How Does the US compare to other geographies? Country / System Real-Time Option Available Slower Alternative? Switzerland SIX 1987 Yes Brazil SITRAF 2

|

|

|

- Rebecca Grant

- 5 years ago

- Views:

Transcription

1 Positioning for Faster Payments Amy K. Morris Sr. Director, ACH Network Rules Catalyst Corporate s Payments Forum 2 Real-Time Payments A Global Trend * Sweden BiR United Kingdom Faster Payments Service Denmark NETS Mexico SPEI United States TBD European Union SEPA Instant Poland Express ELIXIR India IMPS Thailand TBD South Korea HOFINET Japan Zengin Colombia TBD Chile TEF Brazil SITRAF Nigeri a NIP South Africa RTC Singapore Fast and Secure Transfers Australia New Payments Platform *Source: The Clearing House 1

2 How Does the US compare to other geographies? Country / System Real-Time Option Available Slower Alternative? Switzerland SIX 1987 Yes Brazil SITRAF 2002 Yes Mexico SPEI 2004 Yes South Africa RTC 2006 Yes UK Faster Payments 2008 Yes India IMPS 2011 Yes Poland KIR/Express ELIXIR 2011 Yes Source: Celent, a division of Oliver Wyman; Lipis & Lipis research 4 What is Faster? It depends on which step in the process you are referring tof..and the needs of the users Authorization Message / Notification Availability of Funds Bank to Bank Settlement Official movement of dollars 2

3 5 Defining Elements of a Real Time Payment System A real-time payment is an account-to-account credit transfer in which funds are posted to the receiver s account and confirmed to the sending bank within one minute. A realtime payment does not have to settle in real-time. Postingrefers to the point at which funds are posted to the beneficiary s account. Posting can take place in real-time, while settlement takes place at a less rapid rate. Settlement refers to the point at which transactions are settled between banks, either bilaterally or multilaterally, in net or gross amounts. During settlement funds are transferred by banks on accounts held at a commercial or central bank. Data standards define the agreed-to format used to transmit payment messages and/or files between senders and receivers. Data standards can be proprietary or based on recognized coding language. Data standards do not affect the speed of a payment. Remittance data refers to the type and amount of paymentrelated information the data standard carries, that allows the receiver to post a payment or to better understand the payment. 6 3

4 7 Two Approaches Adding transactions with faster funds availability to existing systems, for example, the ACH Both credit and debit payment flows, with existing ability to pass additional information with the payment Developing new systems with faster availability, additional information, improved security, etc. Focus of proposals to the Federal Reserve s Faster Payment Task Force UK Faster Payments, TCH RTP F.there are pros and cons of bothff..plus Hybrid Approaches? 8 Complementary Capabilities End-users have a myriad of payments needs and therefore need a spectrum of payment offerings to meet them: next-day, same-day and immediate payments Different payments systems have different attributes Same-day ACH settlement and real-time payments are complementary, not duplicative initiatives There are discrete use-cases for real-time payments and Same Day ACH Additionally, if real-time payments are built through messaging capabilities, adding multiple same-day ACH windows takes risk out of the system 4

5 9 Same Day ACH and Real-time Payments are two distinct, complementary ways to speed payments SameDay ACH Improved online billpay Hourly payroll and Emergency Payroll Expedited B2C (e.g. insurance payouts) Cash management Faster B2B Accelerated card merchant settlement Real-Time Payments P2P Urgent A2A Immediate billpay with acknowledgment Temporary payroll Emergency B2C (e.g. disaster) Just-in-time B2B Type of Payment Credit or Debit Credit Only Notification to Receiver Same-day (receipt of transaction) Immediate Other Messaging Extensive remittance data can be included with the payment Receiver acknowledgment,request for payment, remittance data, others TBD Payment Finality Reversals and Returns Allowed Irrevocable Receiver Availability Same-day Immediate 10 Real-time Payments SETTING THE STAGE 5

6 11 Real-Time Systems Benefits Depend on Functionality Safe and secure: Do not want account data shared Tokens Routing functionality (directory services) Need strong authentication by FI that has the existing relationship with their customer Transparency: Want to be notified when money has been sent and/or received Want money to be credited or debited from account as quickly as possible to allow end-users to manage their money better Convenient: Need good user interfaces for mobile payments Need to be able to reach all or most end-points (multiple closed loop systems are not convenient) Certainty1.and protection: Want to know the payment is finalfbut want to reverse/claw back in case of misrouted or otherwise faulty paymentsff. So real-time systems often offer more than speed they include additional functionality 12 Benefits are Built or are Required by Rule or Service Agreement In order to receive the promise of a Real-Time system, the functionality and/or business rules need to address any or all of: Posting requirements how fast does the payment need to be made available to the receiver Security requirements robust real-time authentication and any needed screening Notification requirements to sender and receiver Claw back provisions and dispute resolution End user experience to be addressed by system rules or individual FIs using the system? Up-time (24X7? Any exceptions?) Format requirements 6

for implementing safe, ubiquitous, faster")

7 13 Federal Reserve Strategies for Improving the U.S. Payment System - in pursuit of five desired outcomes 1. Actively engage with stakeholders on initiatives designed to improve the U.S. payment system. 2. Identify effective approach(es) for implementing safe, ubiquitous, faster payments. 3. Reduce fraud risk and advance the safety, security and resiliency of the payment system. SECURITY SPEED EFFICIENCY 4. Achieve greater end-to-end efficiency for domestic and cross-border payments. INTERNATIONAL 5. Enhance Federal Reserve Bank payment, settlement and risk management services to address identified gaps. COLLABORATION Mission & Objectives of the Faster Payments Task Force Identify and evaluate approach(es) for implementing a safe, ubiquitous, faster payments capability in the United States Represent1 views on future needs for a safe, ubiquitous faster payments solution Assess1 alternative approach(es) for faster payment capabilities Address1 other issues deemed important to the successful development of effective approaches 14 7

8 15 Federal Reserve s Faster Payment Task Force Approach: Encourage private sector to develop, implement and operate systems with faster funds availability, improved security, more information and improved cross-border access Concludedandissuedfinalreport injuly A Few TakeawaysF. The Faster Payments Task Force calls upon all stakeholders to seize this historic opportunity to realize the vision for a payment system in the United States that is faster, ubiquitous, broadly inclusive, safe, highly secure, and efficient by Achieving the vision will be enabled by ubiquitous receipt where all payment service providers are capable of receiving faster payments and making those funds available to customers in real time. Specifically, the task force has influenced product strategies and developments in the broader marketplace by defining Effectiveness Criteria, showcasing faster payments capabilities, and driving a process for bringing faster payments solutions forward for task force feedback. To maintain this momentum, the task force recommends ongoing collaboration to develop a faster payments system in the United States that fulfills its vision, with work beginning in three key areas: Governance and Regulation, Infrastructure and Sustainability and Evolution. 8

9 Faster Payments Task Force Effectiveness Criteria Ubiquity U.1 Accessibility U.2 Usability U.3 Predictability U.4 Contextual Data Capability U.5 Cross-Border Functionality U.6 Applicability to Multiple Use Cases Speed (Fast) F.1 Fast approval F.2 Fast clearing F.3 Fast availability of funds to payee F.4 Fast settlement among depository institutions and non-bank account providers F.5 Prompt visibility of payment status Efficiency E.1 Enables Competition E.2 Capability to enable value added services E.3 Implementation Timeline E.4 Payment Format Standards E.5 Comprehensiveness E.6 Scalability and Adaptability E.7 Exceptions and Investigations Process Governance G.1 Effective governance G.2 Inclusive governance Safety and Security S.1 Risk management S.2 Payer authorization S.3 Payment finality S.4 Settlement approach S.5 Handling disputed payments S.6 Fraud information sharing S.7 Security controls S.8 Resiliency S.9 End-user data protection S.10 End-user/provider authentication S.11 Participation requirements Legal L.1 Legal framework L.4 Data privacy L.2 Payment system rules L.5 Intellectual privacy L.3 Consumer Protections Governance and Regulation Establishing a formal governance framework; Establishing rules, standards, and a baseline set of requirements for the faster payments system that would enable payments to cross solutions securely and reliably, and ensure end users have predictability and transparency in certain key features pertaining to timing, fees, error resolution and liability; and Evaluating laws and regulations affecting payments and payment service providers to ensure that they are suited to the unique characteristics of realtime payments. 9

10 19 Faster Payments Council August 17, The Governance Framework Formation Team (GFFT) recently concluded a 60-day stakeholder comment period seeking broad industry feedback on the draft Operating Vision of the proposed U.S. Faster Payments Council (FPC) The goal is a ubiquitous, world-class payment system in 2020 where Americans can safely and securely pay anyone, anywhere, at any time and with immediate funds availability. The FPC will help: Drive the emerging faster payments infrastructure toward interoperability; Foster a high-quality user experience for all; and Enable stakeholders to expand their reach and leverage their investments across a broader base of transactions Faster Payments Council Guiding principles are at the core of how the FPC operates Openness and inclusiveness: All members have a voice through equitable Board representation and open opportunities to serve on committees and work groups. Flexibility and responsiveness: The FPC has a flexible structure that can evolve with changing needs, and its processes for establishing policies, guidelines, standards, and/or rules, when deemed necessary, are designed to allow flexibility in implementation. Fairness and transparency: The FPC respects the competitive prerogatives of its member organizations, and strives for equal treatment and consensus in all decisions that have a significant impact on any individual organizations and stakeholder groups. It also provides safeguards for members to share information and collaborate on issues of common interest. 10

the Federal Reserve might need to play to support ubiquity, competition, and equitable access to faster")

11 21 Faster Payments Council 22 Infrastructure Developing a design for faster payments solutions to interoperate via directory services; Requesting the Federal Reserve develop a 24x7x365 settlement service; and Requesting the Federal Reserve explore and assess other operational role(s) the Federal Reserve might need to play to support ubiquity, competition, and equitable access to faster payments. 11

12 23 Sustainability and Evolution Developing methods for fraud detection, reporting, and information sharing to continuously advance the safety and security of the faster payments system; Creating advocacy and education programs to support broad adoption; Researching cross-border payments to identify and address gaps and barriers to enabling faster payments for this use case; and Continuing research on emerging technologies to deepen understanding of the risks they may pose as well as the benefits they may offer, including the potential for serving underserved end users and use cases. 24 Call to Action Whether you are an end user or a financial services innovator, and whether you have participated in the effort to date or not, we are calling on all of you to come together to make this faster payments vision a reality. We ask you to support this effort by: Embracing and promoting the vision and the Effectiveness Criteria; Actively participating in the ongoing dialogue; Contributing to work group efforts and deliverables; and Taking steps to make your own organization faster payments ready by To join in the next phase of this ground-breaking work, visit FasterPaymentsTaskForce.org. 12

13 25 Real-time Payments OPTIONS 26 13

14 27 Considerations

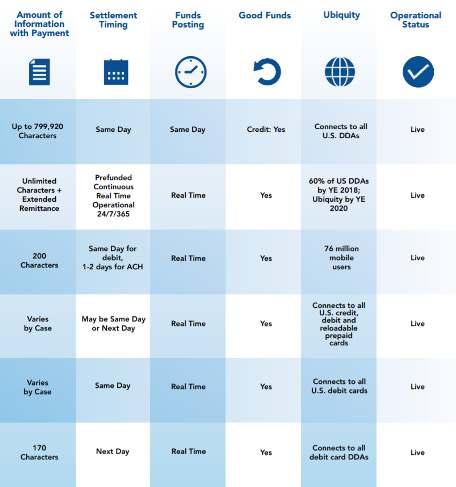

15 29 Real Time Payments by The Clearing House Source: The Clearing House 30 RTP Distinctive Features 15

16 Source: The Clearing House Source: The Clearing House 16

17

18 35 Moving the Money Source: American Bankers Association 36 Faster Payments SAME DAY ACH 18

19 The ACH Network is Thriving On pace to add more than 1 billion transactions for the fourth consecutive year Annual ACH Network Transaction Volume (billions) is estimated based on volume through the 2 nd quarter ACH NETWORK VOLUME BREAKDOWN B2B DIRECT DEPOSIT SAME DAY +5.6% +5.8% +478% 3.3 BILLION INTERNET +13.1% 6.5 BILLION P2P +23.3% 75 MILLION 5.2 BILLION 97 MILLION 19

20 39 Why Same Day ACH? Responding to Market Needs Same Day ACH creates an option to support the needs of your credit union members Same Day ACH payments (credits and debits) can currently be made to every financial institution in the country Same Day ACH Implementation of the Original Rule is Complete The current implementation of Same Day ACH through Phase 3 has resulted in: Two daily Same Day ACH processing windows morning and early afternoon which reach all financial institutions and all accounts Eligibility of most ACH credits and debits for Same Day ACH processing International ACH and transactions over $25,000 are ineligible (approx. 2% of current ACH transaction volume) Ubiquitous funds availability requirement for Same Day ACH credits by 5:00 p.m. RDFI local time Eligibility of all returns for Same Day ACH processing 20

21 41 Same Day ACH Is Also Thriving Transaction Volume (millions) Debits Credits Q17 2Q17 3Q17 4Q17 1Q18 2Q18 42 Expanding Same Day ACH Recently, three new rules were passed to support faster processing and expand Same Day ACH by: 1. Providing faster funds availability for many ACH credits, both Same Day credits and non- Same Day credits 2. Increasing the Same Day ACH dollar limit to $100,000 per transaction 3. Creating a third Same Day ACH processing window that expands access to Same Day ACH for all financial institutions and their customers through later service hours 21

22 43 Expanding Same Day ACH Effective Dates Provide Faster Funds Availability September 20, 2019 Increase the Same Day ACH Dollar Limit March 20, 2020 Expand Access to Same Day ACH with a New Processing Window September 18, 2020 The effective date of the new SDA window is contingent upon receiving timely approval by the Federal Reserve Board of Governors of changes to Federal Reserve services necessary to support it NACHA has been in dialogue with the Board of Governors for more than a year regarding these proposals, and has explicitly asked for the Fed s support The Federal Reserve process likely includes a public comment period on changes to the National Settlement Service for interbank settlement and to the Fedwire Funds Service If approval is received by June 30, 2019, then the effective date of the new SDA window would remain as balloted September 18, 2020 If approval is received between July 1 and December 31, 2019, then the effective date would be extended by 6 months to March 19, Expanding Same Day ACH Functionality Transaction Eligibility (IAT and ENR not eligible) Same Day ACH Processing Deadlines Estimated Settlement Time(s) ACH Credit Funds Availability Faster Funds Availability September 20, 2019 Credits and debits of $25,000 or less 10:30 am ET and 2:45 pm ET 1:00 pm ET and 5:00 pm ET 1:30 pm and 5:00 pm RDFI local time for Same Day credits Increased Dollar Limit March 20, 2020 Credits and debits of $100,000 or less 10:30 am ET and 2:45 pm ET 1:00 p.m. ET and 5:00 pm ET 1:30 pm and 5:00 pm RDFI local time Third Same Day ACH Window September 18, 2020 Credits and debits of $100,000 or less 10:30 am ET and 2:45 pm ET and 4:45 pm ET 1:00 p.m. ET and 5:00 pm ET and 6:00 pm ET 1:30 pm and 5:00 pm RDFI local time and RDFI end of processing day 22

23 45 Providing Faster Funds Availability The rule provides faster funds availability for many ACH credits Funds from Same Day ACH credits processed in the existing, first processing window will be made available by 1:30 p.m. RDFI local time Funds from non-same Day ACH credits will be available by 9:00 a.m. RDFI local time on the settlement day, if the RDFI had them by 5:00 p.m. on the previous day (i.e., apply the existing PPD rule to all ACH credits) Effective date September 20, Providing Faster Funds Availability - Overview This chart show funds availability times for ACH credits, by RDFI receipt time Processing Window/ Schedule First SDA window Second SDA window New, third SDA window RDFI receipt time Current funds availability requirement 1 12:00 noon ET 5:00 p.m. local time 4:00 p.m. ET 5:00 p.m. local time 5:30 p.m. ET N/A Proposed funds availability requirement 1 1:30 p.m. RDFI local time 5:00 p.m. RDFI local time End ofrdfi s processing day 2 Non-SDA credits If received prior to 5:00 p.m. local time - Openingof business for PPD - End of settlement date for non-ppd 9:00 a.m.rdfi local time for all SEC Codes 1 -RDFIs in the Atlantic Time Zone may use Eastern Time as local time for the 1:30 p.m. and 5:00 p.m. requirements 2 -End-of-processing day would be the same standard as with Same Day ACH s original Phases 1 and 2 23

24 47 Increasing the Dollar Limit to $100,000 The rule increases the per-transaction dollar limit for Same Day ACH transactions from $25,000 to $100,000 Both Same Day ACH credits and Same Day ACH debits will be eligible for same day processing up to $100,000 per transaction There are a number of use-cases for which a higher dollar limit would enable ACH end-users to make greater use of Same Day ACH. Effective date of March 20, 2020 By the time this change is effective, the industry will have been processing Same Day ACH credits for 3.5 years and Same Day ACH debits for 2.5 years This should be sufficient experience to enable processing at higher dollar limits 48 Increasing the Dollar Limit Use Cases There are a number of use cases for which end users could make greater use of Same Day ACH credits and debits with a higher per-transaction dollar limit: B2B payments -Approximately 89 percent of B2B payments currently are eligible for SDA. Increasing the limit to $100,000 encompasses an additional 8% of B2B payments, including both credits and debits (based on 2017 volume, this translates into more than 250 million additional B2B payments becoming eligible for SDA) Payroll deposits and funding Payroll processors commonly use an ACH debit to collect funds for a payroll. Even though individual SDA payroll credits are for less than $25,000 each, the single funding debit is for more than $25,000. In other cases, payroll deposits are for more than $25,000, and payroll managers and processors don t want to sort transactions Insurance claims and disaster assistance payments can often be for more than $25,000, and are typically time sensitive for the recipient Tax payments From business to government agencies Merchant funding for payment card transactions - Many merchants receive funds from payment card transactions via ACH credits, and these settlement transactions are often more than $25,000 Account-to-account transfers can often be for more than $25,000. These can be credits or debits Reversals A greater percentage of forward transactions could be reversed using same day processing 24

25 49 Expanding Access to Same Day ACH This rule creates a new Same Day ACH processing window that wil enable ODFIs and their customers to originate SDA transactions for an additional 2 hours each banking day The new window allows Same Day ACH files to be submitted to the ACH Operators until 4:45 p.m. ET (1:45 p.m. PT), providing greater access for all ODFIs and their customers The timing of this new processing window balances expanding access to Same Day ACH with the desire to minimize impacts on financial institutions end-of-day operations and the re-opening of the next banking day 50 Expanding Access to Same Day ACH The Rule The ACH Operators will establish a third, daily Same Day ACH processing and settlement window * ODFIs will be able to submit files of SDA transactions until 4:45 p.m. ET / 1:45 p.m. PT This timing provides ODFIs operating in Pacific Time with a file submission schedule into the early afternoon RDFIs will receive files of SDA transactions by 5:30 p.m. ET / 2:30 p.m. PT Interbank settlement will occur at 6:00 p.m. ET / 3:00 p.m. PT An RDFI must make funds available for SDA credits in this new SDA processing window no later than the end of its processing day This uses the same end-of-day requirement as did Phases 1 and 2 An RDFI could decide to make funds available sooner than the deadline (i.e., an RDFI in Pacific Time could make funds available at 5:00 p.m. Pacific Time) All credits and debits, and all returns, will be eligible for same day processing in the new window; except international ACH transactions (IATs), automated enrollments (ENRs), and forward transactions over the per-transaction dollar limit * The specific ACH Operator processing schedules are not determined by the NACHA Operating Rules, but for this deck are believed to be accurate with respect to ACH Operator intentions. 25

26 51 Expanding Access to Same Day ACH This chart shows the current next-day ACH and same-day ACH schedules, along with the new Same Day ACH schedule *, creating a total of four daily settlements (all times shown in Eastern Time) 3:00 AM 4:00 AM 5:00 AM 6:00 AM 7:00 AM 8:00 AM 9:00 AM 10:00 AM 11:00 AM 12:00 noon 1:00 PM 2:00 PM 3:00 PM Next Day ACH 3:00 AM - ACH Opens 2:15 AM - ODFI Deadline for 6:00 AM - RDFI receipt files of Next-Day ACH Next-Day Transactions 8:30 AM - Settlement for Next Day Transactions 1 4:00 PM 5:00 PM 6:00 PM 7:00 PM 8:00 PM 9:00 PM 10:00 PM 11:00 PM 12:00 midnight 1:00 AM 2:00 AM Same Day ACH 10:30 AM - ODFI Deadline for Same Day Window First window 12:00 Noon - RDFI Receipt Files for Same Day Window 2 1:00 pm - Settlement for Same-Day Transactions Same Day ACH Second window 3 2:45 PM - ODFI Deadline for Same Day Window 4:00 PM - RDFI Receipt Files for Same Day Window 5:00 PM - Settlement for Same-Day Transactions Same Day ACH 4:45 PM - ODFI Deadline for Same Day Window New, third window 5:30 PM - RDFI Receipt Files for Same Day Window 4 Estimated 6:00 PM - Settlement for Same-Day Transactions All times Eastern Time * The specific ACH Operator processing schedules are not determined by the NACHA Operating Rules, but for this deck are believed to be accurate with respect to ACH Operator intentions. 52 Expanding Access to Same Day ACH Schedule at a Glance. Service Current time Expanded Schedule 1 New SDA processing window - ODFI input deadline to ACH Operator N/A 4:45 p.m. ET 1:45 p.m. PT ACH Operator provides output files to RDFIs N/A 5:30 p.m. ET 2:30 p.m. PT Interbank settlement for new SDA window N/A 6:00 p.m. ET 3:00 p.m. PT Federal Reserve National Settlement Service closes 2 Fedwire closes for Settlement Payment Orders Fedwire re-opens for the next banking day 5:30 p.m. ET 2:30 p.m. PT 6:30 p.m. ET 3:30 p.m. PT 9:00 p.m. ET 6:00 p.m. PT 6:30 p.m. ET 3:30 p.m. PT 7:00 p.m. ET 4:00 p.m. PT 9:00 p.m. ET 6:00 p.m. PT 1 -The specific ACH Operator processing schedules are not determined by the NACHA Operating Rules, but for this deck are believed to be accurate with respect to ACH Operator intentions. 2 -The change in the closing time of NSS would be the formal ask by NACHA of the Fed in order to support Rule change for SDA 26

27 53 Expanding Same Day ACH A Few More Things Same Day Entry Fee The existing fee of 5.2 cents per Same Day ACH transaction will apply to forward Same Day ACH transactions in the third processing window, but will not apply to returns or NOCs processed in this window. Eligibility for Same Day ACH Processing This Rule does not change the eligibility of transactions for Same Day ACH processing. IATs and ENRs remain ineligible for Same Day ACH The change to the per-transaction dollar limit is covered by the new Rule Increasing the Same Day ACH Dollar Limit which becomes effective March 20, 2020 (6 months before the new third window implements) Identification of Same Day ACH transactions Same Day ACH transactions in this third Same Day ACH processing window will be identified in the same way as with the existing windows by including a today s date in the Effective Entry Date field, and submitting the transaction timely to the ACH Operator. ODFIs and Originators optionally may use the convention SD1800 in the Company Descriptive Date field for transactions in this new Same Day ACH window As with current Same Day ACH processing, ACH Operators will process stale or invalid Effective Entry Dates in the next available processing window, which could be this new Same Day ACH window 54 Expanding Access to Same Day ACH Returns For ACH transactions that need to be returned, faster processing of the return is typically a win-win for all parties ODFIs and Originators learn about problems sooner RDFIs get exceptions processed and settled faster This rule will allow for faster processing of returns, regardless of whether the forward transaction is a same-day transaction or not Returns that are settled on a same-day basis are not subject to the Same Day Entry Fee Not subject to the eligibility limit on forward transactions (i.e., dollar limit per transaction; IAT) An RDFI is not required to process returns on the same day an Entry is received, regardless of whether the Entry is a Same Day Entry For example, if an RDFI receives a Same Day ACH debit on April 28 that is NSF, it is not required to send the return on April 28 The RDFI is required to send the return so that it is available to the ODFI by the opening of business on April 30 (opening of business 2 Banking Days after the original April 28 Settlement Date) 27

28 55 Expanding Access to Same Day ACH Returns All returns (and Notifications of Change) will be eligible for processing through the third SDA processing window The existing returns-only window provided by the ACH Operators will be absorbed into the new Same Day ACH processing window Enables RDFIs to send returns later into the day, up to 4:45 p.m. ET / 1:45 p.m. PT Greater ability for RDFIs to make use of SDA processing for returns, which would get settled 14.5 hours earlier than next-day returns Returns processing Existing returns only window Returns in new SDA window RDFI submission deadline 4:00p.m. ET 1:00 p.m. PT 4:45p.m. ET 1:45 p.m.et Settlement 1 5:00/5:30 p.m. ET 2:00/2:30 p.m. PT 6:00 p.m. ET 3:00p.m. PT 1 Settlement timing for the existing returns-only window varies by ACH Operator 56 Making Same Day Corporate Payments Uses include: Emergency payments, off-cycle disbursements and corrections or payouts, time critical/due-date payments, account transfers, errors/payment re-initiation, etc. Benefits Treasury: improved working capital/cash flow management/hurdle rate Operations: reduced cost for expedited payments; improved invoice processing/payment cycle time; faster supplier cash application with inclusion of remittance; quicker acquisition of supplies/services Customer Service: predictable timing for disbursements/payouts (e.g. insurance, employee); saves costs for payment receiver Low cost, ubiquitous option to expedite payments; only option for including rich remittance; and can reach any bank account in the U.S. ACH Wire Card Check Expedited option X Pay today! Remittance Unlimited structured Limited unstructured Limitedstructured Unlimited unstructured Reach All DDAs All DDAs Card acceptors All postal addresses Cost Low High Low Low 28

29 57 Receiving Same Day Corporate Payments Uses include: Expedited credit ACH receipt, debit ACH collection and error correction Benefits Treasury: improved working capital/cash flow management/hurdle rate for customer payments/cash concentration; move collections forward one day without changing customer behavior Operations: Low receipt and collection cost/payment compared to other expedited options; improvement to days sales outstanding (DSO) reduction, average days delinquent (ADD), collection effectiveness index (CEI); better cash application cycle time when remittance included; reduced risk for collections quicker cycle for account verification/returns; positive impact to logistics cycle/disbursements of goods/services, improved product throughput with faster availability of good funds Customer Service: accommodate low cost critical/late payments from customers; quicker release of goods/services including for credit hold customers; meets consumer expectations for bank account management/transparency 58 Case Studies 29

30 THANK YOU! 30