Energy Market Update. April 8, Kevin Krcil Chris Dubay

|

|

|

- Duane Edwards

- 6 years ago

- Views:

Transcription

1 Energy Market Update April 8, 2014 Kevin Krcil Chris Dubay

2 Winter Review and Brief Look at Summer 2014 Kevin Krcil, Head of Weather Trading

3 Agenda Winter Review Outcome Polar Vortex Specific Cold Air Events Summer Forecast and Analysis El Nino Drought Various Summer Outlooks 3

4")

4 Winter US Gas weighted heating degree days (GWHDDs) = US GWHDD 10 yr average = US GWHDD 30 yr average = % increase over the 10 yr avg, and 9% increase over the 30 yr avg Ranked 8 th coldest US winter since 1950 (based on GWHDDs) 4

5 Polar Vortex The polar vortex is a persistent, large-scale cyclone (intense area of low pressure) located near both of a planet's geographical poles. They strengthen in the winter and weaken in the summer. They are associated with extreme cold as noted during the January and February episodes, but typically reside near/within the Arctic/Antarctic Circles. 5

January 2014 February 2014 GWHDDs")

6 Monthly Temperature Anomalies (vs. 10 year average) January 2014 February 2014 GWHDDs = 1048 GWHDD 10 year avg. = th coldest since 1950 GWHDDs = 883 GWHDD 10 year avg. = th coldest since

7 Specific Polar Vortex Episodes January th, 2014 February 8-13 th, 2014 GWHDDs = 385 GWHDD 10 year avg. = th coldest since 1950 GWHDDs = 217 GWHDD 10 year avg. = th coldest since

8 A Few Summer Forecast Variables El Nino Drought 8

9 El Nino Regions of Interest El Nino Monitoring /Calculation Regions Current Sea Surface Temperature Anomalies (SSTAs) 9

10 Signs of a Developing El Nino Regional SSTAs Time Series of Equatorial SSTAs 10

11 Drought Drought conditions confined primarily to the Central and Western US Worst conditions continue to be in California El Nino events typically correlate to above average precipitation for most of the US except below average for the West Coast, parts of Texas, and the New England states 11

Winter")

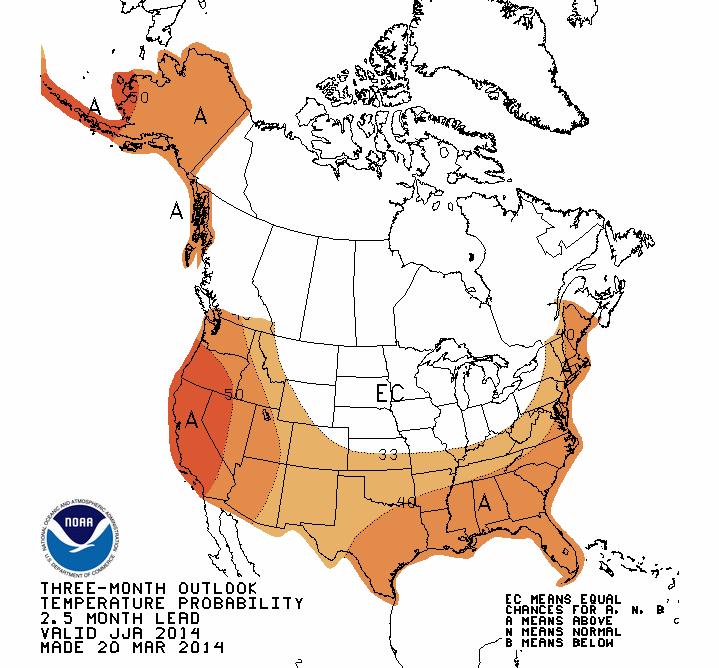

12 El Nino Seasonal Temperature Correlations Summer (Jun-Aug) Winter (Dec-Feb) 12

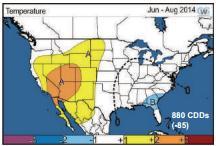

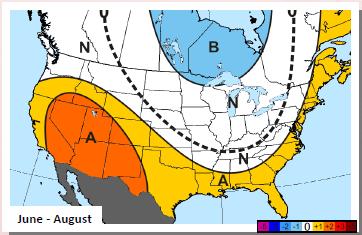

13 Summer Outlooks 13

14 Questions? 14

15 Energy Market Update Chris Dubay, Energy Advisor 15

16 Natural Gas Forwards Rallied to Five-Year Highs Weekly Prompt NYMEX Natural Gas since 2010 $6.149 settle on 2/19/14 $6.49 intraday on 2/21/ Dip in polar vortex caused repeated cold snaps 16

17 And Significant Volatility in Next-Day Electricity Markets $500 $450 Mass-Hub On-Peak DA $400 $350 $300 $250 $200 $150 $100 $50 $- DA = Day-Ahead Electricity Price Mass-Hub On-Peak DA 17

18 BCF Strong Demand Creates Huge Storage Deficit 3,800 3,300 Source: E.I.A. Estimated U.S. Storage Capacity = 4,239 Bcf Current inventory through 3/28/14 = 822 Bcf 51.6% below one year ago 54.7% below 5-year average All-time record of 3,929 Bcf on 11/2/12 2,800 2,300 1,800 1,300 Projected inventory through 4/18/14 = 915 Bcf 815 Bcf below Bcf below 5YA Working Gas Stock This Year (2014) Working Gas Stock Last Year (2013) Year Average ( ) 18

19 Natural Gas 12-mo Strip Seeking Direction 12-mo strip since Jan 1 st 12-mo strip trending slightly down, but mostly sideways 19

20 Impacts on Forward Pricing 20

21 NG Forwards 2014 Spikes; Terms Less Impacted Change since Nov lows Cal 15 Cal 16 Cal month strip Current / Term Change 12-mo $4.52 +$0.92 Cal 15 $4.28 +$0.40 Cal 16 $4.21 +$0.21 Cal 17 $4.28 +$0.15 NYMEX NG prices since late

22 Prolific Shale Growth Continues Price Impact Beyond Current Weather is Bearish Marcellus now represents ~ 20% of U.S. supply Dramatic impact on regional gas basis and transport flows DTI, TCO and TETCO basis significantly below Henry Hub Domestic dry gas production set record in November (67 Bcf/Day) Shale gas limits long-term market upside 22

23 U.S. Becoming a Natural Gas Exporter Why? Lower prices compared to the world 23

24 Longer Term Gas Generation Growing Why? Cheap gas and expensive EPA regulations Low prices of 2012 were first instance of widespread coal-to-gas switching due to price Significant coal retirements already due to low gas prices Additional coal retirements expected due to EPA regulations 24

25 Bearish Bullish Weather Overtakes Shale as Dominant Market Driver But... Shale remains primary long-term driver Near-Term (2014) Huge storage deficit Generator maintenance/refueling Strong winter gas basis Shale production Lower off-peak generation demand from NG > $4.50 Weak summer gas basis Long-Term (>= 2015) Coal plant retirements due to EPA regulations LNG exports Growing industrial demand Abundant shale NG drilling efficiencies - Rig counts don t count End-user efficiency Wildcards include weather, financial markets & speculators, U.S. and global economies, and geopolitical events Repeat of 2008 highs or 2012 lows are unlikely Long-term remained flat as near-term spiked 25

26 Regional Markets Update 26

27 Strong Power to Regional Gas Correlation $65 ISO-NE Mass Hub vs. Algonquin City Gate Calendar 2015 $8.50 $70 NYISO Zone J vs. Transco Zone 6 NY Calendar 2015 $8.00 $6.70 $60 $7.50 $65 $6.20 $7.00 $55 $60 $5.70 $6.50 $5.20 $50 $6.00 $55 $5.50 $4.70 $45 $50 $5.00 $4.20 $40 $4.50 $45 $3.70 NEPOOL - MASS HUB Cal '15 ATC AGT CITYGATE Cal '15 NYISO - ZONE J Cal '15 ATC TRANSCO ZONE 6 NY Cal '15 The information presented above was gathered and compiled by Direct Energy Business for the convenience of its employees, clients, and potential customers and is for informational purposes only. Direct Energy Business makes no representation or warranty regarding the accuracy, reliability, comprehensiveness, or currency of the aforementioned data. This information is being provided as a courtesy and should not be construed as an offer to sell, a solicitation of an offer to buy any exchange-traded futures, options contracts or any energy commodity, or advice regarding the purchase or sale of exchange-traded futures or options contracts. Past performance is not necessarily indicative of future results. Reliance upon this information is at the sole risk of the reader. The information presented above was gathered and compiled by Direct Energy Business for the convenience of its employees, clients, and potential customers and is for informational purposes only. Direct Energy Business makes no representation or warranty regarding the accuracy, reliability, comprehensiveness, or currency of the aforementioned data. This information is being provided as a courtesy and should not be construed as an offer to sell, a solicitation of an offer to buy any exchange-traded futures, options contracts or any energy commodity, or advice regarding the purchase or sale of exchange-traded futures or options contracts. Past performance is not necessarily indicative of future results. Reliance upon this information is at the sole risk of the reader. PJM West Hub vs. Tetco M3 Calendar 2015 $6.90 $55 $6.40 Especially in the Northeast $50 $5.90 $5.40 $45 $4.90 $4.40 $40 $3.90 $35 $3.40 PJM - WEST HUB Cal '15 ATC TETCO M3 Cal '15 The information presented above was gathered and compiled by Direct Energy Business for the convenience of its employees, clients, and potential customers and is for informational purposes only. Direct Energy Business makes no representation or warranty regarding the accuracy, reliability, comprehensiveness, or currency of the aforementioned data. This information is being provided as a courtesy and should not be construed as an offer to sell, a solicitation of an offer to buy any exchange-traded futures, options contracts or any energy commodity, or advice regarding the purchase or sale of exchange-traded futures or options contracts. Past performance is not necessarily indicative of future results. Reliance upon this information is at the sole risk of the reader. 27

28 Regional Considerations NY/NE Power pricing reflects exaggerated movements in the NYMEX, especially during winter months o Severe pipeline constraints limiting reliability and diversification of generation o No pipeline constraint relief until 2017 ISO-NE instituted Winter Reliability Program for winter o o ISO s focus is to maintain reliability, not put a guard on pricing Successful in maintaining reliability, however, higher prices partly due to high price of oil Loss of over 2,100 MWs generation adding to woes over future reliability o 620 MW Vermont Yankee in Q o 1530 MW Brayton Point in May 2017 o 720 MW Salem Harbor in May 2014 (replaced w/ 674 MW gas turbine in 2016) New capacity zone (Lower Hudson Valley Capacity Zone, or LHV) goes into effect May 1, 2014 without price phase-in o Zones G-J (LHV) $9.96 o LI (Zone K) $6.39 o NYC (Zone J) $16.24 o NYCA (ROS) $

29 Regional Considerations - PJM Much like New England/New York coldest weather in 20 years drove short-term markets significantly higher. PJM West Hub day-ahead prices experienced multiple days of $400+. Capacity rates are key cost factors, expect the unexpected. Shale gas supply provides significant price relief in this region. TETCO M3 basis driving power prices. Discount to NYMEX HH still present during summer months. Impacts from EPA regulations that cause coal retirements present risk (see 2014 and 2015 capacity prices). 29

30 Regional Considerations ERCOT/CAISO Limited impact from polar vortex (summer peak market) ERCOT now forecasts slower growth in electricity demand o Now 1.3% YOY growth vs. the 2.5% a year o Reserve margin wouldn t fall below the 13.75% level until 2019 with this growth forecast Raising offer cap to $9,000/MWh is ERCOT s strategy to maintain sufficient capacity for growing peak requirements (no capacity market) Capacity market talks on hold, may revisit the issue in 2015 Drought risk reversed now above-normal precipitation vs. below-normal just one month ago Nuclear generation spring maintenance o Palo Verde, AZ 1,270 MW o Diablo Canyon, CA 1,100 MW 30

31 Questions? 31

32 Thank you for attending today s webinar Today s slide presentation can be found at: updatewebinar 32

Energy Market Update. August 21, Chris Dubay. Energy Advisor

Energy Market Update August 21, 2014 Chris Dubay Energy Advisor NYMEX is Range-bound Again Reached 5-year highs in Feb Prices had been range-bound since late Feb ($4.30 - $4.80) Broke out below range on

Energy Market Update August 21, 2014 Chris Dubay Energy Advisor NYMEX is Range-bound Again Reached 5-year highs in Feb Prices had been range-bound since late Feb ($4.30 - $4.80) Broke out below range on

NYMEX - Annual Strips

Weekly Summary: The U.S. Energy Information Administration reported that natural gas storage fell by 48 billion cubic feet this week, higher than the expected reduction of 39 Bcf but considerably lower

Weekly Summary: The U.S. Energy Information Administration reported that natural gas storage fell by 48 billion cubic feet this week, higher than the expected reduction of 39 Bcf but considerably lower

WEEKLY MARKET UPDATE

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 183 Bcf. The withdrawal for the same week last year was 230 Bcf

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 183 Bcf. The withdrawal for the same week last year was 230 Bcf

MARKET COMMENTARY. Energy and Sustainability Solutions Energy Market Roundup. North America. November 20, 2014 MARKET FUNDAMENTALS OIL PRICE UPDATE

PRICING As unseasonably cold weather and early season snowstorms have blanketed much of the Midwest and Northeast, and natural gas market volatility has reacted predictably. Volatility in the prompt month

PRICING As unseasonably cold weather and early season snowstorms have blanketed much of the Midwest and Northeast, and natural gas market volatility has reacted predictably. Volatility in the prompt month

NYMEX - Annual Strips

Weekly Summary: The US EIA came in with a withdrawal of 34 Bcf in their report on Thursday. It was below expectations of 38-42 Bcf and extremely below the 5 year average of 120 Bcf. Last year this week

Weekly Summary: The US EIA came in with a withdrawal of 34 Bcf in their report on Thursday. It was below expectations of 38-42 Bcf and extremely below the 5 year average of 120 Bcf. Last year this week

Direct Energy Business Monthly Webinar. Expressly for Channel Partners August 5, 2015

Direct Energy Business Monthly Webinar Expressly for Channel Partners August 5, 2015 Webinar Agenda Tim Bigler, Sr. Market Strategist Randall Burns, Power Pricing Supervisor-PJM Commodity Market Update

Direct Energy Business Monthly Webinar Expressly for Channel Partners August 5, 2015 Webinar Agenda Tim Bigler, Sr. Market Strategist Randall Burns, Power Pricing Supervisor-PJM Commodity Market Update

WEEKLY MARKET UPDATE

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 288 Bcf. The withdrawal for the same week last year was 137 Bcf

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 288 Bcf. The withdrawal for the same week last year was 137 Bcf

Andrew D. Weissman Senior Energy Advisor, Haynes and Boone, LLP Chief Executive Officer, EBW AnalyticsGroup

Understand the Factors Behind this Winter s Price Spikes, and their Implications on Near and Longer Term Pricing of Electricity and Natural Gas Andrew D. Weissman Senior Energy Advisor, Haynes and Boone,

Understand the Factors Behind this Winter s Price Spikes, and their Implications on Near and Longer Term Pricing of Electricity and Natural Gas Andrew D. Weissman Senior Energy Advisor, Haynes and Boone,

Markets and Opportunities. Paul Burgener March 2015

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 14, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 14, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

NYMEX - Annual Strips

Week Summary: The EIA reported a storage injection of 112 Bcf for the week ending May 22nd. The much larger-than-expected build in inventories sent NYMEX July gas futures 14.1 cents lower on the day to

Week Summary: The EIA reported a storage injection of 112 Bcf for the week ending May 22nd. The much larger-than-expected build in inventories sent NYMEX July gas futures 14.1 cents lower on the day to

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 31, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 31, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

AEE New England New England Energy Update 1/6/2016. Tim Bigler Senior Market Strategist

AEE New England New England Energy Update 1/6/2016 Tim Bigler Senior Market Strategist Agenda NYMEX NG/Oil Prices New England NG/Electric Prices Future Gas Produc:on Influences New England NG Pipeline

AEE New England New England Energy Update 1/6/2016 Tim Bigler Senior Market Strategist Agenda NYMEX NG/Oil Prices New England NG/Electric Prices Future Gas Produc:on Influences New England NG Pipeline

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 24, 2017 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 24, 2017 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending December 28, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending December 28, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 23, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 23, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

IAF Advisors Energy Market Outlook Kyle Cooper, (713) , March 6, 2015

, March 6, 2015") IAF Advisors Energy Market Outlook Kyle Cooper, (713) 722-7171, Kyle.Cooper@IAFAdvisors.com March 6, 2015 Price Action: The April contract rose 10.5 cents (3.8%) to $2.839 on a 22.9 cent range. Price Outlook:

IAF Advisors Energy Market Outlook Kyle Cooper, (713) 722-7171, Kyle.Cooper@IAFAdvisors.com March 6, 2015 Price Action: The April contract rose 10.5 cents (3.8%) to $2.839 on a 22.9 cent range. Price Outlook:

Ten Years After Gas & Power in Perspective

Regional Market Trends Forum Ten Years After Gas & Power in Perspective Richard Levitan, rll@levitan.com May 1, 2014 Agenda 2014 Polar Vortex v. 2004 Cold Snap Northeast Gas & Power 10 Years After Gas

Regional Market Trends Forum Ten Years After Gas & Power in Perspective Richard Levitan, rll@levitan.com May 1, 2014 Agenda 2014 Polar Vortex v. 2004 Cold Snap Northeast Gas & Power 10 Years After Gas

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending January 5, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending January 5, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 3, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 3, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

IMGA Annual Meeting- NG Fundamentals Update. March 28, 2017

IMGA Annual Meeting- NG Fundamentals Update Presenter Trevor Cooper Name / Date March 28, 2017 Disclaimer Copyright. All rights reserved. Contents of this presentation do not necessarily reflect the Company

IMGA Annual Meeting- NG Fundamentals Update Presenter Trevor Cooper Name / Date March 28, 2017 Disclaimer Copyright. All rights reserved. Contents of this presentation do not necessarily reflect the Company

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 17, 2017 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 17, 2017 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending March 22, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending March 22, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 21, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 21, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 7, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 7, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

IAF Advisors Energy Market Outlook Kyle Cooper, (713) , October 31, 2014

, October 31, 2014") IAF Advisors Energy Market Outlook Kyle Cooper, (713) 722 7171, Kyle.Cooper@IAFAdvisors.com October 31, 2014 Price Action: The December contract rose 17.5 cents (4.7%) to $3.873 on a 33.3 cent range. Price

IAF Advisors Energy Market Outlook Kyle Cooper, (713) 722 7171, Kyle.Cooper@IAFAdvisors.com October 31, 2014 Price Action: The December contract rose 17.5 cents (4.7%) to $3.873 on a 33.3 cent range. Price

Energy Market Overview

Energy Market Overview Mashiur Bhuiyan, PhD October 19, 2016 Disclaimer: This presentation is for informational purposes only and is not intended to provide advice or recommendation on any transaction

Energy Market Overview Mashiur Bhuiyan, PhD October 19, 2016 Disclaimer: This presentation is for informational purposes only and is not intended to provide advice or recommendation on any transaction

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending January 25, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending January 25, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending April 12, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending April 12, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

MARKET INTEL NEWSLETTER

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers January 2019 Fuels Natural Gas Coal The December warm-up continued into the second half of January 2019

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers January 2019 Fuels Natural Gas Coal The December warm-up continued into the second half of January 2019

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending February 15, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending February 15, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Greg Hathaway Energy Source Holdings, LLC

Greg Hathaway Energy Source Holdings, LLC WEATHER THE PICTURE TO THE RIGHT SHOWS THE 2015-16 WINTER HAS BEEN MUCH ABOVE NORMAL. SINCE 2008 THE NATIONAL TEMPERATURE HAS BEEN BELOW NORMAL SIX TIMES 2013-14

Greg Hathaway Energy Source Holdings, LLC WEATHER THE PICTURE TO THE RIGHT SHOWS THE 2015-16 WINTER HAS BEEN MUCH ABOVE NORMAL. SINCE 2008 THE NATIONAL TEMPERATURE HAS BEEN BELOW NORMAL SIX TIMES 2013-14

Electric Forward Market Report

Mar-01 Mar-02 Jun-02 Sep-02 Dec-02 Mar-03 Jun-03 Sep-03 Dec-03 Mar-04 Jun-04 Sep-04 Dec-04 Mar-05 May-05 Aug-05 Nov-05 Feb-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Apr-08 Jun-08 Sep-08 Dec-08

Mar-01 Mar-02 Jun-02 Sep-02 Dec-02 Mar-03 Jun-03 Sep-03 Dec-03 Mar-04 Jun-04 Sep-04 Dec-04 Mar-05 May-05 Aug-05 Nov-05 Feb-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Apr-08 Jun-08 Sep-08 Dec-08

NYMEX UPDATE BULLS & BEARS REPORT

June 30, 2016 NYMEX UPDATE BULLS & BEARS REPORT Author MATTHEW MATTINGLY Energy Analyst / Louisville Ph: 502-895-7882 Author JASON SCARBROUGH VP Risk Management / Houston Ph: 713-899-3639 INTRODUCTION

June 30, 2016 NYMEX UPDATE BULLS & BEARS REPORT Author MATTHEW MATTINGLY Energy Analyst / Louisville Ph: 502-895-7882 Author JASON SCARBROUGH VP Risk Management / Houston Ph: 713-899-3639 INTRODUCTION

Northeast Energy Summit 1 Veterans Way, Suite 200 Carnegie, PA Steve Dean, ASA, P.E. Managing Principal (412)

") Gas Price Spikes and the Impacts on Power Prices and Dispatch September 17, 2014 Management Consultants, Inc. Northeast Energy Summit 1 Veterans Way, Suite 200 Carnegie, PA 15106 Steve Dean, ASA, P.E.

Gas Price Spikes and the Impacts on Power Prices and Dispatch September 17, 2014 Management Consultants, Inc. Northeast Energy Summit 1 Veterans Way, Suite 200 Carnegie, PA 15106 Steve Dean, ASA, P.E.

Regional Energy Commission. Program Outreach

Regional Energy Commission Program Outreach Wednesday, July 13, 2011 Agenda Regional Project Overview Street Lighting Upgrade Outdoor Lighting Upgrade Energy Market Update Market Structure Power & Gas

Regional Energy Commission Program Outreach Wednesday, July 13, 2011 Agenda Regional Project Overview Street Lighting Upgrade Outdoor Lighting Upgrade Energy Market Update Market Structure Power & Gas

Energy Market Intelligence Webinar. January 23, 2019

Energy Market Intelligence Webinar January 23, 2019 Today s Speakers Andrew Durante Meteorologist Ed Fortunato Managing Director, Wholesale Short-Term Fundamentals Greg Kosier Commodities Management Group

Energy Market Intelligence Webinar January 23, 2019 Today s Speakers Andrew Durante Meteorologist Ed Fortunato Managing Director, Wholesale Short-Term Fundamentals Greg Kosier Commodities Management Group

Energy Market Outlook Webinar. December, 2017

Energy Market Outlook Webinar December, 2017 Today s Webinar Agenda Winter Weather Outlook Short-term temperature outlooks Winter weather forecasts colder winter than a year ago? Short-Term Market Fundamentals:

Energy Market Outlook Webinar December, 2017 Today s Webinar Agenda Winter Weather Outlook Short-term temperature outlooks Winter weather forecasts colder winter than a year ago? Short-Term Market Fundamentals:

MARKET INTEL NEWSLETTER

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers January 2018 Fuels Natural Gas A shot of artic air drove prompt-month NYMEX natural gas from a low of

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers January 2018 Fuels Natural Gas A shot of artic air drove prompt-month NYMEX natural gas from a low of

Upcoming CPES Meetings

Upcoming CPES Meetings December 10, 2014: Meet the Regulators January 14, 2015: Legislative Preview February 11, 2015: Connecticut Green Bank with Bryan Garcia March 11, 2015: Connecticut Energy, Environment

Upcoming CPES Meetings December 10, 2014: Meet the Regulators January 14, 2015: Legislative Preview February 11, 2015: Connecticut Green Bank with Bryan Garcia March 11, 2015: Connecticut Energy, Environment

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer.

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

Natural Gas Price Dynamics. Insight to Emerging Trends

Natural Gas Price Dynamics Insight to Emerging Trends January 13, 2011 Natural Gas Price Dynamics Insight to Emerging Trends o o o o Who is Gavilon? History of Natural Gas What Drives Pricing? a. Weather

Natural Gas Price Dynamics Insight to Emerging Trends January 13, 2011 Natural Gas Price Dynamics Insight to Emerging Trends o o o o Who is Gavilon? History of Natural Gas What Drives Pricing? a. Weather

Winter 2015 Cold Weather Operations

Winter 2015 Cold Weather Operations Wes Yeomans Vice President - Operations New York Independent System Operator Management Committee March 31, 2015 Rensselaer, NY 2015 New York Independent System Operator,

Winter 2015 Cold Weather Operations Wes Yeomans Vice President - Operations New York Independent System Operator Management Committee March 31, 2015 Rensselaer, NY 2015 New York Independent System Operator,

Energy Market Intelligence Webinar. February 20, 2019

Energy Market Intelligence Webinar February 20, 2019 Today s Speakers David Ryan Meteorologist Ed Fortunato Managing Director, Wholesale Short-Term Fundamentals Keith Poli Commodities Management Group

Energy Market Intelligence Webinar February 20, 2019 Today s Speakers David Ryan Meteorologist Ed Fortunato Managing Director, Wholesale Short-Term Fundamentals Keith Poli Commodities Management Group

MARKET INTEL NEWSLETTER

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers September 2018 Fuels Natural Gas Coal Natural gas production reached a new record 83.2 Bcf per day in

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers September 2018 Fuels Natural Gas Coal Natural gas production reached a new record 83.2 Bcf per day in

EIA Short-Term Energy and Winter Fuels Outlook

EIA Short-Term Energy and Winter Fuels Outlook NASEO 2015 Winter Energy Outlook Conference Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent

EIA Short-Term Energy and Winter Fuels Outlook NASEO 2015 Winter Energy Outlook Conference Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent

Agenda. Natural gas and power markets overview. Generation retirements and in developments. Future resource mix including large hydro

Agenda Natural gas and power markets overview Generation retirements and in developments Future resource mix including large hydro Balancing environmental, reliability and cost impacts 1 Northeast Utilities

Agenda Natural gas and power markets overview Generation retirements and in developments Future resource mix including large hydro Balancing environmental, reliability and cost impacts 1 Northeast Utilities

Northeast Drives US Basis Trends

Northeast Drives US Basis Trends Rocco Canonica, Director Energy Analysis September 2014 2014 Platts, McGraw Hill Financial. All rights reserved. Benposium 2014. Agenda 2014 Year of Extremes; Review Record

Northeast Drives US Basis Trends Rocco Canonica, Director Energy Analysis September 2014 2014 Platts, McGraw Hill Financial. All rights reserved. Benposium 2014. Agenda 2014 Year of Extremes; Review Record

2010 Annual Winter Reliability Assessment Meeting November 4, Carlos Thillet Manager Gas Supply and Transportation PECO Energy Company

Pennsylvania Public Utility Commission 2010 Annual Winter Reliability Assessment Meeting November 4, 2010 Carlos Thillet Manager Gas Supply and Transportation PECO Energy Company 2010-11 Reliability Overview

Pennsylvania Public Utility Commission 2010 Annual Winter Reliability Assessment Meeting November 4, 2010 Carlos Thillet Manager Gas Supply and Transportation PECO Energy Company 2010-11 Reliability Overview

Energy Market Fundamentals Update

Energy Market Fundamentals Update 16 January 2019 Gregory.Kosier@Constellation.com 213.996.6116 Quick Introduction Exelon s family of companies represents every stage of the energy value chain. Generation

Energy Market Fundamentals Update 16 January 2019 Gregory.Kosier@Constellation.com 213.996.6116 Quick Introduction Exelon s family of companies represents every stage of the energy value chain. Generation

CenterPoint Energy Services. Current Market Fundamentals June 27, 2013

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

Permian Electricity Market Review & Procurement Strategy

Permian Electricity Market Review & Procurement Strategy Natural Gas Society of Permian Basin Coleman Lewis Power Procurement Supervisor Pioneer Natural Resources Targa Resources March 8, 2016 Agenda Electricity

Permian Electricity Market Review & Procurement Strategy Natural Gas Society of Permian Basin Coleman Lewis Power Procurement Supervisor Pioneer Natural Resources Targa Resources March 8, 2016 Agenda Electricity

ISO New England Gambling with Natural Gas U.S. Power and Gas Weekly.

? ISO New England Gambling with Natural Gas U.S. Power and Gas Weekly. Morningstar Commodities Research 25 January 2018 Dan Grunwald Associate, Power and Gas +1 312 244-7135 daniel.grunwald@morningstar.com

? ISO New England Gambling with Natural Gas U.S. Power and Gas Weekly. Morningstar Commodities Research 25 January 2018 Dan Grunwald Associate, Power and Gas +1 312 244-7135 daniel.grunwald@morningstar.com

New England s Energy Mix: Clean, Diverse, Responsive and Getting Even Better

New England s Energy Mix: Clean, Diverse, Responsive and Getting Even Better ENGIE s Distrigas subsidiary is proud of its 45-year history of supplying New England with LNG a critical component of its energy

New England s Energy Mix: Clean, Diverse, Responsive and Getting Even Better ENGIE s Distrigas subsidiary is proud of its 45-year history of supplying New England with LNG a critical component of its energy

CHP Managing Commodity Price Risk

An Introduction to Combined Heat and Power CHP 100 1 Acknowledgements 2 Overview! High and Volatile Natural Gas Prices do not preclude a good CHP project! Managing Commodity Price Risk must be Part of

An Introduction to Combined Heat and Power CHP 100 1 Acknowledgements 2 Overview! High and Volatile Natural Gas Prices do not preclude a good CHP project! Managing Commodity Price Risk must be Part of

Monday, January 27, :34 PM ET Gas reliance under renewed scrutiny after epic power price spikes

Monday, January 27, 2014 4:34 PM ET Gas reliance under renewed scrutiny after epic power price spikes By Everett Wheeler and Peter Marrin Favored for its relatively low price and economic benefits, natural

Monday, January 27, 2014 4:34 PM ET Gas reliance under renewed scrutiny after epic power price spikes By Everett Wheeler and Peter Marrin Favored for its relatively low price and economic benefits, natural

The Polar Vortex and Future Power System Trends National Coal Council Annual Spring Meeting May 14, 2014

The Polar Vortex and Future Power System Trends National Coal Council -- 2014 Annual Spring Meeting May 14, 2014 Outline Introduction to ICF Overview of the Key Issues Price Volatility During Winter 2014

The Polar Vortex and Future Power System Trends National Coal Council -- 2014 Annual Spring Meeting May 14, 2014 Outline Introduction to ICF Overview of the Key Issues Price Volatility During Winter 2014

ENERGY WATCH Authors: Paul Flemming, Julia Criscuolo, Oliver Kleinbub, José Rotger and Scott Niemann

NORTHEAST POWER MARKETS ENERGY WATCH Authors: Paul Flemming, Julia Criscuolo, Oliver Kleinbub, José Rotger and Scott Niemann In light of recent growth in natural gas production growth and expected costs

NORTHEAST POWER MARKETS ENERGY WATCH Authors: Paul Flemming, Julia Criscuolo, Oliver Kleinbub, José Rotger and Scott Niemann In light of recent growth in natural gas production growth and expected costs

MARKET INTEL NEWSLETTER

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers April 2018 Fuels Natural Gas Coal Oil Power Prompt-month NYMEX natural gas traded in a tight range during

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers April 2018 Fuels Natural Gas Coal Oil Power Prompt-month NYMEX natural gas traded in a tight range during

Texas Natural Gas Prices Plunge To All-Time Low Column: U.S. natural gas prices unmoved by colder winter, low

2.69 2.69 2.68 2.68 2.67 2.67 2.66 2.66 2.65 2.65 2.64 Prior Day s NYMEX MAY-19 Contract (CT) 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19

2.69 2.69 2.68 2.68 2.67 2.67 2.66 2.66 2.65 2.65 2.64 Prior Day s NYMEX MAY-19 Contract (CT) 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19

Ponzi Scheme Keeps US Market Well Supplied

www.poten.com June 30, 2011 Ponzi Scheme Keeps US Market Well Supplied Conjuring up images of the dot-com bubble of the late-1990s, the industry leveled charges of unprofessional journalism against a story

www.poten.com June 30, 2011 Ponzi Scheme Keeps US Market Well Supplied Conjuring up images of the dot-com bubble of the late-1990s, the industry leveled charges of unprofessional journalism against a story

Natural Gas Market Conditions; & Gas & Power In New England

March 13, 2013 Nashua, NH Natural Gas Market Conditions; & Gas & Power In New England Presentation to: Consumer Liaison Working Group Stephen Leahy Northeast Gas Association Topics The Best of Times: natural

March 13, 2013 Nashua, NH Natural Gas Market Conditions; & Gas & Power In New England Presentation to: Consumer Liaison Working Group Stephen Leahy Northeast Gas Association Topics The Best of Times: natural

Outlook for Natural Gas Demand for Winter

Outlook for Natural Gas Demand for 2010-2011 Winter Energy Ventures Analysis, Inc. (EVA) Overview Natural gas demand this winter is projected to be about 295 BCF, or 2.5 percent, above demand levels recorded

Outlook for Natural Gas Demand for 2010-2011 Winter Energy Ventures Analysis, Inc. (EVA) Overview Natural gas demand this winter is projected to be about 295 BCF, or 2.5 percent, above demand levels recorded

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION ARIZONA CORPORATION COMMISSION APRIL 6, 2017 DALE PROBASCO MANAGING DIRECTOR ROGER SCHIFFMAN DIRECTOR

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION ARIZONA CORPORATION COMMISSION APRIL 6, 2017 DALE PROBASCO MANAGING DIRECTOR ROGER SCHIFFMAN DIRECTOR

MARKET INTEL NEWSLETTER

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers August 2018 Fuels Natural Gas Coal Oil Power Natural gas production has been steady during the past month,

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers August 2018 Fuels Natural Gas Coal Oil Power Natural gas production has been steady during the past month,

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

EIA: gas storage design capacity slightly up May NYMEX natural gas futures at $2.674/MMBtu drifts in search of support

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX May-18 Contract (CT) 2.78 2.76 2.74 2.72 2.7 2.68

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX May-18 Contract (CT) 2.78 2.76 2.74 2.72 2.7 2.68

C9-19. Slide 1. markets later in the presentation.

C9-19 Slide 1 Mr. Chairman, Commissioners. Today I am pleased to present the Office of Enforcement's Winter 2011-2012 Energy Market Assessment. The Winter Energy Assessment is staff's opportunity to share

C9-19 Slide 1 Mr. Chairman, Commissioners. Today I am pleased to present the Office of Enforcement's Winter 2011-2012 Energy Market Assessment. The Winter Energy Assessment is staff's opportunity to share

MARKET INTEL NEWSLETTER

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers March 2018 Fuels Natural Gas Coal Oil Power Natural gas production continued its upward momentum in March

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers March 2018 Fuels Natural Gas Coal Oil Power Natural gas production continued its upward momentum in March

Marc de Croisset FBR CAPITAL MARKETS & CO. Coal-to-Gas Switching: Distilling the Issue

Marc de Croisset. 646.885.5423. mdecroisset@fbr.com FBR CAPITAL MARKETS & CO. Coal-to-Gas Switching: Distilling the Issue September 20, 2012 Disclosures Important disclosures can be found at the end of

Marc de Croisset. 646.885.5423. mdecroisset@fbr.com FBR CAPITAL MARKETS & CO. Coal-to-Gas Switching: Distilling the Issue September 20, 2012 Disclosures Important disclosures can be found at the end of

Winter Polar Vortex

been impacted? What do we have to say from a supplier s standpoint? As everyone living in the Northeast and much of the Mid-Atlantic knows, this has been one of the coldest winters east of the Rockies

been impacted? What do we have to say from a supplier s standpoint? As everyone living in the Northeast and much of the Mid-Atlantic knows, this has been one of the coldest winters east of the Rockies

NatGasWeather.com Daily Report

NatGasWeather.com Daily Report Issue Time: 4:55 am EDT Thursday, March 16 th, 2017 1-7 Day Weather Summary (Mar 16-22 nd ): Temperatures will remain a bit cold today over the eastern US, although with

NatGasWeather.com Daily Report Issue Time: 4:55 am EDT Thursday, March 16 th, 2017 1-7 Day Weather Summary (Mar 16-22 nd ): Temperatures will remain a bit cold today over the eastern US, although with

Electricity Price Outlook for December By John Howley Senior Economist

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Electricity Price Outlook for December 2017 By John Howley Senior Economist Office of Technical and Regulatory Analysis

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Electricity Price Outlook for December 2017 By John Howley Senior Economist Office of Technical and Regulatory Analysis

Acceptance Natural Gas Demand to Stay High on Cold Weather Forecast

Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.68 2.67 2.66 2.65 2.64 2.63

Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.68 2.67 2.66 2.65 2.64 2.63

New York CES: Renewable Energy Standard Underlying Fundamentals

New York CES: Renewable Energy Standard Underlying Fundamentals Roman Kramarchuk EMA Roundtable Managing Director Global Power, Emissions & Clean Energy February 2, 2017 Why we re different WE TAKE THE

New York CES: Renewable Energy Standard Underlying Fundamentals Roman Kramarchuk EMA Roundtable Managing Director Global Power, Emissions & Clean Energy February 2, 2017 Why we re different WE TAKE THE

ERCOT Summer Reset U.S. Power and Gas Weekly

? ERCOT Summer Reset U.S. Power and Gas Weekly Morningstar Commodities Research 18 July 2018 Dan Grunwald Associate, Power and Gas +1 312 244-7135 daniel.grunwald@morningstar.com Data Sources Used in This

? ERCOT Summer Reset U.S. Power and Gas Weekly Morningstar Commodities Research 18 July 2018 Dan Grunwald Associate, Power and Gas +1 312 244-7135 daniel.grunwald@morningstar.com Data Sources Used in This

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond August 14th, 2012 On behalf of: for: 1 BENTEK Energy Market Information Agenda: U.S. Supply, Demand and Storage Outlook Macro

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond August 14th, 2012 On behalf of: for: 1 BENTEK Energy Market Information Agenda: U.S. Supply, Demand and Storage Outlook Macro

$40 Billion Ichthys LNG Project Begins Gas Exports US' Range Resources to fill Rover gas pipeline volumes by yearend; processing ramps up

Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: O C T O B E R 2 5, 2 1 8 3.26 3.24 3.22 3.2 3.18 3.16 3.14 3.12 3.1

Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: O C T O B E R 2 5, 2 1 8 3.26 3.24 3.22 3.2 3.18 3.16 3.14 3.12 3.1

ENERGY MARKET UPDATE October 9, 2014

ENERGY MARKET UPDATE October 9, 2014 Winter is Right Around the Corner Are You Ready? Six months ago one of the most brutal winters on record in the US was winding down. Many energy consumers, who had

ENERGY MARKET UPDATE October 9, 2014 Winter is Right Around the Corner Are You Ready? Six months ago one of the most brutal winters on record in the US was winding down. Many energy consumers, who had

NORTHEAST POWER MARKETS E NERGY WATCH. Authors: Paul Flemming, Scott Niemann, Julia Criscuolo, and José Rotger

NORTHEAST POWER MARKETS E NERGY WATCH Authors: Paul Flemming, Scott Niemann, Julia Criscuolo, and José Rotger EXECUTIVE SUMMARY In this issue of Energy Watch, ESAI Power discusses the energy margin outlook

NORTHEAST POWER MARKETS E NERGY WATCH Authors: Paul Flemming, Scott Niemann, Julia Criscuolo, and José Rotger EXECUTIVE SUMMARY In this issue of Energy Watch, ESAI Power discusses the energy margin outlook

Market Outlook & Price Projections: Corn, Wheat, Soy Complex & Palm Oil October 7 th, 2016

Market Outlook & Price Projections: Corn, Wheat, Soy Complex & Palm Oil October 7 th, 2016 Patrick Sparks Global Risk Management, Inc. psparks@grmcorp.com 651-209-9503 www.grmcorp.com 1 Commodity trading

Market Outlook & Price Projections: Corn, Wheat, Soy Complex & Palm Oil October 7 th, 2016 Patrick Sparks Global Risk Management, Inc. psparks@grmcorp.com 651-209-9503 www.grmcorp.com 1 Commodity trading

NORTHERN UTILITIES, INC. NEW HAMPSHIRE DIVISION ANNUAL COST OF GAS ADJUSTMENT FILING PREFILED TESTIMONY OF FRANCIS X.

NORTHERN UTILITIES, INC. NEW HAMPSHIRE DIVISION ANNUAL 0-0 COST OF GAS ADJUSTMENT FILING PREFILED TESTIMONY OF FRANCIS X. WELLS Prefiled Testimony of Francis X. Wells Annual 0-0 COG Filing Page of I. INTRODUCTION

NORTHERN UTILITIES, INC. NEW HAMPSHIRE DIVISION ANNUAL 0-0 COST OF GAS ADJUSTMENT FILING PREFILED TESTIMONY OF FRANCIS X. WELLS Prefiled Testimony of Francis X. Wells Annual 0-0 COG Filing Page of I. INTRODUCTION

The Public Need for Gas/Electric Coordination

Pennsylvania Independent Oil & Gas Association May 14, 2014 The Public Need for Gas/Electric Coordination Richard Kruse, VP Regulatory Spectra Energy Our Strong Portfolio of Assets Natural Gas Transmission

Pennsylvania Independent Oil & Gas Association May 14, 2014 The Public Need for Gas/Electric Coordination Richard Kruse, VP Regulatory Spectra Energy Our Strong Portfolio of Assets Natural Gas Transmission

ExxonMobil Resumes Liquefied Natural Gas Production in Papua New Guinea Commodities - Natural Gas Futures Turn Higher After Storage

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.71 2.7 2.69 2.68 2.67 2.66

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.71 2.7 2.69 2.68 2.67 2.66

Natural Gas Trends LNG 17 NYC, June 28, 2011

Bureau of Economic Geology, The University of Texas at Austin Natural Gas Trends LNG 17 NYC, June 28, 211 Balancing Our Energy Future What do we want? Safe, clean, affordable, (abundant) energy Reduced

Bureau of Economic Geology, The University of Texas at Austin Natural Gas Trends LNG 17 NYC, June 28, 211 Balancing Our Energy Future What do we want? Safe, clean, affordable, (abundant) energy Reduced

Overview. Market Alert. Back in the Black: Coal Makes Comeback. Figure 1 - Coal Stockpiles at Power Plants Key Takeaways

May 21, 2014 Market Alert Back in the Black: Coal Makes Comeback Contact: Michael Bennett, mbennett@bentekenergy.com Rocco Canonica, rcanonica@bentekenergy.com Figure 1 - Coal Stockpiles at Power Plants

May 21, 2014 Market Alert Back in the Black: Coal Makes Comeback Contact: Michael Bennett, mbennett@bentekenergy.com Rocco Canonica, rcanonica@bentekenergy.com Figure 1 - Coal Stockpiles at Power Plants

Wyoming Pipeline Authority Public Meeting. Anne Swedberg, Manager, North American Power and Gas Content

Wyoming Pipeline Authority Public Meeting Anne Swedberg, Manager, North American Power and Gas Content 2015 2014 Platts, McGraw Hill Financial. All rights reserved. Benposium 2015. Key Take-Aways US production

Wyoming Pipeline Authority Public Meeting Anne Swedberg, Manager, North American Power and Gas Content 2015 2014 Platts, McGraw Hill Financial. All rights reserved. Benposium 2015. Key Take-Aways US production

Forecasts and Assumptions for IRP. Prepared for PNM September 2016

Forecasts and Assumptions for IRP Prepared for PNM September 2016 Answers for infrastructure and cities. Pace Global Disclaimer This Report was produced by Pace Global, a Siemens business ( Pace Global

Forecasts and Assumptions for IRP Prepared for PNM September 2016 Answers for infrastructure and cities. Pace Global Disclaimer This Report was produced by Pace Global, a Siemens business ( Pace Global

The Top Natural Gas Players In ExxonMobil restarts second PNG LNG train; resumes export

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX May-18 Contract (CT) 2.82 2.81 2.8 2.79 2.78 2.77

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX May-18 Contract (CT) 2.82 2.81 2.8 2.79 2.78 2.77

MARKET INTEL NEWSLETTER

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers February 2018 Fuels Natural Gas Coal Oil Power Intense arctic air in January decided warm up in February

Constellation s MARKET INTEL NEWSLETTER Energy Market Update for Commercial & Industrial Customers February 2018 Fuels Natural Gas Coal Oil Power Intense arctic air in January decided warm up in February

2005 North American Natural Gas Outlook Client Presentation

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

Regional Market Update

March 14, 2014 Providence, RI Regional Market Update Presentation to: NGA Sales & Marketing Conference Thomas Kiley Northeast Gas Association Continued on NGA web site http://www.northeastgas.org/about-nga/antitrust-guidelines

March 14, 2014 Providence, RI Regional Market Update Presentation to: NGA Sales & Marketing Conference Thomas Kiley Northeast Gas Association Continued on NGA web site http://www.northeastgas.org/about-nga/antitrust-guidelines

Seminole Electric proposes $727M natural gas plant In Bad Trade Off, New England Forsakes Natural Gas For Petroleum

Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: D E C E M B E R 2 8, 2 1 7 Prior Day s NYMEX Jan-18 Contract (CT) 2.78

Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: D E C E M B E R 2 8, 2 1 7 Prior Day s NYMEX Jan-18 Contract (CT) 2.78

Substantial Changes Ahead for MISO North Michigan Impacts 2018 MMEA Fall Conference

Substantial Changes Ahead for MISO North Michigan Impacts 2018 MMEA Fall Conference Mike Zenker, Managing Director of Market Analysis NextEra Energy Resources September 13, 2018 2 3 The Following Information

Substantial Changes Ahead for MISO North Michigan Impacts 2018 MMEA Fall Conference Mike Zenker, Managing Director of Market Analysis NextEra Energy Resources September 13, 2018 2 3 The Following Information

IMPACT OF CLOSING NAVAJO GENERATING STATION ON ARIZONA POWER MARKETS

IMPACT OF CLOSING NAVAJO GENERATING STATION ON ARIZONA POWER MARKETS Prepared for: Arizona Corporation Commission Mr. Seth Schwartz President schwartz@evainc.com August 2018 Energy Ventures Analysis 1901

IMPACT OF CLOSING NAVAJO GENERATING STATION ON ARIZONA POWER MARKETS Prepared for: Arizona Corporation Commission Mr. Seth Schwartz President schwartz@evainc.com August 2018 Energy Ventures Analysis 1901

Meeting Natural Gas/Electricity Challenges in New England

N O V E M B E R 1, 2 0 1 3 W A S H I N G T O N, D C Meeting Natural Gas/Electricity Challenges in New England 2013-2014 Winter Energy Outlook Eric Johnson D I R E C T O R, E X T E R N A L A F F A I R S

N O V E M B E R 1, 2 0 1 3 W A S H I N G T O N, D C Meeting Natural Gas/Electricity Challenges in New England 2013-2014 Winter Energy Outlook Eric Johnson D I R E C T O R, E X T E R N A L A F F A I R S

Black Hills Corp proposes 35-mile natural gas pipeline to supply central Wyoming Proposed natural gas plant in Superior dealt setback in

Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Aug-18 Contract (CT) 2.91 2.9 2.89 2.88 2.87 2.86

Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Aug-18 Contract (CT) 2.91 2.9 2.89 2.88 2.87 2.86

Access Northeast: Meeting New England s Energy Needs. Acushnet LNG Advisory Committee June 7, 2016

Access Northeast: Meeting New England s Energy Needs Acushnet LNG Advisory Committee June 7, 2016 Spectra Energy s Facilities in New England Maritimes & Northeast US Approximately 350 miles of pipeline

Access Northeast: Meeting New England s Energy Needs Acushnet LNG Advisory Committee June 7, 2016 Spectra Energy s Facilities in New England Maritimes & Northeast US Approximately 350 miles of pipeline

MACRO OVERVIEW OF DESERT SOUTHWEST POWER MARKET - CHALLENGES AND OPPORTUNITIES

Power Task Force Agenda Number 4. MACRO OVERVIEW OF DESERT SOUTHWEST POWER MARKET - CHALLENGES AND OPPORTUNITIES CENTRAL ARIZONA PROJECT POWER TASK FORCE MEETING MAY 18, 2017 DALE PROBASCO MANAGING DIRECTOR

Power Task Force Agenda Number 4. MACRO OVERVIEW OF DESERT SOUTHWEST POWER MARKET - CHALLENGES AND OPPORTUNITIES CENTRAL ARIZONA PROJECT POWER TASK FORCE MEETING MAY 18, 2017 DALE PROBASCO MANAGING DIRECTOR

2015 The Coal Institute Spring Conference. Swati Daji, SVP Fuels and System Optimization

2015 The Coal Institute Spring Conference Swati Daji, SVP Fuels and System Optimization CAUTION REGARDING PRESENTATION INFORMATION AND FORWARD-LOOKING STATEMENTS Duke Energy, its subsidiaries and affiliates,

2015 The Coal Institute Spring Conference Swati Daji, SVP Fuels and System Optimization CAUTION REGARDING PRESENTATION INFORMATION AND FORWARD-LOOKING STATEMENTS Duke Energy, its subsidiaries and affiliates,