Evolving LNG Market and INPEX`s Value Chain Strategy

|

|

|

- Agatha Wright

- 5 years ago

- Views:

Transcription

1 Evolving LNG Market and INPEX`s Value Chain Strategy JOGMEC Techno Forum November 27th, 2018 Nobuyuki Higashi INPEX Corporation

2 Changing LNG Market and New Business Model

3 Changing LNG Market in Asia 2014 No commitments will result in no FID and a future supply shortage US shale gas can provide HH-linked prices & destination free LNG. 2 We need more domestic gas supply! while domestic prices are much cheaper than international prices Portfolio Trade can be We are a Game Changer! Asian Hubs should be Images courtesy of Master isolated images at FreeDigitalPhotos.net

4 3 Changing LNG Market in Asia

5 Changing LNG Market in Asia 2015 A good balance of diversified prices Low oil prices may continue Are oil-linked gas prices good for us? We need a domestic gas supply chain But how? We have to change our domestic gas price policy A new business model is needed! 4 Images courtesy of Master isolated images at FreeDigitalPhotos.net

6 Traditional Business Model Escrow A/C Buyer Receiving Terminal Pipeline Power City Gas Lender Long-term Contract Finance LNG Vessel Investor Seller License /PSC LNG Plant 5 Host Country Up-stream Infrastructure Investment Gas/LNG Repayment

7 Expanding Flexible Trade Receiving Market Terminal Liberalization Power Pipeline City Gas Buyer Swap Buyer Resale Buyer LNG Vessel Flexible Contract Spot Short-Term Portfolio etc. Investor Seller LNG Plant Host Country Up-stream Infrastructure Investment Gas/LNG Repayment 6

8 Changing Business Model of LNG Project <Conversional> Trading Long Term Contract Long Term Contract Long Term Contract Long Term Contract FID Commencement 10 years 20years of Production <Evolutional> Demand Creation Infrastructure Investment/Value Chain Approach Long Term Contract(10years) Portfolio Volume Trading Long Term Contract(20years) FID Commencement 10 years 20years of Production 7

9 LNG Demand Forecast in Asia 180 LNG Deman Asia - Japan, S Korea, Taiwan (million ton, Wood Mackenzie) Japan South Korea Taiwan LNG Deman Asia- excluding JKT (million ton, Wood Mackenzie) Thailand Singapore Philippines Pakistan Malaysia Indonesia Bunker/FSRU Pacific Bangladesh Vietnam India China

Liquefied Plant(Operating) Liquefied Plant(Planning) 9")

10 Expanding LNG Facilities in ASEAN Receiving Terminal(Operating) Receiving Terminal(Planning) Liquefied Plant(Operating) Liquefied Plant(Planning) 9

11 Increasing Demand in Emerging Asia Buyer Buyer Receiving Market Terminal Liberalization Power Pipeline City Gas Buyer LNG Vessel Spot Short-Term Portfolio etc. Investor Seller LNG Plant Investor 10 Host Country Up-stream Gas Value Chain Basic Infrastructure Receiving Terminal Pipe Line etc. Power City Gas Industry

12 Key Elements for Gas Value Chain International Market Price Reasonable price Alternative Fuel Price Is it profitable to invest in local gas infrastructure? Gas Infrastructure Regulatory Framework Something is needed to restrict the use of coal after COP21 11 Images courtesy of Master isolated images at FreeDigitalPhotos.net

13 Changing LNG Market in Asia 2016 Finance is the Key 12 Images courtesy of Master isolated images at FreeDigitalPhotos.net

14 New Finance Scheme for Flexible Trade Escrow A/C Tranche A Buyer Receiving Market Terminal Liberalization Power Pipeline City Gas Lender A Long-term Contract LNG Vessel Senior Loan Mezzanine Finance Lender B Escrow A/C Tranche B Spot Short-Term Portfolio etc. Investor Seller LNG Plant Host Country Up-stream Infrastructure Investment Gas/LNG Repayment 13

15 New Finance Scheme for Gas Value Chain Tranche A Buyer Receiving Market Terminal Liberalization Power Pipeline City Gas Lender A Lender B Lender C LNG Vessel Senior Loan Tranche B Tranche C Spot Short-Term Portfolio etc. Investor Seller 14 Host Country LNG Plant Up-stream Basic Infrastructure Gas Value Chain Receiving Terminal Pipe Line Investor/ New Buyer Power City Gas Industry

16 Seller`s Approach for Gas Value Chain Buyer Buyer Receiving Market Terminal Liberalization Power Pipeline City Gas Buyer LNG Vessel 15 Lender Sovereign Loan Host Country Investor LNG Plant Up-stream Basic Infrastructure Gas Value Chain Seller Receiving Terminal Pipe Line Spot Short-Term Portfolio etc. PPP Finance Investor/ New Buyer Power City Gas Industry Lender

17 Seller`s Approach for Gas Value Chain Traditional Business Model SPA Utility=LNG Buyer LNG Seller Regas Terminal Power Genaration Power Grid Toll Fee/Charter PPA RegasTerminal IPP LNG Supply to IPP LNG Seller Regas terminal SPA LNG Supply & Regas Terminal LNG Seller Regas terminal Power Power Grid Gas to Power LNG Seller Regas Terminal IPP Power Grid Gas Supply & Downstream LNG Seller Regas Terminal Gas Supply Industry Commercial 16 Residential

18 Changing LNG Market (Summary) 17 Contract Long-term Contract Early commitment Over 20 years Large Volume Destination Clause Price Oil Link Formula Buyer Utilities in NE Asia Shale Revolution Over supply Flexible Supply Market Reform Liberalization Low Price HH link Spat Market FSRU Small Scale LNG Emerging Asia Demand Increase P/L Gas Decrease Contract Long-term Contract Shorten Smaller Flexible volume Destination free Flexible Trade Spot/Swap Price Diversify HH link/hybrid Asian Hub price? Buyer Diversify Emerging Asian buyers Infrastructure needed Less creditworthiness Portfolio Player Multi sources Multi outlets Global network Market Revolution Market Liquidity Asian Hub New Finance Value Chain Player Demand creation Infrastructure Finance Small Scale LNG Technology Economics Finance

19 18 Japan`s New Initiative (18 th Oct. 2017)

20 19 Japan`s New Initiative (22 nd Oct. 2018)

21 INPEX`s Value Chain Strategy

22 Delivering tomorrow s energy solutions May 2018 Copyright INPEX CORPORATION. All rights reserved. VISION2040

23 Targets for the Period until 2040 Sustainable Growth of Oil and Natural Gas E&P Activities A top 10 international oil company Development of Global Gas Value Chain Business A key player in natural gas development and supply in Asia & Oceania Reinforcement of Renewable Energy Initiatives 10% of project portfolio INPEX s Strengths Strong portfolio, partnerships with oil-producing countries, project execution capabilities, diverse human resources, financial soundness, support from the Japanese government Reduce carbon footprint Continuously and sustainably increase corporate value

24 Development of Global Gas Value Chain Business Be a key player in natural gas development and supply in Asia & Oceania Developing Global Gas Value Chain Developing gas demand in Asia and other growing markets Maintaining/strengthenin g supply and demand management and trading functions Increasing domestic supply to over 3 billion m 3 by ensuring a stable supply using the company s domestic infrastructures and cooperating with business partners Upstream gas projects Ichthys Abadi

25 May 11, 2018 Copyright INPEX CORPORATION. All rights reserved. Medium-term Business Plan

26 Medium-term Business Plan INPEX Growth Strategy to 2040 Medium-term Business Plan INPEX initiatives and targets during FY toward Vision Corporate Value INPEX Position in Vision 2040 Renewable Energy Global Gas Value Chain 2 Long-term Growth Drivers Expansion of existing assets New projects, etc. Abadi LNG Project Ichthys LNG Project Existing Upstream Assets Upper / Lower Zakum, ADCO, Minami-Nagaoka, Kashagan, ACG, etc. FY2018 FY2022 1, 2 See Slide Notes (1) on page 22. FY2040 Note: Conceptual diagram Copyright INPEX CORPORATION. All rights reserved. Medium-term Business Plan

Oil and Natural Gas Upstream Abadi LNG Project Conduct pre-feed and FEED works to optimize an onshore LNG development plan for approximately 9.")

27 Medium-term Business Plan Business Targets (1) Oil and Natural Gas Upstream Abadi LNG Project Conduct pre-feed and FEED works to optimize an onshore LNG development plan for approximately 9.5 MTPA of LNG and achieve FID at an early stage Engage and cooperate with all relevant stakeholders including the Indonesian government and local authorities targeting early commercialization Evaluate feasibility of domestic gas supply in Indonesia Aim to start production in late 2020s Pursue efficient development leveraging the expertise and experience acquired through the Ichthys LNG project Masela Block Indonesia Tanimbar Islands Saumlaki Abadi Gas Field Australia Darwin Drillship (As of May 2018) Note: Production volume, capacity and other figures are all on a project 100% basis. Copyright INPEX CORPORATION. All rights reserved. Medium-term Business Plan

Global Gas Value Chain Overseas Achieve top-level LNG entitlement in Asia")

Ichthys LNG Project")

28 Medium-term Business Plan Business Targets (2) Global Gas Value Chain Overseas Achieve top-level LNG entitlement in Asia and Oceania Domestic (Japan) Achieve annual natural gas supply volume of 2.5 Bm 3 Continue marketing activities to further increase annual natural gas supply volume to 3 Bm 3 LNG/Gas marketing for FID on Abadi LNG project Create natural gas demand in Asia and other growing markets Establish a flexible supply system by effectively deploying LNG fleet and strengthening capabilities to adapt to changing markets Midstream and downstream gas businesses FSRU 1 Domestic gas pipeline Create Natural Gas Demand in Growing Markets Gas power plant Naoetsu LNG Terminal 1. FSRU: Floating Storage and Regasification Unit. Photo by courtesy of Mitsui O.S.K. Lines, Ltd. Copyright INPEX CORPORATION. All rights reserved. Medium-term Business Plan Natural Gas Supply Volume (Bm3) FY2017 INPEX upstream gas projects Abadi LNG Project (Production start in late 2020s) Ichthys LNG Project Steady Natural Gas Supply in Japan Oceanic Breeze FY2022 LNG Fleet Pacific Breeze (Ichthys) Oceanic Breeze (Ichthys) Symphonic Breeze (Prelude)

29 INPEX`s Gas Value Chain Strategy Financial Institute Japanese Government (METI) Trading House IOC/NOC INPEX Utility Company INPEX Gas Value Chain Exploration and Production Liquefaction Shipping & Transportation Regasification Gas Supply & Power 28

30 Targeting Business Areas LNG Bunkering FSRU Gas-Fired Power Plant 29 Gas Distribution to Industrial Parks Small Scale LNG

31 The Road Map toward Abadi FID Other Asia Downstream business Opening Indonesia Domestic Market Demand Creation FSRU IPP Small Scale LNG Opening Opening Opening Demand Creation LNG Bunkering Opening New Buyers (Indonesian, other Asian) Off Take Commitment Traditional Anchor Buyers (Japan, Korea, Taiwan) Off Take Commitment Abadi POD Marketing FID Commencement of Production 30

32 Our Experience/Expertise; NAOETSU Model Niigata Naoetsu LNG Terminal Pipeline Ops Center Naoetsu Nagaoka Gas Field Sekihara Underground Gas Storage Toyama LNG Shipping Nagano Fujioka Booster St. Mt. Fuji Mt. Fuji Tokyo Best mix of produced gas and LNG Multi gas sources 1,500km pipelines network. 86 distribution sites 31 Icthys LNG Project in Australia Pacific Ocean Gas Purchase from Shimizu LNG 0 50 years safe operations Gas supply engineering 100 km

33 Power Projects Gas IPP Project (1) Site : Niigata, Japan Plant Capacity : 55MW INPEX Share: 100% Gas IPP Project (2) Site : Niigata, Japan Plant Capacity : 110MW INPEX Share: 5% 32 Mega Solar Project Site: Niigata, Japan Maximum output: 4MW Predicted generation output: 5,330MW/p.a. Geothermal Project Site : Sumatra, Indonesia Plant Capacity : 330MW Consortium members: INPEX, PT Medco Power Indonesia, Ormat Technologies Inc, ITOCHU Corporation, Kyushu Electric Power Co., Inc.

34 Our Experience/Expertise; NAOETSU Model Pipeline Operations Center in NAOETSU SCADA (Supervisory Control and Data Acquisition) system operations Real time monitoring 24hrs, 365 days Gas distributions to various customers via 1,500km pipelines from multi gas sources 34 local distribution companies, 28 industries, 3 independent power producers. Control and Data Acquisition Demand and Supply Control Flow Analysis 33

35 Demand Response Operations Manage demand gaps Winter and summer Weekend and weekday A.I. program applied for Max 48 hrs demand prediction Peak shaving operations Seasonal shaving by Underground Gas Storage. Daily shaving by pressure packing, e.g. boosters. Local Demand Prediction 10,000 Gas Field+UGS+LNG Gas Field+UGS Only Gas Field 8,000 Overall Demand Prediction 6,000 4,000 2,

36 Integration of Domestic Gas & LNG Gas Demand(MMNm3/Y), PL Length(km) 2,500 Imported Gas(Naoetsu) 3rd Party Gas Domestic Gas Field PL Distance Constructing 4 gas processing plants in Minami Nagaoka and several PLs Towards 2.5BCM3 FID Construction Supply to New Market Naoetsu LNG Terminal Receiving from Ichthys

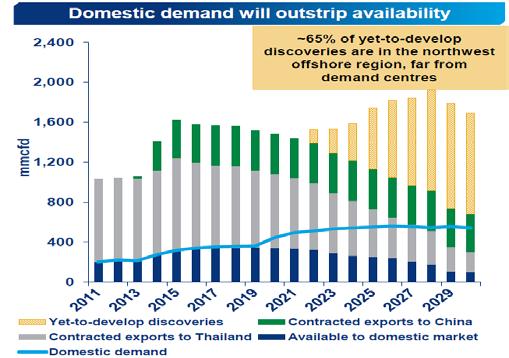

37 36 Domestic Gas and LNG Import in Asia

")

+1 (Bali) Gas Reserves (end")

38 Gas Value Chain in Indonesia Total Pipeline Length:9,700 km (96%) PNA:Arun-Medan, Palembang Area, West Jawa-JKT East Jawa PGN:Sumatra Main Pipeline, Lumpung-JKT, Semarang Gas Transmission Volume:3,000mmcfd Supply volume:900mmcfd FSRU:2 (W. Jawa) +1 (Bali) Gas Reserves (end 2017):PNA 11Tcf, Saka Energi(PGN) 1Tcf 37 PGN annual report

39 Future LNG Market; Gas Value Network Gas Downstream Power Gas Downstream Power Regas Terminal Pipeline TPA TPA Regas Terminal Pipeline Buyer Buyer Buyer Seller Seller LNG Plant Spot Market LNG Plant Upstream Upstream New Buyer New Buyer Seller New Buyer Regas Terminal Regas Terminal LNG Plant Regas Terminal Gas Downstream Power Gas Downstream Power Upstream Gas Downstream Power 38

40 Disclaimer INPEX CORPORATION (INPEX) is not responsible for any loss suffered in connection with the unauthorized use of this presentation or any of the content. INPEX makes no warranties or representations about this presentation or any of its content. INPEX undertakes no obligation to publicly update or revise the disclosure of information in this presentation (including forward-looking information) after the date of this presentation. INPEX excludes, to the maximum extent permitted by law, any liability which may arise as a result of the unauthorized use of this presentation, its content or the information on it. Unless otherwise indicated, INPEX owns the copyright in the content in this presentation. 39

41 Nobuyuki Higashi Corporate Officer Vice President, Global Energy Marketing Division INPEX CORPORATION Nobuyuki Higashi is responsible for gas business development at INPEX CORPORATION where he previously served as Vide President of Corporate Strategy & Planning Division. Prior to joining INPEX in 2013, He spent 31 years as a banking official at the Japan Bank for International Cooperation (JBIC), most recently as Executive Officer overseeing both sovereign and project financing in the oil & gas and infrastructure sectors in the Asia Pacific region. He also previously served as the Japanese Representative Director of the Credit Guarantee Investment Fund (CGIF) established by the ASEAN+3 Forum and the Asian Development Bank (ADB). Higashi has considerable experience in LNG project financing through direct involvement in projects in Australia, Indonesia, Malaysia, Qatar and Russia. He spent two years at the International Energy Agency (IEA) as a gas analyst in where he published "Natural Gas in China", having previously also issued several reports and studies including "The Governing Ability of China, Economics Chapter IX; Energy", a joint research study published in