TOPIC 11: PRE APPOINTMENT PROCEDURES - LETTER OF ENGAGEMENT

|

|

|

- Stephen Stevenson

- 5 years ago

- Views:

Transcription

1 TOPIC 11: PRE APPOINTMENT PROCEDURES - LETTER OF ENGAGEMENT Acceptance of Audit and Review Assignments The Audit Appointment Process 1

2 The First Steps when offered a new Audit Project is sometimes referred to as Client Screening Procedures. The relationship between Auditor and client tends 2

3 to be long term in nature and therefore justifies any effort expended at this early stage to get things right. Client Screening Procedures Pre-Appointment If offered an audit role, the auditor should consider the impact of professional ethics and other requirements in relation to the acceptance of audit and review assignments, including situations in which there is an imposed limitation of scope. In all cases the Auditor should: Ask client for permission to contact outgoing auditor (reject role if client refuses) Contact outgoing auditor, asking for relevant matters (if client has caused problems, may have to say no to the appointment, i.e. disagreements over fees, scope or opinion) Ensure outgoing auditors resignation or removal properly conducted Co Act 2014 S400 (Resignation)/ S394 (Removal) Resignation : A statutory auditor may serve notice in writing on the company stating their intention to resign. The notice must contain a statement to the effect that either: 3

4 (a) there are no circumstances connected with the resignation that should be brought to the notice of the members or creditors of the company, or (b) there are circumstances that the statutory auditor considers should be brought to the attention of members or creditors. Where the statutory auditor serves a notice on the company of their resignation, they must within 14 days send a copy of the notice to the Registrar of Companies. Where the auditor has listed circumstances in the notice that should be brought to the attention of members, the company must within 14 days send a copy of the notice to every person who is entitled to receive a copy. Removal : A company may, by ordinary resolution at a general meeting, remove a statutory auditor and appoint, in his or her place, any other person or persons who have been nominated for appointment by any member of the company and who holds the relevant qualifications as set out in European Communities (Statutory Audits) (Directive 2006/43/EC) Regulations 2010 (S.I. No. 220 of 2010), to become statutory auditor of the company, and whose nomination notice has been given to the members. The passing of a resolution for the removal of the statutory auditor will not be effective unless there are good and substantial grounds for the removal related to the conduct of the auditors in performing his or her duties as auditor of the company, or the passing of the resolution is, in the company s opinion, in the best interests of the company. However, diverging opinions on accounting treatment or audit procedures cannot 4

5 constitute the basis for the passing of any such resolution and reference to the best interests of the company does not include any illegal or improper motive, such as, avoiding disclosures or detection of any failure by the company to comply with its obligations under the Companies Act 2014 Carry out checks to ensure we can be independent (MASSIF!), are competent to do this audit, have necessary resources, logistics and staff etc. Assess whether this work is suitably low risk i.e. : Good long-term prospects ; Well-financed ; Strong internal controls ; Conservative prudent accounting policies; Competent honest management; Few unusual transactions Assess integrity of the company s directors As a commercial organisation, we should also ensure that this client is one we want (e.g. right industry, suitable profit margin available to us etc). Also, in terms of advertising for a new client, the advertising medium should not reflect adversely on the member, CPA or the accountancy profession. Adverts should not - Bring CPA into disrepute 5

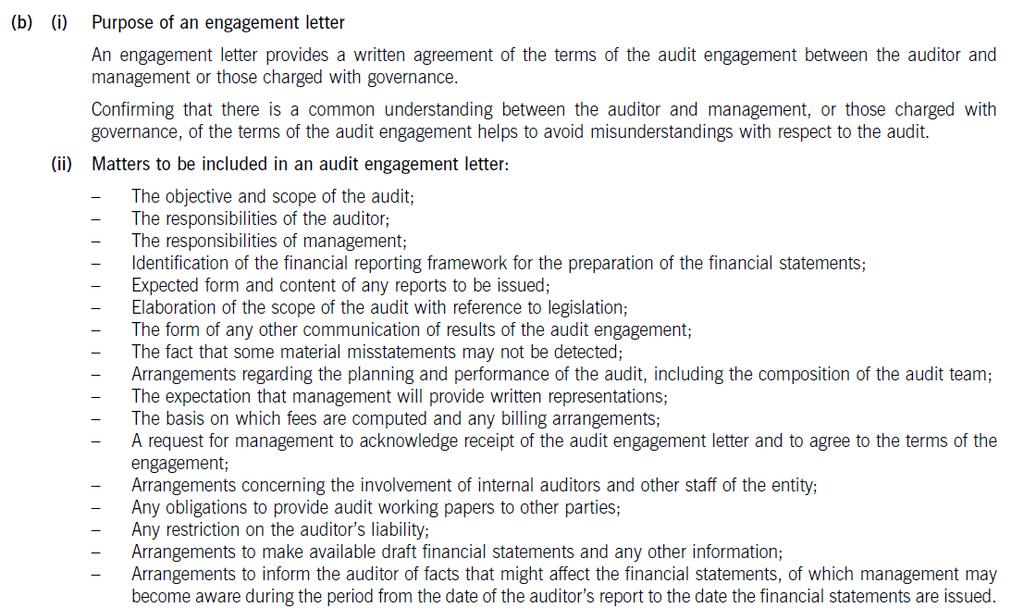

6 - Discredit the services of others - Be Misleading - Fall short of local regulatory requirements Also the member must not engage in lowballing charging less than market rate for an audit whereby the quality of the audit provided maybe threatened and also independence could be questioned IMPOSED LIMITATION OF SCOPE The auditor is entitled to all information and explanations he considers necessary for the conduct of his work. Where auditors know, before accepting an appointment, that their work (or evidence) is going to be restricted, they should not accept the appointment. Likewise, if a restriction is imposed during an audit, resignation should be considered. ENGAGEMENT LETTER The importance of engagement letter cannot be understated as it forms/documents the contract between the Auditor and the Client. This will be the first point of reference should any confusion arise and the Auditor must ensure that all work undertaken is documented within the Engagement Letter. The standard Engagement Letter would be expected to address the following areas. 6

7 The Auditor / Client Contract Audit Fees - how these will be calculated and when payment due. Set out the work The Auditor will do and the manner of completion o Follow auditing standards and regulations o Assess Internal Control System o Seek sufficient, appropriate evidence o Seek Management Assurances o Issue audit opinions o Details of other services, if required Respective Responsibilities, emphasising the Directors o Responsibility for Maintaining and Granting Access to Accounting Records o Management Representations o True & Fair Fin Stats Both Auditor and Management/Those Charged with Governance must sign the Engagement letter. The Engagement letter constitutes a legal contract between the auditors and the client. The Engagement Letter will be sent before the first audit so as to avoid misunderstandings regarding the audit. The letter will be regularly replaced to update it for changes in laws, regulations and standards. Many firms of auditors prefer to send a new letter every year, to emphasise its importance to clients. The issue of an annual Engagement letter is considered best practice. 7

8 ISA 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS Fast Forward The terms of the audit engagement shall be agreed with management and recorded in an audit engagement letter 3.1 Preconditions for an audit ISA 210 Agreeing the terms of audit engagements states that the objective of the auditor is to accept or continue an audit engagement only when the basis on which it is to be carried out has been agreed by establishing whether the preconditions for an audit are present and confirming that there is a common understanding between the auditor and management of the terms of the engagement Key term The preconditions for an audit are the use by management of an acceptable financial reporting framework in the preparation of the financial statements and the agreement of management and, where appropriate, those charged with governance to the premise on which an audit is conducted. To determine whether the preconditions for an audit are present, the auditor shall do the following: Determine whether the financial reporting is acceptable. Factors to consider include the nature of the entity, the purpose of the financial statements, the nature of the financial statements, and whether law or regulation prescribes the applicable financial reporting framework Obtain management s agreement that it acknowledges and understands its responsibilities for the following. Preparing the financial statements in accordance with the applicable financial reporting framework 8

9 Internal control that is necessary to enable the preparation of financial statements which are free from material misstatement Providing the auditor with access to all information of which management is aware that is relevant to the preparation of the financial statements, with additional information that the auditor may request, and with unrestricted access to entity staff from whom the auditor determines it necessary to obtain audit evidence If these preconditions are not present, the auditor shall discuss the matter with management. The auditor shall not accept the audit engagement if: The auditor has determined that the financial reporting framework to be applied is not acceptable Management s agreement referred to above has not been obtained. 3.2 The audit engagement letter Key term The engagement letter is the written terms of an engagement in the form of a letter The auditor shall agree the terms of the engagement with management or those charged with governance and these shall be recorded in an audit engagement letter or other suitable form of written agreement. This has to be done before the audit engagement begins so as to avoid misunderstandings regarding the audit Form and content of the audit engagement letter The audit engagement letter shall include the following: The objective and scope of the audit The auditor s responsibilities Management s responsibilities Identification of the applicable financial reporting framework for the preparation of the financial statements Reference to the expected from and content of any reports to be issued by the auditor and a statement that there may be circumstances in which a report may differ from its expected form and content Additional matters that may be included The audit engagement letter may also make reference to the following: 9

10 Elaboration of scope of audit, including reference to legislation, regulations, ISAs, ethical and other pronouncements Form of any other communication of results of the engagement The fact that due to the inherent limitations of an audit and those of internal control, there is an unavoidable risk that some material misstatements may not be detected, even though the audit is properly planned and performed in accordance with ISAs Arrangements regarding planning and performance, including audit team composition Expectation that management will provide written representations Agreement of management to provide draft financial statements and other information in tome to allow auditor to complete the audit in accordance with proposed timetable Agreement of management to inform auditor of facts that may affect the financial statements, of which management may become aware from the date of the auditor s report to the date of issue of the financial statements Fees and billing arrangements Request for management to acknowledge receipt of the letter and agree to the terms outlined in it Involvement of other auditors and experts Involvement of internal auditors and other staff Arrangements to be made with predecessor auditor Any restriction of auditor s liability Reference to any further agreements between auditor and entity Any obligations to provide audit working papers to other parties Appendix 1 of ISA 210 includes an example of an audit engagement letter 3.3 Recurring audits On recurring audits, the auditor shall assess whether the terms of the engagement need to be revised and whether there is a need to remind the entity of the existing terms. The following factors may indicate that it would be appropriate to revise the terms of the engagement or remind the entity of the existing terms. Any indication that the entity misunderstands the objective and scope of the audit 10

11 Any revised or special terms of the audit engagement A recent change of senior management A significant change in ownership A significant change in nature or size of the entity s business A change in legal or regulatory requirements A change in the financial reporting framework A change in other reporting requirements 3.4 Acceptance of a change in terms A change in the terms of audit engagement prior to completion may result from: (a) (b) (c) A change in circumstances affecting the need for the service A misunderstanding as to the nature of an audit or of an audit or of the related service originally requested A restriction on the scope of the audit engagement, whether imposed by management or caused by circumstances The auditor shall not agree to a change in the terms of the audit engagement where there is no reasonable justification for doing so. In the case of (a) and (b) above, these might be acceptable reasons for requesting a change in the engagement. A change may not be considered reasonable, however, if it seems to relate to information that is incorrect, incomplete or otherwise unsatisfactory. An example of this would be if the auditor could not obtain sufficient appropriate audit evidence for receivables and the entity then asks the auditor to change the engagement from an audit to a review so as to avoid a qualification of the auditor s report. If the auditor is asked to change the audit engagement before it is completed, to an engagement providing a lower level of assurance such as a review or a related service, the auditor shall determine whether there is reasonable justification for doing so because there may be legal or contractual implications. If the terms are changed, the auditor and management shall agree and record the new terms in an engagement letter. However, to avoid confusing users, the report on the related service will not include reference to the original audit engagement or any procedures performed in the original audit engagement (unless the engagement is changed to an agreed-upon procedures engagement, where reference to procedures performed is included in the report). However, if the auditor cannot agree to a change of terms and management does not allow the auditor to carry on with the original audit engagement, the auditor shall withdraw from the engagement and determine whether there is an obligation to report this to other parties (e.g. those charged with governance, owners, regulators). 11

12 Emphasis of Matter Paragraph - ISA If the auditor has determined that the financial reporting framework (Accounting Standards) prescribed by law or regulation would be unacceptable but for the fact that it is prescribed by law or regulation, the auditor shall accept the audit engagement only if the following conditions are present: (a) Management agrees to provide additional disclosures in the financial statements required to avoid the financial statements being misleading; and (b) It is recognized in the terms of the audit engagement that: (i) The auditor s report on the financial statements will incorporate an Emphasis of Matter paragraph, drawing users attention to the additional disclosures, in accordance with ISA (UK and Ireland)

13 Example of an Audit Engagement Letter APPENDIX 1 ISA 210 The following is an example of an audit engagement letter for an audit of general purpose financial statements prepared in accordance with International Financial Reporting Standards. This letter is not authoritative but is intended only to be a guide that may be used in conjunction with the considerations outlined in this ISA. It will need to be varied according to individual requirements and circumstances. It is drafted to refer to the audit of financial statements for a single reporting period and would require adaptation if intended or expected to apply to recurring audits (see paragraph 13 of this ISA). It may be appropriate to seek legal advice that any proposed letter is suitable. *** To the appropriate representative of management or those charged with governance of ABC Company:20 [The objective and scope of the audit] You21 have requested that we audit the financial statements of ABC Company, which comprise the balance sheet as at December 31, 20X1, and the income statement, statement of changes in equity and cash flow statement for the year then ended, and a summary of significant accounting policies and other explanatory information. We are pleased to confirm our acceptance and our understanding of this audit engagement by means of this letter. Our audit will be conducted with the objective of our expressing an opinion on the financial statements. [The responsibilities of the auditor] We will conduct our audit in accordance with International Standards on Auditing (ISAs). Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. Because of the inherent limitations of an audit, together with the inherent limitations of internal control, there is an unavoidable risk that some material misstatements may not be detected, even though the audit is properly planned and performed in accordance with ISAs. In making our risk assessments, we consider internal control relevant to the entity s preparation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity s internal control. However, we will communicate to you in writing concerning any 13

14 significant deficiencies in internal control relevant to the audit of the financial statements that we have identified during the audit. [The responsibilities of management and identification of the applicable financial reporting framework (for purposes of this example it is assumed that the auditor has not determined that the law or regulation prescribes those responsibilities in appropriate terms; the descriptions in paragraph 6(b) of this ISA are therefore used).] Our audit will be conducted on the basis that [management and, where appropriate, those charged with governance]22 acknowledge and understand that they have responsibility: (a) For the preparation and fair presentation of the financial statements in accordance with International Financial Reporting Standards;23 (b) For such internal control as [management] determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error; and (c) To provide us with: (i) Access to all information of which [management] is aware that is relevant to the preparation of the financial statements such as records, documentation and other matters; (ii) Additional information that we may request from [management] for the purpose of the audit; and (iii) Unrestricted access to persons within the entity from whom we determine it necessary to obtain audit evidence. As part of our audit process, we will request from [management and, where appropriate, those charged with governance], written confirmation concerning representations made to us in connection with the audit. We look forward to full cooperation from your staff during our audit. [Other relevant information] [Insert other information, such as fee arrangements, billings and other specific terms, as appropriate.] 14

15 [Reporting] [Insert appropriate reference to the expected form and content of the auditor s report.] The form and content of our report may need to be amended in the light of our audit findings. Please sign and return the attached copy of this letter to indicate your acknowledgement of, and agreement with, the arrangements for our audit of the financial statements including our respective responsibilities. XYZ & Co. Acknowledged and agreed on behalf of ABC Company by (signed)... Name and Title Date Memory Aid for 6 matters to be included in an Audit Engagement Letter Fas Err ) F: The basis on which audit fees are computed A: Arrangements regarding the planning and performance of the audit, including the composition of the audit team S: The Scope of the Audit (i.e. what is being audited) E: Expected form and content of any reports to be issued R: Responsibilities of the Auditor R: Responsibilities of those charged with Governance 15

16 Question: Letter of Engagement 16

17 17