Geopolitics of Natural Gas

|

|

|

- Claire Cox

- 5 years ago

- Views:

Transcription

1 Geopolitics of Natural Gas A joint study from PESD Stanford University and the Baker Institute Rice University David G. Victor and Mark H. Hayes PESD, Stanford University Energy & Resources Group, UC Berkeley 3 December 2003

2 Program on Energy & Sustainable Development Established with EPRI gift to Stanford, 2001 Focus: Politics, Law, Institutions Four Research Platforms Futures for gas Electricity Markets in developing countries Low-income, rural energy markets Futures for climate policy Network operation; half Stanford, half overseas 2

3 Major Points Introduction to the Problem: Expected Gas Demand The Need for Infrastructure Our approach Initial Findings Methodological & Substantive 3

4 Increasing Role of Gas in all Regions: Gas as Fraction of Total Primary Energy 50% 40% 30% 20% IIASA-WEC A3* (1998) OECD Latin America (LAM) China (CPA) India/Pakistan (SAS) Non-OECD Pacific (PAS) Africa (AFR) 10% 0% IEA-WEO (2002) Latin America India/Pakistan China *Note: A3 is a high growth scenario that emphasizes renewables, nuclear, as well as gas 4

5 Global Gas Consumption: IPCC Illustrative Scenarios & IIASA-WEC A3 Tcm/y r IIASA-WEC A Tcf / yr Year IPCC SRES (2000) 5

")

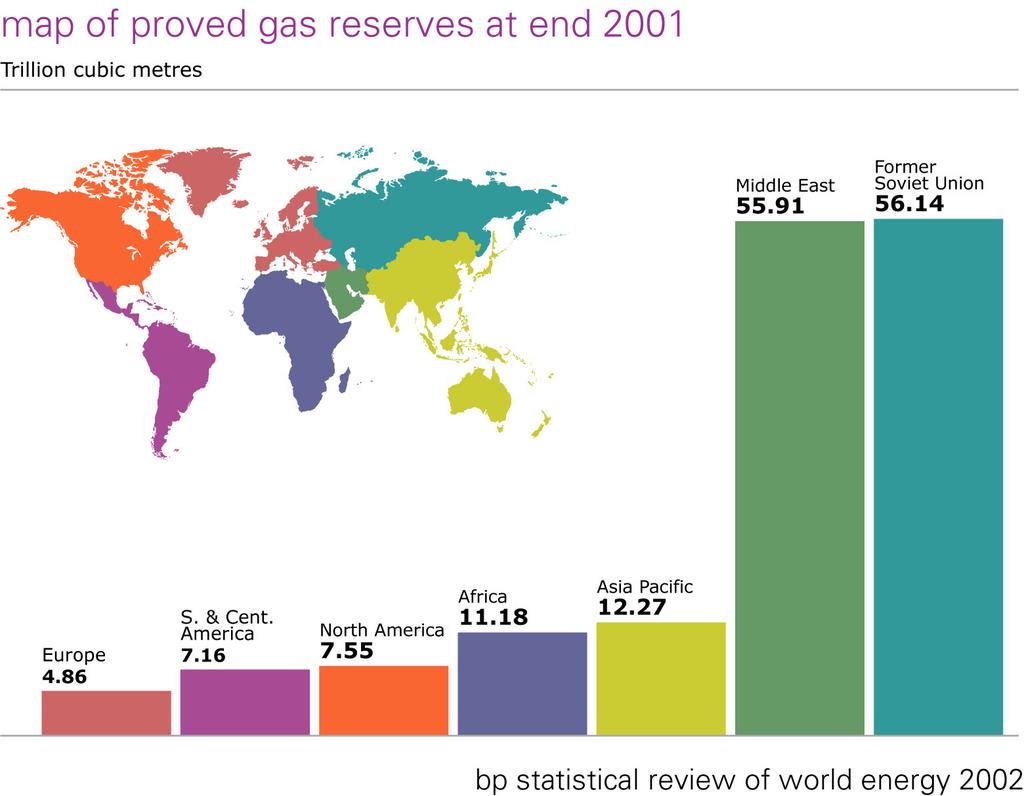

6 Supply and Demand Red: flow: WEO (2002) estimated gas demand, 2030 Green: stock: EIA Current Reserves (rough) 6

7 World Gas Trade 800 Billion Cubic Meters (Bcm) Total World Gas Movement LNG by Pipeline Year 7

8 Geopolitics of Natural Gas Study Two Research Tracks: 1. Historical Case studies Look to the past for insights into why some projects are built, and their consequences. 2. Gas Market Modeling World Gas Trade Model Political Economy Applications 8

9 Six Historical Case Studies Built Projects Author 1. Indonesia LNG to Japan Lewis & von der Mehden 2. Algeria to Italy Hayes 3. Russia to Poland and Germany Victor &Victor 4. Turkmenistan (to Iran, to Russia, Olcott to Pakistan & India) 5. Qatar to Japan Hashimoto 6. Southern Cone (Bolivia to Argentina; Argentina to Chile; Bolivia to Brazil) Mares 9

10 Research Protocol: Why are Some Projects Built, others not? 1. Context: Project Economics and Technology 2. Other Key Explanatory Factors: 1. Political and Policy Drivers 2. Investment climate in host countries 3. Transit countries 4. Offtake quantity and price risk 5. International institutions See: Hayes & Victor, Working Paper #8, at 10

11 Seven Initial Observations 1) Methods 2) The gas weapon 3) Transit countries 4) State control vs. markets 5) The roles of long-term contracts and short term markets 6) Regional Institutions and the peace dividend 7) Spillovers benefits to under-served 11

12 Observation #1: Methods Research Question: Why are some key projects built but others not? Danger: Focus on built projects only Built projects are visible; failures usually not Case selection bias Our solution: studies of alternative projects (APs) 12

13 Observation #2: The Gas Weapon To date, very few political interruptions Non-commercial markets many interruptions (e.g. Ukraine 1990s) The only severe example: early 1980s Algeria Why? Gas pipelines are fixed infrastructures, costly to leave empty Unlike oil using the weapon is usually costly Severe effects on reputation Long-term damage to Algeria s export potential 13

Sardinia transmed Tunisia Sicily Dispenza (2002)")

14 Transmed Gas Pipeline France Magrheb (not built) Spain direct (not built) Sardinia transmed Tunisia Sicily Dispenza (2002) 14

15 Algeria Gas Exports to Italy Delivered Contracted bcm $5.5 $ $3.5 $ *Price in $/mmbtu 15

16 Observation #3: Transit Country Risks Project design vs. project operation. Example: Soviet/Russian gas exports Project design: Soviet era: zero concern for transit countries Today: transit country concerns dominate new project design Project operation: Transit country risks remarkably low Mainly about rent allocation (Are there credible alt. s?) 16

17 [add points here]

18 Observation #4: States and Markets Today: Great Transition from states to markets Poses difficulty for case selection One (of many) issues: Will shift to markets speed or slow the diffusion of gas technology? UK example: markets accelerate dash to gas Most other countries: state itself created gas niches Contrast Russia and Poland Not obvious what the impact of liberalization is on gas use 18

19 Poland: Primary Energy % 80% Share of Final Consumption Coal Bcm Gas Equiv % 40% 20% Oil Gas Hydro 0% Coal Gas Oil Hydro

20 20 FSU: Primary Energy Production, ,000 1,200 1,400 1,600 1, Mtoe 0% 20% 40% 60% 80% 100% Gas Oil Coal Biomass Hydro Nuclear biomass coal oil gas

21 Observation #5: Contracts and Spot Markets First Projects: Always Anchored in Longterm contracts What is a contract? Renegotiation clauses, price & quantity Enforcement of contracts Self-enforcing contracts (esp. pipelines) Outside enforcers (World Bank, western firms) A shift to merchant markets? Example of U.S. gas market and LNG 21

22 Gas and Crude Prices Henry Hub Spot Cushing, OK Crude 8 $/MMBtu /1/89 2/1/91 2/1/93 2/1/95 2/1/97 2/1/99 2/1/01 2/1/03 22

23 Observation #6: A Peace Dividend from Pipelines? Analogy: European Coal and Steel Community and the Treaty of Rome (1957) Same true for pipelines? Southern Cone example No evidence supports this hypothesis Causal arrows run opposite direction peace and institutions allow gas, not vice-versa 23

24 Southern Cone: Gas Interconnections Before 1990 Current and Future Venezuela Venezuela Peru Bolivia Brazil Gas pipeline Bolivia-Argentina 1972 Peru Bolivia Brazil Gas pipeline Santa Cruz-Sao Paulo 1999 Bermejo-Rámos 1988 Chile Paraguay Argentina Uruguay Gas pipeline Bolivia-Chile Atacama 1999 Norandino 1999 GasAndes 1997 Gas pipeline del Pacífico 1999 Chile Paraguay Argentina Uruguay Gas pipeline Paisandú 1998 Gas pipeline Bolivia-Paraguay-Brazil Gas pipeline Mercosur Gas pipeline Uruguaiana 2000 de la Vega, 2000 Gas pipeline Methanex 1996

25 Observation #7: Benefits to Under-served Do large-scale infrastructure projects generate spillover benefits and public goods? Results: as theory would predict State-driven projects assembled through political negotiations: spillovers are key Southern Italy example Market-driven projects: private benefits and scalability dominate decision-making GasAndes example 25

26 What Next? Refining the results And, new questions E.g., does the resource curse apply to Gas? Three Trials in the World Gas Trade Model Real vs. estimated projects in 90s Making a market: China State-owned enterprises: Russia 26

27 0.25 The Value of Soviet & Russian Gas Exports: The Difficulty of SOE reform Gas Price (96'US $ / cubm) billion '96US$ 3 2 Gas Price (96'US $ / Mbtu) 30 billion '96US$ 20 billion '96US$ 15 billion '96US$ billion '96US$ 5 billion Former Soviet Union: Exports (billion cubm/year) Note: Prior to 1992 FSU export, excludes movements between FSU countries. Data source: BP( ), EIA ( ) 0 1 billion '96US$ 27

28 Backup slides follow

29 FSU: Natural Gas Production, Export, Import and Consumption Billion Cubic Meters FSU: Natural Gas Export Gas Consumption Billion Cubic Meters Import Export Production for internal use

30 1970, 3.4 Billion Cubic Meters Poland Austria 1975, 19.3 Billion Cubic Meters Czechoslovakia Poland Austria Italy 1980, 57.6 Billion Cubic Meters Germany Poland Italy 1991, Billion Cubic Meters Czechoslovakia Poland Germany Italy Czechoslovakia 2001, Billion Cubic Meters France Germany Turkey Austria Bulgaria Hungary Iran Poland France Croatia Czech Republic Italy Netherlands Italy Finland France Others Poland Germany Germany Greece Romania Slovakia Turkey 30

31 Poland Primary Energy Consumption % 80% Share of Final Consumption Coal Bcm Gas Equiv % 40% 20% Oil Gas Hydro 0% Gas Oil Hydro 50 Coal

32 Russian Primary Energy Balances 2000 Share of Consumption % 80% 60% GAS 40% Bcm Equivalent OIL 20% COAL HYDRO 0% Gas NUCLEAR Oil Coal Hydro Nuclear 32

33 Italian Gas Supply by Source Bcm Other Algeria Russia Netherlands Libya Domestic Production Source: IEA 33

34 Italian Primary Energy Consumption 350 Share of total % 80% OIL % 40% GAS Bcm % COAL NUCLEAR 0% HYDRO Gas 100 Oil 50 Nuclear Hydro Coal 34

35 35

36 Japan's Primary Energy Balance 1,000 Share of Total 100% % 60% Oil Bcm % Coal 20% Hydro 0% Nuclear Gas Gas 400 Oil 200 Nuclear Coal Hydro 36

37 Singapore Primary Energy Supply % Share of Total Gas % 80% Oil Bcm Natural Gas % 40% 20% Gas Oil

38 Indonesia Primary Energy Supply 120 Share of Total % 80% Oil 60% Bcm Natural Gas % Gas 20% Coal Hydro Gas Oil 20 Hydro - Coal

39 [add points here]

40 Long-term Crude and Gas Prices 40