Peru Field Trip September 2010

|

|

|

- Dorthy Roberts

- 6 years ago

- Views:

Transcription

1 Peru Field Trip September 2010 PERU LNG Antonio Díaz LNG Director Perú

2 2 Disclaimer ALL RIGHTS ARE RESERVED REPSOL YPF, S.A Repsol YPF, S.A. is the exclusive owner of this document. No part of this document may be reproduced (including photocopying), stored, duplicated, copied, distributed or introduced into a retrieval system of any nature or transmitted in any form or by any means without the prior written permission of Repsol YPF, S.A. This document contains statements that Repsol YPF believes constitute forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of These forward-looking statements may include statements regarding the intent, belief, or current expectations of Repsol YPF and its management, including statements with respect to trends affecting Repsol YPF s financial condition, financial ratios, results of operations, business, strategy, geographic concentration, production volume and reserves, as well as Repsol YPF s plans, expectations or objectives with respect to capital expenditures, business, strategy, geographic concentration, costs savings, investments and dividend payout policies. These forward-looking statements may also include assumptions regarding future economic and other conditions, such as future crude oil and other prices, refining and marketing margins and exchange rates. These statements are not guarantees of future performance, prices, margins, exchange rates or other events and are subject to material risks, uncertainties, changes and other factors which may be beyond Repsol YPF s control or may be difficult to predict. Repsol YPF s future financial condition, financial ratios, results of operations, business, strategy, geographic concentration, production volumes, reserves, capital expenditures, costs savings, investments and dividend payout policies, as well as future economic and other conditions, such as future crude oil and other prices, refining margins and exchange rates, could differ materially from those expressed or implied in any such forward-looking statements. Important factors that could cause such differences include, but are not limited to, oil, gas and other price fluctuations, supply and demand levels, currency fluctuations, exploration, drilling and production results, changes in reserves estimates, success in partnering with third parties, loss of market share, industry competition, environmental risks, physical risks, the risks of doing business in developing countries, legislative, tax, legal and regulatory developments, economic and financial market conditions in various countries and regions, political risks, wars and acts of terrorism, natural disasters, project delays or advancements and lack of approvals, as well as those factors described in the filings made by Repsol YPF and its affiliates with the Comisión Nacional del Mercado de Valores in Spain, the Comisión Nacional de Valores in Argentina, and the Securities and Exchange Commission in the United States; in particular, those described in Section 1.3 Key information about Repsol YPF Risk Factors and Section 3 Operating and Financial Review and Prospects in Repsol YPF s Annual Report on Form 20-F for the fiscal year ended December 31, 2009 filed with the US Securities and Exchange Commission and in Section I Risk factors in Repsol YPF s Registration Document filed with the Comisión Nacional del Mercado de Valores in Spain in April Both documents are available on Repsol YPF s website ( In light of the foregoing, the forward-looking statements included in this document may not occur. Repsol YPF does not undertake to publicly update or revise these forward-looking statements even if experience or future changes make it clear that the projected performance, conditions or events expressed or implied therein will not be realized. This document does not constitute an offer to purchase, subscribe, sale or exchange of Repsol YPF's or YPF Sociedad Anonima's respective ordinary shares or ADSs in the United States or otherwise. Repsol YPF's and YPF Sociedad Anonima's respective ordinary shares and ADSs may not be sold in the United States absent registration or an exemption from registration under the US Securities Act of 1933, as amended.

3 3 Agenda Repsol LNG business highlights PERU LNG

Europe USA Latin")

4 4 Repsol in the LNG Value Chain Production Liquefaction Shipping Regas & Transport Market E&P: Gas Production LNG Production Marketing & Transport LNG Regasification NG Commercialization 30% T&T 10% Peru 22.5% ALNG 1,2,3 and 4 20% PERU LNG Off-take: ALNG 2,3 and 4 (28%) PERU LNG (100%) Shipping capacity: 75% Canaport (100% capacity) Europe USA Latin America 11 LNG Carriers Upstream Midstream Downstream

5 5 Repsol s LNG commercial flows Canada Spain Mexico Far East Panama Canal (2014) T&T Peru Argentina Regas capacity Liquefaction capacity Long Term Flows Short Term / Spot Flows

FID: 2007 Production: 75 kboe/d FID: 2006 Production: 121 kboe/d Canaport Start-up: 3Q 2009 Capacity: 10 Bcma Peru LNG")

6 Strong pipeline of Upstream and LNG Projects US GoM Buckskin Shenzi (US GoM) Kinteroni (Peru) Carabobo (Venezuela) FID Pending (2012) Production: 400 kboe/d Carioca (Brazil) Shenzi G-104 & Shenzi-8: increase the potential of the current fields and the North flank I/R (Libya) FID: 2007 Production: 75 kboe/d FID: 2006 Production: 121 kboe/d Canaport Start-up: 3Q 2009 Capacity: 10 Bcma Peru LNG Start-up: 2Q 2010 Capacity: 6 Bcma FID: 2009 Production: 40 kboe/d Margarita Huacaya (Bolivia) FID Pending (2010) Production: 86 kboe/d Guará (Brazil) FID Pending (2010) Production: 250 kboe/d Reggane (Algeria) FID: 2009 Production: 8 Mm 3 /d Cardon IV (Venezuela) FID Pending (2011) Production: 8 Mm 3 /d in 2014 FID Pending (2011) Production: 110 kboe/d Piracucá (Brazil) FID Pending (2011) Production: 25 kboe/d Brazil Abaré, Abaré West & Iguazú in BM-S-9 Panoramix: new discovery in BM-S-48 Morocco Tangier-Larache, first discovery success in Moroccan offshore Sierra Leone & West Africa Venus B-1, first offshore discovery in an unexplored area Start up beyond Note: All production figures indicate gross plateau production Liquids Gas LNG 6

7 7 Agenda Repsol LNG business highlights PERU LNG

DOMESTIC MARKET (NGs & LPGs) LIQUEFACTION LNG COMMERCIALIZATION")

8 8 Repsol s Natural Gas Value Chain in Perú UPSTREAM (Exploration & Production) PIPELINE TRANSPORT (NGs & LPGs) DOMESTIC MARKET (NGs & LPGs) LIQUEFACTION LNG COMMERCIALIZATION Production (gross): NG: 28.3 Mm3/d NGL: 85 Kbopd Pipeline lengths Liquid line: 535 km Gas Line: 715 km Repsol s Partners Hunt Oil SK Corporation Pluspetrol Petrobras Sonatrach Tecpetrol Repsol s Partners Hunt Oil SK Corporation Pluspetrol Sonatrach Tecpetrol Perú Tractebel Graña y Montero PERU LNG Partners Hunt Oil 50% SK Corporation 20% Marubeni 10% Repsol 20% OFF TAKE: 100% Repsol

9 9 Historical Summary First Cargo 22/06 Manzanillo Start up. Financial Close SPA signing with CFE ( Manzanillo) 2005 Agreements with Hunt/ PERULNG With Hunt: Presence in Upstream. Access to Gas Transporting. Participation in PERU LNG. With PERU LNG: 100% Offtaker of LNG production.

10 10 Integrated Project CAMISEA: Blocks 56 & 88 Treatment Plants PAGORENI Block 56 SAN MARTIN CASHIRIARI Block 88 PERU LNG: Liquefaction Plant Marine Terminal Pipeline Malvinas Lima Pipelines PERU LNG Cusco Pisco TGP: Gas Pipeline Liquids Pipeline PERU

11 11 Pipeline Pipeline from Chiquintirca to Pampa Melchorita Construction Contractor: Techint.

12 12 Plant Overview LNG Plant Nominal Capacity : 4.45 Mtpa. Technology : Air Products. LNG Storage capacity: 2 x 130,000 m 3 tanks EPC Contractor: CB&I Marine Terminal Facility capable of receiving LNG Carriers up to 175,000 m km jetty with loading platform and ships dock 800m breakwater EPC Contractor: CDB Consortium (Saipem, Odebrecht and Jan De Nul)

13 13 Project Execution The project objectives were all successfully achieved : Safety Minimum environmental impact. On schedule Within budget. 5,000 CB&I employees on Process area (octubre-09)

and 60 Medical Aids during the whole project. Incident Rate & targets Driving Incident Rate Recordable Incident Rate Lost Time Incident Rate Project 1.93 0.22 0.")

14 14 Safety Industry Standards and PERU LNG objectives have been surpassed. More than 66 million man hours worked. More than 36 million kilometers driven. Only 14 LTI (Lost Time Incidents) and 60 Medical Aids during the whole project. Incident Rate & targets Driving Incident Rate Recordable Incident Rate Lost Time Incident Rate Project Project Target < base 200,000 HH

15 15 Project Schedule May Jun Jul Ago Sept Oct Nov Dec Construction RLFC (16th June) Contractual RLFC (28th May) Commissioning & Start Up First Shipment 22nd June Operation Initial Period Commercial Period Notes: FID: 22nd Dec, Commissioning Started: Feb Initial Period: ~ 4 months. Comercial Period: 18 years RLFC (Ready to Load First Cargo) Commercial Operations Date

16 Cargos and LNG Production 16

17 17 Environmental and Social Responsibility Community relations Agriculture and livestock programs Capacity building programs Health support Educational support Environmental monitoring and biodiversity conservation Archaeological monitoring program Employment generation

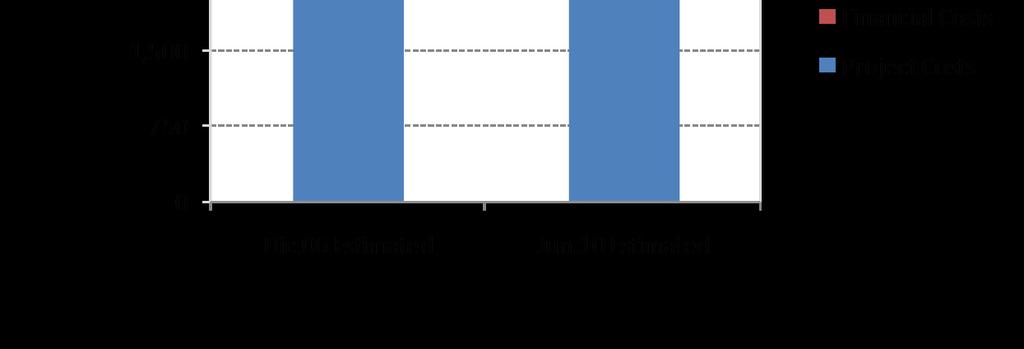

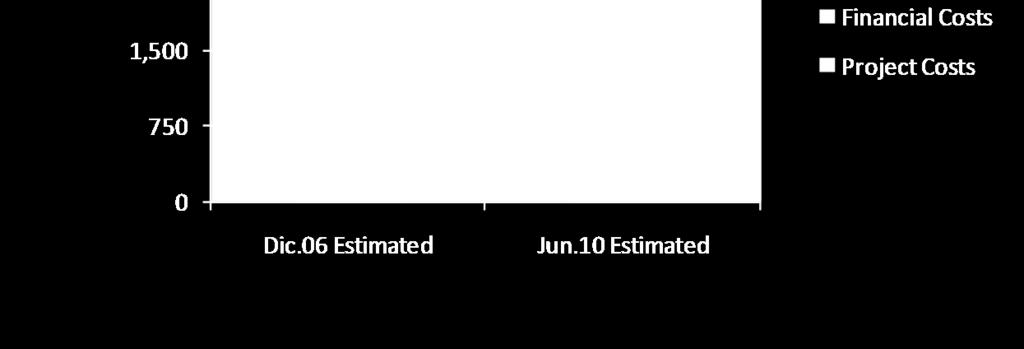

18 18 Total Project Budget -3%

")

19 19 Project External Financing External Financing ( MUS$) Multilateral Agencies 2,050 Local Bonds 200 Total External Financing : MUS$ 2,250

Master Transportation Agreement (MTA) Sales Purchase")

20 20 Project Structure Contractual Framework Investment Agreement GoP / PERU LNG Gas Supply Agreement (GSA) Master Transportation Agreement (MTA) Sales Purchase Agreement (SPA) Camisea / PERU LNG 4.2 TCF Reserves dedicated in Camisea Term: 18 years TgP / PERU LNG Firm Contract 620 M SCFD Term: 23 years. Option18 years. PERU LNG / Repsol Comercializadora FOB ACQ: 218 Tbtu / year. Term: 18 years. Article 62 of the constitution: Laws or legal disposition of any class cannot modify contractual terms.

21 21 Recent GoP Decrees The government of Peru has recently issued two Supreme Decrees instructing Perupetro to renegotiate the License Contracts of blocks 56 and 88 with the aim of: Guaranteeing that the minimum royalties paid for the gas exported will be at least equal to the average of the domestic market The reserves of the block 88 will be fully dedicated to the domestic market. Possible impact to Peru LNG: The License Contracts are protected by the constitution of Peru. They can not be modified by Supreme Decrees, only by mutual agreement. Peru LNG has no obligation to accept a pass-through of any modification by mutual agreement of the license contracts.

22 22 Repsol s Natural Gas Value Chain in Perú UPSTREAM (Exploration & Production) PIPELINE TRANSPORT (NGs & LPGs) DOMESTIC MARKET (NGs & LPGs) LIQUEFACTION LNG COMMERCIALIZATION Production (gross): NG: 28.3 Mm3/d NGL: 85 Kbopd Pipeline lengths Liquid line: 535 km Gas Line: 715 km Repsol s Partners Hunt Oil SK Corporation Pluspetrol Petrobras Sonatrach Tecpetrol Repsol s Partners Hunt Oil SK Corporation Pluspetrol Sonatrach Tecpetrol Perú Tractebel Graña y Montero PERU LNG Partners Hunt Oil 50% SK Corporation 20% Marubeni 10% OFF TAKE: 100% Repsol

Repsol: 100% Off-take CFE SPA Term: 15 years DES Manzanillo.")

23 23 Available Volumes from Peru LNG Plant production volume: 6 Bcma (4.4 Mtpa) Repsol: 100% Off-take CFE SPA Term: 15 years DES Manzanillo. Short / Mid Term volumes Possible excess Quantities (0.19 bcma) Long Term Non committed volumes (1.46bcma)

24 24 PERU LNG Fleet and Commercialization Round trip days CANAPORT 9,628 nm SPAIN COSTA AZUL 21 3,700 nm MANZANILLO 2,586 nm ,614 nm FAR EAST 9,700 nm PERÚ LNG CAMISEA 4,2 MTPA 2 x 130,000 m 3

25 25 Arbitrage Opportunities Source: Platts Potential to obtain very attractive margins in sales of the excess volumes to Far East and Europe

26 Project Pictures MCHE transportation 26

; temporary electrical")

27 Project Pictures Camp site (partial); temporary electrical generation 27

28 Project Pictures Spool manufacturing workshops 28

29 Project Pictures Construction site (Feb 2008) 29

30 Project Pictures Construction site (Apr 2008) 30

31 Project Pictures Construction site (Sept 2008) 31

32 Project Pictures Construction site (Sept 2008) 32

33 Project Pictures Construction site (Sept 2008) 33

34 Project Pictures Construction site (Sept 2008) 34

35 Project Pictures Construction site (March 2009) 35

")

36 Project Pictures LNG tanks construction (March 2009) 36

37 Project Pictures Marine works (March 2009) 37

38 Project Pictures Marine works (September 2009) 38

39 Project Pictures Construction site (July 2009) 39

40 Project Pictures Construction site (July 2009) 40

41 Project Pictures Construction site (July 2009) 41

42 Project Pictures Construction site (Sept 2009) 42

43 Project Pictures Pipeline 43

44 Project Pictures Pipeline 44

45 Pipeline Golden weld 45

46 Vessel: Barcelona Knutsen 46

47 Dedication Ceremony Pampa Melchorita 47

48 Dedication Ceremony Lima Art Museum 48

49 49 Summary You are visiting the most recently started up LNG plant. Peru LNG has been an outstanding project. Constitutional guarantee for contracts. The LNG purchase contract is very important for Repsol, not only in terms of volume, but allowing us to have access to new markets. High value of the Repsol SPA due to the free destination and the arbitrage opportunities.

50 Peru Field Trip September 2010 PERU LNG Antonio Díaz LNG Director Perú

51 Peru Field Trip September 2010 PERU LNG Carlos López Deputy General Manager PERU LNG

52 52 Gas Liquefaction Process MEASUREMENT & CONDITIONING F/G ATM DRYING F/G ACID GAS ELIMINATION LIQUIDS F/G LOADING ARMS WATER M.C.H.E

53 53 Plant Overview LNG Tanks LNG Jetty & Breakwater Gas Conditioning Air Coolers Metering Facilities MCHE Compressors Power Generators

54 54 Plant Tour 1 Conference Room Jetty 2 2 South Side 3 3 North Side

55 Peru Field Trip September 2010 PERU LNG Carlos López Deputy General Manager PERU LNG

56 56 Pipeline World s highest pipeline Monitoreo de la erosión en la playa

57 Pipeline Extremely hard conditions 57

58 Plant 58

59 Marine Terminal 59

DISCLAIMER Forward Looking Statements ALL RIGHTS ARE RESERVED REPSOL YPF, S.A. 2012 Repsol YPF, S.A. Repsol is the exclusive owner of this document. No part of this document may be reproduced (including

DISCLAIMER Forward Looking Statements ALL RIGHTS ARE RESERVED REPSOL YPF, S.A. 2012 Repsol YPF, S.A. Repsol is the exclusive owner of this document. No part of this document may be reproduced (including

REPSOL STARTS UP ITS FIRST GAS LIQUEFACTION PLANT IN LATIN AMERICA

Tel. 91 753 87 87 Press release Madrid, June 10 th 2010 5 pages Antonio Brufau and Alan Garcia inaugurate a new LNG plant in Pampa Melchorita (Peru). REPSOL STARTS UP ITS FIRST GAS LIQUEFACTION PLANT IN

Tel. 91 753 87 87 Press release Madrid, June 10 th 2010 5 pages Antonio Brufau and Alan Garcia inaugurate a new LNG plant in Pampa Melchorita (Peru). REPSOL STARTS UP ITS FIRST GAS LIQUEFACTION PLANT IN

The Camisea Project. San Martín Cashiriari Total Source: DeGolyer & MacNaughton, March 1999

The Camisea Project The Camisea Fields During the period 1981 1987, Royal Dutch Shell conducted exploratory works in a 2 million hectares block in the Ucayali Basin through the execution of 3,000 kilometers

The Camisea Project The Camisea Fields During the period 1981 1987, Royal Dutch Shell conducted exploratory works in a 2 million hectares block in the Ucayali Basin through the execution of 3,000 kilometers

LNG FROM COLOMBIA Platts 13 th Annual Caribbean Energy Jan 24 th 2013

LNG FROM COLOMBIA Platts 13 th Annual Caribbean Energy Jan 24 th 2013 FORWARD LOOKING STATEMENT All monetary amounts are in U.S. dollars unless otherwise stated. This presentation contains forward-looking

LNG FROM COLOMBIA Platts 13 th Annual Caribbean Energy Jan 24 th 2013 FORWARD LOOKING STATEMENT All monetary amounts are in U.S. dollars unless otherwise stated. This presentation contains forward-looking

REPSOL YPF RAISES ITS HYDROCARBONS RESERVES AND RESOURCES ESTIMATE IN THE VACA MUERTA PLAY TO BILLION BARRELS OF OIL EQUIVALENT (Bboe)

") Official Notice Paseo de la Castellana, 278-280 28046 Madrid España Tel. 34 917 538 100 34 917 538 000 Fax 34 913 489 494 www.repsol.com Madrid, February 8 th, 2012 According to the assesment carried out

Official Notice Paseo de la Castellana, 278-280 28046 Madrid España Tel. 34 917 538 100 34 917 538 000 Fax 34 913 489 494 www.repsol.com Madrid, February 8 th, 2012 According to the assesment carried out

PLATTS LNG CONFERENCE HOUSTON, TX. February 2017

PLATTS LNG CONFERENCE HOUSTON, TX February 2017 AES Corporation: A Global Leading Power Company Safe Harbor Disclosure Certain statements in the following presentation regarding AES business operations

PLATTS LNG CONFERENCE HOUSTON, TX February 2017 AES Corporation: A Global Leading Power Company Safe Harbor Disclosure Certain statements in the following presentation regarding AES business operations

Promoting transparency and trust by strengthening community E&S monitoring. PERU LNG s Pipeline Participatory Monitoring Program

1 Promoting transparency and trust by strengthening community E&S monitoring PERU LNG s Pipeline Participatory Monitoring Program PERU LNG Peruvian company formed by Hunt Oil Company (50%), SK (20%), Repsol-YPF

1 Promoting transparency and trust by strengthening community E&S monitoring PERU LNG s Pipeline Participatory Monitoring Program PERU LNG Peruvian company formed by Hunt Oil Company (50%), SK (20%), Repsol-YPF

SUEZ LNG NA: A Leading Player in the U.S. LNG Market. Clay Harris, CEO of SUEZ LNG NA LLC May 30,2007

SUEZ LNG NA: A Leading Player in the U.S. LNG Market Clay Harris, CEO of SUEZ LNG NA LLC May 30,2007 Disclaimer Important Information This communication does not constitute an offer to sell or the solicitation

SUEZ LNG NA: A Leading Player in the U.S. LNG Market Clay Harris, CEO of SUEZ LNG NA LLC May 30,2007 Disclaimer Important Information This communication does not constitute an offer to sell or the solicitation

CHENIERE ENERGY, INC. Louisiana Energy Conference. June 2016

CHENIERE ENERGY, INC. Louisiana Energy Conference June 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within

CHENIERE ENERGY, INC. Louisiana Energy Conference June 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within

LNG Impact on U.S. Domestic Natural Gas Markets

LNG Impact on U.S. Domestic Natural Gas Markets Disclaimer This presentation contains statements about future events and expectations that can be characterized as forward-looking statements, including,

LNG Impact on U.S. Domestic Natural Gas Markets Disclaimer This presentation contains statements about future events and expectations that can be characterized as forward-looking statements, including,

LNG market developments. 12 th of February 2015 Jonathan Raes development EXMAR LNG Infrastructure

LNG market developments 12 th of February 2015 Jonathan Raes development EXMAR LNG Infrastructure Introduction EXMAR & LNG EXMAR Company Introduction Shipping & Energy Infrastructure Provider 1829 shipbuilding

LNG market developments 12 th of February 2015 Jonathan Raes development EXMAR LNG Infrastructure Introduction EXMAR & LNG EXMAR Company Introduction Shipping & Energy Infrastructure Provider 1829 shipbuilding

Chevron Australasia Overview

Chevron Australasia Overview Roy Krzywosinski, Managing Director June 2011 Cautionary Statement CAUTIONARY STATEMENTS RELEVANT TO FORWARD-LOOKING INFORMATION FOR THE PURPOSE OF SAFE HARBOR PROVISIONS OF

Chevron Australasia Overview Roy Krzywosinski, Managing Director June 2011 Cautionary Statement CAUTIONARY STATEMENTS RELEVANT TO FORWARD-LOOKING INFORMATION FOR THE PURPOSE OF SAFE HARBOR PROVISIONS OF

TRINIDAD AND TOBAGO ENERGY CONFERENCE JANUARY 2017

BY TRINIDAD AND TOBAGO ENERGY CONFERENCE JANUARY 2017 *No. of unique client sites Independent and neutral insight. The Rystad Energy business data solution is global. 400 350 300 250 200 150 100 50 0 2010

BY TRINIDAD AND TOBAGO ENERGY CONFERENCE JANUARY 2017 *No. of unique client sites Independent and neutral insight. The Rystad Energy business data solution is global. 400 350 300 250 200 150 100 50 0 2010

ON LIQUEFIED NATURAL GAS (LNG 17) 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17)

17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17)") 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) HOW TO DEVELOP AN ECONOMICAL SMALL CAPACITY FLOATING

17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) HOW TO DEVELOP AN ECONOMICAL SMALL CAPACITY FLOATING

The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports.

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

UPSTREAM PERSPECTIVE ON INDONESIA GAS SUPPLY DEMAND. Jean-Francois Hery Head of Commercial Division

Marc Roussel / Total UPSTREAM PERSPECTIVE ON INDONESIA GAS SUPPLY DEMAND Jean-Francois Hery Head of Commercial Division DISCLAIMER This presentation may include forward-looking statements within the meaning

Marc Roussel / Total UPSTREAM PERSPECTIVE ON INDONESIA GAS SUPPLY DEMAND Jean-Francois Hery Head of Commercial Division DISCLAIMER This presentation may include forward-looking statements within the meaning

An Insight on the Brazilian Gas Industry Challenges. 2 nd Joint Meeting of WOC1 and PGC A - IGU Rio de Janeiro, Feb 19th 2013

An Insight on the Brazilian Gas Industry Challenges 2 nd Joint Meeting of WOC1 and PGC A - IGU Rio de Janeiro, Feb 19th 2013 Total: a worldwide presence Key figures of the Group: More than 90 years of

An Insight on the Brazilian Gas Industry Challenges 2 nd Joint Meeting of WOC1 and PGC A - IGU Rio de Janeiro, Feb 19th 2013 Total: a worldwide presence Key figures of the Group: More than 90 years of

GNL Mejillones, GenCo oriented

GNL Mejillones, GenCo oriented Jean-Michel Cabanes CEO congreso internacional Cigré tuturos desafíos para el sector eléctrico chileno Santiago, November 23 rd, 2015 key issues for flexibility 1. multi-service

GNL Mejillones, GenCo oriented Jean-Michel Cabanes CEO congreso internacional Cigré tuturos desafíos para el sector eléctrico chileno Santiago, November 23 rd, 2015 key issues for flexibility 1. multi-service

Alaska South Central LNG (SCLNG) Project

Project") Alaska South Central LNG (SCLNG) Project Overview for Alaska Legislators February, 2013 - Overview BP, ConocoPhillips, ExxonMobil and TransCanada are working together to progress an Alaska LNG project:

Alaska South Central LNG (SCLNG) Project Overview for Alaska Legislators February, 2013 - Overview BP, ConocoPhillips, ExxonMobil and TransCanada are working together to progress an Alaska LNG project:

Navios South American Logistics Inc. Company Presentation

Navios South American Logistics Inc. Company Presentation April 2013 Forward Looking Statements This presentation contains forward-looking statements (as defined in Section 27A of the Securities Act of

Navios South American Logistics Inc. Company Presentation April 2013 Forward Looking Statements This presentation contains forward-looking statements (as defined in Section 27A of the Securities Act of

World s first LNG from Queensland, Australia A precursor to US LNG exports

World s first LNG from Queensland, Australia A precursor to US LNG exports Jason Klein AGM, America American Petroleum Institute, Houston Chapter Legal notice No representation or warranty, express or

World s first LNG from Queensland, Australia A precursor to US LNG exports Jason Klein AGM, America American Petroleum Institute, Houston Chapter Legal notice No representation or warranty, express or

AES CORPORATION. LNG Review. Aaron Samson Director, LNG Projects

AES CORPORATION LNG Review Aaron Samson Director, LNG Projects December 11, 2006 Safe Harbor Disclosure Certain statements in the following presentation regarding AES s business operations may constitute

AES CORPORATION LNG Review Aaron Samson Director, LNG Projects December 11, 2006 Safe Harbor Disclosure Certain statements in the following presentation regarding AES s business operations may constitute

Sound Marketing for a FLNG Development

Sound Marketing for a FLNG Development Alessandro Della Zoppa EVP LNG eni Midstream Gas & Power Gastech Tokyo, 6 th April 2017 company overview Italian Government 30% 70% Market exploration & production

Sound Marketing for a FLNG Development Alessandro Della Zoppa EVP LNG eni Midstream Gas & Power Gastech Tokyo, 6 th April 2017 company overview Italian Government 30% 70% Market exploration & production

Excelerate Energy: Efficient And Cost-Effective Solutions for the Global Gas Market

Excelerate Energy: Efficient And Cost-Effective Solutions for the Global Gas Market 14 January 2014 Copyright Excelerate Energy L.P. Who We Are: Pioneer and world leader in innovative LNG midstream solutions.

Excelerate Energy: Efficient And Cost-Effective Solutions for the Global Gas Market 14 January 2014 Copyright Excelerate Energy L.P. Who We Are: Pioneer and world leader in innovative LNG midstream solutions.

Background, Issues, and Trends in Underground Hydrocarbon Storage

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

TECNA SABALO TECNA OPENS TECNA FIRST AND CONSULTING PROJECT ITS OFFICES OFFICES IN ACTIVITIES ACTIVITIES GENERATION PERU BEGIN GAS DEW POINT

Business driven Technology TECNA is a global Engineering, Procurement and Construction Company specialized in the execution of projects within the Oil & Gas, Nuclear Energy and Alternative Energies markets.

Business driven Technology TECNA is a global Engineering, Procurement and Construction Company specialized in the execution of projects within the Oil & Gas, Nuclear Energy and Alternative Energies markets.

Dominion Cove Point Export Project Platts 16 th Annual Liquefied Natural Gas February 9, 2017

Dominion Cove Point Export Project Platts 16 th Annual Liquefied Natural Gas February 9, 2017 Note to Investors This presentation contains certain forward-looking statements, including projected future

Dominion Cove Point Export Project Platts 16 th Annual Liquefied Natural Gas February 9, 2017 Note to Investors This presentation contains certain forward-looking statements, including projected future

Anadarko LNG and China

Anadarko LNG and China Scott Moore Vice President Worldwide Marketing US-China Oil and Gas Industry Forum September 26, 2014 Regarding Forward-Looking Statements and Other Matters This presentation contains

Anadarko LNG and China Scott Moore Vice President Worldwide Marketing US-China Oil and Gas Industry Forum September 26, 2014 Regarding Forward-Looking Statements and Other Matters This presentation contains

SONATRACH ALGERIA SONATRACH. Vision & Perspectives. ALGERIA - Energy Day 04th May, 2016 HOUSTON - TEXAS - USA

SONATRACH ALGERIA SONATRACH Vision & Perspectives ALGERIA - Energy Day 04th May, 2016 HOUSTON - TEXAS - USA Sonatrach Corporate Profile : 2015 key figures E&P Midstream Downstream Marketing Discoveries

SONATRACH ALGERIA SONATRACH Vision & Perspectives ALGERIA - Energy Day 04th May, 2016 HOUSTON - TEXAS - USA Sonatrach Corporate Profile : 2015 key figures E&P Midstream Downstream Marketing Discoveries

Regasification N. Atlantic

North Atlantic Basin LNG Week in Review 1 The report is for the week ending December 13. Table 1 to the right tracks 2013 LNG consumption in the Atlantic Basin through December 13 versus the same time

North Atlantic Basin LNG Week in Review 1 The report is for the week ending December 13. Table 1 to the right tracks 2013 LNG consumption in the Atlantic Basin through December 13 versus the same time

Alumina in focus Supply, Demand and Pricing

Alumina in focus Supply, Demand and Pricing 2015 Metal Bulletin B&A Conference Simon Storesund, SVP Commercial, B&A 26 February 2015 (1) Cautionary note Certain statements included within this announcement

Alumina in focus Supply, Demand and Pricing 2015 Metal Bulletin B&A Conference Simon Storesund, SVP Commercial, B&A 26 February 2015 (1) Cautionary note Certain statements included within this announcement

Growth Leadership: Vopak s LNG growth strategy

Growth Leadership: Vopak s LNG growth strategy Capital Markets Day, 7 December 2012 Dirk van Slooten, Global Director LNG Forward-looking statement This presentation contains statements of a forward-looking

Growth Leadership: Vopak s LNG growth strategy Capital Markets Day, 7 December 2012 Dirk van Slooten, Global Director LNG Forward-looking statement This presentation contains statements of a forward-looking

SPE DISTINGUISHED LECTURER SERIES is funded principally through a grant of the SPE FOUNDATION

SPE DISTINGUISHED LECTURER SERIES is funded principally through a grant of the SPE FOUNDATION The Society gratefully acknowledges those companies that support the program by allowing their professionals

SPE DISTINGUISHED LECTURER SERIES is funded principally through a grant of the SPE FOUNDATION The Society gratefully acknowledges those companies that support the program by allowing their professionals

ASX/MEDIA RELEASE 23 APRIL 2015 MAGNOLIA LNG PROJECT TOLLING AGREEMENT UPDATE WITH MERIDIAN LNG

ASX/MEDIA RELEASE 23 APRIL 2015 MAGNOLIA LNG PROJECT TOLLING AGREEMENT UPDATE WITH MERIDIAN LNG The Directors of Liquefied Natural Gas Limited (the Company, ASX Code: LNG) are pleased to advise that its

ASX/MEDIA RELEASE 23 APRIL 2015 MAGNOLIA LNG PROJECT TOLLING AGREEMENT UPDATE WITH MERIDIAN LNG The Directors of Liquefied Natural Gas Limited (the Company, ASX Code: LNG) are pleased to advise that its

OUR CONVERSATION TODAY

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

Global Market Pulp Statistics

Global Market Pulp Statistics Bleached Kraft Pulp November Data 217 Global Statistics for Bleached Kraft Market Pulp The statistics in this file is based on EPIS (European Pulp Industry Sector) data, distributed

Global Market Pulp Statistics Bleached Kraft Pulp November Data 217 Global Statistics for Bleached Kraft Market Pulp The statistics in this file is based on EPIS (European Pulp Industry Sector) data, distributed

Delivering Energy. Upstream Stranded Domestic Gas Potential to meet Energy Demand through LNG Value Chain: Lessons Learned from Senoro-DSLNG

Delivering Energy Upstream Stranded Domestic Gas Potential to meet Energy Demand through LNG Value Chain: Lessons Learned from Senoro-DSLNG Eka Satria, Development Director - PT Medco Energi International

Delivering Energy Upstream Stranded Domestic Gas Potential to meet Energy Demand through LNG Value Chain: Lessons Learned from Senoro-DSLNG Eka Satria, Development Director - PT Medco Energi International

LNG Projects Development of the Future

LNG Projects Development of the Future Gastech, 7 th of April 2017 Hilary Mercer VP Integrated Gas Projects and Executive Director Prelude 1 Definitions & cautionary note The companies in which Royal Dutch

LNG Projects Development of the Future Gastech, 7 th of April 2017 Hilary Mercer VP Integrated Gas Projects and Executive Director Prelude 1 Definitions & cautionary note The companies in which Royal Dutch

TEEKAY LNG PARTNERS Q EARNINGS AND BUSINESS OUTLOOK PRESENTATION February 18, 2016

TEEKAY LNG PARTNERS Q4-2015 EARNINGS AND BUSINESS OUTLOOK PRESENTATION February 18, 2016 Forward Looking Statement This presentation contains forward-looking statements (as defined in Section 21E of the

TEEKAY LNG PARTNERS Q4-2015 EARNINGS AND BUSINESS OUTLOOK PRESENTATION February 18, 2016 Forward Looking Statement This presentation contains forward-looking statements (as defined in Section 21E of the

MARINE WORKS AND TERMINALS

11.2010 MARINE WORKS AND TERMINALS ONSHORE ENGINEERING AND CONSTRUCTION PROJECT REFERENCES People, ideas, energy. Saipem S.p.A. Via Martiri di Cefalonia, 67-20097 San Donato Milanese, Milan - Italy Tel.

11.2010 MARINE WORKS AND TERMINALS ONSHORE ENGINEERING AND CONSTRUCTION PROJECT REFERENCES People, ideas, energy. Saipem S.p.A. Via Martiri di Cefalonia, 67-20097 San Donato Milanese, Milan - Italy Tel.

Al Garcia Business Manager-Americas C4U Trade USA, Inc.

Revealing Global Trade Flows For Propane And Implications For Supply- Future export markets for North American propane and what this means for PDH feedstock security Al Garcia Business Manager-Americas

Revealing Global Trade Flows For Propane And Implications For Supply- Future export markets for North American propane and what this means for PDH feedstock security Al Garcia Business Manager-Americas

TOTAL IN AFRICA: IN FOR THE LONG RUN. Photo: Moho Bilondo, TOTAL

TOTAL IN AFRICA: IN FOR THE LONG RUN Photo: Moho Bilondo, TOTAL Jacques Marraud des Grottes, President Africa, TOTAL E&P Oil Council s 2013 Africa O&G Assembly Paris June 11, 2013 TOTAL, INTEGRATED ENERGY

TOTAL IN AFRICA: IN FOR THE LONG RUN Photo: Moho Bilondo, TOTAL Jacques Marraud des Grottes, President Africa, TOTAL E&P Oil Council s 2013 Africa O&G Assembly Paris June 11, 2013 TOTAL, INTEGRATED ENERGY

Latin-American LNG markets

Latin-American LNG markets Javier Diaz, Manager, Energy Analysis & Consulting S&P Global Platts jdiaz@spglobal.com Platts 16th Annual Liquefied Natural Gas February 9-1, 217 * Houston, Texas Copyright

Latin-American LNG markets Javier Diaz, Manager, Energy Analysis & Consulting S&P Global Platts jdiaz@spglobal.com Platts 16th Annual Liquefied Natural Gas February 9-1, 217 * Houston, Texas Copyright

Yemen LNG Operational feedbacks

Yemen LNG Operational feedbacks APCI Owners Seminar XI September 2013 1 Yemen LNG - Agenda 1. Yemen LNG general presentation 2. Feedback on Plant restarts optimization 3. Other operational feedbacks 2

Yemen LNG Operational feedbacks APCI Owners Seminar XI September 2013 1 Yemen LNG - Agenda 1. Yemen LNG general presentation 2. Feedback on Plant restarts optimization 3. Other operational feedbacks 2

LNG Facts A Primer. Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums. March 10, Kristi A. R.

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

Floating LNG Business A breakthrough in offshore gas monetization

Floating LNG Business A breakthrough in offshore gas monetization LNG Malaysia Forum 2013 19-21 March, Kuala Lumpur Allan Magee, Ph.D. R&D Manager, Offshore Product Line and Technologies, Technip Geoproduction

Floating LNG Business A breakthrough in offshore gas monetization LNG Malaysia Forum 2013 19-21 March, Kuala Lumpur Allan Magee, Ph.D. R&D Manager, Offshore Product Line and Technologies, Technip Geoproduction

LNG market update. Surge in LNG supply creates opportunities to open new markets

LNG market update Surge in LNG supply creates opportunities to open new markets Royal Vopak Analyst Day 2017 Ton Floors, Global LNG Director 12 December 2017 Forward-looking statement This presentation

LNG market update Surge in LNG supply creates opportunities to open new markets Royal Vopak Analyst Day 2017 Ton Floors, Global LNG Director 12 December 2017 Forward-looking statement This presentation

Opportunities and Challenges in the Energy Infrastructure Industry. Louisiana State University Energy Summit

Opportunities and Challenges in the Energy Infrastructure Industry Louisiana State University Energy Summit 1 Kinder Morgan Overview Kinder Morgan is the largest midstream and the third largest energy

Opportunities and Challenges in the Energy Infrastructure Industry Louisiana State University Energy Summit 1 Kinder Morgan Overview Kinder Morgan is the largest midstream and the third largest energy

Navios South American Logistics Inc. Company Presentation

Navios South American Logistics Inc. Company Presentation November 2014 Forward Looking Statements This presentation contains forward-looking statements (as defined in Section 27A of the Securities Act

Navios South American Logistics Inc. Company Presentation November 2014 Forward Looking Statements This presentation contains forward-looking statements (as defined in Section 27A of the Securities Act

Alaska LNG Concept Information. Alaska LNG. Overview. October

Overview October December 3, 2013 Project Overview Project Team BP, ConocoPhillips, ExxonMobil and TransCanada are working together to progress an project: 300+ people involved in project planning and

Overview October December 3, 2013 Project Overview Project Team BP, ConocoPhillips, ExxonMobil and TransCanada are working together to progress an project: 300+ people involved in project planning and

BLM Suspends Natural Gas Waste Standards

Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.86 2.84 2.82 2.8 2.78 2.76

Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.86 2.84 2.82 2.8 2.78 2.76

Gas in Power Generation Sector, the story as told by Jodi-Gas database.

1 GECF Gas in Power Generation Sector, the story as told by Jodi-Gas database. Mohamed Arafat Data Bank Analyst, GECF 14th Regional JODI Training Workshop 9-11 November 2016, Moscow, Russia 2 Agenda Why

1 GECF Gas in Power Generation Sector, the story as told by Jodi-Gas database. Mohamed Arafat Data Bank Analyst, GECF 14th Regional JODI Training Workshop 9-11 November 2016, Moscow, Russia 2 Agenda Why

GLADSTONE TO JAPAN: EXPORT LNG PROJECT. December 2007

GLADSTONE TO JAPAN: EXPORT LNG PROJECT December 2007 Project Summary Sunshine Gas (SHG) and Sojitz Corporation (SOJITZ) formed relationship to combine upstream and downstream resource expertise to identify

GLADSTONE TO JAPAN: EXPORT LNG PROJECT December 2007 Project Summary Sunshine Gas (SHG) and Sojitz Corporation (SOJITZ) formed relationship to combine upstream and downstream resource expertise to identify

DSLNG Project Update. Andy Karamoy PT Donggi Senoro LNG. 4 th LNG Supply, Transport and Storage Indonesia May 2014 Bali, Indonesia

DSLNG Project Update Andy Karamoy PT Donggi Senoro LNG 4 th LNG Supply, Transport and Storage Indonesia 19-21 May 2014 Bali, Indonesia Table of Contents 1. Introduction of Donggi Senoro LNG Project 2.

DSLNG Project Update Andy Karamoy PT Donggi Senoro LNG 4 th LNG Supply, Transport and Storage Indonesia 19-21 May 2014 Bali, Indonesia Table of Contents 1. Introduction of Donggi Senoro LNG Project 2.

Trends, Issues and Market Changes for Crude Oil and Natural Gas

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

SAAM IN ECUADOR. June 13, 2017

SAAM IN ECUADOR June 13, 2017 DISCLAIMER This presentation provides general information about Sociedad Matriz SAAM S.A. ( SMSAAM ) and related companies. It consists of summarized information and does

SAAM IN ECUADOR June 13, 2017 DISCLAIMER This presentation provides general information about Sociedad Matriz SAAM S.A. ( SMSAAM ) and related companies. It consists of summarized information and does

We deliver gas infrastructure

We deliver gas infrastructure We are Uniper We are a leading international energy company with operations in more than 40 countries and around 13,000 employees. We combine a balanced portfolio of modern

We deliver gas infrastructure We are Uniper We are a leading international energy company with operations in more than 40 countries and around 13,000 employees. We combine a balanced portfolio of modern

Operational excellence contributes to lowering LCOE

Operational excellence contributes to lowering LCOE Jean-Marc Lechêne, Executive Vice President & COO London, 21 June 2016 Disclaimer and cautionary statement This presentation contains forward-looking

Operational excellence contributes to lowering LCOE Jean-Marc Lechêne, Executive Vice President & COO London, 21 June 2016 Disclaimer and cautionary statement This presentation contains forward-looking

Crude Oil Price Volatility Crude oil price continued to be volatile (US$/bbl) Continued upswing in Collapse after Rehman shock Price surge aft

Continued upswing in Collapse after Rehman shock Price surge aft") Current Situation and Outlook for the Oil & Gas (LNG) Market Session 2 IEEJ/CNPC ETRI Joint Symposium November 8 th, 2017 Dr. Ken Koyama Chief economist and managing director Institute of Energy Economics,

Current Situation and Outlook for the Oil & Gas (LNG) Market Session 2 IEEJ/CNPC ETRI Joint Symposium November 8 th, 2017 Dr. Ken Koyama Chief economist and managing director Institute of Energy Economics,

Navios South American Logistics Inc. Company Presentation

Navios South American Logistics Inc. Company Presentation August 2013 Forward Looking Statements This presentation contains forward-looking statements (as defined in Section 27A of the Securities Act of

Navios South American Logistics Inc. Company Presentation August 2013 Forward Looking Statements This presentation contains forward-looking statements (as defined in Section 27A of the Securities Act of

Sanford C. Bernstein & Co. 23 rd Strategic Decisions Conference. Steve Angel Chairman, President & Chief Executive Officer. May 31, 2007.

Sanford C. Bernstein & Co. 23 rd Strategic Decisions Conference Steve Angel Chairman, President & Chief Executive Officer May 31, 2007 May 31, 2007 Forward Looking Statement This document contains forward-looking

Sanford C. Bernstein & Co. 23 rd Strategic Decisions Conference Steve Angel Chairman, President & Chief Executive Officer May 31, 2007 May 31, 2007 Forward Looking Statement This document contains forward-looking

Productivity improvements in a changing world

Productivity improvements in a changing world Michael Gollschewski Managing director Pilbara Mines 13 July 2015 Cautionary statement General This presentation has been prepared by Rio Tinto plc and Rio

Productivity improvements in a changing world Michael Gollschewski Managing director Pilbara Mines 13 July 2015 Cautionary statement General This presentation has been prepared by Rio Tinto plc and Rio

Southern Copper Corporation November, 2011

Southern Copper Corporation November, 0 0 I. Introduction Management Presenters Presenter Raul Jacob Title CFO - Peruvian Operations & Company Comptroller Corporate Structure 00.0% (*) AMERICAS MINING

Southern Copper Corporation November, 0 0 I. Introduction Management Presenters Presenter Raul Jacob Title CFO - Peruvian Operations & Company Comptroller Corporate Structure 00.0% (*) AMERICAS MINING

Oil and natural gas: market outlook and drivers

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Jordan LNG Project. Presented By: Eng. Ahmad Zubi / NEPCO

Jordan LNG Project Presented By: Eng. Ahmad Zubi / NEPCO Contents: Part 1 Introduction Part 2 Terminal Project Part 3 LNG Procurement Strategy Part 1 Introduction The Hashemite Kingdom Of Jordan Quick

Jordan LNG Project Presented By: Eng. Ahmad Zubi / NEPCO Contents: Part 1 Introduction Part 2 Terminal Project Part 3 LNG Procurement Strategy Part 1 Introduction The Hashemite Kingdom Of Jordan Quick

REPSOL ESG Road Show. Repsol S.A.

REPSOL 2013 ESG Road Show Repsol S.A. Disclaimer ALL RIGHTS ARE RESERVED REPSOL, S.A. 2013 Repsol, S.A. is the exclusive owner of this document. No part of this document may be reproduced (including photocopying),

REPSOL 2013 ESG Road Show Repsol S.A. Disclaimer ALL RIGHTS ARE RESERVED REPSOL, S.A. 2013 Repsol, S.A. is the exclusive owner of this document. No part of this document may be reproduced (including photocopying),

Small Scale LNG From Concept to Reality. Chris Johnson, General Manager, LNG New Markets, Shell

Small Scale LNG From Concept to Reality Chris Johnson, General Manager, LNG New Markets, Shell 0 Table of Contents Table of Contents... 1 Background... 1 Aims... 4 Methods... 5 Results... 11 Conclusions...

Small Scale LNG From Concept to Reality Chris Johnson, General Manager, LNG New Markets, Shell 0 Table of Contents Table of Contents... 1 Background... 1 Aims... 4 Methods... 5 Results... 11 Conclusions...

Q /05/17. Jon Skule Storheill. Snorre Krogstad

Q1 2017 Jon Skule Storheill Snorre Krogstad 05/05/17 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

Q1 2017 Jon Skule Storheill Snorre Krogstad 05/05/17 www.awilcolng.no - 1 - Disclaimer This presentation may include certain forward-looking statements, forecasts, estimates, predictions, influences and

Asia s First FSRU And its Role in Pushing LNG Development in Indonesia

Asia s First FSRU And its Role in Pushing LNG Development in Indonesia Tammy Meidharma PT Nusantara Regas 4 th LNG Supply, Transportation & Storage Indonesia, 20 May 2014, Stone Hotel, Legian, Bali Overview

Asia s First FSRU And its Role in Pushing LNG Development in Indonesia Tammy Meidharma PT Nusantara Regas 4 th LNG Supply, Transportation & Storage Indonesia, 20 May 2014, Stone Hotel, Legian, Bali Overview

Table 1 Trade movements 2004 LNG (Bcm)

") LNG Prospects for the Future The prospect that LNG could become a major global energy source is one of the most keenly debated issues in the sector. This was reflected in this quarter's survey, conducted

LNG Prospects for the Future The prospect that LNG could become a major global energy source is one of the most keenly debated issues in the sector. This was reflected in this quarter's survey, conducted

DR. CHARLES ELLINAS Executive President. Frederick University, 19 September 2013

Developments and Prospects of Oil & Gas Exploration in the Eastern Mediterranean Region and How these Translate to Employment Opportunities Training and Education Needs DR. CHARLES ELLINAS Executive President

Developments and Prospects of Oil & Gas Exploration in the Eastern Mediterranean Region and How these Translate to Employment Opportunities Training and Education Needs DR. CHARLES ELLINAS Executive President

Reservoir Management at. Pluspetrol S.A. The Company, Expertise and History of its Evolution. Production Growth, a parallelism with Company Evolution

REGIONAL ASSOCIATION OF OIL, GAS & BIOFUELS SECTOR COMPANIES IN LATIN AMERICA AND THE CARIBBEAN Reservoir Management at Pluspetrol S.A. Telmo Gerlero Pluspetrol S.A. 86 th ARPEL Experts Level Meeting (RANE)

REGIONAL ASSOCIATION OF OIL, GAS & BIOFUELS SECTOR COMPANIES IN LATIN AMERICA AND THE CARIBBEAN Reservoir Management at Pluspetrol S.A. Telmo Gerlero Pluspetrol S.A. 86 th ARPEL Experts Level Meeting (RANE)

LNG Market Trends & Price Transparency

LNG Market Trends & Price Transparency Tokyo Fiona Poynter April 2015 London Houston Washington New York Portland Calgary Santiago Bogota Rio de Janeiro Singapore Beijing Tokyo Sydney Dubai Moscow Astana

LNG Market Trends & Price Transparency Tokyo Fiona Poynter April 2015 London Houston Washington New York Portland Calgary Santiago Bogota Rio de Janeiro Singapore Beijing Tokyo Sydney Dubai Moscow Astana

Gas & LNG market developments

BERLIN LONDON MADRID PARIS TURIN WARSAW Gas & LNG market developments 4 th Athens Triennial Meeting, 10-11 Nov. 2017 Kostas Andriosopoulos Professor, Finance and Energy Economics Executive Director, Research

BERLIN LONDON MADRID PARIS TURIN WARSAW Gas & LNG market developments 4 th Athens Triennial Meeting, 10-11 Nov. 2017 Kostas Andriosopoulos Professor, Finance and Energy Economics Executive Director, Research

Extraction The gas is extracted from fields by drilling wells and installing extraction pipes

LNG terminals Enagás, world leader in LNG terminals With eight regasification plants, Enagás is one of the companies with more LNG terminals in the world. We pioneer the development, maintenance and operation

LNG terminals Enagás, world leader in LNG terminals With eight regasification plants, Enagás is one of the companies with more LNG terminals in the world. We pioneer the development, maintenance and operation

FUGRO GROUP LNG FIELD DEVELOPMENT AND FACILITIES. TACKLING your complex challenges. UNDERSTANDING your operational objectives

LNG FIELD DEVELOPMENT AND FACILITIES FUGRO GROUP UNDERSTANDING your operational objectives TACKLING your complex challenges DELIVERING your global success stories LNG FIELD DEVELOPMENT AND FACILITIES Developing

LNG FIELD DEVELOPMENT AND FACILITIES FUGRO GROUP UNDERSTANDING your operational objectives TACKLING your complex challenges DELIVERING your global success stories LNG FIELD DEVELOPMENT AND FACILITIES Developing

OLT Offshore LNG Toscana Alessandro Fino CEO

Small Scale to large Market Strategies & Technologies towards the Mediterranean Area "La logistica primaria per la distribuzione del GNL" OLT Offshore LNG Toscana Alessandro Fino CEO 1 OLT Shareholders

Small Scale to large Market Strategies & Technologies towards the Mediterranean Area "La logistica primaria per la distribuzione del GNL" OLT Offshore LNG Toscana Alessandro Fino CEO 1 OLT Shareholders

Third quarter and first nine months 2017 Results Release. October 19 th, 2017

Third quarter and first nine months 2017 Results Release October 19 th, 2017 Safe harbor statement Any statements contained in this document that are not historical facts are forward-looking statements

Third quarter and first nine months 2017 Results Release October 19 th, 2017 Safe harbor statement Any statements contained in this document that are not historical facts are forward-looking statements

PBF Energy. State College, PA. North East Association of Rail Shippers Fall Conference. October 1, 2014

PBF Energy North East Association of Rail Shippers Fall Conference State College, PA October 1, 2014 Safe Harbor Statements This presentation contains forward-looking statements made by PBF Energy Inc.

PBF Energy North East Association of Rail Shippers Fall Conference State College, PA October 1, 2014 Safe Harbor Statements This presentation contains forward-looking statements made by PBF Energy Inc.

2 nd Quarter Financial Results for Fiscal 2017 November 9, Tadashi Ishizuka Representative Director, President and COO

Business Overview 2 nd Quarter Financial Results for Fiscal 2017 November 9, 2017 Tadashi Ishizuka Representative Director, President and COO Contents 1. Project Orders for the First Half of FY2017 2.

Business Overview 2 nd Quarter Financial Results for Fiscal 2017 November 9, 2017 Tadashi Ishizuka Representative Director, President and COO Contents 1. Project Orders for the First Half of FY2017 2.

Product Line FGS FLOATING GAS SOLUTIONS OVERVIEW

Project Discipline Product Line FGS FLOATING GAS SOLUTIONS OVERVIEW FLOATING GAS SOLUTIONS AT A GLANCE SBM Offshore offers a catalogue of solutions, spanning the entire floating gas value chain, from small

Project Discipline Product Line FGS FLOATING GAS SOLUTIONS OVERVIEW FLOATING GAS SOLUTIONS AT A GLANCE SBM Offshore offers a catalogue of solutions, spanning the entire floating gas value chain, from small

CONCESSION OF GENERAL SAN MARTIN PORT TERMINAL( PISCO) EXECUTIVE SUMMARY PRIVATE INVESTMENT PROMOTION AGENCY

EXECUTIVE SUMMARY PRIVATE INVESTMENT PROMOTION AGENCY") REPUBLIC OF PERU CONCESSION OF GENERAL SAN MARTIN PORT TERMINAL( PISCO) EXECUTIVE SUMMARY PRIVATE INVESTMENT PROMOTION AGENCY COMMITTEE IN SANITATION AND STATE PROJECTS August, 2008 Contact List Name Position

REPUBLIC OF PERU CONCESSION OF GENERAL SAN MARTIN PORT TERMINAL( PISCO) EXECUTIVE SUMMARY PRIVATE INVESTMENT PROMOTION AGENCY COMMITTEE IN SANITATION AND STATE PROJECTS August, 2008 Contact List Name Position

Published on Market Research Reports Inc. (https://www.marketresearchreports.com)

") Published on Market Research Reports Inc. (https://www.marketresearchreports.com) Home > Tanzania Oil Gas Industry Analysis and Forecast Report (Q1 2016) - Supply, Demand, Investments, Competition and

Published on Market Research Reports Inc. (https://www.marketresearchreports.com) Home > Tanzania Oil Gas Industry Analysis and Forecast Report (Q1 2016) - Supply, Demand, Investments, Competition and

Published on Market Research Reports Inc. (https://www.marketresearchreports.com)

") Published on Market Research Reports Inc. (https://www.marketresearchreports.com) Home > Iraq Oil Gas Industry Analysis and Forecast Report (Q1 2016) - Supply, Demand, Investments, Competition and Projects

Published on Market Research Reports Inc. (https://www.marketresearchreports.com) Home > Iraq Oil Gas Industry Analysis and Forecast Report (Q1 2016) - Supply, Demand, Investments, Competition and Projects

The Great Eastern Shipping Co. Ltd. Business & Financial Review April 2010

The Great Eastern Shipping Co. Ltd. Business & Financial Review April 2010 1 Forward Looking Statements Except for historical information, the statements made in this presentation constitute forward looking

The Great Eastern Shipping Co. Ltd. Business & Financial Review April 2010 1 Forward Looking Statements Except for historical information, the statements made in this presentation constitute forward looking

LNG Liquefaction Projects A North America Focus

LNG Training Courses LNG Liquefaction Projects A North America Focus 24-26 January 2018 - Houston Sound understanding of the fundamental economics of North American LNG Exports About the Course A decade

LNG Training Courses LNG Liquefaction Projects A North America Focus 24-26 January 2018 - Houston Sound understanding of the fundamental economics of North American LNG Exports About the Course A decade

Geopolitics of Natural Gas Study Atlantic LNG James A Baker III Institute for Public Policy Rice University James Ball & Rob Shepherd May 2004

Geopolitics of Natural Gas Study Atlantic LNG James A Baker III Institute for Public Policy Rice University James Ball & Rob Shepherd 26-27 May 2004 Gas Strategies Consulting Ltd Rodwell House 100 Middlesex

Geopolitics of Natural Gas Study Atlantic LNG James A Baker III Institute for Public Policy Rice University James Ball & Rob Shepherd 26-27 May 2004 Gas Strategies Consulting Ltd Rodwell House 100 Middlesex

Global Gasoline, Global Condensate and Global Petrochemical Markets to 2020 and How much naphtha will end up in gasoline blending?

Study Prospectus Nexus - The Interaction Between: Global Gasoline, Global Condensate and Global Petrochemical Markets to 2020 and 2025 Can I export more naphtha? Should I build a splitter? Should I build

Study Prospectus Nexus - The Interaction Between: Global Gasoline, Global Condensate and Global Petrochemical Markets to 2020 and 2025 Can I export more naphtha? Should I build a splitter? Should I build

Lehman Brothers T Conference San Francisco. Craig DeYoung, Vice President Investor Relations December 9, 2004

Lehman Brothers T4 2004 Conference San Francisco Craig DeYoung, Vice President Investor Relations December 9, 2004 Safe Harbor Safe Harbor Statement under the U.S. Private Securities Litigation Reform

Lehman Brothers T4 2004 Conference San Francisco Craig DeYoung, Vice President Investor Relations December 9, 2004 Safe Harbor Safe Harbor Statement under the U.S. Private Securities Litigation Reform

EGB Relative Value Report. May152013

EGB May152013 Jul-14 Jul-15 Sep-16 Sep-17 Mar-19 Jul-20 Sep-21 Apr-22 Nov-22 Oct-23 Mar-26 Jul-27 May-34 Mar-37 Jun-44 Jan-62 Austria, 15-May-13 45 bp 35 bp 25 bp 15 bp 5 bp -5 bp -15 bp -25 bp -35 bp

EGB May152013 Jul-14 Jul-15 Sep-16 Sep-17 Mar-19 Jul-20 Sep-21 Apr-22 Nov-22 Oct-23 Mar-26 Jul-27 May-34 Mar-37 Jun-44 Jan-62 Austria, 15-May-13 45 bp 35 bp 25 bp 15 bp 5 bp -5 bp -15 bp -25 bp -35 bp

ELIGIBILITY CRITERIA FOR QUALIFICATION OF EPC CONTRACTORS FOR LNG TERMINAL AT GANGAVARAM, VISAKHAPATNAM, ANDHRA PRADESH (INDIA)

") ELIGIBILITY CRITERIA FOR QUALIFICATION OF EPC CONTRACTORS FOR LNG TERMINAL AT GANGAVARAM, VISAKHAPATNAM, ANDHRA PRADESH (INDIA) Petronet LNG Limited intends to undertake International Competitive Bidding

ELIGIBILITY CRITERIA FOR QUALIFICATION OF EPC CONTRACTORS FOR LNG TERMINAL AT GANGAVARAM, VISAKHAPATNAM, ANDHRA PRADESH (INDIA) Petronet LNG Limited intends to undertake International Competitive Bidding

AMT BEEF & MUTTON MONTHLY REPORT JULY Compiled by Pieter Cornelius E mail: NEXT PUBLICATION 7 AUGUST 2017

Enquiries: Dr Johann van der Merwe Cell: 073 140 2698 Web: www.agrimark.co.za E mail: johnny@amtrends.co.za Compiled by Pieter Cornelius E mail: pieter@amtrends.co.za NEXT PUBLICATION 7 AUGUST AMT BEEF

Enquiries: Dr Johann van der Merwe Cell: 073 140 2698 Web: www.agrimark.co.za E mail: johnny@amtrends.co.za Compiled by Pieter Cornelius E mail: pieter@amtrends.co.za NEXT PUBLICATION 7 AUGUST AMT BEEF

PETROLEUM SECTOR DEVELOPMENT. Industrialization of the Sector in the country and its impact on long term national economy

PETROLEUM SECTOR DEVELOPMENT Industrialization of the Sector in the country and its impact on long term national economy Presentation at KKFP Conference Dili, 27 October 2016 1 OUTLINE 1. Development of

PETROLEUM SECTOR DEVELOPMENT Industrialization of the Sector in the country and its impact on long term national economy Presentation at KKFP Conference Dili, 27 October 2016 1 OUTLINE 1. Development of

Floating LNG What are the key business development risks and mitigation strategies in a FLNG project?

Floating LNG 2013 What are the key business development risks and mitigation strategies in a FLNG project? What are the key challenges? What are some of the risk mitigation strategies? What are some of

Floating LNG 2013 What are the key business development risks and mitigation strategies in a FLNG project? What are the key challenges? What are some of the risk mitigation strategies? What are some of

LNG and storage strategy - follow-up study - Final Presentation 27 September 2017 Jalil Jumriany Energy Markets Global Limited

LNG and storage strategy - follow-up study - Final Presentation 27 September 2017 Jalil Jumriany Energy Markets Global Limited LNG and storage strategy - follow-up study - LNG: Main Findings LNG: Main

LNG and storage strategy - follow-up study - Final Presentation 27 September 2017 Jalil Jumriany Energy Markets Global Limited LNG and storage strategy - follow-up study - LNG: Main Findings LNG: Main

Scaling down LNG. Mariana Ortiz Laborde. Gas Natural Fenosa. Portfolio Manager at Global Gas Division

Scaling down LNG Mariana Ortiz Laborde Portfolio Manager at Global Gas Division Gas Natural Fenosa Executive Committee Workshop March 30, 2017, Muscat, Oman Disclaimer This presentation and the information

Scaling down LNG Mariana Ortiz Laborde Portfolio Manager at Global Gas Division Gas Natural Fenosa Executive Committee Workshop March 30, 2017, Muscat, Oman Disclaimer This presentation and the information

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS Mitchell DeRubis, Senior Energy Analyst Bob Yu, Senior Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments and other related

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS Mitchell DeRubis, Senior Energy Analyst Bob Yu, Senior Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments and other related

Market Alert. China NPK Statistical Update February Highlights. China Plant Nutrient Exports. Exports

Market Alert China NPK Statistical Update February Exports China Customs reported that high-analysis phosphate exports (DAP/ MAP/TSP) fell to 65,200 tonnes in February, a drop of 54% from uary and 58%

Market Alert China NPK Statistical Update February Exports China Customs reported that high-analysis phosphate exports (DAP/ MAP/TSP) fell to 65,200 tonnes in February, a drop of 54% from uary and 58%