Chuenchom Sangarasri Greacen Renewable Energy Workshop and Study Trip organized by MEE NET 23 January 2013

|

|

|

- Dwight Rice

- 5 years ago

- Views:

Transcription

1 Chuenchom Sangarasri Greacen Renewable Energy Workshop and Study Trip organized by MEE NET 23 January 2013

2 Thailand s Electricity Industry Structure: The Enhanced Single Buyer Model Source: Data as of December 2010, compiled from EGAT s 2010 Annual Report, section 2.1: Planning and Strategy

3

4 Data source: Energy Information Administration 2008

5 Thailand s Fuel Mix for Power Generation Imported 4% Diesel 0.03% Renewable 2% Hydro 3% Fuel Oil 0.34% Coal 18% Natural Gas 73% Total Installed Capacity: 31,517 MW (2010) 5

6 20-Year Energy Efficiency Development Plan (EEDP) 15-Year Renewable Energy Development Plan (REDP) updated to AEDP at the end of 2011 Power Development Plan (PDP) 5-Year Natural Gas Supply Plan

7 Prepared by different government divisions Not unified into a comprehensive plan Prioritizing different policy goals Security of supply Diversification Returns on Investment of Capital (ROIC) Climate Change Economics Conflicting targets (esp. the PDP vs. the REDP; PDP vs. EEDP) Limited public participation Resource options identified but not evaluated

8 Source: Ministry of Energy, Thailand 20-Year Energy Efficiency Development Plan ( ).

9 Source: Ministry of Energy, Thailand 20-Year Energy Efficiency Development Plan ( ).

10 Source: Ministry of Energy, Thailand 20-Year Energy Efficiency Development Plan ( ).

11 Source: Ministry of Energy, Alternative Energy Development Plan

12 Source: Ministry of Energy, Alternative Energy Development Plan

13 Source: Ministry of Energy, Alternative Energy Development Plan

14 Feed-in tariffs EPPO 14

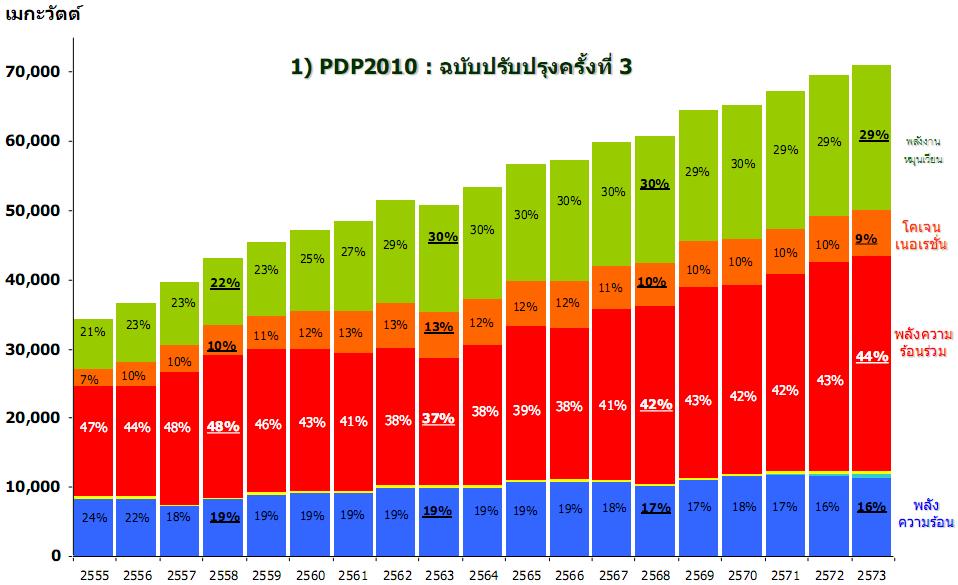

15 nuclear EE/DSM Others Oil/gas RE DEDE Cogen Hydro imports Hydro Gas Coal New generation includes: 11,669 MW of imports 8,400 MW of coal plants 16,670 MW of gas plants 5,000 MW of nuclear

16

17 Technical limitations? High costs? Limited availability? Structural bias against RE?

18 Real Levelized Cost (Cents/kWh $) Source: Northwest Power and Conservation Council, 5 th Plan. In Pacific Northwest, USA, EE is considered the cheapest supply option Cost comparison for different supply options in Pacific Northwest, USA EE Renewables Coal Gas turbines Combined cycle Cumulative Resource Potential (Average Megawatts)

19 Cumulative Capacity (MW)* Pacific NW: meeting growing demand through mainly investments in RE and EE Coal-fired (ICG) (MW) CCGTurbine (MW) SCGTurbine (MW) Wind (MW) Energy Efficiency (amw) Source: Northwest Power and Conservation Council

20 Choice of supply options considered in the PDP by EGAT 700 MW Coal-fired power plant 700 MW gas-fired combined cycle plant 230 MW gas-fired open cycle plant 1,000 MW nuclear plant Hydro imports are politically negotiated outside of PDP process DSM/EE, RE, Distributed generation not considered as supply options

21 Cost (Baht/kWh) Nuclear Coal Gas CCGT Oil (Thermal) Gas turbine RE Solar Wind Waste Biomass Source: EGAT, PDP 2007 Presentation at Public Hearing, 2 April 2007.

22 Supply options Generation Trans missio n 1 Cost estimate (Baht/kWh) Distrib CO 3 2 Other ution 2 envi impacts 4 Social impacts Total DSM SPP cogeneration (PES > 10%) VSPP (Renewable) Bulk supply tariff (~ 2.62) + Adder (0.3 8) low gas CC low medium 3.93 Coal High 5.82 Nuclear High very high หมายเหต 1. ใช สมมต ฐานว าต นท นร อยละ 12.4 ของค าไฟฟ ามาจากธ รก จสายส ง 2. ใช สมมต ฐานว าต นท นร อยละ 14.5 ของค าไฟฟ ามาจากธ รก จจ าหน าย 3. ค า CO2 ท 10 ย โร/ต น 4. ค า Externality ตามการศ กษา Extern E ของสหภาพย โรป และน ามาปร บลดตามค า GDP ต อห วของไทย The World Bank, Impact of Energy Conservation, DSM and Renewable Energy Generation on EGAT s PDP, ตามระเบ ยบ SPP 7. ท มา : กฟผ. 8. California Public Utilities Commission (CPUC), 2050 Multi-Sector CO2 Emissions Abatement Analysis Calculator, Cost of liability protection, Journal Regulation

23 Centralized & decentralized generation HV Transmission HV substation MV distribution Cogeneration Distribution transformer LV distribution Biomass Plant/ Large solar farm Gasifier/ Solar farm/ Biogas Plant

24 E u ro C e n ts / K W h Thailand Decentralized generation brings down costs Ireland retail costs for new capacity PDP 2007 requires 2 trillion baht to implement, comprising: million B generation 1,482,000 transmission 595, Transmission adds 40% to generation costs % C entral / 0 % D E 75% / 25% 50% / 50% 25% / 75% 0 % C entral / 100% D % DE of Tota l Ge ne ra tion O & M of New C apac ity F uel C apital Am oriz ation + P rofit O n New C apac ity T & D Am oriz ation on New T & D Source: World Alliance for Decentralized Energy, April 2005

25 Financial criteria for utilities link profits to investments Thailand uses outdated returnbased regulation WB s promoted financial criteria such as self financing ratio (SFR) also have similar effects ROIC (Return on Invested Capital means: the more you invest, the more profits ROIC = Net profit after tax Invested capital EGAT 6.4% MEA 5.8% PEA Result : EGAT favors capital-intensive investments (centralized plants) by its organization or subsidiary companies. Allowing more EE or RE generation hurts EGAT s bottom line

26 Utilities are incentivized to prioritize capitalintensive, centralized generation Lack of integration of EE/RE in planning process Arbitrary quota system Costs Exclusion of T&D costs (not to mention externality costs) makes cost comparison between RE and other generation unfair

27 Creation of Management Committee to screen VSPP applications creates governance problems Lack of clear criteria Political connections and intervention Lack of enforceable environmental safegard framework for <10MW generation Lack of policy certainties Lack of predictability and periodic updates of purchase prices to reflect changes in costs Lack of price differentiation for smaller-scale RE Lack of financial support for community/smallscale RE

28 Energy Efficiency and Renewable Energy Act Integration of EE/RE in planning process with priority given to clean, cost-effective options Feed-in tariffs with clear mechanisms for periodic tariff updates transparent application process Proper premiums (reflecting T&D, externality benefits) given to home/community-scale RE systems Creation of enforceable environmental safeguards for <10MW generation Adoption of performance-based regulation, integrated resource planning

29 chomsgreacen at gmail dot com