Global LNG Dynamics and South East Mediterranean Hydrocarbons Potential

|

|

|

- Christina Black

- 5 years ago

- Views:

Transcription

1 Global LNG Dynamics and South East Mediterranean Hydrocarbons Potential Athanasios Pitatzis! Workshop of SPE Kavala Section activities and EMaTTech research advances! Global Oil&Gas: Black Sea & Mediterranean Exhibition and Conference Athens,Greece,23/09/2015

2 Presentation s Contents Global LNG Dynamics Facts and Data South East Mediterranean Hydrocarbons Potential Connect East Mediterranean Producers with International Gas Markets via: 1. CNG FCNG Cargos 2. FLNG LNG Cargos 3. Pipelines

3 Global LNG Dynamics The chart above illustrates the dynamics of the global LNG prices from May 2013 to July 2015

4 Global LNG Dynamics

5 Global LNG Dynamics LNG trade reached its second historical high, totaling some MT the last year, in comparison with the recent years has decrease only 0.4 MT Spot LNG prices in the Asia Pacific and the Atlantic for September 2015 delivery being concluded at approximately $8.00/MMBtu. Also according to the FGE Energy Consultants and Bloomberg LNG prices may sink as low as $4 per million British thermal units by 2017 because of a glut and probably won t rise above $8 before Global LNG market dominated by oil-indexed import contracts (74% versus 26% GOG), GOG competition has been growing particularly in liquid Northwest European gas markets such as those of UK, Belgium, Denmark, Germany, Ireland and Netherlands

6 Global LNG Dynamics According to the international media US LNG export contracts linked to the Dutch TTF instead of the US Henry Hub due to the difference in the price, $6 7/MMBtu VS $2-3/MMBtu USA Shale gas output increased the last years with final outcome additional LNG volumes coming on market from the USA. In the same time Europe seems an emerging market for US LNG due to the decrease on European gas production due to the decrease from Groningen gas field in the Netherlands

7 Global LNG Dynamics According to the International Gas Union:

8 Global LNG Dynamics According to the International Energy Agency:

9 Global LNG Dynamics According to the International Energy Agency:

10 South East Mediterranean Hydrocarbons Potential Greece upstream sector Cyprus upstream sector Israel upstream sector Lebanon upstream sector Egypt upstream sector

11 Prinos oil Field is the only producing reservoir in Greece Recent oil and gas exploration blocks was acquired by Energean Oil and Gas and Hellenic Petroleum Further efforts to attract foreign investors to invest in Greece oil and gas sector Introduce national strategy for the exploration and exploitation of hydrocarbons of the Greek Exclusive Economic Zone Greece

12 Aphrodite gas field is the only proven gas reservoir in Cyprus First priority for the country must be the development of Aphrodite gas reservoir by the companies and the connection of this field with international gas markets Further efforts to attract foreign investors to invest in Cyprus oil and gas sector Introduce a national strategy for Cyprus to become in the future a regional natural gas hub Cyprus

13 Border Issues with Israel regarding their exclusive economic zones Security issues, the country is located near to Syria Delays on the offshore license round which had launched since 2013 Improve the efficiency of oil and gas government and regulatory agencies Introduce national strategy for the exploration and exploitation of hydrocarbons of the Lebanon Exclusive Economic Zone Lebanon

14 Israel B o r d e r I s s u e s w i t h L e b a n o n regarding their exclusive economic zones Security issues, the country is located near to Syria Improve the efficiency of oil and gas g o v e r n m e n t a n d r e g u l a t o r y agencies, for instance the dispute between Noble Energy and Delek with antitrust authority of Israel Introduce national export strategy for Israel proved oil and gas reserves Source: Offshore Energy Today

until 1th of January 2015 Egypt holds 77 trillion cubic feet (Tcf) or 2,188 trillion cubic meters of proved natural gas reserves New discovery of")

15 According to Oil and Gas Journal and to U.S Energy Information Administration (EIA) until 1th of January 2015 Egypt holds 77 trillion cubic feet (Tcf) or 2,188 trillion cubic meters of proved natural gas reserves New discovery of Zohr gas field (30 Tcf) Introduce national strategy for the development of Egypt s proved natural gas reserves, the dilemma of allowing exports? Egypt

16 East Mediterranean gas producers International gas markets Geopolitical Issues Commercia l Issues Political Issues. Security Issues

17 Aphrodite gas field - Cyprus Natural Gas Reservoirs of East Mediterranean Tamar gas field - Israel Leviathan gas field - Israel Zohr gas field - Egypt 5 Tcf 10 Tcf 22 Tcf 30 Tcf

18 East Mediterranean LNG Option for Exports The following options were mostly discussed during the last years: 1. To combine the Leviathan and Aphrodite volumes and ship LNG from the Vassilikos LNG facility in Cyprus 2. To transport gas to Egypt, Idku, and re-export it to the EU (liquefying it, shipping to Europe and re-gasifying) Main Markets to export East Mediterranean gas are Europe and Asia Pacific region

19 East Mediterranean Pipelines Option East Mediterranean proposal pipelines projects: 1. East Med, technical difficulties regarding the construction and operation due to deep depth of the sea in the region 2. Pipeline from Cyprus to Turkey, geopolitically almost impossible scenario 3. Connection via undersea pipelines Cyprus and Egypt and Israel with Cyprus, strategic investment, promotes the cooperation between the 3 countries

As the construction of the Coselle CNG ship was recently approved by the American Bureau of Shipping, this technological solution does make CNG an economical and flexible option for seaborne")

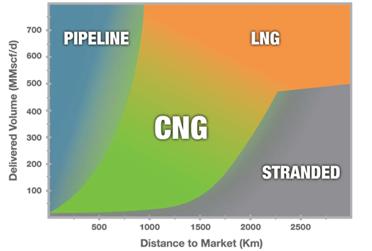

20 East Mediterranean CNG Option The commercially viable and politically neutral solution to export small volumes of natural gas (>5tcf) from Cyprus to Turkey seems to be Floating Compressed Natural Gas (FCNG) As the construction of the Coselle CNG ship was recently approved by the American Bureau of Shipping, this technological solution does make CNG an economical and flexible option for seaborne transportation of natural gas for distances of maximum 2,500 km From the security point of view for FCNG vessels are fit exactly for East Med region because can be located far from the coastline and therefore are not exposed to the same risks of terrorist activity as onshore infrastructure Source: Sea NG

21 East Mediterranean CNG Option According to the Sea NG: Offshore Gas Production using CNG Ships and/or FLNG The production vessel (or platform) is conventional and can be used for both CNG and FLNG Instead of compressing gas into a pipeline, reservoir gas is compressed into CNG ships on a continuous basis

22 East Mediterranean CNG Option

23 Source: Sea NG East Mediterranean CNG Option

24 Regional net-backs CNG vs. LNG vs. FLNG vs. Pipeline Source: Sea NG

25 Evaluate the regional and international market dynamics East Mediterranean Business Gas Export Strategy Evaluate the regional geopolitical landscape Implementation of the Business Gas Export Strategy

26 Conclusion To unlock the full potential of East Mediterranean Hydrocarbons we need to use for the transportation of natural gas to regional markets the CNG technology and to international markets the LNG solution via Egypt or via Vassilikos Terminal on Cyprus (proposed for construction) East Mediterranean gas producers has an open window opportunity to develop the existing gas fields until 2020 The topic energy security will play a significant role for countries like Israel and Egypt regarding their oil and gas policies

27 References Part of the information for this presentation derived from the article Games Changers for LNG markets in the East Mediterranean: A New Market Environment for the Emerging Exporters in the Region which was published on the website European Energy review on 9 th of September 2015 Article Coordinator: Daria Nochevnik is Chief Analyst Natural Gas and LNG for European Energy Review and Deputy Head for Greek Energy Forum on Brussels Coauthor: Athanasios Pitatzis, Industrial/Petroleum Engineer, Oil and Gas Analyst and member of Greek Energy Forum and SPE Kavala Section

28 Questions