Trading Carbon Assets. Asia Carbon Exchange Pte Ltd A member of Asia Carbon Global

|

|

|

- Owen McLaughlin

- 5 years ago

- Views:

Transcription

1 Asia Trading Carbon Assets Asia Carbon Exchange Pte Ltd A member of Asia Carbon Global

2 Basics of Emissions Trading What options are most cost-effective? Company A can reduce 1000 tons CO 2e at $2/ton = $2000 Company B can reduce 1000 tons CO 2e at $6/ton = $6000 SELL BUY 1000 tons CO 2e at $4/ton = $4000 Company A - Seller $2000 Profit $2000 Savings Company B - Buyer Asia Carbon Global

3 Carbon Market : Demand Market Area Japan 800,000,000 Carbon Credit Shortage (in tons CO 2 ) - ( ) However, fungibility of CERs will be limited by EU-LD, expressed in % of EU allowances, and differentiated in each EU country Canada 1,350,000,000 Europe 1,600,000,000 Total Short 3,750,000,000 Source: Natsource & ACX Source: EU Comparison of proposed vs. approved caps for 2008 to 2012 Asia Carbon 2008

4 Carbon Market : Supply Market Up to 2012 (Million tons CO 2 ) Up to 2020 (Million tons CO 2 ) CDM 2,744 6,527 JI ( ) Source :UNEP Risø Centre Sept 2008 Asia Carbon 2008

5 CDM Update : UNFCCC

6 CDM Update : UNFCCC

7 Source :UNEP Risø Centre May 2008

8 Source :UNEP Risø Centre May 2008

9 Trade Figures

10 Primary CDM/JI Buyers

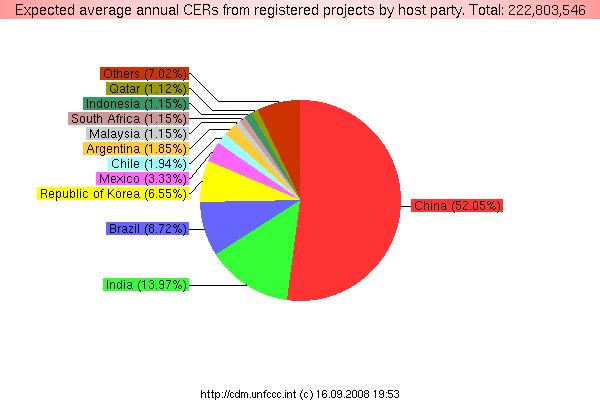

11 Asia and CDM Giants India China 1046 projects 1377 projects 417 Mn CERs (15% of global carbon market & ~19% of Asia) 1464 Mn CERs (53% of Global carbon market & 67% of Asia ) 76 Mn CERs per year (annual avg.) 294 Mn CERs per year (annual avg.) Banking CERs Flexible pricing Bilateral CERs China DNA floor price Renewable Energy dominated HFC/ Landfill (CH 4 )/ Chemicals (N 2 O) No tax on CERs Sliding scale tax on CERs (2-65%) Global 2744 Mn CERs Malaysia, Indonesia and Vietnam emerging significantly in Palm, Cement, Geothermal and Hydro sectors Source :UNEP Risø Centre Sept 2008

12 Rest of Asia: Source of CERs Malaysia promoting only bilateral CDM projects (sectors : Palm and landfill) Indonesia emerging strong : Palm, Sago, Hydro, Geothermal, Biodiesel & Landfill Thailand :Sago, Biomass and landfill. Researched on trading unilateral CERs Vietnam : Hydro dominant and efficient DNA. Complexity in finalizing the country baseline scenario and Additionality Laos & Cambodia : Hydro dominant (one EE project registered : brewery!) Myanmar : recently notified DNA! Keen to develop landfill, forestry and hydro projects Asia Carbon involved

13 Carbon Trading: Unilateralism Source :ACX - August 2008

14 Transactions OTC (Over the counter) Transactions The majority of volume of carbon trading still executed OTC EUA trading well established; structured products CERs are transacted throughout the origination cycle pcers (primary forwards): OTC broker, Auction Secondary forwards(guaranteed): OTC brokers, Banks, Exchange Spot : OTC brokers, Banks, Exchange, Auction Derivatives: Listed futures; OTC

15 Trading and Exchanges : Fundamentals Making CERs a fungible commodity Price Discovery Transparency Distribution Network Competitive Transaction Costs Standardized Documentation Vintage based trading Level playing field Low procurement costs Product development Robust platform; Building trustworthy relationships

16 Regional Exchanges

17 Price Basis of the CER Percentage of the average weighted price of EUAs traded during a predetermined period in the future. Percentage of EU Compliance Penalty Targets during each compliance period & Average current price offered on 1 on 1 ERPA negotiations Average price of CERs offered by national governmental programs globally. Average price of CERs offered by Carbon Funds China CERs Floor Price ( 9 / CER)

18 Key Price Determinants CDM Risks Host country approval Validation Registration ER vintage: pre or post 2012 Transaction cost Liability for underperformance 6-22 Euros per CER Other determinants Creditworthiness of project sponsor Viability of underlying project Physical status of project Additional environment and social benefits Asia Carbon 2007

19 CERs : Risk Vs Price Source: EcoSecurities CER Price increases Only a PIN (or less) available Project developing new methodology No Host government approval Poor Credit or No Credit Project not registered Flexible CER delivery schedule No punitive damages Unilateral Advance payment Payment upon CER issuance into pending account Source: Natsource Approved methodology Host government approval Strong project partners, technology supplier, EPC, Operator, etc. Good Credit Ability for buyer to become a Project Participant Project is registered Guaranteed delivery schedule with punitive damages for non-delivery Payment on delivery into buyer s national registry account

20 CDM cycle : Risk allocation PI N PD D DNA approv al Validati on Registrat ion PIN Monitorin g Verificati on Issua nce Medium-risk forwards Low-risk forwards Registered projects Issued CERs Source : GTZ CDM newsletter Asia Carbon 2008

21 CER Price Trend

22 CER Dec 08 Future

23 EUA Dec 08 Future

.")

24 EUA-CER spread : a few points EUAs-pCERs spread range : 28% - 72% (average of 51%) since Supply /Demand. EUA 225mt shortfall per year through phase2 ( ). Enough CERS Spot spread now narrowing for 2008; Post-2012 still the major risk; also national linkage(usa ). Compliance period starts 2008 Spread is increasing for Medium Risk (early cycle) forwards [before & during Validation] and Low Risk forwards [Registered] due to rising EUAs price CERs represent good value for EU compliance buyers. ( but imports are limited ) Asia Carbon Global 2008

25 EUA/CER DEC08 Spread

26 CER Prices

27 ACG An Overview Group s activities conceptualized, researched and developed since 2001 Founded : Feb two years ahead of Kyoto coming into force One stop shop services : Carbon Advisory through Carbon Trading Presently operating 17 entities in 9 countries Presence in The Netherlands (Annex I) : to aggregate Buyers Asian presence in Singapore (Non Annex I) to develop unilateral CDM projects and also Aggregate Sellers of CERs Strategic Alliance Japan, China, Korea, Bangladesh & Pakistan Centers of Excellence in Singapore, Vietnam, India, Indonesia Advance stage of development for a Centre of Excellence in China Current portfolio includes over 130 projects with 35 Mn CERs potential New services : VERs Trading & Registry & Projects monitoring Asia Carbon 2008

28 Group s Unique Business Model Vertically Integrated to provide a one stop solution in carbon advisory, carbon finance and carbon asset management One stop solution In Carbon advisory Carbon Finance & Carbon Asset management Carbon Asset Management Carbon Finance & Project Finance Vertically Integrated Business Model ACXChange AC-ADF Carbon Advisory AC CE

29 ACX-Change First on line exchange in the world to Provide a common platform for Sellers and Buyers of Carbon Assets Outside of EU Allowances Web based online trading platform (spot and auction modules) Trading of multiple products (CERs, VERs, EUAs, ERUs, AAUs etc.,) Built in registry and trading facilities Soft launch Carbon Expo - May 2005, Cologne, Germany. Fully operational since November 2005 Carried out several online auctions 4.7 Mn CERs 30 Mn 150,000 VERs 3.76 Mn Improvised and new look & feel platform May 2006, Cologne, Germany Launched VERs trading module May 2007 Cologne, Germany

30 Asia Carbon s Achievements and Awards Golden Peacock Eco-Innovation Award 2007 Energy Business Asia Awards 2007 Revision in methodology for India project New Consolidated Methodology approved by UNFCCC for a Singapore-Indonesia Project

31 The supreme reality of our time is the vulnerability of our planet. John F. Kennedy Thank you Immanuel Edward. J. A Asia Carbon Exchange Pte Ltd 140, Cecil Street, #15-00A Singapore Ph: Fax: eddie@asiacarbon.com