Slovenian Electricity Market

|

|

|

- Vivien Marshall

- 5 years ago

- Views:

Transcription

1 Slovenian Electricity Market mag. Karlo Peršolja general manager Borzen, d.o.o. Zagreb,

Market")

2 Slovenian Electricity Market development Energy law (EZ) Market opening (partialy) Market rules Imbalance settlement Daily cross-border auctions Market 100% open EZ-A EZ-B EZ-C EZ-D European internal electricity market Market-coupling with Italy EZ-E MR-A MR2 MR2-A Energy Agency established Borzen established Borzen PX (electronic) Foreign traders don t need licences BSP PX established Balancing market & intra-day market opening

3 The Role of Borzen

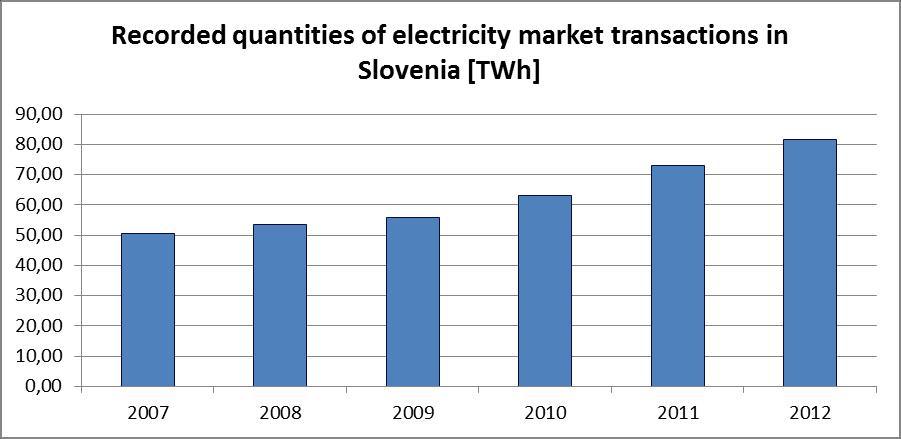

4 Growth of Slovenian Market

5 Yearly Consumption and Peak Power * Source: Elektro-Slovenija d.o.o.

6 * Source: Elektro-Slovenija d.o.o. Slovenian Transmission Network

7 The ITA SLO Market Coupling project Project initiated by GME and Borzen in 2007 MoU between the companies signed in Q BSP SouthPool joined the MoU immediately after establishment Governments of Slovenia and Italy expressed support in a joint declaration The Italian Republic and the Republic of Slovenia agreed as follows: [ ] To support the activities aimed at further integration of European internal energy market, also in the field of Energy Community, including the cooperation between GME and Borzen Proposal formally submitted to the TSOs (TERNA and ELES) and Regulators (Italian and Slovenian)

8 The ITA SLO Market Coupling project (cont.) Project start , thus currently in its third year Very stable operations thusfar Pentalateral project : ELES, TERNA, BSP, GME, BORZEN Drastic increase in BSP trading volumes to approx. 4,4 TWh (roughly 1/3 of SLO domestic consumption) Consequently Stable, liquid SLO price signal Reliance on possibility to sell / buy on the PX Implicit selling to foreign markets (or buying from foreign markets) Higher efficiency and generally lower operational costs

9 Volumes of Production, Consumption, and Cross-border Trade (Schedule) Prices on EPEX lower than BSP, prices on GME higher

10 Volumes of Production, Consumption, and Cross-border Trade (Schedule) Prices on EPEX higher than BSP, high hydro production

11 Status of Renewables on the SLO market Historical role of large hydro and also small hydro (big expansion in the 1980s and 1990s) Support scheme (feed-in) in use from 2001; updated in 2009 In recent years: very steep rise of solar PV (from 2 to 200+ MW from 2009 to 2012), also of biogas Relative stagnation of other sources, especially hydro, mainly due to complicated approval procedures (right to build, environmental procedures etc.) Rising role of high-efficiency cogeneration, which is also supported through the feed-in support sheme

12 The Slovenian Feed-in-Tariff experience System updated in 2009 Technology differentiated FITs; support based on cost calculations In around 3 and a half years: Number of producers up from around 600 to around 2000 Installed capacity up by around 20-25% PV boom : from 1,6 MW beginning 2009 to around 10 MW mid 2010 and around 35MW end 2010 and projected around 200MW end main reasons for the rise in investments: 1. Generally higher support levels 2. Less alternative investment possibilities (due to recession) 3. Fall in prices of some equipment (e.g. solar PV!)

13 Eligible production units High-efficiency CHP units (up to 200MW), RES units (up to 125MW). CHP units up to 1MW and RES units up to 5MW may choose the support type, while larger units may only receive the operating support, i.e. must sell the electricity on the market. CHP units receive support for 10 years, RES for 15.

14 Types of support Guaranteed purchase (GP): Means that a power plant enters the Centre for RES/CHP support s balance group that operates within Borzen. In such a case the beneficiary sells electricity to the Centre for RES/CHP support and issues a uniform invoice at the price for guaranteed purchase. In this case the producer does not and is not permitted to conclude a separate market agreement for the sale of electricity. Operating support / premium (OS): If the beneficiary decides for operating support, this means that they have concluded an open contract on the market ( the market agreement for the sale of electricity ). The beneficiary issues separate invoices: for electricity to their supplier / trader and for support to Borzen (The Centre for RES/CHP support).

15 State of play april 2013

16 State of play (cont.) Year Electricity (GWh) Cost (mio EUR) , , , ,8 The steep rise of costs is due to higher support levels and to the fact that the majority of investments were into highsupport, low-capacity-factor solar PV (>40% cost in 2013). In 2013 the cost are projected to exceed 100 mio EUR.

17 Potential Hydro, although already central among RES, is in development: Sava river chain, possibly Mura river; development of smaller units dependent on project approval procedures Due to rising system costs it is expected that PV development will slow down (several support-level cuts were already implemented) There is potential in industrial and residential CHP, although these projects are of course more complex Wind energy is practically non-existent (excp. 1 unit 2MW) If Slovenia is to keep its 25% target for 2020, investments must continue! There is room for development for RES in electricity, but even more in RES heating / cooling (e.g. Slovenia has a large potential in wood biomass)

18 Thank you for your attention!