Ahmed-Sr. Officer (Internal Audit-BSRM) Assurance

Assurance") Assurance 1 CONTENTS OF ASSURANCE 01. Preliminary of Assurance: 1.01 Assurance Engagement: 1.02 Key elements of an assurance engagement: 1.03 Levels of assurance 1.04 Objective of an Audit: 1.05 True &

Assurance 1 CONTENTS OF ASSURANCE 01. Preliminary of Assurance: 1.01 Assurance Engagement: 1.02 Key elements of an assurance engagement: 1.03 Levels of assurance 1.04 Objective of an Audit: 1.05 True &

FRAUD IN GOVERNMENT AN OPEN DISCUSSION. Presented By William Blend, CPA, CFE

FRAUD IN GOVERNMENT AN OPEN DISCUSSION Presented By William Blend, CPA, CFE AGENDA Fraud and Ethics Discussion Fraud Triangle and Beyond Data from 2016 ACFE Report to the Nations Recent Fraud Investigations

FRAUD IN GOVERNMENT AN OPEN DISCUSSION Presented By William Blend, CPA, CFE AGENDA Fraud and Ethics Discussion Fraud Triangle and Beyond Data from 2016 ACFE Report to the Nations Recent Fraud Investigations

Chapter 11 The Revenues, Receivables and Receipts Process

Chapter 11 The Revenues, Receivables and Receipts Process Understanding the Revenue, Receivables and Receipts Process The auditor must understand the business s method of generating revenues and use of

Chapter 11 The Revenues, Receivables and Receipts Process Understanding the Revenue, Receivables and Receipts Process The auditor must understand the business s method of generating revenues and use of

INTERNAL CONTROLS AND FRAUD DETECTION. Jill Reyes, Director Laura Manlove, Manager

INTERNAL CONTROLS AND FRAUD DETECTION Jill Reyes, Director Laura Manlove, Manager Today s presenters Jill Reyes Director, Risk Advisory Services RSM US LLP Melbourne, Florida jill.reyes@rsmus.com +1 321

INTERNAL CONTROLS AND FRAUD DETECTION Jill Reyes, Director Laura Manlove, Manager Today s presenters Jill Reyes Director, Risk Advisory Services RSM US LLP Melbourne, Florida jill.reyes@rsmus.com +1 321

CHAPTER 5 INFORMATION TECHNOLOGY SERVICES CONTROLS

5-1 CHAPTER 5 INFORMATION TECHNOLOGY SERVICES CONTROLS INTRODUCTION In accordance with Statements on Auditing Standards Numbers 78 and 94, issued by the American Institute of Certified Public Accountants

5-1 CHAPTER 5 INFORMATION TECHNOLOGY SERVICES CONTROLS INTRODUCTION In accordance with Statements on Auditing Standards Numbers 78 and 94, issued by the American Institute of Certified Public Accountants

Internal Audit Policy and Procedures Internal Audit Charter

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Data-Driven Approaches to Identifying Risk and Indicators of Fraud November 2013

Data-Driven Approaches to Identifying Risk and Indicators of Fraud November 2013 David Coderre Public Servant in Residence Office of the Comptroller General of Canada 1 Agenda The problem Subjective and

Data-Driven Approaches to Identifying Risk and Indicators of Fraud November 2013 David Coderre Public Servant in Residence Office of the Comptroller General of Canada 1 Agenda The problem Subjective and

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

Journal of Business & Economics Research January 2006 Volume 4, Number 1

Family Owned Business Fraud: The Silent Thief M. Tony Bledsoe, (E-mail: bledsoem@meredith.edu), Meredith College Susan B. Wessels, (E-mail: wesselss@meredith.edu), Meredith College Abstract The ACFE 2002

Family Owned Business Fraud: The Silent Thief M. Tony Bledsoe, (E-mail: bledsoem@meredith.edu), Meredith College Susan B. Wessels, (E-mail: wesselss@meredith.edu), Meredith College Abstract The ACFE 2002

Kianoff & Associates Crystal Clear Reports for Sage 100

Kianoff & Associates Crystal Clear Reports for Sage 100 We have developed Crystal Reports for all current versions of Sage 100 and are available for most all modules. Accounts Payable BP801- Vendor File

Kianoff & Associates Crystal Clear Reports for Sage 100 We have developed Crystal Reports for all current versions of Sage 100 and are available for most all modules. Accounts Payable BP801- Vendor File

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 500

500") Issued 07/11 Compiled 10/15 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 500 Audit Evidence (ISA (NZ) 500) This compilation was prepared in October 2015 and incorporates amendments up to and including

Issued 07/11 Compiled 10/15 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 500 Audit Evidence (ISA (NZ) 500) This compilation was prepared in October 2015 and incorporates amendments up to and including

Several unallowable expenditures and exceptions to policy were noted.

Several unallowable expenditures and exceptions to policy were noted. In our testing of 16 disbursement/pcard transactions, 12 travel transactions, and 9 gift transactions, we noted 6 transactions contained

Several unallowable expenditures and exceptions to policy were noted. In our testing of 16 disbursement/pcard transactions, 12 travel transactions, and 9 gift transactions, we noted 6 transactions contained

You can easily view comparative data and drill through for transaction details.

analyzing financial and operational information (such as number of sales reps, occupancy rates or cycle time), giving you a very powerful business management tool that leverages your financial data. You

analyzing financial and operational information (such as number of sales reps, occupancy rates or cycle time), giving you a very powerful business management tool that leverages your financial data. You

Fundamentals Level Skills Module, Paper F8. Section B

Answers Fundamentals Level Skills Module, Paper F8 Audit and Assurance September/December 2015 Answers Section B 1 Ethical threats and managing these risks (i) Ethical threat The finance director is the

Answers Fundamentals Level Skills Module, Paper F8 Audit and Assurance September/December 2015 Answers Section B 1 Ethical threats and managing these risks (i) Ethical threat The finance director is the

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

Guide to Internal Controls

Guide to Internal Controls Updated January 2017 The Guide to Internal Controls was developed to help you establish and maintain effective internal controls in your department/division. This guide summarizes

Guide to Internal Controls Updated January 2017 The Guide to Internal Controls was developed to help you establish and maintain effective internal controls in your department/division. This guide summarizes

MODULE 2: Engagement Planning (11% 17%)

") AU2 Advanced External Auditing MODULE 2: Engagement Planning (11% 17%) Lecturer: Glen B. Carlson, B. Comm.(Honours), C.G.A. Module 2 engagement planning Module 2 covers the planning of an audit engagement,

AU2 Advanced External Auditing MODULE 2: Engagement Planning (11% 17%) Lecturer: Glen B. Carlson, B. Comm.(Honours), C.G.A. Module 2 engagement planning Module 2 covers the planning of an audit engagement,

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

CIA Test Preparation Part I

CIA Test Preparation Part I Study Unit Five: Specific Controls June 2012 Agenda: Accounting Cycles and Associated Controls Management Controls 5.1 Accounting Cycles and Associated Controls Internal auditors

CIA Test Preparation Part I Study Unit Five: Specific Controls June 2012 Agenda: Accounting Cycles and Associated Controls Management Controls 5.1 Accounting Cycles and Associated Controls Internal auditors

Company owners and managers may hesitate to admit it, but fraud could be taking

CREDIT & FINANCE Do You Trust Your Employees? Occupational fraud can cost companies big money, but is preventable BY DAN ALAIMO Key Elements Occupational fraud is a common and costly part of the workplace,

CREDIT & FINANCE Do You Trust Your Employees? Occupational fraud can cost companies big money, but is preventable BY DAN ALAIMO Key Elements Occupational fraud is a common and costly part of the workplace,

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING CONTENTS

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

BIG LOTS, INC. CODE OF BUSINESS CONDUCT AND ETHICS

September 2003 BIG LOTS, INC. CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business principles to guide all directors, officers and associates

September 2003 BIG LOTS, INC. CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business principles to guide all directors, officers and associates

Year-End Close Checklists

Sage Master Builder Year-End Close Checklists Calendar-year, Fiscal-year, Combined NOTICE This document and the Sage Master Builder software may be used only in accordance with the accompanying Sage Master

Sage Master Builder Year-End Close Checklists Calendar-year, Fiscal-year, Combined NOTICE This document and the Sage Master Builder software may be used only in accordance with the accompanying Sage Master

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards

Chapter 2 Professional Standards") Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

GUIDE FOR END-OF-YEAR AP BEST PRACTICES

GUIDE FOR END-OF-YEAR AP BEST PRACTICES TABLE OF CONTENTS 04 Year-End Checklist for Accounts Payable 05 Sample Year-End Calendar 07 Master Vendor File Cleanup & Maintenance 11 1099 Misc. Reporting & Corrections

GUIDE FOR END-OF-YEAR AP BEST PRACTICES TABLE OF CONTENTS 04 Year-End Checklist for Accounts Payable 05 Sample Year-End Calendar 07 Master Vendor File Cleanup & Maintenance 11 1099 Misc. Reporting & Corrections

Design of Apps for Armchair Auditors to Analyze Government Procurement Contract

Design of Apps for Armchair Auditors to Analyze Government Procurement Contract Jun Dai Rutgers University Qiao Li Rutgers University Miklos A. Vasarhelyi Rutgers University Introduction Government procurement:

Design of Apps for Armchair Auditors to Analyze Government Procurement Contract Jun Dai Rutgers University Qiao Li Rutgers University Miklos A. Vasarhelyi Rutgers University Introduction Government procurement: