Analyses market and policy trends for electricity, heat and transport Investigates the strategic drivers for RE deployment Benchmarks the impact and c

|

|

|

- Sylvia Murphy

- 6 years ago

- Views:

Transcription

Energy Seminar Tokyo, 7 March")

1 Paolo Frankl Head Renewable Energy Division International Energy Agency Institute of Energy Economics, Japan (IEEJ) Energy Seminar Tokyo, 7 March 2012 OECD/IEA 2011

2 Analyses market and policy trends for electricity, heat and transport Investigates the strategic drivers for RE deployment Benchmarks the impact and cost effectiveness of economic support policies Provides best practice policy principles Covers 56 countries and all world regions Book and 3 supporting information papers

![Generation 2010 [TWh] CAGR 2005](/docs-images/73/69333327/images/3-3.jpg "2010 [%] 338 296 31 3503 74 26.")

3 IEEJ: April 2012 All Reserved Right Strong Growth in RE Electricity and shift to Asia Wind Bioenergy Solar PV Hydro other Generation 2010 [TWh] CAGR [%] % 8.8% 50.8% 3.1% 4.6%

4 Costs are Reducing Hydro and some biomass and geothermal already cost competitive Additional technologies getting competitive in a broader set of circumstances PV decreasing costs by 19% for each doubling of cumulative installed capacity Opens up new deployment opportunities Data from Breyer and Gerlach, 2010

5 Policies could radically alter the long term energy outlook World primary energy demand by scenario Mtoe Current Policies Scenario New Policies Scenario 450 Scenario In the New Policies Scenario, demand increases by 40% between 2009 & 2035 OECD/IEA 2011

6 Low carbon power technologies come of age GW Global installed power generation capacity in the New Policies Scenario Fossil fuel additions Nuclear additions Renewable additions Existing 2010 capacity Renewables & nuclear power account for more than half of all the new capacity added worldwide through to 2035 OECD/IEA 2011

7 Efficiency gains can contribute most to emissions reductions World energy related CO 2 emissions abatement in the 450 Scenario relative to the New Policies Scenario Gt New Policies Scenario Scenario Abatement Efficiency 72% 44% Renewables 17% 21% Biofuels 2% 4% Nuclear 5% 9% CCS 3% 22% Total (Gt CO 2 ) Energy efficiency measures driven by strong policy action across all sectors account for 50% of the cumulative CO 2 abatement over the Outlook period OECD/IEA 2011

8 Moving towards cleaner forms of electricity generation Electricity generation by selected low carbon technology & share of electricity generation by scenario, 2009 and 2035 TWh Nuclear Hydro Wind Biomass Solar PV Other renew. CCS Low carbon 100% 80% 60% 40% 20% 0% Share of electricity generation 2009 Incremental to 2035 over 2009: New Policies Scenario 450 Scenario Low carbon generation increases 2.5 times between 2009 & 2035 in the New Policies Scenario & almost quadruples in the 450 Scenario OECD/IEA 2011

9 Less nuclear means more of everything else Power generation by fuel in the New Policies Scenario and Low Nuclear Case TWh : New Policies Scenario 2035: Low Nuclear Case 0 Nuclear Coal Gas Renewables The biggest chunk of the lost nuclear generation is replaced by power generation from coal, leading to a 6% increase in CO 2 emissions in the power sector OECD/IEA 2011

10 The majority of energy subsidies still go to fossil fuels World subsidies to fossil fuels consumption & renewable energy Fossil fuel consumption Renewable energy production Fossil fuels subsidies amounted to $409 billion in 2010 down from the peak of $550 billion in 2008 but still much larger than subsidies to renewables, which reached $66 billion in 2010 OECD/IEA 2011

11 The overall value of subsidies to renewables is set to rise Billion dollars (2010) Global subsidies to renewables based electricity and biofuels in the New Policies Scenario Biofuels Electricity 50 Renewable subsidies of $66 billion in 2010 (compared with $409 billion for fossil fuels), need to climb to $250 billion in 2035 as rising deployment outweighs improved competitiveness OECD/IEA

12 The door to 2 C 2 C is closing, but will we be locked in? OECD/IEA 2011 World energy related CO 2 emissions in the Current Policies and 450 Scenarios and from locked in infrastructure in 2010 and with delay Gt C trajectory 2 C trajectory Delay until 2017 Delay until 2015 Emissions from existing infrastructure Without further action, by 2017 all CO 2 emissions permitted in the 450 Scenario will be locked in by existing power plants, factories, buildings, etc.

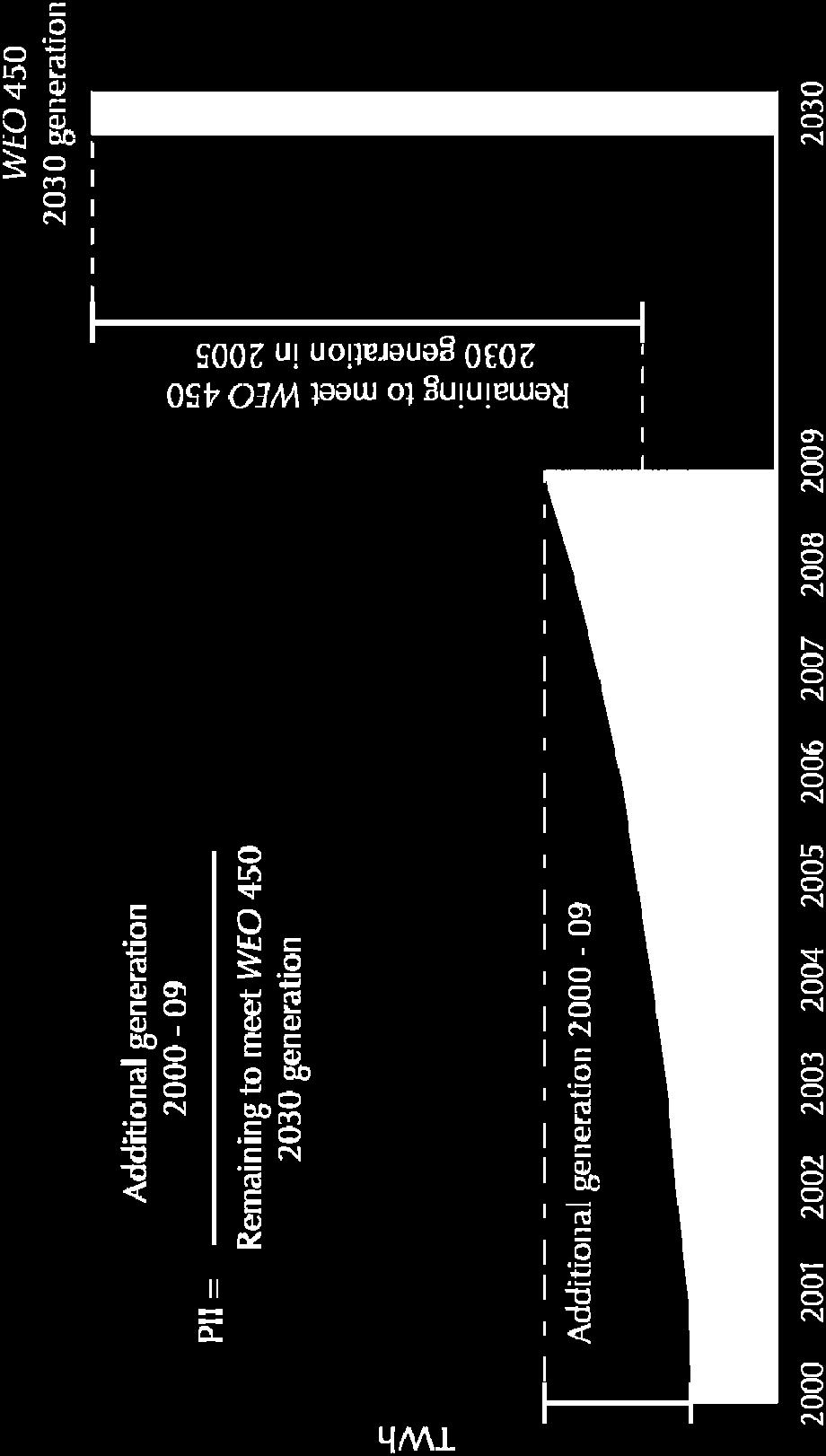

13 Measuring Policy Impact Methodology OECD/IEA, 2012

14 Are Policies Successfully Encouraging Deployment? Example: Onshore Wind OECD/IEA, 2012

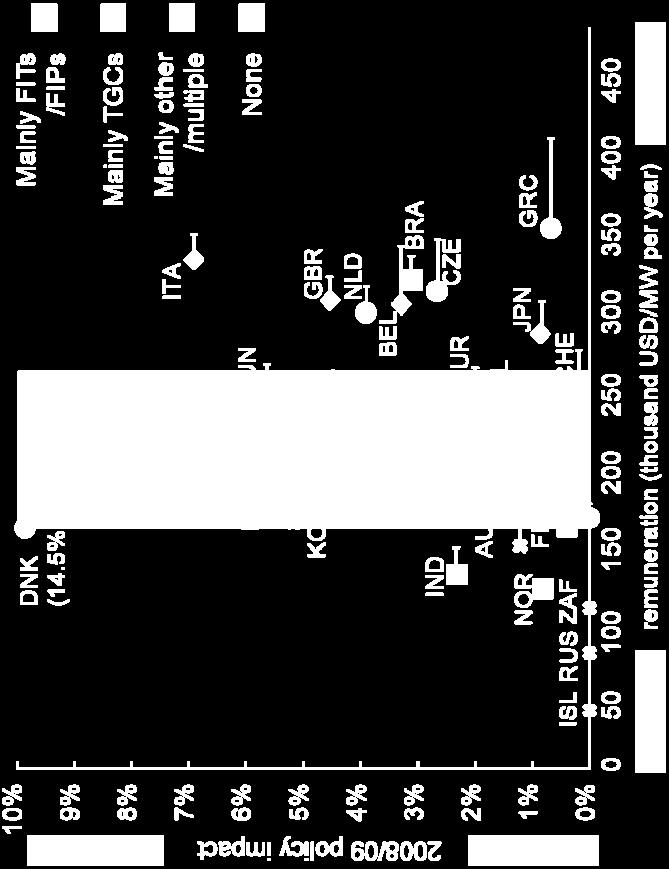

15 Are payments for Generators in a Reasonable Range? Ex: Onshore Wind 2009 OECD/IEA, 2012

16 Impact vs Cost Effectiveness Example: Onshore Wind OECD/IEA, 2012

17 Emerging Policy Challenges PV Cumulative global PV capacity Sources: IEA, EA PVPS, EPIA Concentrated booming PV growth raises policy cost concerns in several EU countries Policies are not adapting quickly enough However, pressure will reduce as new markets emerge

18 Adjust Tariffs On time & Often Solar PV in Germany Key point: Gap between incentives and costs and large, one off tariff decreases can trigger sales rush

19 Importance of var RE WEO 450 Scenario electricity projections EU 4% 15% 25% 29% 17% 32% 46% 51%

20 Emerging challenges: grid integration Variability is not new, but it does get bigger Demand Demand net of wind and solar Source: Western Wind and Solar Integration Study, GE Energy for NREL (2010)

21 Flexibility is key There are 4 flexible resources Dispatchable power plants Demand side Response (via smart grid) Energy storage facilities Interconnection with adjacent markets Industrial A biomass fired power plant residential A pumped hydro facility Scandinavian interconnections

22 Grid integration of var RE Snapshot of present penetration potentials

23 Best Practice Policy Principles Predictable RE policy framework, integrated into overall energy strategy Portfolio of incentives based on technology and market maturity Dynamic policy approach based on monitoring of national and global market trends Tackle non economic barriers Address system integration issues

24 Policy Priorities: Changing Over Time Inception Take off Consolidation Deployment Clear RE strategy and targets Attractive support Set up regulatory framework Predictable and rapidly adaptive incentives Focus on noneconomic barriers Manage total support costs System integration and transformation Market design and expose RE to competition Public acceptance Time

25 Market Expansion Opportunities New opportunities Leading countries New opportunities

26 Conclusions Policies have started delivering in terms of RE deployment and cost reduction RE getting competitive in a broader set of circumstances However major economic and non economic barriers persist and sustained policy effort is still needed Deploying Renewables identifies best practice policy principles Cost effective, dynamic, integrated approach Aims to help sharing best practice internationally so that countries can learn from each other

27 Contact: IEEJ: April 2012 All Right Reserved Links RE Publications Home > Publications > Search per Topic: Renewables RE Policy Database Contacts

Politique et sécurité énergétique dans le contexte des nouvelles énergies

Politique et sécurité énergétique dans le contexte des nouvelles énergies Didier Houssin Director, Energy Markets and Security International Energy Agency Colloque L Energie : enjeux socio-économiques

Politique et sécurité énergétique dans le contexte des nouvelles énergies Didier Houssin Director, Energy Markets and Security International Energy Agency Colloque L Energie : enjeux socio-économiques

Global trends in Renewables and the Chilean context

Global trends in Renewables and the Chilean context Carlos Gascó Travesedo Senior Analyst International Energy Agency Santiago de Chile 3 September 2011 OECD/IEA 2011 Drivers for Renewables Deployment

Global trends in Renewables and the Chilean context Carlos Gascó Travesedo Senior Analyst International Energy Agency Santiago de Chile 3 September 2011 OECD/IEA 2011 Drivers for Renewables Deployment

OECD/IEA World Energy Outlook 2011

World Energy Outlook 211 The context: fresh challenges add to already worrying trends Economic concerns have diverted attention from energy policy and limited the means of intervention Post-Fukushima,

World Energy Outlook 211 The context: fresh challenges add to already worrying trends Economic concerns have diverted attention from energy policy and limited the means of intervention Post-Fukushima,

The Role of Technology in Future Energy Supply (WEO2011, ETP2010) C. Besson, Office of Chief Economist Brussels, November 15th 2011

C. Besson, Office of Chief Economist Brussels, November 15th 2011") The Role of Technology in Future Energy Supply (WEO2011, ETP2010) C. Besson, Office of Chief Economist Brussels, November 15th 2011 Policies have a large impact on the long-term energy outlook Mtoe World

The Role of Technology in Future Energy Supply (WEO2011, ETP2010) C. Besson, Office of Chief Economist Brussels, November 15th 2011 Policies have a large impact on the long-term energy outlook Mtoe World

Fostering Long-Term Investment in Energy

Fostering Long-Term Investment in Energy Dr. Paolo Frankl Head of Renewable Energy Division International Energy Agency B20 Energy Forum, 2 October 2015 Billion dollars Oil price drop and short-term Global

Fostering Long-Term Investment in Energy Dr. Paolo Frankl Head of Renewable Energy Division International Energy Agency B20 Energy Forum, 2 October 2015 Billion dollars Oil price drop and short-term Global

Energy Technology Perspectives for a Clean Energy Future

Energy Technology Perspectives for a Clean Energy Future Ms. Maria van der Hoeven Executive Director International Energy Agency Madrid, 2 September 212 OECD/IEA 212 Key messages 1. A sustainable energy

Energy Technology Perspectives for a Clean Energy Future Ms. Maria van der Hoeven Executive Director International Energy Agency Madrid, 2 September 212 OECD/IEA 212 Key messages 1. A sustainable energy

Where do we want to go?

Where do we want to go? Dave Turk, Acting Director, Sustainability, Technology and Outlooks EU Talanoa Conference, 13 June 218, Brussels IEA Where do we want to go? Global energy-related CO 2 emissions

Where do we want to go? Dave Turk, Acting Director, Sustainability, Technology and Outlooks EU Talanoa Conference, 13 June 218, Brussels IEA Where do we want to go? Global energy-related CO 2 emissions

Medium and long-term perspectives for PV. Dr. Paolo Frankl Division Head Renewable Energy Division International Energy Agency

Medium and long-term perspectives for PV Dr. Paolo Frankl Division Head Renewable Energy Division International Energy Agency Solar Power Summit, Brussels, 7-8 March 2017 Annual additions (GW) Cumulative

Medium and long-term perspectives for PV Dr. Paolo Frankl Division Head Renewable Energy Division International Energy Agency Solar Power Summit, Brussels, 7-8 March 2017 Annual additions (GW) Cumulative

Medium Term Renewable Energy Market Report 2013

Renewable Energy Market Report 213 Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 213 OECD/IEA 213 MTRMR methodology and scope Analysis of drivers and challenges for RE

Renewable Energy Market Report 213 Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 213 OECD/IEA 213 MTRMR methodology and scope Analysis of drivers and challenges for RE

Medium Term Energy Market Outlook IEEJ Energy Seminar October 213 Keisuke Sadamori, Director, Energy Markets & Security, IEA Primary Energy Supply from Fossil Fuels Mtoe 5 45 4 35 3 25 2 15 1 5 2 21 22

Medium Term Energy Market Outlook IEEJ Energy Seminar October 213 Keisuke Sadamori, Director, Energy Markets & Security, IEA Primary Energy Supply from Fossil Fuels Mtoe 5 45 4 35 3 25 2 15 1 5 2 21 22

World Energy Outlook Dr. Fatih Birol IEA Chief Economist Rome, 18 November 2009

World Energy Outlook 29 Dr. Fatih Birol IEA Chief Economist Rome, 18 November 29 Change in primary energy demand in the Reference Scenario, 27-23 Coal Oil Gas Nuclear OECD Non-OECD Hydro Biomass Other

World Energy Outlook 29 Dr. Fatih Birol IEA Chief Economist Rome, 18 November 29 Change in primary energy demand in the Reference Scenario, 27-23 Coal Oil Gas Nuclear OECD Non-OECD Hydro Biomass Other

Agenda Short and medium term impact of the German moratorium Longer term challanges: maintaining supply security during decarbonization

Challenges in electricity a focus on Europe Agenda Short and medium term impact of the German moratorium Longer term challanges: maintaining supply security during decarbonization Germany: Moderate, 10%

Challenges in electricity a focus on Europe Agenda Short and medium term impact of the German moratorium Longer term challanges: maintaining supply security during decarbonization Germany: Moderate, 10%

Medium Term Renewable Energy Market Report Michael Waldron Senior Energy Market Analyst Renewable Energy Division International Energy Agency

Medium Term Renewable Energy Market Report 13 Michael Waldron Senior Energy Market Analyst Renewable Energy Division International Energy Agency OECD/IEA 13 Methodology and Scope OECD/IEA 13 Analysis of

Medium Term Renewable Energy Market Report 13 Michael Waldron Senior Energy Market Analyst Renewable Energy Division International Energy Agency OECD/IEA 13 Methodology and Scope OECD/IEA 13 Analysis of

Clean energy technologies: tracking progress and the role of digitalization

Clean energy technologies: tracking progress and the role of digitalization Peter Janoska and George Kamiya, Energy Environment Division, IEA COP23 16 November 2017 IEA OECD/IEA 2017 The IEA works around

Clean energy technologies: tracking progress and the role of digitalization Peter Janoska and George Kamiya, Energy Environment Division, IEA COP23 16 November 2017 IEA OECD/IEA 2017 The IEA works around

Renewables for Africa and for the World

RENEWABLE ENERGY Renewables for Africa and for the World Paul Simons Deputy Executive Director International Energy Agency SAIREC, Cape Town, 5 October 2015 Profound changes underway in energy markets

RENEWABLE ENERGY Renewables for Africa and for the World Paul Simons Deputy Executive Director International Energy Agency SAIREC, Cape Town, 5 October 2015 Profound changes underway in energy markets

World Energy Outlook 2010 Renewables in MENA. Maria Argiri Office of the Chief Economist 15 December 2010

World Energy Outlook 2010 Renewables in MENA Maria Argiri Office of the Chief Economist 15 December 2010 The context: a time of unprecedented uncertainty The worst of the global economic crisis appears

World Energy Outlook 2010 Renewables in MENA Maria Argiri Office of the Chief Economist 15 December 2010 The context: a time of unprecedented uncertainty The worst of the global economic crisis appears

Role of clean energy in the context of Paris Agreement

Role of clean energy in the context of Paris Agreement Peter Janoska, Energy Analyst, IEA COP 23, Bonn, 15 November 2017 IEA The IEA works around the world to support an accelerated clean energy transitions

Role of clean energy in the context of Paris Agreement Peter Janoska, Energy Analyst, IEA COP 23, Bonn, 15 November 2017 IEA The IEA works around the world to support an accelerated clean energy transitions

Enel Green Power and the Renewable Energies Scenario

Enel Green Power and the Renewable Energies Scenario Francesco Starace - CEO Enel Green Power IEA Working Party on Renewable Energy Technologies - The Role of Renewables in the Energy Transformation: The

Enel Green Power and the Renewable Energies Scenario Francesco Starace - CEO Enel Green Power IEA Working Party on Renewable Energy Technologies - The Role of Renewables in the Energy Transformation: The

The World Energy Outlook after the Financial Crisis

The World Energy Outlook after the Financial Crisis Presentation to the UNECE Committee on Sustainable Energy Geneva, 19 November 2009 Trevor Morgan Senior Economist International Energy Agency The context

The World Energy Outlook after the Financial Crisis Presentation to the UNECE Committee on Sustainable Energy Geneva, 19 November 2009 Trevor Morgan Senior Economist International Energy Agency The context

Medium Term Renewable Energy Market Report 2016

Medium Term Renewable Energy Market Report 2016 Clean Energy Investment and Trends IETA Pavilion COP22, Marrakech November 10, 2016 Liwayway Adkins Environment and Climate Change Unit International Energy

Medium Term Renewable Energy Market Report 2016 Clean Energy Investment and Trends IETA Pavilion COP22, Marrakech November 10, 2016 Liwayway Adkins Environment and Climate Change Unit International Energy

Are Sustainable Urban Energy Systems Essential for a New Deal on Energy Access for Africa? By Dave Turk, Head of IEA Energy Environment Division

Are Sustainable Urban Energy Systems Essential for a New Deal on Energy Access for Africa? By Dave Turk, Head of IEA Energy Environment Division OECD/IEA, 2016 The IEA works around the world to support

Are Sustainable Urban Energy Systems Essential for a New Deal on Energy Access for Africa? By Dave Turk, Head of IEA Energy Environment Division OECD/IEA, 2016 The IEA works around the world to support

Profound changes underway in energy markets Signs of decoupling of energy-related CO 2 emissions and global economic growth Oil prices have fallen pre

Keisuke Sadamori Director of Energy Markets and Security, IEA The 88th IEEJ Energy Seminar, 5th October 215 Profound changes underway in energy markets Signs of decoupling of energy-related CO 2 emissions

Keisuke Sadamori Director of Energy Markets and Security, IEA The 88th IEEJ Energy Seminar, 5th October 215 Profound changes underway in energy markets Signs of decoupling of energy-related CO 2 emissions

IE A EPRI October 8th, 2014 Challenges to the electricity sector under decarbonisation. Edouard Sauvage, Director of Strategy, GDF SUEZ CONFIDENTIEL

IE A EPRI October 8th, 2014 Challenges to the electricity sector under decarbonisation Edouard Sauvage, Director of Strategy, GDF SUEZ CONFIDENTIEL Is the decarbonisation of the electricity sector the

IE A EPRI October 8th, 2014 Challenges to the electricity sector under decarbonisation Edouard Sauvage, Director of Strategy, GDF SUEZ CONFIDENTIEL Is the decarbonisation of the electricity sector the

The G8 Climate Change Initiative: What it means for building performance

INTERNATIONAL ENERGY AGENCY The G8 Climate Change Initiative: What it means for building performance Paul Waide Senior Policy Analyst Energy Efficiency and Environment Division International Energy Agency

INTERNATIONAL ENERGY AGENCY The G8 Climate Change Initiative: What it means for building performance Paul Waide Senior Policy Analyst Energy Efficiency and Environment Division International Energy Agency

Overview of APERC Activities

Overview of APERC Activities APEC NEW AND RENEWABLE ENERGY TECHNOLOGIES 34 th EXPERT GROUP MEETING 26-28 April,2010 Kuala Lumpur, Malaysia Asia-Pacific Energy Research Centre (APERC) 1. Role of APERC Outline

Overview of APERC Activities APEC NEW AND RENEWABLE ENERGY TECHNOLOGIES 34 th EXPERT GROUP MEETING 26-28 April,2010 Kuala Lumpur, Malaysia Asia-Pacific Energy Research Centre (APERC) 1. Role of APERC Outline

World Energy Outlook 2009 Key results and messages of the 450 Scenario

World Energy Outlook 29 Key results and messages of the 45 Scenario Marco Baroni Office of the Chief Economist International Energy Workshop Stockholm, 22 June 21 Mtoe World primary energy demand by fuel

World Energy Outlook 29 Key results and messages of the 45 Scenario Marco Baroni Office of the Chief Economist International Energy Workshop Stockholm, 22 June 21 Mtoe World primary energy demand by fuel

APEC Energy Demand and Supply Outlook, 6 th Edition

APEC Energy Demand and Supply Outlook, 6 th Edition Cecilia Tam Special Advisor, APERC Asia Pacific Energy Research Centre Business as Usual (BAU) Scenario 2 Mtoe Energy intensity index Outlook for APEC

APEC Energy Demand and Supply Outlook, 6 th Edition Cecilia Tam Special Advisor, APERC Asia Pacific Energy Research Centre Business as Usual (BAU) Scenario 2 Mtoe Energy intensity index Outlook for APEC

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dave Turk, Director (Acting) of Sustainability, Technology and Outlooks 16 November 2017 COP23, IETA Pavilion IEA Introduction

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dave Turk, Director (Acting) of Sustainability, Technology and Outlooks 16 November 2017 COP23, IETA Pavilion IEA Introduction

Context Three numbers and three core global energy challenges: 6.5 million premature deaths each year can be attributed to air pollution 2.7 degrees i

Renewables 217 Heymi Bahar IEEJ, Tokyo 31 October 217 Context Three numbers and three core global energy challenges: 6.5 million premature deaths each year can be attributed to air pollution 2.7 degrees

Renewables 217 Heymi Bahar IEEJ, Tokyo 31 October 217 Context Three numbers and three core global energy challenges: 6.5 million premature deaths each year can be attributed to air pollution 2.7 degrees

Toshiyuki Shirai Senior Energy Analyst, IEA. October 27, Manila

Toshiyuki Shirai Senior Energy Analyst, IEA October 27, Manila Southeast Asia: the energy context n Southeast Asia is emerging as major global energy player Ø Strong economic & population growth, urbanisation

Toshiyuki Shirai Senior Energy Analyst, IEA October 27, Manila Southeast Asia: the energy context n Southeast Asia is emerging as major global energy player Ø Strong economic & population growth, urbanisation

Energy Technology Perspectives 2014 Harnessing Electricity s Potential

The Global Outlook An active transformation of the energy system is essential to meet long-term goals. (ETP 2014) charts a course by which policy and technology together become driving forces in transforming

The Global Outlook An active transformation of the energy system is essential to meet long-term goals. (ETP 2014) charts a course by which policy and technology together become driving forces in transforming

IEEJ: December 2013 All Right Reserved Implications of the Changing Energy Map Comments for IEA WEO 2013 Symposium Tokyo 28 November, 2013 The Institu

Implications of the Changing Energy Map Comments for IEA WEO 2013 Symposium Tokyo 28 November, 2013 The Institute of Energy Economics, Yukari Yamashita Board Member, Director Energy Data and Modelling

Implications of the Changing Energy Map Comments for IEA WEO 2013 Symposium Tokyo 28 November, 2013 The Institute of Energy Economics, Yukari Yamashita Board Member, Director Energy Data and Modelling

Tipping the energy world off its axis Four large-scale upheavals in global energy : - The United States is turning into the undisputed global leader f

The rapidly changing global energy landscape Dr. Fatih Birol Executive Director, International Energy Agency IEEJ, Tokyo, 27 February 2018 IEA Tipping the energy world off its axis Four large-scale upheavals

The rapidly changing global energy landscape Dr. Fatih Birol Executive Director, International Energy Agency IEEJ, Tokyo, 27 February 2018 IEA Tipping the energy world off its axis Four large-scale upheavals

Tipping the energy world off its axis Four large-scale upheavals in global energy : - The United States is turning into the undisputed global leader f

The rapidly changing global energy landscape Dr. Fatih Birol Executive Director, International Energy Agency IEEJ, Tokyo, 27 February 2018 IEA Tipping the energy world off its axis Four large-scale upheavals

The rapidly changing global energy landscape Dr. Fatih Birol Executive Director, International Energy Agency IEEJ, Tokyo, 27 February 2018 IEA Tipping the energy world off its axis Four large-scale upheavals

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dave Turk, Acting Director, Directorate of Sustainability, Technology and Outlooks, IEA IEA Innovation for Cool Earth Forum

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dave Turk, Acting Director, Directorate of Sustainability, Technology and Outlooks, IEA IEA Innovation for Cool Earth Forum

Introduction to medium term reports Based on the most recent data available 5 years outlook is important for policy making Natural gas and renewables

IEA Medium-Term Market Reports IEEJ Seminar Tokyo, 20 September 2012 Didier Houssin Director, Energy Markets and Security International Energy Agency OECD/IEA 2011 Introduction to medium term reports Based

IEA Medium-Term Market Reports IEEJ Seminar Tokyo, 20 September 2012 Didier Houssin Director, Energy Markets and Security International Energy Agency OECD/IEA 2011 Introduction to medium term reports Based

IEA Roadmap Workshop Sustainable Biomass Supply for Bioenergy and Biofuels September 2010

IEA Roadmap Workshop Sustainable Biomass Supply for Bioenergy and Biofuels 15-16 September 2010 Adam Brown Anselm Eisentraut Renewable Energy Division We need a global 50% CO 2 cut by 2050 Gt CO2 60 55

IEA Roadmap Workshop Sustainable Biomass Supply for Bioenergy and Biofuels 15-16 September 2010 Adam Brown Anselm Eisentraut Renewable Energy Division We need a global 50% CO 2 cut by 2050 Gt CO2 60 55

The IEA CCS Roadmap. Coal is an important part of global energy supply. 17-Mar-10. Brian Ricketts International Energy Agency

The IEA CCS Roadmap UK Advanced Power Generation Technology Forum Workshop on Carbon Abatement Technologies - development and implementation of future UK strategy London, 16 March 2010 Brian Ricketts International

The IEA CCS Roadmap UK Advanced Power Generation Technology Forum Workshop on Carbon Abatement Technologies - development and implementation of future UK strategy London, 16 March 2010 Brian Ricketts International

OECD/IEA Chapter 4 Natural gas

Chapter 4 Natural gas Are we entering a Golden Age of Gas? Natural gas can enhance security of supply: global resources exceed 25 years of current producaon; while in each region, resources exceed 75 years

Chapter 4 Natural gas Are we entering a Golden Age of Gas? Natural gas can enhance security of supply: global resources exceed 25 years of current producaon; while in each region, resources exceed 75 years

IEEJ:October 2016 IEEJ2016 The global energy outlook and what it means for Japan Paul Simons Deputy Executive Director, International Energy Agency Ja

The global energy outlook and what it means for Japan Paul Simons Deputy Executive Director, International Energy Agency Japan IDR launch Tokyo, 21 September 2016 Long-term energy demand set to grow fast

The global energy outlook and what it means for Japan Paul Simons Deputy Executive Director, International Energy Agency Japan IDR launch Tokyo, 21 September 2016 Long-term energy demand set to grow fast

World Energy Outlook 2010

World Energy Outlook 2010 Nobuo Tanaka Executive Director International Energy Agency Cancun, 7 December 2010, IEA day The context: A time of unprecedented uncertainty The worst of the global economic

World Energy Outlook 2010 Nobuo Tanaka Executive Director International Energy Agency Cancun, 7 December 2010, IEA day The context: A time of unprecedented uncertainty The worst of the global economic

Spencer Dale Group chief economist

Spencer Dale Group chief economist Energy Outlook scenarios Primary energy consumption by fuel CO 2 emissions Billion toe Gt of CO 2 25 4 Renew.* 5 4 Evolving transition (ET) More energy (ME) Less globalization

Spencer Dale Group chief economist Energy Outlook scenarios Primary energy consumption by fuel CO 2 emissions Billion toe Gt of CO 2 25 4 Renew.* 5 4 Evolving transition (ET) More energy (ME) Less globalization

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dr. Uwe Remme, IEA wholesem Annual Conference, 3 July 2017, London IEA IEA Energy Technology & Policy Activities Scenarios

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dr. Uwe Remme, IEA wholesem Annual Conference, 3 July 2017, London IEA IEA Energy Technology & Policy Activities Scenarios

World Energy Outlook Dr. Fatih Birol IEA Chief Economist Riyadh, 12 January 2010

World Energy Outlook 29 Dr. Fatih Birol IEA Chief Economist Riyadh, 12 January 21 Change in primary energy demand in the Reference Scenario, 27-23 Coal Oil Gas Nuclear OECD Non-OECD Hydro Biomass Other

World Energy Outlook 29 Dr. Fatih Birol IEA Chief Economist Riyadh, 12 January 21 Change in primary energy demand in the Reference Scenario, 27-23 Coal Oil Gas Nuclear OECD Non-OECD Hydro Biomass Other

REmap 2030 Analysis for Ukraine

REmap 2030 Analysis for Ukraine Kiev,12 March, 2015 REmap Ukraine background Ukraine is part of the first volume of IRENA s global renewable energy roadmap (REmap) Ukraine is among the largest 26 energy

REmap 2030 Analysis for Ukraine Kiev,12 March, 2015 REmap Ukraine background Ukraine is part of the first volume of IRENA s global renewable energy roadmap (REmap) Ukraine is among the largest 26 energy

Delivering on the clean energy agenda: prospects and the role for policy

Delivering on the clean energy agenda: prospects and the role for policy 6th Asian Ministerial Energy Roundtable 9 November 2015 Keisuke Sadamori Director, Energy Markets and Security Climate pledges shift

Delivering on the clean energy agenda: prospects and the role for policy 6th Asian Ministerial Energy Roundtable 9 November 2015 Keisuke Sadamori Director, Energy Markets and Security Climate pledges shift

Energy Efficiency: The Win Win Solution for Energy Security and Sustainable Development

Energy Efficiency: The Win Win Solution for Energy Security and Sustainable Development Lisa Ryan Energy efficiency and environment division, IEA Presented at the Special event in the context of the Joint

Energy Efficiency: The Win Win Solution for Energy Security and Sustainable Development Lisa Ryan Energy efficiency and environment division, IEA Presented at the Special event in the context of the Joint

World Energy Outlook Isabel Murray Russia Programme Manager Moscow, 3 February 2010

World Energy Outlook 2009 Isabel Murray Russia Programme Manager Moscow, 3 February 2010 Key Differences between the WEO and Primes Model WEO is designed as a tool for policy makers: > to understand current

World Energy Outlook 2009 Isabel Murray Russia Programme Manager Moscow, 3 February 2010 Key Differences between the WEO and Primes Model WEO is designed as a tool for policy makers: > to understand current

Renewable Energy Perspectives and Roadmaps 2010

Per lo sviluppo di una filiera industriale delle rinnovabili in Italia Renewable Energy Perspectives and Roadmaps 2010 Rome, 13 July 2010 Roberto VIGOTTI Chair REWP IEA Energy scenarios. What for? neither

Per lo sviluppo di una filiera industriale delle rinnovabili in Italia Renewable Energy Perspectives and Roadmaps 2010 Rome, 13 July 2010 Roberto VIGOTTI Chair REWP IEA Energy scenarios. What for? neither

GE OIL & GAS ANNUAL MEETING 2016 Florence, Italy, 1-2 February

Navigating energy transition Keisuke Sadamori Director for Energy Markets and Security IEA GE OIL & GAS ANNUAL MEETING 2016 Florence, Italy, 1-2 February 2016 General Electric Company - All rights reserved

Navigating energy transition Keisuke Sadamori Director for Energy Markets and Security IEA GE OIL & GAS ANNUAL MEETING 2016 Florence, Italy, 1-2 February 2016 General Electric Company - All rights reserved

Decarbonization pathways and the new role of DSOs

Decarbonization pathways and the new role of DSOs Kristian Ruby Secretary General Eurelectric 3 April 2019 We have modelled 3 deep decarbonization scenarios based on electrification of key economic sectors

Decarbonization pathways and the new role of DSOs Kristian Ruby Secretary General Eurelectric 3 April 2019 We have modelled 3 deep decarbonization scenarios based on electrification of key economic sectors

Wind Energy in the Mitigation of Carbon Emissions

Wind Energy in the Mitigation of Carbon Emissions WindPower 2009 Walter Short and Patrick Sullivan May 6, 2009 NREL is a national laboratory of the U.S. Department of Energy Office of Energy Efficiency

Wind Energy in the Mitigation of Carbon Emissions WindPower 2009 Walter Short and Patrick Sullivan May 6, 2009 NREL is a national laboratory of the U.S. Department of Energy Office of Energy Efficiency

The start of a new energy era?

The start of a new energy era? 2015 has seen lower prices for all fossil fuels Oil & gas could face second year of falling upstream investment in 2016 Coal prices remain at rock-bottom as demand slows

The start of a new energy era? 2015 has seen lower prices for all fossil fuels Oil & gas could face second year of falling upstream investment in 2016 Coal prices remain at rock-bottom as demand slows

Energy and CO 2 Emissions Outlook

INTERNATIONAL ENERGY AGENCY Energy and CO 2 Emissions Outlook World Energy Outlook - 2006 Laura Cozzi Economic Analysis Division The Reference Scenario: World Primary Energy Demand 18 000 16 000 14 000

INTERNATIONAL ENERGY AGENCY Energy and CO 2 Emissions Outlook World Energy Outlook - 2006 Laura Cozzi Economic Analysis Division The Reference Scenario: World Primary Energy Demand 18 000 16 000 14 000

CCT2009. Dresden, 20 May Clean Coal Technologies An IEA View on Potentials and Perspectives

CCT2009 Dresden, 20 May 2009 Clean Coal Technologies An IEA View on Potentials and Perspectives Antonio Pflüger Head, Energy Technology Collaboration Division International Energy Agency INTERNATIONAL

CCT2009 Dresden, 20 May 2009 Clean Coal Technologies An IEA View on Potentials and Perspectives Antonio Pflüger Head, Energy Technology Collaboration Division International Energy Agency INTERNATIONAL

Christine Lins Executive Secretary

Christine Lins Executive Secretary christine.lins@ren21.net Tokyo, 25 October 2017 REN21 Renewables 2017 Global Status Report The report features: Global Overview Market & Industry Trends Distributed Renewable

Christine Lins Executive Secretary christine.lins@ren21.net Tokyo, 25 October 2017 REN21 Renewables 2017 Global Status Report The report features: Global Overview Market & Industry Trends Distributed Renewable

Global Bioenergy Market Developments

Global Bioenergy Market Developments Dr. Heinz Kopetz World Bioenergy Association Tokyo, 9 March 2012 Japan Renewable Energy Foundation - Revision 2012 The importance of biomass Biomass is organic matter

Global Bioenergy Market Developments Dr. Heinz Kopetz World Bioenergy Association Tokyo, 9 March 2012 Japan Renewable Energy Foundation - Revision 2012 The importance of biomass Biomass is organic matter

John Gale General Manager IEA Greenhouse Gas R&D Programme

The role of CCS as a climate change mitigation option, Energy technology perspectives p John Gale General Manager IEA Greenhouse Gas R&D Programme Public Power Corporation Seminar on CCS Athens, Greece

The role of CCS as a climate change mitigation option, Energy technology perspectives p John Gale General Manager IEA Greenhouse Gas R&D Programme Public Power Corporation Seminar on CCS Athens, Greece

OECD/IEA Dr Fatih Birol IEA Executive Director Oslo, Norway 20 November 2018

Dr Fatih Birol IEA Executive Director Oslo, Norway 20 November 2018 Global energy demand and the growing IEA Family Share of IEA member and association Global energy countries demand in global energy demand

Dr Fatih Birol IEA Executive Director Oslo, Norway 20 November 2018 Global energy demand and the growing IEA Family Share of IEA member and association Global energy countries demand in global energy demand

Roadmap for Solar PV. Michael Waldron Renewable Energy Division International Energy Agency

Roadmap for Solar PV Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 2014 IEA work on renewables IEA renewables website: http://www.iea.org/topics/renewables/ Renewable Policies

Roadmap for Solar PV Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 2014 IEA work on renewables IEA renewables website: http://www.iea.org/topics/renewables/ Renewable Policies

World Energy Outlook Dr. Fatih Birol IEA Chief Economist 24 November 2010

World Energy Outlook 2010 Dr. Fatih Birol IEA Chief Economist 24 November 2010 The context: a time of unprecedented uncertainty The worst of the global economic crisis appears to be over but is the recovery

World Energy Outlook 2010 Dr. Fatih Birol IEA Chief Economist 24 November 2010 The context: a time of unprecedented uncertainty The worst of the global economic crisis appears to be over but is the recovery

Power Markets in an Era of Low-Marginal Costs

14 September 2017 Power Markets in an Era of Low-Marginal Costs Resources for the Future and NREL Workshop David Littell Principal The Regulatory Assistance Project (RAP) 550 Forest Avenue, Suite 203 Portland,

14 September 2017 Power Markets in an Era of Low-Marginal Costs Resources for the Future and NREL Workshop David Littell Principal The Regulatory Assistance Project (RAP) 550 Forest Avenue, Suite 203 Portland,

Competitive energy landscape in Europe

President of Energy Sector, South West Europe, Siemens Competitive energy landscape in Europe Brussels, siemens.com/answers Agenda Europe s competitiveness depends on an affordable and reliable energy

President of Energy Sector, South West Europe, Siemens Competitive energy landscape in Europe Brussels, siemens.com/answers Agenda Europe s competitiveness depends on an affordable and reliable energy

Contribution of Renewables to Energy Security Cédric PHILIBERT Renewable Energy Division

Contribution of Renewables to Energy Security Cédric PHILIBERT Renewable Energy Division EUFORES Parliamentary Dinner Debate, Brussels, 9 September, 2014 What Energy Security is about IEA defines energy

Contribution of Renewables to Energy Security Cédric PHILIBERT Renewable Energy Division EUFORES Parliamentary Dinner Debate, Brussels, 9 September, 2014 What Energy Security is about IEA defines energy

Energy Technology Perspectives 2017 The Role of CCS in Deep Decarbonisation Scenarios

Energy Technology Perspectives 2017 The Role of CCS in Deep Decarbonisation Scenarios Dr. Uwe Remme, IEA International Energy Workshop, 19 June 2018, Gothenburg IEA How far can technology take us? 40 Reference

Energy Technology Perspectives 2017 The Role of CCS in Deep Decarbonisation Scenarios Dr. Uwe Remme, IEA International Energy Workshop, 19 June 2018, Gothenburg IEA How far can technology take us? 40 Reference

Current New and Renewable Energy Utilization in Japan

APEC EGNRET 34, Kuala Lumpur Current New and Renewable Energy Utilization in Japan April 26, 2010 Takao Ikeda The Institute of Energy Economics, Japan (IEEJ) Ken Johnson New Energy and Industrial Technology

APEC EGNRET 34, Kuala Lumpur Current New and Renewable Energy Utilization in Japan April 26, 2010 Takao Ikeda The Institute of Energy Economics, Japan (IEEJ) Ken Johnson New Energy and Industrial Technology

The challenges of a changing energy landscape

The challenges of a changing energy landscape October 26 th 2016 Maria Pedroso Ferreira EDP Energy Planning maria.pedrosoferreira@edp.pt Agenda 1 A changing energy landscape 2 Challenges and opportunities

The challenges of a changing energy landscape October 26 th 2016 Maria Pedroso Ferreira EDP Energy Planning maria.pedrosoferreira@edp.pt Agenda 1 A changing energy landscape 2 Challenges and opportunities

The Future of Global Energy Markets: Implications for Security, Sustainability and Economic Growth

The Future of Global Energy Markets: Implications for Security, Sustainability and Economic Growth Dr. Fatih Birol, Executive Director, International Energy Agency Delft University of Technology, 20 March

The Future of Global Energy Markets: Implications for Security, Sustainability and Economic Growth Dr. Fatih Birol, Executive Director, International Energy Agency Delft University of Technology, 20 March

Third IEA IEF OPEC Symposium on Gas and Coal Market Outlooks. Tim Gould, IEA

Third IEA IEF OPEC Symposium on Gas and Coal Market Outlooks Tim Gould, IEA A new fuel in pole position Change in global primary energy demand Mtoe 2 000 1990-2015 2015-2040 Rest of world 1 500 1 000 Renewables

Third IEA IEF OPEC Symposium on Gas and Coal Market Outlooks Tim Gould, IEA A new fuel in pole position Change in global primary energy demand Mtoe 2 000 1990-2015 2015-2040 Rest of world 1 500 1 000 Renewables

OECD/IEA 2016 OECD/IEA Canberra November 2016

Canberra November 2016 The global energy context today Key points of orientation: Middle East share in global oil production in 2016 at highest level for 40 years Transformation in gas markets deepening

Canberra November 2016 The global energy context today Key points of orientation: Middle East share in global oil production in 2016 at highest level for 40 years Transformation in gas markets deepening

POWER CHOICES Pathways to carbon-neutral electricity in Europe by 2050 Nicola Rega Advisor Environment and Sustainable Development Policy

POWER CHOICES Pathways to carbon-neutral electricity in Europe by 2050 Nicola Rega Advisor Environment and Sustainable Development Policy Bruges, 18 March 2010 Representing the electricity industry at

POWER CHOICES Pathways to carbon-neutral electricity in Europe by 2050 Nicola Rega Advisor Environment and Sustainable Development Policy Bruges, 18 March 2010 Representing the electricity industry at

World Energy Outlook 2004

INTERNATIONAL ENERGY AGENCY World Energy Outlook 2004 Claude Mandil Executive Director International Energy Agency International Energy Symposium, IEEJ Tokyo 16 November 2004 Global Energy Trends: Reference

INTERNATIONAL ENERGY AGENCY World Energy Outlook 2004 Claude Mandil Executive Director International Energy Agency International Energy Symposium, IEEJ Tokyo 16 November 2004 Global Energy Trends: Reference

Integrating climate, air pollution & universal access: The Sustainable Development Scenario

Integrating climate, air pollution & universal access: The Sustainable Development Scenario Dr. Timur Gül, IEA COP23, Bonn, 16 November 2017 Context The SDGs recognise climate change, air pollution and

Integrating climate, air pollution & universal access: The Sustainable Development Scenario Dr. Timur Gül, IEA COP23, Bonn, 16 November 2017 Context The SDGs recognise climate change, air pollution and

IEA Technology Roadmap: Delivering sustainable bioenergy

IEA Technology Roadmap: Delivering sustainable bioenergy Adam Brown ETIP Bioenergy, 11 April 218 OECD/IEA 217 Roadmap launched IEA Bioenergy Roadmap launched on 3 November 217 at joint IEA and Mission

IEA Technology Roadmap: Delivering sustainable bioenergy Adam Brown ETIP Bioenergy, 11 April 218 OECD/IEA 217 Roadmap launched IEA Bioenergy Roadmap launched on 3 November 217 at joint IEA and Mission

WORLD ENERGY OUTLOOK Dr. Fatih Birol Chief Economist Head, Economic Analysis Division

WORLD ENERGY OUTLOOK 2002 Dr. Fatih Birol Chief Economist Head, Economic Analysis Division World Energy Outlook Series World Energy Outlook 1998 World Energy Outlook - 1999 Insights: Looking at Energy

WORLD ENERGY OUTLOOK 2002 Dr. Fatih Birol Chief Economist Head, Economic Analysis Division World Energy Outlook Series World Energy Outlook 1998 World Energy Outlook - 1999 Insights: Looking at Energy

World Energy Outlook Bo Diczfalusy, Näringsdepartementet

World Energy Outlook 2013 Bo Diczfalusy, Näringsdepartementet Energy demand & GDP Trillion dollars (2012) 50 40 30 20 10 000 Mtoe 8 000 6 000 4 000 GDP: OECD Non-OECD TPED (right axis): OECD Non-OECD 10

World Energy Outlook 2013 Bo Diczfalusy, Näringsdepartementet Energy demand & GDP Trillion dollars (2012) 50 40 30 20 10 000 Mtoe 8 000 6 000 4 000 GDP: OECD Non-OECD TPED (right axis): OECD Non-OECD 10

Energy Outlook for ASEAN+3

The 15 th ASEAN+3 Energy Security Forum March, 218 Energy Outlook for ASEAN+3 Ryo Eto The Institute of Energy Economics, JAPAN (IEEJ) Contents Introduction Modeling framework, Major assumptions TPES, FEC

The 15 th ASEAN+3 Energy Security Forum March, 218 Energy Outlook for ASEAN+3 Ryo Eto The Institute of Energy Economics, JAPAN (IEEJ) Contents Introduction Modeling framework, Major assumptions TPES, FEC

Facing the global energy trilemma: growth, climate and universal access

Facing the global energy trilemma: growth, climate and universal access Ivan Faiella Bank of Italy Structural Analysis Department* Climate Finance e accesso universale all'energia Nona Conferenza Banca

Facing the global energy trilemma: growth, climate and universal access Ivan Faiella Bank of Italy Structural Analysis Department* Climate Finance e accesso universale all'energia Nona Conferenza Banca

THE BALTICS THE FIRST REGION IN THE EU TO BECOME 100% RES

THE BALTICS THE FIRST REGION IN THE EU TO BECOME 100% RES Christian Breyer, Michael Child and Dmitrii Bogdanov Lappeenranta University of Technology (LUT), Finland 17 th Inter-Parliamentary Meeting on

THE BALTICS THE FIRST REGION IN THE EU TO BECOME 100% RES Christian Breyer, Michael Child and Dmitrii Bogdanov Lappeenranta University of Technology (LUT), Finland 17 th Inter-Parliamentary Meeting on

The global energy outlook to 2025 and the megatrends impacting energy markets beyond that Sydney, 16 September Keisuke Sadamori Director

The global energy outlook to 2025 and the megatrends impacting energy markets beyond that Sydney, 16 September 2015 Keisuke Sadamori Director OECD/IEA - 2013 Slide 2 Demand/Supply Balance until 4Q16* mb/d

The global energy outlook to 2025 and the megatrends impacting energy markets beyond that Sydney, 16 September 2015 Keisuke Sadamori Director OECD/IEA - 2013 Slide 2 Demand/Supply Balance until 4Q16* mb/d

OECD/IEA Brent Wanner, Senior Energy Analyst Stockholm, 24 November 2015

Brent Wanner, Senior Energy Analyst Stockholm, 24 November 2015 The start of a new energy era? 2015 has seen lower prices for all fossil fuels Oil & gas could face second year of falling upstream investment

Brent Wanner, Senior Energy Analyst Stockholm, 24 November 2015 The start of a new energy era? 2015 has seen lower prices for all fossil fuels Oil & gas could face second year of falling upstream investment

Interim results IEA technology roadmap: geothermal heat and power. Dr Milou Beerepoot Senior analyst, International Energy Agency

Interim results IEA technology roadmap: geothermal heat and power Dr Milou Beerepoot Senior analyst, International Energy Agency Share of non-hydro renewables in electricity production of IEA countries

Interim results IEA technology roadmap: geothermal heat and power Dr Milou Beerepoot Senior analyst, International Energy Agency Share of non-hydro renewables in electricity production of IEA countries

Renewables after COP-21 A global perspective. Dr. Fatih Birol Executive Director International Energy Agency

Renewables after COP-21 A global perspective Dr. Fatih Birol Executive Director International Energy Agency 17 th Symposium, Syndicat des Énergies Renouvelables, Unesco, Paris, 4 February 2016 The start

Renewables after COP-21 A global perspective Dr. Fatih Birol Executive Director International Energy Agency 17 th Symposium, Syndicat des Énergies Renouvelables, Unesco, Paris, 4 February 2016 The start

TABLE OF CONTENTS 6 RENEWABLES 2017

TABLE OF CONTENTS Executive summary... 13 1. Recent renewable energy deployment trends... 17 Highlights... 17 Electricity... 18 Technology deployment summary... 18 Regional deployment summary... 20 Transport...

TABLE OF CONTENTS Executive summary... 13 1. Recent renewable energy deployment trends... 17 Highlights... 17 Electricity... 18 Technology deployment summary... 18 Regional deployment summary... 20 Transport...

World primary energy demand in the t Reference Scenario: this is unsustainable!

OECD/IEA OECD/IEA -29-29 World primary energy demand in the t Reference Scenario: this is unsustainable! Mtoe 18 Other renewables 16 Hydro 14 12 Nuclear 1 Biomass 8 Gas 6 Coal 4 Oil 2 198 199 2 21 22 23

OECD/IEA OECD/IEA -29-29 World primary energy demand in the t Reference Scenario: this is unsustainable! Mtoe 18 Other renewables 16 Hydro 14 12 Nuclear 1 Biomass 8 Gas 6 Coal 4 Oil 2 198 199 2 21 22 23

Renewables: challenges and opportunities for the power grid Cédric PHILIBERT Renewable Energy Division International Energy Agency

Renewables: challenges and opportunities for the power grid Cédric PHILIBERT Renewable Energy Division International Energy Agency Atoms for the Future, Paris, 22 October 2013 Positive mid-term outlook

Renewables: challenges and opportunities for the power grid Cédric PHILIBERT Renewable Energy Division International Energy Agency Atoms for the Future, Paris, 22 October 2013 Positive mid-term outlook

Strong focus on market and policy analysis

OECD/IEA - 2015 Founded in 1974 OECD agency 29 member countries 1 new applicant - Mexico 3 associate countries: China, Indonesia, Thailand 240 staff in Paris secretariat The European Commission also participates

OECD/IEA - 2015 Founded in 1974 OECD agency 29 member countries 1 new applicant - Mexico 3 associate countries: China, Indonesia, Thailand 240 staff in Paris secretariat The European Commission also participates

World Energy Outlook 2013

World Energy Outlook 2013 Paweł Olejarnik IEA Energy Analyst Warszawa, 15 Listopada 2013 The world energy scene today Some long-held tenets of the energy sector are being rewritten Countries are switching

World Energy Outlook 2013 Paweł Olejarnik IEA Energy Analyst Warszawa, 15 Listopada 2013 The world energy scene today Some long-held tenets of the energy sector are being rewritten Countries are switching

Plenary session 4: Uptake of Clean Technologies: Disruption and Coexistence of New and Existing Technologies the Way Ahead.

India Plenary session 4: Uptake of Clean Technologies: Disruption and Coexistence of New and Existing Technologies the Way Ahead Background Paper New Delhi Disclaimer The observations presented herein

India Plenary session 4: Uptake of Clean Technologies: Disruption and Coexistence of New and Existing Technologies the Way Ahead Background Paper New Delhi Disclaimer The observations presented herein

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan Aligning Policies for the Transition to a Low-carbon Economy: OECD Recommendations and Implications for Asia-Pacific

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan Aligning Policies for the Transition to a Low-carbon Economy: OECD Recommendations and Implications for Asia-Pacific

GLOBAL RENEWABLE ENERGY MARKET OUTLOOK 2013

GLOBAL RENEWABLE ENERGY MARKET OUTLOOK 213 FACT PACK GUY TURNER HEAD OF ECONOMICS AND COMMODITIES APRIL 22, 213 PRESENTATION TITLE, DAY MONTH YEAR 1 INTRODUCTION This year s Global Renewable Energy Market

GLOBAL RENEWABLE ENERGY MARKET OUTLOOK 213 FACT PACK GUY TURNER HEAD OF ECONOMICS AND COMMODITIES APRIL 22, 213 PRESENTATION TITLE, DAY MONTH YEAR 1 INTRODUCTION This year s Global Renewable Energy Market

Economies of Scale vs the Learning Curve Joan MacNaughton, Senior Vice President, Power & Environmental Policies

Economies of Scale vs the Learning Curve Joan MacNaughton, Senior Vice President, Power & Environmental Policies BIEE 8th Academic Conference, 23 September 2010 Agenda The challenge Meeting the challenge

Economies of Scale vs the Learning Curve Joan MacNaughton, Senior Vice President, Power & Environmental Policies BIEE 8th Academic Conference, 23 September 2010 Agenda The challenge Meeting the challenge

Energy Technology Perspectives 2006

Energy Technology Perspectives 2006 Results, Technologies and R&D Needs Dolf Gielen RD&D Workshop, 15-16 February 2007 OECD/IEA 2007 Structure of this Presentation Technology development ETP2006 scenarios

Energy Technology Perspectives 2006 Results, Technologies and R&D Needs Dolf Gielen RD&D Workshop, 15-16 February 2007 OECD/IEA 2007 Structure of this Presentation Technology development ETP2006 scenarios

Perspective on Accelerating RE to reach ASEAN s 23% aspirational target. Asia Clean Energy Forum 2017, ADB, Manila Deep-dive session - 6 June 2017

Perspective on Accelerating RE to reach ASEAN s 23% aspirational target Asia Clean Forum 2017, ADB, Manila Deep-dive session - 6 June 2017 DICLAIMER The views, opinions, and information expressed in this

Perspective on Accelerating RE to reach ASEAN s 23% aspirational target Asia Clean Forum 2017, ADB, Manila Deep-dive session - 6 June 2017 DICLAIMER The views, opinions, and information expressed in this

12 th International Energy Forum

12 th International Energy Forum 29-31 March 2010, Cancun Global Energy Markets: Reducing Volatility and Uncertainty Nobuo Tanaka Executive Director, International Energy Agency Current spotlight on financial

12 th International Energy Forum 29-31 March 2010, Cancun Global Energy Markets: Reducing Volatility and Uncertainty Nobuo Tanaka Executive Director, International Energy Agency Current spotlight on financial

Harmony The role of nuclear energy meeting electricity needs in the 2 degree scenario. Agneta Rising Director General

Harmony The role of nuclear energy meeting electricity needs in the 2 degree scenario Agneta Rising Director General Harmony January 2017 THE CURRENT STATUS OF NUCLEAR ENERGY 2 Global consumption of electricity

Harmony The role of nuclear energy meeting electricity needs in the 2 degree scenario Agneta Rising Director General Harmony January 2017 THE CURRENT STATUS OF NUCLEAR ENERGY 2 Global consumption of electricity

OECD/IEA World Energy Outlook 2011 focus on oil, gas and coal

World Energy Outlook 2011 focus on oil, gas and coal The context: fresh challenges add to already worrying trends Economic concerns have diverted attention from energy policy and limited the means of intervention

World Energy Outlook 2011 focus on oil, gas and coal The context: fresh challenges add to already worrying trends Economic concerns have diverted attention from energy policy and limited the means of intervention

Executive Summary. Background. Market developments. Key finding

Executive Summary Executive Summary Background This publication reviews the success of policy implementation and development based on a analysis of market trends in the three renewable energy (RE) sectors

Executive Summary Executive Summary Background This publication reviews the success of policy implementation and development based on a analysis of market trends in the three renewable energy (RE) sectors

OECD/IEA Dr Fatih Birol IEA Executive Director Berlin, 16 November 2018

Dr Fatih Birol IEA Executive Director Berlin, 16 November 2018 Global energy demand and the growing IEA Family Share of IEA member and association Global energy countries demand in global energy demand

Dr Fatih Birol IEA Executive Director Berlin, 16 November 2018 Global energy demand and the growing IEA Family Share of IEA member and association Global energy countries demand in global energy demand

Renewable Heat Market Developments

Renewable Heat Market Developments Anselm Eisentraut Bioenergy Analyst IEA Paris 9 April 214 OECD/IEA 214 What is heat? Heat within the energy system Buildings sector - Cooking - Water heating - Space

Renewable Heat Market Developments Anselm Eisentraut Bioenergy Analyst IEA Paris 9 April 214 OECD/IEA 214 What is heat? Heat within the energy system Buildings sector - Cooking - Water heating - Space