Positioning For Growth While Weathering The Storm. Investor Relations Presentation 2009

|

|

|

- Rosalind Jordan

- 5 years ago

- Views:

Transcription

1 Positioning For Growth While Weathering The Storm Investor Relations Presentation 2009

2 Forward-looking Statement Today s presentation may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of These forward-looking statements include statements as to expectations, beliefs and future financial performance, such as statements relating to the Company s business prospects, future sales, market growth, gross margin and other statements that are not of historical fact. Investors are cautioned that all forward-looking statements are based on management s current expectations and include known and unknown risks, uncertainties and other factors, many of which the Company is unable to predict or control, that may cause the Company s actual results or performance to materially differ from any future results or performance expressed or implied. These risks and uncertainties include the timing and development of the Company s products and services and market acceptance of the Company s new and revised product offerings, and other risk factors disclosed by the Company from time to time in its filings with the SEC, including in its Annual Report on Form 10-K for the year ended December 31, 2008.

2008 Rev.")

3 An Overview of ION Business: Advanced geophysical hardware, software, imaging services, and data libraries across the seismic workflow Mission: To solve the most challenging geophysical imaging problems with highly productive systems and services. Customers: E&P firms and seismic contractors Operations: 1,400 professionals operating from 20 offices worldwide Financials: (NYSE) 2008 Rev. $680 million 2008 adjusted EBITDA $156 million 2009 Guidance Rev. $620-$680 million EPS 0-16 cents, EBITDA $ million Estimated 2009 Debt. Service $ 50 million [ 3 ]

4 ION Served Market Approximately $3.8 Billion 2008 Land Systems Marine Systems Data Processing ION Competition 2D Regional Multi-client Programs Marine systems does not include permanent OBC [ 4 ]

5 Revenues and Business Mix Since the Inception of Our New Strategy in Consolidated Revenues ($ Millions) CAGR = 35% Mix of Business by Segment (Percentage of 2008 Revenues) 100% = $680 million $259M (39%) ION Solutions $37M (5%) CSL $200M (29%) Land Imaging Systems $183M (27%) Marine Imaging Systems [ 5 ]

6 Blue-Chip Customer Base Top Customers 2008 Revenue by Customer Global Contractor 7.6% Global Contractor 7.2% Global Contractor 5.4% Global Contractor 5.1% Global Contractor 4.3% Independent Oil Co. 3.6% Global Contractor 3.3% National Oil Company 3.1% National Oil Company 2.8% Regional Contractor 2.8% International Oil Company 2.7% Regional Contractor 2.5 All Others 45.4% [ 6 ]

7 Business Increasingly International Location of Discoveries > 100 MMBOE Discoveries mmboe mmboe mmboe 1000 UP mmboe Source: CERA. [ 7 ]

8 2009 Plan Assumptions and Short Term Strategy Assumptions Oil prices in the $40/ bbl range during 2009-Expect Rebound in the $50-$ 60/bbl range in Underlying fundamentals have not changed, i.e. long term supply problem. Financial crisis will likely aggravate the problem. Very weak North America and Russian land markets Larger well capitalized IOC s and NOC s likely to maintain longer term exploration programs. Strategy Manage more for cash than earnings (e.g. conservative on financing deals, cost control via 13% headcount reduction, salary freeze, etc.) Preserve longer term strategic initiatives with R&D spending reduced by 10% but still at 7% of revenues at $45 million in Strengthen organization after 5 years of rapid growth while retaining key employees with innovative HR programs. [ 8 ]

9 Industry Faces Significant Future Demand Challenges Worldwide Decline Rate 6.8% [ 9 ]

10 Our Long Term Strategy Solving the most complex reservoir imaging problems A leader in geophysical imaging technology and services that aims at solving the toughest problems. Balanced portfolio from early adopter technology for future growth to more mature products and services for earnings and cash flows. Asset light We don t provide the actual field services which require large investments in people and equipment that is mainly a logistics business. Strong investment in R&D aimed at technology leadership in our core areas, including game changers Target oil companies to pull through new technologies by solving their most challenging reservoir imaging problems with cost effective technology and services. Global presence through regional business structure and strong local partnerships. Innovative business models that differentiates ION from our competitors [ 10 ]

11 Diversified Technology Portfolio with Products in Various Stages of the Product Lifecycle A Portfolio Approach 2004 System Four Vibrators Geophones Streamer Products Image ARAM products complement our product portfolio with robust margin products in the heart of their lifecycle DigiRANGE II 2007 Scorpion Wave Equation PreSDM Spectra Vibrators Geophones Birds Land Marine Seismic Imaging Solutions & Data Processing ISS and Data Library Gator Kirchhoff PreSDM Full-wave Processing DigiFIN FireFly ORCA VS Ocean RTM Image MSX Early Market Growth Mature End of Life Significant Investments in in R&D

12 Seismic Imaging Solutions Segment Seismic Data Processing Services Integrated Seismic Solutions (ISS) Seismic Data Libraries GXT Imaging Solutions Leading Depth Imaging Technology. Focused on most difficult imaging problems Marine and land. AXIS Geophysics Group Acquired and merged into GXT. Specialist s in land imaging. IP in new technologies such as wide azimuth applications. Deal origination for oil company underwritten multiclient projects. Full solution proprietary surveys Marine and Land Test vehicle of ION new systems technology, e.g. FireFly. Result of ISS multi-client projects. Global portfolio of Regional Span Libraries. Focused on Exploration hotspots. Strong brand in high-end niche business.

13 Seismic from an Oil Company Perspective ION Prepared to Address the Fundamental Questions Entrapment Gas Cap Oil W ater Seal Rock Reservoir Rock Migration 120 F Generation 350 F The Fundamental E&P Questions How is the petroleum system put together? Do I have a trap? Do I have a reservoir? What fills the reservoir? Addressed via ION Offerings BasinSPANs Structural imaging - RTM Lithology imaging - Full-wave Fluid detection Full-wave [ 13 ]

")

14 ION s Global Footprint in Data Processing January 2004 Geophysical Service Centers (GSCs) [ 14 ]

15 ION 2009 Global Processing Scale GSC Project Experience [ 15 ]

16 Imaging Technology Timeline HGSC Resource Evolution Cumulative total processors Cumulative peak performance (GFlops) Cumulative total memory (GB) GFLOPS RTM Beam Migration late 1999 mid 2001 early 2002 mid 2003 mid 2003 mid 2004 early 2006 Mid 2007 Mid 2008 One-way WEM Purchase Date Kirchhoff PreSDM [ 16 ]

17 West Africa Imaging Example RTM Defines the Up-dip Limit of Potential Reservoirs KIRCHHOFF RTM? [ 17 ]

18 RESERVOIR SOLUTIONS DELTAIC / BRAIDED CHANNELS SYSTEMS [ 18 ]

zoom")

19 Dajing Oil Field 30% of China Production In Serious Decline 45 well heads (counting the work-over rig) zoom [ 19 ]

20 High density drilling highly obstructed area Candidate for both Full Wave imaging and FireFly [ 20 ]

21 Some Key Wells with Cumulative Production > 1MMBO Cummulative Production >5 mmbo 2-3 mmbo 1-2 mmbo [ 21 ]

, fluids, and fracture patterns")

22 Reasons For Full-wave Survey In Dajing Enhanced bandwidth 3C Digital MEMS sensors capture lower lows and higher highs, which translates into improved reservoir resolution and is less sensitive to ambient noise. Improved reservoir characterization full-wave seismic data lets one better determine lithology (rock type), fluids, and fracture patterns Improved productivity rather than deploying an array of 6, 12, or more geophones, only one single-point 3C sensor is required [ 22 ]

23 Overview of a BasinSPAN Program Comprehensive view of the petroleum system Integrates geology and geophysics Ultra-deep view Source rock deposition Migration pathways Sediment fairways Customized program design Acquisition technology & methods Seismic data processing Funded and underwritten Energy ministry NOC E&P operators BasinSPAN applications Develop a better understanding of existing play types / identify new play concepts Allow host governments to attract new investment Allow better evaluation of license round offerings and resulting work commitments [ 23 ]

24 Why the Arctic? High Potential in the Region Estimates place 25% of all remaining undiscovered reserves in the Arctic. Source: USGS, World Petroleum Assessment [ 24 ]

25 Marine Imaging Systems Segment Towed Streamer Acquisition Systems Marine Positioning Systems Ocean Bottom Acquisition Systems DigiSTREAMER Marine Streamer DigiBird and DigiFIN Marine Positioning System VectorSeis Ocean Redeployable Seabed System Second bite of Apple-new product-line for ION. Short term incremental business. Supports longer term integration strategy. Clear leader in positioning devices, both lateral and horizontal. Trend to more accurate shooting supports increasing sales. Solid spares and repairs business. Orca-Concept Systems products-also high share. First seabed digital full wave system. Highly productive system. Excellent in obstructed areas. Mainly used for reservior characterization. [ 25 ]

26 Summary on Total Vessels/etc Towed Streamer Fleet Capacity Range: Vessel count Capacity Range: Streamer km Hi 3D Hi 2D/Low 3D 2D Streamer Km Low Streamer Km High 40 Capacity Range: [ 26 ]

27 A Matter of Perspective 16 x 12km Spread Configuration Overlaid on Manhattan 16 x 12 towed streamer spread configuration [ 27 ]

28 Analogy: Commercial Air Travel vs. Towed Streamer Operational Planning Commercial Air Travel Flight Plan Towed Streamer [IA] Survey Plan [ 28 ]

29 Analogy: Commercial Air Travel vs. Towed Streamer Operational Command & Control Intelligence Commercial Air Travel Auto Pilot Towed Streamer [IA] Orca [ 29 ]

30 Analogy: Commercial Air Travel vs. Towed Streamer Dynamic Operational Execution Commercial Air Travel Towed Streamer [IA] Dynamic Horizontal Control Tail rudder DigiFIN Dynamic Vertical Control Wing flaps AcousticBird [ 30 ]

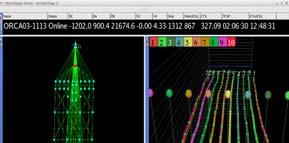

![[IA] in Action Orca](/docs-images/89/99251251/images/31-1.jpg "Software")

31 [IA] in Action Orca Software Controlling the Streamer Spread via DigiFIN [ 31 ]

High Density-Full Wave (Scorpion).")

32 Land Imaging Systems Segment Land Acquisition Systems Vibrators and Energy Sources Geophone Firefly World s First digital Full Wave Cable-less Recording System Highly productive system Access in challenging topologies. Records Digital Full Wave Scorpion and ARAM Cabled Recording System Low cost, highly reliable analog system (ARAM) High Density-Full Wave (Scorpion). X-VIB / ADV-IV Vibrator Vehicles Industry workhorse Highly reliable in both desert and Arctic shooting. Pelton Source Controllers Energy Source Controllers Controller for both Vib and dynamite shooting. Designed for efficient operations. SM-24 Geophone Analog Sensor Leadership analog geophone. ARAM s land-based analog products will will complement existing product portfolio [ 32 ]

33 Majority of Global Resource Base is Onshore Hydrocarbon Distribution in the Top 25 Basins Known Reserves + Mean Undiscovered Resources Billions of Barrels of Oil Equivalent 40 34* Offshore 29% 100% = 3,058 Billion BOE Known Reserves = 2,141 Undiscovered = 917 Onshore 71% Source: USGS 2000 Worldwide Reserves Assessment (as published in Hart s E&P) Onshore offshore splits were estimated in mixed basins Some geographically-proximate basins were combined to simplify the illustration * Western Canada excludes tar sands and heavy oil (assessment was for conventional resources only) [ 33 ]

34 2008 Estimated Global Seismic Crew Count Estimates for 2008 (1) Total (2) EAME & ISC Russia & CIS China/AP North America Latin America WGN working EY # of Crews Dynamite/Vibe Mix 55% / 45% 25% / 75% 50% / 50% 80% / 20% 40% / 60% 78% / 22% 2D/3D Mix 40% / 60% 50% / 50% 55% / 45% 40% / 60% 20% / 80% 35% / 65% 1) Estimates based on interviews with GBD, Solutions, financial reports & filings, equity analyst reports, company websites, gov t agency reports 2) World Geophysical News underestimates #crews in Russia/CIS, China/AP, and in India (ISC). Crew counts in these regions are based on internal crew-channel database updated in early 2009 [ 34 ]

35 Land Technology Trends High Density Shooting for higher resolution Shallow plays such as Heavy Oil are 10X trace density of more conventional basins Benefits seen above leading to a move towards denser sampling in mature basins to resolve tougher interpretations Wide Azimuth for lateral variation Fracture detection for optimal lateral drilling in tight sands and shales Digital Full-Wave for Reservoir Description 4D-3C work in Oil Sands increasing - SAGD programs come on-stream Shale gas plays largest reservoirs discovered in last decade Evidence of better shallow imaging with converted-wave acquisition Deeper plays in more difficult areas longer offsets required Older seismic surveys do not have the velocity resolution required (velocity resolution proportional to offset distance) to extract rock property information properly High-productivity Vibroseis Operations with continuous recording Pushing both cable & cable-less acquisition technology to upgrade to a high standard of synchronization and efficiency in data-quality control [ 35 ]

36 Demand for Increasing Channel Count Need for better reservoir description driving demand [ 36 ]

[")

37 Land Survey Schematic Cable-based Recording System (Scorpion or ARIES) [ 37 ]

38 Land Survey Schematic Cableless Recording System (FireFly) [ 38 ]

39 The FireFly Ecosystem A Comprehensive Approach Survey design for optimum image Navigation and positioning Node-based, full-wave recording system GIS planning and operations support Comprehensive data management [ 39 ]

40 FireFly Commercialization Update A combination of sales and rental/purchase agreements China Qaidam Basin 3D First commercial sale of FireFly Receiver stations: 10,808 Source points: 13,632 In progress Chopo Sur 3D Comesa and Pemex 270 sq km March 09 Source points: 5498 Receiver points: Q2 09 Baby & Big Blocker BP NAG Baby blocker: 7 sq mi; March 09 Big Blocker 68 sq mi: Q3 09 Dallas Shreveport ISS Haynesville 2D 5760 source points receiver points Q2 09 [ 40 ]

41 ION Land Acquisition System Strategy In the Context of Technology Adoption Cycles* High Channel Count Analog [Middle East, North Africa] Low Channel Count Analog [US Mid-continent - Conventional] II High Channel Count Digital [China, Russia, India, W. Canada] Cableless [US Rockies, Unconventional] Version 2 Innovators Early Adopters Early Majority Late Majority Laggards * Courtesy of Geoffrey Moore and The Chasm Group [ ]

42 Summary The beginning of economic recovery will likely drive oil prices back to $60-$70 bbl or higher. Supply will once again become the main driver. ION s short term goal is to weather the storm by focusing on cash management, including tight cost controls while preserving technical leadership in core areas. Sufficient free cash flow within guidance range to service the companies debt- and due to high variable cost business can ratchet down even more if necessary. Strong R&D investment is coming to commercial fruition with DigiFin, Orca, FireFly, ARIES II, etc. ION is well positioned for growth once the market turns, likely in [ 42 ]

43 Appendix [ 43 ]

44 Net Revenues 2008 vs ($ Millions) $800 $ $600 $ $ $ $200 $ $ [ 44 ]

45 Revenues and Gross Margin Percent 2008 vs Revenues ($ Millions) Gross Margin % [ 45 ]

46 Segment Revenues 2008 vs ($ Millions) Land Imaging Systems Marine Imaging Systems Seismic Imaging Solutions GXT Data Management Solutions Concept Systems [ 46 ]

47 EBITDA 2008 vs ($ Millions) (10) (35) (60) * EBITDA (earnings before net interest expense, taxes, depreciation, and amortization) * Restated [ 47 ]

48 Diluted EPS 2008 vs $0.60 $0.50 $0.52 * $0.50 * $0.40 $0.30 $0.20 $0.10 $0.22 $0.33 $ * Excludes one time charges [ 48 ]

49 Balance Sheet Highlights 12/31/05 12/31/06 12/31/07 12/31/08 Total LT Debt $71.5 MM $71.0 MM $9.8 MM $253.5 MM LT Debt/Cap 12.1% 11.9% 1.6% 24.9% Net Debt/Cap 10.2% 10.2% -1.9% 25.2% Cash & Equity $15.9 MM $17.1 MM $36.4 MM $35.2 MM [ 49 ]

50 Balance Sheet Highlights (continued) Q Q Q Q Inventory $163.9 MM $189.2 MM $254.8 MM $262.5 MM Cash Balance $36.0 MM $18.8 MM $32.2 MM $35.2 MM Net Debt ($13.2 MM) $3.7 MM $282.7 MM $256.7 MM Leverage* (0.1) * Net Debt to EBITDA [ 50 ]

51 Updated Annual Guidance Full-Year Revenues $620 $680 MM Diluted EPS $0.00 $0.16 [ 51 ]

52 ION Total Revenues Revenues in $ Millions ION Solutions Land Marine CSL E Gross margin 30.6% Op margin 10.1% 36 38% 20 22% [ 52 ]