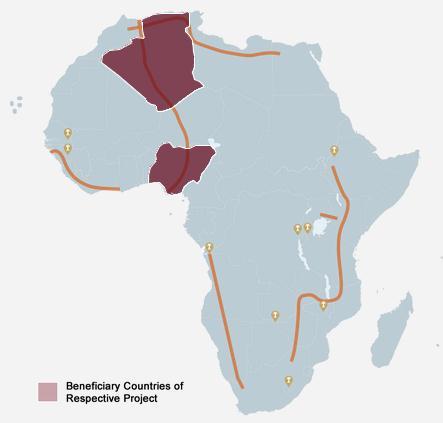

Nigeria, Niger, Algeria West Africa 4,400 km pipeline from Warri (Nigeria), through Niger to Hassi R Mel in Algeria

|

|

|

- Lesley Wood

- 6 years ago

- Views:

Transcription

1 Project Number: E /E /E Project Title: Nigeria Algeria Pipeline Status: S2 Feasibility/needs assessment Countries Region Project Location (current line routing) Sector Sub - sector Project description Objectives Economic Sustainability and expected benefits Nigeria, Niger, Algeria West Africa 4,400 km pipeline from Warri (Nigeria), through Niger to Hassi R Mel in Algeria Energy Transmission Natural gas pipeline for export to Europe. The Nigeria Algeria Pipeline is also referred to as the Trans Sahara gas pipeline (TSGP). Diversification of export route for marketing Nigerian natural gas Integrating economies and strengthening regional cooperation Boosting domestic gas supply in the countries Assisting in the fight against desertification through sustainable and reliable gas supply Nigerian gas reserves are estimated at 5 trillion cubic meters equal to roughly 10 years of consumption of the EU. In light of growing demand factors from Europe due to the depletion of European gas fields, and the need for an alternative to Russian gas, the demand from Europe is likely to remain high. Hence, this project would enable these African economies access a new market for their gas reserves, thereby increasing their incomes. REC Project Sponsors Implementing Authorities The TSGP would contribute to eliminating natural gas flaring in Nigeria. The TSGP is also has the critical advantage of supplying gas to Northern Nigeria, Niger, Southern Algeria, as well as Burkina Faso, and Southern Mali which are currently affected by high energy prices and desertification. AMU, ECOWAS, CEN - SAD Governments of Nigeria, Niger, Algeria Nigeria s Infrastructure Concession and Regulatory Commission, Nigerian National Petroleum Corporation (NNPC), Sonatrach (Algeria), the Niger National Oil Company, as well as the Union du Maghreb Arabe and the Economic Community of West African States Project Status Feasibility studies concluded and accepted by sponsors in September 2006 Inter-governmental agreement (IGA) between sponsor governments executed and ratified NNPC progressing with the Trans-Nigerian Segment of the Pipeline to kick-start and fast track the initiative Total estimated Project Value Way Forward Political Support USD 20 billion Market revalidation study; the project feasibility study is currently being revalidated Conclude the Trans-Nigerian optimization study and identify critical areas of synergy with the Trans Sahara Gas Pipeline from a construction point of view Update the IGA in line with an alternative Sonatrach participating arrangement and secure internal NASS ratification Commence with the relevant Directorates of NNPC, the review of supply options based on the revalidated study of the market and economics of gas supply Planned commencement year: 2015; Construction duration: 4 years The pipeline was selected as a Presidential Infrastructure Champion Initiative project. The Nigerian government has made a commitment of USD 400 million in the 2013 budget to finance the project up to the next stage. 1

2 2

3 Background 14 January 2002 Memorandum of Understanding to jointly develop the TSGP project was signed during the inaugural session of a Bi-National Commission between Nigeria and Algeria March, 2003 Nigerian National Petroleum Corporation (NNPC) and the Algerian Sonatrach executed a preliminary study agreement. September 2006 Feasibility studies concluded, and were accepted by sponsors February 2008 The Republic of Niger was admitted as project cosponsor at Abuja. 3 July 2009 An Intergovernme ntal Agreement (IGA) between sponsor governments was signed at Abuja. The ratification of the IGA by sponsor governments has been carried out by Niger and Algeria. The review of the unincorporated joint venture agreement (UJVA) between the three countries is on hold pending the resolution of Sonatrach s participation in Nigeria s upstream activities. In 2013, Nigeria set aside a sum of US$400 million for construction of the Calabar-Ajaokota-Kano pipeline; first direct activity to bring gas into the TSGP project. Economic Sustainability and Strategic Importance Natural gas is poised to occupy a more important place in the worldwide energy balance. Coupled with other renewable energy sources, natural gas is an energy source of choice for the development of Africa and offers a vehicle for its integration with the world economy. The main objectives of this project are as follows: Diversification of export route for marketing Nigerian natural gas Integration of the economies of the sub-region in line with objectives of NEPAD Strengthening regional cooperation Creation of wealth and poverty alleviation by opening up economic growth opportunities in the subregion 3

4 Boosting the GDP and improving the living standards of the people within the sub-region Boosting domestic gas supply in the country Assisting in the fight against desertification through sustainable and reliable gas supply Being the first of this kind, this project is an example of South-South integration and also has the potential to reinforce the role of energy in bridging the gap between Europe and Africa. With this pipeline, Africa can contribute to the global market with a sustained and diversified supply of natural gas that countries with excess demand are looking for, particularly the European Union (EU), which is a proximate market. EU access to Nigerian gas reserves is particularly crucial since European gas consumption and gas imports will increase significantly in the future. An increase in demand for natural gas and declining domestic production will result in a significant growth of import dependency. Consequently, natural gas imports may reach 85% of EU gas consumption by 2030 compared to 50% in This raises significant concerns about the EU's long-term security of supply. This is particularly the case given the growing dependency upon gas imports originating from a limited number of supplier nations, combined with the need for long distance transport infrastructures. Various elements, underpin the European need for Nigerian gas including: DEPLETION OF EUROPEAN GAS FIELDS: As domestic production declines, by 2025, 80% of the gas the EU consumes will be imported, compared with 58% in This means the continent will have to import nearly Tcf (200 billion cubic meters) more gas a year than it does now. DEMAND FOR OIL IN EUROPE IS LIKELY TO REMAIN HIGH: Natural gas demand in the EU is expected to rise by 43% by 2030 and the amount of additional supplies needed will likely increase from 10% in 2015, up to 22% in 2020, and to roughly 39% in The factors contributing to the high European demand for natural gas include environmental concerns over greenhouse gas emissions, choice to use natural gas being financially attractive for the electric power sector, slowdown in European nuclear energy development, and the credibility of reaching an offtake agreement. UNCERTAINTY OVER THE FEASIBILITY OF SHALE-GAS PRODUCTION IN EUROPE: As shale gas is a booming energy source in the United States, companies are now looking for shale gas in Europe. However, among the impediments to a similar boom in Europe are the depth of the deposits, regulatory issues, lack of supply chain, lack of appropriate rigs and equipment, conflicts with surface owners over developments in heavily populated Europe, and concerns over the environmental impact of industrial development. Hence, at this point, Europe s shale-gas appears to offer a meaningful but small target. PREFERENCE FOR A GAS PIPELINE OVER LIQUEFIED NATURAL GAS (LNG) TECHNOLOGY: Despite recent improvements, LNG is considered cost competitive with pipelines only over distances greater than 4,800 kilometres. According to this criterion, the 4,400 kilometres of the TSGP makes the pipeline more competitive than LNG. Further, another key criticism is that, 15 18% of gas is wasted during the process of liquefaction. Also, though both the TSGP and the LNG option would contribute to eliminating natural gas flaring in Nigeria. The TSGP is also has the critical advantage of supplying gas to Northern Nigeria, Niger, Southern Algeria, as well as Burkina Faso, and Southern Mali which are currently affected by high energy prices and desertification. 4

5 PRESENCE OF SUFFICIENT NIGERIAN RESERVES: Nigeria has the 7th largest gas reserves in the world. The gas quality is high, being particularly rich in liquids and low in sulphur. To date, although Nigeria has not explored for gas, the scope for huge growth exists. Further, there are large local economic benefits of this project, as listed below. The TSGP between Algeria and Nigeria will recover flared gas in Nigeria and bring it through a pipeline toward the European market. This gas is burnt currently in flares and hence, represents a loss of energy equivalent to barrels/day for Nigeria and thus has serious consequences on the environment. The TSGP will provide energy to the areas which is crosses, thereby contributing particularly to the revival of those areas, where there exists water and fertile land. Also, it will enable several countries in the region to access electricity. The TSGP will facilitate exploration by international companies and this will not only create economic activity and employment in the short run, but may also lead to new sources of energy being discovered in the region. Enhanced economic activity will have a stabilising effect on the region and will prevent the presently wandering populations from moving. The distribution of natural gas for energy would prevent usage of wood for this purpose, and therefore reduce deforestation. Hence, it can be said that the TSGP project has the potential to yield to economic and social benefits for the countries involved, reducing the basic cost of the energy need of the sub-region in addition to boosting the establishment of industries using cheaper energy, thus creating conducive conditions for sustainable growth and development. 5

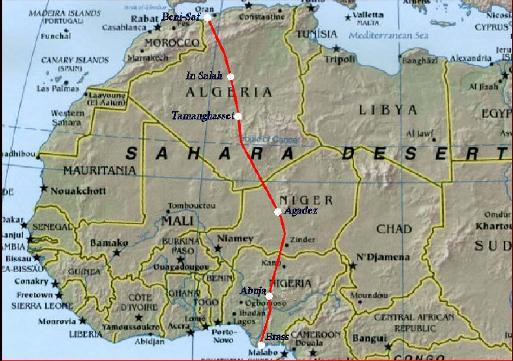

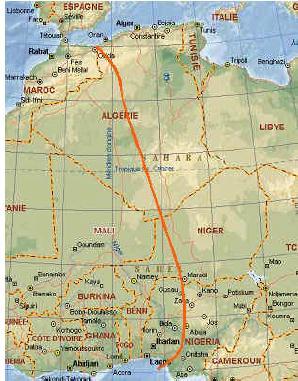

6 Technical Specifications The Trans-Saharan Gas Pipeline (TSGP) is a proposed natural gas pipeline from Nigeria to Algeria designed to supply Europe by connecting to the existing Trans-Mediterranean, Maghreb-Europe, Medgaz and Galsi pipelines across the Mediterranean coast. The length of the pipeline is estimated at roughly 4,400 kilometers. The pipeline would initiate in the swampy region of the Niger Delta basin, then across the cultivated lands and tropical forests of North Nigeria. In Niger, the pipeline would cross the Sahel region, a semi-arid tropical savanna preceding the Sahara desert. Almost half of the proposed route traverses arid expanses before crossing over the Atlas Mountains, finally reaching Hassi R Mel, a hub for natural gas and oil pipelines running to the Algerian coast. The route of the pipeline will be as follows: Nigeria Calabar-Kano-Nigerian border with Niger Republic = 1037km Niger Nigerian border with Niger, which extends/continues to the Nigerien border with Algeria = 841km Algeria Gas Infrastructure pipeline route within Algeria = 2303km Subsea The border between Algeria & Spain = 220km En route to Europe, it will connect to the existing Trans-Mediterranean, Maghreb-Europe, Medgaz (which started operations in early 2011) and Galsi (expected to come on stream in 2014) gas pipelines. Once functioning, the TSGP is expected to reach a capacity of 1,059 billion cubic feet or 30 billion cubic meters of natural gas per year. 6

7 Project Structure SONATRACH (ALGERIA) NIGER NATIONAL OIL COMPANY (NIGER) PROJECT SPONSORS: GOVT.S OF NIGERIA, ALGERIA, NIGER NIGERIIA- ALGERIA GAS PIPELINE Nigeria's Infrastructure Concession and Regulatory Commission NIGERIAN NATIONAL PETROLEUM CORPORATIO N (NIGERIA) FINANCINCIN G: DFIS AND PRIVATE SECTOR DEMAND: EU The proposed Nigeria Algeria pipeline project will involve the cooperation of three countries as coowners of the site. The demand for energy will come from the EU, the 3 countries utilities: NNPC for Nigeria, Sonatrach for Algeria and the Niger National Oil Company for Niger. Nigeria s Infrastructure Concession and Regulatory Commission is the focal point responsible for developing financing options for the project through a public private partnership (PPP). 7

8 Project Status Current Position Phase 5: Operation Phase 1: Conceptual Project developmen t philosophy Sponsors buy-in Appoint Consultant Phase 2: Feasibility Determine Gas Market /demand scenario Identify Gas supply sources Establish Pipeline Infrastructure requirement Determine EIA/SIA Issues Establish Project cost Estimates Policy Regulatory and Institutional Framework Analysis, Economic and Financial Analysis and Regional Benefit Phase 3: Definitional Develop Sponsors JV Agreement Select Consultant / Financial Adviser Incorporate SPV/TSGP Company Identify and obtain long-term commitments for the development and supply of gas and for gas buyers in Europe Establish TSGP companies, carry out EIA/SIA, route survey and implement them FEED, EPC contract packages, etc Execute Commercial/Term Sheets/ Agreement Prepare a Final Development Plan Conduct upstream resources due diligence Complete tendering for EPC Conclude land acquisition Take FID Phase 4: Construction Implement EPC to Mechanical Completion Develop company Policies & Standards Develop company HR Resources Institute continuous Corporate Governance Transition to business unit Develop sustainable CSR Deliver Gas Meet contractual obligations Commit for expansion Meet Shareholder expectations Meet environmenta l/social standards Maintain CSR 8

9 The status update on the project is as follows: NNPC progressing with the Trans-Nigerian Segment of the Pipeline to kick-start and fast track the initiative Completed the FEED of a 2X48 pipeline from Calabar, via Ajaokuta to Kano Identified and surveyed the pipeline right of way Carrying out an optimization study of the pipeline to enable domestic utilization in the first instance During construction, loop pipeline at critical locations River Crossings etc. to reduce construction costs when full TSGP capacity pipeline is being deployed Progress engineering design and commence construction ACTIVITIES within Nigeria in 2013 Market Revalidation : TSGP sponsors to carry out a full market revalidation in 2013 Assess changing global market dynamics, particularly in Europe in view of USA shale gas, Russian pipeline to southern Europe, LNG imports etc. Revalidate economics of project and impact on overall pipeline design and scope Project Governance Issues o Nigeria is making Progress in securing NASS ratification of the IGA for the project Gas Supply o NNPC re-assessing gas supply options in view of unprecedented growth in domestic gas demand vis-à-vis demand at the initiation of the project o Also making progress on the alternative for Sonatrach s participation in the Nigerian upstream as basis for progressing with the project PPP o ICRC in collaboration with NNPC, has undertaken the following towards the successful implementation of the project: Constitution of an inter-ministerial team made up of NNPC, ICRC, Debt Management office (DMO), and Nigerian electricity regulatory commission (NERC) to fast track the implementation of the project through a PPP model Engagement of private investors and financial institutions such as the AFDB, African Finance Corporation (AFC) and European Investment Bank (EIB) to provide funding for the actualization of the project o While the following are in progress: The review of the Gas Transmission Tariff Study Consultation strategies to discuss a way forward with other sponsoring governments on the ratification of the IGA. 9

10 The next steps on the project will be as follows: Kick-off the market revalidation study in the 4 th quarter 2013 Conclude the Trans-Nigerian optimization study and identify critical areas of synergy with the TSGP from a construction point of view Update the IGA in line with the alternative Sonatrach participating arrangement and secure internal NASS ratification Commence with the relevant DIRECTORATES OF NNPC, the review of supply options based on the revalidated study of the market and economics of gas supply Risk Analysis Potential Risk Description Impact on Project Mitigation Arrangement Fall in European Will impact project Demand viability Inflation project costs of Financial Status There are alternative sources for EU demand Inflation of project cost may lead to tariff structures that less viable May impact project feasibility, if tariffs become too high for off-takers Continued discussions between project sponsors and EU buyers New feasibility study to assess demand conditions. New feasibility study to assess feasible tariff structures. Total estimated Project Value USD 20,000,000,000 Highlights of feasibility study (2006): PIPELINE CAPEX USD10 billion 48 line diameter USD13.7 billion 56 line diameter GAS GATHERING CAPEX USD 3 billion BORDER PRICE US$/MMBTU $25 40/BBL OIL PROJECT FUNDING EQUITY + DEBT FINANCING INTERNAL RATE OF RETURN % EQUITY PAYBACK 4 7 YEARS GAS MARKET IN EUROPE GAS MARKET OF 20BCM/Y (2BCF/D) EXISTS FROM 2015 Preparation cost Incurred USD 2 billion Preparation cost planned/remaining USD 3/1 billion Planned debt equity ratio Funding Gap USD 20 billion 10

11 11

AN OVERVIEW OF THE NIGERIAN DOWNSTREAM GAS MARKET. Emeka Onyegbule Market Competition and Rates Division, NERC Abuja 27 th November 2012

AN OVERVIEW OF THE NIGERIAN DOWNSTREAM GAS MARKET Emeka Onyegbule Market Competition and Rates Division, NERC Abuja 27 th November 2012 Presentation Outline Background Challenges and Obstacles to Gas development

AN OVERVIEW OF THE NIGERIAN DOWNSTREAM GAS MARKET Emeka Onyegbule Market Competition and Rates Division, NERC Abuja 27 th November 2012 Presentation Outline Background Challenges and Obstacles to Gas development

Gas for Power: The Future of Gas as an Energy Solution for Nigeria. by Engr. Saidu A. Mohammed. Nigerian National Petroleum Corporation (NNPC)

") Gas for Power: The Future of Gas as an Energy Solution for Nigeria by Engr. Saidu A. Mohammed Group Executive Director/COO, Gas and Power Nigerian National Petroleum Corporation (NNPC) at The Annual Powering

Gas for Power: The Future of Gas as an Energy Solution for Nigeria by Engr. Saidu A. Mohammed Group Executive Director/COO, Gas and Power Nigerian National Petroleum Corporation (NNPC) at The Annual Powering

German Marshall Fund Brussels Forum. Dev Sanyal, chief executive, alternative energy and executive vice president, regions

German Marshall Fund Brussels Forum Dev Sanyal, chief executive, alternative energy and executive vice president, regions Thank you, it s a pleasure to be involved in the Brussels Forum again this year.

German Marshall Fund Brussels Forum Dev Sanyal, chief executive, alternative energy and executive vice president, regions Thank you, it s a pleasure to be involved in the Brussels Forum again this year.

Update on the Nigerian Gas Master-plan

June 5 th 2013 NOG Tech Lagos, Nigeria Update on the Nigerian Gas Master-plan Dr. David Ige Group Executive Director, Gas & Power NNPC Outline Overview of the Nigerian Gas Sector Our Scorecard Gas Industrialization

June 5 th 2013 NOG Tech Lagos, Nigeria Update on the Nigerian Gas Master-plan Dr. David Ige Group Executive Director, Gas & Power NNPC Outline Overview of the Nigerian Gas Sector Our Scorecard Gas Industrialization

The West African Gas Pipeline An Overview

The West African Gas Pipeline An Overview Ing. Ken Yeboah. MBA, BSc. (MBA-IMRE Alumnus) Presentation Outline Introduction Background Objectives Ownership and Sponsorship Project Description Benefits (Economic/Social/Environmental)

The West African Gas Pipeline An Overview Ing. Ken Yeboah. MBA, BSc. (MBA-IMRE Alumnus) Presentation Outline Introduction Background Objectives Ownership and Sponsorship Project Description Benefits (Economic/Social/Environmental)

Developing Domestic Gas Infrastructure...a private sector approach

Developing Domestic Gas Infrastructure...a private sector approach The Nigerian Infrastructure Summit Transcorp Hilton, Abuja 6 th -8 th August 2008 Wale Tinubu Oando PLC 1 Outline 1.0 Background Nigerian

Developing Domestic Gas Infrastructure...a private sector approach The Nigerian Infrastructure Summit Transcorp Hilton, Abuja 6 th -8 th August 2008 Wale Tinubu Oando PLC 1 Outline 1.0 Background Nigerian

Meeting the Growing Need for Natural Gas Imports in the EU >

Nord Stream A Successful Major Infrastructure Project and the Way Forward > Paul Corcoran, Financial Director, Nord Stream AG The European Gas Conference 2013, Vienna CEO PERSPECTIVES major supply routes

Nord Stream A Successful Major Infrastructure Project and the Way Forward > Paul Corcoran, Financial Director, Nord Stream AG The European Gas Conference 2013, Vienna CEO PERSPECTIVES major supply routes

NATURAL GAS AND ALGERIAN STRATEGY FOR RENEWABLE ENERGY

The 2nd Arab Cleaner Production Workshop Amman, 28-30 August 2007 NATURAL GAS AND ALGERIAN STRATEGY FOR RENEWABLE ENERGY Presented by: Mr L.AZZAZ- ALGERIA National Institute of Planning and Statistics

The 2nd Arab Cleaner Production Workshop Amman, 28-30 August 2007 NATURAL GAS AND ALGERIAN STRATEGY FOR RENEWABLE ENERGY Presented by: Mr L.AZZAZ- ALGERIA National Institute of Planning and Statistics

Lighting up and powering Africa with the African Development Bank. A quick overview

Lighting up and powering Africa with the African Development Bank A quick overview Hello! I am Amadou Hott Vice President Vice-President, Power, Energy, Climate and Green Growth Presentation outline The

Lighting up and powering Africa with the African Development Bank A quick overview Hello! I am Amadou Hott Vice President Vice-President, Power, Energy, Climate and Green Growth Presentation outline The

The Galsi project. The Galsi project Presentation

The Galsi project The Galsi project Presentation Index The Galsi project Technical figures Strategic value Project phase SLIDE 2/19 / JANUARY 2010 The Galsi project who we are Galsi was formed in 2003

The Galsi project The Galsi project Presentation Index The Galsi project Technical figures Strategic value Project phase SLIDE 2/19 / JANUARY 2010 The Galsi project who we are Galsi was formed in 2003

CANADA S OIL & NATURAL GAS PRODUCERS. OIL AND NATURAL GAS PRIORITIES for a prosperous British Columbia

CANADA S OIL & NATURAL GAS PRODUCERS OIL AND NATURAL GAS PRIORITIES for a prosperous British Columbia KEY POINTS THE OIL AND NATURAL GAS INDUSTRY: Delivers jobs and economic benefits to B.C. Operates with

CANADA S OIL & NATURAL GAS PRODUCERS OIL AND NATURAL GAS PRIORITIES for a prosperous British Columbia KEY POINTS THE OIL AND NATURAL GAS INDUSTRY: Delivers jobs and economic benefits to B.C. Operates with

AFRICA A NEW PLAYER IN THE ENERGY MARKET: - EAST AFRICA - EAST MEDITERRANEAN

AFRICA A NEW PLAYER IN THE ENERGY MARKET: - EAST AFRICA - EAST MEDITERRANEAN Eng. Khaled Abubakr Middle East & Africa Regional Coordinator, IGU Chairman, Egyptian Gas Association Chairman, TAQA Arabia

AFRICA A NEW PLAYER IN THE ENERGY MARKET: - EAST AFRICA - EAST MEDITERRANEAN Eng. Khaled Abubakr Middle East & Africa Regional Coordinator, IGU Chairman, Egyptian Gas Association Chairman, TAQA Arabia

Introduction, Vision and Team Q2 2019

Introduction, Vision and Team Q2 2019 1 Gas Midstream in SSA Why target mid-stream SSA? Natural gas infrastructure in Sub-Saharan is an open energy value chain segment presenting a large opportunity to

Introduction, Vision and Team Q2 2019 1 Gas Midstream in SSA Why target mid-stream SSA? Natural gas infrastructure in Sub-Saharan is an open energy value chain segment presenting a large opportunity to

SUB-SAHARAN AFRICA (SSA) POWER SECTOR STRATEGY. October 2016

POWER SECTOR STRATEGY. October 2016") SUB-SAHARAN AFRICA (SSA) POWER SECTOR STRATEGY October 2016 Table of Contents Table of Contents 1. How we approach assessment of a regional market? 2. Example: Sub-Sahara Africa (SSA) 3. SSA strategy on

SUB-SAHARAN AFRICA (SSA) POWER SECTOR STRATEGY October 2016 Table of Contents Table of Contents 1. How we approach assessment of a regional market? 2. Example: Sub-Sahara Africa (SSA) 3. SSA strategy on

European Economic and Social Committee OPINION

European Economic and Social Committee TEN/589 An EU strategy for liquefied natural gas and gas storage OPINION of the European Economic and Social Committee on the Communication from the Commission to

European Economic and Social Committee TEN/589 An EU strategy for liquefied natural gas and gas storage OPINION of the European Economic and Social Committee on the Communication from the Commission to

TAPI Pipeline Project. Presentation to ECO Chamber of Commerce and Industry (ECO CCI) 16 October 2018

16 October 2018") TAPI Pipeline Project Presentation to ECO Chamber of Commerce and Industry (ECO CCI) 16 October 2018 Introduction to the Project TAPI Pipeline Project was originally conceived in the 1990s with a view

TAPI Pipeline Project Presentation to ECO Chamber of Commerce and Industry (ECO CCI) 16 October 2018 Introduction to the Project TAPI Pipeline Project was originally conceived in the 1990s with a view

Investment Opportunities for Private Participation in Gas Supply and Infrastructure in Nigeria

March 2014 Lagos Investment Opportunities for Private Participation in Gas Supply and Infrastructure in Nigeria Dr. David Ige Group Executive Director, Gas & Power NNPC March 2014 Lagos Engr. Sam Ndukwe

March 2014 Lagos Investment Opportunities for Private Participation in Gas Supply and Infrastructure in Nigeria Dr. David Ige Group Executive Director, Gas & Power NNPC March 2014 Lagos Engr. Sam Ndukwe

RENEWABLE ENERGY IN THE SERVICE OF HUMANITY

Towards Sustainable Energy RENEWABLE ENERGY IN THE SERVICE OF HUMANITY Mahama Kappiah Executive Director ECREEE OUTLINE Background : West Africa Overview Of ECREEE and Priority Activities Solar RE Resources

Towards Sustainable Energy RENEWABLE ENERGY IN THE SERVICE OF HUMANITY Mahama Kappiah Executive Director ECREEE OUTLINE Background : West Africa Overview Of ECREEE and Priority Activities Solar RE Resources

Innovative Financing through Innovative Partnerships. Nora Berrahmouni, Christophe Besacier FAO Forestry Department

Innovative Financing through Innovative Partnerships Nora Berrahmouni, Christophe Besacier FAO Forestry Department Presentation of two examples 1. Support to the implementation of the Great Green Wall

Innovative Financing through Innovative Partnerships Nora Berrahmouni, Christophe Besacier FAO Forestry Department Presentation of two examples 1. Support to the implementation of the Great Green Wall

DUAL PLENARY SESSION: Energy Market Integration - Developments in LNG

DUAL PLENARY SESSION: Energy Market Integration - Developments in LNG Effects of recent and future developments in LNG markets on the interconnectedness of regional gas markets Fisoye Delano Poten & Partners

DUAL PLENARY SESSION: Energy Market Integration - Developments in LNG Effects of recent and future developments in LNG markets on the interconnectedness of regional gas markets Fisoye Delano Poten & Partners

Table 1 Trade movements 2004 LNG (Bcm)

") LNG Prospects for the Future The prospect that LNG could become a major global energy source is one of the most keenly debated issues in the sector. This was reflected in this quarter's survey, conducted

LNG Prospects for the Future The prospect that LNG could become a major global energy source is one of the most keenly debated issues in the sector. This was reflected in this quarter's survey, conducted

EUROPEAN ENERGY MARKET:

EUROPEAN ENERGY MARKET: RE-DESIGNING THE FRAMEWORK The Cyprus-EU Presidency Summit Cyprus Energy Regulatory Authority George Shammas Chairman October 8 th -9 th, Nicosia Email:info@cera.org.cy website:www.cera.org.cy

EUROPEAN ENERGY MARKET: RE-DESIGNING THE FRAMEWORK The Cyprus-EU Presidency Summit Cyprus Energy Regulatory Authority George Shammas Chairman October 8 th -9 th, Nicosia Email:info@cera.org.cy website:www.cera.org.cy

The Nigerian Power Sector A case study of Power sector reform and the role of PPP

The Nigerian Power Sector A case study of Power sector reform and the role of PPP Erik Fernstrom World Bank November 14, 2011 1 Background: Nigeria Nigeria: Population is the seventh largest in the World,

The Nigerian Power Sector A case study of Power sector reform and the role of PPP Erik Fernstrom World Bank November 14, 2011 1 Background: Nigeria Nigeria: Population is the seventh largest in the World,

Solon Kassinis Director - Energy Service

New Energy Sources of Supply for Europe: The Prospects for Southeast Europe and Eastern Mediterranean Solon Kassinis Director - Energy Service 16 th Roundtable with the Government of Greece Transforming

New Energy Sources of Supply for Europe: The Prospects for Southeast Europe and Eastern Mediterranean Solon Kassinis Director - Energy Service 16 th Roundtable with the Government of Greece Transforming

Indaba Energy Leaders Dialogue (IELD)

") Indaba Energy Leaders Dialogue (IELD) Featuring the Trilemma Ministerial Roundtable 17 February 2015, Johannesburg, South Africa Debrief and Summary Notes Over 40 energy leaders representing the entire

Indaba Energy Leaders Dialogue (IELD) Featuring the Trilemma Ministerial Roundtable 17 February 2015, Johannesburg, South Africa Debrief and Summary Notes Over 40 energy leaders representing the entire

SOUTH-EAST EUROPE: A STRATEGIC ROLE IN EURO-ATLANTIC ENERGY SECURITY

ENERGY REALITY IN SOUTH-EAST EUROPE INTERNATIONAL CONFERENCE, 31 MAY 2012, GRAND HOTEL UNION LJUBLJANA, SLOVENIA SOUTH-EAST EUROPE: A STRATEGIC ROLE IN EURO-ATLANTIC ENERGY SECURITY Peter Poptchev, Ambassador-at-large

ENERGY REALITY IN SOUTH-EAST EUROPE INTERNATIONAL CONFERENCE, 31 MAY 2012, GRAND HOTEL UNION LJUBLJANA, SLOVENIA SOUTH-EAST EUROPE: A STRATEGIC ROLE IN EURO-ATLANTIC ENERGY SECURITY Peter Poptchev, Ambassador-at-large

NABUCCO Why? - When? - Some Myths and Facts

NABUCCO Why? - When? - Some Myths and Facts More than ever, Nabucco is needed for the following reasons: With the gas crisis in the winter of 2008 and 2009, European consumers have experienced personally

NABUCCO Why? - When? - Some Myths and Facts More than ever, Nabucco is needed for the following reasons: With the gas crisis in the winter of 2008 and 2009, European consumers have experienced personally

Lecture 12. LNG Markets

Lecture 12 LNG Markets Data from BP Statistical Review of World Energy 1991 to 2016 Slide 1 LNG Demand LNG demand is expected to grow from China, India and Europe in particular. Currently biggest importer

Lecture 12 LNG Markets Data from BP Statistical Review of World Energy 1991 to 2016 Slide 1 LNG Demand LNG demand is expected to grow from China, India and Europe in particular. Currently biggest importer

ENVIRONMENT AND ENERGY BULLETIN

ENVIRONMENT AND ENERGY BULLETIN Vol. 3 No. 2 June 2011 Editor: Jock A. Finlayson THE NATURAL GAS STORY Both globally and in North America, natural gas is poised to play a bigger role in meeting the energy

ENVIRONMENT AND ENERGY BULLETIN Vol. 3 No. 2 June 2011 Editor: Jock A. Finlayson THE NATURAL GAS STORY Both globally and in North America, natural gas is poised to play a bigger role in meeting the energy

Concept Note Expert Working Group on PPPs in Africa s Electricity Sector

UNITED NATIONS ECONOMIC COMMISSION FOR AFRICA Concept Note Expert Working Group on PPPs in Africa s Electricity Sector Introduction This initiative is intended to launch an effort by the United Nations

UNITED NATIONS ECONOMIC COMMISSION FOR AFRICA Concept Note Expert Working Group on PPPs in Africa s Electricity Sector Introduction This initiative is intended to launch an effort by the United Nations

Energy Security in the Baltic Sea Region

SPEECH/08/296 Andris Piebalgs Energy Commissioner Energy Security in the Baltic Sea Region Speech at the Baltic Sea Regional Business Forum (Plenary Session: Energy Security) Riga, 3 June 2008 Dear Minister

SPEECH/08/296 Andris Piebalgs Energy Commissioner Energy Security in the Baltic Sea Region Speech at the Baltic Sea Regional Business Forum (Plenary Session: Energy Security) Riga, 3 June 2008 Dear Minister

Cotonou Agreement 1) OBJECTIVE 2) ACT 3) SUMMARY.

OBJECTIVE 2) ACT 3) SUMMARY.") Cotonou Agreement http://www.acp.int/en/conventions/cotonou/accord1.htm 1) OBJECTIVE To set up a new framework for cooperation between the members of the African, Caribbean and Pacific Group of States

Cotonou Agreement http://www.acp.int/en/conventions/cotonou/accord1.htm 1) OBJECTIVE To set up a new framework for cooperation between the members of the African, Caribbean and Pacific Group of States

Outline 1 Introduction : Key Data of Malaysia 2 Energy Policies Electricity Sector in Malaysia Challenges in Meeting Future Energy Demand Mo

TRAINING AND DIALOGUE PROGRAMS OF JICA ENERGY POLICY COUNTRY PRESENTATION: MALAYSIA May 2011 1 Outline 1 Introduction : Key Data of Malaysia 2 Energy Policies 3 4 5 6 7 Electricity Sector in Malaysia Challenges

TRAINING AND DIALOGUE PROGRAMS OF JICA ENERGY POLICY COUNTRY PRESENTATION: MALAYSIA May 2011 1 Outline 1 Introduction : Key Data of Malaysia 2 Energy Policies 3 4 5 6 7 Electricity Sector in Malaysia Challenges

For personal use only

1 December 2016 Tlou Energy Limited ( Tlou or the Company ) LESEDI PROJECT UPDATE AND FIELD DEVELOPMENT PROGRAM Tlou Energy Limited, the AIM and ASX listed company focused on delivering power in Botswana

1 December 2016 Tlou Energy Limited ( Tlou or the Company ) LESEDI PROJECT UPDATE AND FIELD DEVELOPMENT PROGRAM Tlou Energy Limited, the AIM and ASX listed company focused on delivering power in Botswana

JAES Action Plan Partnership on Climate Change and Environment

JAES Action Plan 2011-2013 Partnership on Climate Change and Environment Overview The first Action Plan (2008-2010) for the implementation of the Joint Africa-EU Strategy (JAES) adopted in Lisbon Summit

JAES Action Plan 2011-2013 Partnership on Climate Change and Environment Overview The first Action Plan (2008-2010) for the implementation of the Joint Africa-EU Strategy (JAES) adopted in Lisbon Summit

The global energy arena

Redner: Peter Mather Veranstaltungstermin: 20. Januar 2015 Ort: Handelsblatt Energietagung, Berlin Titel: BP Regional Vice President Europe und Head of Country UK Es gilt das gesprochene Wort. Introduction

Redner: Peter Mather Veranstaltungstermin: 20. Januar 2015 Ort: Handelsblatt Energietagung, Berlin Titel: BP Regional Vice President Europe und Head of Country UK Es gilt das gesprochene Wort. Introduction

Scoping Study Highlights Chad Liquefied Natural Gas (LNG) Project

Project") Scoping Study Highlights Chad Liquefied Natural Gas (LNG) Project CHAD LNG PROJECT SCOPING STUDY HIGHLIGHTS A long-term significant Investment Prefeasibility study to begin to evaluate the project optimisations,

Scoping Study Highlights Chad Liquefied Natural Gas (LNG) Project CHAD LNG PROJECT SCOPING STUDY HIGHLIGHTS A long-term significant Investment Prefeasibility study to begin to evaluate the project optimisations,

Connecting Possibilities

Living Energy Connecting Possibilities Scenarios for Optimizing Energy Systems Answers for energy. We invest more in efficient power generation so you can generate more return on investment. Affordability

Living Energy Connecting Possibilities Scenarios for Optimizing Energy Systems Answers for energy. We invest more in efficient power generation so you can generate more return on investment. Affordability

Offshore Tanzania. Equinor in Tanzania

Block 2 Tanzania An emerging gas sector Major gas discoveries have been made offshore Tanzania and the country emerges as a potential large gas producer in East Africa. In Block 2, Equinor together with

Block 2 Tanzania An emerging gas sector Major gas discoveries have been made offshore Tanzania and the country emerges as a potential large gas producer in East Africa. In Block 2, Equinor together with

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project June 20, 2008 Barry Pulliam Senior Economist Econ One Research 5th Floor 601 W 5th Street Los Angeles, California 90071 213

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project June 20, 2008 Barry Pulliam Senior Economist Econ One Research 5th Floor 601 W 5th Street Los Angeles, California 90071 213

KARENSLYST ALLÉ 4, 0278 OSLO, NORWAY P.O. BOX 157, 0212 OSLO, NORWAY

KARENSLYST ALLÉ 4, 0278 OSLO, NORWAY P.O. BOX 157, 0212 OSLO, NORWAY Content About us 2 Our model 3 Our experience 4 Oil and Gas (E&P) 5 Liquefied Natural Gas (LNG) 5 Regasification of LNG (FSRU) 6 Environment

KARENSLYST ALLÉ 4, 0278 OSLO, NORWAY P.O. BOX 157, 0212 OSLO, NORWAY Content About us 2 Our model 3 Our experience 4 Oil and Gas (E&P) 5 Liquefied Natural Gas (LNG) 5 Regasification of LNG (FSRU) 6 Environment

Corporate Brochure Q2 2019

Corporate Brochure Q2 2019 2 Purpose Why target mid-stream SSA? Why target MGA? Monetizing Gas Africa (MGA) maximizes commercial availability of natural gas by increasing infrastructure in Sub-Saharan

Corporate Brochure Q2 2019 2 Purpose Why target mid-stream SSA? Why target MGA? Monetizing Gas Africa (MGA) maximizes commercial availability of natural gas by increasing infrastructure in Sub-Saharan

A AFRICA EU DECLARATION ON CLIMATE CHANGE

A AFRICA EU DECLARATION ON CLIMATE CHANGE BACKGROUND /PREAMBULAR PARAGRAPHS 1. During the 11 th Ministerial Meeting of the African and EU Troikas that took place in Addis Ababa on 20 and 21 November 2008

A AFRICA EU DECLARATION ON CLIMATE CHANGE BACKGROUND /PREAMBULAR PARAGRAPHS 1. During the 11 th Ministerial Meeting of the African and EU Troikas that took place in Addis Ababa on 20 and 21 November 2008

Gas & Power Sector in Nigeria Issues and Challenges Engr. Kunle Allen (MD/CEO) Gas Aggregation Company Nigeria Limited (GACN)

Gas Aggregation Company Nigeria Limited (GACN)") The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still

The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still

Nigeria Liquefied Natural Gas Company, Bonny Island, Nigeria

NIGERIAN GAS MASTER PLAN: STRENGTHENING THE NIGERIA GAS INFRASTRUCTURE BLUEPRINT AS A BASE FOR EXPANDING REGIONAL GAS MARKET Ukpohor, Excel Theophilus O. Nigeria Liquefied Natural Gas Company, Bonny Island,

NIGERIAN GAS MASTER PLAN: STRENGTHENING THE NIGERIA GAS INFRASTRUCTURE BLUEPRINT AS A BASE FOR EXPANDING REGIONAL GAS MARKET Ukpohor, Excel Theophilus O. Nigeria Liquefied Natural Gas Company, Bonny Island,

UNDERSTANDING NATURAL GAS MARKETS. Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015

UNDERSTANDING NATURAL GAS MARKETS Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015 Table of Contents 3 Overview Natural Gas is an Important Source of Energy for the United States.

UNDERSTANDING NATURAL GAS MARKETS Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015 Table of Contents 3 Overview Natural Gas is an Important Source of Energy for the United States.

COMBATING CLIMATE CHANGE AND LAND DEGRADATION IN THE WEST AFRICAN SAHEL: A MULTI-COUNTRY STUDY OF MALI, NIGER AND SENEGAL

COMBATING CLIMATE CHANGE AND LAND DEGRADATION IN THE WEST AFRICAN SAHEL: A MULTI-COUNTRY STUDY OF MALI, NIGER AND SENEGAL BY PROF. S.A. IGBATAYO HEAD, DEPARTMENT OF ECONOMICS & MANAGEMENT STUDIES AFE BABALOLA

COMBATING CLIMATE CHANGE AND LAND DEGRADATION IN THE WEST AFRICAN SAHEL: A MULTI-COUNTRY STUDY OF MALI, NIGER AND SENEGAL BY PROF. S.A. IGBATAYO HEAD, DEPARTMENT OF ECONOMICS & MANAGEMENT STUDIES AFE BABALOLA

SYNOPSIS OF THE 2017 NATIONAL GAS POLICY

SYNOPSIS OF THE 2017 NATIONAL GAS POLICY Introduction On Wednesday, June 28, 2017, the Federal Executive Council (FEC) at its monthly meeting approved the National Gas Policy, 2017 ( NGP ). The NGP, which

SYNOPSIS OF THE 2017 NATIONAL GAS POLICY Introduction On Wednesday, June 28, 2017, the Federal Executive Council (FEC) at its monthly meeting approved the National Gas Policy, 2017 ( NGP ). The NGP, which

European Gas & LNG Markets, Energy Policy, and Geopolitics October 2016

European Gas & LNG Markets, Energy Policy, and Geopolitics October 2016 www.rapidangroup.com Leslie.palti-guzman@rapidangroup.com t. +1 301.656.4480 No Quotation or Distribution 1 EU LNG Demand Key Themes:

European Gas & LNG Markets, Energy Policy, and Geopolitics October 2016 www.rapidangroup.com Leslie.palti-guzman@rapidangroup.com t. +1 301.656.4480 No Quotation or Distribution 1 EU LNG Demand Key Themes:

Energy Security. Revision Booklet

Energy Security Revision Booklet This is a sample edition of the Energy Security Revision Booklet. The total content has been reduced in this copy, and content watermarked. The Revision Booklet available

Energy Security Revision Booklet This is a sample edition of the Energy Security Revision Booklet. The total content has been reduced in this copy, and content watermarked. The Revision Booklet available

ISSUES OF GAS SUPPLY SECURING

Economic Commission for Europe - Committee on Sustainable Energy - Securing Affordable and Sustainable Energy DEPUTY HEAD OF STRATEGIC DEVELOPMENT DEPARTMENT SERGEY PANKRATOV 17.11.2011 Gazprom remains

Economic Commission for Europe - Committee on Sustainable Energy - Securing Affordable and Sustainable Energy DEPUTY HEAD OF STRATEGIC DEVELOPMENT DEPARTMENT SERGEY PANKRATOV 17.11.2011 Gazprom remains

List of Acronyms... v. I. Introduction II. Key Activities and Results within the Cluster... 2

Aide-Mémoire 13th Session of the Regional Coordination Mechanism of UN Agencies and Organizations Working in Africa in Support of the African Union and its NEPAD Programme (RCM-Africa) Addis Ababa, Ethiopia

Aide-Mémoire 13th Session of the Regional Coordination Mechanism of UN Agencies and Organizations Working in Africa in Support of the African Union and its NEPAD Programme (RCM-Africa) Addis Ababa, Ethiopia

African Development Bank Group Climate finance for Africa in Action

African Development Bank Group Climate finance for Africa in Action 20 October, 2012 Outline I. The Challenges Ahead II. III. Climate change finance instruments Project examples 2 I. The Challenge Ahead

African Development Bank Group Climate finance for Africa in Action 20 October, 2012 Outline I. The Challenges Ahead II. III. Climate change finance instruments Project examples 2 I. The Challenge Ahead

Council of the European Union Brussels, 28 June 2017 (OR. en)

") Council of the European Union Brussels, 28 June 2017 (OR. en) 10534/17 ENER 301 'I' ITEM NOTE From: General Secretariat of the Council To: Permanent Representatives Committee (Part 1) Subject: EU-Japan

Council of the European Union Brussels, 28 June 2017 (OR. en) 10534/17 ENER 301 'I' ITEM NOTE From: General Secretariat of the Council To: Permanent Representatives Committee (Part 1) Subject: EU-Japan

The role of natural gas in the transition to achieving sustainable energy for all in Africa. 16 July ENGIE, A World Leader in Energy

The role of natural gas in the transition to achieving sustainable energy for all in Africa 16 July 2016 PRESENTATION ENGIE, A World Leader in Energy By Karim Barbir, Director of Gas Chain, ENGIE The views

The role of natural gas in the transition to achieving sustainable energy for all in Africa 16 July 2016 PRESENTATION ENGIE, A World Leader in Energy By Karim Barbir, Director of Gas Chain, ENGIE The views

gas 2O18 Analysis and Forecasts to 2O23

Market Report Series gas 2O18 Analysis and Forecasts to 2O23 executive summary INTERNATIONAL ENERGY AGENCY The IEA examines the full spectrum of energy issues including oil, gas and coal supply and demand,

Market Report Series gas 2O18 Analysis and Forecasts to 2O23 executive summary INTERNATIONAL ENERGY AGENCY The IEA examines the full spectrum of energy issues including oil, gas and coal supply and demand,

WORLD BANK- AUC- ACPC EGM ON ENHANCING THE CLIMATE RESILIENCE OF AFRICA S INFRASTRUCTURE

AFRICAN UNION WORLD BANK- AUC- ACPC EGM ON ENHANCING THE CLIMATE RESILIENCE OF AFRICA S INFRASTRUCTURE AUC PRESENTATION ON PIDA - ENERGY COMPONENT by Philippe NIYONGABO Head of Energy Division, Infrastructure

AFRICAN UNION WORLD BANK- AUC- ACPC EGM ON ENHANCING THE CLIMATE RESILIENCE OF AFRICA S INFRASTRUCTURE AUC PRESENTATION ON PIDA - ENERGY COMPONENT by Philippe NIYONGABO Head of Energy Division, Infrastructure

January Christof Rühl, Group Chief Economist

January 213 Christof Rühl, Group Chief Economist Contents Introduction Global energy trends Outlook 23: Fuel by fuel Implications Energy Outlook 23 BP 213 Introduction Global energy trends Outlook 23:

January 213 Christof Rühl, Group Chief Economist Contents Introduction Global energy trends Outlook 23: Fuel by fuel Implications Energy Outlook 23 BP 213 Introduction Global energy trends Outlook 23:

REPORT the Commission and the Secretary-General/High Representative European Council An external policy to serve Europe's energy interests

COUNCIL OF THE EUROPEAN UNION Brussels, 30 May 2006 9971/06 POLG 73 ER 176 V 326 DEVG 158 RELEX 371 TRANS 150 ELARG 59 RECH 151 REPORT from : to : Subject : the Commission and the Secretary-General/High

COUNCIL OF THE EUROPEAN UNION Brussels, 30 May 2006 9971/06 POLG 73 ER 176 V 326 DEVG 158 RELEX 371 TRANS 150 ELARG 59 RECH 151 REPORT from : to : Subject : the Commission and the Secretary-General/High

World Energy Outlook Dr. Fatih Birol IEA Chief Economist Rome, 18 November 2009

World Energy Outlook 29 Dr. Fatih Birol IEA Chief Economist Rome, 18 November 29 Change in primary energy demand in the Reference Scenario, 27-23 Coal Oil Gas Nuclear OECD Non-OECD Hydro Biomass Other

World Energy Outlook 29 Dr. Fatih Birol IEA Chief Economist Rome, 18 November 29 Change in primary energy demand in the Reference Scenario, 27-23 Coal Oil Gas Nuclear OECD Non-OECD Hydro Biomass Other

Opportunities for Regional and Domestic use of Associated Gas in Nigeria OPEC/World Bank Workshop on Global Gas Flaring Reduction

Opportunities for Regional and Domestic use of Associated Gas in Nigeria OPEC/World Bank Workshop on Global Gas Flaring Reduction Vienna Austria - July 1, 2005 PETROLEUM NATIONAL NIGERIAN 1 CORPORATION

Opportunities for Regional and Domestic use of Associated Gas in Nigeria OPEC/World Bank Workshop on Global Gas Flaring Reduction Vienna Austria - July 1, 2005 PETROLEUM NATIONAL NIGERIAN 1 CORPORATION

Support to African countries in implementation of the UN Convention to Combat Desertification (Report to the Third Conference of the Parties)

") European Community Support to African countries in implementation of the UN Convention to Combat Desertification (Report to the Third Conference of the Parties) June 1999 Contents 1. Overview: EC-Africa

European Community Support to African countries in implementation of the UN Convention to Combat Desertification (Report to the Third Conference of the Parties) June 1999 Contents 1. Overview: EC-Africa

Development. and. Further

03 TowardGrowth Further Development and The Osaka Gas Group is actively investing in areas aimed at expanding new businesses as part of efforts to realize its long-term management vision and mediumterm

03 TowardGrowth Further Development and The Osaka Gas Group is actively investing in areas aimed at expanding new businesses as part of efforts to realize its long-term management vision and mediumterm

GLNG project sanctioned. Final investment decision on US$16 billion 2-train 7.8 mtpa project

Media enquiries Investor enquiries Matthew Doman Andrew Nairn +61 8 8116 5260 / +61 (0) 421 888 858 +61 8 8116 5314 / +61 (0) 437 166 497 matthew.doman@santos.com andrew.nairn@santos.com 13 January 2011

Media enquiries Investor enquiries Matthew Doman Andrew Nairn +61 8 8116 5260 / +61 (0) 421 888 858 +61 8 8116 5314 / +61 (0) 437 166 497 matthew.doman@santos.com andrew.nairn@santos.com 13 January 2011

African Gas Infrastructure: Project Development and Financing

23 May 2017 African Gas Infrastructure: Project Development and Financing 1 Gas Midstream in SSA What is Gas Infrastructure? Context What is in scope for midstream gas infrastructure? State of play Project

23 May 2017 African Gas Infrastructure: Project Development and Financing 1 Gas Midstream in SSA What is Gas Infrastructure? Context What is in scope for midstream gas infrastructure? State of play Project

Renewable Energy Policy in the European Union

SPEECH/05/665 Stavros Dimas Member of the European Commission, Responsible for Environment Renewable Energy Policy in the European Union The Beijing International Renewable Energy Conference Beijing, 7

SPEECH/05/665 Stavros Dimas Member of the European Commission, Responsible for Environment Renewable Energy Policy in the European Union The Beijing International Renewable Energy Conference Beijing, 7

Status: S3 programme/project structuring and promotion to obtain financing. Project Number: E.07.1 Project Title: Sambangalou Dam

Project Number: E.07.1 Project Title: Sambangalou Dam Status: S3 programme/project structuring and promotion to obtain financing Countries Region Senegal, Guinea, Gambia West Africa Project Location It

Project Number: E.07.1 Project Title: Sambangalou Dam Status: S3 programme/project structuring and promotion to obtain financing Countries Region Senegal, Guinea, Gambia West Africa Project Location It

10th German-African-Energy Forum, Hamburg, April 25 & 26, 2016

INGA? What is Inga A brief history Recent development The current tender WHAT IS INGA? What is INGA? The best hydroelectric site in the World Total potential 44 GW (roughly equivalent 44 nuclear power

INGA? What is Inga A brief history Recent development The current tender WHAT IS INGA? What is INGA? The best hydroelectric site in the World Total potential 44 GW (roughly equivalent 44 nuclear power

Congo (Brazzaville) Background

Background") Page 1 of 6 Congo (Brazzaville) Last Updated: Dec. 14, 2011 Background Congo is a mature oil province with declining production; however, new offshore oil fields have recently reversed this trend and boosted

Page 1 of 6 Congo (Brazzaville) Last Updated: Dec. 14, 2011 Background Congo is a mature oil province with declining production; however, new offshore oil fields have recently reversed this trend and boosted

AmCham EU Position on Shale Gas Development in the EU

AmCham EU Position on Shale Gas Development in the EU Page 1 of 5 4 January 2013 AmCham EU Position on Shale Gas Development in the EU Shale gas could play an important role in the EU energy mix and policymakers

AmCham EU Position on Shale Gas Development in the EU Page 1 of 5 4 January 2013 AmCham EU Position on Shale Gas Development in the EU Shale gas could play an important role in the EU energy mix and policymakers

State of the Energy Union 2015 COMMISSION STAFF WORKING DOCUMENT. on the European Energy Security Strategy

EUROPEAN COMMISSION Brussels, 18.11.2015 SWD(2015) 404 final State of the Energy Union 2015 COMMISSION STAFF WORKING DOCUMENT on the European Energy Security Strategy EN EN 1. Introduction Energy security

EUROPEAN COMMISSION Brussels, 18.11.2015 SWD(2015) 404 final State of the Energy Union 2015 COMMISSION STAFF WORKING DOCUMENT on the European Energy Security Strategy EN EN 1. Introduction Energy security

International Conference Global Security in the 21st Century Perspectives from China and Europe

International Conference Perspectives from China and Europe Jointly organized by KAS and Institute of World Economics and Politics (IWEP), Beijing September 18-19, 27, Beijing Energy Supply Security: Demands

International Conference Perspectives from China and Europe Jointly organized by KAS and Institute of World Economics and Politics (IWEP), Beijing September 18-19, 27, Beijing Energy Supply Security: Demands

GAS ROUNDABOUT EXCESS CAPACITY. Myths and facts: The Netherlands as a. and EIB investments in

Myths and facts: Rotterdam Europort and third Maasvlakte (under construction) Photo: Frans de Wit on flickr/ CC BY-NC-ND 2.0 The Netherlands as a GAS ROUNDABOUT and EIB investments in EXCESS CAPACITY Introduction

Myths and facts: Rotterdam Europort and third Maasvlakte (under construction) Photo: Frans de Wit on flickr/ CC BY-NC-ND 2.0 The Netherlands as a GAS ROUNDABOUT and EIB investments in EXCESS CAPACITY Introduction

Options to scale up solar PV in. Vietnam. - Introduction. Vietnam

Options to scale up solar PV in Vietnam - Introduction Vietnam November 2015 Solar PV scale up in Vietnam INTRODUCTION Overall objectives To accelerate PV scale up in order to fulfill GoV target in a sustainable

Options to scale up solar PV in Vietnam - Introduction Vietnam November 2015 Solar PV scale up in Vietnam INTRODUCTION Overall objectives To accelerate PV scale up in order to fulfill GoV target in a sustainable

Summary Report of Multi-stakeholder Dialogue on Implementing Sustainable Development 1 February 2010, New York

- 1 - UNITED NATIONS DEPARTMENT OF ECONOMIC AND SOCIAL AFFAIRS DIVISION FOR SUSTAINABLE DEVELOPMENT Summary Report of Multi-stakeholder Dialogue on Implementing Sustainable Development 1 February 2010,

- 1 - UNITED NATIONS DEPARTMENT OF ECONOMIC AND SOCIAL AFFAIRS DIVISION FOR SUSTAINABLE DEVELOPMENT Summary Report of Multi-stakeholder Dialogue on Implementing Sustainable Development 1 February 2010,

The Nabucco Pipeline Project Fourth Corridor to Europe

The Nabucco Pipeline Project Fourth Corridor to Europe Gas pipes may be made of steel, but Nabucco can cement the links between our people (José Manuel Barroso, 13 July 2009, Ankara) RWE Supply & Trading

The Nabucco Pipeline Project Fourth Corridor to Europe Gas pipes may be made of steel, but Nabucco can cement the links between our people (José Manuel Barroso, 13 July 2009, Ankara) RWE Supply & Trading

Nigeria: Carbon Credit Development for Flare Reduction Projects. Guidebook

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Nigeria: Carbon Credit Development for Flare Reduction Projects ICF Consulting Ltd Guidebook

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Nigeria: Carbon Credit Development for Flare Reduction Projects ICF Consulting Ltd Guidebook

The Impact of the Recession on Gas Markets

The Impact of the Recession on Gas Markets What has changed in our Brave New World Gas demand dropped by 2% Bigger drops in OECD region, FSU, Latin America But some notable exceptions: China, India Some

The Impact of the Recession on Gas Markets What has changed in our Brave New World Gas demand dropped by 2% Bigger drops in OECD region, FSU, Latin America But some notable exceptions: China, India Some

LNG Markets in Transition : Will East meet West?

LNG Markets in Transition : Will East meet West? Jean-Marc Hosanski World Conference Tokyo, June 2nd, 2003 WOC 10 Thank you Mister Chairman, Ladies and Gentlemen, Distinguished Guests, My objective today

LNG Markets in Transition : Will East meet West? Jean-Marc Hosanski World Conference Tokyo, June 2nd, 2003 WOC 10 Thank you Mister Chairman, Ladies and Gentlemen, Distinguished Guests, My objective today

IDC s role in boosting private investment in Energy Infrastructure

Day Month Year IDC s role in boosting private investment in Energy Infrastructure Lindi Toyi PPP SBU Head : Industrial Development Corporation NEPAD-OECD AFRICA INVESTMENT INITIATIVE 11-12 November 2009

Day Month Year IDC s role in boosting private investment in Energy Infrastructure Lindi Toyi PPP SBU Head : Industrial Development Corporation NEPAD-OECD AFRICA INVESTMENT INITIATIVE 11-12 November 2009

Respondents Countries by Countries by Region (18) RECS (6) Region Region Countries

RECS (6) Region Region Countries") Implementation of the Abuja Declaration on Fertilizers for an African Green Revolution A Progress Report By Dr. Maria Wanzala IFDC/NEPAD Outline of Presentation Background Progress at the regional level

Implementation of the Abuja Declaration on Fertilizers for an African Green Revolution A Progress Report By Dr. Maria Wanzala IFDC/NEPAD Outline of Presentation Background Progress at the regional level

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. THE GAS PACKAGE - THE ROLE OF US LNG European Parliament Public Hearing Andrew Walker Vice-President, Strategy, Cheniere Marketing May 23, 2016 Forward Looking Statements This presentation

CHENIERE ENERGY, INC. THE GAS PACKAGE - THE ROLE OF US LNG European Parliament Public Hearing Andrew Walker Vice-President, Strategy, Cheniere Marketing May 23, 2016 Forward Looking Statements This presentation

Power, Energy Climate and Green Growth Complex. Strategy and Project pipeline

Power, Energy Climate and Green Growth Complex Strategy and Project pipeline 2 The New Deal for Energy in Africa 3 African Development Bank launched the New Deal on Energy for Africa in 2016 Lighting up

Power, Energy Climate and Green Growth Complex Strategy and Project pipeline 2 The New Deal for Energy in Africa 3 African Development Bank launched the New Deal on Energy for Africa in 2016 Lighting up

Rwanda, Burundi, Democratic Republic of Congo (DRC) East Africa Near Lake Kivu and the Ruzizi River at the border of Rwanda and the DRC

East Africa Near Lake Kivu and the Ruzizi River at the border of Rwanda and the DRC") Project Number: E.12.1 Project Title: Ruzizi III Hydropower Project Status: S3 programme/project structuring and promotion to obtain financing Countries Region Rwanda, Burundi, Democratic Republic of Congo

Project Number: E.12.1 Project Title: Ruzizi III Hydropower Project Status: S3 programme/project structuring and promotion to obtain financing Countries Region Rwanda, Burundi, Democratic Republic of Congo

Vol. - 1, Issue: June WTO Memberships in Africa: No of member nations: 42. Newest Entry: Seychelles (April, 2015) No of Observer nations: 5

No of Observer nations: 5") Vol. - 1, Issue: June 2015 India established its trade relations with the African countries as long back as in the 16th century. As emerging economies, India and Africa have a lot in common- rich natural

Vol. - 1, Issue: June 2015 India established its trade relations with the African countries as long back as in the 16th century. As emerging economies, India and Africa have a lot in common- rich natural

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS

EUROPEAN COMMISSION Brussels, XXX COM(2016) 49/2 COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS on

EUROPEAN COMMISSION Brussels, XXX COM(2016) 49/2 COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS on

Supply Scenarios TYNDP 2015

Supply Scenarios TYNDP 2015 Data basis René Döring Adviser System Development Brussels, 30 April 2014 Introduction Characteristic of an ENTSOG supply scenario Assumption on a possible gas supply potential

Supply Scenarios TYNDP 2015 Data basis René Döring Adviser System Development Brussels, 30 April 2014 Introduction Characteristic of an ENTSOG supply scenario Assumption on a possible gas supply potential

The Future of European Energy Security

The Future of European Energy Security Professor Øystein Noreng, BI Norwegian School of Management Energy and Climate Policy - Supply Security in International Comparison, 12th Annual Meeting of the Reform

The Future of European Energy Security Professor Øystein Noreng, BI Norwegian School of Management Energy and Climate Policy - Supply Security in International Comparison, 12th Annual Meeting of the Reform

Terasen Gas (Vancouver Island) Inc. Evidence In Response to VIEC CPCN Application for the VIGP

Inc. Evidence In Response to VIEC CPCN Application for the VIGP") Page 1 Section 1. Introduction 1.1 Terasen Gas (Vancouver Island) Inc (TGVI), formerly Centra Gas British Columbia, provides natural gas transmission and distribution services to more than 76,000 residential,

Page 1 Section 1. Introduction 1.1 Terasen Gas (Vancouver Island) Inc (TGVI), formerly Centra Gas British Columbia, provides natural gas transmission and distribution services to more than 76,000 residential,

ENERGY PRIORITIES FOR EUROPE

ENERGY PRIORITIES FOR EUROPE Presentation of J.M. Barroso, President of the European Commission, to the European Council of 4 February 2011 Contents 1 I. Why energy policy matters II. Why we need to act

ENERGY PRIORITIES FOR EUROPE Presentation of J.M. Barroso, President of the European Commission, to the European Council of 4 February 2011 Contents 1 I. Why energy policy matters II. Why we need to act

Among these I cover the following: - Fields development plan (FDP) - Conceptual studies for surface facilities

- Conceptual studies for surface facilities") SAID ALI CURRICULUM VITEA Cite du 20 Aout, Villa N 44 BOUMERDES 35000 ALGERIA Tel : 00 213 24 794 367 Mobile : 00 213 553 394 856 E-mail :saidali.al@hotmail.com Skills My activities refer to the oil and

SAID ALI CURRICULUM VITEA Cite du 20 Aout, Villa N 44 BOUMERDES 35000 ALGERIA Tel : 00 213 24 794 367 Mobile : 00 213 553 394 856 E-mail :saidali.al@hotmail.com Skills My activities refer to the oil and

Algeria Power Market Outlook to Business Propensity Indicator (BPI), Market Trends, Regulations and Competitive Landscape

, Market Trends, Regulations and Competitive Landscape") Algeria Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulations and Competitive Landscape Reference Code: GDPE0569ICR Publication Date: August 2012 Thermal Installed

Algeria Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulations and Competitive Landscape Reference Code: GDPE0569ICR Publication Date: August 2012 Thermal Installed

Emerging Legal and Policy Strategies for Climate Change Adaptation: Opportunities and Constraints for Action in Africa

Emerging Legal and Policy Strategies for Climate Change Adaptation: Opportunities and Constraints for Action in Africa By Dr. Emmanuel B Kasimbazi Associate Professor, School of Law, Makerere University,

Emerging Legal and Policy Strategies for Climate Change Adaptation: Opportunities and Constraints for Action in Africa By Dr. Emmanuel B Kasimbazi Associate Professor, School of Law, Makerere University,

Council conclusions on Energy 2020: A Strategy for competitive, sustainable and secure energy

COUNCIL OF THE EUROPEAN UNION Council conclusions on Energy 2020: A Strategy for competitive, sustainable and secure energy 3072th TRANSPORT, TELECOMMUNICATIONS and ERGY Council meeting Brussels, 28 February

COUNCIL OF THE EUROPEAN UNION Council conclusions on Energy 2020: A Strategy for competitive, sustainable and secure energy 3072th TRANSPORT, TELECOMMUNICATIONS and ERGY Council meeting Brussels, 28 February

LNG TRADE FLOWS. Hans Stinis Shell Upstream International

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

Synergies between UNFCCC and UNCCD in Africa: Experiences made in implementing the UNCCD

Synergies between UNFCCC and UNCCD in Africa: Experiences made in implementing the UNCCD Bettina Horstmann, Coordinator Africa Unit, UNCCD Secretariat. United Nations Convention to Combat Desertification

Synergies between UNFCCC and UNCCD in Africa: Experiences made in implementing the UNCCD Bettina Horstmann, Coordinator Africa Unit, UNCCD Secretariat. United Nations Convention to Combat Desertification

Asian Gas Summit 2013 December 3, Asia driving natural gas growth

IGU Asian Gas Summit 2013 December 3, 2013 Asia driving natural gas growth Jérôme Ferrier President IGU Allocated time: 30 minutes Dr. Manmohan Singh, Hon ble Prime Minister of India Shri S. Jaipal Reddy,

IGU Asian Gas Summit 2013 December 3, 2013 Asia driving natural gas growth Jérôme Ferrier President IGU Allocated time: 30 minutes Dr. Manmohan Singh, Hon ble Prime Minister of India Shri S. Jaipal Reddy,

Developments in gas pipelines and LNG infrastructure for closing EU-30 gas supply demand gap

ECN Seminar Prague, June 12th, 2003 Gas Supply Security in an Enlarged Europe Developments in gas pipelines and LNG infrastructure for closing EU-30 gas supply demand gap Presentation by: Patrick Cayrade

ECN Seminar Prague, June 12th, 2003 Gas Supply Security in an Enlarged Europe Developments in gas pipelines and LNG infrastructure for closing EU-30 gas supply demand gap Presentation by: Patrick Cayrade

LNG Opportunities. An Oil Search Perspective. PNG Chamber of Mines and Petroleum 28 November Oil Search Limited ARBN

LNG Opportunities An Oil Search Perspective PNG Chamber of Mines and Petroleum 28 November 2017 Oil Search Limited ARBN 055 079 868 Strong long-term global LNG market fundamentals ASIAN DEMAND (MTPA) 364

LNG Opportunities An Oil Search Perspective PNG Chamber of Mines and Petroleum 28 November 2017 Oil Search Limited ARBN 055 079 868 Strong long-term global LNG market fundamentals ASIAN DEMAND (MTPA) 364

Security of natural gas supply in Spain. Mariano Marzo Fac. Geology Univ. Barcelona

Security of natural gas supply in Spain Mariano Marzo Fac. Geology Univ. Barcelona 1 Spain s Primary Energy Mix 2007 HC = 84% 2 Natural Gas Consumption in EU27 in 2007 3 The Spanish gas market differs

Security of natural gas supply in Spain Mariano Marzo Fac. Geology Univ. Barcelona 1 Spain s Primary Energy Mix 2007 HC = 84% 2 Natural Gas Consumption in EU27 in 2007 3 The Spanish gas market differs