Gintautas Kutka Executive director Lithuanian Shipowners Association. LNG seminar 16 June, 2011

|

|

|

- Isabella Randall

- 5 years ago

- Views:

Transcription

1 Gintautas Kutka Executive director Lithuanian Shipowners Association LNG seminar 16 June, 2011

2 CLIMATE CHANGE (CO2) Shipping maintransporter of global trade (90%) counts FOR 2 to 4% of global CO 2. Ongoing measures to further improve.

3 BUSINESS SCENARIO Under a business as usual scenario for growth in energy demand the global transport sector will consume about 40% more energy in 2030 that it uses today. More aggressive scenario accelerated investments in electric vehicles and advanced biofuels are needed by 2020.

4 LIFE OF SHIPS The average expected life of ships varies with economic cycles. A particular challenge for new technology deployment in shipping industry is very long service life of ships.

5

6 AIR EMISSIONS No complacency

7 CLIMATE CHANGE (CO2) A VARIETY OF ACTIONS UNDER CONSIDERATION (AND APPLIED) TECHNICAL OPERATIONAL OPTIONS More efficient engines, hull, propeller design, etc.: IN PROCESS

, Shore electricity (many questions including technical): IN PROCESS.")

8 CLIMATE CHANGE (CO2) A VARIETY OF ACTIONS UNDER CONSIDERATION (AND APPLIED) TECHNICAL OPERATIONAL OPTIONS Operational/technical measures, Reduction of speed, Alternative fuels/energy (LNG), Shore electricity (many questions including technical): IN PROCESS.

9 CLIMATE CHANGE (CO2) A VARIETY OF ACTIONS UNDER CONSIDERATION (AND APPLIED) LEGISLATIVE OPTIONS DIFFERENTIATION IN HARBOUR DUES: EXISTING. Caution on distortion of competition, redistribution of charges and commercial character of ports and port charges INCLUSION OF MARITIME TRANSPORT IN A GLOBAL EMISSION SCHEME (ETS) LEVY

10 INCREASING FUEL EFFICIENCY OF SHIPS

11 MARPOL ANNEX VI OUTCOME OF IMO/SULPHUR OXIDE max.4,5 % - presently global limit. max.3,5 % - as from max.0,5 % - as from 2020 or 2025, depending on review results 2018.

12 MARPOL VI enforced emission control areas(eca) On 19/05/2005 Baltic sea declared as emission control area. On 11/08/2007 North Sea and English canal declared as ECA. MAX. SULPHUR CONTENT Max.1,0 % - as from 01/07/2010 Max.0,1 % - as from 01/01/2015 Max. 0,1 % - as 01/01/2010 in EU ports

13 MARPOL ANNEX VI OUTCOME OF IMO SHIPPING INDUSTRY WELCOMES THIS GLOBAL AGREEMENT BUT: Draws attention to the potential danger of shifting cargo from sea to road through the 0,1% sulphur in the ECAS in 2015 Seriously endangers modal shift from land to sea -> risk of paralysing intra EU transport

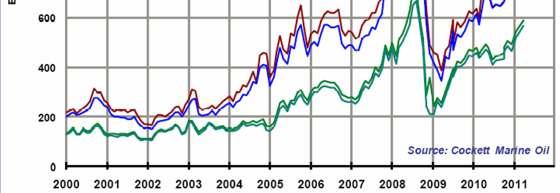

14 FUEL PRICE EVALUATION ROTTERDAM EXCHANGE

15 CHANGE SCENARIOUS OF FUEL PRICES Price LSFO Low price MGO Low price LSFO Base price MGO Base price LSFO High price MGO High price USD/t FUEL PRICES, , Rotterdam: LSFO (MAX.1,5 %) 698 USD/t; MGO 959 USD/t.

16 COST MODEL APPLIED TO FOUR SHORTSEA SHIPPING ROUTES

17 IMPACT OF FUEL PRICES TO RO-RO SECTOR 24 hours sailing time 35.5 hours sailing time HFO (1,5%) BASE MGO (0,1%) BASE HFO (1,5%) LOW MGO (0,1%) LOW HFO (1,5%) HIGH MGO (0,1%) HIGH

18 IMPACT FOR SSS ISL BREMEN ROUTE TO BALTIC: 46% loss of traffic trailers shifted to road containers shifted to road. 187 million kilometer extra on german roads.

19 OPTIONS TO CONFORM TO SULPHUR REQUIREMENTS (1) Don t sail within ECA Use MGO instead LSFO

20 OPTIONS TO CONFORM TO SULPHUR REQUIREMENTS (2) To install scrubber To use LNG for steaming

21 SCRUBBING TECHNOLOGY (1) Land based scrubbing technology is existing, however technical and other problems may be expected when transferring this land based technology to ships. It should be realised that different systems are proposed (Open-loop, Closed-loop, Dry system, Hybrid, Ecospec) and that each system requires a different approach on the technical side as well as on the treatment on the generated waste side. Some companies testing scrubbing installations had to replace piping systems due to corrosion after one year of use.

22 SCRUBBING TECHNOLOGY (2) The fuel consumption will increase with 2 to 3 %. On RoRo, RoPax and passenger vessels a scrubber installation will be most challenging due to the weight (stability issue), design and decreased deadweight of the vessel. Retrofitting on existing vessels, particularly on older types, is found to be less practicable and extremely costly. Some feasibility studies indicate a mean price of 4.5 million per installation. The other outstanding problem is on residues and waste management. No clear discharge standards for all systems.

23 LNG TECHNOLOGY THE OUTSTANDING PROBLEMS ARE MAINLY: The LNG bunkering availability and bunkering infrastructure. Costs involved. Regulatory issues mainly for safe bunkering.

24 LARGE LNG TERMINALS IN EUROPE NO BUNKERING

25 SULPHUR 0.1 % IN THE ECAs AS FROM 2015 WAY FORWARD CONCLUSIONS : Key factor: need for certainty on technical, legal and economical aspects. Financial support from Member States (State Aids) and from the Commission are available (TEN-T, Marco Polo) under restrictive conditions. The Commission will favor existing financial schemes and long term investments.

26 SULPHUR 0.1 % IN THE ECAs AS FROM 2015 WAY FORWARD CONCLUSIONS : Designating additional ECAs is maybe the solution but this is the privilege of IMO parties (Member States). Backtracking on IMO decision is not a realistic option. Dedicated measures are necessary to facilitate the transition in 2015 (pilot project support, incentives, adequate infrastructure).

27 Thank you for your attention! Lithuanian Shipowners association Naujoji Uosto 8, LT 92125, Klaipeda Tel/Fax