The VLGC Market. Prepared for the IMSF, ALBA, Athens, May Presented by Dr. Mariniki Psifia, Market Analyst. IMSF Forum (9 th 11 th May 2016)

|

|

|

- Meryl Gwen Randall

- 6 years ago

- Views:

Transcription

1 Latsco Shipping Limited The VLGC Market Prepared for the IMSF, ALBA, Athens, May 2016 Presented by Dr. Mariniki Psifia, Market Analyst Latsco Shipping Limited IMSF Forum (9 th 11 th May 2016)

2 Disclaimer This presentation (including any oral presentation) (the presentation ) is intended solely for the purposes of the IMS Forum 2016 and its participants. This presentation is confidential and must not be copied, reproduced, published, distributed, disclosed or passed to any other person at any time without the prior written consent of Dr. Mariniki Psifia. Without prejudice to the generality of the foregoing, this presentation may not be published, distributed or transmitted by any means or media, directly or indirectly, in whole or in part, in or into the United States. This presentation is for information purposes only. The information and opinions provided in this presentation are, unless otherwise stated herein, provided as of the date of this presentation and are subject to change. Certain statements are forwardlooking statements. The forward-looking statements include statements typically containing the words intends, expects, anticipates, targets, plans, estimates and words of similar import. These forward-looking statements speak only as at the date of this presentation or as otherwise specifically provided herein. The forward-looking statements are based on numerous assumptions and such assumptions may or may not prove to be correct. No one undertakes to update or revise such forward-looking statements. This presentation does not constitute legal, valuation, tax, or financial consulting advice, nor is it a statement on the performance, management capability or future potential (good or bad) of the company(ies), industry(ies), product(s), region(s) or country(ies) discussed. Those interested in specific guidance for shipping, legal, strategic, and/or financial or accounting matters should seek competent professional assistance from their own advisors. Any commentary, observation or discussion contained in this presentation about a country, industry or company does not constitute a recommendation to buy or sell company shares or make investment decisions. Although the statements in this presentation are derived from or based upon various and credible information sources and/or economic models that the author believes to be reliable, the author does not guarantee their accuracy, reliability, or quality, and any such information, or resulting analyses, may be incomplete, rounded, inaccurate or condensed. All estimates included in this presentation are subject to change without notice. This presentation is for informational purposes only and may or may not be intended as a recommendation to invest or an offer or solicitation with respect to the purchase or sale of a security, stock, limited partnership instrument, or financial vehicle. This presentation reflects the views of its author and not of any one else (including of any former or current employer).

3 LPG Shipping

4 Liquefied Petroleum Gas (LPG) is a global industry Sources Processing industries Transport User Natural Gas well Gas Plant Natural Gas Pipeline Power Generation LNG liquefaction Residential / LNG Commercial LPG Petrochemical gases Industrial Ammonia Auto Condensates (CPP) Oil well Refinery LPG Further refining Clean Products Chemicals Dirty Products Agricultural LPG consists of propane and butane, petroleum gases that originate either from crude oil and/or natural gas Despite being gaseous at ambient pressure and temperature, propane and butane both liquefy relatively easily under pressure, refrigeration or combination of the two LPG is a clean energy source compared to many other fossil fuels and it has numerous applications LPG is substitutable in many of its applications, and its pricing is influenced by its competition with other fuels or feedstocks Source: Various

5 The Baltic Liquefied Petroleum Index (BLPGI) through the years Source: The Baltic Exchange

6 The U.S. poised to become the top LPG exporter within a few years U.S. Exports of Propane and Propylene are expected to hit unprecedented levels by 2017 due to additional export projects to the fastest growing LPG exporter in the world over a 6 year time span!??? From the LPG sector s importer of last resort Source: U.S. E.I.A, 2016

7 The US confirmed its place as the world s leading exporter of LPG in 2015 with over 19.7 mio mt of exports a 40.1% y/y growth Data Source: GTIS, IHS

8 2015 What happened last year Data Source: Clarksons SIN, Platts LPGaswire, Factsset, GTIS, IHS

9 2016 Where are we this year?

10 Crude oil prices, Naphtha vs Propane

11 Correlations between WTI, Henry Hub Natural Gas and Propane Mont Belvieu WTI vs Henry Hub Natural Gas Propane Mont Belvieu vs WTI Propane Mont Belvieu vs Henry Hub Natural Gas Propane prices are highly correlated to Crude oil prices by

750,0 ($50) 700,0 650,0 600,0 550,0 500,0 450,0 400,0 350,0 300,0 250,0 200,0 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16")

12 The West East Arb is firmly closed FOB Propane Houston vs Arab Gulf The West- East Arb 000,0 950,0 $/mt FOB Houston FOB Arab Gulf $125 $100 $75 ARB OPEN ARB CLOSED 900,0 $50 850,0 800,0 $25 $0 ($25) 750,0 ($50) 700,0 650,0 600,0 550,0 500,0 450,0 400,0 350,0 300,0 250,0 200,0 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Data Source: FactSet, Platts ($75) ($100) ($125) Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Percentage of the Freight element to Japan CFR Price 70,0% Houston to Japan AG to Japan 60,0% 50,0% 40,0% 30,0% 20,0% 10,0% 0,0% Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Prepared Oct-15 by Dr. Jan-16 Mariniki Apr-16 PSIFIA, 2016

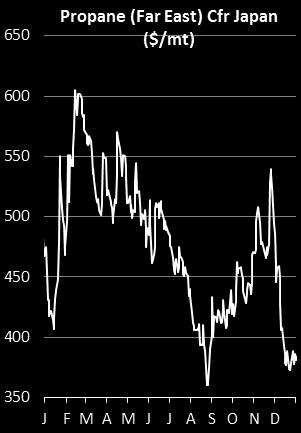

13 Weaker crude prices and ample supply pulled down the LPG prices in Asia Data Source: FactSet, Platts, GTIS

14 The VLGC Freight Market

Freight:")

15 Today, VLGC Net Time Charter rate are below $20,000/day (-79% y/y) Freight: AG-Chiba / Houston - Chiba VLGC Net Timecharter Rates Source: The Baltic Exchange

16 Oct-95 Oct-96 Oct-97 Oct-98 Oct-99 Oct-00 Oct-01 Oct-02 Oct-03 Oct-04 Oct-05 Oct-06 Oct-07 Oct-08 Oct-09 Oct-10 Oct-11 Oct-12 Oct-13 Oct-14 Oct-15 Oct-16 Oct-17 Oct-18 Jan-08 Aug-08 Mar-09 Oct-09 May-10 Dec-10 Jul-11 Feb-12 Sep-12 Apr-13 Nov-13 Jun-14 Jan-15 Aug-15 Mar-16 Oct-16 May-17 Dec-17 Jul-18 VLGC Timecharter Rates (TC) fell below long-term historical averages 1 Year VLGC TC Rates decreased by 63.2% since Jul ,000 cbm LPG TC Equivalent decreased by 84% since Jul ,000 per Month 2015-jul; $2 219, ,000 per Month 82/84K CBM LPG TCE 5 years average $4 038, Yr Time-Charter 5 years average 10 years average years average $1 257, $938, $1 646, $1 174, apr; $816, $704, des; $400, Source: Clarksons SIN

17 Dec-02 Apr-03 Massive cost savings for the owners because of the dramatic decline in bunker costs in 2015.do not apply anymore Aug-03 Dec-03 Apr-04 Aug-04 Dec-04 Apr-05 Aug-05 Dec-05 Apr-06 Aug-06 Dec-06 Apr-07 Aug-07 Dec-07 Apr-08 Aug-08 Dec-08 Apr-09 Aug-09 Dec-09 Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11 Apr-12 Aug-12 Dec-12 Apr-13 Aug-13 Dec-13 Apr-14 Aug-14 Dec-14 Apr-15 Aug-15 Dec-15 Apr ,0% Bunkers Cost to Gross TCE ~ Ratio 90,0% 80,0% 70,0% 60,0% 50,0% 40,0% 30,0% 20,0% 10,0% 0,0%

18 The LPG Trade during 2015 and 1Q-2016

19 World LPG Trade Development For 2016 LPG exports are expected to increase by 12% to 82 mio mt Major LPG Importers Major LPG Exporters Data Source: GTIS. ^forecasting as per various sources

20 In Q1-2016, propane and butane trade fell by 1.7% y-o-y to mio mt* Data Source: GTIS. * Preliminary data as per data collection on 4 th May 2016

absorbing the main increment of those cargoes Data Source: GTIS - IHS, May")

21 All of US 2015 LPG exports found homes with Asian countries (China, Japan, S. Korea) absorbing the main increment of those cargoes Data Source: GTIS - IHS, May 2016

22 US Terminal Export Capacity & VLGC liftings from Targa & Enterprise (2014 Feb 2016) Estimated North America LPG Export Volume Capacities US LPG Export Scenarios based on Terminal Capacity ,20 Mio MT 1,88 5,1 6,81 7,37 3,40 6,70 11,69 6,20 6,20 6,20 6,20 6,20 6,70 16,00 4, Mio Mt 2014: On average 18.2 liftings per month Est. total lifted quantity 9.64 mio mt KinderMorgan Sage Phillips 66 Oxy Sunoco DCP Petredec/Martin Gas Trafigura Sunoco/MarkWest PetroGas Targa Enterprise 26,16 19,69 VLGC Estimated Liftings from Targa and Enterprise, TX (mio mt) Terminal Capacity Terminal utilization 75.3% 37,14 26,00 27,95 29,71 Exports 70.0% 75.3% 80.0% 2015 Terminal Capacity : On average 18.6 liftings per month Est. total lifted quantity 9.8 mio mt 2016 Export Scenarios (% of Terminal Capacity) 1,00 0,80 0,60 0,40 0,20 - J-14 F-14 M-14 A-14 M-14 J-14 J-14 A-14 S-14 O-14 N-14 D-14 J-15 F-15 M-15 A-15 M-15 J-15 J-15 A-15 S-15 O-15 N-15 D-15 J-16 F-16 Data Source: GTIS / IHS. Lifting data are from AIS

23 Middle East LPG Exports during 2015 and 1Q-2016 Split between Long-Haul and Short-Haul Importers 100 % Long-Haul Short-Haul 90 % 80 % 70 % 60 % 22% 24% 30% 35% 40% 44% 49% 63% 69% 60% 50 % AG to China: +15.6% y/y 40 % 30 % 20 % 10 % 70% 65% 60% 56% 51% 37% 31% 40% 3,50 3,00 2,50 2,00 1,50 1,00 0,50 0,00 Who has exported the most during Q & Q Mio mt [Q1-2015] [Q1-2016] 1,18 0,02 0,01 3,23 2,71 2,43 1,95 1,39 0,95 0,73 0,77 0,86 Bahrain Iran Kuwait Qatar Saudi Arabia UAE 0 % M-2016 Middle East LPG Exports y/y comparison in mio mt* y-o-y 3M M-2016 y-o-y China % % India % % Japan % % Indonesia % % Korea, South % % Thailand % % Other % % Total* % % Data Source: GTIS. * Preliminary data as per data collection on 4 th May 2016

24 (f) 2017 (f) 2018 (f) 2019 (f) 2020 (f) 0,71 1,58 0,71 2,52 2,89 2,31 3,74 2,81 3,74 Iran LPG Exports following the removal of International Sanctions and South Pars 24- phase development plans 10 mio MT Iran LPG Historical and Future Estimated Exports Other Middle East Asia & Oceania Africa The South Pars fields Natural gas production from South Pars is critical to meet increasing domestic consumption and Iran s current & future export obligations The South Pars Development Plans ,23 0,52 0,40 0,63 Data Source: GTIS and Information from 10 th LPG Trade Summit, Istanbul 2015, FGE. Prepared by Dr. Mariniki Psifia

25 During Q1-2016, China s seaborne LPG imports totalled 4.4 mio mt, up by 47.8% y-o-y 18,0 Mio mt UAE Iran Kuwait USA Saudi Arabia Other 16,0 14,0 North America 36,16% Africa 8,66% Asia & Oceania 3,04% Eurasia 0,05% Europe 1,98% 2,49 12,0 10,0 Middle East 50,11% 3,57 8,0 6,0 1,78 2,56 0,77 3,58 4,0 2,0 0,0 1,01 1,48 1,47 1,21 1,06 0,99 5,04 1,19 0,73 0,59 3,69 0,68 1,14 0,44 1,21 0,77 0,38 0,60 0,54 0,60 0,41 0,63 0,82 1,09 1, ^ Data: GTIS / HIS. 2016^: 3M-2016

26 India LPG Imports keep increasing Yearly Indian LPG Imports Monthly Indian LPG Imports 9 8 Mio mt Qatar Saudi Arabia Bahrain Other United Arab Emirates Kuwait Iran 0,75 0,9 0,8 0,7 Mio mt [Imp 2014] [Imp 2015] 7 0,86 0,6 6 1,55 2,22 0,5 0,4 5 0,78 0,99 1,61 1,60 4 0,63 1,42 1,30 3 1,76 1,11 1,22 0,45 2 0,23 0,30 0,27 3,67 3,42 1,06 1,25 1,44 1,26 1,60 1 2,11 1,71 0,41 0,26 0,38 0, Data Source: GTIS/IHS 0,3 100 % 90 % 80 % 70 % 60 % 50 % 40 % 30 % 20 % 10 % 0 % Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Propane and Butane split Butane Propane J-15 F-15 M-15 A-15 M-15 J-15 J-15 A-15 S-15 O-15 N-15 D-15

27 The VLGC Fleet

28 J - 16 F - 16 M - 16 A - 16 M - 16 J - 16 J - 16 A - 16 S - 16 O - 16 N - 16 D LPG Fundamentals: Supply VLGC units currently number 220 ships of a total 17.38m cu.m, The y-o-y VLGC growth is today equal to 29.4% in number of vessels and it is expected to exceed the 34.17% by June The orderbook is quite heavy for the specific sector with 29.2% of the fleet in cu.m terms currently on order (65 vessels). Since the beginning of 2016, 22 VLGC of a total 1.84 mio cu.m were delivered and 3 new VLGC orders were placed to the shipyards # of vessels VLGC Supply Growth* in number of vessels y-o-y growth 28% VLGC 2016; 23,7% 3 Estimated Deliveries 25% 11 y-o-y growth 24 23% 2015; 21,5% 20% 25 18% 12 Deliveries and Orderbook in number of vessels VLGC LGC MGC HGC 80 VLGC LGC MGC HGC % % 10% M A I % 5% 3% 0% -3% Source: Clarksons. * Slippage and Cancellations are not included

Orderbook - to - Fleet Ratio (in number of vessels) 65 VLGC 2 LGC 38 MGC 98 HGC 33 HGC Data: Clarksons")

29 LPG Fleet Size Ranges, Cargo Capability & Tank Type The fleet (in number of vessels) Orderbook (in number of vessels) Orderbook - to - Fleet Ratio (in number of vessels) 65 VLGC 2 LGC 38 MGC 98 HGC 33 HGC Data: Clarksons SIN

30 Currently the VLGC fleet stands at 220 vessels of mio cu.m ,0 18,0 16,0 14,0 12,0 # of vessels vessels are older than 20 years old VLGC average age is 9.4 years old to 4 5 to 9 10 to to to to In just 10 years, the average VLGC age fell by 47.7% to less than 9.4 years old Average Age 18,0 15,7 14,9 14,3 14,1 13,9 13,0 12, VLGC 61,000 cu.m. The Fleet 220 VLGC Fleet Profile in million cu.m. The Orderbook LPG in number of vessels Fleet As of Start Deliveries Demolitions - - Fleet As of today NET FLEET CHANGE Orderbook [ ] Orderbook to Fleet 29.2% 29.5% Ethane Capable 5 10,0 10,4 9,40 8, Mar-16 Data: Clarksons SIN VLGC VLGC

31 VLGC Fleet Per Year of Built & Orderbook 50 NUMBER OF VESSELS VLGC Fleet [Contract Year 2014] [Contract Year 2015] [Contract Year 2016] YEAR OF BUILT Source: Clarksons SIN

Shanghai")

32 The VLGC Orderbook per Yard The Orderbook per Yard (in number of vessels) Scheduled Deliveries per Year (in number of vessels) Shanghai Waigaoqiao; 2; DSIC Offshore; 5; 3,6% 9,1% Shanghai Waigaoqiao MHI Nagasaki MHI Nagasaki; 8; 14,5% Kawasaki HI Sakaide 1 3 Jiangsu New YZJ 2 Jiangnan SY Group 2 Kawasaki HI Sakaide; 4.2% Hyundai; 27; 49,1% DSIC Offshore Hyundai Jiangnan Changxing; 12.5% Jiangnan SY Group; 4; 7,3% Daewoo (DSME) Source: Clarksons SIN

$/Day $140 000 82K CBM LPG TCE Rates VLGC Growth* Y-o-Y Growth 35,0% $130 000 apr.")

33 des.11 feb.12 apr.12 jun.12 aug.12 okt.12 des.12 feb.13 apr.13 jun.13 aug.13 okt.13 des.13 feb.14 apr.14 jun.14 aug.14 okt.14 des.14 feb.15 apr.15 jun.15 aug.15 okt.15 des.15 feb.16 apr.16 VLGC y-o-y fleet growth and timecharter equivalent rates (TCE) $/Day $ K CBM LPG TCE Rates VLGC Growth* Y-o-Y Growth 35,0% $ apr.16; 30,51% $ ,0% $ $ ,0% $ $ ,0% $ $ ,0% $ $ ,0% $ $ ,0% $ $0 0,0% Historical Data: Clarksons SIN. * VLGC Growth in cu.m

34 As per current shipyard delivery schedule, it is estimated that the VLGC fleet y-o-y growth will peak in June 2016 Source: Historical Data Clarksons SIN

35 Thank you!

I.M. Skaugen SE AGM 2015 Presentation April 28th 2015

I.M. Skaugen SE AGM 2015 Presentation April 28th 2015 1 Agenda Highlights Core business 2 Restructuring efforts continued with positive effects USDm Leading to reduced financial expenses and a lower cost

I.M. Skaugen SE AGM 2015 Presentation April 28th 2015 1 Agenda Highlights Core business 2 Restructuring efforts continued with positive effects USDm Leading to reduced financial expenses and a lower cost

Cass Business School Presentation 29 January London

Cass Business School Presentation 29 January 2018 - London Connecting high quality analytics with commercial decision making Commercial Advice Consulting Market Insights Multiclient Products Retainer Agreements

Cass Business School Presentation 29 January 2018 - London Connecting high quality analytics with commercial decision making Commercial Advice Consulting Market Insights Multiclient Products Retainer Agreements

Finding Global End Use Markets for the Growing LPG Supply

Finding Global End Use Markets for the Growing LPG Supply March 7, 2017 Dr. Walt Hart, Vice President, IHS Natural Gas Liquids Walt.Hart@ihsmarkit.com 2 Finding Global End Use Markets for the Growing LPG

Finding Global End Use Markets for the Growing LPG Supply March 7, 2017 Dr. Walt Hart, Vice President, IHS Natural Gas Liquids Walt.Hart@ihsmarkit.com 2 Finding Global End Use Markets for the Growing LPG

Outlook Overview. LPG Imports. LPG Exports. Fleet supply. Ton-mile. Freight rates

Outlook Overview LPG Exports LPG Imports Fleet supply Ton-mile Freight rates Exports via VLGC from North America is estimated to continue growing. Middle East growth rate slows down due to Iranian sanctions

Outlook Overview LPG Exports LPG Imports Fleet supply Ton-mile Freight rates Exports via VLGC from North America is estimated to continue growing. Middle East growth rate slows down due to Iranian sanctions

Shipping Market Outlook

Shipping Market Outlook Hamburg, 19 November 15 Slide 1 Market Environment Structural Trends of Global Dry Market North America Lower energy prices and higher consumer confidence will bode well for container

Shipping Market Outlook Hamburg, 19 November 15 Slide 1 Market Environment Structural Trends of Global Dry Market North America Lower energy prices and higher consumer confidence will bode well for container

LPG PRICES IN AN INCREASINGLY VOLATILE MARKET

Information Analytics Expertise JUNE 214 LPG PRICES IN AN INCREASINGLY VOLATILE MARKET 18 th Annual Asia LPG Seminar Ronald L. Gist, Director +1 832 29 4426 Ron.Gist@ihs.com 214 IHS / ALL RIGHTS RESERVED

Information Analytics Expertise JUNE 214 LPG PRICES IN AN INCREASINGLY VOLATILE MARKET 18 th Annual Asia LPG Seminar Ronald L. Gist, Director +1 832 29 4426 Ron.Gist@ihs.com 214 IHS / ALL RIGHTS RESERVED

IHS LATIN AMERICA LPG SEMINAR

ENTERPRISE PRODUCTS PARTNERS L.P. IHS LATIN AMERICA LPG SEMINAR November 8, 2016 Joseph Fasullo Manager, International NGLs ALL RIGHTS RESERVED. ENTERPRISE PRODUCTS PARTNERS L.P. enterpriseproducts.com

ENTERPRISE PRODUCTS PARTNERS L.P. IHS LATIN AMERICA LPG SEMINAR November 8, 2016 Joseph Fasullo Manager, International NGLs ALL RIGHTS RESERVED. ENTERPRISE PRODUCTS PARTNERS L.P. enterpriseproducts.com

LNG Facts A Primer. Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums. March 10, Kristi A. R.

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

LNG Shipping: How Long Will The Good Times Last?

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

Export Demand for Propane and Butane Platts 7 th Annual NGLs Conference

Export Demand for Propane and Butane Platts 7 th Annual NGLs Conference October 31, 2017 Forward - Looking Information This presentation contains forward-looking statements and forward-looking information

Export Demand for Propane and Butane Platts 7 th Annual NGLs Conference October 31, 2017 Forward - Looking Information This presentation contains forward-looking statements and forward-looking information

Q /11/17. Jon Skule Storheill. Øyvind Ryssdal

Q3 2017 Jon Skule Storheill Øyvind Ryssdal 17/11/17 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

Q3 2017 Jon Skule Storheill Øyvind Ryssdal 17/11/17 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

LPG Shipping Outlook

banchero costa LPG Shipping Outlook (an analysis of the fleet profile, trade prospects, and rates) September 2018 bancosta blue studies volume WET 2018/#17 banchero costa research www.bancosta.com ; research@bancosta.com

banchero costa LPG Shipping Outlook (an analysis of the fleet profile, trade prospects, and rates) September 2018 bancosta blue studies volume WET 2018/#17 banchero costa research www.bancosta.com ; research@bancosta.com

Pareto. Conference Jon Skule Storheill 13/

Pareto Conference 2017 Jon Skule Storheill 13/09 2017 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

Pareto Conference 2017 Jon Skule Storheill 13/09 2017 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

Energy and commodity price benchmarking and market insights

Energy and commodity price benchmarking and market insights London, Houston, Washington, New York, Portland, Calgary, Santiago, Bogota, Rio de Janeiro, Singapore, Beijing, Tokyo, Sydney, Dubai, Moscow,

Energy and commodity price benchmarking and market insights London, Houston, Washington, New York, Portland, Calgary, Santiago, Bogota, Rio de Janeiro, Singapore, Beijing, Tokyo, Sydney, Dubai, Moscow,

The Outlook for the Global LPG Market

The Outlook for the Global LPG Market International LP Gas Seminar 213 Ken Otto February 28, 212 Dai-Ichi Hotel Tokyo, Japan 212, IHS Inc. No portion of this presentation may be reproduced, reused, or

The Outlook for the Global LPG Market International LP Gas Seminar 213 Ken Otto February 28, 212 Dai-Ichi Hotel Tokyo, Japan 212, IHS Inc. No portion of this presentation may be reproduced, reused, or

Energy in 2011 disruption and continuity

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Richard de Caux, Refining Analyst, Group Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Richard de Caux, Refining Analyst, Group Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding

TANKER MARKET INSIGHT

TANKER MARKET INSIGHT October 18 Research Department, Teekay Tankers Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jul-18 Aug-18 Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jul-18 Aug-18 $ 000s

TANKER MARKET INSIGHT October 18 Research Department, Teekay Tankers Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jul-18 Aug-18 Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jul-18 Aug-18 $ 000s

The Role of GCC s Natural Gas in the World s Gas Markets

World Review of Business Research Vol. 1. No. 2. May 2011 Pp. 168-178 The Role of GCC s Natural Gas in the World s Gas Markets Abdulkarim Ali Dahan* The objective of this research is to analyze the growth

World Review of Business Research Vol. 1. No. 2. May 2011 Pp. 168-178 The Role of GCC s Natural Gas in the World s Gas Markets Abdulkarim Ali Dahan* The objective of this research is to analyze the growth

3-1. Effect of Crude Oil Price Drop on the Global Energy Market

APERC Workshop at EWG52 Moscow, Russia, 18 October, 2016 3-1. Effect of Crude Oil Price Drop on the Global Energy Market James Kendell Vice President, APERC Background and outline of the study Background

APERC Workshop at EWG52 Moscow, Russia, 18 October, 2016 3-1. Effect of Crude Oil Price Drop on the Global Energy Market James Kendell Vice President, APERC Background and outline of the study Background

Al Garcia Business Manager-Americas C4U Trade USA, Inc.

Revealing Global Trade Flows For Propane And Implications For Supply- Future export markets for North American propane and what this means for PDH feedstock security Al Garcia Business Manager-Americas

Revealing Global Trade Flows For Propane And Implications For Supply- Future export markets for North American propane and what this means for PDH feedstock security Al Garcia Business Manager-Americas

Effect of Crude Oil Price Drop on the Global Energy

2016/EWG52/WKSP1/003 Effect of Crude Oil Price Drop on the Global Energy Submitted by: APERC Asia Pacific Energy Research Centre Workshop Moscow, Russia 18 October 2016 APERC Workshop at EWG52 Moscow,

2016/EWG52/WKSP1/003 Effect of Crude Oil Price Drop on the Global Energy Submitted by: APERC Asia Pacific Energy Research Centre Workshop Moscow, Russia 18 October 2016 APERC Workshop at EWG52 Moscow,

4 TH GAS FORUM. Jean Jaylet, Senior Vice President Strategy, Markets & LNG. May 30 th, 2016

4 TH GAS FORUM Jean Jaylet, Senior Vice President Strategy, Markets & LNG May 30 th, 2016 THE LNG MARKET TODAY 2005: 143 MT 13 exporters 15 importers ~60 flows 2015: 250 MT 19 exporters 34 importers ~160

4 TH GAS FORUM Jean Jaylet, Senior Vice President Strategy, Markets & LNG May 30 th, 2016 THE LNG MARKET TODAY 2005: 143 MT 13 exporters 15 importers ~60 flows 2015: 250 MT 19 exporters 34 importers ~160

Lunch Session. Oil and Gas Security. Aad van Bohemen, IEA/Energy Policy and Security Division 6 March 2018 (APEC-OGSNF) IEA OECD/IEA 2017

IEA OECD/IEA 2017") Lunch Session Oil and Gas Security Aad van Bohemen, IEA/Energy Policy and Security Division 6 March 2018 (APEC-OGSNF) IEA Long-term Energy Markets Outlook Key takeaways from WEO 2017 India takes the lead,

Lunch Session Oil and Gas Security Aad van Bohemen, IEA/Energy Policy and Security Division 6 March 2018 (APEC-OGSNF) IEA Long-term Energy Markets Outlook Key takeaways from WEO 2017 India takes the lead,

Energy in 2011 disruption and continuity

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Paul Appleby, Head of Energy Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding remarks Energy

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Paul Appleby, Head of Energy Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding remarks Energy

An overview of the global LPG market and its impact in Latin America

An overview of the global LPG market and its impact in Latin America Rio de Janeiro, 33 rd AIGLP Conference Vanessa Viola SVP Latin America, Argus March 218 London Houston Moscow Singapore Dubai New York

An overview of the global LPG market and its impact in Latin America Rio de Janeiro, 33 rd AIGLP Conference Vanessa Viola SVP Latin America, Argus March 218 London Houston Moscow Singapore Dubai New York

Argus European LPG Markets LPG Shipping - Current Challenges and Future Opportunities

Argus European LPG Markets 2013. LPG Shipping - Current Challenges and Future Opportunities A presentation prepared by ViaMar AS, Oslo All information provided by ViaMar AS, whether oral or written, is

Argus European LPG Markets 2013. LPG Shipping - Current Challenges and Future Opportunities A presentation prepared by ViaMar AS, Oslo All information provided by ViaMar AS, whether oral or written, is

Q /08/18. Jon Skule Storheill. Øyvind Ryssdal

Q2 2018 Jon Skule Storheill Øyvind Ryssdal 30/08/18-1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and projections regarding

Q2 2018 Jon Skule Storheill Øyvind Ryssdal 30/08/18-1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and projections regarding

Oil and natural gas: market outlook and drivers

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Capesize market outlook

Capesize market outlook China Iron Ore 2016, Metal Bulletin, Beijing Cheng Shan LI, dry bulk analyst 3 March 2016 Disclaimer The material and the information (including, without limitation, any future

Capesize market outlook China Iron Ore 2016, Metal Bulletin, Beijing Cheng Shan LI, dry bulk analyst 3 March 2016 Disclaimer The material and the information (including, without limitation, any future

Q /11/16. Jon Skule Storheill. Snorre Krogstad

Q3 2016 Jon Skule Storheill Snorre Krogstad 18/11/16 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

Q3 2016 Jon Skule Storheill Snorre Krogstad 18/11/16 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

Energy in Perspective

Energy in Perspective BP Statistical Review of World Energy 27 Christof Rühl Deputy Chief Economist London, 12 June 27 Outline Introduction What has changed? The medium term What is new? 26 in review Conclusion

Energy in Perspective BP Statistical Review of World Energy 27 Christof Rühl Deputy Chief Economist London, 12 June 27 Outline Introduction What has changed? The medium term What is new? 26 in review Conclusion

TANKER MARKET INSIGHT

TANKER MARKET INSIGHT July 18 Research Department, Teekay Tankers Jun-17 Jul-17 Aug-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jun-17 Jul-17 Aug-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 $ 000s /

TANKER MARKET INSIGHT July 18 Research Department, Teekay Tankers Jun-17 Jul-17 Aug-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jun-17 Jul-17 Aug-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 $ 000s /

OIL PRICES Developments and Effects. Mag. Johannes Benigni, January 2001 PVM Oil Associates - Vienna Strategic Energy Services

OIL PRICES Developments and Effects Mag. Johannes Benigni, January 2001 PVM Oil Associates - Vienna Strategic Energy Services PRICE MOVERS Gasoil 0.2 FOB Barges [USD/mt mt] 350 320 290 Rigid Emission Controls

OIL PRICES Developments and Effects Mag. Johannes Benigni, January 2001 PVM Oil Associates - Vienna Strategic Energy Services PRICE MOVERS Gasoil 0.2 FOB Barges [USD/mt mt] 350 320 290 Rigid Emission Controls

Short-Term and Long-Term Outlook for Energy Markets

Short-Term and Long-Term Outlook for Energy Markets Guy Caruso Administrator, Energy Information Administration guy.caruso@eia.doe.gov Fueling the Future: Energy Policy in New England December 2, 25 Boston,

Short-Term and Long-Term Outlook for Energy Markets Guy Caruso Administrator, Energy Information Administration guy.caruso@eia.doe.gov Fueling the Future: Energy Policy in New England December 2, 25 Boston,

I.M. Skaugen SE Result 2014 Presentation February 2015

I.M. Skaugen SE Result 2014 Presentation February 2015 1 Agenda Highlights Core business Financials 2 Restructuring efforts continued with positive effects USDm Leading to reduced financial expenses and

I.M. Skaugen SE Result 2014 Presentation February 2015 1 Agenda Highlights Core business Financials 2 Restructuring efforts continued with positive effects USDm Leading to reduced financial expenses and

Industrial Prices a cyclical rebound, a muted recovery, or no recovery at all?

Pricing & Purchasing Summit Industrial Prices a cyclical rebound, a muted recovery, or no recovery at all? 26 September 2016 ihsmarkit.com John Mothersole, Director, +1 202 481 9227, john.mothersole@ihsmarkit.com

Pricing & Purchasing Summit Industrial Prices a cyclical rebound, a muted recovery, or no recovery at all? 26 September 2016 ihsmarkit.com John Mothersole, Director, +1 202 481 9227, john.mothersole@ihsmarkit.com

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

Fundamental Prospecting - time for another gold rush?

Fundamental Prospecting - time for another gold rush? Dr Adam Kent - Maritime Strategies International (MSI) 30th Annual Marine Money Money Week New York City June 19 th to 21 st 2017 Agenda Fundamental

Fundamental Prospecting - time for another gold rush? Dr Adam Kent - Maritime Strategies International (MSI) 30th Annual Marine Money Money Week New York City June 19 th to 21 st 2017 Agenda Fundamental

Fundamental Prospecting - time for another gold rush?

Fundamental Prospecting - time for another gold rush? Dr Adam Kent - Maritime Strategies International (MSI) 30th Annual Marine Money Money Week New York City June 19 th to 21 st 2017 Agenda Fundamental

Fundamental Prospecting - time for another gold rush? Dr Adam Kent - Maritime Strategies International (MSI) 30th Annual Marine Money Money Week New York City June 19 th to 21 st 2017 Agenda Fundamental

Mont Belvieu NGL Infrastructure

Mont Belvieu NGL Infrastructure September 24, 2012 www.enterpriseproducts.com All rights reserved. Enterprise Products Partners L.P. Mike Smith Senior Vice President Forward Looking Statements This presentation

Mont Belvieu NGL Infrastructure September 24, 2012 www.enterpriseproducts.com All rights reserved. Enterprise Products Partners L.P. Mike Smith Senior Vice President Forward Looking Statements This presentation

LNG SECTOR REPORT The recovery is happening

EQUITY RESEARCH 8 September 216 Research report prepared by DNB Markets, a division of DNB Bank ASA LNG SECTOR REPORT The recovery is happening We have only made marginal adjustments to our LNG outlook,

EQUITY RESEARCH 8 September 216 Research report prepared by DNB Markets, a division of DNB Bank ASA LNG SECTOR REPORT The recovery is happening We have only made marginal adjustments to our LNG outlook,

$40 Billion Ichthys LNG Project Begins Gas Exports US' Range Resources to fill Rover gas pipeline volumes by yearend; processing ramps up

Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: O C T O B E R 2 5, 2 1 8 3.26 3.24 3.22 3.2 3.18 3.16 3.14 3.12 3.1

Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: O C T O B E R 2 5, 2 1 8 3.26 3.24 3.22 3.2 3.18 3.16 3.14 3.12 3.1

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION APRIL 2018 RIYADH, SAUDI ARABIA APRIL 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECAST ON

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION APRIL 2018 RIYADH, SAUDI ARABIA APRIL 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECAST ON

LSU Natural Gas Conference

LSU Natural Gas Conference Presented by: Bob Purgason VP Gulfcoast Region Williams Companies Introduction Structural shift in natural gas pricing The crude to gas ratio: A critical relationship for NGL

LSU Natural Gas Conference Presented by: Bob Purgason VP Gulfcoast Region Williams Companies Introduction Structural shift in natural gas pricing The crude to gas ratio: A critical relationship for NGL

Role of PDH in Asian Propylene Supply Market

Role of PDH in Asian Propylene Supply Market Chul-Jin (CJ) Kim CEO April 19, 2017 Agenda 1. SK Introduction 2. Asian Propylene Market 3. PDH as on-purpose process 4. Our Values to Customers 5. Key takeaways

Role of PDH in Asian Propylene Supply Market Chul-Jin (CJ) Kim CEO April 19, 2017 Agenda 1. SK Introduction 2. Asian Propylene Market 3. PDH as on-purpose process 4. Our Values to Customers 5. Key takeaways

Gastech LPG & Petrochemical Shipping: Current Status & Outlook. A better market, but for how long?

Gastech 25 LPG & Petrochemical Shipping: Current Status & Outlook A better market, but for how long? Nicola Williams Gas & Chemicals Division Clarksons Gastech 25 Overview of the LPG Carrier Fleet It is

Gastech 25 LPG & Petrochemical Shipping: Current Status & Outlook A better market, but for how long? Nicola Williams Gas & Chemicals Division Clarksons Gastech 25 Overview of the LPG Carrier Fleet It is

U.S. Natural Gas Market Dynamics

U.S. Natural Gas Market Dynamics University of Houston Global Energy Management Institute The Future of the Gulf Coast Petrochemical Industry Michael Speltz April 29, 2005 ChevronTexaco 2002 Legal Disclaimer

U.S. Natural Gas Market Dynamics University of Houston Global Energy Management Institute The Future of the Gulf Coast Petrochemical Industry Michael Speltz April 29, 2005 ChevronTexaco 2002 Legal Disclaimer

3 rd Quarter 2013 Results November 22th, 2013

3 rd Quarter 2013 Results November 22th, 2013 Disclaimer Forward-Looking Statements This presentation contains forward-looking statements within the meaning of applicable federal securities laws. Such

3 rd Quarter 2013 Results November 22th, 2013 Disclaimer Forward-Looking Statements This presentation contains forward-looking statements within the meaning of applicable federal securities laws. Such

MENA Energy Trends. June Edward Bell Commodities Analyst Emirates NBD Research

MENA Energy Trends Edward Bell Commodities Analyst Emirates NBD Research June 216 www.emiratesnbdresearch.com 1 (Proved reserves, trn cu metres) (Proved reserves, trn cu metres) (Proved reserves, m bbl)

MENA Energy Trends Edward Bell Commodities Analyst Emirates NBD Research June 216 www.emiratesnbdresearch.com 1 (Proved reserves, trn cu metres) (Proved reserves, trn cu metres) (Proved reserves, m bbl)

DORIAN LPG September 2017

DORIAN LPG September 2017 Disclaimer Forward-Looking Statements This presentation contains certain forward-looking statements including analyses and other information based on forecasts of future results

DORIAN LPG September 2017 Disclaimer Forward-Looking Statements This presentation contains certain forward-looking statements including analyses and other information based on forecasts of future results

Key Challenges for the Development of LNG

17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) Key Challenges for the Development of LNG in

17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) Key Challenges for the Development of LNG in

Q /05/17. Jon Skule Storheill. Snorre Krogstad

Q1 2017 Jon Skule Storheill Snorre Krogstad 05/05/17 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

Q1 2017 Jon Skule Storheill Snorre Krogstad 05/05/17 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

Energy Outlook. Kurt Barrow Vice President, Oil Markets, Midstream and Downstream Insights, IHS Markit

Energy Outlook Kurt Barrow Vice President, Oil Markets, Midstream and Downstream Insights, IHS Markit kurt.barrow@ihsmarkit.com Building a Foundation for Profitable Growth in Uncertain Markets Agenda Short-term

Energy Outlook Kurt Barrow Vice President, Oil Markets, Midstream and Downstream Insights, IHS Markit kurt.barrow@ihsmarkit.com Building a Foundation for Profitable Growth in Uncertain Markets Agenda Short-term

NASEO WINTER ENERGY OUTLOOK

ENTERPRISE PRODUCTS PARTNERS L.P. NASEO WINTER ENERGY OUTLOOK October, 2014 Mike Smith Group Sr. Vice President ALL RIGHTS RESERVED. ENTERPRISE PRODUCTS PARTNERS L.P. enterpriseproducts.com DISCLAIMER

ENTERPRISE PRODUCTS PARTNERS L.P. NASEO WINTER ENERGY OUTLOOK October, 2014 Mike Smith Group Sr. Vice President ALL RIGHTS RESERVED. ENTERPRISE PRODUCTS PARTNERS L.P. enterpriseproducts.com DISCLAIMER

Tanker Market Insight November Research Department, Strategic Development

Tanker Market Insight November 17 Research Department, Strategic Development Nov-16 Dec-16 Feb-17 Mar-17 May-17 Jun-17 Aug-17 Sep-17 Nov-16 Dec-16 Feb-17 Mar-17 May-17 Jun-17 Aug-17 Sep-17 $ 000s / day

Tanker Market Insight November 17 Research Department, Strategic Development Nov-16 Dec-16 Feb-17 Mar-17 May-17 Jun-17 Aug-17 Sep-17 Nov-16 Dec-16 Feb-17 Mar-17 May-17 Jun-17 Aug-17 Sep-17 $ 000s / day

Freight: A key determinant to future exports?

MetalBulletin Asian Bauxite and Alumina 2014 Freight: A key determinant to future exports? Ralph Leszczynski 29-30 October 2014, Singapore group www.bancosta.com ; research@bancosta.com usd/day Baltic

MetalBulletin Asian Bauxite and Alumina 2014 Freight: A key determinant to future exports? Ralph Leszczynski 29-30 October 2014, Singapore group www.bancosta.com ; research@bancosta.com usd/day Baltic

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. Factors Affecting Global Coal-Gas Competition NGI Workshop - Global Competition Between Coal and Natural Gas October 15th 218 Najla Jamoussi Director, Market Fundamentals & Corporate

CHENIERE ENERGY, INC. Factors Affecting Global Coal-Gas Competition NGI Workshop - Global Competition Between Coal and Natural Gas October 15th 218 Najla Jamoussi Director, Market Fundamentals & Corporate

DEMOLITION MONTHLY MARKET REPORT

ISSUE NO. 6/ JUNE LITION MONTHLY MARKET REPORT LITION ACTIVITY PER VESSEL TYPE LITION ACTIVITY PER UPDATE LITION ACTIVITY PRICES PER MAIN LITION COUNTRIES GOLDEN DESTINY LITION MONTHLY REPORT/ LITION ACTIVITY

ISSUE NO. 6/ JUNE LITION MONTHLY MARKET REPORT LITION ACTIVITY PER VESSEL TYPE LITION ACTIVITY PER UPDATE LITION ACTIVITY PRICES PER MAIN LITION COUNTRIES GOLDEN DESTINY LITION MONTHLY REPORT/ LITION ACTIVITY

Feedstock Challenges and Market Implications for Middle East Petrochemical Producers

Feedstock Challenges and Market Implications for Middle East Petrochemical Producers Agenda 1. Current MENA gas situation 2. Country examples (Saudi Arabia, Kuwait, UAE) 3. Implications for petrochemicals

Feedstock Challenges and Market Implications for Middle East Petrochemical Producers Agenda 1. Current MENA gas situation 2. Country examples (Saudi Arabia, Kuwait, UAE) 3. Implications for petrochemicals

Impact of American Unconventional Oil and Gas Revolution

National University of Singapore Energy Studies Institute 18 May 215 Impact of American Unconventional Oil and Gas Revolution Edward C. Chow Senior Fellow Revenge of the Oil Price Cycle American Innovation:

National University of Singapore Energy Studies Institute 18 May 215 Impact of American Unconventional Oil and Gas Revolution Edward C. Chow Senior Fellow Revenge of the Oil Price Cycle American Innovation:

2016 Propane Market Outlook: Driving Change in Consumer Propane Markets

0 2016 Propane Market Outlook: Driving Change in Consumer Propane Markets NPGA Southeastern Convention & International Propane Expo April 8, 2016 Presented by: Michael Sloan ICF International 9300 Lee

0 2016 Propane Market Outlook: Driving Change in Consumer Propane Markets NPGA Southeastern Convention & International Propane Expo April 8, 2016 Presented by: Michael Sloan ICF International 9300 Lee

The Great Eastern Shipping Co. Ltd. Business & Financial Review August 2015

The Great Eastern Shipping Co. Ltd. Business & Financial Review August 2015 1 Forward Looking Statements Except for historical information, the statements made in this presentation constitute forward looking

The Great Eastern Shipping Co. Ltd. Business & Financial Review August 2015 1 Forward Looking Statements Except for historical information, the statements made in this presentation constitute forward looking

Global LNG Market dynamics, key trends and market outlook

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

The World First Ever Very Large Ethane Carrier (VLEC)

") The World First Ever Very Large Ethane Carrier (VLEC) Gastech 2017, Tokyo 4 th April 2017 This document contains information resulting from testing, experience and know-how of GTT, which are protected

The World First Ever Very Large Ethane Carrier (VLEC) Gastech 2017, Tokyo 4 th April 2017 This document contains information resulting from testing, experience and know-how of GTT, which are protected

Quarterly Oil Market Update. Supply factors weigh heavily on oil

($ per barrel) Quarterly Oil Market Update Supply factors weigh heavily on oil Summary Brent oil prices are trading above $80 per barrel (pb), the highest level since early November 20, on the back of

($ per barrel) Quarterly Oil Market Update Supply factors weigh heavily on oil Summary Brent oil prices are trading above $80 per barrel (pb), the highest level since early November 20, on the back of

Investor Presentation

Investor Presentation First nine months 2017 activity update October 18, 2017 Disclaimer This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use

Investor Presentation First nine months 2017 activity update October 18, 2017 Disclaimer This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use

Energy and commodity price benchmarking and market insights

Energy and commodity price benchmarking and market insights London, Houston, Washington, New York, Portland, Calgary, Santiago, Bogota, Rio de Janeiro, Singapore, Beijing, Tokyo, Sydney, Dubai, Moscow,

Energy and commodity price benchmarking and market insights London, Houston, Washington, New York, Portland, Calgary, Santiago, Bogota, Rio de Janeiro, Singapore, Beijing, Tokyo, Sydney, Dubai, Moscow,

Milken Institute: Center for Accelerating Energy Solutions

Milken Institute: Center for Accelerating Energy Solutions Center for Accelerating Energy Solutions Promotes policy and market mechanisms to build a more stable and sustainable energy future Identifies

Milken Institute: Center for Accelerating Energy Solutions Center for Accelerating Energy Solutions Promotes policy and market mechanisms to build a more stable and sustainable energy future Identifies

Brian A. Habacivch Constellation, Commodities Management Group October 20, 2018

North American Energy Outlook The Transformative Role of Shale in the Global Hydrocarbons Market Why It Matters to Commercial, Institutional, and Industrial End Users Brian A. Habacivch Constellation,

North American Energy Outlook The Transformative Role of Shale in the Global Hydrocarbons Market Why It Matters to Commercial, Institutional, and Industrial End Users Brian A. Habacivch Constellation,

The Effects of Hurricane Harvey on the US Winter Propane Outlook

Prepared for the National Propane Gas Association 217 Fall Board of Directors Meeting The Effects of Hurricane Harvey on the US Winter Propane Outlook October 1, 217 August, 216 Debnil Chowdhury, Director,

Prepared for the National Propane Gas Association 217 Fall Board of Directors Meeting The Effects of Hurricane Harvey on the US Winter Propane Outlook October 1, 217 August, 216 Debnil Chowdhury, Director,

Business Performance in FY2009 and Outlook for FY2010. Mitsui O.S.K. Lines, Ltd. April 2010

Business Performance in FY2009 and Outlook for FY2010 Mitsui O.S.K. Lines, Ltd. April 2010 HP Contents FY2009 Results [Consolidated] 2 Key Points of FY2009 Full-year Results [Consolidated] 4 Results Comparison

Business Performance in FY2009 and Outlook for FY2010 Mitsui O.S.K. Lines, Ltd. April 2010 HP Contents FY2009 Results [Consolidated] 2 Key Points of FY2009 Full-year Results [Consolidated] 4 Results Comparison

Global energy markets

For Woodrow Wilson Center Global Energy Forum September 21, 215 Washington, DC by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent

For Woodrow Wilson Center Global Energy Forum September 21, 215 Washington, DC by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent

The dry bulk freight market: Prospects for recovery?

MetalBulletin Asian Bauxite and Alumina 2013 The dry bulk freight market: Prospects for recovery? Ralph Leszczynski 30-31 October 2013, Singapore research www.bancosta.it ; research@bancosta.it Legal notice:

MetalBulletin Asian Bauxite and Alumina 2013 The dry bulk freight market: Prospects for recovery? Ralph Leszczynski 30-31 October 2013, Singapore research www.bancosta.it ; research@bancosta.it Legal notice:

Liquefied Natural Gas (LNG) Production and Markets. By: Jay Drexler, Dino Kasparis, and Curt Knight

Production and Markets. By: Jay Drexler, Dino Kasparis, and Curt Knight") Liquefied Natural Gas (LNG) Production and Markets By: Jay Drexler, Dino Kasparis, and Curt Knight Outline Purpose of the presentation What is Liquefied Natural Gas? (LNG) LNG Operations Brief History

Liquefied Natural Gas (LNG) Production and Markets By: Jay Drexler, Dino Kasparis, and Curt Knight Outline Purpose of the presentation What is Liquefied Natural Gas? (LNG) LNG Operations Brief History

Presentation2. Agenda. Page. Argus Americas LPG Summit - Miami February 5th, Ted Young, CFO

Presentation2 Agenda Page Argus Americas LPG Summit - Miami February 5th, 2015 Ted Young, CFO [CLIENT NAME] Disclaimer Forward-Looking Statements This Presentation contains certain forward-looking statements

Presentation2 Agenda Page Argus Americas LPG Summit - Miami February 5th, 2015 Ted Young, CFO [CLIENT NAME] Disclaimer Forward-Looking Statements This Presentation contains certain forward-looking statements

International Energy Outlook: key findings in the 216 Reference case World energy consumption increases from 549 quadrillion Btu in 212 to 629 quadril

EIA's Global Energy Outlook For The Institute of Energy Economics, Japan October 5, 216 Japan By Adam Sieminski, Administrator U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

EIA's Global Energy Outlook For The Institute of Energy Economics, Japan October 5, 216 Japan By Adam Sieminski, Administrator U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

Global Gasoline, Global Condensate and Global Petrochemical Markets to 2020 and How much naphtha will end up in gasoline blending?

Study Prospectus Nexus - The Interaction Between: Global Gasoline, Global Condensate and Global Petrochemical Markets to 2020 and 2025 Can I export more naphtha? Should I build a splitter? Should I build

Study Prospectus Nexus - The Interaction Between: Global Gasoline, Global Condensate and Global Petrochemical Markets to 2020 and 2025 Can I export more naphtha? Should I build a splitter? Should I build

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION MAY 2018 RIYADH, SAUDI ARABIA MAY 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON THE

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION MAY 2018 RIYADH, SAUDI ARABIA MAY 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON THE

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 3, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 3, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Energy and commodity price benchmarking and market insights

Energy and commodity price benchmarking and market insights London, Houston, Washington, New York, Portland, Calgary, Santiago, Bogota, Rio de Janeiro, Singapore, Beijing, Tokyo, Sydney, Dubai, Moscow,

Energy and commodity price benchmarking and market insights London, Houston, Washington, New York, Portland, Calgary, Santiago, Bogota, Rio de Janeiro, Singapore, Beijing, Tokyo, Sydney, Dubai, Moscow,

Seminole Electric proposes $727M natural gas plant In Bad Trade Off, New England Forsakes Natural Gas For Petroleum

Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: D E C E M B E R 2 8, 2 1 7 Prior Day s NYMEX Jan-18 Contract (CT) 2.78

Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: D E C E M B E R 2 8, 2 1 7 Prior Day s NYMEX Jan-18 Contract (CT) 2.78

Market Alert. China NPK Statistical Update October 2016 Statistics. China MOP Imports. China Exports. China Imports

Market Alert China NPK Statistical Update October Statistics China showed signs of life in October on both the import and export front, though overseas shipments of key fertilizer products continued to

Market Alert China NPK Statistical Update October Statistics China showed signs of life in October on both the import and export front, though overseas shipments of key fertilizer products continued to

Madrid WPC Breakfast Conference 7 May Keisuke SADAMORI Director of Energy Markets and Security IEA

Madrid WPC Breakfast Conference 7 May 2015 Keisuke SADAMORI Director of Energy Markets and Security IEA OECD/IEA 2014 Oil prices ease in March, but recover in early April $/bbl 120 110 100 90 80 70 60

Madrid WPC Breakfast Conference 7 May 2015 Keisuke SADAMORI Director of Energy Markets and Security IEA OECD/IEA 2014 Oil prices ease in March, but recover in early April $/bbl 120 110 100 90 80 70 60

TANKER MARKET INSIGHT

TANKER MARKET INSIGHT April 18 Research Department, Strategic Development Mar-17 Apr-17 May-17 Jul-17 Aug-17 Oct-17 Nov-17 Jan-18 Feb-18 Mar-17 Apr-17 May-17 Jul-17 Aug-17 Oct-17 Nov-17 Jan-18 Feb-18 $

TANKER MARKET INSIGHT April 18 Research Department, Strategic Development Mar-17 Apr-17 May-17 Jul-17 Aug-17 Oct-17 Nov-17 Jan-18 Feb-18 Mar-17 Apr-17 May-17 Jul-17 Aug-17 Oct-17 Nov-17 Jan-18 Feb-18 $

Where are we in the market cycles? 16 October 2018

Where are we in the market cycles? 16 October 218 Marine Money Greek Shipfinance Forum Athens Prepared by Angelica Kemene Head of Market Analysis & Intelligence Market Fundamentals Cycles & Prices & Trends

Where are we in the market cycles? 16 October 218 Marine Money Greek Shipfinance Forum Athens Prepared by Angelica Kemene Head of Market Analysis & Intelligence Market Fundamentals Cycles & Prices & Trends

Weber US Crude Oil Trade Report

Weber US Crude Oil Trade Report j, 23 f, 31 m, 26 a, 3 m, 32 j, 24 216 217 Linear (216) Linear (217) The ability of US producers to continue to grow production in an environment of sub $5Bbl prices was

Weber US Crude Oil Trade Report j, 23 f, 31 m, 26 a, 3 m, 32 j, 24 216 217 Linear (216) Linear (217) The ability of US producers to continue to grow production in an environment of sub $5Bbl prices was

Financial Results Meeting: The 1st 3 Months of FY Ending March (April 1, 2016 June 30, 2016) August 9, 2016

August 9, 2016") Financial Results Meeting: The 1st 3 Months of FY Ending March 2017 (April 1, 2016 June 30, 2016) August 9, 2016 Unification of Accounting Period Unify accounting period (financial reporting period) of

Financial Results Meeting: The 1st 3 Months of FY Ending March 2017 (April 1, 2016 June 30, 2016) August 9, 2016 Unification of Accounting Period Unify accounting period (financial reporting period) of

Milk and Milk Products: Price and Trade Update

Milk and Milk Products: Price and Trade Update International dairy prices December 2017 1 The FAO Dairy Price Index d 204.2 points in November, up 11.2 points (5.8 percent) from January 2017. At this level,

Milk and Milk Products: Price and Trade Update International dairy prices December 2017 1 The FAO Dairy Price Index d 204.2 points in November, up 11.2 points (5.8 percent) from January 2017. At this level,

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 17, 2017 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 17, 2017 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Weber US Crude Oil Trade Report

Weber US Crude Oil Trade Report j f a m j j Imports 216 215 Linear (216) Linear (215) US Crude Oil Imports set to contract It is estimated that seaborne crude oil imports increased by around 12% in 216

Weber US Crude Oil Trade Report j f a m j j Imports 216 215 Linear (216) Linear (215) US Crude Oil Imports set to contract It is estimated that seaborne crude oil imports increased by around 12% in 216

EIA Winter Fuels Outlook

EIA 2018 19 Winter Fuels Outlook U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov The main determinants of winter heating fuels expenditures are temperatures and prices

EIA 2018 19 Winter Fuels Outlook U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov The main determinants of winter heating fuels expenditures are temperatures and prices

WORLD ENERGY OUTLOOK. 9 th Annual GPCA Forum. Information Analytics Expertise NOVEMBER 23, 2014

Information Analytics Expertise NOVEMBER 23, 214 WORLD ENERGY OUTLOOK 9 th Annual GPCA Forum Blake Eskew, Vice President IHS Energy - Oil Markets & Downstream +1 713 331 4 Blake.Eskew@ihs.com 214 IHS Short

Information Analytics Expertise NOVEMBER 23, 214 WORLD ENERGY OUTLOOK 9 th Annual GPCA Forum Blake Eskew, Vice President IHS Energy - Oil Markets & Downstream +1 713 331 4 Blake.Eskew@ihs.com 214 IHS Short

U.S. Oil Prices Outlook January 2019

U.S. Oil Prices Outlook January 219 Oil Prices OPEC+ decision to reduce output prevented prices from declining further The expiration of import waivers of Iranian oil could have a positive effect on prices

U.S. Oil Prices Outlook January 219 Oil Prices OPEC+ decision to reduce output prevented prices from declining further The expiration of import waivers of Iranian oil could have a positive effect on prices

May 2008 COMPANY OVERVIEW & UPDATE

May 2008 COMPANY OVERVIEW & UPDATE Important Notice Forward-looking statements and figures in this presentation are based on Hyundai Merchant Marine s current expectations and no assurances can be made

May 2008 COMPANY OVERVIEW & UPDATE Important Notice Forward-looking statements and figures in this presentation are based on Hyundai Merchant Marine s current expectations and no assurances can be made

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 14, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 14, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

7. Gas. Resources and Energy Quarterly December

7. Gas Resources and Energy Quarterly December 18 42 7.1 Summary The value of Australia s LNG exports is forecast to increase from $31 billion in 17 18 to $5 billion in 18 19, driven by higher export volumes

7. Gas Resources and Energy Quarterly December 18 42 7.1 Summary The value of Australia s LNG exports is forecast to increase from $31 billion in 17 18 to $5 billion in 18 19, driven by higher export volumes

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 21, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 21, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

The Great Deflation in Oil: Impact on the Polyester Chain

Information Analytics Expertise The Great Deflation in Oil: Impact on the Polyester Chain Indian Polyester 215 19 June, Mumbai Ashish Pujari, Senior Director (Aromatics & Fibers) + 65 6439 61 Ashish.Pujari@ihs.com

Information Analytics Expertise The Great Deflation in Oil: Impact on the Polyester Chain Indian Polyester 215 19 June, Mumbai Ashish Pujari, Senior Director (Aromatics & Fibers) + 65 6439 61 Ashish.Pujari@ihs.com

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending March 22, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending March 22, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Dry Bulk Freight Market: Review of 2012 & Prospects For Recovery Metal Bulletin Bauxite & Alumina Conference Singapore October 2012

Dry Bulk Freight Market: Review of 212 & Prospects For Recovery Metal Bulletin Bauxite & Alumina Conference Singapore 3-31 Whilst care and attention has been taken to ensure that the information contained

Dry Bulk Freight Market: Review of 212 & Prospects For Recovery Metal Bulletin Bauxite & Alumina Conference Singapore 3-31 Whilst care and attention has been taken to ensure that the information contained