Opportuni)es and Consequences of the US Shale Revolu)on. Eric N. Smith Tulane Energy Ins)tute 7/9/16

|

|

|

- Evan Stevens

- 5 years ago

- Views:

Transcription

1 Opportuni)es and Consequences of the US Shale Revolu)on Eric N. Smith Tulane Energy Ins)tute 7/9/16

on is driven by stronger oil demand growth and unexpected supply cuts 6-14-16")

2 The surplus of supply over demand in the first half is currently about 800,000 b/d compared with the ini)al expecta)on of 1.5 million b/d in January. The sharp reduc)on is driven by stronger oil demand growth and unexpected supply cuts

in May 2016 Along with other factors such as rising oil demand and falling U.S.")

3 Unplanned global oil supply disrup)ons averaged more than 3.6 million barrels per day (b/d) in May 2016 Along with other factors such as rising oil demand and falling U.S. crude oil produc)on, the rise in disrup)ons contributed to a month-over-month $5 per barrel increase in Brent crude oil spot prices in May-2016.

al expecta)on of 1.2 million b/d.")

4 This year s first quarter shows year-over-year growth of 1.6 million b/d, up from an ini)al expecta)on of 1.2 million b/d. IEA has increased annual demand growth to 1.3 million b/d from 1.2 million b/d

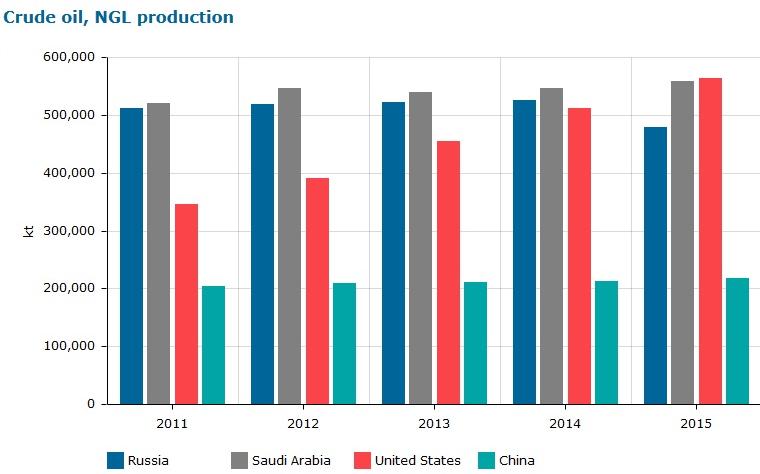

5 1 1

6

7

8

9 One consequence is a volume decline in imports and a price war with the Saudi (bbl/day) EIA

10 Overall, Crude Oil Imports have Declined

11 Light, Sweet Crude Oil Imports have Declined Significantly

12 However, Heavy, Sour Crude Oil Imports Have Increased

13

14

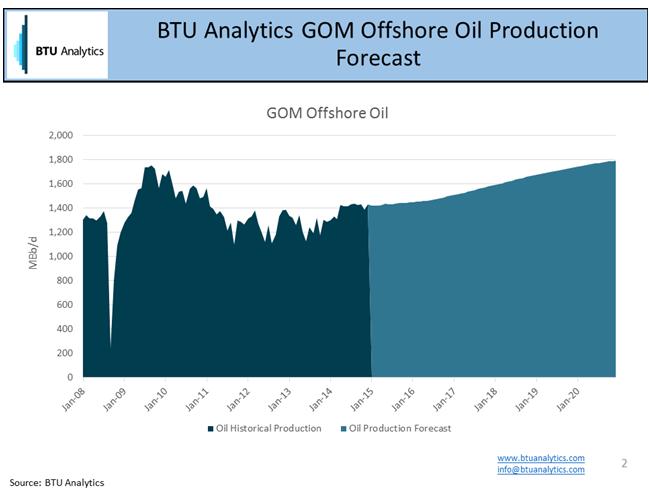

![BOEM 2017-2022 OCS Oil and Gas Leasing Program Dra] Proposed Program announced 1/27/15 including 13 lease sales including 10 in the GOM Area and one sale each in the Chukchi Sea, Beaufort Sea and](/docs-images/89/100158143/images/15-0.jpg "Cook Inlet Areas. No sales are proposed in the Pacific or Atlan)c OCS.")

15 BOEM OCS Oil and Gas Leasing Program Dra] Proposed Program announced 1/27/15 including 13 lease sales including 10 in the GOM Area and one sale each in the Chukchi Sea, Beaufort Sea and Cook Inlet Areas. No sales are proposed in the Pacific or Atlan)c OCS. The comment period for the proposed program opened on March 18, 2016 and closed on June 16, 2016 Residual from Lease Schedule Lease Schedule

16 42 TCF 29 TCF 14 TCF = 48% 29 TCF = 69%

ca flowing South")

17 Flow Paderns Will Change with Marcellus/U)ca flowing South East

18 Spot Henry Hub Gas Price over recent 12 months

19

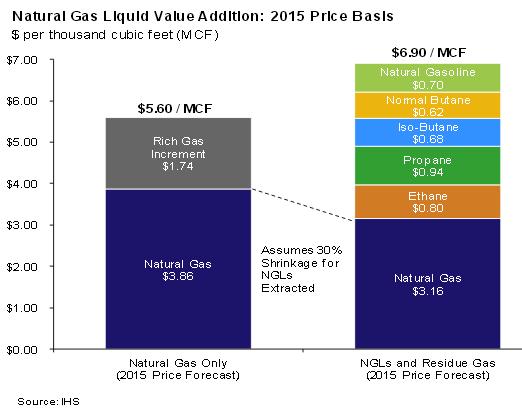

20 The Ra?onale for Wet Gas Produc?on As US gas demand increased, we began building mul)ple LNG import terminals in order to sa)sfy demand growth in the face of stagnant produc)on. In the early 2000s, experiments by Mitchell Energy combining horizontal drilling with sequen)al fracking were successful in the Barned dry gas shale in Texas. Addi)onal success was then seen in the Haynesville shale in Louisiana. The addi)on of new dry gas supplies reduced the retail price of gas, rendering the higher cost LNG import business moot. It costs the same to drill and frack a wet gas well as it does a dry gas well. Because extracted NGLs could be sold for more than dry gas. Operators switched to drilling wet gas reserves. The average wellhead price increased to the point where wells were viable, even if dry gas was only selling for $2.00/mcf. Eventually, the extra NGL produc)on suppressed the price of NGLs, but not before sejng off booms in the petrochemical business and the NGL export business. The price of extracted NGLs then fell to where the margin didn t cover the variable cost of extrac)on and transporta)on. Gas operators and processors then began to reject NGLs. That is, they let them remain in the gas leaving the processing plant. Currently 45% of the Ethane produced at the wellhead is being rejected.

21 Wet Gas vs. Dry Gas (Natural Gas becomes the by-product) 6 5 Break-Even Price ($/Mcf) Barned Fayedeville Marcellus Shale Haynesville Shale Eagle Ford (Wet Gas Well) Source: Deutsche Bank, Penn Virginia Corporation

22

23

24

25

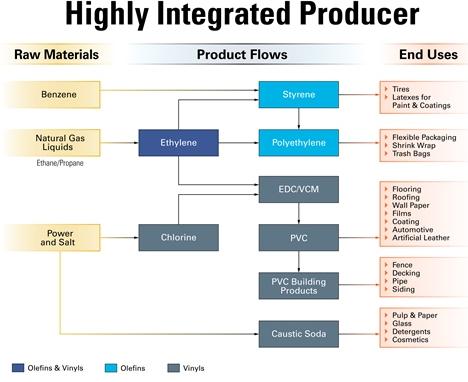

26 What are the Downstream Markets for NGLs?

27 Ethane reflects Natural Gas Price Others reflect Crude Oil Price

28 Growth across the board but highest in Asia

29

30

31

32

33

34 Announced US Ethylene Cracker Expansions Calvert City - $300 mm to use Ethane from the Marcellus Shale

35 Announced New US ethylene production facilities

on")

36 New Polyethylene Polymeriza)on Projects

37 What you Need to Expand Ethane Exports New Marine Technology Ineos is building a fleet of eight Liquid Ethane Transporters Asked why the project makes sense, one commentator says: One word: shale.

onal, with 3.0 million long tons going southbound and 2.6 million long tons going northbound (from the Pacific to the Atlan)c).")

38 How About the New Panama Canal Locks? In 2015, diesel fuel and gasoline made up the largest share of southbound traffic, totaling 9.5 million long tons and 9.1 million long tons, respec)vely. Crude oil traffic was significantly smaller and bidirec)onal, with 3.0 million long tons going southbound and 2.6 million long tons going northbound (from the Pacific to the Atlan)c). HGLs exceeded crude oil southbound volume. The second ship through the new locks was an LPG unit headed from Houston to Asia.

39 Taken as a whole, U.S./Canadian PE sales were up 6.3 percent to 40.6 billion pounds in 2015, with almost 77 percent going into the domes)c market and 23 percent going to exports. U.S./Canadian HDPE sales were up 7.5 percent in 2015 to more than 18.9 billion pounds. Domes)c sales actually fell by 1.5 percent, but they were propped up by explosive 57.5 percent growth in exports. Almost 78 percent of regional HDPE sales went into the domes)c market, with the remainder sold as exports. For LDPE, 2015 U.S./Canadian sales grew 2.8 percent to more than 7.1 billion pounds. As with HDPE, a domes)c sales loss of 1.2 percent was counteracted by a gain of 16.4 percent in export sales. In LLDPE, U.S./Canadian sales grew 6.6 percent to more than 14.6 billion pounds in Domes)c sales growth of 2.7 percent was enhanced by a 21.3 percent jump in export sales. Film markets were a major driver for domes)c LLDPE growth in 2015 Much of this collec)ve growth was based on shipments to Asia. However, China is rapidly increasing its own cracker and polymeriza)on capacity along with MTO and CTO efforts.

40 Conclusions 1) Propane and Ethane will be sourced along the Gulf Coast and in the Marcellus and U)ca shale plays. The bulk of exis)ng US steam crackers (~31) and polymeriza)on capacity is along the Gulf Coast. We expect the bulk of new cracker capacity to be installed there as well. 2) New capacity will also be seen in the northeast. Shell announced a new facility in Pennsylvania based on Marcellus/U)ca NGLs. Mariner West Pipeline will deliver NGLs to Sarnia, Ont. While another export pipeline will support Western Canada. A third pipeline, Mariner East, will service the new Marcus Hook liquefac)on and export facility. 3) Beyond North American consump)on, propane, propylene, ethane, ethylene and polymer chips will all be exported from the US. 4) Depending on polymer economics, interna)onal petrochemical companies should con)nue to convert from Naphtha to Ethane/Propane as primary feed stocks for ethylene produc)on. 5) Don t forget China s effort to produce olefins from Methanol and from Coal.