The World of Energy Behind and Beyond Forecasts

|

|

|

- Lucas Barton

- 5 years ago

- Views:

Transcription

1 The World of Energy Behind and Beyond Forecasts Houston Kristine Klavers 28 February 2018 London Houston Moscow Singapore Dubai New York Beijing Kiev Tokyo Astana Shanghai Rio de Janeiro Washington DC Riga Calgary Brussels Cape Town Mexico City Berlin San Francisco Sydney Market Reporting Consulting Events

2 Argus Media group notices 2 The Argus Media group (referred to herein as Argus ) makes no representations or warranties or other assurance, express or implied, about the accuracy or suitability of any information in this presentation and related materials (such as handouts, other presentation documents and recordings and any other materials or information distributed at or in connection with this presentation). The information or opinions contained in this presentation are provided on an as is basis without any warranty, condition or other representation as to its accuracy, completeness, or suitability for any particular purpose and shall not confer rights or remedies upon the recipients of this presentation or any other person. Data and information contained in the presentation come from a variety of sources, some of which are third parties outside Argus control and some of which may not have been verified. All analysis and opinions, data, projections and forecasts provided may be based on assumptions that are not correct or which change, being dependent upon fundamentals and other factors and events subject to change and uncertainty; future results or values could be materially different from any forecast or estimates described in the presentation. To the maximum extent permitted by law, Argus expressly disclaims any and all liability for any direct, indirect or consequential loss or damage, claims, costs and expenses, whether arising in negligence or otherwise, in connection with access to, use or application of these materials or suffered by any person as a result of relying on any information included in, or omission from, this presentation and related materials or otherwise in connection therewith. The information contained in this presentation and related materials is provided for general information purposes only and should not be construed as legal, tax, accounting or investment advice or the rendering of legal, consulting, or other professional services of any kind. Users of these materials should not in any manner rely upon or construe the information or resource materials in these materials as legal, or other professional advice and should not act or fail to act based upon the information in these materials.

3 Agenda 3 1. What is an energy Price Reporting Agency? 2. Forecasting of energy fundamentals 3. Feedstocks and products trends and outlook 4. How do market forecasts support energy related investment decisions? 5. Concluding thoughts About Argus

4 The World of Energy Behind and Beyond Forecasts What is an energy Price Reporting Agency? Market Reporting Consulting Events

5 What is a Price Reporting Agency (PRA) 5 Publishers of commodity market data Prices, reports and databases Informed comments, analysis and news Provide definition to non-standard (spot) physical markets Define the methodology of published prices and ensure it is transparent Define the basis, location, size, time period and specification of the contract being assessed or reported Collect, collate, clarify and verify market information Explain and justify decisions Operate according to best practices and IOSCO Principles

6 How does the PRA system work? 6 Commodity trading companies voluntarily submit pricing or transaction data to the publisher by phone, , IM, trading platforms, etc. Publishers validate and organize the data and create price assessments, making sure published methodology is used. These price assessments are offered to the industry on a subscription basis. Indices are used in: Term contracts - Financial derivatives Financial reporting - Internal transfer pricing, etc. In petroleum, about 10% of physical moves on spot, and 90% on contracts tied to published index prices

7 Who are the PRAs? 7 Globally recognized energy related PRAs are: Argus ICIS OPIS Platts In addition, some entities are not PRAs but do provide commodity price references, such as the CME and Ice s trading platforms, as well as Thomson Reuters, The Wall Street Journal, Bloomberg, Global View, etc.

8 Argus Media Inc. and Argus Consulting Services staff members in 21 global offices Publishes 11,000+ daily spot and forward price assessments Publisher of commodity prices, data and statistics, with consultancy services and conferences.

9 The World of Energy Behind and Beyond Forecasts Forecasting of energy fundamentals Market Reporting Consulting Events

10 Forecasting is an art 10 Source: EIA

11 Scenario based forecast Offers more value than single, most likely forecasts. Gives the opportunity to pick a preference or probability, weight the various scenarios or perform stress tests by combining the forecasts with their business model. Provides better insights than a traditional sensitivity analysis because no single variable ever changes alone. There is significant correlation between common valuation variables. Light Crude Oil History and Forecast (Yearly average nominal prices) $120 $110 $100 $90 $80 $70 $60 $50 $40 $30 $20 Brent/NSD (high demand case) Brent/NSD (base case) Brent/NSD (high supply case) HIGH DEMAND HIGH SUPPLY

12 Our crude oil price forecast process 12

13 Forecast risk issue identification and development 13 Typical risk issues considered for crude oil Geopolitical event Production and refining process technology development Transportation technology development (vehicles) Tariffs Regulatory change (e.g., emissions, MARPOL VI) Forex Recession GDP shift and/or CPI Inflation Logistics availability Environmental and pandemic events

14 The World of Energy Behind and Beyond Forecasts Feedstocks and products trends and outlook: - Crude production, demand, price and export - Gasoline and diesel production, demand and trade - Electric vehicles - Gas/LNG - LPG/NGLs - Petrochemicals - Not included are biofuels, asphalt, petcoke Market Reporting Consulting Events

-Regulations")

15 15 The integrated world of energy GAS NGL Methanol LNG LPG Variables Products Offshore & Onshore CRUDE Gasoline Jet Diesel -Demand (GDP) -Regulations -Technology -Price -Logistics -Alternatives Variables Feedstock Fuel Oil -Demand -Quality -Price Coker VGO Asphalt Base oil Petcoke

16 Global GDP growth underpinned by Asia-Pacific % 5.0% 4.0% China and India % 2.0% 1.0% 0.0% Africa Asia Pacific Europe FSU Middle East North America South America Source: World Bank; 10 year CAGR

17 Global oil demand, supply and cumulative oversupply 17

18 Crude oil prices 18

19 Top global crude oil producers 19 Source: Argus, eia 2017 data are yearly average production rates, through October

20 US crude oil exports soar after ban lifted 20 Source: Argus, eia 2017 data are average through October

21 Houston export market developing rapidly 21 Source: Argus Media Inc.

22 22 Worldwide, both distillate and gasoline growth are robust mn b/d G/D ratio CAGRs 2000 to to 2017 Gasoline 2.61% 1.80% Distillate 0.29% 1.34% CAGR compound annual growth rate Gasoline Distillate G/D Demand Ratio Data from IEA, EIA and Argus

23 US gasoline and blendstock export destinations 23 Source: Argus, eia

24 24 US diesel export destinations 000 bpd 1,200 1, Latin America China & Singapore Canada Europe Other Source: Argus, eia

25 Effects of electric vehicle (EV) development mln North America 400 mln Europe 1,500 mln Asia-Pacific , Source: OICA, Argus, regional associations

26 New inventions need to meet scale 26

Feedstock Wax Asphalt 35,000ppm >30")

27 Production chain and drivers 27 Products Old S specifications New S specifications Crude - Quality - Prices - Availability Light gases Light distillates LPG NGLs Petrochemicals Gasoline Naphtha 30ppm 10ppm - Medium - Heavy - Light Medium distillates Kerosene/Jet fuel Gas oil Diesel 500ppm 15ppm Heavy ends Heavy fuel oils Base Oil (II) Feedstock Wax Asphalt 35,000ppm >30 ppm 5,000ppm <30 ppm

will increase There will be")

28 28 Far reaching impacts from MARPOL bunker change What is MARPOL? Marine Pollution International Convention for the Prevention of Pollution from Ships MARPOL Annex VI limits bunker fuel sulfur to 0.5% on 1 January 2020 MARPOL will likely be the most significant event in decades The shipping industry is responsible Demand for low sulfur fuels (and light/sweet crudes) will increase There will be winners and losers Gasoline and other feedstocks will also be affected MARPOL s biggest unknown is the level of non-compliance

29 Natural gas demand growth Bcm Global natural gas demand Rest of World 800 US Middle East Europe Russia China Asean India Source: eia

30 Bcf/d US LNG capacity under construction 30 Ramp-up timeline Date Project Company Sabine Pass Cheniere Energy Cove Point Dominion Energy 8 Peak Baseload 2018 Elba Island Kinder Morgan Feb-2016 Feb-2017 Feb-2018 Feb Freeport Freeport LNG 2019 Corpus Christi Cheniere Energy 2019 Cameron Sempra Energy 2019 Sabine Pass Cheniere Energy Source: Argus

31 US will have third largest LNG capacity by Bcf/d Papua New Guinea Russia Trinidad and Tobago Algeria Indonesia Nigeria Indonesia US Australia Qatar Source: Argus

32 32 Nomenclature Gas, LPG, NGL, propane, butane, etc. Methane (C 1 H 4 ) Dry gas or natural gas Ethane (C 2 H 6 ) Natural gases Propane (C 3 H 8 ) Butane (C 4 H 10 ) Isobutane (C 4 H 10 ) LPG NGLs Pentanes (C 5 H 12 ) Naphtha Natural gasoline Condensate Heavier fractions Non-hydrocarbon gases such as: CO2, H 2 O, H 2 S, N 2, etc. International Energy Agency

33 Global LPG production by source 33 mn t 350 Refinery Production Gas Processing Argus Consulting Notes: 2016 data is provisional

34 Asia is the key center of incremental demand 34 mn t US Europe Asia-Pacific Latin America Africa Argus Consulting, 2017

35 Global outlook for LPG consumption by sector 35 mn t Residential Agricultural Industrial Commercial Transport Refinery fuel Petrochemical Other non-energy Consumption Argus Consulting, 2017

36 The next decade will be long LPG 36 Global LPG structural balance, mn t Total Consumption Total Production Net Position Argus Consulting, 2017

37 Petrochemical investments continue to grow 37 37

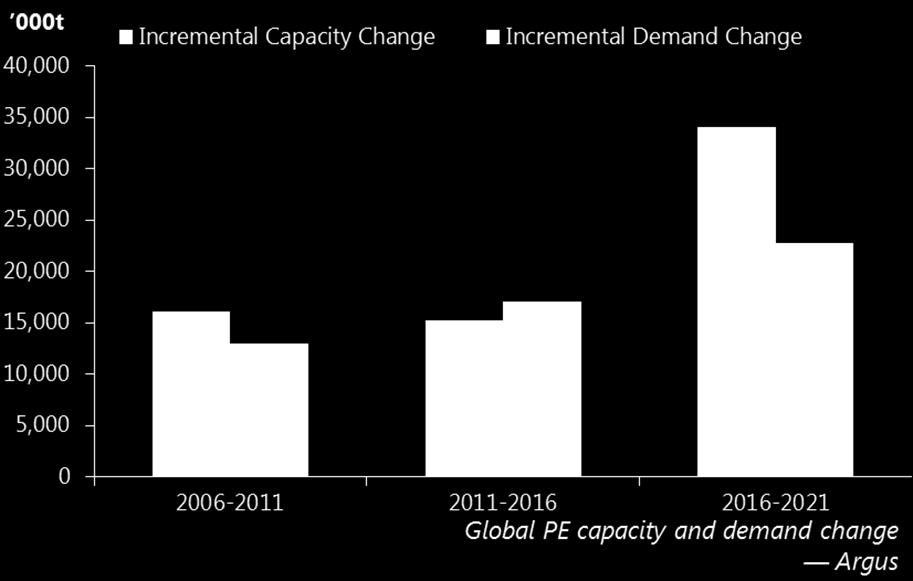

38 Global ethylene capacity growth mn t mn t

39 The World of Energy Behind and Beyond Forecasts How do market forecasts support energy related investment decisions? Market Reporting Consulting Events

40 40 Analysis required for investments To raise capital for new energy related investments you need: Technical Due Dilligence Investment Market Analysis Legal Analysis

41 The World of Energy Behind and Beyond Forecasts Concluding thoughts Market Reporting Consulting Events

42 42 Concluding thoughts PRAs own their market fundamentals data. Forecasting is an art: You need an experienced multifaceted expert to lead forecasts. Scenario-based forecasts are more powerful and useful than single line forecasts. Risk issue identification and development is critical. It all starts with refined product demand forecast. Shale exploration transformed US. Chinese growth shapes the world of energy. Refining competition has turned global, not just local. Alternative sources are growing and help shape our world of energy. Escalating global product trade will set price relationships. Every molecule counts!

43 London Houston Moscow Singapore Dubai New York Beijing Kiev Tokyo Astana Shanghai Rio de Janeiro Washington DC Riga Calgary Brussels Cape Town Mexico City Berlin San Francisco Sydney

400-7860 Houston www.argusmedia.com http://blog.argusmedia.com Stay Connected @ArgusMedia +Argusmediaplus Argus-media argusmediavideo Copyright notice Copyright 2018 Argus Media group.")

44 Kristine Klavers Senior Vice President, Consulting Americas +1 (713) Houston Stay +Argusmediaplus Argus-media argusmediavideo Copyright notice Copyright 2018 Argus Media group. All rights reserved. All intellectual property rights in this presentation and the information herein are the exclusive property of Argus and and/or its licensors and may only be used under licence from Argus. Without limiting the foregoing, you will not copy or reproduce any part of its contents (including, but not limited to, single prices or any other individual items of data) in any form or for any purpose whatsoever without the prior written consent of Argus. Trademark notice ARGUS, the ARGUS logo, Argus publication titles, and Argus index names are trademarks of Argus Media Limited. For additional information, including details of our other trademarks, visit argusmedia.com/trademarks.