British Columbia s LNG Advantage

|

|

|

- Opal Griffin

- 5 years ago

- Views:

Transcription

1 British Columbia s LNG Advantage Steve Carr. Deputy Minister Ministry of Natural Gas Development 2014 CAPP SCOTIABANK Investment Symposium West Coast LNG Panel Plenary Panel

2 Our Competitive Position Short transport times to Asian markets Competitive fiscal policies Secure, stable government World leading environmental standards Ongoing First Nations engagement Large gas reserves Labour availability Strong regulatory regime 2

3 Short transport times to Asian markets Canada 7,300 km 10 days US Gulf Coast 17,145 km 23.5 days Mozambique 13,000 km 17 days Australia West 6,855 km 9.5 days Australia East 7,000 km 9.5 days Source: IHS CERA 3

4 Fiscal and Policy Framework Elements of B.C. s Competitive Framework for LNG development: Tax regime Environmental policies First Nations Upstream development Labour supply Regulatory 4

5 Competitive Framework: Tax B.C. is committed to providing certainty on tax Designed to keep B.C. competitive with other jurisdiction Ensure proponents get capital out early Based on four core principles for fair and balanced approach:: 5

6 LNG Income Tax: Creating certainty for LNG development Applies to income from liquefaction process at LNG facility and applies to LNG for both domestic and export markets 6

7 Application of LNG Income Tax (Plant Producing 12 MTPA) 7

8 Is B.C. a competitive jurisdiction? 8

9 International Competitiveness: EY Study EY analysis & report: review of tax and royalty regimes of key competitor jurisdictions Australia Alaska, Georgia, Louisiana, Oregon and Texas Concluded B.C. is competitive Low overall tax burden and competitive royalty regime 9

10 Competitive Tax Regime for LNG: EY Study 10

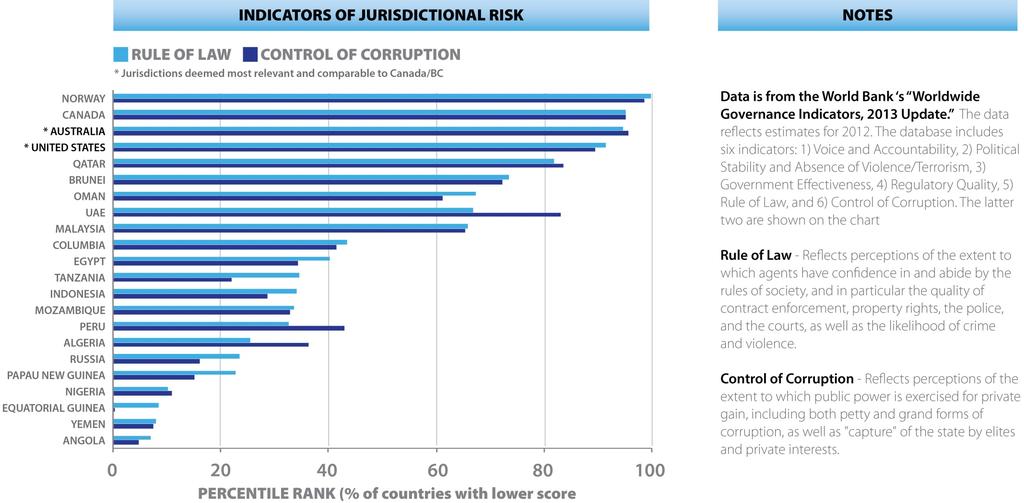

11 Low Risk Jurisdiction 11

12 Policy Framework: Environmental Policies World-class environmental policies: Strong regulatory regime Legislated aggressive GHG reduction targets Revenue neutral carbon tax Carbon neutral government Legislated requirement for 93% clean energy Committed to maintaining leadership on climate change and clean energy by ensuring the cleanest LNG operations in the world 12

13 GHG Emissions and LNG As cleanest burning fossil fuel, natural gas is part of a global climate solution When replacing coal, LNG can be up to 20% lower GHG emissions for the full fuel cycle GHG Policy We are considering a single, world-leading GHG benchmark for LNG facilities We exploring flexible compliance options to meet GHG benchmark B.C. will look to mitigate costs 13

14 Policy Framework: First Nations First Nations are generally supportive of LNG development as a low risk resource B.C. is involved in LNG-related negotiations with approximately 34 First Nations First Nation opportunities in agreements include: Financial benefits from B.C. Environmental initiatives Skills training and jobs LNG opportunities throughout B.C. value chain: upstream, midstream and downstream 14

15 First Nations: Agreements Upstream Several upstream agreements in place with First Nations near gas fields and negotiating new agreements with remaining First Nations Midstream Precedent with Pacific Trails Pipeline agreement with First Nations Limited Partnership and pursuing agreements for new pipelines with about 30 First Nations along pipeline routes Downstream Some agreements with Haisla First Nation and revenue sharing negotiations underway for new LNG development on provincial lands 15

2,933 trillion cubic feet (tcf)")

16 Policy Framework: Upstream Development (B.C. s resource base) 2,933 trillion cubic feet (tcf) of natural gas from tight and shale Montney play has 1,965 tcf of gas 271 tcf is expected to be recoverable for market Horn River play has 448 tcf of gas 78 tcf is expected to be recoverable for market 16

17 Upstream Development: Competitiveness Upstream competitiveness key element of LNG overall competitiveness New Royalty Program New royalty program ( Tier 1 ) to incent drilling activity in shallower areas Opens up 32 trillion cubic feet of natural gas to development in the Montney Other upstream initiatives being considered 3-year Infrastructure Royalty Credit Program Pilot new royalty credit program targeted to innovative, clean technologybased joint infrastructure projects (e.g. water recycling, GHG emission reduction projects, etc.) New OGRRIP capital triggered by positive Final Investment Decisions 17

18 Access to Labour Invest with Confidence LNG projects need Sufficient supply of skilled workers A stable labour environment that supports business Collaborative government B.C. s Highly Skilled Workforce 2.4 million workers largest workforce in western Canada Canada has the highest rate of post-secondary education in the world World-class education and training system 18

19 Labour Supply Plan Priorities K-12 System Public and Private Post-Secondary Institutions Apprenticeship Systems Labour Market Programs Web and Marketing Promotion and Attraction Labour Mobility Credential Harmonization Federal and Provincial Immigration Streams Temporary Foreign Workers Foreign Qualifications Recognition 19

20 Strong Regulatory Regime Community Planning Permitting Environmental 20

21 B.C. is an attractive place to invest Continue to work to ensure that B.C. remains competitive Global and economic conditions will continue to be considered as B.C. finalizes the key components of the LNG Income tax and environmental policies to ensure B.C. remains competitive 21

22 2014 INTERNATIONAL LNG IN BC CONFERENCE MAY VANCOUVER CONVENTION CENTER 22

LNG. Liquefied Natural Gas A Strategy for B.C. s Newest Industry

LNG Liquefied Natural Gas A Strategy for B.C. s Newest Industry LIQUEFIED NATURAL GAS Message from the Premier The BC Jobs Plan released in September is all about leveraging our competitive advantages

LNG Liquefied Natural Gas A Strategy for B.C. s Newest Industry LIQUEFIED NATURAL GAS Message from the Premier The BC Jobs Plan released in September is all about leveraging our competitive advantages

N E W S R E L E A S E

For Immediate Release 2012PREM0014-000104 Feb. 3, 2012 N E W S R E L E A S E Ministry of Energy and Mines Natural gas fuelling new economic opportunities VANCOUVER Premier Christy Clark today announced

For Immediate Release 2012PREM0014-000104 Feb. 3, 2012 N E W S R E L E A S E Ministry of Energy and Mines Natural gas fuelling new economic opportunities VANCOUVER Premier Christy Clark today announced

2017/ /20 SERVICE PLAN

Ministry of Natural Gas Development and Minister Responsible for Housing 2017/18 2019/20 SERVICE PLAN February 2017 For more information on the British Columbia Ministry of Natural Gas Development and

Ministry of Natural Gas Development and Minister Responsible for Housing 2017/18 2019/20 SERVICE PLAN February 2017 For more information on the British Columbia Ministry of Natural Gas Development and

Canadian LNG Projects

Canadian LNG Projects Key Development and Financing Issues By Christopher Langdon, Paul Cassidy and Gordon Nettleton of McCarthy Tétrault and Stephen McWilliams of Latham & Watkins 1 First published in

Canadian LNG Projects Key Development and Financing Issues By Christopher Langdon, Paul Cassidy and Gordon Nettleton of McCarthy Tétrault and Stephen McWilliams of Latham & Watkins 1 First published in

Alaska LNG. Commercializing. Daniel S. Sullivan Commissioner, Alaska Department of Natural Resources

Commercializing Alaska LNG Daniel S. Sullivan Commissioner, Alaska Department of Natural Resources SPOTLIGHT SESSION: The North American LNG Market Imports, Exports or Both LNG17, Wednesday, April 17,

Commercializing Alaska LNG Daniel S. Sullivan Commissioner, Alaska Department of Natural Resources SPOTLIGHT SESSION: The North American LNG Market Imports, Exports or Both LNG17, Wednesday, April 17,

BRITISH COLUMBIA CARBON TAX. Partnership for Market Readiness Technical Workshop February 2016

BRITISH COLUMBIA CARBON TAX Partnership for Market Readiness Technical Workshop February 2016 British Columbia s Diversified Economy Share of BC real GDP at basic prices (chained $2007) by major industry,

BRITISH COLUMBIA CARBON TAX Partnership for Market Readiness Technical Workshop February 2016 British Columbia s Diversified Economy Share of BC real GDP at basic prices (chained $2007) by major industry,

Research Projects as of March 27, 2018

2017-2018 Research Projects as of March 27, 2018 CARBON MANAGEMENT IMPACTS ON ELECTRICITY MARKETS IN CANADA This project is designed to gain insights into challenges and opportunities carbon management

2017-2018 Research Projects as of March 27, 2018 CARBON MANAGEMENT IMPACTS ON ELECTRICITY MARKETS IN CANADA This project is designed to gain insights into challenges and opportunities carbon management

Status of Shale Gas Development in New Brunswick. Habitation 2012

Status of Shale Gas Development in New Brunswick Angie Leonard, Senior Advisor, CAPP Habitation 2012 St. Andrews, New Brunswick February 9, 2012 What Is CAPP? CAPP s mission is to enhance the economic

Status of Shale Gas Development in New Brunswick Angie Leonard, Senior Advisor, CAPP Habitation 2012 St. Andrews, New Brunswick February 9, 2012 What Is CAPP? CAPP s mission is to enhance the economic

British Columbia s Carbon Tax Strengths and Opportunities

British Columbia s Carbon Tax Strengths and Opportunities Submission to the Select Standing Committee on Finance and Government Services Oct 24, 2008 Submitted by: Matt Horne B.C. Energy Solutions program,

British Columbia s Carbon Tax Strengths and Opportunities Submission to the Select Standing Committee on Finance and Government Services Oct 24, 2008 Submitted by: Matt Horne B.C. Energy Solutions program,

A Federal View of Canada s Oil and Gas Sector. John Foran Director, Oil & Gas Policy and Regulatory Affairs Division Natural Resources Canada

A Federal View of Canada s Oil and Gas Sector John Foran Director, Oil & Gas Policy and Regulatory Affairs Division Natural Resources Canada Outline of Remarks 2 Purpose: 15 minute overview to spur discussion

A Federal View of Canada s Oil and Gas Sector John Foran Director, Oil & Gas Policy and Regulatory Affairs Division Natural Resources Canada Outline of Remarks 2 Purpose: 15 minute overview to spur discussion

International and Intergovernmental Relations

International and Intergovernmental Relations BUSINESS PLAN 2006-09 ACCOUNTABILITY STATEMENT The business plan for the three years commencing April 1, 2006 was prepared under my direction in accordance

International and Intergovernmental Relations BUSINESS PLAN 2006-09 ACCOUNTABILITY STATEMENT The business plan for the three years commencing April 1, 2006 was prepared under my direction in accordance

As the Government of Canada advances the development of Budget 2017, outlined below are priority recommendations from Teck for your consideration.

Marcia Smith Senior Vice President, Sustainability and External Affairs marcia.smith@teck.com Teck Resources Limited Suite 3300, 550 Burrard Street Vancouver, BC Canada V6C 0B3 +1 604 699 4616 Dir +1 604

Marcia Smith Senior Vice President, Sustainability and External Affairs marcia.smith@teck.com Teck Resources Limited Suite 3300, 550 Burrard Street Vancouver, BC Canada V6C 0B3 +1 604 699 4616 Dir +1 604

Ministry of the Economy. Plan for saskatchewan.ca

Ministry of the Economy Plan for 2016-17 saskatchewan.ca Table of Contents Statement from the Ministers... 1 Response to Government Direction... 2 Operational Plan... 3 Highlights...10 Financial Summary...11

Ministry of the Economy Plan for 2016-17 saskatchewan.ca Table of Contents Statement from the Ministers... 1 Response to Government Direction... 2 Operational Plan... 3 Highlights...10 Financial Summary...11

Liquefied natural gas, carbon pollution, and British Columbia in 2017

Liquefied natural gas, carbon pollution, and British Columbia in 2017 An overview of B.C. LNG issues in the context of climate change by Dylan Heerema and Maximilian Kniewasser August 2017 Summary The

Liquefied natural gas, carbon pollution, and British Columbia in 2017 An overview of B.C. LNG issues in the context of climate change by Dylan Heerema and Maximilian Kniewasser August 2017 Summary The

NATIONAL ENERGY BOARD

NATIONAL ENERGY BOARD IN THE MATTER OF the National Energy Board Act, RSC 1985, c N- 7, as may be amended from time to time, and the Regulations made thereunder; AND IN THE MATTER OF an application by

NATIONAL ENERGY BOARD IN THE MATTER OF the National Energy Board Act, RSC 1985, c N- 7, as may be amended from time to time, and the Regulations made thereunder; AND IN THE MATTER OF an application by

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

Monthly Snapshot August 31, 2014

Monthly Snapshot August 31, 2014 The following organizations and consultant lobbyists submitted their registrations under the BC Lobbyists Registration Act between August 1 and August 31, 2014. Here is

Monthly Snapshot August 31, 2014 The following organizations and consultant lobbyists submitted their registrations under the BC Lobbyists Registration Act between August 1 and August 31, 2014. Here is

LNG Market Outlook and Arbitrage Opportunities

LNG Market Outlook and Arbitrage Opportunities Rajnish Goswami Senior Vice President Head of Gas & Power Consulting Asia Workshop on Liberialisation of Malaysian Gas Market KL, 23 April 2015 1 Trusted

LNG Market Outlook and Arbitrage Opportunities Rajnish Goswami Senior Vice President Head of Gas & Power Consulting Asia Workshop on Liberialisation of Malaysian Gas Market KL, 23 April 2015 1 Trusted

OUTLINE PART I: Introduction to Alaska and its Enormous Resource Basin PART II: Progress on Gas Commercialization/LNG PART III: Why Alaska? Comparativ

ALASKA GAS OPPORTUNITIES LNG PRODUCER- CONSUMER CONFERENCE Tokyo, Japan September 19, 2012 Commissioner Daniel S. Sullivan Alaska Department of Natural Resources www.dnr.alaska.gov OUTLINE PART I: Introduction

ALASKA GAS OPPORTUNITIES LNG PRODUCER- CONSUMER CONFERENCE Tokyo, Japan September 19, 2012 Commissioner Daniel S. Sullivan Alaska Department of Natural Resources www.dnr.alaska.gov OUTLINE PART I: Introduction

Hydraulic Fracturing Principles and Operating Practices

Hydraulic Fracturing Principles and Operating Practices Select Committee on Hydraulic Fracturing January 31, 2014 Alex Ferguson, VP Policy & Environment 1 Hydraulic Fracturing is not new Natural gas and

Hydraulic Fracturing Principles and Operating Practices Select Committee on Hydraulic Fracturing January 31, 2014 Alex Ferguson, VP Policy & Environment 1 Hydraulic Fracturing is not new Natural gas and

Canadian Oil and Gas Industry: What lies ahead

Canadian Oil and Gas Industry: What lies ahead Presented by Dinara Millington Vice President, Research Canadian Energy Research Institute June 10, 2015 1 Canadian Energy Research Institute Overview Founded

Canadian Oil and Gas Industry: What lies ahead Presented by Dinara Millington Vice President, Research Canadian Energy Research Institute June 10, 2015 1 Canadian Energy Research Institute Overview Founded

Searching for Tight Gas Reservoirs By Alex Chakhmakhchev and Kris McKnight

Searching for Tight Gas Reservoirs By Alex Chakhmakhchev and Kris McKnight Along with coal bed methane (CBM) and shale gas, tight gas is becoming a hot exploration target around the globe. This paper examines

Searching for Tight Gas Reservoirs By Alex Chakhmakhchev and Kris McKnight Along with coal bed methane (CBM) and shale gas, tight gas is becoming a hot exploration target around the globe. This paper examines

2018/ /21 SERVICE PLAN

Ministry of Energy, Mines and Petroleum Resources 2018/19 SERVICE PLAN February 2018 For more information on the Ministry of Energy, Mines and Petroleum Resources contact: Deputy Minister s Office PO BOX

Ministry of Energy, Mines and Petroleum Resources 2018/19 SERVICE PLAN February 2018 For more information on the Ministry of Energy, Mines and Petroleum Resources contact: Deputy Minister s Office PO BOX

Our Strategy for Climate Action

Our Strategy for Climate Action Introduction Climate change is real, it is directly influenced by human activity, and it requires decisive global action to address. At Teck, we believe our company and

Our Strategy for Climate Action Introduction Climate change is real, it is directly influenced by human activity, and it requires decisive global action to address. At Teck, we believe our company and

Mineral Exploration Challenges and Opportunities

Mineral Exploration Challenges and Opportunities Minerals North Thursday, April 27, 2006 Dan M. Jepsen, RPF President & CEO Association for Mineral Exploration British Columbia (AME BC) Over 3,700 individual

Mineral Exploration Challenges and Opportunities Minerals North Thursday, April 27, 2006 Dan M. Jepsen, RPF President & CEO Association for Mineral Exploration British Columbia (AME BC) Over 3,700 individual

International and Intergovernmental Relations

BUSINESS PLAN 2000-03 International and Intergovernmental Relations ACCOUNTABILITY STATEMENT This Business Plan for the three years commencing April 1, 2000 was prepared under my direction in accordance

BUSINESS PLAN 2000-03 International and Intergovernmental Relations ACCOUNTABILITY STATEMENT This Business Plan for the three years commencing April 1, 2000 was prepared under my direction in accordance

POTENTIAL GAS COMMITTEE REPORTS INCREASE IN MAGNITUDE OF U.S. NATURAL GAS RESOURCE BASE

For Release April 8, 2015, 1100 EDT Contact: Dr. John B. Curtis, Potential Gas Agency, Colorado School of Mines, Golden, CO 80401-1887. Telephone 303-273-3886; fax 303-273-3574; ldepagni@mines.edu. POTENTIAL

For Release April 8, 2015, 1100 EDT Contact: Dr. John B. Curtis, Potential Gas Agency, Colorado School of Mines, Golden, CO 80401-1887. Telephone 303-273-3886; fax 303-273-3574; ldepagni@mines.edu. POTENTIAL

TRINIDAD AND TOBAGO ENERGY CONFERENCE JANUARY 2017

BY TRINIDAD AND TOBAGO ENERGY CONFERENCE JANUARY 2017 *No. of unique client sites Independent and neutral insight. The Rystad Energy business data solution is global. 400 350 300 250 200 150 100 50 0 2010

BY TRINIDAD AND TOBAGO ENERGY CONFERENCE JANUARY 2017 *No. of unique client sites Independent and neutral insight. The Rystad Energy business data solution is global. 400 350 300 250 200 150 100 50 0 2010

THE ENERGY DEVELOPMENT CYCLE

THE ENERGY DEVELOPMENT CYCLE PRE-PROJECT EXPLORATION APPRAISAL & DEVELOPMENT OPERATION CLOSURE USE Risks & Opportunities Across the Development Cycle Activities prior to the start of the individual project

THE ENERGY DEVELOPMENT CYCLE PRE-PROJECT EXPLORATION APPRAISAL & DEVELOPMENT OPERATION CLOSURE USE Risks & Opportunities Across the Development Cycle Activities prior to the start of the individual project

World and U.S. Fossil Fuel Supplies

World and U.S. Fossil Fuel Supplies Daniel O Brien and Mike Woolverton, Extension Agricultural Economists K State Research and Extension Supplies of fossil fuel resources used for energy production vary

World and U.S. Fossil Fuel Supplies Daniel O Brien and Mike Woolverton, Extension Agricultural Economists K State Research and Extension Supplies of fossil fuel resources used for energy production vary

Unconventional Gas Market Appraisal

Unconventional Gas Market Appraisal Chris Bryceland June 2013 Agenda Headline facts Fundamentals of unconventional gas Global resources Selected markets Economic impacts Supply chain opportunities Conclusions

Unconventional Gas Market Appraisal Chris Bryceland June 2013 Agenda Headline facts Fundamentals of unconventional gas Global resources Selected markets Economic impacts Supply chain opportunities Conclusions

Shale Gas Global. New Zealand LPG

Shale Gas Global New Zealand LPG New Zealand LPG Where to from here? 2 LPG ('000 Tonnes) 300 LPG Production and Demand to 2018 (calendar year) 250 200 150 100 50 0 2000 2005 2010 2015 Kapuni Kupe McKee/Mangahewa

Shale Gas Global New Zealand LPG New Zealand LPG Where to from here? 2 LPG ('000 Tonnes) 300 LPG Production and Demand to 2018 (calendar year) 250 200 150 100 50 0 2000 2005 2010 2015 Kapuni Kupe McKee/Mangahewa

Province of British Columbia and First Nations LNG Alliance Joint Engagement Report

Province of British Columbia and First Nations LNG Alliance Joint Engagement Report Contents 1. EXECUTIVE SUMMARY 4 2. BACKGROUND AND METHODOLOGY 6 3. STATUS OF THE LNG INDUSTRY IN BC 7 4. REGIONAL ENGAGEMENT

Province of British Columbia and First Nations LNG Alliance Joint Engagement Report Contents 1. EXECUTIVE SUMMARY 4 2. BACKGROUND AND METHODOLOGY 6 3. STATUS OF THE LNG INDUSTRY IN BC 7 4. REGIONAL ENGAGEMENT

The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports.

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

For personal use only

Horizon Oil Limited ABN 51 009 799 455 Level 6, 134 William Street, Woolloomooloo NSW Australia 2011 Tel +61 2 9332 5000, Fax +61 2 9332 5050 www.horizonoil.com.au 29 November 2017 The Manager, Company

Horizon Oil Limited ABN 51 009 799 455 Level 6, 134 William Street, Woolloomooloo NSW Australia 2011 Tel +61 2 9332 5000, Fax +61 2 9332 5050 www.horizonoil.com.au 29 November 2017 The Manager, Company

Opportunities and Challenges in the Energy Infrastructure Industry. Louisiana State University Energy Summit

Opportunities and Challenges in the Energy Infrastructure Industry Louisiana State University Energy Summit 1 Kinder Morgan Overview Kinder Morgan is the largest midstream and the third largest energy

Opportunities and Challenges in the Energy Infrastructure Industry Louisiana State University Energy Summit 1 Kinder Morgan Overview Kinder Morgan is the largest midstream and the third largest energy

Workshop on APEC Coal Supply Security Tokyo 20 March 2015

Workshop on APEC Coal Supply Security Tokyo 20 March 2015 Possible coal supply risk factors that influence Asia-Pacific markets: A Canadian perspective Francois Nguyen, Principal, Global Energy Strategic

Workshop on APEC Coal Supply Security Tokyo 20 March 2015 Possible coal supply risk factors that influence Asia-Pacific markets: A Canadian perspective Francois Nguyen, Principal, Global Energy Strategic

THE NORTHERN GATEWAY PIPELINE: A POSSIBLE CORRIDOR TO SEED RENEWABLE ENERGY IN BRITISH COLUMBIA, CANADA. McGill University, Montreal, Quebec, H3A 2A7

World Mining Congress 2013 THE NORTHERN GATEWAY PIPELINE: A POSSIBLE CORRIDOR TO SEED RENEWABLE ENERGY IN BRITISH COLUMBIA, CANADA Mory Ghomshei 1,2,*, Ferri Hassani 1, John Meech 2, and Nima Mousavi 3

World Mining Congress 2013 THE NORTHERN GATEWAY PIPELINE: A POSSIBLE CORRIDOR TO SEED RENEWABLE ENERGY IN BRITISH COLUMBIA, CANADA Mory Ghomshei 1,2,*, Ferri Hassani 1, John Meech 2, and Nima Mousavi 3

American Strategy and US Energy Independence

Cordesman: Strategy and Energy Independence 10/21/13 1 American Strategy and US Energy Independence By Anthony H. Cordesman October 21, 2013 Changes in energy technology, and in the way oil and gas reserves

Cordesman: Strategy and Energy Independence 10/21/13 1 American Strategy and US Energy Independence By Anthony H. Cordesman October 21, 2013 Changes in energy technology, and in the way oil and gas reserves

LAND AND WATER BRITISH COLUMBIA INC. A Corporation of the Government of British Columbia

LAND AND WATER BRITISH COLUMBIA INC. A Corporation of the Government of British Columbia Service Plan Fiscal 2003/2004-2005/2006 National Library of Canada Cataloguing in Publication Data Land and Water

LAND AND WATER BRITISH COLUMBIA INC. A Corporation of the Government of British Columbia Service Plan Fiscal 2003/2004-2005/2006 National Library of Canada Cataloguing in Publication Data Land and Water

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

For personal use only. AWE Limited. Asian Roadshow Presentation. June 2012

AWE Limited Asian Roadshow Presentation June 2012 Disclaimer This presentation may contain forward looking statements that are subject to risk factors associated with the oil and gas businesses. It is

AWE Limited Asian Roadshow Presentation June 2012 Disclaimer This presentation may contain forward looking statements that are subject to risk factors associated with the oil and gas businesses. It is

Responsible Shale Development. Enhancing the Knowledge Base on Shale Oil and Gas in Canada

Responsible Shale Development Enhancing the Knowledge Base on Shale Oil and Gas in Canada Energy and Mines Ministers Conference Yellowknife, Northwest Territories August 2013 Responsible Shale Development:

Responsible Shale Development Enhancing the Knowledge Base on Shale Oil and Gas in Canada Energy and Mines Ministers Conference Yellowknife, Northwest Territories August 2013 Responsible Shale Development:

Developments in North American Oil, Gas, and LNG

Developments in North American Oil, Gas, and LNG Presented to the Australian Institute of Energy September 29, 2015 David L. Wochner, Partner, Washington, DC Copyright 2015 by K&L Gates LLP. All rights

Developments in North American Oil, Gas, and LNG Presented to the Australian Institute of Energy September 29, 2015 David L. Wochner, Partner, Washington, DC Copyright 2015 by K&L Gates LLP. All rights

Responsible Energy Development Capitalizing on the Benefits of shale gas and tight oil development in Atlantic Canada

Responsible Energy Development Capitalizing on the Benefits of shale gas and tight oil development in Atlantic Canada Core Energy Conference October 8, 2014 Bob Bleaney VP, External Affairs Canadian Association

Responsible Energy Development Capitalizing on the Benefits of shale gas and tight oil development in Atlantic Canada Core Energy Conference October 8, 2014 Bob Bleaney VP, External Affairs Canadian Association

US Oil and Gas Import Dependence: Department of Energy Projections in 2011

1800 K Street, NW Suite 400 Washington, DC 20006 Phone: 1.202.775.3270 Fax: 1.202.775.3199 Email: acordesman@gmail.com Web: www.csis.org/burke/reports US Oil and Gas Import Dependence: Department of Energy

1800 K Street, NW Suite 400 Washington, DC 20006 Phone: 1.202.775.3270 Fax: 1.202.775.3199 Email: acordesman@gmail.com Web: www.csis.org/burke/reports US Oil and Gas Import Dependence: Department of Energy

Balanced Budget B 2007

3 3 4 3 4 3 2 0 0 0 6 0 8 8 8 0 0 0 0 1 Balanced Budget B 2007 0 B 1 2 3 0 0 0 5 4 6 7 2 0 0 6 0 7 0 0 8 0 0 5 0 0 0 0 9 0 8 0 7 0 0 0 6 0 5 0 0 Ministry of Economic Development 2007/08 2009/10 SERVICE

3 3 4 3 4 3 2 0 0 0 6 0 8 8 8 0 0 0 0 1 Balanced Budget B 2007 0 B 1 2 3 0 0 0 5 4 6 7 2 0 0 6 0 7 0 0 8 0 0 5 0 0 0 0 9 0 8 0 7 0 0 0 6 0 5 0 0 Ministry of Economic Development 2007/08 2009/10 SERVICE

World Energy Outlook 2035: A focus on LNG supply and demand dynamics

World Energy Outlook 2035: A focus on LNG supply and demand dynamics M.H. Siddiqui, Prescience, USA 1 Agenda The Energy Outlook in 2035 involving major landscape changes in supply, demand, fossil fuels,

World Energy Outlook 2035: A focus on LNG supply and demand dynamics M.H. Siddiqui, Prescience, USA 1 Agenda The Energy Outlook in 2035 involving major landscape changes in supply, demand, fossil fuels,

HORIZON OIL (HZN) PNG PETROLEUM AND ENERGY SUMMIT PRESENTATION

PNG PETROLEUM AND ENERGY SUMMIT PRESENTATION") Horizon Oil Limited ABN 51 009 799 455 Level 6, 134 William Street, Woolloomooloo NSW Australia 2011 Tel +61 2 9332 5000, Fax +61 2 9332 5050 www.horizonoil.com.au The Manager, Company Announcements ASX

Horizon Oil Limited ABN 51 009 799 455 Level 6, 134 William Street, Woolloomooloo NSW Australia 2011 Tel +61 2 9332 5000, Fax +61 2 9332 5050 www.horizonoil.com.au The Manager, Company Announcements ASX

Sound Marketing for a FLNG Development

Sound Marketing for a FLNG Development Alessandro Della Zoppa EVP LNG eni Midstream Gas & Power Gastech Tokyo, 6 th April 2017 company overview Italian Government 30% 70% Market exploration & production

Sound Marketing for a FLNG Development Alessandro Della Zoppa EVP LNG eni Midstream Gas & Power Gastech Tokyo, 6 th April 2017 company overview Italian Government 30% 70% Market exploration & production

NARUC. Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

POTENTIAL GAS COMMITTEE REPORTS UNPRECEDENTED INCREASE IN MAGNITUDE OF U.S. NATURAL GAS RESOURCE BASE

For Release June 18, 2009, 1100 EDT Contact: Dr. John B. Curtis, Potential Gas Agency, Colorado School of Mines, Golden, CO 80401-1887. Telephone 303-273-3886; fax 303-273-3574; ldepagni@mines.edu. POTENTIAL

For Release June 18, 2009, 1100 EDT Contact: Dr. John B. Curtis, Potential Gas Agency, Colorado School of Mines, Golden, CO 80401-1887. Telephone 303-273-3886; fax 303-273-3574; ldepagni@mines.edu. POTENTIAL

Executive Summary. 6 Natural Resource Permitting Project

Section 1 Executive Summary Initiative Summary Initiative Name 1 : Initiative Abbreviation: Initiative Description: NRPP Implementation Programs 2 : Lead Sector, Ministry or Agency: Need for Investment:

Section 1 Executive Summary Initiative Summary Initiative Name 1 : Initiative Abbreviation: Initiative Description: NRPP Implementation Programs 2 : Lead Sector, Ministry or Agency: Need for Investment:

Increasing Industrial Demand As Easy (or not) as 1, 2, 3

as 1, 2, 3") Increasing Industrial Demand As Easy (or not) as 1, 2, 3 Marcellus & Manufacturing Conference Charleston, WV March 23, 2016 API s Market Development Group API is the only national trade association representing

Increasing Industrial Demand As Easy (or not) as 1, 2, 3 Marcellus & Manufacturing Conference Charleston, WV March 23, 2016 API s Market Development Group API is the only national trade association representing

International Shale Development Challenges & Opportunities: Argentina

International Shale Development Challenges & Opportunities: Argentina October 21, 2015 Chuck Whisman, Global Energy Market Director, CH2M Charles.Whisman@ch2m.com Discussion Overview Review History of

International Shale Development Challenges & Opportunities: Argentina October 21, 2015 Chuck Whisman, Global Energy Market Director, CH2M Charles.Whisman@ch2m.com Discussion Overview Review History of

Major Changes in Natural Gas Transportation Capacity,

Major Changes in Natural Gas Transportation, The following presentation was prepared to illustrate graphically the areas of major growth on the national natural gas pipeline transmission network between

Major Changes in Natural Gas Transportation, The following presentation was prepared to illustrate graphically the areas of major growth on the national natural gas pipeline transmission network between

HORIZON OIL (HZN) PNG INVESTMENT CONFERENCE PRESENTATION

PNG INVESTMENT CONFERENCE PRESENTATION") Horizon Oil Limited ABN 51 009 799 455 Level 6, 134 William Street, Woolloomooloo NSW Australia 2011 Tel +61 2 9332 5000, Fax +61 2 9332 5050 www.horizonoil.com.au 7 September 2017 The Manager, Company

Horizon Oil Limited ABN 51 009 799 455 Level 6, 134 William Street, Woolloomooloo NSW Australia 2011 Tel +61 2 9332 5000, Fax +61 2 9332 5050 www.horizonoil.com.au 7 September 2017 The Manager, Company

2016/ /19 SERVICE PLAN

Ministry of Aboriginal Relations and Reconciliation SERVICE PLAN February 2016 For more information on the British Columbia Ministry of Aboriginal Relations and Recociliation, see Ministry Contact Information

Ministry of Aboriginal Relations and Reconciliation SERVICE PLAN February 2016 For more information on the British Columbia Ministry of Aboriginal Relations and Recociliation, see Ministry Contact Information

Mineral Resource Policy for New Brunswick

Mineral Resource Policy for New Brunswick Natural Resources and Energy DECEMBER 1993 ISBN 1-55137-110-3 TABLE OF CONTENTS page Introduction... 1 Investment Climate and Land Use... 2 Priority lnitiatives...

Mineral Resource Policy for New Brunswick Natural Resources and Energy DECEMBER 1993 ISBN 1-55137-110-3 TABLE OF CONTENTS page Introduction... 1 Investment Climate and Land Use... 2 Priority lnitiatives...

Shale Gas as an Alternative Petrochemical Feedstock

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Industry Perspectives on Oil and Gas Development in Canada s Arctic: Opportunities and Challenges

Industry Perspectives on Oil and Gas Development in Canada s Arctic: Opportunities and Challenges Paul Barnes, Manager - Atlantic Canada & Arctic Presentation to Nunavut Oil and Gas Summit Iqaluit, Nunavut

Industry Perspectives on Oil and Gas Development in Canada s Arctic: Opportunities and Challenges Paul Barnes, Manager - Atlantic Canada & Arctic Presentation to Nunavut Oil and Gas Summit Iqaluit, Nunavut

2010/ /13 SERVICE PLAN

Ministry of Energy, Mines and Petroleum Resources 2010/11 2012/13 SERVICE PLAN March 2010 For more information on the British Columbia Ministry of Energy, Mines and Petroleum Resources see Ministry Contact

Ministry of Energy, Mines and Petroleum Resources 2010/11 2012/13 SERVICE PLAN March 2010 For more information on the British Columbia Ministry of Energy, Mines and Petroleum Resources see Ministry Contact

APPENDIX C: FUEL PRICE FORECAST

Seventh Northwest Conservation and Electric Power Plan APPENDIX C: FUEL PRICE FORECAST Contents Introduction... 3 Dealing with Uncertainty and Volatility... 4 Natural Gas... 5 Background... 5 Price Forecasts...

Seventh Northwest Conservation and Electric Power Plan APPENDIX C: FUEL PRICE FORECAST Contents Introduction... 3 Dealing with Uncertainty and Volatility... 4 Natural Gas... 5 Background... 5 Price Forecasts...

Prospects for unconventional natural gas supply in Asia

Perth, 16 February 2016 Prospects for unconventional natural gas supply in Asia Roberto F. Aguilera Background Expansion of natural gas share in primary energy mix, especially Asia Gas demand is dominated

Perth, 16 February 2016 Prospects for unconventional natural gas supply in Asia Roberto F. Aguilera Background Expansion of natural gas share in primary energy mix, especially Asia Gas demand is dominated

Briefing Memo: The Aphrodite gas field and the southeastern Mediterranean's new energy triangle THE HELLENIC AMERICAN LEADERSHIP COUNCIL

THE HELLENIC AMERICAN LEADERSHIP COUNCIL Briefing Memo: The Aphrodite gas field and the southeastern Mediterranean's new energy triangle Prepared by: Georgia Logothetis Managing Director Hellenic American

THE HELLENIC AMERICAN LEADERSHIP COUNCIL Briefing Memo: The Aphrodite gas field and the southeastern Mediterranean's new energy triangle Prepared by: Georgia Logothetis Managing Director Hellenic American

The Tar Sands and a Cap and Trade System for Reducing Greenhouse Gas Pollution

The Tar Sands and a Cap and Trade System for Reducing Greenhouse Gas Pollution The election of President Barack Obama has significantly changed the political landscape for action on climate change in the

The Tar Sands and a Cap and Trade System for Reducing Greenhouse Gas Pollution The election of President Barack Obama has significantly changed the political landscape for action on climate change in the

CHAPTER 2: CARBON CAPTURE AND STORAGE

CHAPTER 2: CARBON CAPTURE AND STORAGE INTRODUCTION This chapter provides an assessment of the role of carbon capture and storage (CCS) in Qatar and other Gulf Cooperation Council (GCC) countries; barriers

CHAPTER 2: CARBON CAPTURE AND STORAGE INTRODUCTION This chapter provides an assessment of the role of carbon capture and storage (CCS) in Qatar and other Gulf Cooperation Council (GCC) countries; barriers

Prudent Development. Realizing the Potential of North America s Abundant Natural Gas and Oil Resources

Prudent Development Realizing the Potential of North America s Abundant Natural Gas and Oil Resources A Comprehensive Assessment to 2035 with Views through 2050 September 15, 2011 1 Today s Discussion

Prudent Development Realizing the Potential of North America s Abundant Natural Gas and Oil Resources A Comprehensive Assessment to 2035 with Views through 2050 September 15, 2011 1 Today s Discussion

Making Cents of the Eastern Australian Gas Market

Making Cents of the Eastern Australian Gas Market Professor Quentin Grafton (Quentin.Grafton@anu.edu.au) Crawford School of Public Policy The Australian National University 29 November 2017 Based on co-authored

Making Cents of the Eastern Australian Gas Market Professor Quentin Grafton (Quentin.Grafton@anu.edu.au) Crawford School of Public Policy The Australian National University 29 November 2017 Based on co-authored

2018/ /21 SERVICE PLAN

Ministry of Jobs, Trade and Technology 2018/19 2020/21 SERVICE PLAN February 2018 For more information on the Ministry of Jobs, Trade and Technology contact: Ministry of Jobs, Trade and Technology PO BOX

Ministry of Jobs, Trade and Technology 2018/19 2020/21 SERVICE PLAN February 2018 For more information on the Ministry of Jobs, Trade and Technology contact: Ministry of Jobs, Trade and Technology PO BOX

Copies of this strategy are available from:

Copies of this strategy are available from: Alberta Human Resources and Employment 6 th floor, Centre West Building 10035-108 th Street Edmonton, AB T5J 3E1 Phone: (780) 644-4306 Toll-free in Alberta,

Copies of this strategy are available from: Alberta Human Resources and Employment 6 th floor, Centre West Building 10035-108 th Street Edmonton, AB T5J 3E1 Phone: (780) 644-4306 Toll-free in Alberta,

LNG TRADE FLOWS. Hans Stinis Shell Upstream International

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

Labour Market Information ( ) Engineers, Geoscientists, Technologists and Technicians in B.C.

Engineers, Geoscientists, Technologists and Technicians in B.C.") Labour Market Information (2015-2024) Engineers, Geoscientists, Technologists and Technicians in B.C. As part of its Labour Market Information Project, the Asia Pacific Gateway Skills Table provides in-depth

Labour Market Information (2015-2024) Engineers, Geoscientists, Technologists and Technicians in B.C. As part of its Labour Market Information Project, the Asia Pacific Gateway Skills Table provides in-depth

Benchmarking of Sawmill Industries in North America, Europe, Chile, Australia and New Zealand

Benchmarking of Sawmill Industries in North America, Europe, Chile, Australia and New Zealand An intensive examination of the costs and efficiencies of sawmilling industries Over $10 billion of investment

Benchmarking of Sawmill Industries in North America, Europe, Chile, Australia and New Zealand An intensive examination of the costs and efficiencies of sawmilling industries Over $10 billion of investment

National Energy Board. Report on Plans and Priorities Part III Estimates. The Honourable Christian Paradis, P.C., M.P.

National Energy Board Report on Plans and Priorities 2010-2011 Part III Estimates Gaétan Caron Chair and CEO National Energy Board The Honourable Christian Paradis, P.C., M.P. Minister Natural Resources

National Energy Board Report on Plans and Priorities 2010-2011 Part III Estimates Gaétan Caron Chair and CEO National Energy Board The Honourable Christian Paradis, P.C., M.P. Minister Natural Resources

Ministry of Finance Comptroller General Victoria, BC

Ministry of Finance Comptroller General Victoria, BC Provide your strong leadership, financial aptitude, and communication skills to this integral role in the executive team The Ministry of Finance plays

Ministry of Finance Comptroller General Victoria, BC Provide your strong leadership, financial aptitude, and communication skills to this integral role in the executive team The Ministry of Finance plays

Anadarko LNG and China

Anadarko LNG and China Scott Moore Vice President Worldwide Marketing US-China Oil and Gas Industry Forum September 26, 2014 Regarding Forward-Looking Statements and Other Matters This presentation contains

Anadarko LNG and China Scott Moore Vice President Worldwide Marketing US-China Oil and Gas Industry Forum September 26, 2014 Regarding Forward-Looking Statements and Other Matters This presentation contains

AmCham EU position on Shale Gas Development in the EU

AmCham EU position on Shale Gas Development in the EU Page 1 of 6 7 February 2014 AmCham EU position on Shale Gas Development in the EU Background A number of EU Member States are exploring the potential

AmCham EU position on Shale Gas Development in the EU Page 1 of 6 7 February 2014 AmCham EU position on Shale Gas Development in the EU Background A number of EU Member States are exploring the potential

Alliance Pipeline. BMO Western Canadian Tour

Alliance Pipeline BMO Western Canadian Tour September 16, 2014 Forward-Looking Information Certain information contained in this presentation constitutes forwardlooking statements. The words anticipate,

Alliance Pipeline BMO Western Canadian Tour September 16, 2014 Forward-Looking Information Certain information contained in this presentation constitutes forwardlooking statements. The words anticipate,

Potential Supply of Natural Gas in the United States Report of the Potential Gas Committee (December 31, 2016)

") Potential Supply of Natural Gas in the United States Report of the Potential Gas Committee (December 31, 2016) Press Conference, Washington, D.C., July 19, 2017 Executive Summary 2 Potential Gas Committee

Potential Supply of Natural Gas in the United States Report of the Potential Gas Committee (December 31, 2016) Press Conference, Washington, D.C., July 19, 2017 Executive Summary 2 Potential Gas Committee

Oil and Gas Exploration and Pipelines

Oil and Gas Exploration and Pipelines Highlights Issues covered today will touch on a few concepts that have been presented in the course Externalities (difference between private and social cost) Shadow

Oil and Gas Exploration and Pipelines Highlights Issues covered today will touch on a few concepts that have been presented in the course Externalities (difference between private and social cost) Shadow

2015/ /18 SERVICE PLAN

Ministry of Aboriginal Relations and Reconciliation SERVICE PLAN February 2015 For more information on the British Columbia Ministry of Aboriginal Relations and Reconciliation, see Ministry Contact Information

Ministry of Aboriginal Relations and Reconciliation SERVICE PLAN February 2015 For more information on the British Columbia Ministry of Aboriginal Relations and Reconciliation, see Ministry Contact Information

BRITISH COLUMBIA INSTITUTE OF TECHNOLOGY

BRITISH COLUMBIA INSTITUTE OF TECHNOLOGY THREE-YEAR BUSINESS PLAN 2014 /15 2016 /17 September 2014 95% Employment among recent degree graduates One of BC s Top Employers since 2011 TABLE OF CONTENTS Executive

BRITISH COLUMBIA INSTITUTE OF TECHNOLOGY THREE-YEAR BUSINESS PLAN 2014 /15 2016 /17 September 2014 95% Employment among recent degree graduates One of BC s Top Employers since 2011 TABLE OF CONTENTS Executive

Investor Presentation September 2016

Investor Presentation September 2016 1 LEGAL DISCLAIMER Statements made by representatives for ATCO Ltd. and information provided in this presentation may be considered forward-looking statements. By their

Investor Presentation September 2016 1 LEGAL DISCLAIMER Statements made by representatives for ATCO Ltd. and information provided in this presentation may be considered forward-looking statements. By their

Labour Market Information, Engineers, Geoscientists, Technologists and Technicians in B.C.

Labour Market Information, 2015-2024 Engineers, Geoscientists, Technologists and Technicians in B.C. As part of its Labour Market Information Project, Asia Pacific Gateway Skills Table provides in-depth

Labour Market Information, 2015-2024 Engineers, Geoscientists, Technologists and Technicians in B.C. As part of its Labour Market Information Project, Asia Pacific Gateway Skills Table provides in-depth

AGM Presentation and Strategy Update

AGM Presentation and Strategy Update RBR Group Limited () 29 November 2016 Business Snapshot Diversified labour services and training provider complementary businesses with retained exposure to resources

AGM Presentation and Strategy Update RBR Group Limited () 29 November 2016 Business Snapshot Diversified labour services and training provider complementary businesses with retained exposure to resources

The subordinate legal or constitutional status of local government has been a long-standing concern of local government in British Columbia.

APPENDIX C TO: FROM: UBCM Members Councillor Joanne Monaghan, President DATE: September 8, 1995 RE: RECOGNITION OF LOCAL GOVERNMENT AS AN ORDER OF GOVERNMENT ITEM #3(a) October 4, 1995 B.C. COMMUNITIES

APPENDIX C TO: FROM: UBCM Members Councillor Joanne Monaghan, President DATE: September 8, 1995 RE: RECOGNITION OF LOCAL GOVERNMENT AS AN ORDER OF GOVERNMENT ITEM #3(a) October 4, 1995 B.C. COMMUNITIES

BC HYDRO DRAFT INTEGRATED RESOURCE PLAN 2012

BC HYDRO DRAFT INTEGRATED RESOURCE PLAN 2012 A Plan to Meet B.C. s Future Electricity Needs EXECUTIVE SUMMARY May 2012 bchydro.com/irp INTRODUCTION TO THE DRAFT PLAN Electricity powers our lives it lights

BC HYDRO DRAFT INTEGRATED RESOURCE PLAN 2012 A Plan to Meet B.C. s Future Electricity Needs EXECUTIVE SUMMARY May 2012 bchydro.com/irp INTRODUCTION TO THE DRAFT PLAN Electricity powers our lives it lights

Clean-Tech Innovation Strategy for the B.C. Forest Sector

Clean-Tech Innovation Strategy for the B.C. Forest Sector 2016 2024 One of the keys to having a globally competitive forest sector is the commitment to innovation, whether it s new harvesting techniques,

Clean-Tech Innovation Strategy for the B.C. Forest Sector 2016 2024 One of the keys to having a globally competitive forest sector is the commitment to innovation, whether it s new harvesting techniques,

11/18/2011. Moderate demand increase High depletion rate. Alfa Laval 1. Sammy Hulpiau Segment Manager Energy & Environment. mb/d.

Oil & Gas Sammy Hulpiau Segment Manager Energy & Environment Oil production investments are rapidly growing mb/d 120 100 80 60 NGLs Unconventional oil Crude oil fields yet to be developed or found Crude

Oil & Gas Sammy Hulpiau Segment Manager Energy & Environment Oil production investments are rapidly growing mb/d 120 100 80 60 NGLs Unconventional oil Crude oil fields yet to be developed or found Crude

Energy in Australia: A Queensland Perspective

Energy in Australia: A Queensland Perspective David Camerlengo Trade & Investment Commissioner, North America Trade & Investment Queensland API, Houston May 13, 2014 Overview of Queensland Source: BREE

Energy in Australia: A Queensland Perspective David Camerlengo Trade & Investment Commissioner, North America Trade & Investment Queensland API, Houston May 13, 2014 Overview of Queensland Source: BREE

LNG Market through. Serving the Asia Pacific. Jordan Cove LNG. Vern A. Wadey. Vice President

Serving the Asia Pacific LNG Market through Jordan Cove LNG Vern A. Wadey Vice President Pacific North West Economic Region 25th Annual Summit Big Sky, Montana Monday, July 13, 2015 Veresen Inc.: A strong,

Serving the Asia Pacific LNG Market through Jordan Cove LNG Vern A. Wadey Vice President Pacific North West Economic Region 25th Annual Summit Big Sky, Montana Monday, July 13, 2015 Veresen Inc.: A strong,

INDUSTRY TRAINING AUTHORITY THREE-YEAR STRATEGIC PLAN Three-Year Strategic Plan:

INDUSTRY TRAINING AUTHORITY THREE-YEAR STRATEGIC PLAN 2017 2019 Three-Year Strategic Plan: 2017 2019 1 The Industry Training Authority (ITA) is leading an ambitious and innovative three-year journey to

INDUSTRY TRAINING AUTHORITY THREE-YEAR STRATEGIC PLAN 2017 2019 Three-Year Strategic Plan: 2017 2019 1 The Industry Training Authority (ITA) is leading an ambitious and innovative three-year journey to

British Columbia s. VVater Act. Modernization. Policy Proposal on British Columbia s new Water Sustainability Act. December 2010

British Columbia s VVater Act Modernization Policy Proposal on British Columbia s new Water Sustainability Act December 2010 British Columbia has a rich heritage in our lakes, rivers and streams. Linked

British Columbia s VVater Act Modernization Policy Proposal on British Columbia s new Water Sustainability Act December 2010 British Columbia has a rich heritage in our lakes, rivers and streams. Linked

Integrated Resource Plan. Appendix 2A Electric Load Forecast

Integrated Resource Plan Appendix 2A 2012 Electric Load Forecast Electric Load Forecast Fiscal 2013 to Fiscal 2033 Load and Market Forecasting Energy Planning and Economic Development BC Hydro 2012 Forecast

Integrated Resource Plan Appendix 2A 2012 Electric Load Forecast Electric Load Forecast Fiscal 2013 to Fiscal 2033 Load and Market Forecasting Energy Planning and Economic Development BC Hydro 2012 Forecast

International Energy Outlook: key findings in the 216 Reference case World energy consumption increases from 549 quadrillion Btu in 212 to 629 quadril

EIA's Global Energy Outlook For The Institute of Energy Economics, Japan October 5, 216 Japan By Adam Sieminski, Administrator U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

EIA's Global Energy Outlook For The Institute of Energy Economics, Japan October 5, 216 Japan By Adam Sieminski, Administrator U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

The Economic Value of American Coal Exports

August 2012 The Economic Value of American Coal Exports Summary of Findings The United States has the world s largest endowment of low-cost, high quality coal reserves. These reserves can be competitively

August 2012 The Economic Value of American Coal Exports Summary of Findings The United States has the world s largest endowment of low-cost, high quality coal reserves. These reserves can be competitively

Energy and Natural Resources

Energy and Natural Resources 7.1 Introduction This chapter evaluates the potential impacts of the proposed project s Technology and Marine Terminal Alternatives and a No-Action Alternative, as well as

Energy and Natural Resources 7.1 Introduction This chapter evaluates the potential impacts of the proposed project s Technology and Marine Terminal Alternatives and a No-Action Alternative, as well as

Alaska South Central LNG (SCLNG) Project

Project") Alaska South Central LNG (SCLNG) Project Overview for Alaska Legislators February, 2013 - Overview BP, ConocoPhillips, ExxonMobil and TransCanada are working together to progress an Alaska LNG project:

Alaska South Central LNG (SCLNG) Project Overview for Alaska Legislators February, 2013 - Overview BP, ConocoPhillips, ExxonMobil and TransCanada are working together to progress an Alaska LNG project: