Global Lead Supply: Recent Trends and Short Term Outlook

|

|

|

- Bernard Walton

- 5 years ago

- Views:

Transcription

1 Metal Bulletin s 7 th World Lead Conference Milan, Italy Global Lead Supply: Recent Trends and Short Term Outlook Paul White International Lead and Zinc Study Group (ILZSG) 11 th March 2015

2 Presentation Outline ILZSG Overview Lead Mine Supply Trends and Developments Industry Structure Short Term Forecasts Longer Term Outlook Conclusions 2

3 ILZSG Overview Intergovernmental organization set up within the UN system Significant level of industry representation Established by UN in 1959 in New York Moved to London in 1977 From start of 2006 ILZSG, ICSG & INSG co located in Lisbon, Portugal 3

4 ILZSG Membership Membership open to any country involved in lead and/or zinc production, usage, or trade. 29 members (>85% of global lead/zinc industry): Australia Germany Morocco Serbia Belgium India Namibia Sweden Brazil Iran Netherlands Thailand Bulgaria Ireland Norway United States Canada China Italy Japan Peru Poland European Community Finland France Korea Rep. Mexico Portugal Russian Fed. 4

5 ILZSG Overview Work of the Group Promote Market Transparency Closely monitor production, consumption, prices, stocks, trade flows and market balances Reports and directories Facilitate Co operation Between Government and Industry Twice yearly meetings Special conferences/seminars In depth Research into Issues of Interest/Concern to Members Environmental legislation Economic developments 5

6 Presentation Outline ILZSG Overview Lead Mine Supply Trends and Developments Industry Structure Short Term Forecasts Longer Term Outlook Conclusions 6

7 World Lead Mine Output 1964 to 2014 Source: ILZSG 7

8 6000 Growth in Lead Mine Output has been in China 000 tonnes China 2000 World Ex China Source: ILZSG

9 Lead is Mined as a By product of Zinc There are very few mines where Pb is the main product: Doe Run s mines in Missouri, USA Lucky Friday, USA Paroo Station (Magellan), Australia Tighza, Morocco Black Mountain, South Africa 9

10 Annual Capacity of 5 Largest Zn Mines Mine Source: ILZSG Capacity/yr 000t Capacity/yr 000t Lead Zinc Mine Lead Zinc Brunswick No Rampura Agucha Tara Red Dog Kidd Creek Century Pine Point Mount Isa Anvil McArthur River Total Total

11 % Zn 7,5 7,3 7,1 6,9 6,7 6,5 Falling Lead and Zinc Mine Grades Zn (LHS) Pb (RHS) % Pb 2,8 2,7 2,6 2,5 2,4 6,3 6,1 5,9 5,7 Source: Wood Mackenzie, Macquarie Research 5, f 2,3 2,2 2,1 2 11

12 A Silver Lining can be Important Cannington, Australia San Cristobal, Bolivia Fresnillo, Mexico Garpenburg, Sweden Sindesar Khurd, India Chungar, Peru Greens Creek, United States El Mochito, Honduras 12

13 Global Primary and Secondary Lead Output 000 tonnes Total 2000 Secondary Source: ILZSG

14 Ex China Secondary Lead Currently Accounts for 75% of Total Output 000 tonnes Total Secondary Source: ILZSG

15 Paroo Station (Magellan) Timeline Jan 05 March 07 Feb 10 April 11 Jan 13 Mar 13 Feb 14 mine commissioned output suspended due to contamination problems at port mine reopened mine placed on care and maintenance due to issues with concs transportation name changed from Magellan to Paroo Station reopened under managemment of Enirgi Metal Group idled due to fall in lead prices 15

16 Lead Mine Supply Source: ILZSG 16

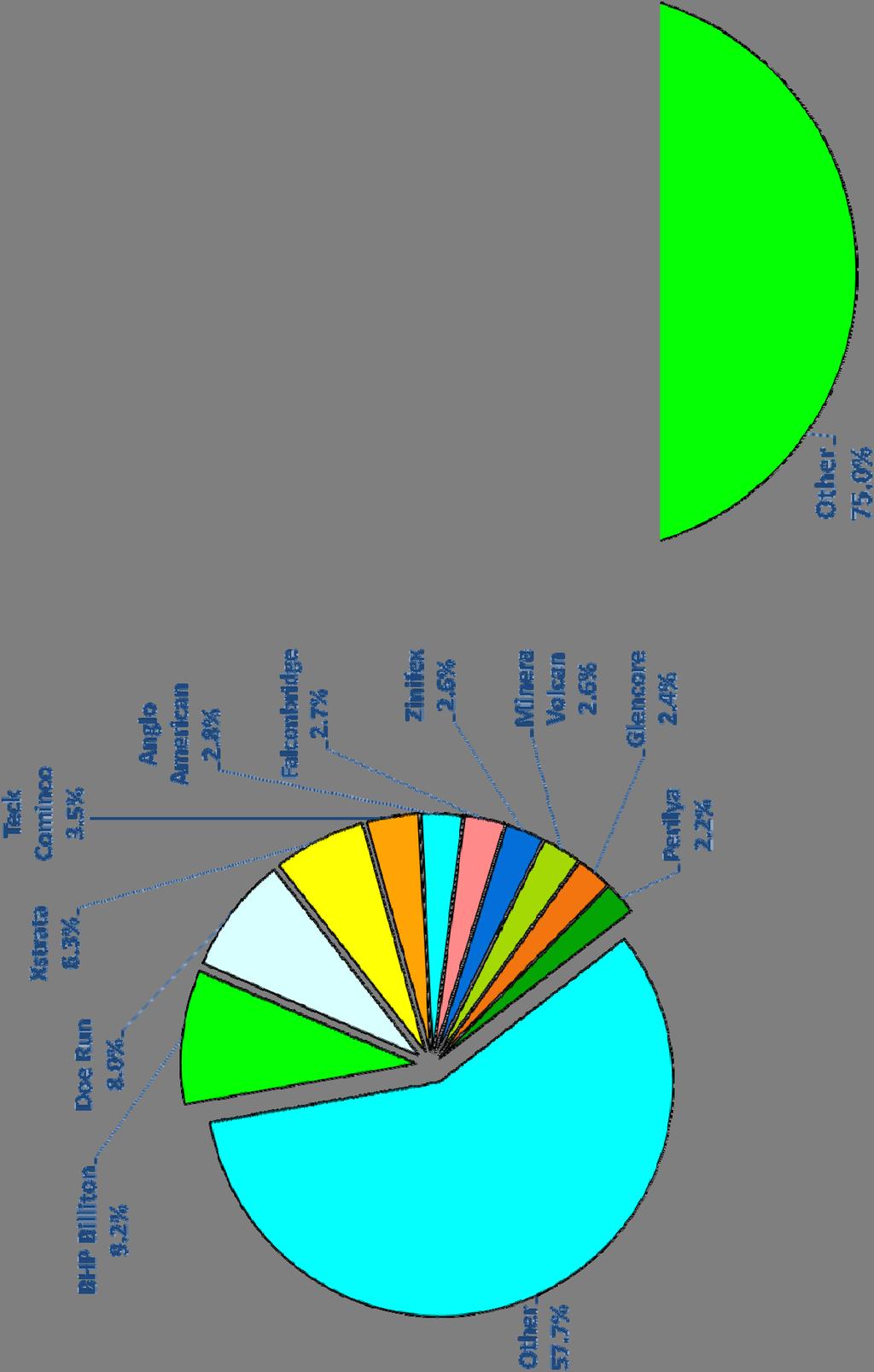

17 Distribution of Lead Mine Supply Other 12% Europe 12% Canada 5% Mexico Peru Europe 9% Mexico 5% 9% Peru USA Canada 4% 6% 15% Other 2% 11% USA 9% Australia 21% China 21% Australia 14% China 45% Source: ILZSG 17

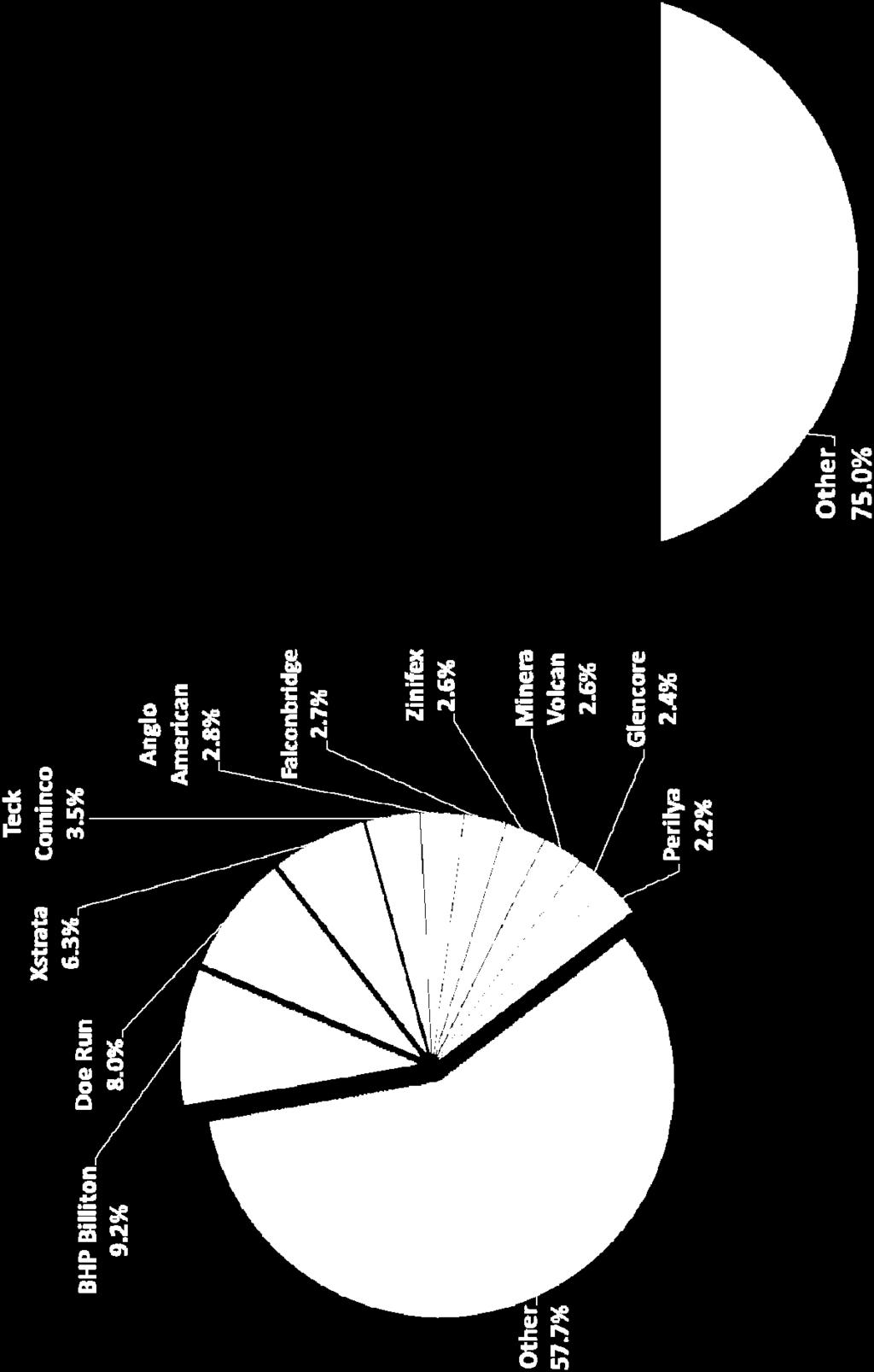

18 Chinese Investment Rising Dudar, Pakistan CMG/Hunan Nonferrous 100% Broken Hill, Australia Shenzhen Zhongjin 52% Golden Grove, Australia MMG 100% Rosebury, Australia MMG 100% Century, Australia MMG 100% Teck, Canada China Investment Corp 17% % of total lead mine supply controlled by Chinese coys = approx 58% + interests in a number of new projects including Wolverine, Izok Lake, Dugald River and Selwyn 18

19 Presentation Outline ILZSG Overview Lead Mine Supply Trends and Developments Industry Structure Short Term Forecasts Longer Term Outlook Conclusions 19

20 Merger & Acquisition Activity Merger of Zinifex and Oxiania and subsequent purchase of Oz Minerals by MMG Purchase of Anglo s Pb and Zn assets by Vedanta Nyrstar s purchases of: Breakwater Resources Gordonsville East Tennessee Mines Coricancha Cotanga Pucarrajo Purchase of Xstrata by Glencore 20

21 Distribution of Lead Mine Output 2004 vs Source: Wood Mackenzie / ILZSG 21

22 Highly Fragmented Structure of Lead Mine Output in China Structure of Lead Mine Output in China 2014 Large scale 0 Middle scale 20 Small scale 350+ Private small mine 500+ Number of Mines 870+ Source: Antaike 22

23 Presentation Outline ILZSG Overview Lead Mine Supply Trends and Developments Industry Structure Short Term Forecasts Longer Term Outlook Conclusions 23

24 World Lead Mine Supply Forecast ILZSG Forecast (October 2014) 12.0% 10.0% Global Annual Change 2015 Global 5.5% China 8.5% Ex China 2.2% 8.0% 6.0% 4.0% 2.0% 0.0% f 2015f Source: ILZSG 24

25 Chinese Lead Metal Output Grows at Faster Rate than Mine Output Source: ILZSG 25

26 China Becomes Significant Importer of Lead Concentrates Source: ILZSG 26

27 Selected Recent Lead Mine Openings and Closures Openings: Paroo Station, Australia George Fisher, Australia (expansion) McArthur River, Australia (expansion) Garpenburg, Sweden (expansion) Kayar, India Closures: Brunswick, Canada Paroo Station, Australia 85,000t 36,000t 51,000t 20,000t 15,000t 55,000t 85,000t

28 World Lead Metal Supply Forecast ILZSG Forecast 2015 Global 2.2% China 4.5% Ex China 0.3% 8.0% 7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% 1.0% Global Annual Change f 2015f Source: ILZSG 28

29 Decline in USA Refined Lead Output 000 tonnes Exide Technologies 65 kt/yr secondary plant at Frisco closes in Nov12 JCI plant in S. Carolina opens in Sep12 Exide Technologies 70 kt/yr secondary plant at Reading closes in Mar13 Doe Run s 220 kt/yr Herculaneum plant closes in Dec13 Operations suspended at Exide Technologies 88 kt/yr Vernon plant in Mar14 Source: ILZSG 29

30 La Oroya, Peru Shutdown Again Sep 14 June 14 Dec 12 Apr 12 Jun Profit Investment Consulting replace Right Business as administrators operations suspended production restarted Right Business appointed as administrators operations suspended smelter commissioned refinery commissioned 30

31 Lead Smelter Output Future Developments Possible reopening of 25 kt/yr Karachipampa Kivcet plant in Bolivia commissioned in Sept 14 after 26 year wait but then closed in Oct kt/yr Zellidja primary operation in Morocco may reopen under ownership of Binani Group Nyrstar s Port Pirie complex in Australia being converted into flexible metals recovery facility 31

32 Presentation Outline ILZSG Overview Lead Mine Supply Trends and Developments Industry Structure Short Term Forecasts Longer Term Outlook Conclusions 32

33 Lead Producing Mines due to Close in Next 2 Years Mine Century, Australia Bukowno Olkusz, Poland Lisheen, Ireland Annual Capacity 40,000t 26,000t 30,000t Forecast Closure

34 Limited Number of Committed Lead Mine Projects Mine Dugald River, Australia Lady Loretta, Australia Paroo Station, Australia Caribou, Canada Halfmile Lake, Canada Ozernoye, Russia Shalkiya, Kazakhstan Annual Capacity* 28,000t 15,000t 85,000t 15,000t 16,000t 50,000t 30,000t *Pb Metal contained Open 2017 (new mine) 2016 (expansion) 2016 (reopening) 2015 (reopening) 2016 (new mine) 2019 (new mine) 2018 (new mine) Source: New Mines and Smelters 2015 Report, ILZSG 34

and NFC (China) Possible")

35 ernoye Project, Russia Located in Rep. of Buryatia in Southern Siberia 50:50 j/v between MBC (Russia) and NFC (China) Possible 50Kt/year lead Extensive infrastructure requirements

36 Selected Lead Mine Projects Under Consideration ine urce: New Mines and Smelters 2014 and 15 Reports, ILZSG ackett River, Canada ine Point, Canada elwyn, Canada ing, Henan, China ala Hamza, Algeria airi, Indonesia ehbiabad, Iran ordero, Mexico Estimated Addition to Annual Capacity 20,000t (new mine) 30,000t (reopening) 39,000t (new mine) 30,000t (new mine) 36,000t (new mine) 36,000t (new mine) 70,000t (new mine) 30,000t (new mine)

37 ala Hamza Project, Algeria Large deposit identified Joint venture between Terramin and Algerian State Possible 36kt/year lead Estimated 5 year construction period

38 ehdiabad Project, Iran World s largest undeveloped zinc deposit Possible 70kt/year lead 25% of resource is oxide New joint venture between Russian Technologies and

39 Conclusions China currently consumes 70% of global lead concentrate production 75% of refined lead metal produced ex China is from recycled materials Lead is mined as a by product of zinc and, to a much smaller extent, silver In recent years zinc mines have been producing less lead Increased environmental legislation has reduced the attractiveness of identifying and developing lead mines Outside China only a limited quantity of new lead mine

40 THANK YOU!