Chapter 06. Audit Planning, Understanding the Client, Assessing Risks, and Responding. McGraw-Hill/Irwin

|

|

|

- Oliver O’Neal’

- 5 years ago

- Views:

Transcription

1 Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

2 Obtaining Clients Submit a proposal Contact the audit committee Make fee arrangements Communicate with the predecessor auditor Topics Integrity of management Disagreements over accounting principles Communications to those charged with governance regarding fraud and noncompliance with laws Communication to management and those charged with governance concerning internal control significant deficiencies and material weaknesses. Predecessor s understanding of reason for change of auditors Other Overall procedure is important for evaluation of management integrity 6-2

3 The Audit Process-- Steps After obtaining a client, the audit process includes: 1. Plan the audit 2. Obtain an understanding of the client and its environment, including internal control 3. Assess the risks of material misstatement and design further audit procedures 4. Perform further audit procedures 5. Complete the audit 6. Form an opinion and issue the audit report This chapter emphasizes obtaining a client and steps

4 Stages of an Audit--Diagram 6-4

5 1. Plan the Audit Establish an understanding with the client This is ordinarily accomplished through use of an engagement letter Related, determine that The firm meets professional independence requirements There are no issues relating to management integrity The client understands the terms of the engagement 6-5

6 Name of the entity Management responsibilities Financial statements Items Included in Engagement Letters Establishing effective internal control over financial reporting Compliance with laws and regulations Making records available to the auditors Providing written representations at end of the audit, including that adjustments discovered by the auditors and not recorded to the financials are not material Auditor responsibilities Conducting an audit in accordance with GAAS Obtaining an understanding of internal control to plan audit and to determine the nature, timing and extent of procedures Making communications required by GAAS 6-6

7 Engagement Letters--Optional Items Arrangements regarding Conduct of the audit (e.g., timing, client assistance) Use of specialists or internal auditors Obtaining information from predecessor auditors Fees and billing Other services to be provided, such as examination of internal control over financial reporting Limitation of or other arrangements regarding liability of auditors or client Conditions under which access to the auditors working papers may be granted to others 6-7

8 Audit Planning Overall Develop an overall audit strategy and an audit plan Plan use of client s staff Plan involvement of other CPAs Arrange for specialists On first year audits: Communicate with predecessor auditors Establish opening balances on the financial statements 6-8

9 2. Obtain an Understanding of the Client and its Environment Perform risk assessment procedures, including Inquiries of management and others within the entity Analytical procedures Observation and inspection relating to client activities, operations, documents, reports and premises. Other procedures, such as inquiries of others outside the company (e.g., legal counsel, valuation experts) and reviewing information from external sources such as analysts, banks, rating organizations, journals. 6-9

10 Understanding the Client s Business Nature of the Client Competitive position Organizational structure Accounting policies and procedures Ownership Capital structure Product and service lines Critical business processes Internal control 6-10

11 Understanding the Client s Business, Industry, Regulatory, and Other Factors Competitive environment Supplier and customer relationships Technology developments Major laws and regulations Economic conditions Attractiveness of the industry Barriers to entry Strength of competitors Bargaining power of suppliers of raw materials and labor Bargaining power of customers 6-11

12 Understanding the Client s Business Objectives, Strategies & Business Risks Objectives Overall plans Operating and financial strategies Operational actions to achieve objectives Business risks Threats to achieving objectives 6-12

13 Understanding the Client s Business Measuring and Reviewing Performance Budgets Key performance indicators Variance analysis Segment performance reports Balanced scorecard External parties 6-13

14 Understanding the Client s Business Internal Control Need knowledge and understanding of how a client s internal control works: What controls exists Who performs them How various types of transactions are processed and recorded What accounting records and supporting documentation exist 6-14

15 Understanding the Client s Business Sources of Information Inquiries of management Industry Accounting and Auditing Guides Industry Risk Alerts Trade journals and news stories Government publications Prior company annual reports and SEC filings Prior tax returns Electronic sources Ex. web pages for company Tour of plant and offices Analytical procedures The statement of cash flows and obtaining an understanding of the client 6-15

16 Determining Materiality Use professional judgment and based on reasonable person Considers both Quantitative and qualitative factors Materiality used in Planning the audit At the overall financial statement level Allocate to individual accounts Evaluating audit findings 6-16

17 Materiality Definitions FASB (included in SASs) The magnitude of an omission or misstatement of financial information that, in the light of surrounding circumstances, makes it probable that he judgment of a reasonable person relying on the information could have been changed or influenced by the omission or misstatement. PCAOB interpretation of federal securities laws A fact is material if there is a substantial likelihood that the fact would have been viewed by the reasonable investor as having significantly altered the total mix of information made available. 6-17

18 3. Assess the Risks of Material Misstatement and Design Further Audit Procedures Overall approach What could go wrong? How likely is it that it will go wrong? What are the likely amounts involved? Particularly consider Inherent risks Risks of material misstatement due to fraud (fraud risks) Design further audit procedures 6-18

19 Two types Assessing Fraud Risks Fraudulent financial reporting (management fraud) Misappropriation of assets (defalcations) Procedures to assess fraud risks Discussion among engagement team Inquiries of management and other personnel Risk assessment analytical procedures (to aid in planning the audit) Considering fraud risk factors Incentives Opportunity Attitude 6-19

20 Assessing Fraud Risks Identifying Fraud Risks Considerations in identifying fraud risks Type Significance Likelihood that it will result in a material misstatement Pervasiveness 6-20

21 Responding to Fraud Risks Overall response Professional skepticism and audit evidence Assigning personnel and supervision Accounting principles Predictability of auditing procedures Alterations in audit procedures More reliable evidence Shifting timing to year end Increasing sample sizes Response to the possibility of management override Examining journal entries Review accounting estimates for biases Evaluating the business rationale for significant unusual transactions 6-21

22 Consideration of Fraud Throughout the Audit Evaluating the results of audit tests Discovery of fraud Communication to appropriate level of management If fraud involves senior management or material misstatement communicate to audit committee 6-22

23 Design Further Audit Procedures Types Tests of controls Analytical procedures (1/2) Tests of details of transactions and balances Audit procedures Inspection Observation Inquiry Confirmation Recalculation Reperformance 6-23

24 Design Further Audit Procedures (2/2) Further audit procedures should include Substantive procedures for all relevant assertions Tests of controls when the auditors risk assessment includes an expectation that controls are operating effectively, or when substantive procedures alone are not sufficient Procedures should be linked with the assessed risks of material misstatement at the relevant assertion level Overall responses when assessed risks of material misstatement are high Heightened professional skepticism Assigning more experienced staff Assigning staff with specialized skills Providing more supervision 6-24

25 Audit Documentation Audit Documentation Risk assessment Discussion of the audit team, elements of understanding, assessment of risk of material misstatement and risks identified Procedure results Overall responses, nature, timing and extent of further audit procedures, linkage of procedures with assessed risks, results of audit procedures, conclusions reached about operating effectiveness of controls, significant risk identified, circumstances in which substantive procedures alone will not provide sufficient evidence Consideration of fraud Similar to risk assessment as document discussion, procedures used to identify fraud risks, fraud risk and response, any other conditions that caused fraud-related procedures and communications with management or audit committee. 6-25

26 Audit Trail A trail of evidence that links source documents, journal entries and ledger entries Auditor may follow the audit trail in either of two directions related to the direction of testing Test for existence or occurrence Test for completeness 6-26

27 Direction of Audit Testing 6-27

28 Transaction cycles Auditors consideration of internal control is often organized around client s major transaction cycles (examples) Revenue cycle Acquisition cycle Conversion cycle Payroll cycle Investing cycle Financing cycle 6-28

29 Transactions Affecting Accounts Receivable 6-29

30 Audit Program Systems portion Deals with client s internal control Evidence of test of controls and assessing control risk Substantive test portion Deals with financial statement account balances Indirect and direct verification of income statement accounts 6-30

31 Indirect Verification of Income Statement Accounts 6-31

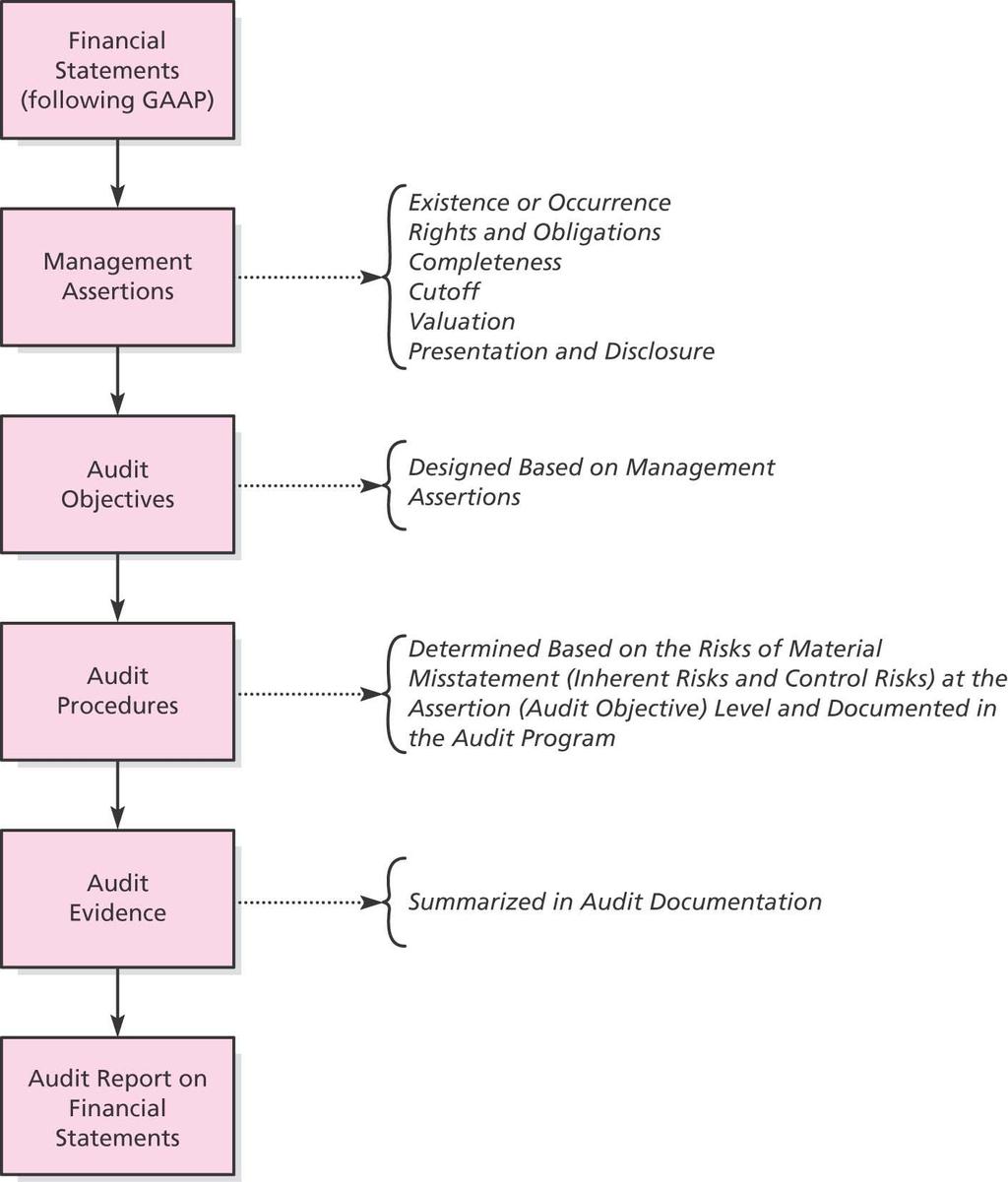

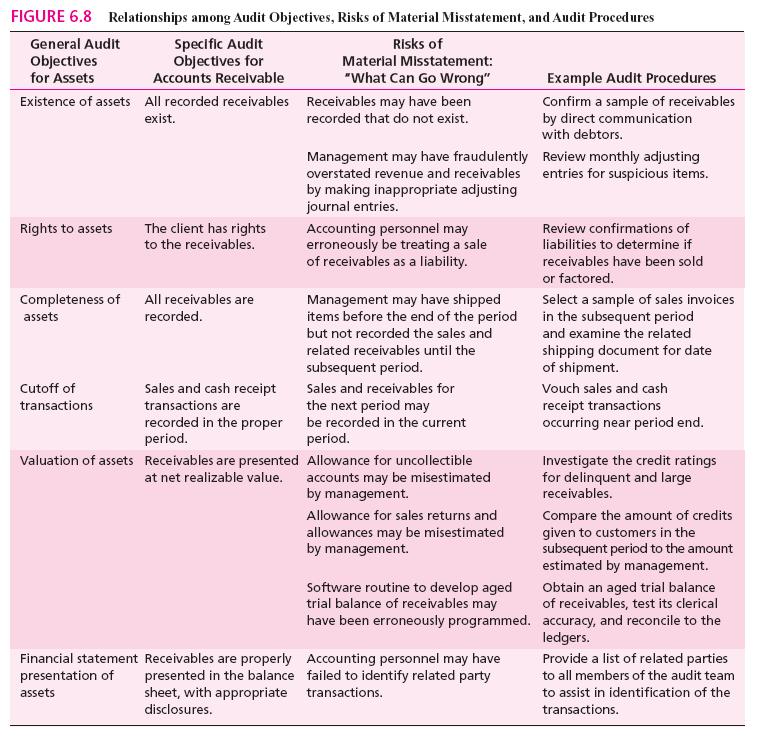

32 Objectives of Substantive Programs for Asset Accounts Establish the existence of assets Establish that the company has rights to the assets Establish the completeness of recorded assets Verify the cutoff of transactions Determine the appropriate valuation of the assets and accuracy of related transactions Determine the appropriate financial statement presentation and disclosure of the assets 6-32

33 Relationship of Financial Statement Assertions to the Audit 6-33

34 Relationships among Audit Objectives, Risks of Material Misstatement, and Audit Procedures 6-34

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

Chapter 18. Integrated Audits of Public Companies. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

AUDIT RESPONSIBILITIES AND OBJECTIVES

AUDIT RESPONSIBILITIES AND OBJECTIVES CHAPTER 6 Copyright 2017 Pearson Education, Ltd. 6-1 CHAPTER 1 LEARNING OBJECTIVES 6-1 Explain the objective of conducting an audit of financial statements and an

AUDIT RESPONSIBILITIES AND OBJECTIVES CHAPTER 6 Copyright 2017 Pearson Education, Ltd. 6-1 CHAPTER 1 LEARNING OBJECTIVES 6-1 Explain the objective of conducting an audit of financial statements and an

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE CONTENTS

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

Mapping of Original ISA 315 to New ISA 315 s Standards and Application Material (AM) Agenda Item 2-C

Agenda Item 2-C") Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a. AUDITING THEORY Risk Assessment and Response to Assessed Risks

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

VERSION #1 WRITE ON YOUR SCANTRON!!!

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

Chapter 16. Auditing Operations and Completing the Audit. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 16 Auditing Operations and Completing the Audit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Auditing Operations Corporate earnings are considered as

Chapter 16 Auditing Operations and Completing the Audit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Auditing Operations Corporate earnings are considered as

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

2. The auditors' report on a corporation's financial statements usually is addressed to the president of the company.

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining)

") Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a AUDITING THEORY AUDIT PLANNING

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

Audit Evidence. ISA 500 Issued December International Standard on Auditing

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

Chapter 02. Professional Standards. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,

An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements

ASB Meeting July 30 August 1, 2013 Agenda Item 3B AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

ASB Meeting July 30 August 1, 2013 Agenda Item 3B AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

IAASB CAG Public Session (March 2018) CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1

CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1") Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

covered member immediate family impaired not a covered member close relative not impaired

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

SRI LANKA AUDITING STANDARD 315 (REVISED)

") SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements

SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements

(Effective for audits of financial statements for periods ending on or after December 15, 2013) CONTENTS

CONTENTS") INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

International Standard on Auditing (Ireland) 315

315") International Standard on Auditing (Ireland) 315 Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and its Environment MISSION To contribute to Ireland having

International Standard on Auditing (Ireland) 315 Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and its Environment MISSION To contribute to Ireland having

International Standard on Auditing (Ireland) 500 Audit Evidence

500 Audit Evidence") International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

STANDING ADVISORY GROUP MEETING

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING CONSIDERATION OF OUTREACH AND RESEARCH REGARDING THE AUDITOR'S

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING CONSIDERATION OF OUTREACH AND RESEARCH REGARDING THE AUDITOR'S

MODULE 2: Engagement Planning (11% 17%)

") AU2 Advanced External Auditing MODULE 2: Engagement Planning (11% 17%) Lecturer: Glen B. Carlson, B. Comm.(Honours), C.G.A. Module 2 engagement planning Module 2 covers the planning of an audit engagement,

AU2 Advanced External Auditing MODULE 2: Engagement Planning (11% 17%) Lecturer: Glen B. Carlson, B. Comm.(Honours), C.G.A. Module 2 engagement planning Module 2 covers the planning of an audit engagement,

Chapter 5. Evidence and Documentation. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 5 Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Relationship of Audit LO# 1 Evidence to the Audit Report Financial statements

Chapter 5 Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Relationship of Audit LO# 1 Evidence to the Audit Report Financial statements

Mapping Document AU Section 322 to Clarified Statement on Auditing Standards Using the Work of Internal Auditors

1 MAPPING DOCUMENT CLARIFIED STATEMENT ON AUDITING STANDARDS USING THE WORK OF INTERNAL AUDITORS This mapping document demonstrates how the material in extant AU section 322, The Auditor s Consideration

1 MAPPING DOCUMENT CLARIFIED STATEMENT ON AUDITING STANDARDS USING THE WORK OF INTERNAL AUDITORS This mapping document demonstrates how the material in extant AU section 322, The Auditor s Consideration

Detailed competency map

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

Chapter 4. Risk Assessment. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 4 Risk Assessment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Audit Risk The risk that an auditor expresses an unqualified opinion on materially

Chapter 4 Risk Assessment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Audit Risk The risk that an auditor expresses an unqualified opinion on materially

Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

6 Assessment of risk Introduction General risk assessment Specific risk assessment Reliability factors 50 6.

The Institute of Chartered Accountants of Sri Lanka Audit Manual Guidance Notes CONTENTS 1 Using the ICASL Audit Manual 3 1.1 Introduction 3 1.2 Referencing system 3 1.3 Forms 3 1.4 Printing 3 2 Key Issues

The Institute of Chartered Accountants of Sri Lanka Audit Manual Guidance Notes CONTENTS 1 Using the ICASL Audit Manual 3 1.1 Introduction 3 1.2 Referencing system 3 1.3 Forms 3 1.4 Printing 3 2 Key Issues

Chapter 7. Auditing Internal Control over Financial Reporting. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 7 Auditing Internal Control over Financial Reporting McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Management Responsibilities under Section 404 Management

Chapter 7 Auditing Internal Control over Financial Reporting McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Management Responsibilities under Section 404 Management

PLEASE complete #1-25 on your green scantron and the rest of them in your blue book.

Name: Date: You can keep this exam. PLEASE complete #1-25 on your green scantron and the rest of them in your blue book. 1. To qualify as "principal auditor" and render an opinion on the financial statements

Name: Date: You can keep this exam. PLEASE complete #1-25 on your green scantron and the rest of them in your blue book. 1. To qualify as "principal auditor" and render an opinion on the financial statements

Consideration of Fraud in a Financial Statement Audit (Redrafted) *

*") STATEMENT ON AUDITING STANDARDS Consideration of Fraud in a Financial Statement Audit (Redrafted) * Statement on Auditing Standards (SAS) Consideration of Fraud in a Financial Statement Audit (Redrafted)

STATEMENT ON AUDITING STANDARDS Consideration of Fraud in a Financial Statement Audit (Redrafted) * Statement on Auditing Standards (SAS) Consideration of Fraud in a Financial Statement Audit (Redrafted)

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS

TECHNICAL COMPETENCE REQUIREMENTS") REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

IAASB Main Agenda (March 2005) Page Agenda Item 12-C

Page Agenda Item 12-C") IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

Audit Evidence. SSA 500, Audit Evidence superseded the SSA of the same title in September 2009.

SINGAPORE STANDARD SSA 500 ON AUDITING Audit Evidence SSA 500, Audit Evidence superseded the SSA of the same title in September 2009. SSA 610 (Revised 2013), Using the Work of Internal Auditors gave rise

SINGAPORE STANDARD SSA 500 ON AUDITING Audit Evidence SSA 500, Audit Evidence superseded the SSA of the same title in September 2009. SSA 610 (Revised 2013), Using the Work of Internal Auditors gave rise

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008

10 July 2008") Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

Auditing and Attestation (AUD) - Content Outline Effective January 2014

- Content Outline Effective January 2014") Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

THE AUDITOR S RESPONSES TO ASSESSED RISKS SRI LANKA AUDITING STANDARD 330 THE AUDITOR S RESPONSES TO ASSESSED RISKS

SRI LANKA STANDARD 330 THE AUDITOR S RESPONSES TO ASSESSED RISKS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph Introduction Scope of

SRI LANKA STANDARD 330 THE AUDITOR S RESPONSES TO ASSESSED RISKS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph Introduction Scope of

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

Institute of Chartered Accountants of India. Standards on Auditing

Institute of Chartered Accountants of India Standards on Auditing Presented by: CA Sunil Nagrani February 16, 2013 Contents SA 315 - Identifying and Assessing the Risk of Material Misstatement Through

Institute of Chartered Accountants of India Standards on Auditing Presented by: CA Sunil Nagrani February 16, 2013 Contents SA 315 - Identifying and Assessing the Risk of Material Misstatement Through

IAASB Main Agenda (December 2004) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

APPENDIX A. Audit Findings Report. For the Year ended March 31, 2017

APPENDIX A Audit Findings Report For the Year ended March 31, 2017 Annual General Meeting June 19, 2017 Muskoka Algonquin Healthcare Audit Findings Report For the year ended March 31, 2017 Chartered Professional

APPENDIX A Audit Findings Report For the Year ended March 31, 2017 Annual General Meeting June 19, 2017 Muskoka Algonquin Healthcare Audit Findings Report For the year ended March 31, 2017 Chartered Professional

Audit Practice Introduced by HKSA (HKSA 315 and 330) 1 February 2008

1 February 2008") Audit Practice Introduced by HKSA (HKSA 315 and 330) 1 February 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Audit Practice Introduced by HKSA (HKSA 315 and 330) 1 February 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

WATCH WORDS FROM THE PEER REVIEW PROCESS

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

Due: Tuesday, May 1, 2007 by 5:45 p.m.

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

International Standard on Auditing (UK and Ireland) 500

500") Standard Audit and Assurance Financial Reporting Council October 2009 International Standard on Auditing (UK and Ireland) 500 Audit evidence The FRC is responsible for promoting high quality corporate

Standard Audit and Assurance Financial Reporting Council October 2009 International Standard on Auditing (UK and Ireland) 500 Audit evidence The FRC is responsible for promoting high quality corporate

1. Auditors may be independent in fact but not independent in appearance. 3. Attestation standards provide guidance for a wide variety of engagements

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

International Standard on Auditing (UK) 315 (Revised June 2016)

315 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 315 (Revised June 2016) Identifying and Assessing the Risks of Material Misstatement Through Understanding

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 315 (Revised June 2016) Identifying and Assessing the Risks of Material Misstatement Through Understanding

Audit Evidence. HKSA 500 Issued July 2009; revised July 2010, May 2013, February 2015, August 2015, June 2017

HKSA 500 Issued July 2009; revised July 2010, May 2013, February 2015, August 2015, June 2017 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard

HKSA 500 Issued July 2009; revised July 2010, May 2013, February 2015, August 2015, June 2017 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard

Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 February 2008 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment INTERNATIONAL STANDARD ON AUDITING

ISA 315 February 2008 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment INTERNATIONAL STANDARD ON AUDITING

ISA 240 (Redrafted), The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements

, The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements") CONFORMING AMENDMENTS TO OTHER STANDARDS AS A RESULT OF ISA 265, COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHANGED WITH GOVERNANCE AND MANAGEMENT ISA 240 (Redrafted), The Auditor s Responsibilities

CONFORMING AMENDMENTS TO OTHER STANDARDS AS A RESULT OF ISA 265, COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHANGED WITH GOVERNANCE AND MANAGEMENT ISA 240 (Redrafted), The Auditor s Responsibilities

AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS: GUIDANCE FOR AUDITORS OF SMALLER PUBLIC COMPANIES

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State

Scope of this SA Effective Date Objective Definitions Sufficient Appropriate Audit Evidence... 6

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State

AT Assertions, Audit Procedures and Audit Evidence Red Sirug Page 1

AUDITING THEORY Red Sirug ASSERTIONS A ND A UDIT OBJECTIVES ASSERTIONS, A UDIT PROCEDURES A ND A UDIT EVIDENCE Nature of Assertions: Financial statements are not statements of facts. They are a collection

AUDITING THEORY Red Sirug ASSERTIONS A ND A UDIT OBJECTIVES ASSERTIONS, A UDIT PROCEDURES A ND A UDIT EVIDENCE Nature of Assertions: Financial statements are not statements of facts. They are a collection

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards

Chapter 2 Professional Standards") Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

3/29/15. Module 3: Audit objectives, evidence, procedures, and documentation

Assignment reminder: Assignment #1 (see Module 5) is due at the end of Week 5 (see Course Schedule). You may wish to take a look at it now in order to familiarize yourself with the requirements and to

Assignment reminder: Assignment #1 (see Module 5) is due at the end of Week 5 (see Course Schedule). You may wish to take a look at it now in order to familiarize yourself with the requirements and to

Chapter 8. Planning and Testing Operating Effectiveness of Internal Control over Financial Reporting. Prepared by Richard J.

Chapter 8 Planning and Testing Operating Effectiveness of Internal Control over Financial Reporting Prepared by Richard J. Campbell Copyright 2011, Wiley and Sons Learning Objectives 1. Learn the relationships

Chapter 8 Planning and Testing Operating Effectiveness of Internal Control over Financial Reporting Prepared by Richard J. Campbell Copyright 2011, Wiley and Sons Learning Objectives 1. Learn the relationships

Audit Evidence This section is effective for audits of financial statements for periods ending on or after December 15, 2012.

Audit Evidence 395 AU-C Section 500 Audit Evidence Source: SAS No. 122; SAS No. 128. See section 9500 for interpretations of this section. Effective for audits of financial statements for periods ending

Audit Evidence 395 AU-C Section 500 Audit Evidence Source: SAS No. 122; SAS No. 128. See section 9500 for interpretations of this section. Effective for audits of financial statements for periods ending

Auditing Standards and Practices Council

Auditing Standards and Practices Council AUDIT EVIDENCE PHILIPPINE STANDARDON AUDITING 500 (REVISED) AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December

Auditing Standards and Practices Council AUDIT EVIDENCE PHILIPPINE STANDARDON AUDITING 500 (REVISED) AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December

Pre-Engagement Activities and Audit Planning By: Tariq Mahmood FCA, ACMA

Model Audit Practice Manual Pre-Engagement Activities and Audit Planning By: Tariq Mahmood FCA, ACMA Today s Learnings Pre-Engagement Activities Audit Planning Procedures Completion of Sample Forms (Annexures)

Model Audit Practice Manual Pre-Engagement Activities and Audit Planning By: Tariq Mahmood FCA, ACMA Today s Learnings Pre-Engagement Activities Audit Planning Procedures Completion of Sample Forms (Annexures)

Navigating the PCAOB s and SEC s internal control expectations A discussion. June 2015

Navigating the PCAOB s and SEC s internal control expectations A discussion June 2015 Setting the scene ICFR guidance: PCAOB Auditing Standard No. 5 (May 2007) PCAOB staff views: An Audit of Internal Control

Navigating the PCAOB s and SEC s internal control expectations A discussion June 2015 Setting the scene ICFR guidance: PCAOB Auditing Standard No. 5 (May 2007) PCAOB staff views: An Audit of Internal Control

Presenter: CPA CATHERINE MUEMA

Presenter: CPA CATHERINE MUEMA ISA 230 requires an auditor to prepare audit documentation that is sufficient and appropriate to support the basis for the Auditor s report and confirm that the audit process

Presenter: CPA CATHERINE MUEMA ISA 230 requires an auditor to prepare audit documentation that is sufficient and appropriate to support the basis for the Auditor s report and confirm that the audit process

EFFICIENT USE OF AUDIT COMMITTEES

AGENDA EFFICIENT USE OF AUDIT COMMITTEES BRENT YOUNG, CPA JERRY GAITHER, CPA Best practices related to: Audit Committee Process Internal Audit Risk Management 2 AUDIT COMMITTEE PROCESS AND PROCEDURES Audit

AGENDA EFFICIENT USE OF AUDIT COMMITTEES BRENT YOUNG, CPA JERRY GAITHER, CPA Best practices related to: Audit Committee Process Internal Audit Risk Management 2 AUDIT COMMITTEE PROCESS AND PROCEDURES Audit

Chapter 02. Professional Standards. Multiple Choice Questions. 1. Control risk is

Chapter 02 Professional Standards Multiple Choice Questions 1. Control risk is A. the probability that a material misstatement could not be prevented or detected by the entity's internal control policies

Chapter 02 Professional Standards Multiple Choice Questions 1. Control risk is A. the probability that a material misstatement could not be prevented or detected by the entity's internal control policies

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING All public companies either have begun or will soon begin a process, required under Section 404 of the Sarbanes-Oxley Act of 2002 ( SOX ), of reviewing

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING All public companies either have begun or will soon begin a process, required under Section 404 of the Sarbanes-Oxley Act of 2002 ( SOX ), of reviewing

International Auditing and Assurance Standards Board ISA 500. April International Standard on Auditing. Audit Evidence

International Auditing and Assurance Standards Board ISA 500 April 2009 International Standard on Auditing Audit Evidence International Auditing and Assurance Standards Board International Federation of

International Auditing and Assurance Standards Board ISA 500 April 2009 International Standard on Auditing Audit Evidence International Auditing and Assurance Standards Board International Federation of

ISA 500. Issued March 2009; updated June International Standard on Auditing. Audit Evidence

ISA 500 Issued March 2009; updated June 2018 International Standard on Auditing Audit Evidence INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE The Malaysian Institute of Accountants has approved

ISA 500 Issued March 2009; updated June 2018 International Standard on Auditing Audit Evidence INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE The Malaysian Institute of Accountants has approved

IAASB Main Agenda (September 2004) Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540

Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540") IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

The Auditor s Responses to Assessed Risks

SINGAPORE STANDARD SSA 330 ON AUDITING The Auditor s Responses to Assessed Risks SSA 330, The Auditor s Responses to Assessed Risks superseded SSA 330, The Auditor s Procedures in Response to Assessed

SINGAPORE STANDARD SSA 330 ON AUDITING The Auditor s Responses to Assessed Risks SSA 330, The Auditor s Responses to Assessed Risks superseded SSA 330, The Auditor s Procedures in Response to Assessed

Audit Workshop Part 2 12 December 2009

Audit Workshop Part 2 12 December 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson Consulting Limited 1 Agenda for Part 1 and Part 2 Planning Risk

Audit Workshop Part 2 12 December 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson Consulting Limited 1 Agenda for Part 1 and Part 2 Planning Risk

Cost Auditing Standard Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment

Cost Auditing Standard - 104 Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Auditing Standard (Cost Auditing Standard - 104) on Knowledge

Cost Auditing Standard - 104 Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Auditing Standard (Cost Auditing Standard - 104) on Knowledge

13-A. Fraud Phase II Issues Paper

IAASB Main Agenda Page 2002 855 Agenda Item 13-A Convergence with US Fraud Standard 1. In March 2001, the IAPC approved revisions to ISA 240 The Auditor s Responsibility to Consider Fraud and Error in

IAASB Main Agenda Page 2002 855 Agenda Item 13-A Convergence with US Fraud Standard 1. In March 2001, the IAPC approved revisions to ISA 240 The Auditor s Responsibility to Consider Fraud and Error in

Report on Inspection of KPMG AG Wirtschaftspruefungsgesellschaft (Headquartered in Berlin, Federal Republic of Germany)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

IAASB Main Agenda (March 2019) Agenda Item

Agenda Item") Agenda Item 8 B (For Reference) INTERNATIONAL STANDARD ON AUDTING (ISA) 500, AUDIT EVIDENCE (INCLUDING CONSEQUENTIAL AND CONFORMING AMENDMENTS FROM ISA 540 (REVISED) 1 ) Introduction Scope of this ISA

Agenda Item 8 B (For Reference) INTERNATIONAL STANDARD ON AUDTING (ISA) 500, AUDIT EVIDENCE (INCLUDING CONSEQUENTIAL AND CONFORMING AMENDMENTS FROM ISA 540 (REVISED) 1 ) Introduction Scope of this ISA

and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

IFACIAAS Board IAASB Main Agenda (April 2013) Agenda Iten 5-D Final Pronouncement March 2012 International Standard on Auditing ISA 315 (Revised), Identifying and Assessing the Risks of Material Misstatement

IFACIAAS Board IAASB Main Agenda (April 2013) Agenda Iten 5-D Final Pronouncement March 2012 International Standard on Auditing ISA 315 (Revised), Identifying and Assessing the Risks of Material Misstatement

Internal controls over Financial Reporting Key concepts. Presentation by Jayesh Gandhi at WIRC

Internal controls over Financial Reporting Key concepts Presentation by Jayesh Gandhi at WIRC Page 1 ICFR Key Concepts WIRC 28 May 2016 Agenda Scope and requirements Overview of internal controls as per

Internal controls over Financial Reporting Key concepts Presentation by Jayesh Gandhi at WIRC Page 1 ICFR Key Concepts WIRC 28 May 2016 Agenda Scope and requirements Overview of internal controls as per

After completing this Session, you should be able to answer the following questions:

About this Course Welcome to CMA Auditing Course, Part II. Below, you will find a short summary of the modules. Upon registration, further introductory resources will tell you: How the course is organized

About this Course Welcome to CMA Auditing Course, Part II. Below, you will find a short summary of the modules. Upon registration, further introductory resources will tell you: How the course is organized

AUDIT TECHNIQUES---SA 500

AUDIT TECHNIQUES---SA 500 Audit techniques stand for the methods that are adopted by an auditor to obtain evidence. Audit evidence Information used by the auditor in arriving at the conclusions on which

AUDIT TECHNIQUES---SA 500 Audit techniques stand for the methods that are adopted by an auditor to obtain evidence. Audit evidence Information used by the auditor in arriving at the conclusions on which

PCAOB Auditing Standard 15 addresses audit evidence. What is audit evidence?

PCAOB Auditing Standard 15 addresses audit evidence. What is audit evidence? Audit evidence is all the information, whether obtained from audit procedures or other sources, that is used by the auditor

PCAOB Auditing Standard 15 addresses audit evidence. What is audit evidence? Audit evidence is all the information, whether obtained from audit procedures or other sources, that is used by the auditor

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing 330 (Redrafted) THE AUDITOR S RESPONSES TO ASSESSED RISKS Introduction PHILIPPINE STANDARD ON AUDITING 330 (REDRAFTED) THE AUDITOR

Auditing and Assurance Standards Council Philippine Standard on Auditing 330 (Redrafted) THE AUDITOR S RESPONSES TO ASSESSED RISKS Introduction PHILIPPINE STANDARD ON AUDITING 330 (REDRAFTED) THE AUDITOR

IAASB Main Agenda (December 2008) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2008) Page 2008 2669 Agenda Item 2-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL (Effective for audits of financial statements

IAASB Main Agenda (December 2008) Page 2008 2669 Agenda Item 2-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL (Effective for audits of financial statements

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young. Lessons on Audit Risk. Responding to fraud risk

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

APPENDIX A. Audit Findings Report. For the Year ended March 31, 2016

APPENDIX A Audit Findings Report For the Year ended March 31, 2016 Annual General Meeting June 20, 2016 Muskoka Algonquin Healthcare Audit Findings Report For the year ended March 31, 2016 Chartered Professional

APPENDIX A Audit Findings Report For the Year ended March 31, 2016 Annual General Meeting June 20, 2016 Muskoka Algonquin Healthcare Audit Findings Report For the year ended March 31, 2016 Chartered Professional

Special Audit Techniques. CA Final Paper 3: Advanced Auditing & Professional Ethics Chapter 5 CA Arijit Chakraborty

Special Audit Techniques CA Final Paper 3: Advanced Auditing & Professional Ethics Chapter 5 CA Arijit Chakraborty 2 Agenda for discussion - Special Audit Techniques Audit evidence -Confirmation, inquiry,

Special Audit Techniques CA Final Paper 3: Advanced Auditing & Professional Ethics Chapter 5 CA Arijit Chakraborty 2 Agenda for discussion - Special Audit Techniques Audit evidence -Confirmation, inquiry,

Report on Inspection of K. R. Margetson Ltd. (Headquartered in Vancouver, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Vancouver, Canada) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Vancouver, Canada) Issued by the Public Company Accounting

Does Your Report Pass Muster in a BV Audit?

American Society of Appraisers International Appraisal Conference Does Your Report Pass Muster in a BV Audit? Raymond Rath, ASA, CEIV, CFA Globalview Advisors LLC October 9, 2018 Introduction Valuation

American Society of Appraisers International Appraisal Conference Does Your Report Pass Muster in a BV Audit? Raymond Rath, ASA, CEIV, CFA Globalview Advisors LLC October 9, 2018 Introduction Valuation

IAASB Main Agenda (June 2008) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (June 2008) Page 2008 595 Agenda Item 2-A PROPOSED INTERNATIONAL STANDARD ON AUDITING 500 (REDRAFTED) OBTAINING SUFFICIENT APPROPRIATE AUDIT EVIDENCE (Mark-up Showing Changes from March

IAASB Main Agenda (June 2008) Page 2008 595 Agenda Item 2-A PROPOSED INTERNATIONAL STANDARD ON AUDITING 500 (REDRAFTED) OBTAINING SUFFICIENT APPROPRIATE AUDIT EVIDENCE (Mark-up Showing Changes from March