THE PETROLEUM INDUSTRY RESETS: PERSPECTIVES ON THE ROAD AHEAD

|

|

|

- Alaina Shaw

- 5 years ago

- Views:

Transcription

1 THE PETROLEUM INDUSTRY RESETS: PERSPECTIVES ON THE ROAD AHEAD Oklahoma Independent Petroleum Association Annual Meeting Las Colinas, Texas June 12, 2016 Pete Stark, Senior Research Director and Advisor Steve Trammel, Research Director and Advisor 2016 IHS. ALL RIGHTS RESERVED.

2 A Great Energy Shakeout The year 2016 has been one of survival and opportunity. The oil, gas, and coal industries all face low prices and overcapacity. Economic growth, policy uncertainties and volatility are at record levels. Costs and technology are changing at unprecedented speeds. With advent of US shales, reactivity of supply to prices was transformed into a three layered supply equation: New strategies by low-cost producers in the Gulf Middle East To Freeze or Not to Freeze, that is the question. High reactivity US shales creating short response cycles to prices A low reactivity global system, with long-cycle decisions and outcomes 2

3 Key messages for the global crude oil market Eying a move from glut to balance: The role of price sensitive and political barrels The global oil market will move from supply glut to balance, with this turning point to begin in the third quarter. Next quarter seasonal demand strength will push world liquids demand above liquids supply for the first time since Continued production declines of price-sensitive barrels especially US tight oil are critical to this transition. This is a slow process and, looking to 2017, the market is expected to stay roughly balanced limiting upward price pressure. IHS projects Dated Brent will average about $50/bbl in 3 rd Qtr and $52/bbl in (Increased volatility) Greater-than-expected growth in production of political barrels could prolong the supply glut. Production changes in Iran, Libya, and other areas are not price sensitive they depend on political decisions that could lead to large upward swings in output levels, and in short order. Iran will lift its crude oil output somewhat further in the near-term to 3.6 MMb/d by mid-2017, up from an estimated 2.9 MMb/d in January, when sanctions were lifted. Saudi Arabia to boost oil production by 100 Mb/d during 2 nd half 2016 and by another 300 Mb/d in with less spare capacity. Low end of the cost curve is expanding and outlook for U.S. recovery is extended. Gulf 5 to add > 2 MMb/d by US crude-oil production is expected to fall from 9.1 million barrels per day (MMb/d) in first quarter 2016 to 8.5 MMb/d in early 2017 a six month delay from April 2016 outlook. Upside price risks now more prominent than downside (Nigeria 700 Mb/d; Canada 1.1MMb/d; Brazil, Venezuela, US growth lowered through Despite a lackluster global economy, strength in US and China gasoline consumption and Indian liquids demand continues to underpin global liquids demand growth. Global liquids demand will rise by about 1.1 MMb/d in 2016 growth that is critical to reducing the global supply overhang. Major structural changes to global oil market challenge E&P strategies going forward. Low-cost oil supplies increase at expense of high cost oil. More power to big producers. Reduced spare capacity increases risks of price volatility. Access to capital with uncertain company valuations is a major challenge. 3

4 Global Oil Markets Long Term Price and Margins Update / First Quarter 2016 Snapshot of global oil fundamentals and prices Snapshot of global oil fundamentals and price outlook FUNDAMENTALS PRICES World economic growth 2.5% 2.7% 2.6% 2.6% 3.1% (from previous year) World oil (liquids) demand growth* (from previous year in MMb/d) Non-OPEC liquids supply growth* (from previous year in MMb/d) Call on OPEC crude* (annual average in MMb/d) OPEC production* (annual average in MMb/d) Dated Brent $ 109 $ 99 $ 52 $ 44 $ 52 (annual average per barrel) WTI $ 98 $ 93 $ 49 $ 43 $ 50 (annual average per barrel) *This outlook is based on our April 2016 balances, which we plan to release along with our monthly Global Crude Oil Markets Market Briefing. Notes: OPEC production includes production from all current members (including Indonesia). Liquids supply includes crude oil, condensate, and natural gas liquids (NGLs). Liquids demand includes all refined products, blended biofuels, synthetic fuels, as well as liquefied petroleum gases (LPGs) and ethane. Call on OPEC crude = total global liquids demand - non-opec liquids supply - OPEC condensate and NGL supply - processing gains - biofuel supply - other liquids supply. OPEC spare capacity is for crude oil only. Figures are rounded. MMb/d = Million barrels per day. Source: IHS, Argus Media Limited 2016 IHS 4

5 Regional economic growth outlook Percent growth in real GDP Regional real GDP growth rates rates in in Global economic growth remains sluggish 2.3% in 2016, with real North America 2.2% 2.7% world GDP projected to remain flat with % at 2.6%, rising to United States 2.3% 2.8% 3.1% in 2017, and 3.2% in Reinforces 1.9% the view that global Europe 1.8% 2.1% economy not headed for recession OECD Asia Pacific -2.7% Eurasia -1.0% 1.2% 4.8% Non-OECD While global Asia (ex China) financial volatility could return at any time, 5.0% the 5.3% fundamental drivers of continued growth are still in place 6.9% China 6.3% 6.3% Upward 2.4% Middle pressures East on headline inflation will 2.1% likely be small, 3.2% especially in With most commodities facing a market still -0.4% Latin America -0.5% 1.7% characterized by structural oversupply albeit 2.8% diminishing any Africa 2.9% 3.6% increase in prices in 2016 will be limited 2.6% World 2.6% 3.1% Negative interest rates in the developed world are helping to ease pressures on emerging-market currencies. 1.3% 1.4% 1.5% -4% -2% 0% 2% 4% 6% 8% Percent growth in real GDP Financial 2015markets have become 2016 much less 2017 pessimistic since mid- Notes: Global GDP growth calculated using real local currency growth rates, aggregated using real exchange rate-based weights. North America includes the United States and Canada. Latin America includes Mexico. February Source: IHS 2016 IHS 5

6 MMb/d Supply growing faster than demand set the stage for the oil price crash and is still pressuring markets in 2016 Liquids demand vs. supply annual growth Demand Supply OPEC Supply Over-supply Non-OPEC Supply Notes: Liquids supply includes crude oil, condensate, and natural gas liquids (NGLs). Liquids demand includes all refined products, blended biofuels, synthetic fuels, as well as Strong supply growth in 2014 and 2015 crashed oil prices Non-OPEC supply growth mainly US unconventionals, which alone grew twice as fast as global 2014 demand OPEC countries also increased supply in 2015: Saudi Arabia and Iraq Markets begin to tighten in 2016 Non-OPEC declines in response to very low prices OPEC increases as Iranian barrels begin to come back Growth beyond 2017 assumes improved average GDP and improved average annual oil demand vs, supply additions 6

7 United States Brazil Canada Indonesia Colombia India Argentina Kazakhstan Norway United Kingdom Oman Russia Azerbaijan China Mexico Million barrels per day The US, Canada and Brazil account for virtually all Non- OPEC supply growth Non-OPEC crude oil production annual change Outside of North America and Brazil, the rest of Non- OPEC has not been able to increase overall net production Reduced maintenance and project delays are likely to further impact Non-OPEC supply by 2017 US production growth slowed dramatically in 2015, and will decline in Notes: Data are for 15 largest non-opec crude producing countries in Source: IHS 7

8 Million barrels per day OPEC spare capacity Thin spare capacity (2% of world oil market) will become a serious issue in late-2016 with increased risk of price spikes and volatility OPEC spare crude oil production capacity Source: IHS 2016 IHS 8

9 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Global production outages remain high, which might add downside risk if reversed Global production outages ('000 b/d) Libya -1,000-1,500 Iran -2,000 Iraq -2,500 Nigeria -3,000 Non OPEC -3,500 Saudi, Kuwait -4,000 Source: IHS, EIA 2014 IHS Oil production offline remains historically high at nearly 3.5 million barrels/day Libya > 1 million b/d Iran ~750 thousand b/d. How many b/d added in 2016? Other countries, OPEC (Nigeria, Neutral Zone) and non-opec (S. Sudan) add another 1.5 million b/d offline. IHS does not see a likelihood of countries other than Iran adding supply in but 9

10 Million barrels per day US crude oil production Declines expected to continue for the next three months as sharp drop in activity reverberates across the US onshore Monthly US crude oil production Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 History Outlook Source: EIA (history through January 2016); IHS (estimates for February 2016 and March 2016, and outlook) 2016 IHS 10

11 US supply system reacts Capital discipline Cost-cutting initiatives Workforce reductions Rig cancellations Focus on standardization US is the fastest responding supply system weeks or months not years The wide range of well productivity creates opportunity for significant play selectivity & high-grading in the US onshore Cost reductions by service companies greatest and quickest in the US onshore Productivity improvements in the US onshore are still occurring Company positions vary greatly acreage quality and for US tight oil, cash suffocation and empty wallets trump full portfolios 11

12 Capital efficiency gains resetting the US onshore system, but were slowing as of Q US crude production since peak rig count 000 b/d 9,600 9,500 9,400 9,300 9,200 9,100 9,000 8,900 8,800 8,700 8,600 Source: IHS Energy, Baker Hughes, EIA US production # oil rigs # oil rigs 1,800 1,600 1,400 1,200 1, Cumulative US onshore cost reductions US oil production rose from 6 million b/day in January 2011 to 9.6 million b/d in spring The sharp drop in oil rigs was expected by many to slow US production and used as a leading indicator. Decline in costs and high-grading allowed for huge capital efficiency gains (65%) and mitigated the supply impact from cut in oil rigs. US onshore production decreased in the second half of 2015 and will continue into Gulf of Mexico deepwater production increased in 2015 and will continue to grow slowly from sanctioned projects. 12 0% -5% -10% -15% -20% -25% -30% -35% -40% Source: IHS/PacWest 14Q4 15Q1 15Q2 15Q3 15Q4

13 Stack Play getting more stacked, but limited drilling has not exposed a clear sweet spot Horizontal drilling has been reported in four primary formations: Oswego, Meramec, Osage, and Hunton Good and poor performing wells are scattered across the STACK play fairway. The most favorable trend established to date is the NW-SE fairway in NE Kingfisher County with a number of 1st and 2nd quintile wells in Hunton, Oswego and Mississippi Lime reservoirs. Too few wells have been drilled to delineate clear sweet spots or clear non-commercial trends. Delineation of the most favorable horizons and geography will require substantial additional drilling. 13

14 Anadarko Basin Woodford: Sweet spots and productivity gains Similar to peak rates, normalized productivity has been increasing since operators began developing the SCOOP. Normalized productivity rates have risen nearly 50% since Continental entered the subplay, although the Traditional Cana had modest gains over the same period. Productivity in the Ardmore subplay has, on average, held constant until recently, giving way to declining productivity, suggesting migration to less prospective areas in the subplay. 14

15 64% of new US onshore production breaks even at <= $50/barrel WTI (including a 10% return) WTI $/barrel breakeven ranges: 2014 new volumes at estimated 2015 well costs Above $60 $50-$60 $40-$50 $30-$40 <$30 Source: IHS Bakken Shale Permian Horizontals Thousands barrels/day Eagleford Shale Other Plays IHS analyzed 3.2 million bbl/d of new onshore production in 2014 to estimate the WTI price needed to break even (including a 10% return) at 2015 cost levels, which are expected to be 30% below 2014 costs. In the 2015 cost structure, new US onshore production breakeven economics: 64% <= $50/barrel WTI 46% <= $40/barrel WTI IHS expects US production will fall at < $45 WTI from the peak about 9.6 million b/d to about 8.7 million b/d by June

16 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 Quarterly average price per barrel Benchmark crude price outlook Prices expected to slowly recover from 1Q 2016 low with Dated Brent to average about $41/bbl for full year 2016 and $49/bbl in 2017 Brent and other benchmark crude price outlook to 2017 $140 $120 Outlook Assumptions Oil prices remain low enough to keep pushing US crude production lower in the coming months $100 $80 $60 $40 No coordinated production cuts by the governments of OPEC/non-OPEC countries in the near-term Global liquids demand remains relatively robust at about 1.2 MMb/d Price outlook risks $20 $0 Upside: Non-OPEC, non-us crude production falls more rapidly than expected in response to lower prices Source: IHS Dated Brent LLS WTI 2016 IHS Downside: Crude output from Iran, Libya, or the Neutral Zone rises more than anticipated; US crude production more resilient than expected Benchmark crude price outlook (dollars per barrel) 3Q Q Q Q Q Q Q Q Q Q Q Q Q Q 2017 Dated Brent $ $ $ $ $ $ $ $ $ $ $ $ $ $ LLS $ $ $ $ $ $ $ $ $ $ $ $ $ $ WTI $ $ $ $ $ $ $ $ $ $ $ $ $ $ Source: IHS, Argus Media Limited 2016 IHS 16

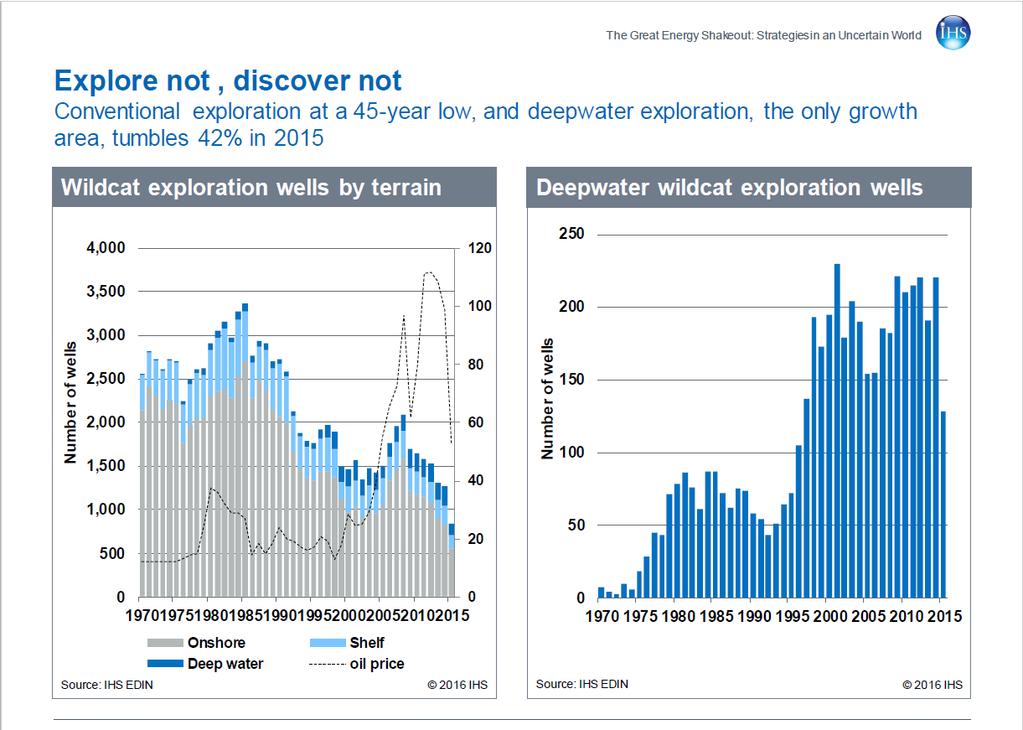

17 17

18 Many tight conventional plays compare well with the nine leading shale plays Average IP rate (boe/d) Horizontal wells drilled Leading shale and tight conventional oil plays: Average 24-hour IP rates and number of horizontal wells drilled between 1 January 2010 and 25 June ,400 1,200 1, S S S S S S S S Average gas IP (boe/d) Average oil I/P (b/d) Number of horizontal wells S designates shale plays. Others are tight conventional plays. S 9,000 8,000 7,000 6,000 5,000 4,000 3,000 2,000 1,000 0 Source: IHS The leading tight conventional plays have IP rates that compare well with the leading shale plays. However, of the 26,232 wells represented on this chart, only 10% have been drilled in the tight conventional plays. This suggests considerable upside potential in the tight conventional plays should the activity levels increase to that of the shales. 18

19 World oil (liquids) demand growth to average 1.2 MMb/d in 2016 and 1.4 MMb/d in

20 Refilling the hopper: Roughly 40 million b/d of new crude production needed by 2030 to offset declines and meet new demand The price collapse is not permanent Future barrels are going to be more expensive to find and produce 2016 IHS IHS upstream project and cost analysis indicate a price of $100/Bbl is needed by 2025 to provide needed supply growth, even as upstream costs reset at a lower level 20

21 The Natural Gas Market Weathering Excess Supply U.S. gas producers explore new markets to absorb surplus supplies--the gradual recovery in supply demand balance continues to drag Multiple factors indicate that oversupplies and price pressure will remain well into 2016 but with a brighter prospect for the future For U.S gas storage levels-- High gas production along with mostly milder-than-normal weather has induced low winter-to-date storage withdrawals, resulting in a U.S. Lower 48 inventory surplus of more than 728 Bcf relative to the five-year average. Injection began March 11! Expected production cuts over the next several months, owing to low prices, will further reduce injections. IHS Energy expects the end-october inventory to reach 4,077 Bcf still an end-october record At current prices, little or no additional coal-to-gas switching is possible, and production declines will be required to balance the market. Exports and power demand underpin demand growth After a Fall inventory maximum, which could still stress capacity (at 4,115 Bcf max), the gas market tightens significantly. To support demand growth, a production increase is required. Prices rise significantly: $2.10 in 2016; $2.86 in

22 Gas Storage Inventory Price Projections 22

23 1/1/2006 6/1/ /1/2006 4/1/2007 9/1/2007 2/1/2008 7/1/ /1/2008 5/1/ /1/2009 3/1/2010 8/1/2010 1/1/2011 6/1/ /1/2011 4/1/2012 9/1/2012 2/1/2013 7/1/ /1/2013 5/1/ /1/2014 3/1/2015 8/1/2015 1/1/2016 6/1/ /1/2016 4/1/2017 9/1/2017 Lower 48 associated gas production Porting shale technology from gas to oil Driving rapid expansion of associated gas production but starting to fall with oil Lower 48 associated gas production growth relative to January Actual Forecast Source: IHS 23

24 Bcf/d Full US gas production with associated gas Lower 48 total total gas production Marcellus PA 10 - Associated gas Associated Gas Marcellus PA Marcellus WV Utica Barnett Fayetteville Haynesville Smaller Plays DUCs Other - Dry Gas Other - Wet Gas CBM GOM Deep GOM Shelf Source: IHS 24

25 Bcf/d Dry gas production dependent on the associated gas outlook Lower 48 associated gas production Eagle Ford 5 0 Permian Conventional Cotton Valley Anadarko Penn Anadarko Wash Woodford - Cana Woodford - Ardmore SCOOP Bakken Cotton Valley Eagle Ford Mississippian Lime Permian Conventional Permian Unconventional Wattenberg Niobrara Fracture Play Other - Gassy Oil Other - Oil Source: IHS 25

26 Bcf/d Sustained lower prices and increasing focus on capital discipline keeping a lid on near-term production growth Lower 48 total total gas production Marcellus PA Marcellus WV Utica Barnett Eagle Ford Fayetteville Haynesville Permian plays Smaller plays DUC Other - Dry Gas Other - Wet Gas Other - Gassy Oil Other - Oil CBM GoM Deep Source: IHS Marcellus PA Marcellus and Utica shales are primary drivers of production growth. Productivity gains outstrip infrastructure growth in the near term, keeping the regional basis depressed. IHS projections for two quarters of sub-$45 WTI oil prices is a major component of the outlook for associated gas. Increased focus on capital discipline in 2016 in both oil and gas directed drilling will be a key factor affecting development plans and rig counts. 26

27 More than 1,400 Tcf of gas resource has a Henry Hub break-even price of $4/MMBtu or less Costs are falling Volumes are rising IHS estimates total North American resources in excess of 4,000 Tcf 27

28 Bcf/d Bcf/d New US lower-48 supply outlook focuses more production growth in Appalachia October 2015 US lower-48 natural gas productive capacity outlook September 2015 US lower-48 natural gas productive capacity outlook Other Bakken Barnett Cotton Valley Eagle Ford Fayetteville Haynesville Marcellus Major Permian Plays Pinedale/Jonah Utica Woodford/SCOOP Other Bakken Barnett Cotton Valley Eagle Ford Fayetteville Haynesville Marcellus Major Permian Plays Pinedale/Jonah Utica Woodford/SCOOP Source: IHS Energy, IHS North American Supply Analytics, IHS North American Performance Evaluator Source: IHS Energy, IHS North American Supply Analytics, IHS North American Performance Evaluator 28

29 Bcf/d Bcf/d The Marcellus and Utica continue to show how prolific they are, growing significantly in the new outlook Marcellus productive capacity forecast Utica productive capacity forecast September Marcellus October Marcellus September Utica October Utica Source: IHS Energy, IHS North American Supply Analytics, IHS North American Performance Evaluator Notes: Major Permian plays include Bone Spring, Spraberry, Wolfcamp Delaware, and Wolfcamp Midland Source: IHS Energy, IHS North American Supply Analytics, IHS North American Performance Evaluator 29

30 Utica and Marcellus Current Sweetspots Marcellus/Utica pipeline expansion infrastructure investments will slow after Market Opportunity------Increasing transportation cost associated with Marcellus/Utica pipeline expansions could eventually begin to outweigh the favorable resource economics of these two plays, encouraging production growth from other regions, such as the Gulf Coast, which are closer to downstream markets 30

31 This shifting regional picture, caused primarily by dramatic growth in Appalachian production, will require new long-haul pipelines Infrastructure required to achieve continental balance To Midwest/E Can Bcf/d Northeast Bcf/d West/SW Bcf/d Transco/Other SE 1.0 Bcf/d * Sabal Trail/FGT expansion Bcf/d Notes: Northeast includes US Northeast and Atlantic Canada. Source: IHS Energy 2016 IHS 31

32 Monthly Rig Count Low gas prices continue to discourage operators from deploying additional rigs to most gassy plays US lower-48 onshore rig count Marcellus PA Marcellus WV Utica Barnett Eagle Ford Fayetteville Haynesville Permian plays Smaller plays Other - Dry Gas Other - Wet Gas Other - Gassy Oil Other - Oil Permian Plays Eagle Ford Marcellus PA Marcellus WV Utica The outlook for natural gas drilling remains at bay due largely to the success in the Marcellus and to the prospectivity of the Utica. First year decline rates in Marcellus wells were reduced to about 57% from the approximately 65% modelled previously. Recent well performance supports the new decline rate. Rig counts in the Eagle Ford and Permian Basin, key contributors of associated gas, are expected to begin rebounding in Source: IHS 2016 IHS 32

33 US demand by sector: Pace of growth question in early years, but not long term Overall growth rate averages 1.8% annually, or 1.8 Bcf/d annually total of 44.7 Bcf/d The power growth in early years has likely been undercut by renewables development, and reduced electricity demand. However, longer term, without tax credits gas would capture a larger share of power market again. There is also some upside in export and industrial markets. 33

34 Mexico the Gas Market. 34

35 Global LNG demand a longer view Global LNG market is currently suffering from oversupply, weak demand, and revived competition from low-cost oil, clouding the outlook for new projects in the near term US LNG set to play a pivotal role in providing a floor for global LNG spot prices beyond 2016 but will be among the most expensive supply sources because its feedstock is procured via pipeline and is resalable into the liquid US gas market Expected prorated capacity, 5.3 MMtpa in 2016, 13.1 MMtpa in 2017, and 21.2 MMtpa (2.8 Bcfd) in Implication is that it will still take time for the US LNG industry to provide a volumetrically substantial floor at $4 5/MMBtu for spot prices 35

36 Key Gas Takeaways The North American natural gas market is oversupplied, as a mild winter and robust production have kept storage inventories near record highs. With coal-to-gas displacement already maximized and heating load declining, the demand side will be unable to reduce this imbalance and the supply side will have to respond. Prices are dropping to induce production cuts. North American natural gas prices will fall to an 18-year low in We expect Henry Hub prices to average $2.10/MMBtu for the year and $2.86/MMBtu for Pipeline constraints and prices have dropped below variable cost in the Marcellus/Utica (the swing supply source) to induce production cuts in that region with US supply tightening by the end of Expected production cuts over the next several months speeding up the slow supply/demand balance Exports and power demand underpin demand growth After a Fall inventory maximum, which could still stress capacity (at 4,115 Bcf max), the gas market tightens significantly. To support demand growth, a production increase is required. Exports to Mexico in the next few years also help rebalance the market. Relatively low prices along with new pipeline capacity will induce increased pipeline exports to Mexico in as the domestic power sector demand ramps up. Global LNG market is currently suffering from oversupply, weak demand, and revived competition from low-cost oil, clouding the outlook for new projects 36