EMV and Apple Pay. The world of credit cards is on the move.

|

|

|

- Amie Matthews

- 5 years ago

- Views:

Transcription

1 EMV and Apple Pay The world of credit cards is on the move.

2 Today we will talk about The basics of EMV and Apple Pay. There are a lot of details we could get lost in. This is a high-level overview. We ll break between topics so you can share your thoughts on them.

3 EMV Europay, Mastercard, and VISA Provides increased security via a special chip on the card. Addresses fraud for card-present transactions. EMV cards make payment in one of two ways: contactless, contact Cards can be either/or, or both. POS terminals must support EMV for it to work

4 Resistance is futile/useless Eventually all cards will go to EMV There s a liability shift in October 2015 If you don t have EMV cards by October 2015, and the merchants do, the liability for fraud is with you. If you do, and merchants do, the liability is with you. The only time you re not liable is if you have EMV cards, and the merchants don t.

5 Who is liable for fraud after October? Merchant has EMV POS terminals Merchant doesn t have EMV POS terminals You don t have EMV cards You You You have EMV cards You Merchant

6 So why worry about it? It s going there. All cards will probably be there eventually. If you are not on EMV, and most others are, it s very possible that fraud would have happened on other cards will shift to your cards. That is, you may be targeted more because your cards are not as secure.

7 Roll-out timeframes Probably 9-12 months Could be longer now if there is a line If you haven t already started, you re probably too late to hit the liability shift deadline, but again, that may not be too critical

8 Considerations for EMV Contact vs. contactless vs. dual-interface cards Payment applications (software on the chip that runs authentication) Cardholder verification methods (signature, none, online/offline PIN) Timing (when to do it) Reissuing cycles

9 Processing considerations Authorization systems Changes to rules logic for authorizations and fraud scoring Card files for personalization managers Online card authentication Systems that manager cardholder information EMV data preparation and key management Reporting services Changes to issuer s card management system Changes to authorization and clearing systems Updated reporting

10 Card fulfillment considerations A chip with one or more payment applications must be embedded into the card. Cards must still have mag stripe. Chip type: dual interface or contact-only Chip operating system Chip memory size

11 Back office support considerations Customer service Fraud management: fraud may shift to non-emv transactions Dispute resolution processes Customer and employee education

12 Card re-issuance All at once: quite expensive; may be better for smaller portfolios; may place burden on customer service channels because of a lot of questions from members at once Replace cards on normal replacement cycle Hybrid: re-issue some off-cycle (high spenders, affluent cardholders, frequent travelers), and the rest on-cycle

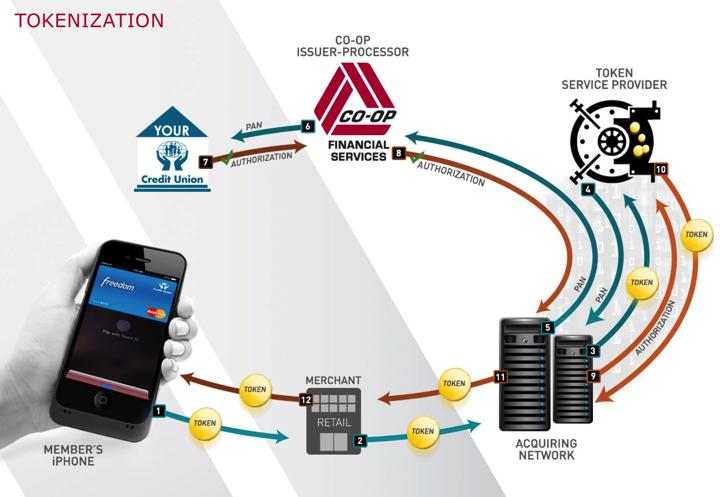

13 You have lots of options More complex cards will cost more Your processor and other vendors will actually do a lot of the work, and will help you through the process. If you process in-house, you ll be doing a lot of the work I am unsure if there are core system considerations. Anyone out there know the answer to that question?

14

15

16 Great resources from CSCU

17 Discuss your thoughts on: Have you started the process already? How has the experience been? How much is/will this costing you? How are/will you issuing the cards? Are you in favor of spending the extra for contactless?

18 Apple Pay A means whereby consumers use their phones to pay at POS terminals. Already the most prevalent mobile payment solution. Introduced in September. Utilizes a little something called tokenization

19

20 Tokenization Merchants never see credit card numbers. In Apple Pay, tokens are phone-specific. Compromised tokens don t mean card reissuance. The token is simply deactivated. VISA provides you with a portal where you manage tokens.

21 Issuing tokens Cardholder requests token with Apple Apple sends the request to VISA, which checks it against a BIN range, and sends the token back to Apple If something doesn t pass inspection, the member is in yellow path authentication They must contact the issuer to clear up the problem This yellow path has been a source of fraud

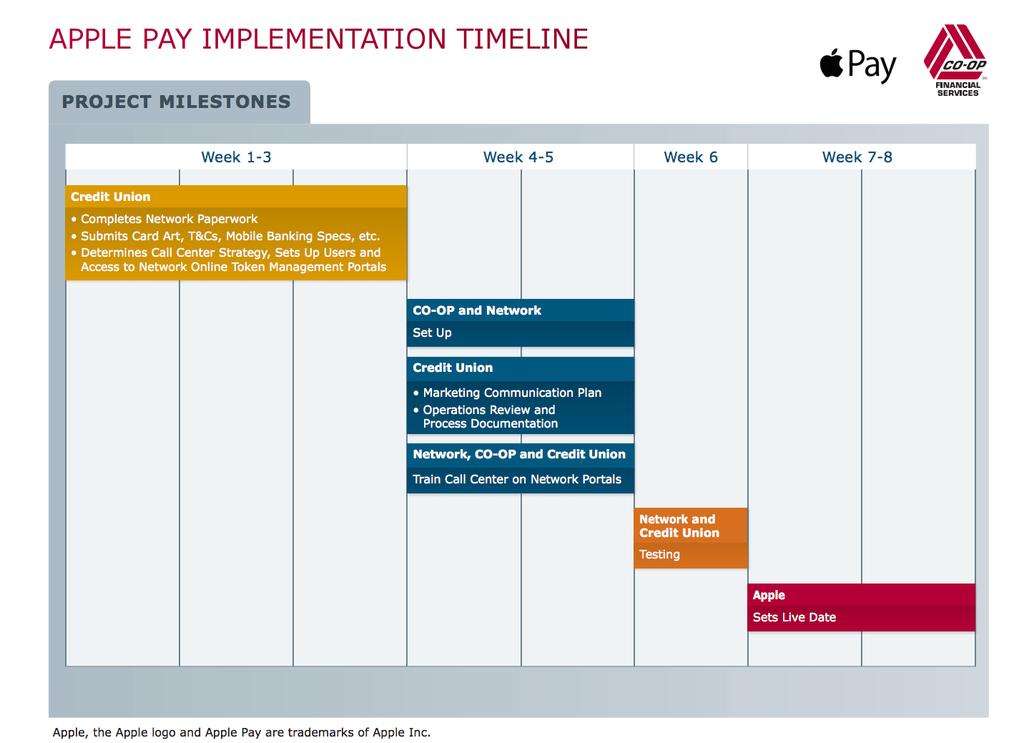

22 How to enroll Talk with your issuer processor Currently requires a 3-year contract 95% of your cards must be eligible for Apple Pay 8-10 week implementation timeframe

23 Process to implement Verify processor readiness Define Terms and Conditions text Sign Apple agreement Network setup (a few weeks) Agree to Visa/MasterCard/network fees Apple setup (a few weeks) Agree to processor fees Call center setup Open implementation project with Customer notification process setup processor Apple Pay validation, go/no-go Define parameters for setup (testing) Gather card art and logo images Launch to members

24

25 Cost Setup costs with Apple, VISA, and your processor Core system shouldn t need updating Apple charges 15 basis points on credit Apple charges $0.005 on debit Supposedly, Apple Pay will reduce card-not-present fraud

26 To get the ball rolling... Talk with your processor Good resources here: