Un mundo sin petróleo?

|

|

|

- Allan Preston

- 5 years ago

- Views:

Transcription

1 Un mundo sin petróleo? Mariano Marzo (Facultat de Geologia, UB) ATEQ , Tarragona

2 Energy use grows with economic development GE=GE

3 Energy use grows with economic development GE=GE

4 The hydrocarbon s man

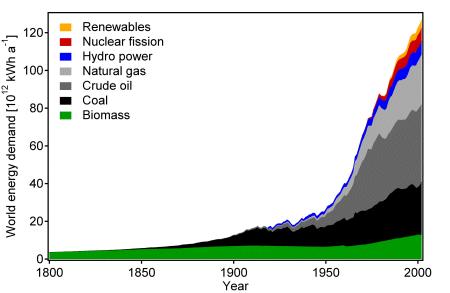

5 World total primary energy supply by fuel **Other includes geothermal, solar, wind, heat, etc.

6 World oil consumption by sector *Other sectors comprises agriculture, commercial & public service, residential and non-specified.

7 World primary energy demand by fuel Their share in total demand will increase from 80% to 82% IEA, WEO 2004 Fossil fuels will continue to dominate global energy use. They will account for around 85% of the increase in world primary demand.

8 Transport oil demand and GDP, IEA,WEO 2004

9 Regional shares in world primary energy demand Two-thirds of the increase in global energy demand will come from developing countries By 2030, they will account for almost half of total demand, in line with their more rapid economic and population growth. IEA, WEO 2004

10

11

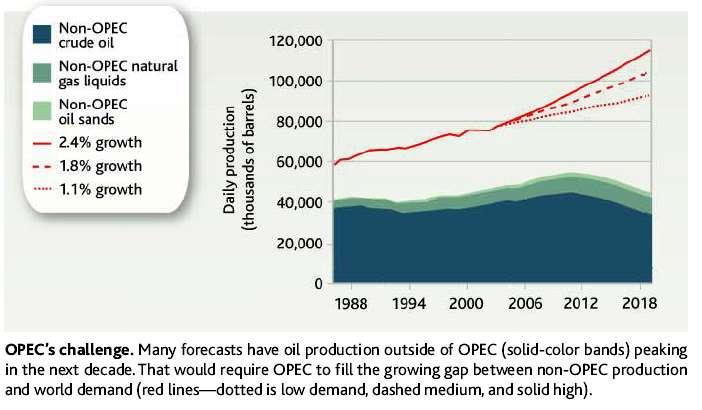

12

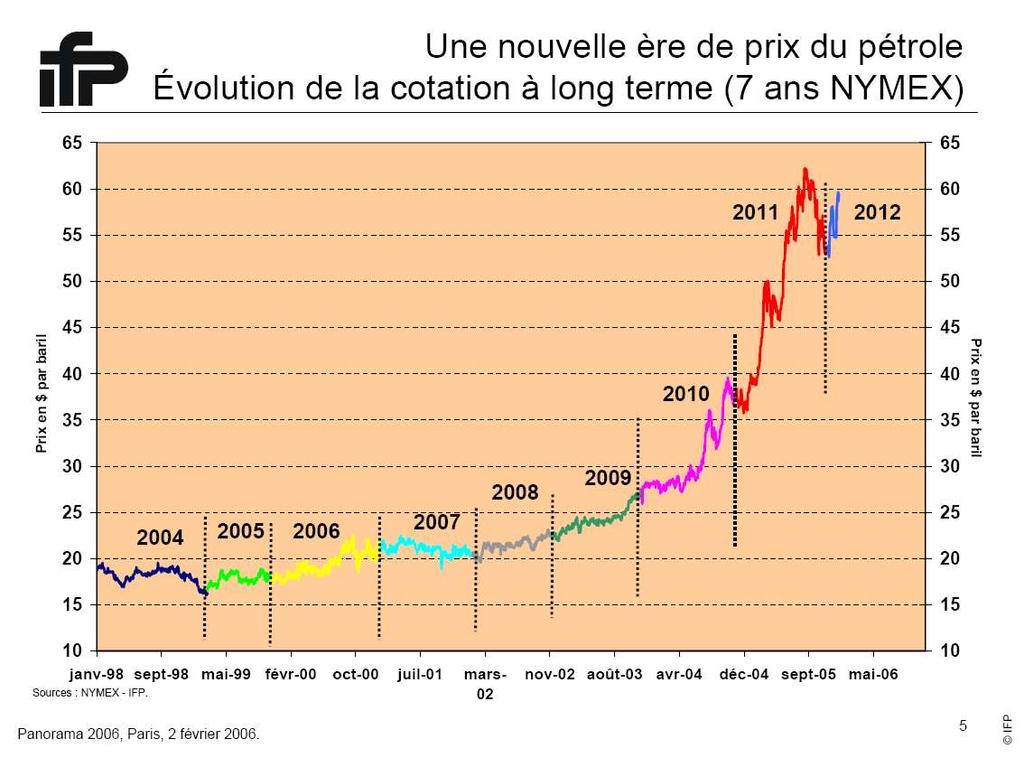

13 Basically since we have futures markets in oil, the expectations on long term price of oil were extraordinarily stable - at around 20$/bl. That meant that, at all times, and whatever the actual spot price was, oil prices were expected to come back (upwards, or downwards, depending on where it would be then) to that level. The view of the market on future prices of oil has changed in the past 2 years. The market expects oil prices to still be around 6070$/bl 5 years from now, and not to drift down to 20$/bl or somewhere in between. 11-S Irak War

14

15 Downstream and upstream problems Producción Exploración Transporte Precio EL CÍRCULO DEL MERCADO DEL PETRÓLEO Demanda "Stock" de productos Refineria.

16 Upstream: the visible part of the iceberg

17 Declining discoveries Rising finding & development costs

18 Cumulative oil and gas discoveries and new wildcat wells drilled, World Energy Outlook 2004

19 A growing gap

20 New discoveries UK North Sea: more difficult, less prolific, more expensive

21 Depletion

22 AIE: Decline rates range from 5% to 11% per year. By 2030, most oil production worldwide will come from capacity that is yet to be built World Energy Outlook 2004

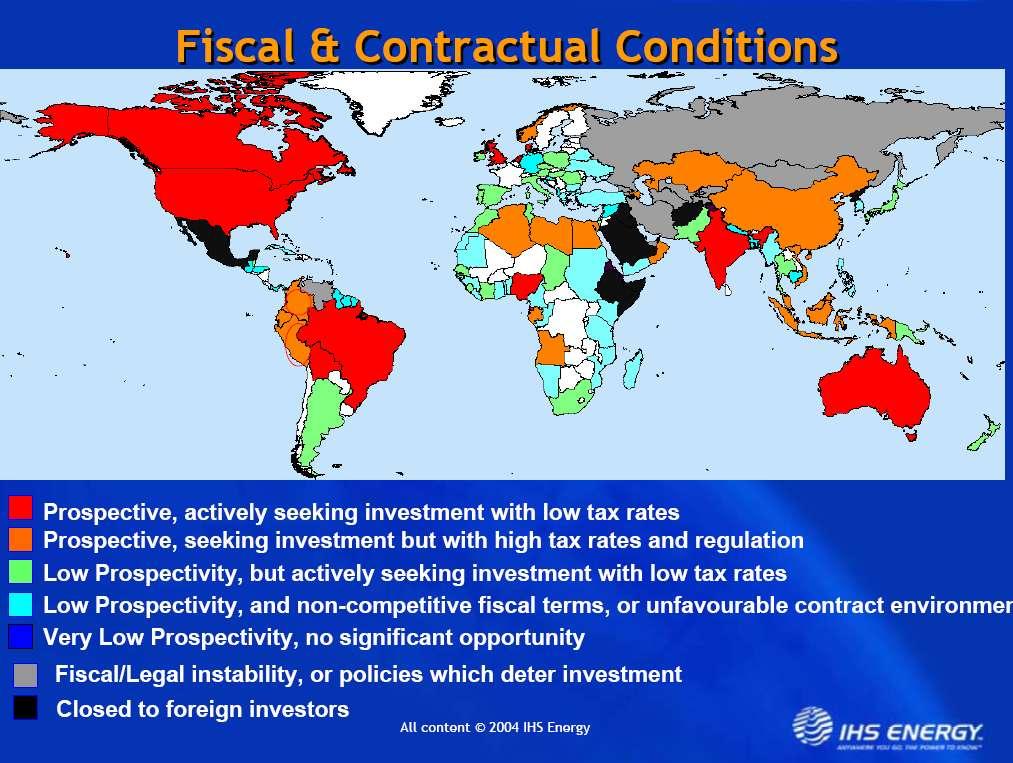

23 The 3 terms of the equation New production, Type 3 depletion and demand milliion b/d year

24 The price to pay: Trillions (1012) US $ Rising dependency from Middle East Risk of supply disruptions

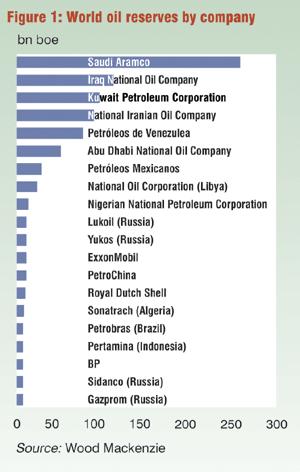

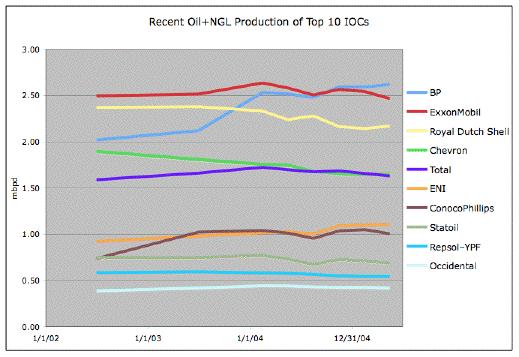

25 : 3x1012 US $ (E & P 70%) x 106 per year / 287,7 x 106 per day World Energy Outlook 2004

WEO")

26 Major net inter-regional oil trade flows (mb/d) WEO 2004

27 Choke points WEO 2004

28 Geopolitical uncertainties

29 Higher prices = more discoveries? Longwell,H.J., CEO ExxonMobil, 2002

30 The key is access to new areas

31

32 Reserves: IOC s vs NOC s

33 Chinese and Indian NOC s

34 The submerged part of the iceberg: peak oil

35 Pessimists ( Hubbertites )

36 Optimists ( Cornucopias ) Annual Production Scenarios for the Mean Resource Estimate and Different Growth Rates (Decline R/P = 10) 70 USGS Estimates of Ultimate Recovery 3% Growth Billion Barrels per Year Ultimate Recovery Probability BBls Low (95 %) 2,248 Mean (expected value) 3,003 High (5 %) 3,896 2% Growth 1% Growth Decline R/P = 10 History Mean

37 USGS (95%, 50% and 5%) vs the rest Published Estimates of World Oil Ultimate Recovery USGS 5% 2000 USGS Mean 2000 USGS 95% 2000 Campbell 1995 Masters 1994 Campbell 1992 Bookout 1989 Masters 1987 Martin 1984 Nehring 1982 Halbouty 1981 Meyerhoff 1979 Nehring 1978 Nelson 1977 Folinsbee 1976 Adams & Kirby 1975 Linden 1973 Moody 1972 Moody 1970 Shell 1968 Weeks 1959 MacNaughton 1953 Weeks 1948 Pratt Source: USGS and Colin Campbell Trillions of Barrels EIA

38 SCIENCE, 18 NOVEMBER 2005, VOL 310

39

40 In ads that Chevron has been running in major newspapers and magazines, we are told that we the world is using two barrels for every one it finds. "One thing is clear: the era of easy oil is over," say the ads.

41 J. Herolds: big oil & peak oil Total: 2007 ExxonMobil, BP & Shell: 2008 Chevron:2009 Big oil: no comment

42 ExxonMobil's own production statistics

43

44

45 The world needs a new energy transition. This, if ever, could take decades What can be done in the meanwhile?

46 PEAKING OF WORLD OIL PRODUCTION: IMPACTS, MITIGATION, & RISK MANAGEMENT Robert L. Hirsch, SAIC, Project Leader Roger Bezdek, MISI Robert Wendling, MISI February 2005

47

48

49

50

51 CONCLUSIONS The future of global oil supply: plenty of challenges and uncertainties No agreement on available resources and reserves No agreement on the date of peak oil ( ?) Increasing dependence from Middle East and OPEC Geopolitics: the new great game Trillions in investments (70% E&P) High-risk of temporary supply disruptions Tight supply/demand Price volatility The era of cheap and easy oil is over A new situation that along with global warming demands a new energetic model

52 Fasten your seat belts! We are entering the second half of the age of oil