Rice Global E&C Forum

|

|

|

- Rhoda Garrett

- 5 years ago

- Views:

Transcription

1 Rice Global E&C Forum "Will Shale revolution trigger game changes in Asian Energy Market and LNG?" Tevin Vongvanich President and Chief Executive Officer PTT Exploration and Production Public Company Limited 19 March

2 Unconventional: Future World Energy Supply Oil & gas still play major roles to serve world s primary energy demand mmboepd Unconventional resources will become a key sources for oil and gas production mmboepd 350 CAGR 1.7% CAGR 2.0% % % Hydro/renew Coal Oil Uncoventional and Mega trend Nuclear Natural Gas Conventional Unconventional and Mega trend: Shale Gas, Tight Oil, Heavy Oil/Oil Sands, GTL, Russia, Caspian area, Artic, etc. Source: EIA, Wood Mackenzie, Deutsche Bank 2

US Shale Oil Canadian Oil Sands N. American Uncon. Gas Venezuela Tar sands Europe Uncon.")

3 World Resources Move toward Unconventional 100% 25% 1, Shale oil Shale gas 3% 27% 13% 32% CBM Ultra heavy oil Deepwater oil Deepwater gas Conventional Other Resources (bn BOE) US Shale Oil Canadian Oil Sands N. American Uncon. Gas Venezuela Tar sands Europe Uncon. Brazil Deepwater Deepwater Med plays Algeria Tight Gas Ultra Deepwater Jordan Shale Gas DRC Heavy Oil Oman Tight Gas Mozambique Deepwater China Uncon. Gas Indonesia CBM China Deepwater Indonesia/ Malaysia Deepwater CBM Argentina Tight Gas Gt. Australia Bight Deepwater Source: GSB CSA analysis (2011) based on EXP, Wood Mackenzie, IHS, DOE data Source: GSB CSA analysis (2011) based on EXP, Wood Mackenzie, HIS, DOE data 3

4 Global Shale Gas Opportunities Estimated 2011 Global Unconventional 5.7 Gas Production bcfd 13 bcfd 17.5 bcfd Shale Tight Gas CBM Resource represents the total recoverable reserves assuming 100% of the play is drilled Estimated represent plays covered in Wood Mackenzie s Unconventional Gas Service Source: Wood Mackenzie

5 Why Shale Gas Succeed in North America? 1 2 Technological capabilities and innovations Existing infrastructure and customer markets Upper Middle Lower Horizontal drilling and multi-stage fracture stimulation successfully applied. A relatively large and capable service sector provided Established oil field infrastructure e.g. field gathering systems, local and regional pipelines, gas plants, and refineries Functional transportation infrastructure; roads and bridges 3 Rules and legislation Existing rules and legislation regarding mineral rights, leasing, right of ways, are typically in place A favorable business environment in North America, including favorable tax structures Source: Team Analysis 5

6 mmcfd Over 50% of the US Gas Supply will come from Shale Gas in ,000 90,000 80,000 70,000 60,000 50,000 40,000 54% 46% 30,000 20,000 10, Indigenous Production 43,746 45,635 52,640 49,699 58,614 66,275 77,382 88,132 Demand 46,011 53,822 65,970 60,200 64,320 69,188 77,309 87,464 Conventional, CBM and Tight Gas Shale Gas Net Import 2,264 8,187 13,330 10,501 5,705 2,913 (72) (668) Source: Wood Mackenzie s North America Gas Service 6

7 Shale Discoveries led to the Disconnection emerge in Gas and Oil Price Gas (Henry Hub) versus Oil (WTI, Brent) price index during Index (2000=1) 3.0 Brent 2.5 WTI HH Henry Hub WTI Brent Source: Wood Mackenzie 7

8 Current Natural Gas Pricing Disparities create Unprecedented for LNG Trading Gas price (Henry Hub) versus Japan LNG Import during Natural Gas Spot (US$/Mmbtu) $15.31 $10.30 $12.18 $3.13 Source: Bloomberg; prices as of 1/29/2013; Cheniere corporate presentation 8

9 Will Surplus from North America Shale be exported to Global Market? Currently planned and potential LNG projects in North America will add an additional ~204 MMpta of liquefaction capacity by the year LNG MARINE TERMINALS Liquefaction Facility Stage Approved Source: Wood Mackenzie, FERC, Equity Research Note: Regulatory process for Sabine Pass Trains 5-6 has not yet begun North American Liquefaction Facilities First LNG shipment Country Canada Canada Canada Canada Canada Project name Sabine Pass T1-4 Prince Rupert T1-2 Cameron LNG T1-3 Corpus Christi Dominion Cove (Cove Point) Freeport LNG T1-4 Lavaca Bay Oregon LNG BC LNG Kitimat LNG T1-2 Gulf Coast LNG Trunkline LNG T1-3 (Lake Charles) Petronas progress LNG Gulf LNG (Pascagoula) LNG Canada Jordan Cove LNG T1-2 (Coos Bay) Southern LNG (Elba Island) Alaska Valdez Total Possible Capacity Additions per Year Liquefaction capacity increase (Mmtpa) Capacity (Mmtpa) Capacity (Bcf/d) Acc. Status Approved 9

10 Over 15% of Global LNG will be supplied from Unconventional Gas by 2018 Global Liquefaction Capacity by Country mmtpa Shale gas and other discoveries have led to a number of proposed LNG facility worldwide. LNG will be supplied from unconventional gas over 15% by Shale gas export licenses and infrastructure are the major challenges Unconventional Gas Malaysia Indonesia Qatar Australia Nigeria Others Source: Wood Mackenzie 10

11 Increasing M&A Asian NOCs in Unconventional Increasing M&A Asian NOCs Key Asian NOCs M&A Deals in 2012 Total deals value (US$ bn) 250 Total deals count (#) CNOOC / Nexen $18.5bn Petronas / Progress $5.3bn Sinopec/Talisman $1.5bn ONGC / Hess $1bn % % 87% % 13% 20% Sinopec / Devon $2.4bn Deals count Rest of world Asian NOCs Completed transaction Ongoing transaction Pertamina / Harvest $0.7bn PTTEP / Cove $1.9bn CNOOC / BG $1.9bn Source: Wood Mackenzie Upstream Services, PLS and Derrick, IHS Herold Inc 11

12 12

1 Production Oman Thailand (18) 13 Production 5 Exploration South East Asia(15) 4")

1 Development 2 Exploration Australia New Zealand Source:")

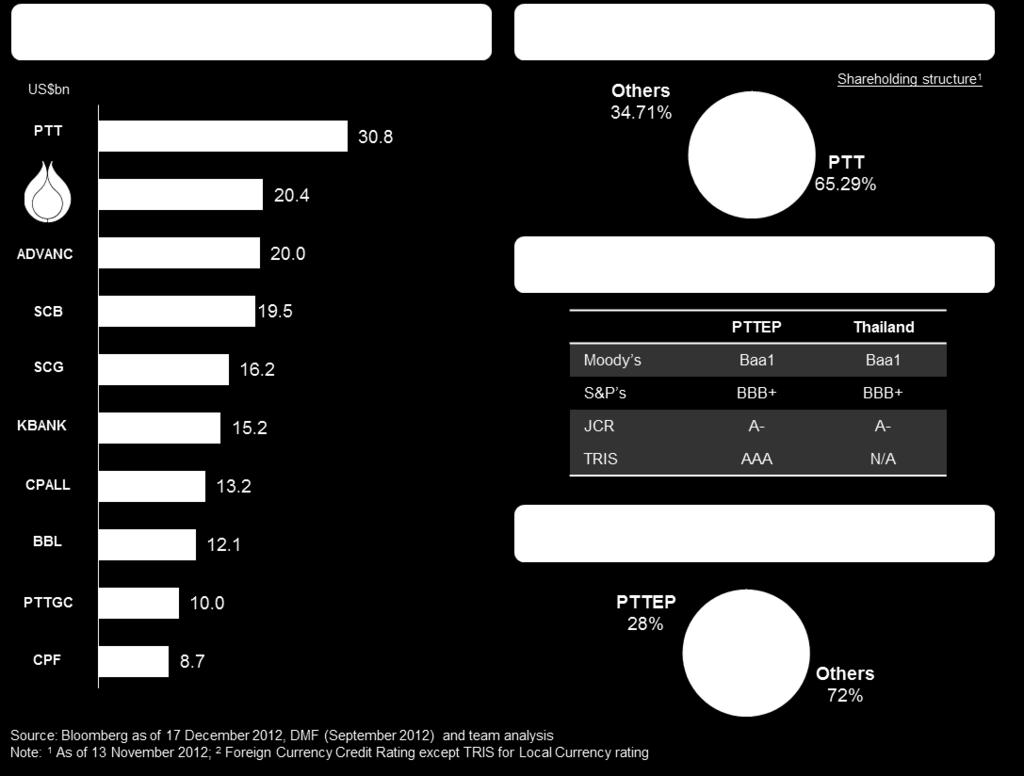

13 PTTEP Assets: 44 projects in 12 countries North America (1) 1 Production Canada Africa (6) 1 Development 5 Exploration Algeria Mozambique Kenya Middle East (1) 1 Production Oman Thailand (18) 13 Production 5 Exploration South East Asia(15) 4 Production 1 Development 10 Exploration Myanmar Vietnam Indonesia Cambodia PTTEP s Asset Base North America, 17% Africa 16% Australia 17% Thailand and SEA 49% Middle East 1% Australasia (3) 1 Development 2 Exploration Australia New Zealand Source: PTTEP 13

International Domestic")

14 PTTEP s Aspiration and its Growth Strategy 900 Production Volume (KBOE/D) International Domestic Source: PTTEP 14

15 PTTEP Recent M&A to leverage the LNG value chain to Thailand Kenya Blocks L5, L7, L11, L11B, L12 Block L10A Block L10B KENYA Acreage 30,632km 2 10,516km 2 TANZANIA L10A L10B Kenya L5,L7,L11A, L11B,L12 Operator Anadarko 50% BG 40% BG 45% Partner Total Cover Energy 40% 10% Premier Pan Cont. Cove Energy 20% 15% 25% Premier Pan Cont. Cove Energy 25% 15% 15% Mozambique Offshore Area 1 Onshore Rovuma Rovuma Onshore MOZAMBIQUE Mnazi Bay Rovuma Offshore Mozambique Offshore Area 1 Onshore Rovuma Acreage Operator Partner 9,562 km 2 14,958 Km 2 Anadarko 36.5% Anadarko 35.7% Mitsui ENH Bharat Petroleum Videocom Cover Energy 20.0% 15.0% 10.0% 10.0% 8.5% Maurel & Prom Wentworth Resources ENH Cove Energy 27.7% 11.6% 15.0% 10.0% Contingent Resources 27 to 60+ Tcf (P90 P10 recoverable) Anadarko Source: PTTEP 15

16 Key Takeaways The rise of North American unconventional is a gamechanging event Other majors e.g. China Argentina will take time to develop unconventional gas. North America remain unconventional gas leader in next decade LNG from unconventional will add into world market. Natural gas price disparities among North America, Europe, and Asia will reduce Asia NOCs shall build up capability and be ready to cope with unconventional challenges 16

17 Thank you PASSION TO EXPLORE WITH RESPONSIBILITY Effectiveness and Transparency drive our Growth and Stability At PTTEP we commit to strong Corporate Governance 17