European Gas Markets Summit. February 15th 2011

|

|

|

- Ashlee Short

- 6 years ago

- Views:

Transcription

1 Will oil indexation in long term take or pay contracts survive the current divergence between the prices of crude oil and traded gas? Howard V Rogers Senior Research Fellow, OIES Natural Gas Programme howard.rogers@oxfordenergy.org European Gas Markets Summit February 15th

2 OIES* Natural Gas Research Programme WE ARE: a gas research programme at an independent academic institute, part of Oxford University, specialising in fossil fuel research WE ARE NOT: consultants sellers of exclusive, high price business reports WE PRODUCE: independent research on national and international gas issues WE ARE FUNDED BY: sponsorship by companies and governments in gas producing and consuming countries Information about our Institute, our Programme and its publications can be found on our website: *Oxford Institute for Energy Studies is an educational charity 2 2 2

3 Relevant Published Papers Is there a rationale for the continuing link to oil product prices in Continental European long term gas contracts? Jonathan Stern, April 2007 Continental European Long Term Gas Contracts: is a transition away from oil product-linked pricing inevitable and imminent? Jonathan Stern, September 2009 LNG trade-flows in the Atlantic Basin, trends and discontinuities, Howard Rogers March 2010 Free to download from 3 3

4 Key Themes Why traditional long-term contracts are largely indexed to oil. The pressures for change parts 1 and 2 Are the current concessions the thin end of the wedge or just a temporary phenomenon? 4

5 The original rationale for indexing gas prices to oil in long term contracts Groningen Field, Holland Low Cost Base, pricing dilemma Priced on basis of competitiveness with consumers alternative fuels (oil products). Same rationale adopted for pipeline imports from Russia, Norway and North Africa. Contract price linked to time averaged values of fuel oil and gasoil with contract year (October September) requirement to take or pay for circa 85% of the Annual Contract Quantity. Price re-openers periodically. 5

6 Reasons cited for continuing the linkage between oil and gas prices Oil and gas compete for the same enduser market. Oil and gas compete for upstream resources. Oil Indexation required to mitigate upstream and transportation investment risk. 6

7 Oil and Gas Compete for Same End User Market? US Power Generation Produced from Natural Gas and Oil Products Source: EIA 7

8 Oil and Gas Compete for Upstream Resources? US Gas and Oil Operating Rig Count Source: Baker Hughes 8

9 A More Accurate Assessment: For the US for : Oil and gas prices only establish links infrequently because there is only limited burner tip competition, and this only pertains within a certain range of supply demand tension. Oil and Gas Upstream opportunities are pursued on their own merit, although upward pressure on upstream cost base will effect the LRMC of both oil and gas. 9

10 Oil Indexation Mitigates Upstream Risk? European Gas Market similar in size to US Market (550 bcma vs 650 bcma). If oil indexed contracts disappeared overnight there is no reason to believe Europe would be destined to remain less liquid* than US. UK Market has very successfully attracted new supply and infrastructure without resort to oil-indexed contracts. Oil Indexation passes risk onto end-users whose business may not be related to oil * Ability to absorb incremental new supplies without significant market disruption. 10

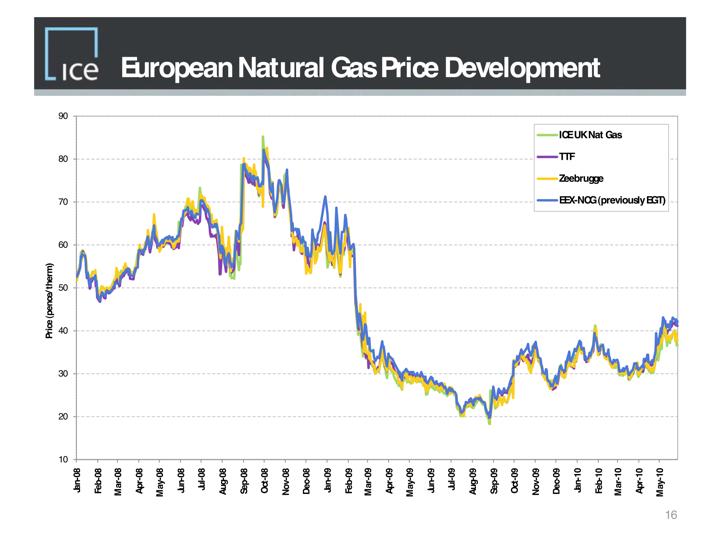

11 European Oil-Indexed Contract Prices have bunched to form an arbitrage band Source: Argus LNG 11

12 UK Gas Prices Past Convergence Nov 2005 cold weather. Limited IUK imports due to CSO on Continent. Coincided with High Asian spot LNG prices and Hurricane Katrina Rough Storage Facility down until June 2006 due to fire. Bacton Terminal fire. Russia- Ukraine Crisis. AGIP Recession hits demand & supply glut. Shutdown of IUK due to Liquids Contamination NBP UK Market tightening due to production decline. Langeled pipeline starts up. CATS Pipeline outage. Japanese Kashiwazaki- Kariwa Nuclear plant down; tight LNG market Cold winter 09/10 allows arbitrage with continent. LNG supply variable. Sources: Platts, BAFA, 12

13 The Pressures for Change 1 The Supply Glut Surge in Global LNG Supply, Surge in US shale gas production, Reduction in gas demand due to recession. 13

14 European LNG Imports Jan 2005 Dec 2010 The Wave Hits Europe Source: Waterborne LNG 14

15 mmcm/day 3,000 2,500 2,000 1,500 1, ,500 3,000 2,500 2,000 1,500 1, Demand in Key Global LNG Europe Demand vs 2008: - 5.3% YTD 2010 vs 2009: +7.3% Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec US, Canada & Mexican Demand vs 2008: - 1.1% YTD 2010 vs 2009: +5.3% Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Source: IEA Monthly Data, EIA, Waterborne LNG Markets 700 mmcm/day mmcm/day Asia LNG Imports vs 2008: - 3.9% vs 2009: % - Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 600 Asia LNG Imports Japan, Korea, Taiwan Japan, Korea, Taiwan Japan, Korea, Taiwan 2010 vs 2009: % vs 2009: % 2010 China, India China, India China, India Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 15

16 Gas Prices AGIP = Average German Import Price (Oil Indexed Gas) NBP = UK National balancing Point Price HH = Henry Hub US Price Brent Japanese cif LNG AGIP Predictor AGIP NBP HH Sources: Argus, BAFA, EIA, ICIS Heren, Own analysis 16

17 North Atlantic LNG Balance North America LNG Imports 0 Storage Inj./Withdrawal Europe Supply & Demand Demand LNG Imports Domestic Production Pipeline ACQ CY 07/08 109% CY 08/09 CY 09/10 CY 10/11 CY 11/12 CY 12/13 Pipeline of ACQ 92% 98% % 102% 112% Pipeline imports (Russia, N Africa, Azerbaijan & Iran) Sources: IEA Monthly Data, Waterborne LNG, Own Analysis % of TOP level achieved 17

18 The Pressures for Change 2 Buyer Psychology Liberalisation has changed the market characteristics (to the detriment of LT contract buyer): EU and National Legislation (3 rd Package) Destination clauses abolished. Unbundling Rules TPA for Infrastructure Capacity Allocation and Congestion Management Rules. Commitments of EU gas-importing companies regarding release of entry capacities. Limitations of long-term sales contracts Reduction of TSO market areas in Germany. Source: E.On Ruhrgas 18

19 Klaus Schafer, Eon-Ruhrgas, ONS 2010 Hubs are the reference point when customers talk to us LTC s in their current form no longer reflect the market We have to re-engineer the LTC s to anticipate the future needs of the market: price levels, indexation and review mechanism

20 Europe s Gas Schizophrenia Traditional Utility Mindset Trading Mindset If necessary I m willing to pay a premium over spot prices for flexibility. I (hope I) can force my customers to buy gas from me at oil indexed prices. I m not especially concerned what the absolute hub price level is, provided I m not exposed to higher cost supply positions. I can take storage capacity if I need flexibility. 20

21 Concessions & Impacts Norwegian Gas to European Continent: 15% priced on spot (WGI 21/4/2010). Gazprom to Unspecified Italian buyer: Period of carry forward of underlifted 2009 gas extended from 3 to 5 years, reductions in take or pay volumes for a few years, lower price for gas taken above take or pay levels. (WGI 17/2/2010) Wingas to Eneco an element of non-traditional pricing (WGI 5/1/2011) Gazprom to E.On Ruhrgas: future take or pay gas from Gazprom will be partially indexed to spot prices; the portion being in the low double digits (WGI 24/2/2010) 21

22 Observed Impact on Average German Import Price 22

23 European Long Term Contracts: Evolution? Trader? 23

24 European Contracts - Evolutionary Paths? UK Liberalisation & Oversupply Uncontracted Gas UK British Gas Long Term Indexed Contracts Hub indexed LTC s Renegotiated Multi/mixed -? Indexed Contracts EU Policy & Oversupply Continental European LT Oil Indexed Contracts 24

25 Be Careful What you Wish for. A liberalised European market would be one where 25% of supply is Russian Pipeline gas. Gazprom export monopoly could heavily influence hub prices through market power. However, this would encourage other supply sources to supply Europe (shale gas, LNG ). At least we would have a grown-up commodity market where price reflected fundamentals. 25

26 Conclusions Continuing Rationale for Oil Indexed Contracts? Largely historic: Gas preferred fuel in domestic and residential space heating and the power sector. But producers like it. In the short term it provides the perception of a low-risk cocoon. In the longer term it erodes power demand growth relative to coal, and industrial demand to overseas markets where gas prices are lower. Oil-Indexed Contracts have Dominated the European Market Apart from periods of abnormal supply surplus/tightness, European hub prices have converged on oil indexed prices through arbitrage. The argument that traded hub liquidity is too low, when used to justify maintaining oil indexation, is a circular one. If oil indexation disappeared tomorrow, Europe would be a liquid traded market almost as large as the US. Pressures for Change The supply glut left many buyers unable to meet ToP in CY 2008/9 and they are still disadvantaged relative to hub prices in CY 2009/10. As the system tightens (in large part due to cold winters and Asian LNG demand growth) the supply glut catalyst is receding. The ongoing pressure for change is now driven by buyer psychology. Mixed indexation and even hub-indexed long term contracts may be transitionary species on an evolutionary path to a liberalised European market. Be Careful What You Wish For.. Upstream producers who like oil-indexed contracts could be tempted by the prospect of being able to fine tune hub prices given their market power. However, like OPEC in the oil sector, this may also incentivise new sources of supply, more able to access a liberalised European market. 26

27 Thank You for your attention. Howard V Rogers Senior Research Fellow, OIES Natural Gas Programme howard.rogers@oxfordenergy.org 27

28 28 28

European Gas Contracts: Will Oil-Indexation Persist?

European Gas Contracts: Will Oil-Indexation Persist? Howard V Rogers Senior Research Fellow, OIES Natural Gas Programme BIEE Seminar Gas Outlook Winter 2011 and Beyond 10th October 2011 OIES Natural Gas

European Gas Contracts: Will Oil-Indexation Persist? Howard V Rogers Senior Research Fellow, OIES Natural Gas Programme BIEE Seminar Gas Outlook Winter 2011 and Beyond 10th October 2011 OIES Natural Gas

Energy in 2011 disruption and continuity

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Richard de Caux, Refining Analyst, Group Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Richard de Caux, Refining Analyst, Group Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding

Energy in 2011 disruption and continuity

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Paul Appleby, Head of Energy Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding remarks Energy

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Paul Appleby, Head of Energy Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding remarks Energy

Gas Pricing in Transi,on: different issues in different regions

Gas Pricing in Transi,on: different issues in different regions Professor Jonathan Stern Chairman and Senior Research Fellow OIES Gas Programme UKERC Workshop: The Global Gas Challenge implica,ons for

Gas Pricing in Transi,on: different issues in different regions Professor Jonathan Stern Chairman and Senior Research Fellow OIES Gas Programme UKERC Workshop: The Global Gas Challenge implica,ons for

Oxford Institute for Energy Studies Natural Gas Programme Howard V Rogers

Oxford Institute for Energy Studies Natural Gas Programme Howard V Rogers LNG Costs, Russian Exports and Global Interactions December 9 th & 1 th 215 WE ARE: A gas research programme at a Recognised Independent

Oxford Institute for Energy Studies Natural Gas Programme Howard V Rogers LNG Costs, Russian Exports and Global Interactions December 9 th & 1 th 215 WE ARE: A gas research programme at a Recognised Independent

International gas markets: recent developments and prospects

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

International Pressures on European Energy Supplies: what are the natural gas issues?

International Pressures on European Energy Supplies: what are the natural gas issues? Professor Jonathan Stern Chairman and Senior Research Fellow, Natural Gas Research Programme, Oxford Institute for

International Pressures on European Energy Supplies: what are the natural gas issues? Professor Jonathan Stern Chairman and Senior Research Fellow, Natural Gas Research Programme, Oxford Institute for

An overview of the European Energy Markets

An overview of the European Energy Markets The European energy markets remain very unsettled Despite positive achievements, many challenges have to be overcome at COP21 conference Utilities financial performances

An overview of the European Energy Markets The European energy markets remain very unsettled Despite positive achievements, many challenges have to be overcome at COP21 conference Utilities financial performances

The European Gas Market Rodrigo Pinto Scholtbach Senior Gas Market Analyst International Energy Agency Paris 3th September, The Hague

The European Gas Market 2015-2020 Rodrigo Pinto Scholtbach Senior Gas Market Analyst International Energy Agency Paris 3th September, The Hague Europe: an atypical market Growing demand / Increase of self

The European Gas Market 2015-2020 Rodrigo Pinto Scholtbach Senior Gas Market Analyst International Energy Agency Paris 3th September, The Hague Europe: an atypical market Growing demand / Increase of self

2010 Winter Outlook & a future view

2010 Winter Outlook & a future view Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Presentation

2010 Winter Outlook & a future view Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Presentation

New Delhi 24 November th IEF-IGU Ministerial Gas Forum IEF Background Materials

New Delhi 24 November 2016 5 th IEF-IGU Ministerial Gas Forum IEF Background Materials Overview 1. 3+3 Challenges 2. 7 Observations on gas markets 3. What the JODI Gas Data Base Shows 4. 3 Proposals 7

New Delhi 24 November 2016 5 th IEF-IGU Ministerial Gas Forum IEF Background Materials Overview 1. 3+3 Challenges 2. 7 Observations on gas markets 3. What the JODI Gas Data Base Shows 4. 3 Proposals 7

those where domestic gas prices and affordability both in absolute terms and relative to other sources of energy are likely to restrict development of

Can Demand for Imported LNG in Asia Increase Because It is a Cleaner Energy Source? Jonathan Stern * Introduction During the period 2014-21, global LNG supply is expected to increase from around 320 Bcm

Can Demand for Imported LNG in Asia Increase Because It is a Cleaner Energy Source? Jonathan Stern * Introduction During the period 2014-21, global LNG supply is expected to increase from around 320 Bcm

Bcma Global LNG Liqufaction capacity existing & FID d/under construction

OXFORD INSTITUTE FOR ENERGY STUDIES Natural Gas Research Programme Asian LNG Market Development to 2025: pricing and contractual challenges Professor Jonathan Stern Chairman and Senior Research Fellow

OXFORD INSTITUTE FOR ENERGY STUDIES Natural Gas Research Programme Asian LNG Market Development to 2025: pricing and contractual challenges Professor Jonathan Stern Chairman and Senior Research Fellow

Crude Oil Price Volatility Crude oil price continued to be volatile (US$/bbl) Continued upswing in Collapse after Rehman shock Price surge aft

Continued upswing in Collapse after Rehman shock Price surge aft") Current Situation and Outlook for the Oil & Gas (LNG) Market Session 2 IEEJ/CNPC ETRI Joint Symposium November 8 th, 2017 Dr. Ken Koyama Chief economist and managing director Institute of Energy Economics,

Current Situation and Outlook for the Oil & Gas (LNG) Market Session 2 IEEJ/CNPC ETRI Joint Symposium November 8 th, 2017 Dr. Ken Koyama Chief economist and managing director Institute of Energy Economics,

Summary LNG, an increasingly important energy option in Asia and the rest of the world But challenges remain for LNG to play an expected bigger role S

Prospect and Challenges in the World and Asian LNG Market LNG Producer Consumer Conference September 19, 2012 The Institute of Energy Economics Japan Ken Koyama 0 Summary LNG, an increasingly important

Prospect and Challenges in the World and Asian LNG Market LNG Producer Consumer Conference September 19, 2012 The Institute of Energy Economics Japan Ken Koyama 0 Summary LNG, an increasingly important

Chapter 2. Background. October 2016

Chapter 2 Background October 2016 This chapter should be cited as ERIA (2016), Background, in Koyama K., I. Kutani and Y. Li (eds.), Joint Study for Liquefied Natural Gas Market. ERIA Research Project

Chapter 2 Background October 2016 This chapter should be cited as ERIA (2016), Background, in Koyama K., I. Kutani and Y. Li (eds.), Joint Study for Liquefied Natural Gas Market. ERIA Research Project

Let our team of experienced analysts provide the information and insight you need to stay ahead of the global gas markets.

OCTOBER 2017 Natural Gas Service overview The global gas market is going through a rapid evolution. Disparate and regionally separate gas markets are being brought together through the expansion of global

OCTOBER 2017 Natural Gas Service overview The global gas market is going through a rapid evolution. Disparate and regionally separate gas markets are being brought together through the expansion of global

Energy in Perspective

Energy in Perspective BP Statistical Review of World Energy 27 Christof Rühl Deputy Chief Economist London, 12 June 27 Outline Introduction What has changed? The medium term What is new? 26 in review Conclusion

Energy in Perspective BP Statistical Review of World Energy 27 Christof Rühl Deputy Chief Economist London, 12 June 27 Outline Introduction What has changed? The medium term What is new? 26 in review Conclusion

The Impact of the Recession on Gas Markets

The Impact of the Recession on Gas Markets What has changed in our Brave New World Gas demand dropped by 2% Bigger drops in OECD region, FSU, Latin America But some notable exceptions: China, India Some

The Impact of the Recession on Gas Markets What has changed in our Brave New World Gas demand dropped by 2% Bigger drops in OECD region, FSU, Latin America But some notable exceptions: China, India Some

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/82/85327793.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 6 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG and Natural Gas Price Assessment 26 th March 6 th April 2018 LNG Analysis Global LNG

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 6 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG and Natural Gas Price Assessment 26 th March 6 th April 2018 LNG Analysis Global LNG

2

The Pricing of Internationally Traded Gas: the search for new fundamentals Jonathan Stern and Howard Rogers IEEJ Tokyo, March 6, 2013 2 The Pricing of Internationally Traded Gas, ed. Jonathan Stern (OIES/OUP

The Pricing of Internationally Traded Gas: the search for new fundamentals Jonathan Stern and Howard Rogers IEEJ Tokyo, March 6, 2013 2 The Pricing of Internationally Traded Gas, ed. Jonathan Stern (OIES/OUP

The global gas market price dynamics and implications for Norway

The global gas market price dynamics and implications for Norway www.woodmac.com May 2009 Kerry Anne Shanks Delivering commercial insight to the global energy industry Introduction The energy industry

The global gas market price dynamics and implications for Norway www.woodmac.com May 2009 Kerry Anne Shanks Delivering commercial insight to the global energy industry Introduction The energy industry

Hub-based Pricing: European Lessons for Asia

Hub-based Pricing: European Lessons for Asia Alexander Medvedev Deputy Chairman of Gazprom Management Committee, Director General of Gazprom Export GASTECH North East Asia Gas Pricing Gathering Seoul,

Hub-based Pricing: European Lessons for Asia Alexander Medvedev Deputy Chairman of Gazprom Management Committee, Director General of Gazprom Export GASTECH North East Asia Gas Pricing Gathering Seoul,

Energy Research and Forecasts Analysis and Commentary Overview

Energy Research and Forecasts Analysis and Commentary Overview Analysis and Commentary Overview With Commodities Research & Forecasts exclusively available in Thomson Reuters Eikon you can take an intelligent

Energy Research and Forecasts Analysis and Commentary Overview Analysis and Commentary Overview With Commodities Research & Forecasts exclusively available in Thomson Reuters Eikon you can take an intelligent

4 TH GAS FORUM. Jean Jaylet, Senior Vice President Strategy, Markets & LNG. May 30 th, 2016

4 TH GAS FORUM Jean Jaylet, Senior Vice President Strategy, Markets & LNG May 30 th, 2016 THE LNG MARKET TODAY 2005: 143 MT 13 exporters 15 importers ~60 flows 2015: 250 MT 19 exporters 34 importers ~160

4 TH GAS FORUM Jean Jaylet, Senior Vice President Strategy, Markets & LNG May 30 th, 2016 THE LNG MARKET TODAY 2005: 143 MT 13 exporters 15 importers ~60 flows 2015: 250 MT 19 exporters 34 importers ~160

Gas Markets in 2015: Outlook and Challenges

The 418th Forum on Research Work Gas Markets in 2015: Outlook and Challenges December 19, 2014 Tetsuo Morikawa The Institute of Energy Economics, Japan Natural Gas Demand in Major Regions Natural Gas Demand

The 418th Forum on Research Work Gas Markets in 2015: Outlook and Challenges December 19, 2014 Tetsuo Morikawa The Institute of Energy Economics, Japan Natural Gas Demand in Major Regions Natural Gas Demand

3-1. Effect of Crude Oil Price Drop on the Global Energy Market

APERC Workshop at EWG52 Moscow, Russia, 18 October, 2016 3-1. Effect of Crude Oil Price Drop on the Global Energy Market James Kendell Vice President, APERC Background and outline of the study Background

APERC Workshop at EWG52 Moscow, Russia, 18 October, 2016 3-1. Effect of Crude Oil Price Drop on the Global Energy Market James Kendell Vice President, APERC Background and outline of the study Background

Effect of Crude Oil Price Drop on the Global Energy

2016/EWG52/WKSP1/003 Effect of Crude Oil Price Drop on the Global Energy Submitted by: APERC Asia Pacific Energy Research Centre Workshop Moscow, Russia 18 October 2016 APERC Workshop at EWG52 Moscow,

2016/EWG52/WKSP1/003 Effect of Crude Oil Price Drop on the Global Energy Submitted by: APERC Asia Pacific Energy Research Centre Workshop Moscow, Russia 18 October 2016 APERC Workshop at EWG52 Moscow,

Outlook for Gas Markets

IEEJ IEEJ:Published 2015 年 7 in 月 August 禁無断転載 2015 All rights reserved The 420th Forum on Research Work July 10, 2015 Outlook for Gas Markets The Institute of Energy Economics, Japan Tetsuo Morikawa Manager,

IEEJ IEEJ:Published 2015 年 7 in 月 August 禁無断転載 2015 All rights reserved The 420th Forum on Research Work July 10, 2015 Outlook for Gas Markets The Institute of Energy Economics, Japan Tetsuo Morikawa Manager,

Prospects for Corn Trade in 2018/19 and Beyond

Prospects for Corn Trade in 2018/19 and Beyond Ben Brown Department of Agricultural, Environmental, and Development Economics The Ohio State University February 15, 2019 The agricultural industry is a

Prospects for Corn Trade in 2018/19 and Beyond Ben Brown Department of Agricultural, Environmental, and Development Economics The Ohio State University February 15, 2019 The agricultural industry is a

Energy Security in North East Asia

Energy Security in North East Asia International Workshop on Cooperative Measures in Northeast Asian Petroleum Sector: Focusing on Asian Premium Issues September 6, 2003 The Palace Hotel, Seoul Ken Koyama,

Energy Security in North East Asia International Workshop on Cooperative Measures in Northeast Asian Petroleum Sector: Focusing on Asian Premium Issues September 6, 2003 The Palace Hotel, Seoul Ken Koyama,

Gas Markets Globalization: Perspectives and Limits

Gas Markets Globalization: Perspectives and Limits By: Sid Ahmed Hamdani, Senior Business Analyst, Sonatrach, Algeria Date:04 June 2012 Venue: Kuala Lumpur Towards Gas Market Globalization? Increasing

Gas Markets Globalization: Perspectives and Limits By: Sid Ahmed Hamdani, Senior Business Analyst, Sonatrach, Algeria Date:04 June 2012 Venue: Kuala Lumpur Towards Gas Market Globalization? Increasing

2005 North American Natural Gas Outlook Client Presentation

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

Are European hubs driving global gas prices?

Are European hubs driving global gas prices? Flame 2017 Olly Spinks www.timera-energy.com olly.spinks@timera-energy.com 1 Timera Energy offers expertise on value & risk in energy markets Specialist energy

Are European hubs driving global gas prices? Flame 2017 Olly Spinks www.timera-energy.com olly.spinks@timera-energy.com 1 Timera Energy offers expertise on value & risk in energy markets Specialist energy

Natural Gas Pricing and Its Future

Natural Gas Pricing and Its Future Europe as the Battleground Oil-Indexation - 1962/3 1962 Commercial quantities of natural gas forced a re-think -Notade Pous Prices based on Netback Value of alternative

Natural Gas Pricing and Its Future Europe as the Battleground Oil-Indexation - 1962/3 1962 Commercial quantities of natural gas forced a re-think -Notade Pous Prices based on Netback Value of alternative

European Gas Price, Volatility & Security of Supply

European Gas Price, Volatility & Security of Supply Dr. Ashna Rahman Head of Analytics & Consulting (EMEA) September, 213. 213 Platts, McGraw Hill Financial. All rights reserved. Key Points European gas

European Gas Price, Volatility & Security of Supply Dr. Ashna Rahman Head of Analytics & Consulting (EMEA) September, 213. 213 Platts, McGraw Hill Financial. All rights reserved. Key Points European gas

LNG and storage strategy - follow-up study - Final Presentation 27 September 2017 Jalil Jumriany Energy Markets Global Limited

LNG and storage strategy - follow-up study - Final Presentation 27 September 2017 Jalil Jumriany Energy Markets Global Limited LNG and storage strategy - follow-up study - LNG: Main Findings LNG: Main

LNG and storage strategy - follow-up study - Final Presentation 27 September 2017 Jalil Jumriany Energy Markets Global Limited LNG and storage strategy - follow-up study - LNG: Main Findings LNG: Main

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION APRIL 2018 RIYADH, SAUDI ARABIA APRIL 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECAST ON

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION APRIL 2018 RIYADH, SAUDI ARABIA APRIL 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECAST ON

LNG market transformation

LNG market transformation How the next 5 years will change the rules December 2017 www.timera-energy.com 1 Contents Section Contents Summary 5 key takeaways 3 Asian portfolio positions Top 5 Asian buyer

LNG market transformation How the next 5 years will change the rules December 2017 www.timera-energy.com 1 Contents Section Contents Summary 5 key takeaways 3 Asian portfolio positions Top 5 Asian buyer

Gas Market Report 2017

Gas Market Report 2017 Peter Fraser, Head of the Gas Coal and Power Markets Division Norwegian Ministry of Petroleum and Energy, Oslo, 5 th September 2017 IEA Gas in today s world The contribution of gas

Gas Market Report 2017 Peter Fraser, Head of the Gas Coal and Power Markets Division Norwegian Ministry of Petroleum and Energy, Oslo, 5 th September 2017 IEA Gas in today s world The contribution of gas

CenterPoint Energy Services. Current Market Fundamentals June 27, 2013

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

Another Bull Market Consolidation or. for the

Another Bull Market Consolidation or Have Oil Prices Headed South for the John Cook Director, EIA Petroleum Division New York Energy Forum September 5, Winter? Limited Spare Capacity Weather/ Hurricane

Another Bull Market Consolidation or Have Oil Prices Headed South for the John Cook Director, EIA Petroleum Division New York Energy Forum September 5, Winter? Limited Spare Capacity Weather/ Hurricane

Lunch Session. Oil and Gas Security. Aad van Bohemen, IEA/Energy Policy and Security Division 6 March 2018 (APEC-OGSNF) IEA OECD/IEA 2017

IEA OECD/IEA 2017") Lunch Session Oil and Gas Security Aad van Bohemen, IEA/Energy Policy and Security Division 6 March 2018 (APEC-OGSNF) IEA Long-term Energy Markets Outlook Key takeaways from WEO 2017 India takes the lead,

Lunch Session Oil and Gas Security Aad van Bohemen, IEA/Energy Policy and Security Division 6 March 2018 (APEC-OGSNF) IEA Long-term Energy Markets Outlook Key takeaways from WEO 2017 India takes the lead,

2009 Changing the scene

2009 Changing the scene Gas demand in Europe and in other major economies is weakening Industrial demand strongly affected by the economic crisis Demand in the power generation sector suffers from relatively

2009 Changing the scene Gas demand in Europe and in other major economies is weakening Industrial demand strongly affected by the economic crisis Demand in the power generation sector suffers from relatively

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/89/100997948.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 23 rd March 2018 [LNG MARKET ANALYSIS ] 2 LNG Price Assessment and Natural Gas 12 th 23 rd March 2018 LNG Analysis Global LNG prices

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 23 rd March 2018 [LNG MARKET ANALYSIS ] 2 LNG Price Assessment and Natural Gas 12 th 23 rd March 2018 LNG Analysis Global LNG prices

Gas Market Report 2017

Gas Market Report 2017 Center on Global Energy Policy, Columbia/SIPA Columbia Club, 13 July 2017 IEA Gas in today s world q The contribution of gas Versatile fuel within the energy system, helping to address

Gas Market Report 2017 Center on Global Energy Policy, Columbia/SIPA Columbia Club, 13 July 2017 IEA Gas in today s world q The contribution of gas Versatile fuel within the energy system, helping to address

Winter Outlook 2009/10. 8 th October 2009 Peter Parsons

Winter Outlook 29/1 8 th October 29 Peter Parsons Agenda Winters 28/9 & 29/1 Gas Demand Gas Supply Electricity Demand Electricity Supply 28/9 Overview Winter 28/9 characterised by: Periods of cold weather,

Winter Outlook 29/1 8 th October 29 Peter Parsons Agenda Winters 28/9 & 29/1 Gas Demand Gas Supply Electricity Demand Electricity Supply 28/9 Overview Winter 28/9 characterised by: Periods of cold weather,

European pricing dynamics

OXFORD INSTITUTE FOR FOR ENERGY STUDIES Natural Gas Research Programme European pricing dynamics Dr. Thierry Bros Senior Research Fellow Flame Amsterdam 11 May 2017 Main steps of European gas 1986: Privatisation

OXFORD INSTITUTE FOR FOR ENERGY STUDIES Natural Gas Research Programme European pricing dynamics Dr. Thierry Bros Senior Research Fellow Flame Amsterdam 11 May 2017 Main steps of European gas 1986: Privatisation

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET Summary findings from a comparison of data and forecast on the oil market by the International Energy Agency, and Organization of the Petroleum

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET Summary findings from a comparison of data and forecast on the oil market by the International Energy Agency, and Organization of the Petroleum

Major challenges for the Russian gas export strategy. Tatiana Mitrova, Ph. D. Gubkin University Energy Research Institute of the RAS

Major challenges for the Russian gas export strategy Tatiana Mitrova, Ph. D. Gubkin University Energy Research Institute of the RAS Groningen, 23 November, 2010 Eurasian gas market 2 New transitional period

Major challenges for the Russian gas export strategy Tatiana Mitrova, Ph. D. Gubkin University Energy Research Institute of the RAS Groningen, 23 November, 2010 Eurasian gas market 2 New transitional period

The Asian LNG Market Strides Ahead

The Asian LNG Market Strides Ahead Hong Chou Hui, Managing Editor, Platts Asia LNG Asia s LNG market continued to evolve in 2011, as the volatility of the last few years, coupled with a major crisis in

The Asian LNG Market Strides Ahead Hong Chou Hui, Managing Editor, Platts Asia LNG Asia s LNG market continued to evolve in 2011, as the volatility of the last few years, coupled with a major crisis in

LNG Market Trends & Price Transparency

LNG Market Trends & Price Transparency Tokyo Fiona Poynter April 2015 London Houston Washington New York Portland Calgary Santiago Bogota Rio de Janeiro Singapore Beijing Tokyo Sydney Dubai Moscow Astana

LNG Market Trends & Price Transparency Tokyo Fiona Poynter April 2015 London Houston Washington New York Portland Calgary Santiago Bogota Rio de Janeiro Singapore Beijing Tokyo Sydney Dubai Moscow Astana

Global Market Pulp Statistics

Global Market Pulp Statistics Bleached Kraft Pulp November Data 217 Global Statistics for Bleached Kraft Market Pulp The statistics in this file is based on EPIS (European Pulp Industry Sector) data, distributed

Global Market Pulp Statistics Bleached Kraft Pulp November Data 217 Global Statistics for Bleached Kraft Market Pulp The statistics in this file is based on EPIS (European Pulp Industry Sector) data, distributed

European gas demand and import scenarios: can we connect the future to the present?

European gas demand and import scenarios: can we connect the future to the present? Professor Jonathan Stern, Chairman and Senior Research Fellow OIES Gas Programme GAC Seminar on Scenarios and Forecasts,

European gas demand and import scenarios: can we connect the future to the present? Professor Jonathan Stern, Chairman and Senior Research Fellow OIES Gas Programme GAC Seminar on Scenarios and Forecasts,

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/83/87599942.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 20 th April 2018 LNG and Natural Gas Price Assessment 14 th 20 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 20 th April 2018 LNG and Natural Gas Price Assessment 14 th 20 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

Energy and commodity price benchmarking and market insights

Energy and commodity price benchmarking and market insights London, Houston, Washington, New York, Portland, Calgary, Santiago, Bogota, Rio de Janeiro, Singapore, Beijing, Tokyo, Sydney, Dubai, Moscow,

Energy and commodity price benchmarking and market insights London, Houston, Washington, New York, Portland, Calgary, Santiago, Bogota, Rio de Janeiro, Singapore, Beijing, Tokyo, Sydney, Dubai, Moscow,

The Shifting Sands of Natural Gas Abundance

August 17, 2016 The Shifting Sands of Natural Gas Abundance Richard Meyer Manager, Energy Analysis & Standards Here s how global energy changed between 2014 and 2015. Winners were oil, natural gas, renewables.

August 17, 2016 The Shifting Sands of Natural Gas Abundance Richard Meyer Manager, Energy Analysis & Standards Here s how global energy changed between 2014 and 2015. Winners were oil, natural gas, renewables.

STEAM AND COKING COAL PRICES

ENERGY PRICES AND TAXES, 3rd Quarter 2004 - xi STEAM AND COKING COAL PRICES Larry Metzroth, Principal Administrator Energy Statistics Division SUMMARY This article provides analyses of customs unit values

ENERGY PRICES AND TAXES, 3rd Quarter 2004 - xi STEAM AND COKING COAL PRICES Larry Metzroth, Principal Administrator Energy Statistics Division SUMMARY This article provides analyses of customs unit values

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION MAY 2018 RIYADH, SAUDI ARABIA MAY 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON THE

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION MAY 2018 RIYADH, SAUDI ARABIA MAY 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON THE

Hydrogen Would Prefer Russian Pipeline Gas

Hydrogen Would Prefer Russian Pipeline Gas Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* 26th meeting of the EU-Russia Gas Advisory Council s Work Stream on

Hydrogen Would Prefer Russian Pipeline Gas Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* 26th meeting of the EU-Russia Gas Advisory Council s Work Stream on

Global Gas and LNG in Flux. Michael Smith, Gas Trading Analytics BIEE Gas Outlook Seminar, 10th October 2011

Global Gas and LNG in Flux Michael Smith, Gas Trading Analytics BIEE Gas Outlook Seminar, th October 211 Cautionary Statement This presentation and its contents have been provided to you for informational

Global Gas and LNG in Flux Michael Smith, Gas Trading Analytics BIEE Gas Outlook Seminar, th October 211 Cautionary Statement This presentation and its contents have been provided to you for informational

Eeekonomics: BEG/CEE UT Annual Meeting. Commentary: European Live Issues, Post recession Demand. European gas demand post Fukushima Outline

Gas Research Programme ENERGY STUDIES Natural G Eeekonomics: BEG/CEE UT Annual Meeting Houston, 7 December 2011 Commentary: European Live Issues, Post recession Demand Dr Anouk Honore Senior Research Fellow

Gas Research Programme ENERGY STUDIES Natural G Eeekonomics: BEG/CEE UT Annual Meeting Houston, 7 December 2011 Commentary: European Live Issues, Post recession Demand Dr Anouk Honore Senior Research Fellow

How LNG Supply Additions Could Affect Gas Prices in Europe?

How LNG Supply Additions Could Affect Gas Prices in Europe? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* C5, Gas and LNG Supply Contracts Forum Berlin, June

How LNG Supply Additions Could Affect Gas Prices in Europe? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* C5, Gas and LNG Supply Contracts Forum Berlin, June

NATURAL GAS IN ASIA: The Challenges of Growth in China, India, Japan and Korea

NATURAL GAS IN ASIA: The Challenges of Growth in China, India, Japan and Korea Professor Jonathan Stern Director of Gas Research Oxford Institute for Energy Studies Institute of Energy Economics, Japan

NATURAL GAS IN ASIA: The Challenges of Growth in China, India, Japan and Korea Professor Jonathan Stern Director of Gas Research Oxford Institute for Energy Studies Institute of Energy Economics, Japan

FUTURE LNG PRICE IN ASIAN MARKET. Main author. Takeo Suzuki Senior Coordinator THE INSTITUTE OF ENERGY ECONOMICS, JAPAN JAPAN

FUTURE LNG PRICE IN ASIAN MARKET Verwijderd: THE Verwijderd: IN FUTURE Main author Takeo Suzuki Senior Coordinator THE INSTITUTE OF ENERGY ECONOMICS, JAPAN JAPAN Verwijderd:, ABSTRACT This paper reviews

FUTURE LNG PRICE IN ASIAN MARKET Verwijderd: THE Verwijderd: IN FUTURE Main author Takeo Suzuki Senior Coordinator THE INSTITUTE OF ENERGY ECONOMICS, JAPAN JAPAN Verwijderd:, ABSTRACT This paper reviews

Energy Statistics: Making the Numbers Count

Energy Statistics: Making the Numbers Count IFEG Autumn Seminar, 5 th November 29 Paul Appleby, BP Group Economics Team Working with Energy Statistics The key challenges. Finding relevant & reliable data

Energy Statistics: Making the Numbers Count IFEG Autumn Seminar, 5 th November 29 Paul Appleby, BP Group Economics Team Working with Energy Statistics The key challenges. Finding relevant & reliable data

The IEA s Gas 2017 Report - LNG moves to the front

The IEA s Gas 2017 Report - LNG moves to the front Peter Fraser, Head of the Gas, Coal and Power Division EMART Energy, Amsterdam, 5 October 2017 IEA Gas in today s world The contribution of gas Versatile

The IEA s Gas 2017 Report - LNG moves to the front Peter Fraser, Head of the Gas, Coal and Power Division EMART Energy, Amsterdam, 5 October 2017 IEA Gas in today s world The contribution of gas Versatile

Renewables investment boost in a global uncertain context

Renewables investment boost in a global uncertain context 31/3/217 Claudio Machetti 1 Technology cost reduction Cost evolution for selected technologies 28-216 12 Index 28 = 1 8 6 4 2 Upstream oil & gas

Renewables investment boost in a global uncertain context 31/3/217 Claudio Machetti 1 Technology cost reduction Cost evolution for selected technologies 28-216 12 Index 28 = 1 8 6 4 2 Upstream oil & gas

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/82/85327769.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 13 th April 2018 LNG and Natural Gas Price Assessment 3 rd 13 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 13 th April 2018 LNG and Natural Gas Price Assessment 3 rd 13 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

Wholesale Prices Drivers & Implications. John Heffernan Power Trading Manager Bord Gais Energy Limited

Wholesale Prices Drivers & Implications John Heffernan Power Trading Manager Bord Gais Energy Limited Energy s League Table 3 Gas 23.70% 4 Hydro 6.70% 5 Nuclear 4.40% 6 Renewables 2.70% 2 Your Electricity

Wholesale Prices Drivers & Implications John Heffernan Power Trading Manager Bord Gais Energy Limited Energy s League Table 3 Gas 23.70% 4 Hydro 6.70% 5 Nuclear 4.40% 6 Renewables 2.70% 2 Your Electricity

US LNG competitiveness in Asia. in changing oil and gas price

US LNG competitiveness in Asia Pacific: cost plus vs. oil indexation in changing oil and gas price environment Prof. Dr. Andrey A. Konoplyanik, Adviser to Director General, Gazprom export LLC, Professor

US LNG competitiveness in Asia Pacific: cost plus vs. oil indexation in changing oil and gas price environment Prof. Dr. Andrey A. Konoplyanik, Adviser to Director General, Gazprom export LLC, Professor

LNG Shipping: How Long Will The Good Times Last?

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

Challenges to JCC Pricing in Asian LNG Markets

February 2014 Challenges to JCC Pricing in Asian LNG Markets Howard V Rogers and Jonathan Stern OIES PAPER: NG 81 views of the Oxford Institute for Energy Studies or any of its members. Copyright 2014

February 2014 Challenges to JCC Pricing in Asian LNG Markets Howard V Rogers and Jonathan Stern OIES PAPER: NG 81 views of the Oxford Institute for Energy Studies or any of its members. Copyright 2014

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

LNG in the Asia Pacific

2016/EWG52/WKSP1/004 LNG in the Asia Pacific Submitted by: APERC Asia Pacific Energy Research Centre Workshop Moscow, Russia 18 October 2016 APERC Workshop at EWG52 Moscow, Russia, 18 October, 2016 3-2.

2016/EWG52/WKSP1/004 LNG in the Asia Pacific Submitted by: APERC Asia Pacific Energy Research Centre Workshop Moscow, Russia 18 October 2016 APERC Workshop at EWG52 Moscow, Russia, 18 October, 2016 3-2.

European gas price evolution and supply challenges

European gas price evolution and supply challenges Ben Wetherall Head of Gas ICIS Israel Energy and Business Convention 3-4 Nov 2014 Agenda European demand and price evolution Supply and challenges Turkish

European gas price evolution and supply challenges Ben Wetherall Head of Gas ICIS Israel Energy and Business Convention 3-4 Nov 2014 Agenda European demand and price evolution Supply and challenges Turkish

Energy Outlook. Kurt Barrow Vice President, Oil Markets, Midstream and Downstream Insights, IHS Markit

Energy Outlook Kurt Barrow Vice President, Oil Markets, Midstream and Downstream Insights, IHS Markit kurt.barrow@ihsmarkit.com Building a Foundation for Profitable Growth in Uncertain Markets Agenda Short-term

Energy Outlook Kurt Barrow Vice President, Oil Markets, Midstream and Downstream Insights, IHS Markit kurt.barrow@ihsmarkit.com Building a Foundation for Profitable Growth in Uncertain Markets Agenda Short-term

RYSTAD ENERGY GAS PERSPECTIVES. Jakarta, November 20 th 2017

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

European Gas Markets

European Gas Markets Globalisation; Commoditisation; Demand Destruction Pierre Noël EPRG, University of Cambridge GDF Suez Brussels, 8 February 212 EPRG, University of Cambridge Economic & social science

European Gas Markets Globalisation; Commoditisation; Demand Destruction Pierre Noël EPRG, University of Cambridge GDF Suez Brussels, 8 February 212 EPRG, University of Cambridge Economic & social science

PGC B Strategy - Triennium November 18 20, 2014 Bratislava. By: Ashkan Esmaeilifar

1 PGC B Strategy - Triennium 2012 2015 November 18 20, 2014 Bratislava By: Ashkan Esmaeilifar 2 COUNTRY PROFILE Area (km 2 ): 49,035 Population: 5,379,000 Capital: Bratislava Member of OECD, WTO, NATO,

1 PGC B Strategy - Triennium 2012 2015 November 18 20, 2014 Bratislava By: Ashkan Esmaeilifar 2 COUNTRY PROFILE Area (km 2 ): 49,035 Population: 5,379,000 Capital: Bratislava Member of OECD, WTO, NATO,

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer.

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

Japan s LNG Prices Trending Upwards

Japan s LNG Prices Trending Upwards David Wood David Wood & Associates, Lincoln UK Published in Energy Tribune December 2007 Japan is the world's largest LNG consumer and imported 81.86 bcm of natural

Japan s LNG Prices Trending Upwards David Wood David Wood & Associates, Lincoln UK Published in Energy Tribune December 2007 Japan is the world's largest LNG consumer and imported 81.86 bcm of natural

The Future of European Energy Security

The Future of European Energy Security Professor Øystein Noreng, BI Norwegian School of Management Energy and Climate Policy - Supply Security in International Comparison, 12th Annual Meeting of the Reform

The Future of European Energy Security Professor Øystein Noreng, BI Norwegian School of Management Energy and Climate Policy - Supply Security in International Comparison, 12th Annual Meeting of the Reform

Energy markets the short and the long term

Energy markets the short and the long term Christof Rühl, Chief Economist, BP BP 2012 Outline The economy A year of disruptions Long term implications Conclusion Global growth: slow and on life support

Energy markets the short and the long term Christof Rühl, Chief Economist, BP BP 2012 Outline The economy A year of disruptions Long term implications Conclusion Global growth: slow and on life support

LNG Market Outlook. South East Europe Energy Dialogue Thessaloniki, 2 nd -3 rd June, Panayotis Kanellopoulos Managing Director 1

LNG Market Outlook South East Europe Energy Dialogue Thessaloniki, 2 nd -3 rd June, 2011 Panayotis Kanellopoulos Managing Director 1 M&M GAS CO M&M Gas Co S.A. is a private corporation founded in 2010,

LNG Market Outlook South East Europe Energy Dialogue Thessaloniki, 2 nd -3 rd June, 2011 Panayotis Kanellopoulos Managing Director 1 M&M GAS CO M&M Gas Co S.A. is a private corporation founded in 2010,

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/83/87599992.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 8 th June 2018 LNG and Natural Gas Price Assessment 28 th May 8 th June 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Stable to bullish

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 8 th June 2018 LNG and Natural Gas Price Assessment 28 th May 8 th June 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Stable to bullish

WILL THERE BE A TWO-TIER LNG CONTRACT PRICING MECHANISM IN ASIA?

WILL THERE BE A TWO-TIER LNG CONTRACT PRICING MECHANISM IN ASIA? By: Kyoichi Miyazaki Majed Limam Poten & Partners, Inc., New York Date: 5 th June, 2012 Venue: Kuala Lumpur, Malaysia $/MMBtu 2 Gas prices

WILL THERE BE A TWO-TIER LNG CONTRACT PRICING MECHANISM IN ASIA? By: Kyoichi Miyazaki Majed Limam Poten & Partners, Inc., New York Date: 5 th June, 2012 Venue: Kuala Lumpur, Malaysia $/MMBtu 2 Gas prices

THE JANUARY 2009 RUSSIA- UKRAINE GAS CRISIS: implications for Europe

THE JANUARY 2009 RUSSIA- UKRAINE GAS CRISIS: implications for Europe Professor Jonathan Stern Director of Gas Research Oxford Institute for Energy Studies IMEMO, Moscow March 26, 2009 OIES* OIES* OXFORD

THE JANUARY 2009 RUSSIA- UKRAINE GAS CRISIS: implications for Europe Professor Jonathan Stern Director of Gas Research Oxford Institute for Energy Studies IMEMO, Moscow March 26, 2009 OIES* OIES* OXFORD

GLOBAL OIL MARKET TRENDS

GLOBAL OIL MARKET TRENDS Brent timeline and latest forward curve: Prompt prices recovering, back-end more stable ICE Brent crude, historical front month contract price and latest forward curve Our view

GLOBAL OIL MARKET TRENDS Brent timeline and latest forward curve: Prompt prices recovering, back-end more stable ICE Brent crude, historical front month contract price and latest forward curve Our view

Russian Pipeline Gas: Problem or Part of the Solution?

Russian Pipeline Gas: Problem or Part of the Solution? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* Flame, Amsterdam, May 14, 2018 *Views expressed in this

Russian Pipeline Gas: Problem or Part of the Solution? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* Flame, Amsterdam, May 14, 2018 *Views expressed in this

US Oil and Natural Gas Perspective

Presentation to the WEC-Mexican Committee 31 January 2018 US Oil and Natural Gas Perspective Guy Caruso Senior Advisor 1 Source: EIA 2 US Perspective: from Resource Scarcity to. - US is heading towards

Presentation to the WEC-Mexican Committee 31 January 2018 US Oil and Natural Gas Perspective Guy Caruso Senior Advisor 1 Source: EIA 2 US Perspective: from Resource Scarcity to. - US is heading towards

BP Statistical Review of World Energy

BP Statistical Review of World Energy July 2016 bp.com/statisticalreview #BPstats BP p.i.c.2016 BP Statistical Review of World Energy July 2016 2015: A year of plenty Richard de Caux, head of refining

BP Statistical Review of World Energy July 2016 bp.com/statisticalreview #BPstats BP p.i.c.2016 BP Statistical Review of World Energy July 2016 2015: A year of plenty Richard de Caux, head of refining

Fabio Ballini World Maritime University

Pricing on gas: focus on LNG sectors Fabio Ballini World Maritime University What are the benefits of LNG? Environmental Benefits Table 3: Compering alterative technologies and fuels Source: SSPA, TC/1208-05-2100

Pricing on gas: focus on LNG sectors Fabio Ballini World Maritime University What are the benefits of LNG? Environmental Benefits Table 3: Compering alterative technologies and fuels Source: SSPA, TC/1208-05-2100

GLOBALISING GAS MARKETS IS CONVERGENCE IN PROSPECT?

GLOBALISING GAS MARKETS IS CONVERGENCE IN PROSPECT? Howard V Rogers Director of Natural Gas Research Oxford Institute for Energy Studies KEYWORDS: convergence, arbitrage, hubs, JCC, contracts, Black Swans,

GLOBALISING GAS MARKETS IS CONVERGENCE IN PROSPECT? Howard V Rogers Director of Natural Gas Research Oxford Institute for Energy Studies KEYWORDS: convergence, arbitrage, hubs, JCC, contracts, Black Swans,

Regasification N. Atlantic

North Atlantic Basin LNG Week in Review 1 The report is for the week ending December 13. Table 1 to the right tracks 2013 LNG consumption in the Atlantic Basin through December 13 versus the same time

North Atlantic Basin LNG Week in Review 1 The report is for the week ending December 13. Table 1 to the right tracks 2013 LNG consumption in the Atlantic Basin through December 13 versus the same time

Strategic Natural Gas Markets

Strategic Natural Gas Markets Kang Wu and Rami Shabaneh KAPSARC Presentation at the 8th GPCA Fertilizer Convention, The Ritz-Carlton Hotel, Bahrain, September 27-28, 2017 Agenda 1. Natural Gas Supply and

Strategic Natural Gas Markets Kang Wu and Rami Shabaneh KAPSARC Presentation at the 8th GPCA Fertilizer Convention, The Ritz-Carlton Hotel, Bahrain, September 27-28, 2017 Agenda 1. Natural Gas Supply and

The Low-Cost OPEC Cycle: The Big Elephant in the Room

The Low-Cost OPEC Cycle: The Big Elephant in the Room Bassam Fattouh Oxford Institute for Energy Studies PRESENTED AT THE BANK OF ENGLAND Jan- Mar- May- Jul- Sep- Nov- Jan- Mar- May- Jul- Sep- Nov- Jan-16

The Low-Cost OPEC Cycle: The Big Elephant in the Room Bassam Fattouh Oxford Institute for Energy Studies PRESENTED AT THE BANK OF ENGLAND Jan- Mar- May- Jul- Sep- Nov- Jan- Mar- May- Jul- Sep- Nov- Jan-16

Ponzi Scheme Keeps US Market Well Supplied

www.poten.com June 30, 2011 Ponzi Scheme Keeps US Market Well Supplied Conjuring up images of the dot-com bubble of the late-1990s, the industry leveled charges of unprofessional journalism against a story

www.poten.com June 30, 2011 Ponzi Scheme Keeps US Market Well Supplied Conjuring up images of the dot-com bubble of the late-1990s, the industry leveled charges of unprofessional journalism against a story

Update on the Asian Wood Markets

Update on the Asian Wood Markets RISI North American Conference Boston, USA October 16 18, 2017 Bob Flynn Director, International Timber, RISI Copyright 2017 RISI, Inc. Proprietary Information Agenda Market

Update on the Asian Wood Markets RISI North American Conference Boston, USA October 16 18, 2017 Bob Flynn Director, International Timber, RISI Copyright 2017 RISI, Inc. Proprietary Information Agenda Market