Global Wood Flows: 2011 and Beyond

|

|

|

- Jade Watts

- 5 years ago

- Views:

Transcription

1 Global Wood Flows: 211 and Beyond Bob Flynn Director, International Timber FRA Webinar, April 13, 211

2 Global Wood Flow - Agenda Impact of the Japanese earthquake and tsunami Pacific Rim Woodchip Market Review and Outlook Atlantic Region Woodchip Market China s Timber Supply Deficit major driver of international trade in forest products 2

3 3

4 4

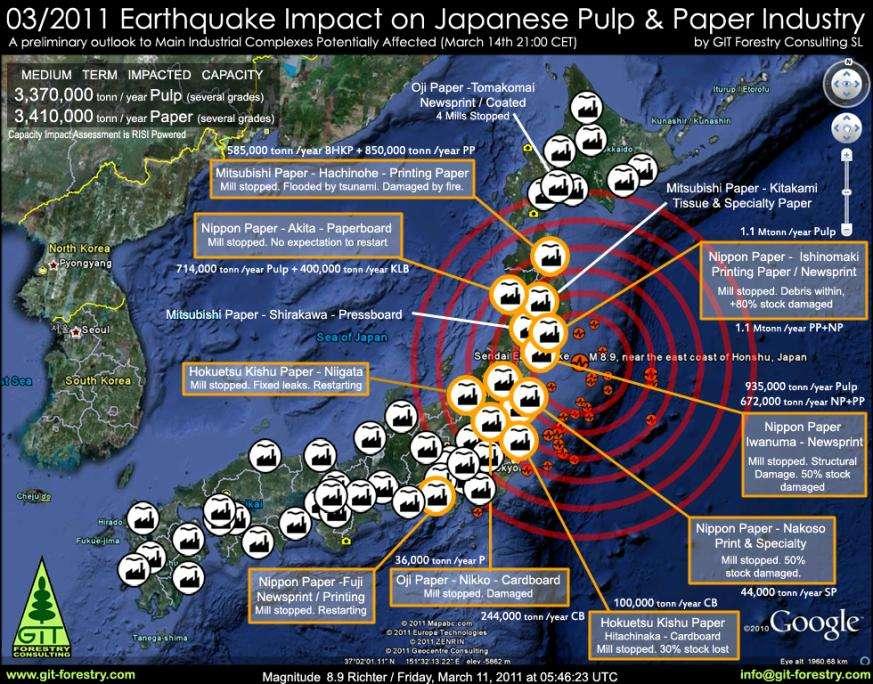

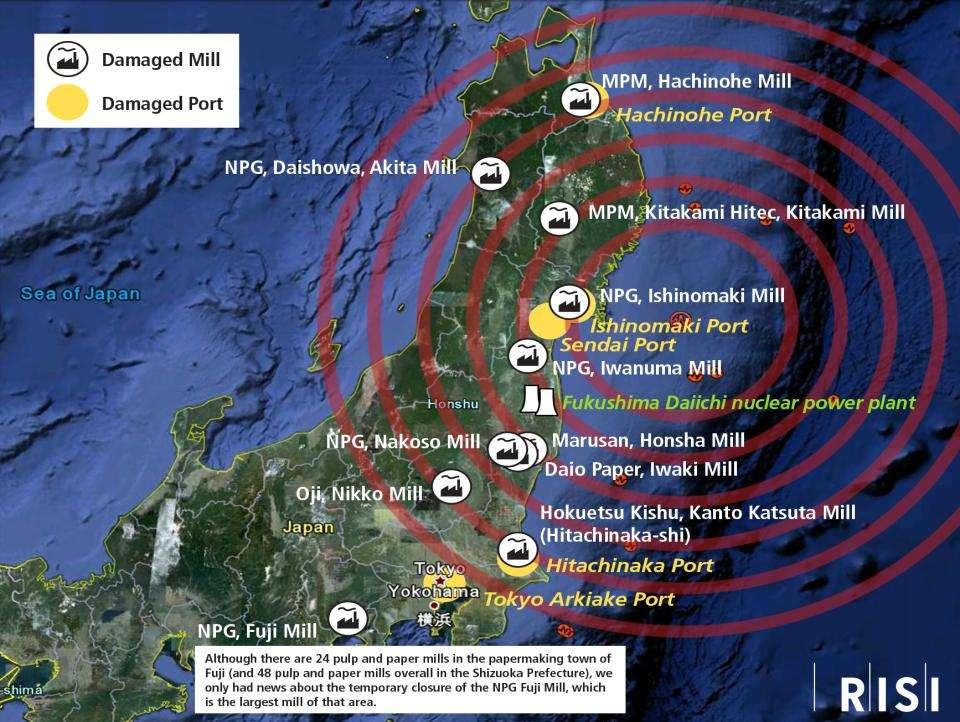

5 Information is still incomplete, as 2, people are feared dead or missing 5

6 Entire towns have been wiped off the map 6

7 Japanese companies are understandably in a state of confusion 7

8 And parents have more pressing concerns than worrying about how many tonnes of pulp will be produced next month 8

9 Woodchip Consumption at Affected Mills: May not be as bad as early estimates assumed Total Woodchip Consumption in Japan 21: 16m BDMT Affected Mills Consumption Unaffacted Mills 9

10 Australia and Chile will likely be affected most, as they are the largest suppliers to Japan 1

11 In aftermath of earthquake, reconstruction efforts could have a measurable impact on global wood product markets, as Japan was already the 3rd largest importer 11

12 Additional softwood log imports would most likely come from North America 12

13 European sawmills could also benefit from reconstruction, as they have been major suppliers to Japan already 13

14 Port Damage Is Extensive Major damage to ports handling 7% of Japan s industrial output Tokyo and all ports south operating normally after brief shutdown Damage primarily to mid-sized container ports Only two of the twelve major ports where bulk carriers or tankers can dock were damaged Port closures in the weeks following the tsunami were costing Japan $3.4 billion per day in lost seaborne trade (Journal of Commerce) 14

15 Pacific Rim Woodchip Markets 15

16 Million BDMT Woodchip imports in Asia fell 17% in 29, but rebounded to a new record volume of 18.2 million BDMT in 21 Pacific Rim Woodchip Imports, E 2 18 Japan HW Japan SW Other E Source: RISI s International Pulpwood Trade Review

17 Million BDMT The share of hardwood chips in the Pacific Rim trade has increased from 77% in 1994 to 88% in Pacific Rim Woodchip Trade by Species Softwood Hardwood E 17

18 Japan dominated the woodchip markets for 4 years, but its market share fell from 85% in 28 to 67% in 21, as Chinese imports have surged Asian Woodchip Import Markets, January-December /29 Japan 12,272 9,7 1,1 11% China 1,28 2,66 4,478 68% Taiwan % Korea % Total Hardwood 14,847 12,66 16,55 27% Softwood Japan 2,45 1,46 2,17 43% China % Total Softwood 2,454 1,58 2,166 44% Total All 17,31 14,168 18,221 29% 18

19 Thousand BDMT China s hardwood chip imports jumped from 1. million BDMT in 28 to 4.5 million BDMT in 21, with 87% coming from Southeast Asia 5 4 China: Hardwood Chip Imports by Source Other Australia Indonesia Thailand Vietnam

20 Thousand BDMT Southeast Asia has suddenly become the key supply region for the Asian woodchip markets 5 Hardwood Chip Supply to Pacific Rim, 29 & Australia Chile S Africa Vietnam Thailand Indonesia 2

eucalyptus logs like these are used for veneer")

21 Pulpwood is expensive in China, as even very small (8cm+) eucalyptus logs like these are used for veneer 21

22 F 211F 212F 213F 214F 215F Pacific Rim imports of hardwood chips will set another new record in 211.and in 212, 213, etc. 24 China Japan Korea Taiwan Forecast

23 F 212F 213F 214F 215F Softwood chip markets in Asia will remain much smaller and slower growing than hardwood markets, although China could expand much faster than forecast 3.5 Japan China Forecast

24 98-1Q 98-4Q 99-3Q -2Q 1-1Q 1-4Q 2-3Q 3-2Q 4-1Q 4-Q4 5-Q3 6-Q2 7-Q1 7-Q4 8-Q3 9-Q2 1-Q1 1-Q4 US$ per BDMT Australia has been the dominant supplier of hardwood chips, but now have by far the most expensive fiber 25 Chile and Australia: E. globulus FOB Pricing, Q4 2 Australia Chile

25 Million Cubic Feet Japanese companies have controlled the logistics of the international chip trade by owning most woodchip carriers, but this is now changing 6 New Woodchip Carriers, , by Owner Country Chinese Japanese 25

26 Atlantic Region Woodchip and Biomass Markets 26

27 Thousand Cubic Meters The Atlantic region market for pulpwood imports (pulplogs and chips) is much smaller than the Pacific market, and has mostly shifted to woodchips 3 25 Eucalyptus Pulplog Exports to Europe Brazil Chile Argentina Uruguay Congo

28 Thousand Cubic Meters Despite the log export tax, Russia s exports of birch pulplogs to Finland and Sweden revived in 21 but the Baltics are still the largest suppliers Sweden and Finland Pulplog Imports, by Source Softwood Hardwood Softwood Hardwood Russia Baltics 28

29 Thousand BDMT Turkey has been the largest woodchip importer in the Atlantic region, but imports surged in Spain and Portugal in 21, and Morocco began importing 7 Atlantic Region Woodchip Imports from Overseas Spain Portugal Turkey Norway Sweden Finland Morocco USA 29

30 Uruguay is the largest supplier of hardwood fiber to the Atlantic markets, the USA is the largest supplier of softwood --- but only to Turkey 1, Atlantic Region Woodchip Sources, Softwood Hardwood Uruguay Brazil Canada Congo Chile USA Venezuela 3

31 Uruguay is the largest supplier of pulpwood to the Atlantic markets, but what will happen when the Stora Enso/Arauco mill starts up in late 213? Supply and Demand of Eucalyptus in Uruguay, Source: Pike y Compania 14 Demand Supply Balance

32 Million Green Tonnes If all proposed new biomass power plants in Europe are built, and co-firing proceeds as planned, global capacity will be strained trying to supply the biomass fiber UK Total 29 Timber Harvest and New Biomass Demand UK 29 Harvest New Biomass Demand 32

33 Thousand Tonnes Capacity There has been a stampede to develop new wood pellet projects in North America to provide biomass for the anticipated European demand 4,5 North America: Existing (27) Wood Pellet Capacity and New/Announced Projects 4, 3,5 Existing Announced 3, 2,5 2, 1,5 1, 5 South Central South Atlantic North East Lake States US West E Canada W Canada 33

34 The European demand for biomass imports is growing, but has been slower to develop than most wood pellet producers expected 1,8 North America: Wood Pellet Exports to Europe 1,5 1,2 USA W Canada E Canada

35 The Netherlands has been the biggest importer of wood pellets in Europe, followed by the UK, Denmark, Sweden and Belgium Other UK Italy Sweden Netherlands Denmark Belgium Major Wood Pellet Importers in Europe, Thousand Tonnes 35

36 Wood pellet capacity is likely to expand significantly, but will this mean greater competition for fiber with pulp producers? Wood Pellet Capacity in Major Supplying Countries, 29 & Forecast Source: RISI 211 North American Biomass Review USA Canada Russia South America Oceania Other Asia 36

37 The new mega wood pellet plants are essentially pulp mill scale facilities based on pulpwood logs Green Circle Bioenergy, USA, 5, tonnes (28) Vyborgskaya Cellulose, Russia, 9, tonnes (211) Georgia Biomass, USA, 75, tonnes (211) Suzano, Brazil, 3 X 1. million tonnes (????) Large producers like Pinnacle Pellets and Pacific Bioenergy now using a combination of sawmill residues and logging residues from beetle-killed timber In North America, the only wood pellet projects moving forward are those tied directly to end-users in Europe like RWE 37

38 To date, almost all biomass imports from overseas to Europe have been in pellet form Phytosanitary regulations require heat treatment for imports of softwood chips from North America and hardwood chips with oak. No company has been prepared to this, to date. Biowood Norway is importing woodchips from Canada and now Liberia to produce wood pellets. Greenfield biomass power plants in the UK based on woodchips have all been delayed until 214 or later. One company from Liberia has already exported some rubberwood biomass chips to Italy and other EU countries for energy; another company plans to begin a similar operation in Ghana this year. 38

39 China: Expanding market for logs, chips and anything else with wood fiber in it.. 39

40 China is now the world s second largest economy 16% 14% 12% 1% 8% 6% 4% 2% % China: Real GDP Growth (GDP at PPP, constant 25$; Annual Percentage Change) Annual Percent Change ,, 13,5, 12,, 1,5, 9,, 7,5, 6,, 4,5, 3,, 1,5, 4

41 Million Cubic Meters, RWE China has a large and growing timber supply deficit, despite having very large areas of plantations 14 China's Growing Timber Deficit, Woodchips Pulp Wood Panels Lumber Logs

42 Jan-8 Mar-8 May-8 Jul-8 Sep-8 Nov-8 Jan-9 Mar-9 May-9 Jul-9 Sep-9 Nov-9 Jan-1 Mar-1 May-1 Jul-1 Sep-1 Nov-1 Jan-11 Canada is the largest supplier of softwood lumber to China, and its market share is still expanding 6 China: Softwood Lumber Imports 5 4 Canada USA Russia Other

43 China is the world s largest market for paper grade pulp imports, and dissolving pulp imports are also growing rapidly Other Mech/Semi-chem UKP BHKP BSKP

44 There are many listed companies with timber assets in China today, but none come anywhere close to matching the performance of Sino-Forest Sino-Forest Revenue and New Income Revenue Net Income

45 In China s 12 th Five Year Plan ( ), timber harvest quotas have been expanded for plantations, but reduced for natural forests 4, 35, 3, 25, 2, 15, 1, 5, China: Timber Harvest Quota by Province 11th Plan 12th Plan - Guangxi Sichuan Fujian Jiangxi NE China SOE 45

46 Jan-6 Apr-6 Jul-6 Oct-6 Jan-7 Apr-7 Jul-7 Oct-7 Jan-8 Apr-8 Jul-8 Oct-8 Jan-9 Apr-9 Jul-9 Oct-9 Jan-1 Apr-1 Jul-1 Oct-1 Jan-11 For the first time, non-russian sources of softwood logs in China exceeded Russian imports, starting in August Russia Non-Russian

47 New Zealand has gained the most market share as imports of softwood logs from Russia declined in China, but the US is now also gaining fast 25 China: Softwood Log Imports by Source 2 15 USA Canada Aust N Zealand Russia

48 Thousand Cubic Meters Softwood log exports from the US Pacific Northwest have exploded as activity has now spread to many ports US and Canada Softwood Log Exports, to Japan, China, Korea, 29 & 21 7, 6, USA 5, 4, 3, 2, Canada Korea China Japan 1,

49 Million cubic Meters Russia s log export tariff is less of a factor in the China market going forward, as a greater volume is being imported in sawnwood form rather than logs 3 Russian Softwood Log and Lumber Exports to China 25 2 Logs Lumber

50 China s timber supply deficit will continue to expand, due primarily to demand from the pulp and paper sector and for lumber imports 2 Woodchips Pulp 15 Wood Panels Lumber Logs

51 Summary Woodchip imports in Asia are surging to record levels, as China seeks primarily hardwood fiber for domestic pulp production. The impact of the Japanese earthquake and tsunami are still not fully known, but may not have much long-term effect. The Atlantic woodchip market has expanded, and includes demand for fiber both for pulp and MDF production. This is a diverse market, some supply sources may not be sustainable. International trade in biomass fiber, almost all wood pellets, continues to expand as European power companies seek reliable long-term supply sources. But growth has been much lower than most participants had forecast, and much still needs to be done to develop both the supply and market sides of the trade. China s demand for imported wood fiber is continuing to expand, although at a slower rate --- with lumber, pulp and woodchip imports expected to grow the fastest in the next 4-5 years. 51

52 Questions? Bob Flynn Director, International Timber, RISI Phone: Web site: This presentation based on two recent reports: 1) 211 International Pulpwood Trade Review 2) China Timber Supply and Demand Outlook, Brochures for these reports are available for download along with copies of this presentation (or contact author) 52