Historical chlorine demand growth is characterized by a boom and bust cycle that tracks global GDP growth rate closely. Typically, demand will

|

|

|

- Rosemary Barnett

- 6 years ago

- Views:

Transcription

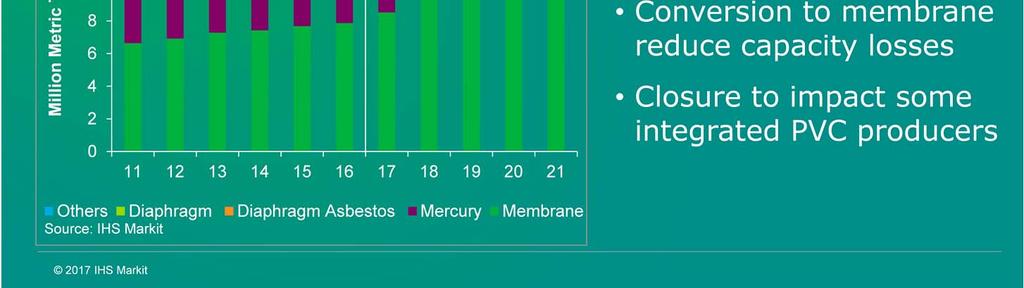

1 Historical chlorine demand growth is characterized by a boom and bust cycle that tracks global GDP growth rate closely. Typically, demand will rebound immediately after declining and this cycle seems to repeat itself every six to eight years. True enough, the decline in 2015 was followed by a swift recovery last year. What has happened? What are the changes that have occurred over the past 12 months? How will the road to recovery for global chlorine demand look like in the next five years'? This presentation will provide an update of the global chlor-alkali market, from the perspective of chlorine supply and demand, highlighting the key drivers and the regional dynamics that are shaping the global chlorine market. 1

2 Global ECU margins had stayed healthy in 2016, especially for the Northeast Asia region producers, where its ECU margins have turn the corners to generate positive return, supported by the strong recovery in caustic and PVC prices during the 2H European producers' ECU margins were still on an upward trajectory last year, while North American producers had fairly steady returns. 2

3 3

4 4

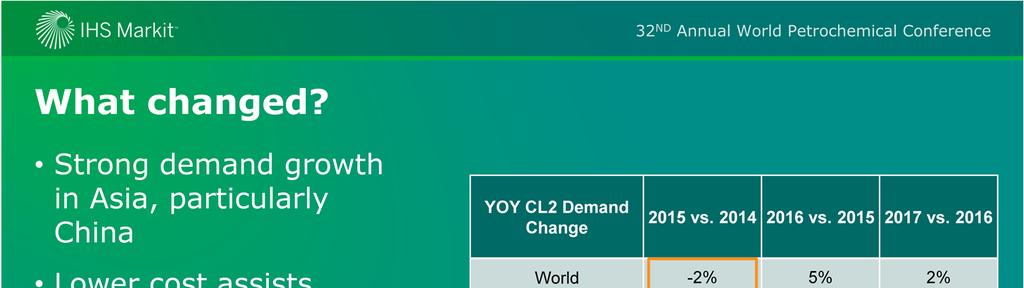

5 Historically, chlorine demand growth is characterized by a boom and bust cycle that tracks global GDP growth rate closely. Demand normally rebounds after the economy is out of recession and typically, the rate of demand growth will be faster than the rate of its decline. However, the global chlorine had experienced a peculiarity not seen before 2015, which was a demand contraction despite the global economy not being in recession. This peculiarity was a direct result of a sharp decline in China's chlorine demand in 2015, which has contracted by 5% when compared with previous year. Lower spending on construction sector and inventories overhang from raw materials to finished products in the form of unoccupied building and underutilized infrastructures are suppressing the demand for chlorine. As a result, the overall global chlorine demand shrunk by around 2.0%. The rebound in global chlorine demand growth in 2016 is rather spectacular, increasing by around 5% globally, largely supported by China's gain of about 10%. 5

6 6

7 The above graph shows chlorine capacity excess on a global basis. The numbers in the graph are derived by simply subtracting demand from capacity as shown by the bars and then dividing the net excess by capacity to derive the excess capacity on a percentage basis. Global chlorine excess capacity has stayed above the 20 percent level over the past five years. The excess in supply appears to have passed its peak in We expect an improvement going into the second half of this decade. The combined factors of Northeast Asia stopping expansion, rationalization in European capacity, little expansion in North America plus demand catching up with supply should reduce global excess to around 12 percent or less by

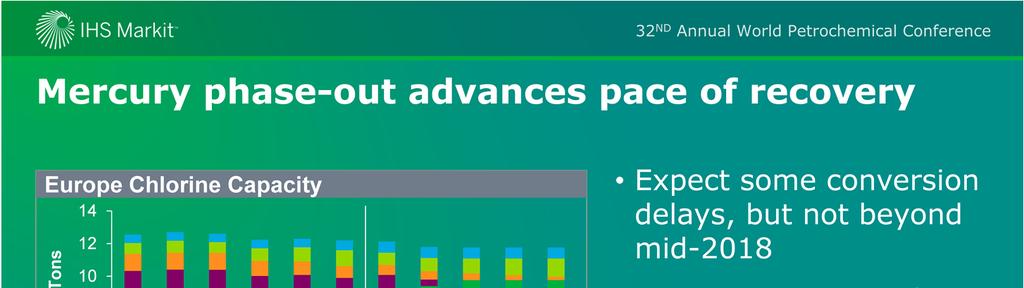

8 World chlorine capacity is now around 88 million metric tons. Over the next several years, global capacity is likely to stagnate with little expansions. However, there will be new capacity being build but mostly to replace older plants that are still employing the diaphragm and mercury cells technology. Mercury cell technology, which is primarily still used in Europe, will be nearly eliminated before the end of this decade. North America still has a substantial amount of diaphragm cell process but this will decline over time as older capacity is rationalized and new membrane cell processes are installed. 8

9 9

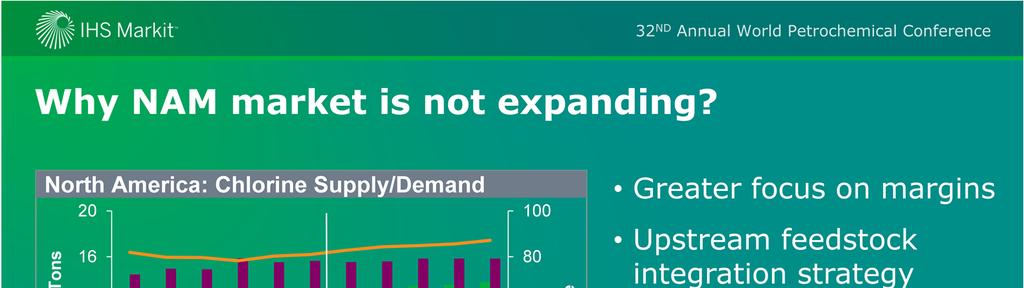

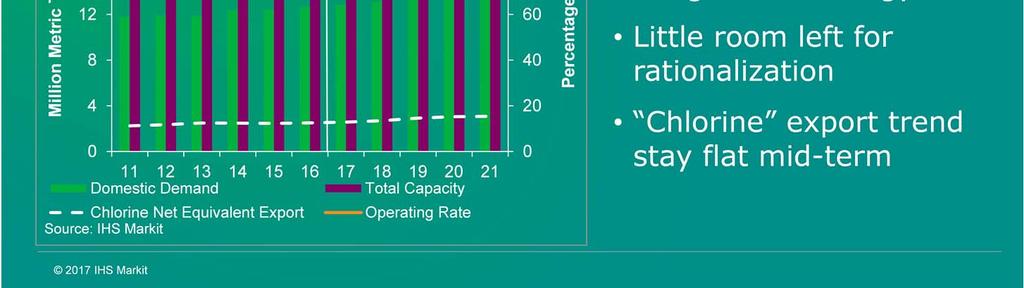

10 Over the next five years, chlorine demand in Northeast Asia is forecasted to increase by around 5.0 million metric tons, higher than supply expansion of less than half a million metric tons. This will provide an opportunity for demand to catch up with supply and the excess supply situation is expected to diminish rather quickly, resulting in improvement of plant operating rates in Northeast Asia to above 85% by China has stopped expansion. The poor return from the industry over the past several years has impacted investment decisions in China and this has been demonstrated by the absence of any large scale expansion during the second half of this decade. 10

11 The chart shows the year-on-year demand changes for chlorine, based on key downstream applications in China. The rebound in China's chlorine demand growth in 2016, estimated at around 1.8 million metric tons, was the major driver that propelled global demand to grow by 5%. Major chlorine demand improvement was seen in the Chinese vinyls and "others" sector which include demand for burner- HCL. Going forward, the average demand growth for chlorine in China is forecasted to increase by approximately 1.0 million metric tons per year from now till

12 The above chart is showing the price trends for merchant chlorine and caustic soda in the Chinese domestic market. The average ECU value over the past five years for Chinese producers has been around the $440 per ECU tons. This represents a decline of around 15% compared with the average of the previous 5 years. Based on our latest view, we expect Chinese producer's ECU value to improve to $480 per ECU tons level, on average for the next two years, largely supported by a more positive outlook on caustic prices in the domestic market. 12

13 13

14 14

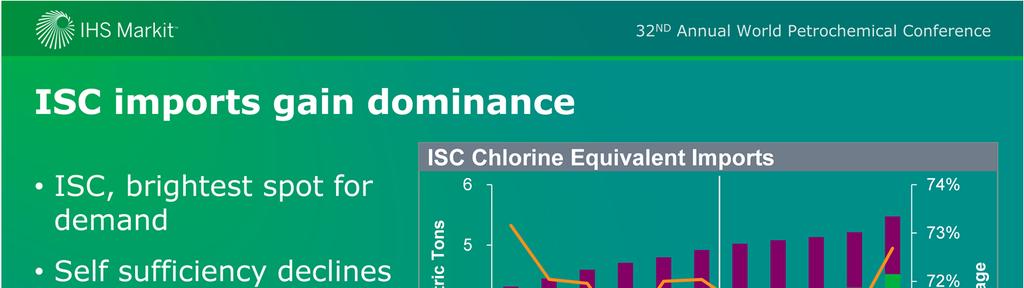

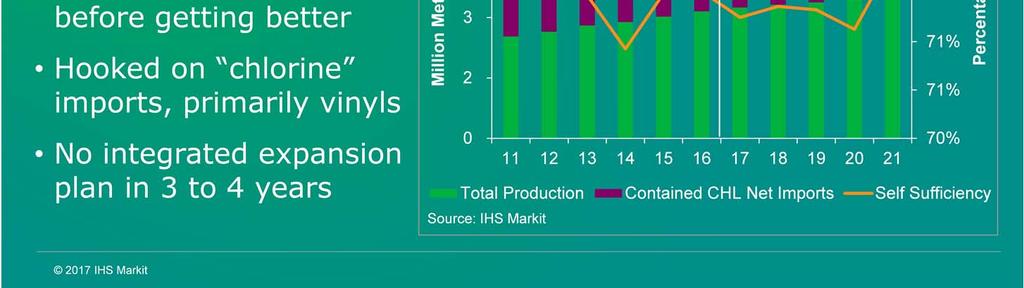

15 15

16 16

17 North America and Middle-East will have very limited investment on chlorine assets over the next 5 years despite their established status as a low cost region for energy and feedstocks. Most capital investments in the U.S. are being directed to monetize cheap gases by producing key feedstock such as ethylene. The lower capital cost and better implied return for ethylene derivative products such Polyethylene and Mono-ethylene Glycol are seen as more attractive options for downstream investment when compare with chlorine and its derivatives such as PVC. As a result, there are no aggressive plans for vinyls capacity expansion, both in North America and the Middle East. The table shows that the investment decision is skewed towards Polyethylene with very little knock-on effect on the chlor-alkali & vinyls chain. 17

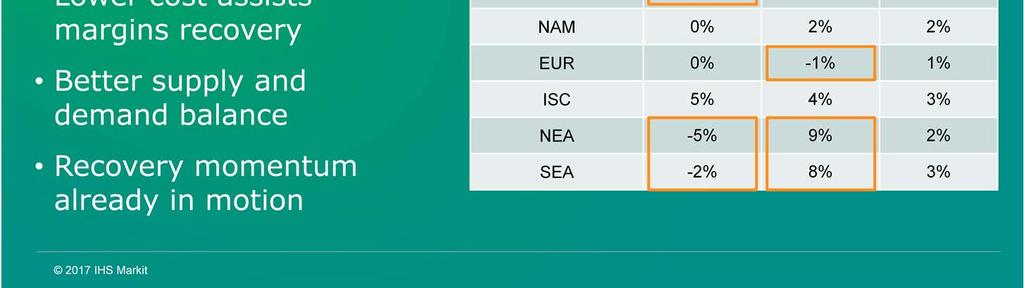

18 18

for the respective sectors in percentage.")

19 In the above chart, the size of the bubbles represents the chlorine demand from end-users in million metric ton for 2016, reading from the Y-axis. The X-axis represents IHS Markit assessment of the potential annual average growth rate (AAGR) for the respective sectors in percentage. Some chlorine derivatives markets are more important than others due to its larger market size and stronger demand growth. Vinyls product is the single largest consumer of chlorine. Although its growth projection over the next five years is forecasted at only around 2-3% per year, its contribution in term of volume expansion is close to 40% of total chlorine demand in the forecasted period. The only sector that is forecast to register a slightly negative chlorine growth rate is the pulp and paper industries. MDI, TDI and ECH will be the fastest growing market for chlorine, with their demand growing at to 4-5% per year. 19

20 Global chlorine demand is forecasted to increase by around 8 million metric tons over the next five years. This is marginally higher than our previous view due to the recovery in Northeast Asia and faster growth rates in India and China In the above chart, the size of the bubble represents the per capita consumption in KG per person for the respective region or country in 2016 while the annual average growth projection over the next five years is represented by the percentage on the X-axis. Out of the BRIC (Brazil, Russia, India and China) club, the demand growth will be driven by India & China, while domestic chlorine demand in Brazil & Russia will stagnate or register slower growth rate due to economic downturn and geopolitical conflict. 20

21 21

and Northeast Asia (NEA). NAM chlorine equivalent export is projected to expand from 2.")

22 Elementary chlorine is not traded across region, but its derivatives such as EDC, VCM and PVC are traded extensively across the world. The two major net chlorine equivalent exporters in the world are North America (NAM) and Northeast Asia (NEA). NAM chlorine equivalent export is projected to expand from 2.5 million metric tons to almost 3.0 million metric tons by 2021 via increases in EDC and PVC export volumes to Southeast Asia, India and South America. NEA chlorine equivalent export largely consists of VCM and PVC being shipped out to SEA and the Indian subcontinent, respectively. The European import and export position is projected to be almost balanced by Its net PVC export position will be "neutralized" by its requirement to import EDC from outside the region within the next five years. 22

23 Energy prices are anticipated to increase going forward and this will have an impact on regional ECU cash cost. Depending on the type of fuel sources used, the impact to cash cost will vary. In the case of North America, natural gas, the primary energy source use for the chlor-alkali industry, will see a minimum price increase, resulting in negligible changes to NAM ECU cost. Meanwhile, chlorine plants in Europe and Northeast Asia, which consume a mix coal, fuel oil and natural gas, may experience a greater impact on their ECU cost. In relative term, over the next two years, ECU cost in Northeast Asia will increase more than those in WEP and NAM markets. 23

24 Going forward, chlorine supply/demand is anticipated to improve as reinvestment on new capacity has practically stopped amid weak return, particularly in NEA. This will allow time for demand to play catch-up with capacity and towards the end of this decade, global plant operating rate is projected to reach above 85%. NEA may even need some reinvestment by the end of the decade as plant operating rate will reach above 90%. 24

25 The turning point for NEA producer's margins recovery was in Going forward, we anticipate a continuation on the region ECU margins recovery with a year-on-year improvement till it reaches its peak earning cycle towards the year In West Europe, producers ECU margins did well in 2016 and this will continues through the forecast period. West Europe is the largest beneficiary of lower energy prices and couple with its weak euro currency, has reduces its ECU cash cost in terms of the U.S. dollar. Capacity rationalization in Europe will further solidify producer s position to increase their margins, especially after We expect North American producers margins to remain robust throughout the forecast period given their advantage cost position. 25

26 26

2 nd Asia Bauxite & Alumina Conference

2 nd Asia Bauxite & Alumina Conference Global Caustic Update: Challenges and Opportunities, from a buyer s perspective. Eddie Kok Director IHS Chemical Eddie.kok@ihs.com Caustic, Impact To The Alumina

2 nd Asia Bauxite & Alumina Conference Global Caustic Update: Challenges and Opportunities, from a buyer s perspective. Eddie Kok Director IHS Chemical Eddie.kok@ihs.com Caustic, Impact To The Alumina

State of the Industry

33 Reunión Anual Latinoamericana de Petroquímica Outlook State of the Industry Global Renaissance Challenges and Opportunities Gary K. Adams Former CMAI President & Chief Advisor, IHS Chemical 2013, IHS

33 Reunión Anual Latinoamericana de Petroquímica Outlook State of the Industry Global Renaissance Challenges and Opportunities Gary K. Adams Former CMAI President & Chief Advisor, IHS Chemical 2013, IHS

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-First Meeting April 18, 2015 IMFC Statement by H.E. Abdalla Salem El-Badri Secretary-General The Organization of the Petroleum Exporting Countries

International Monetary and Financial Committee Thirty-First Meeting April 18, 2015 IMFC Statement by H.E. Abdalla Salem El-Badri Secretary-General The Organization of the Petroleum Exporting Countries

Polyester Value Chain Challenges Ahead

Polyester Value Chain Challenges Ahead IndianOil Petrochemical Conclave Sanjay Sharma, Managing Director Middle East & India February 7, 2014 Dubai, UAE Global Chemicals Investment Focused In Three Regions

Polyester Value Chain Challenges Ahead IndianOil Petrochemical Conclave Sanjay Sharma, Managing Director Middle East & India February 7, 2014 Dubai, UAE Global Chemicals Investment Focused In Three Regions

THE CHEMICALS INDUSTRY OPPORTUNITIES TO INCREASE ENERGY EFFICIENCY, TO REDUCE GREENHOUSE GAS EMISSIONS AND TO LIMIT MERCURY DISCHARGES CONCEPT NOTE

1 THE CHEMICALS INDUSTRY OPPORTUNITIES TO INCREASE ENERGY EFFICIENCY, TO REDUCE GREENHOUSE GAS EMISSIONS AND TO LIMIT MERCURY DISCHARGES CONCEPT NOTE Summary: This note provides a brief overview of the

1 THE CHEMICALS INDUSTRY OPPORTUNITIES TO INCREASE ENERGY EFFICIENCY, TO REDUCE GREENHOUSE GAS EMISSIONS AND TO LIMIT MERCURY DISCHARGES CONCEPT NOTE Summary: This note provides a brief overview of the

POLYOLEFINS THE NEVER ENDING STORY

MARCH 2016 POLYOLEFINS THE NEVER ENDING STORY Martin Wiesweg Senior Director Polymers EMEA +49 211 97550707 Martin.Wiesweg@ihs.com Western Europe stays on a slow growth path World Economic Outlook / March

MARCH 2016 POLYOLEFINS THE NEVER ENDING STORY Martin Wiesweg Senior Director Polymers EMEA +49 211 97550707 Martin.Wiesweg@ihs.com Western Europe stays on a slow growth path World Economic Outlook / March

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Eighth Meeting October 12 13, 2018 Statement No. 38-5 Statement by Mr. Barkindo OPEC Statement by H.E. Mohammad Sanusi Barkindo Secretary General

International Monetary and Financial Committee Thirty-Eighth Meeting October 12 13, 2018 Statement No. 38-5 Statement by Mr. Barkindo OPEC Statement by H.E. Mohammad Sanusi Barkindo Secretary General

World Petrochemical Markets Positioning Asia for the Future

World Petrochemical Markets Positioning Asia for the Future Gary Adams President GAdams@cmaiglobal.com APIC Marketing Seminar by CMAI Singapore, May 27, 2008 Singapore Shanghai 2008 APIC New York CMAI

World Petrochemical Markets Positioning Asia for the Future Gary Adams President GAdams@cmaiglobal.com APIC Marketing Seminar by CMAI Singapore, May 27, 2008 Singapore Shanghai 2008 APIC New York CMAI

Chemicals Industry Outlook

Chemicals Industry Outlook VERSION 02 YEAR 13 OUTLOOK: Positive fundamentals & outlook www.eulerhermes.us Key Points The U.S. chemical manufacturing industry is growing and is supported by increasing demand

Chemicals Industry Outlook VERSION 02 YEAR 13 OUTLOOK: Positive fundamentals & outlook www.eulerhermes.us Key Points The U.S. chemical manufacturing industry is growing and is supported by increasing demand

WOOD INDUSTRY SECTOR OVERVIEW OCTObER 2016

WOOD INDUSTRY SECTOR OVERVIEW october 2016 global market The Global Sawlog Price Index (GSPI) increased by 4.2% in the second quarter of 2016 when compared to the first quarter This increase is the greatest

WOOD INDUSTRY SECTOR OVERVIEW october 2016 global market The Global Sawlog Price Index (GSPI) increased by 4.2% in the second quarter of 2016 when compared to the first quarter This increase is the greatest

Statement by H.E. Mohammad Sanusi Barkindo Secretary General Organization of the Petroleum Exporting Countries (OPEC) to the Intergovernmental Group

to the Intergovernmental Group") Statement by H.E. Mohammad Sanusi Barkindo Secretary General Organization of the Petroleum Exporting Countries (OPEC) to the Intergovernmental Group of Twenty Four (G-24) Meeting of Ministers and Governors

Statement by H.E. Mohammad Sanusi Barkindo Secretary General Organization of the Petroleum Exporting Countries (OPEC) to the Intergovernmental Group of Twenty Four (G-24) Meeting of Ministers and Governors

Industrial Prices a cyclical rebound, a muted recovery, or no recovery at all?

Pricing & Purchasing Summit Industrial Prices a cyclical rebound, a muted recovery, or no recovery at all? 26 September 2016 ihsmarkit.com John Mothersole, Director, +1 202 481 9227, john.mothersole@ihsmarkit.com

Pricing & Purchasing Summit Industrial Prices a cyclical rebound, a muted recovery, or no recovery at all? 26 September 2016 ihsmarkit.com John Mothersole, Director, +1 202 481 9227, john.mothersole@ihsmarkit.com

Monthly Bulletin January 2014

Monthly Bulletin January 2014 Page 2 of 12 Executive Summary Butadiene: The US butadiene contract price marker posted by IHS Chemical increased 1 cent per pound to 55.4 cents per pound ($1,221 per ton)

Monthly Bulletin January 2014 Page 2 of 12 Executive Summary Butadiene: The US butadiene contract price marker posted by IHS Chemical increased 1 cent per pound to 55.4 cents per pound ($1,221 per ton)

Downstream Polymers Industry Outlook

Downstream Polymers Industry Outlook Presentation at Textiles and Plastics Investors Conclave Surat, India 02 September 2018 Sanjay Sharma Vice President, IHS Markit Chemical Consulting Middle East and

Downstream Polymers Industry Outlook Presentation at Textiles and Plastics Investors Conclave Surat, India 02 September 2018 Sanjay Sharma Vice President, IHS Markit Chemical Consulting Middle East and

IHS CHEMICAL Chlor-Alkali Process Summary. Process Economics Program Review Chlor-Alkali Process Summary. PEP Review

` IHS CHEMICAL Process Economics Program Review 2016-12 September 2016 ihs.com PEP Review 2016-12 Ron Smith Sr. Principal Analyst IHS Chemical PEP Review 2016-12 PEP Review 2016-12 Ron Smith, Sr. Principal

` IHS CHEMICAL Process Economics Program Review 2016-12 September 2016 ihs.com PEP Review 2016-12 Ron Smith Sr. Principal Analyst IHS Chemical PEP Review 2016-12 PEP Review 2016-12 Ron Smith, Sr. Principal

ACP2005:World Trade Outlook 6 Countries

_ ACP2005:World Trade Outlook 6 Countries GLOBAL MACROECONOMIC SCENARIOS AND WORLD TRADE STATISTICS AND FORECAST FOR THE PANAMA CANAL AUTHORITY Contract SAA-146531 World Sea Trade Outlook World Sea Trade

_ ACP2005:World Trade Outlook 6 Countries GLOBAL MACROECONOMIC SCENARIOS AND WORLD TRADE STATISTICS AND FORECAST FOR THE PANAMA CANAL AUTHORITY Contract SAA-146531 World Sea Trade Outlook World Sea Trade

Outlook for Global Recovered Paper (RCP or PfR) Markets

Markets") Outlook for Global Recovered Paper (RCP or PfR) Markets European Conference March 217 Kurt Schaefer VP, Fiber Hannah Zhao Senior Economist, Recovered Paper PMIs Booming in China and Globally Official (China),

Outlook for Global Recovered Paper (RCP or PfR) Markets European Conference March 217 Kurt Schaefer VP, Fiber Hannah Zhao Senior Economist, Recovered Paper PMIs Booming in China and Globally Official (China),

OPEC Statement to the Spring Meetings of the IMF/World Bank, April Copyright 2019 OPEC

Statement by H.E. Mohammad Sanusi Barkindo Secretary General Organization of the Petroleum Exporting Countries (OPEC) to the Intergovernmental Group of Twenty Four (G-24) Meeting of Ministers and Governors

Statement by H.E. Mohammad Sanusi Barkindo Secretary General Organization of the Petroleum Exporting Countries (OPEC) to the Intergovernmental Group of Twenty Four (G-24) Meeting of Ministers and Governors

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION APRIL 2018 RIYADH, SAUDI ARABIA APRIL 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECAST ON

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION APRIL 2018 RIYADH, SAUDI ARABIA APRIL 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECAST ON

Argus Ethylene Annual 2017

Argus Ethylene Annual 2017 Market Reporting Petrochemicals illuminating the markets Consulting Events Argus Ethylene Annual 2017 Summary Progress to the next peak of the economic cycle, now expected by

Argus Ethylene Annual 2017 Market Reporting Petrochemicals illuminating the markets Consulting Events Argus Ethylene Annual 2017 Summary Progress to the next peak of the economic cycle, now expected by

Global Petrochemical Market Outlook Planning For Growth Given Heightened Uncertainty In Market Fundamentals

ASIA CHEMICAL CONFERENCE Presentation Global Petrochemical Market Outlook Planning For Growth Given Heightened Uncertainty In Market Fundamentals November 2016, Singapore ihsmarkit.com Mark Eramo, VP Global

ASIA CHEMICAL CONFERENCE Presentation Global Petrochemical Market Outlook Planning For Growth Given Heightened Uncertainty In Market Fundamentals November 2016, Singapore ihsmarkit.com Mark Eramo, VP Global

Determinants of recovered plastics and recovered paper prices. October 2008

Determinants of recovered plastics and recovered paper prices October 2008 Overview Key relationships in the plastics and paper markets Stylised models Risk analysis - scenarios 2 Model schematic: plastics

Determinants of recovered plastics and recovered paper prices October 2008 Overview Key relationships in the plastics and paper markets Stylised models Risk analysis - scenarios 2 Model schematic: plastics

700 Quadrillion Btu History Projections. Energy Consumption (Quadrillion Btu) Carbon Dioxide Emissions (Million Metric Tons Carbon Equivalent) Region

Carbon Dioxide Emissions (Million Metric Tons Carbon Equivalent) Region") Highlights World energy consumption is projected to increase by 59 percent from 1999 to 22. Much of the growth in worldwide energy use is expected in the developing world in the IEO21 reference case forecast.

Highlights World energy consumption is projected to increase by 59 percent from 1999 to 22. Much of the growth in worldwide energy use is expected in the developing world in the IEO21 reference case forecast.

A new era for the global steel industry

A new era for the global steel industry Prepared for: Alacero 58: Paradisus Resort Hotel, Cancun November 2017 Prepared by: Dr. Paul Butterworth Research Manager - Steel Raw Materials, Steel Costs and

A new era for the global steel industry Prepared for: Alacero 58: Paradisus Resort Hotel, Cancun November 2017 Prepared by: Dr. Paul Butterworth Research Manager - Steel Raw Materials, Steel Costs and

IATA ECONOMIC BRIEFING APRIL 2009

IATA ECONOMIC BRIEFING APRIL 2009 AIR FREIGHT TIMELY INDICATOR OF ECONOMIC TURNING POINT Air freight has proved to be a very timely indicator of overall world trade volumes. IATA releases data on a particular

IATA ECONOMIC BRIEFING APRIL 2009 AIR FREIGHT TIMELY INDICATOR OF ECONOMIC TURNING POINT Air freight has proved to be a very timely indicator of overall world trade volumes. IATA releases data on a particular

TRCC CANADA Monthly Bulletin. December 2016 Issue

TRCC CANADA Monthly Bulletin December 2016 Issue Butadiene: In the US, IHS Chemical s marker for the December US butadiene contract price decreased 0.4 cents per pound to 52.0 cents per pound ($1,146 per

TRCC CANADA Monthly Bulletin December 2016 Issue Butadiene: In the US, IHS Chemical s marker for the December US butadiene contract price decreased 0.4 cents per pound to 52.0 cents per pound ($1,146 per

International Trade Extra-EU chemicals trade balance

The EU chemicals trade surplus at record level in 2010 Trade Flows ( billions) 150 140 130 120 110 100 90 80 70 60 50 40 30 20 10 0 47 41 39 15 21 22 1990 1994 1998 2002 2006 2010 Extra-EU balance Extra-EU

The EU chemicals trade surplus at record level in 2010 Trade Flows ( billions) 150 140 130 120 110 100 90 80 70 60 50 40 30 20 10 0 47 41 39 15 21 22 1990 1994 1998 2002 2006 2010 Extra-EU balance Extra-EU

Global Petrochemicals The Game has Changed: Shale Impact on Chemicals

Global Petrochemicals The Game has Changed: Shale Impact on Chemicals Presented by: Dewey Johnson VP Market Research-IHS-Chemical 28 February, 2013 Moody Gardens Hotel Galveston, Texas Rapidly Changing

Global Petrochemicals The Game has Changed: Shale Impact on Chemicals Presented by: Dewey Johnson VP Market Research-IHS-Chemical 28 February, 2013 Moody Gardens Hotel Galveston, Texas Rapidly Changing

STRUCTURAL CHANGES IN THE WORLD OF METHANOL

OCTOBER 2016 STRUCTURAL CHANGES IN THE WORLD OF METHANOL 34th IHS World Methanol Conference Olivier Maronneaud, Principal Analyst, global methanol/acetyls +44 20 8544 7970 Olivier.maronneaud@ihsmarkit.com

OCTOBER 2016 STRUCTURAL CHANGES IN THE WORLD OF METHANOL 34th IHS World Methanol Conference Olivier Maronneaud, Principal Analyst, global methanol/acetyls +44 20 8544 7970 Olivier.maronneaud@ihsmarkit.com

Susquehanna Chemical Conference. March 14, 2012

Susquehanna 2012 Chemical Conference March 14, 2012 1 Company Overview Olin Corporation Olin FY 2011 FY 2010 Revenue: $ 1,961 $ 1,586 EBITDA: $ 508 $ 188 Pretax Operating Inc.: $ 380 $ 77 EPS (Diluted):

Susquehanna 2012 Chemical Conference March 14, 2012 1 Company Overview Olin Corporation Olin FY 2011 FY 2010 Revenue: $ 1,961 $ 1,586 EBITDA: $ 508 $ 188 Pretax Operating Inc.: $ 380 $ 77 EPS (Diluted):

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION MAY 2018 RIYADH, SAUDI ARABIA MAY 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON THE

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION MAY 2018 RIYADH, SAUDI ARABIA MAY 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON THE

TRCC CANADA Monthly Bulletin MARCH 2016 ISSUE

TRCC CANADA Monthly Bulletin MARCH 2016 ISSUE Executive Summary Butadiene: IHS Chemical s marker for the March US butadiene contract price rolled over at 25.1 cents per pound ($553 per ton). This reflects

TRCC CANADA Monthly Bulletin MARCH 2016 ISSUE Executive Summary Butadiene: IHS Chemical s marker for the March US butadiene contract price rolled over at 25.1 cents per pound ($553 per ton). This reflects

The Great Deflation in Oil: Impact on the Polyester Chain

Information Analytics Expertise The Great Deflation in Oil: Impact on the Polyester Chain Indian Polyester 215 19 June, Mumbai Ashish Pujari, Senior Director (Aromatics & Fibers) + 65 6439 61 Ashish.Pujari@ihs.com

Information Analytics Expertise The Great Deflation in Oil: Impact on the Polyester Chain Indian Polyester 215 19 June, Mumbai Ashish Pujari, Senior Director (Aromatics & Fibers) + 65 6439 61 Ashish.Pujari@ihs.com

2011 Economic State of the B.C. Forest Sector

2011 Economic State of the B.C. Forest Sector June 2012 Prepared by Jie Shu, Economic Analyst Competitiveness and Innovation Branch 1 Questions Addressed How well is B.C. s forest sector doing? How competitive

2011 Economic State of the B.C. Forest Sector June 2012 Prepared by Jie Shu, Economic Analyst Competitiveness and Innovation Branch 1 Questions Addressed How well is B.C. s forest sector doing? How competitive

IHS REVIEWS CONTRASTING 2016 MARKETS: DRY BULK & DIRTY TANKER

Information IHS MARITIME Analytics & TRADE Expertise FEBRUARY 216 IHS REVIEWS CONTRASTING 216 MARKETS: DRY BULK & DIRTY TANKER Dalibor Gogic, Principal Analyst +44 23 253 2388 Dalibor.Gogic@ihs.com Global

Information IHS MARITIME Analytics & TRADE Expertise FEBRUARY 216 IHS REVIEWS CONTRASTING 216 MARKETS: DRY BULK & DIRTY TANKER Dalibor Gogic, Principal Analyst +44 23 253 2388 Dalibor.Gogic@ihs.com Global

CARGO E-CHARTBOOK Q OVERVIEW

CARGO E-CHARTBOOK Q OVERVIEW Airline cargo businesses are starting to see an improvement in forward looking demand indicators, but continued increases in capacity have placed downward pressure on yields

CARGO E-CHARTBOOK Q OVERVIEW Airline cargo businesses are starting to see an improvement in forward looking demand indicators, but continued increases in capacity have placed downward pressure on yields

Strategic Sourcing: Which Regional Price Discrepancies are Sustainable? Katherine Lewis Director, European Pricing and Purchasing 24 June 2009

Strategic Sourcing: Which Regional Price Discrepancies are Sustainable? Katherine Lewis Director, European Pricing and Purchasing 24 June 2009 Bottom Line Even though metals price differentials registering

Strategic Sourcing: Which Regional Price Discrepancies are Sustainable? Katherine Lewis Director, European Pricing and Purchasing 24 June 2009 Bottom Line Even though metals price differentials registering

RECENT MARKET DEVELOPMENTS

RECENT MARKET DEVELOPMENTS DSTI/SU/SC(215)9 Summary of recent developments Economic outlook has weakened Steel market sentiment is down Demand for steel falling in major economies Broad-based decline in

RECENT MARKET DEVELOPMENTS DSTI/SU/SC(215)9 Summary of recent developments Economic outlook has weakened Steel market sentiment is down Demand for steel falling in major economies Broad-based decline in

Oil Price Adjustments

Contact: Ed Sullivan, Group VP & Chief Economist, (847) 972-9006, esullivan@cement.org February 2016 Oil Price Adjustments Overview A combination of global supply and demand issues have forced oil prices

Contact: Ed Sullivan, Group VP & Chief Economist, (847) 972-9006, esullivan@cement.org February 2016 Oil Price Adjustments Overview A combination of global supply and demand issues have forced oil prices

Finnish Forest Sector Economic Outlook

Finnish Forest Sector Economic Outlook 2013 2014 Executive summary 23.10.2013 Improving Prospects for the Finnish Forest Sector The production, exports and the export unit prices of the Finnish forest

Finnish Forest Sector Economic Outlook 2013 2014 Executive summary 23.10.2013 Improving Prospects for the Finnish Forest Sector The production, exports and the export unit prices of the Finnish forest

TRENDS IN THE POLYMERS MARKET

IHS CHEMICAL TRENDS IN THE POLYMERS MARKET Jesse Tijerina, Managing Director, Consulting Americas +1 281 752 3251 jesse.tijerina@ihs.com ENERGY Million barrels per day A Period of Deflated Prices and Squeezed

IHS CHEMICAL TRENDS IN THE POLYMERS MARKET Jesse Tijerina, Managing Director, Consulting Americas +1 281 752 3251 jesse.tijerina@ihs.com ENERGY Million barrels per day A Period of Deflated Prices and Squeezed

Country Report of Taiwan, R.O.C.

Country Report of Taiwan, R.O.C. Chii Tai Chen Secretary of International Affairs Committee May, 2017 OUTLINE 1. Review of Economic Performance in 2016 and Outlook in 2017 2. Overall Condition of Steel

Country Report of Taiwan, R.O.C. Chii Tai Chen Secretary of International Affairs Committee May, 2017 OUTLINE 1. Review of Economic Performance in 2016 and Outlook in 2017 2. Overall Condition of Steel

Agrievolution Business Barometer. October Public excerpt of the survey on the worldwide development of the agricultural machinery business

Agrievolution Business Barometer Public excerpt of the survey on the worldwide development of the agricultural machinery business ober 2017 16 th edition Contact: philip.nonnenmacher@vdma.org Page 1 20th

Agrievolution Business Barometer Public excerpt of the survey on the worldwide development of the agricultural machinery business ober 2017 16 th edition Contact: philip.nonnenmacher@vdma.org Page 1 20th

PTT Polymer Marketing Company Limited Polyethylene Market in China

PTT Polymer Marketing Company Limited Polyethylene Market in China Analyst Meeting: Knowledge Sharing Session February 20, 2015 Europe Economic QE US QE Exit Interest Ukraine Russia Sanctioned Oil Price

PTT Polymer Marketing Company Limited Polyethylene Market in China Analyst Meeting: Knowledge Sharing Session February 20, 2015 Europe Economic QE US QE Exit Interest Ukraine Russia Sanctioned Oil Price

Global Gas and Steam Turbine Markets Conventional Thermal Power Expansion Driven by Emerging Markets and Rising Natural Gas Availability

Global Gas and Steam Turbine Markets Conventional Thermal Power Expansion Driven by Emerging Markets and Rising Natural Gas Availability June 2014 Executive Summary Return to contents 4 Key Findings Global

Global Gas and Steam Turbine Markets Conventional Thermal Power Expansion Driven by Emerging Markets and Rising Natural Gas Availability June 2014 Executive Summary Return to contents 4 Key Findings Global

Opportunities and Challenges from New Chemical and Plastics Investment

LSU Energy Summit 26 October 2016 Opportunities and Challenges from New Chemical and Plastics Investment Martha Gilchrist Moore Sr. Director, Policy Analysis and Economics Shifting Competitive Dynamics

LSU Energy Summit 26 October 2016 Opportunities and Challenges from New Chemical and Plastics Investment Martha Gilchrist Moore Sr. Director, Policy Analysis and Economics Shifting Competitive Dynamics

North American Timber Outlook

North American Timber Outlook Conditions Required for a Widespread Revival North American Conference October 2017 Peter Barynin Principal Economist, Timber Copyright 2017 RISI, Inc. Proprietary Information

North American Timber Outlook Conditions Required for a Widespread Revival North American Conference October 2017 Peter Barynin Principal Economist, Timber Copyright 2017 RISI, Inc. Proprietary Information

DAIRY AND DAIRY PRODUCTS

3. COMMODITY SNAPSHOTS Market situation DAIRY AND DAIRY PRODUCTS International dairy prices started to increase in the last half of 2016, with butter and whole milk powder (WMP) accounting for most of

3. COMMODITY SNAPSHOTS Market situation DAIRY AND DAIRY PRODUCTS International dairy prices started to increase in the last half of 2016, with butter and whole milk powder (WMP) accounting for most of

In the domestic market of the EU a modest growth of dairy consumption can be expected, mainly in the cheese sector.

EU Dairy Markets, Situation and Outlook, June 2017 by Erhard Richarts, Dairy Market Consultant, Chairman of IFE (Institut für Ernährungs-wirtschaft e. V., Kiel) Highlights: Special report produced for

EU Dairy Markets, Situation and Outlook, June 2017 by Erhard Richarts, Dairy Market Consultant, Chairman of IFE (Institut für Ernährungs-wirtschaft e. V., Kiel) Highlights: Special report produced for

The Outlook for the Global LPG Market

The Outlook for the Global LPG Market International LP Gas Seminar 213 Ken Otto February 28, 212 Dai-Ichi Hotel Tokyo, Japan 212, IHS Inc. No portion of this presentation may be reproduced, reused, or

The Outlook for the Global LPG Market International LP Gas Seminar 213 Ken Otto February 28, 212 Dai-Ichi Hotel Tokyo, Japan 212, IHS Inc. No portion of this presentation may be reproduced, reused, or

Finding Global End Use Markets for the Growing LPG Supply

Finding Global End Use Markets for the Growing LPG Supply March 7, 2017 Dr. Walt Hart, Vice President, IHS Natural Gas Liquids Walt.Hart@ihsmarkit.com 2 Finding Global End Use Markets for the Growing LPG

Finding Global End Use Markets for the Growing LPG Supply March 7, 2017 Dr. Walt Hart, Vice President, IHS Natural Gas Liquids Walt.Hart@ihsmarkit.com 2 Finding Global End Use Markets for the Growing LPG

Polyolefins: : North America And The World

Polyolefins: : North America And The World Nick Vafiadis Business Director - Polyolefins nvafiadis@cmaiglobal.com October, 2008 Chicago, IL, U.S.A. Singapore Shanghai Flexible Houston Packaging: New York

Polyolefins: : North America And The World Nick Vafiadis Business Director - Polyolefins nvafiadis@cmaiglobal.com October, 2008 Chicago, IL, U.S.A. Singapore Shanghai Flexible Houston Packaging: New York

By Gorkem Bolaca Director

International Steel Trading In The Light Of Global Economic Facts HONG KONG, NOVEMBER 2012 By Gorkem Bolaca Director AGENDA Economic Growth and International Trade China Turkey The Future Dynamics of the

International Steel Trading In The Light Of Global Economic Facts HONG KONG, NOVEMBER 2012 By Gorkem Bolaca Director AGENDA Economic Growth and International Trade China Turkey The Future Dynamics of the

Advanced Strategy for the Energy Future

Advanced Strategy for the Energy Future ACEEE Market Symposium on Market Transformation Elizabeth Dutrow U.S. Environmental Protection Agency April 1, 2008 1 Overview Planning for the energy future Robust

Advanced Strategy for the Energy Future ACEEE Market Symposium on Market Transformation Elizabeth Dutrow U.S. Environmental Protection Agency April 1, 2008 1 Overview Planning for the energy future Robust

EU steel market situation and outlook. Key challenges

72nd session of the OECD Steel Committee Paris, 31th May 2012 EU steel market situation and outlook Key challenges Construction: bleak 2012 outlook as project funding dries up 2011: overall growth but

72nd session of the OECD Steel Committee Paris, 31th May 2012 EU steel market situation and outlook Key challenges Construction: bleak 2012 outlook as project funding dries up 2011: overall growth but

International Grain Price Prospects and Food Security

USA Ukraine 123 North Post Oak Lane 4A Baseyna Street Suite 410 Mandarin Plaza, 8th floor Houston, Texas, 77024, USA Kyiv, 01004, Ukraine Tel: +1 (713) 621-3111 Tel: +380 (44) 284-1289 www.bleyzerfoundation.org

USA Ukraine 123 North Post Oak Lane 4A Baseyna Street Suite 410 Mandarin Plaza, 8th floor Houston, Texas, 77024, USA Kyiv, 01004, Ukraine Tel: +1 (713) 621-3111 Tel: +380 (44) 284-1289 www.bleyzerfoundation.org

CORN: MARKET TO REFLECT U.S. AND CHINESE CROP PROSPECTS

CORN: MARKET TO REFLECT U.S. AND CHINESE CROP PROSPECTS JULY 2001 Darrel Good 2001 - No. 6 Summary The USDA s June Acreage and Grain Stocks reports provided some modest fundamental support for the corn

CORN: MARKET TO REFLECT U.S. AND CHINESE CROP PROSPECTS JULY 2001 Darrel Good 2001 - No. 6 Summary The USDA s June Acreage and Grain Stocks reports provided some modest fundamental support for the corn

Improvement in global production and a gradual recovery in ending stocks over the past three years have allowed the global wheat market to balance at

Wheat Improvement in global production and a gradual recovery in ending stocks over the past three years have allowed the global wheat market to balance at much lower prices than in the 2007/08 to 2012/13

Wheat Improvement in global production and a gradual recovery in ending stocks over the past three years have allowed the global wheat market to balance at much lower prices than in the 2007/08 to 2012/13

Update: The Global Demand for Wood Fibre

Update: The Global Demand for Wood Fibre Timber Invest Europe Conference, London Bob Flynn Director, International Timber October 25, 21 End-use Market Sectors for Timberland Investments Pulp and Paper

Update: The Global Demand for Wood Fibre Timber Invest Europe Conference, London Bob Flynn Director, International Timber October 25, 21 End-use Market Sectors for Timberland Investments Pulp and Paper

Rice price relationships are becoming distorted again this year. The relatively thin rice market compared to other agricultural commodities and concen

Rice Rice price relationships are becoming distorted again this year. The relatively thin rice market compared to other agricultural commodities and concentration of trade in Asia are factors that are

Rice Rice price relationships are becoming distorted again this year. The relatively thin rice market compared to other agricultural commodities and concentration of trade in Asia are factors that are

BP Energy Outlook 2016 edition

BP Energy Outlook 216 edition Mark Finley 14th February 216 Outlook to 235 bp.com/energyoutlook #BPstats Economic backdrop Trillion, $21 25 Other 2 India Africa 15 China 1 OECD 5 OECD 1965 2 235 GDP 2

BP Energy Outlook 216 edition Mark Finley 14th February 216 Outlook to 235 bp.com/energyoutlook #BPstats Economic backdrop Trillion, $21 25 Other 2 India Africa 15 China 1 OECD 5 OECD 1965 2 235 GDP 2

CORN: SMALLER SUPPLIES ON THE HORIZON. April 2001 Darrel Good No. 3

CORN: SMALLER SUPPLIES ON THE HORIZON April 2001 Darrel Good 2001- No. 3 Summary The USDA s March Grain Stocks and Prospective Plantings report released on March 30 provided some fundamentally supportive

CORN: SMALLER SUPPLIES ON THE HORIZON April 2001 Darrel Good 2001- No. 3 Summary The USDA s March Grain Stocks and Prospective Plantings report released on March 30 provided some fundamentally supportive

Fig. 1: Scheme of the PVC integrated complex

Fig. 1: Scheme of the PVC integrated complex Main raw materials: As it can be seen from the above diagram, the main two raw materials are NaCl Salt and Natural gas (methane) which are planned to be supplied

Fig. 1: Scheme of the PVC integrated complex Main raw materials: As it can be seen from the above diagram, the main two raw materials are NaCl Salt and Natural gas (methane) which are planned to be supplied

Emerging Raw Material Supply for the Western World Market

Emerging Raw Material Supply for the Western World Market Introduction Nellie A. Perry, Vice President, C5 Monomers and Polymers, Argus DeWitt, Houston, TX For years N. America has had an abundance of

Emerging Raw Material Supply for the Western World Market Introduction Nellie A. Perry, Vice President, C5 Monomers and Polymers, Argus DeWitt, Houston, TX For years N. America has had an abundance of

Landscape of the European Chemical Industry 2017

EU28 Cefic Number of companies Turnover 28,221 520.2 billion National contact Direct Employees 1,155,000 René van Sloten Executive Director rvs@cefic.be A CORNERSTONE OF THE EUROPEAN ECONOMY The chemical

EU28 Cefic Number of companies Turnover 28,221 520.2 billion National contact Direct Employees 1,155,000 René van Sloten Executive Director rvs@cefic.be A CORNERSTONE OF THE EUROPEAN ECONOMY The chemical

Growing Pains. Soybean Meal Demand Key to U.S. Crush Industry s Outlook as Capacity Grows. Key Points: Introduction. by Will Secor.

December 2018 Growing Pains Soybean Meal Demand Key to U.S. Crush Industry s Outlook as Capacity Grows Key Points: n The historically strong crush margins that soybean processors have enjoyed in recent

December 2018 Growing Pains Soybean Meal Demand Key to U.S. Crush Industry s Outlook as Capacity Grows Key Points: n The historically strong crush margins that soybean processors have enjoyed in recent

Caustic Soda Methodology

Copyright 2014 Reed Business Information Ltd. ICIS is a part of the Reed Elsevier plc group Caustic Soda Methodology Caustic soda, with its co-product chlorine, is produced via an electrolysis of brine,

Copyright 2014 Reed Business Information Ltd. ICIS is a part of the Reed Elsevier plc group Caustic Soda Methodology Caustic soda, with its co-product chlorine, is produced via an electrolysis of brine,

Positioning for growth

Positioning for growth Investor presentation October 9, 2018 covestro.com Positioning for growth Investment highlights of new 500kt world-scale MDI plant in USA Attractive MDI industry with above GDP growth

Positioning for growth Investor presentation October 9, 2018 covestro.com Positioning for growth Investment highlights of new 500kt world-scale MDI plant in USA Attractive MDI industry with above GDP growth

Explaining and Understanding Declines in U.S. CO 2 Emissions

Explaining and Understanding Declines in U.S. CO 2 Emissions Zeke Hausfather Seven key factors, combined with the impacts of a prolonged economic slowdown, have led U.S. CO2 emissions to fall to 1996 levels,

Explaining and Understanding Declines in U.S. CO 2 Emissions Zeke Hausfather Seven key factors, combined with the impacts of a prolonged economic slowdown, have led U.S. CO2 emissions to fall to 1996 levels,

SOYBEANS: LARGE U.S. CROP, WHAT ABOUT SOUTH AMERICA?

SOYBEANS: LARGE U.S. CROP, WHAT ABOUT SOUTH AMERICA? OCTOBER 2004 Darrel Good 2004 B NO. 8 Summary The USDA now forecasts the 2004 U.S. soybean crop at 3.107 billion bushels, 271 million larger than the

SOYBEANS: LARGE U.S. CROP, WHAT ABOUT SOUTH AMERICA? OCTOBER 2004 Darrel Good 2004 B NO. 8 Summary The USDA now forecasts the 2004 U.S. soybean crop at 3.107 billion bushels, 271 million larger than the

FHWA Forecasts of Vehicle Miles Traveled (VMT): May 2014

: May 2014") FHWA Forecasts of Vehicle Miles Traveled (VMT): May 2014 Office of Highway Policy Information Federal Highway Administration May 22, 2014 Highlights Long-Term Economic Outlook Under the IHS Baseline economic

FHWA Forecasts of Vehicle Miles Traveled (VMT): May 2014 Office of Highway Policy Information Federal Highway Administration May 22, 2014 Highlights Long-Term Economic Outlook Under the IHS Baseline economic

IFA Medium-Term Fertilizer Outlook

IFA Medium-Term Fertilizer Outlook 2015 2019 Olivier Rousseau IFA Secretariat Afcome 2015 Reims, France October 21 st - 23 rd 2015 Outlook for World Agriculture and Fertilizer Demand Economic and policy

IFA Medium-Term Fertilizer Outlook 2015 2019 Olivier Rousseau IFA Secretariat Afcome 2015 Reims, France October 21 st - 23 rd 2015 Outlook for World Agriculture and Fertilizer Demand Economic and policy

Short-Term Fertilizer Outlook

A/10/170 December 2010 36 th IFA Enlarged Council Meeting New Delhi (India), 2-4 December 2010 Short-Term Fertilizer Outlook 2010-2011 Patrick Heffer and Michel Prud homme International Fertilizer Industry

A/10/170 December 2010 36 th IFA Enlarged Council Meeting New Delhi (India), 2-4 December 2010 Short-Term Fertilizer Outlook 2010-2011 Patrick Heffer and Michel Prud homme International Fertilizer Industry

Global Ethylene Vinyl Acetate(EVA) Market Study ( )

Market Study ( )") Global Ethylene Vinyl Acetate(EVA) Market Study (2014 2025) Table of Contents 1. INTRODUCTION 1.1. Introduction to Ethylene Vinyl Acetate Market Product Description Materials, Grades & Properties Industry

Global Ethylene Vinyl Acetate(EVA) Market Study (2014 2025) Table of Contents 1. INTRODUCTION 1.1. Introduction to Ethylene Vinyl Acetate Market Product Description Materials, Grades & Properties Industry

The Chlorine Industry. Alistair Steel European Sector Social Dialogue Committee 29 th September 2009

The Chlorine Industry Alistair Steel European Sector Social Dialogue Committee 29 th September 2009 Who Is Euro Chlor? We represent the European Chlor-Alkali Industry 40 members 70+ Manufacturing sites

The Chlorine Industry Alistair Steel European Sector Social Dialogue Committee 29 th September 2009 Who Is Euro Chlor? We represent the European Chlor-Alkali Industry 40 members 70+ Manufacturing sites

Disclosure of FY2015 financial results

0 Disclosure of FY2015 financial results 1 2 FY2015 first half financial highlights Revenue was 542.9 billion, up 30.1 billion compared to the same period last year. Business profit was 40.2 billion, down

0 Disclosure of FY2015 financial results 1 2 FY2015 first half financial highlights Revenue was 542.9 billion, up 30.1 billion compared to the same period last year. Business profit was 40.2 billion, down

The Future Role of Gas

The Future Role of Gas GECF Global Gas Outlook 24 Insights Presentation for the 3rd IEA-IEF-OPEC Symposium on Gas and Coal Market Outlooks Dmitry Sokolov Head of Energy Economics and Forecasting Department

The Future Role of Gas GECF Global Gas Outlook 24 Insights Presentation for the 3rd IEA-IEF-OPEC Symposium on Gas and Coal Market Outlooks Dmitry Sokolov Head of Energy Economics and Forecasting Department

Contents. The Global Paper Market Current Review

Contents The Global Paper Market Current Review Introduction... 2 Current Global Outlook for the Paper Industry... 4 Key players & Risk Rating... 4 China... 5 The USA... 5 Japan... 5 Global paper and board

Contents The Global Paper Market Current Review Introduction... 2 Current Global Outlook for the Paper Industry... 4 Key players & Risk Rating... 4 China... 5 The USA... 5 Japan... 5 Global paper and board

APEC Energy Outlook and Security Issues Asia Pacific Energy Research Centre (APERC)

") APEC Energy Outlook and Security Issues (APERC) Summary of APERC Presentation Energy demand in the APEC region is projected to rise by almost 60 percent between 1999 and 2020, at 2.1 percent per annum.

APEC Energy Outlook and Security Issues (APERC) Summary of APERC Presentation Energy demand in the APEC region is projected to rise by almost 60 percent between 1999 and 2020, at 2.1 percent per annum.

Global Price and Production Forecast

Global Price and Production Forecast Ron Plain Professor of Ag Economics, University of Missouri-Columbia, 220 Mumford Hall, Columbia, MO 65211 USA; Email: plainr@missouri.edu Introduction Last year, 2008,

Global Price and Production Forecast Ron Plain Professor of Ag Economics, University of Missouri-Columbia, 220 Mumford Hall, Columbia, MO 65211 USA; Email: plainr@missouri.edu Introduction Last year, 2008,

Wood Mackenzie Gas Market Outlook

Wood Mackenzie Gas Market Outlook Southern Gas Association April 20, 2009 Amber McCullagh Short-Term Outlook 2008 markets were volatile as underlying fundamentals shifted rapidly Three primary phases:

Wood Mackenzie Gas Market Outlook Southern Gas Association April 20, 2009 Amber McCullagh Short-Term Outlook 2008 markets were volatile as underlying fundamentals shifted rapidly Three primary phases:

CARGO E-CHARTBOOK Q OVERVIEW

CARGO E-CHARTBOOK Q OVERVIEW Airline cargo businesses are starting to see a slightly better demand environment and further improvement in forward looking indicators, but continued increases in capacity

CARGO E-CHARTBOOK Q OVERVIEW Airline cargo businesses are starting to see a slightly better demand environment and further improvement in forward looking indicators, but continued increases in capacity

AGRI-News. Magnusson Consulting Group. Agricultural Outlook Long Term Outlook Brazil Soybean Planting Larger Acres - Larger Crop

AGRI-News Magnusson Consulting Group Volume 1, Issue 3 Nov 2018 Brazil Soybean Planting Larger Acres - Larger Crop In 2018, Brazil became the largest soybean producer in the world surpassing the United

AGRI-News Magnusson Consulting Group Volume 1, Issue 3 Nov 2018 Brazil Soybean Planting Larger Acres - Larger Crop In 2018, Brazil became the largest soybean producer in the world surpassing the United

Business as Usual (BAU) Preliminary Scenario Results

Preliminary Scenario Results") 6 th APEC Energy Demand and Supply Outlook Business as Usual (BAU) Preliminary Scenario Results Cecilia Tam Deputy Vice President, APERC Asia Pacific Energy Research Centre This presentation is for review

6 th APEC Energy Demand and Supply Outlook Business as Usual (BAU) Preliminary Scenario Results Cecilia Tam Deputy Vice President, APERC Asia Pacific Energy Research Centre This presentation is for review

Moving from Irrational Exuberance to a New Normal in the Polyester & PET Value Chain

Moving from Irrational Exuberance to a New Normal in the Polyester & PET Value Chain JENNY YI SENIOR ANALYST ANALYTICS & CONSULTING, ICIS, ASIA www.icis.com 1 Corporate Structure ICIS is an independent

Moving from Irrational Exuberance to a New Normal in the Polyester & PET Value Chain JENNY YI SENIOR ANALYST ANALYTICS & CONSULTING, ICIS, ASIA www.icis.com 1 Corporate Structure ICIS is an independent

Short Term Energy Outlook March 2011 March 8, 2011 Release

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

EXECUTIVE SUMMARY. Economic Outlook for Southeast Asia, China and India Special supplement: Update June 2016 UPDATE

EXECUTIVE SUMMARY Economic Outlook for Southeast Asia, China and India 2016 Special supplement: Update June 2016 UPDATE JUNE 2016 Executive Summary: update on the Economic Outlook for Southeast Asia, China

EXECUTIVE SUMMARY Economic Outlook for Southeast Asia, China and India 2016 Special supplement: Update June 2016 UPDATE JUNE 2016 Executive Summary: update on the Economic Outlook for Southeast Asia, China

The Aluminium Industry February 2018

Introduction The Aluminium Industry February 2018 Aluminium is the second most used metal in the world after steel and the third most available element in the earth constituting almost 7.3 per cent by

Introduction The Aluminium Industry February 2018 Aluminium is the second most used metal in the world after steel and the third most available element in the earth constituting almost 7.3 per cent by

U.S. Carbon Dioxide Emissions in 2009: A Retrospective Review

U.S. Carbon Dioxide Emissions in 2009: A Retrospective Review The U.S. Energy Information Administration (EIA) recently expanded its reporting of energyrelated carbon dioxide emissions starting in the

U.S. Carbon Dioxide Emissions in 2009: A Retrospective Review The U.S. Energy Information Administration (EIA) recently expanded its reporting of energyrelated carbon dioxide emissions starting in the

The GDP growth rate remains high in India and Indonesia, the major markets in the region.

1 2 The GDP growth rate remains high in India and Indonesia, the major markets in the region. Apart from Thailand where has been hit by devastating flood, the economic conditions in Asia remained strong.

1 2 The GDP growth rate remains high in India and Indonesia, the major markets in the region. Apart from Thailand where has been hit by devastating flood, the economic conditions in Asia remained strong.

CARGO E-CHARTBOOK Q OVERVIEW

CARGO E-CHARTBOOK Q4 OVERVIEW Airline cargo businesses continue to face difficult conditions with demand for air freight falling in Q4, yields continuing to trend downward, and oil prices remaining high.

CARGO E-CHARTBOOK Q4 OVERVIEW Airline cargo businesses continue to face difficult conditions with demand for air freight falling in Q4, yields continuing to trend downward, and oil prices remaining high.

Career Strategies in Today s Market Yale School of Architecture

Career Strategies in Today s Market Yale School of Architecture 02.23.2016 - P. Bernstein 1 Overview 1. Global Economics: Where is there building? 2. Professional Economics: How does the economy affect

Career Strategies in Today s Market Yale School of Architecture 02.23.2016 - P. Bernstein 1 Overview 1. Global Economics: Where is there building? 2. Professional Economics: How does the economy affect

OECD FAO Agricultural Outlook

OECD FAO Agricultural Outlook 2018 ca 7. DAIRY AND DAIRY PRODUCTS Chapter 7. Dairy and dairy products This chapter describes the market situation and highlights the latest set of quantitative medium-term

OECD FAO Agricultural Outlook 2018 ca 7. DAIRY AND DAIRY PRODUCTS Chapter 7. Dairy and dairy products This chapter describes the market situation and highlights the latest set of quantitative medium-term

Lower Long Run Average Cotton Prices * Terry Townsend Executive Director

INTERNATIONAL COTTON ADVISORY COMMITTEE 169 K Street NW, Suite 7, Washington, DC 6 USA Telephone () 463-666 Fax () 463-695 e-mail secretariat@icac.org Lower Long Run Average Cotton Prices * Terry Townsend

INTERNATIONAL COTTON ADVISORY COMMITTEE 169 K Street NW, Suite 7, Washington, DC 6 USA Telephone () 463-666 Fax () 463-695 e-mail secretariat@icac.org Lower Long Run Average Cotton Prices * Terry Townsend

Recent trends in trade

level 2 Recent trends in trade Marc Bacchetta ERSD - WTO Trends in trade Dramatic increase in both the volumes and values of trade between 1980 and 2011, mostly manufactured goods. World trade grew much

level 2 Recent trends in trade Marc Bacchetta ERSD - WTO Trends in trade Dramatic increase in both the volumes and values of trade between 1980 and 2011, mostly manufactured goods. World trade grew much

IEF Industry Advisory Committee Workshop 27 th February,2018 India Energy & Oil demand Outlook

IEF Industry Advisory Committee Workshop 27 th February,2018 India Energy & Oil demand Outlook Dr. R.K. Malhotra Director General Federation of Indian Petroleum Industry Contents Global economy outlook

IEF Industry Advisory Committee Workshop 27 th February,2018 India Energy & Oil demand Outlook Dr. R.K. Malhotra Director General Federation of Indian Petroleum Industry Contents Global economy outlook

Energy Perspectives 2013 Long-run macro and market outlook

Energy Perspectives 213 Long-run macro and market outlook Eirik Wærness, Chief Economist Security Classificatio n: Internal Status: Draft Energy Perspectives 213 www.statoil.com/energyperspectives Outlook

Energy Perspectives 213 Long-run macro and market outlook Eirik Wærness, Chief Economist Security Classificatio n: Internal Status: Draft Energy Perspectives 213 www.statoil.com/energyperspectives Outlook

Oil and natural gas: market outlook and drivers

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Recommendation: HOLD Estimated Fair Value: $58.00-$77.00*

Recommendation: HOLD Estimated Fair Value: $58.00-$77.00* 1. Reasons for the Recommendation Reason #1 PepsiCo s strongest asset is their snack portfolio. PepsiCo is the world s largest snack food company.

Recommendation: HOLD Estimated Fair Value: $58.00-$77.00* 1. Reasons for the Recommendation Reason #1 PepsiCo s strongest asset is their snack portfolio. PepsiCo is the world s largest snack food company.

BUILDING U.S. AGRICULTURAL EXPORTS: ONE BRIC AT A TIME

BUILDING U.S. AGRICULTURAL EXPORTS: ONE BRIC AT A TIME By Jason Henderson After declining during the recession, U.S. protein exports have started to rebound with the global economy. The strength of the

BUILDING U.S. AGRICULTURAL EXPORTS: ONE BRIC AT A TIME By Jason Henderson After declining during the recession, U.S. protein exports have started to rebound with the global economy. The strength of the