Energy Q&A. NAESB, 8 April 2015 BEG/CEE-UT, 1

|

|

|

- Ralf Jones

- 5 years ago

- Views:

Transcription

1 Energy Q&A NAESB, 8 April 2015 BEG/CEE-UT, 1

2 PRICE TRENDS BEG/CEE-UT, 2

3 Oil Price History $160 $140 $120 Cushing, OK WTI Spot Price FOB (Dollars per Barrel) Europe Brent Spot Price FOB (Dollars per Barrel) WTI-Brent Spread "Arab Spring" 2010 $10 Saudi Market $5 Share Strategy II 2014 $0 Price, $/BBL $100 $80 $60 $40 $20 Saudi Market Share Strategy I, 1986 Desert Storm, 1990 USD Neutral Asia Financial Collapse, China "Coming Out: Party, Iraq War, U.S.-Europe Financial Collapse, USD Neutral US LTO Glut -$5 -$10 -$15 -$20 -$25 WTI minus Brent, $/BBL $0 -$30 CME/NYMEX, EIA, CEE compilation BEG/CEE-UT, 3

4 Gas Price History $16 $14 Henry Hub Monthly Average Spot Price ($/MMBtu) Avg Feb 89-Feb 92 ($1.61) Avg Mar 92-Dec 98 ($2.11) U.S. shale gas drilling boom U.S. shale oil drilling boom $12 $10 $8 Avg Jan 99-Dec 01 ($3.46) Avg Jan 02-Sep 09 ($6.32) Avg Oct 09-Present ($3.83) GOM Hurricane Events El Paso pipeline explosion, Carlsbad, NM August 19, 2000 California market failure, Peak LNG imports with new regas capacity March-August 2007 Feb 2007, "Henry Hub at $3 or $5 published (Foss, OIES NG 18) Dec 2011, "Henry Hub at $3 or $10 published (Foss, OIES NG 58) $6 $ Energy Policy Act $2 Enron bankruptcy December 4, 2001 Lehman Brothers bankruptcy September 15, 2008 $0 Feb-89 Feb-90 Feb-91 Feb-92 Feb-93 Feb-94 Feb-95 Feb-96 Feb-97 Feb-98 Feb-99 Feb-00 Feb-01 Feb-02 Feb-03 Feb-04 Feb-05 Feb-06 Feb-07 Feb-08 Feb-09 Feb-10 Feb-11 Feb-12 Feb-13 Feb-14 Feb-15 CME/NYMEX, EIA, CEE compilation BEG/CEE-UT, 4

5 Price Drivers and Expectations Oil Saudi/GCC market share strategy and demand response US LTO surplus (condy) Iran, Iraq current/potential capacity, 9 MMBD (black oil) ST still price shoes to drop, MT long recovery ( at least 5 years until see $100 oil, if), 1990s scenario Gas Domestic drivers: unmotivated producers, motivated customers Policy impacts NAM trade ST already see effects of oil price, MT wellhead value likely sustained by HH BEG/CEE-UT, 5

6 PRODUCTION BEG/CEE-UT, 6

7 Shales: A Quick History Long history of production from shales example, Antrim in Michigan Upper Bakken vertical wells drilled, 1976 Upper Bakken horizontal wells drilled, 1987 Mitchell Energy drills vertical wells in Barnett (Texas) in 1989 Baker Hughes acquires Eastman Christensen for horizontal drilling tool and other technology 1990 National Petroleum Council seminal natural gas supply study points to role of non-conventional sources (CBM, shale, tight sands), 1992 Chevron drills Barnett vertical wells and improves measures of oil and gas in place (OGIP) measures, 1997 Mitchell absorbs CVX talent, demonstrates hydraulic fracturing, use of 3-D seismic, slick water frac Devon acquires Mitchell, 2002, spawns a series of transactions that expanded or created new unconventional players BEG/CEE-UT, 7

8 Perspective Helps Everybody looked at that technology (Mitchell Energy) was developing of hydraulic fracturing and said it doesn t work, said Devon Energy s co-founder and chief executive officer, Larry Nichols recalls in a company video here. It s old, it s tired... there s nothing there. Everyone knows that. Don t waste your time. From The Energy Fix, Jim Pierobon, 5 August BEG/CEE-UT, 8

9 *Feeling the need the need for shale: Oil 350,000 Federal OCS--Gulf of Mexico Field Production Midwest (PADD 2) Field Production Gulf Coast (PADD 3) Field Production U.S. Field Production of Crude Oil 300, ,000 Production from shale is about 70% of U.S. total Thousand Barrels 200, , ,000 Mainly West Texas and Eagle Ford 50,000 Mainly Bakken 0 Top Gun BEG/CEE-UT, 9

10 Feeling the need the need for shale: Gas 35,000,000 Canada remains about 10% of total dry gas supply 30,000,000 Now 50% of production Million Cubic Feet 25,000,000 20,000,000 15,000,000 10,000,000 Onshore (Conventional) CBM Shale 5,000,000 - Offshore (Federal, State) Note: 2014 data are estimates Gross withdrawals; CEE based on EIA and other sources BEG/CEE-UT, 10

11 Do producers like to lose money? Oil 50% 40% Y-Y Chg U.S. Crude Oil Production Y-Y Chg WTI Initial shale oil tests 200% 150% 30% 20% 100% Y-Y Chg Production 10% 0% -10% 50% 0% Y-Y Chg WTI -20% -30% Many reasons for recent production growth including: lease requirements, hedging, need to sustain cash flows -50% -100% BEG/CEE-UT, 11

12 Do producers like to lose money? Gas 20% 15% Y-Y Chg U.S. Natural Gas Marketed Production Y-Y Chg Henry Hub Dry Gas production drop 300% with low gas price 250% 10% 200% Y-Y Chg Production 5% 0% -5% 150% 100% 50% 0% Y-Y Chg HH -10% -15% -50% AG production surge with high oil price -100% BEG/CEE-UT, 12

13 Eagle Ford Shale BEG/CEE-UT, 13

from all wells drilled in the Middle Bakken from")

14 Bakken Shale: Middle Bakken TudorPickeringHolt & Co. Note: Represents cumulative 12-month production (mboe) from all wells drilled in the Middle Bakken from Source: ESRI, Drilling Info, TPH Research BEG/CEE-UT, 14

15 Bakken Shale: Three Forks TudorPickeringHolt & Co. Note: Represents cumulative 12-month production (mboe) from all wells drilled in the Three Forks from Source: ESRI, Drilling Info, TPH Research BEG/CEE-UT, 15

16 Shale Oil View: TPH Comments on Bakken Industry focused on driving down well costs over the last few years after costs surged on tight service capacity and accelerated drilling programs. With held by production (HBP) commitments met and well costs reduced 15-20%, the industry focused in earnest on optimizing completions. While drilling efficiencies may continue to improve, many operators saw spud to total depth (TD) times approaching 20 days, making additional drilling cost reductions harder to achieve. One size will NOT fit all. Operators testing a variety of completion designs across the basin with a particular interest in slickwater fracs and a trend towards larger volumes of smaller mesh proppant. In general, better quality acreage is the focus of new completions designs. Tests expanding into Tier 2 positions. Ceramics: To use or not to use? That is the question. Some operators in the deeper part of the basin are doubling down and increasing ceramic use, while others are shifting their capital in favor of larger volumes of sand (100 mesh and #40/70 mesh sand). Completions being tested Slickwater hydraulic fracturing Increased proppant volumes: 2-10x standard completions in the basin Increased stage count combined with higher density clusters on plug and perf designs BEG/CEE-UT, 16

")

17 Barnett Shale BEG Shale Gas Resource Assessment (Sloan Foundation) BEG/CEE-UT, 17

BEG/CEE-UT,")

18 Haynesville Shale OGIP free Productivity Overpressured BEG Shale Gas Resource Assessment (Sloan Foundation) BEG/CEE-UT, 18

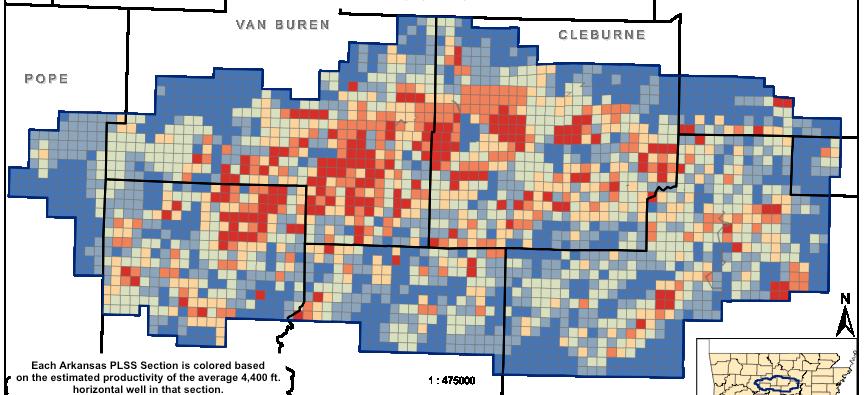

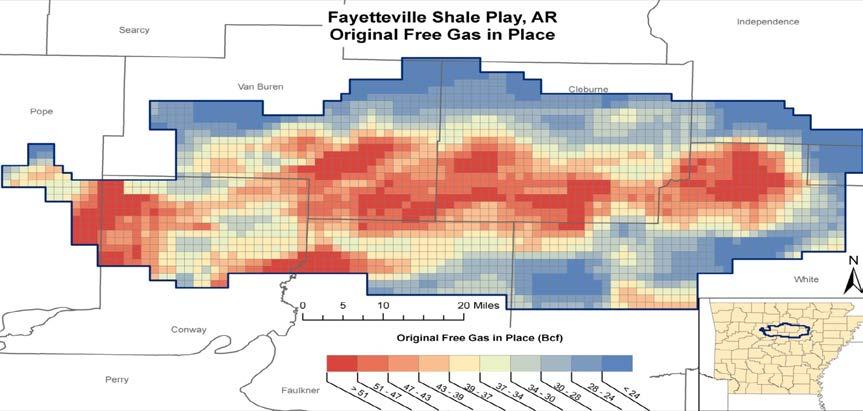

19 Fayetteville Shale OGIP free Natural Fractures Productivity BEG Shale Gas Resource Assessment (Sloan Foundation) BEG/CEE-UT, 19

20 Type Curves and Costs: Preliminary Results Do not cite BEG Shale Gas Resource Assessment (Sloan Foundation) BEG/CEE-UT, 20

21 Well Economics $18 $16 $14 $12 $10 $8 $6 $4 $2 Barnett Low Btu Barnett High Btu Fville Shallow Fville Medium Fville Deep Hville PA Dry PA Wet PA Rich Do not cite $0 Tier 1 Tier 2 Tier 3 Tier 4 Tier 5 Tier 6 Tier 7 Tier 8 Tier 9 Tier 10 What matters most: Costs (depth & length), by-products (ng vs. liquids), taxes. BEG Shale Gas Resource Assessment (Sloan Foundation) BEG/CEE-UT, 21

22 Tcf / year Production Sensitivity to Price 6$/MMBtu EIA price 4$/MMBtu Do not cite We expect liquids rollover to follow a similar, perhaps faster, path BEG Shale Gas Resource Assessment (Sloan Foundation) BEG/CEE-UT, 22

23 ECONOMICS BEG/CEE-UT, 23

24 Wellhead BE does not necessarily = Company BE Fast NPV attractive to investors Companies need enough tails to support business Continuous outlays of capital Onshore shale oil and offshore deep water can demonstrate comparable returns over time ainabilitypossible/shale-bubble/ 3% Challenge for companies is building robust portfolios Companies report only best wells ( 3% of total ) Company portfolios are highly variable (acreage, liquids, recovery, cost) Companies routinely deploy 100% of capital across portfolios in which, on average, 80% of production comes from 20% of fracs 67% 30% Best Wells, NPV>0 BE Wells, NPV=0 Worst Wells, NPV<0 BEG/CEE-UT, 24

25 Upstream Matters! Part Deux We add 2014 reporting data and affirm key considerations going forward Our sample represents the top tier of U.S. producers including leading shale players. We have *restated work from earlier research for changes to our sample and methodology The 15 publicly traded companies we use comprise 68% of Top 40 gas producers (NGSA.org) and 33% of U.S. marketed natural gas production In this snapshot including 2014 reporting we state results mainly in barrel of oil equivalent terms Overall, while FD capex has dropped, largely a result of increased volumes, cash costs remain substantial and stubborn High Cost Producer Average Low Cost Producer High Cost Producer Average Low Cost Producer High Cost Producer Average Low Cost Producer High Cost Producer Average Low Cost Producer High Cost Producer Average Low Cost Producer High Cost Producer Average Low Cost Producer $0 $20 $40 $60 $80 $100 3-Yr MA FD Costs/3-Yr MA Additions ($/BOE) Annual Cash Costs per Bbl of Production ($/BOE) FD = capital spending for exploration and development, calculated on a 3-year basis and applied to 3-year reserve additions as a moving average (MA) Cash cost = current year lease operating expense, general and administra tive, marketing, taxes (including state production tax), interest on debt, applied to current year production The cheapest producers are also the gassiest smaller companies that, for the most part, did not move out of gas and into liquids because of cost and capital constraints. BEG/CEE-UT, 25 *

26 How much spending? With what results?? 3-Year Capex Spending ($MM) $300,000 15,167 $250,000 11,969 3-Year Reserve Additions (MMBOE) 16,000 14,409 13,767 14,000 12,107 12,000 In the complex commodity markets of today, U.S. producer performance and cost is increasingly relied upon as a guide to possible floor prices and longer term price trends. We use 3 year rolling total FD spending against 3 year reserve additions to reach FD/BOE. The capex requirements to high grade upstream, especially shale, portfolios has been considerable, exceeding $270 billion by Substantial write downs and impairments were taken in 2012 (slide 3) as a result of the steep fall in gas prices. Reductions in capex are discernible when 2013 data are added but rose again in We use cash cost against current production for cash cost/boe. Companies have grown production on a BOE basis by about 22 percent since Natural gas remains the dominant proportion of production streams but 2014 showed a marked shift. This pattern holds when we compare our results to other research. 9 of the 15 companies in our sample are predominantly gas producers (50 to nearly 100 percent of production) including 6 that are among the shale specialists and 1 integrated major. Capex Total Production (MMBOE) $200,000 8,993 10,000 $150,000 8,000 $270,763 $210,908 $228,185 $100,000 $224,103 $241,876 6,000 $170,556 4,000 $50,000 2,000 $ U.S. Total Production (MMBOE) Ratio of Natural Gas:Total U.S. Production 3,000 64% 2,500 2,000 1,500 1, % 62% 2,466 2,511 61% 61% 2,380 60% 2,215 2,059 59% 2,036 58% 57% 56% 54% 53% 52% 50% Additions Natural Gas Split % BEG/CEE-UT, 26

27 Bonus: Sources of Additions 8,000 6,000 Most booked additions come from drilling out acreage as opposed to improved recovery. 4,000 2, ,000-4,000 Purchases of Reserves (MMBOE) Extensions & Discoveries (MMBOE) Improved Recovery (MMBOE) Total Revisions (MMBOE) BEG/CEE-UT, 27

28 Computing Returns U.S. producers have demonstrated success in key shale plays but it is not an easy business. In BOE terms, on average and as of 2014, the full cycle cost for our sample is close to $50 per BOE with a 10 percent return assumed. However, a 10 percent return does not provide sufficient recovery of capital spent in a current year. Alternatively, we use a return equal to capex spent that year against current production. With the alternative criteria imposed, the average full cycle cost for 2014 was about $80 per BOE. We believe this suggests an oil price signal of at least $80 is needed to sustain activity for our sample and the industry. We note that many producers realize considerably less than the traded domestic oil prices. Condensate, the main component of many production streams, typically sells $20-25 below West Texas Intermediate. Overall, the industry remains predominantly cash flow negative. Companies have had to spend capital well above cash flow from operations to replace production and improve leasehold positions. With lower oil prices companies are working to adjust capital spending to fall within cash flows. $50 $40 $30 $20 $10 $0 $100 $80 $60 $40 $20 $0 10% Return ($/BOE) Annual Cash Costs per Bbl of Production ($/BOE) 3-Yr MA FD Costs/3-Yr MA Additions ($/BOE) Return of Current Capex ($/BOE) Annual Cash Costs per Bbl of Production ($/BOE) 3-Yr MA FD Costs/3-Yr MA Additions ($/BOE) BEG/CEE-UT, 28

29 Implications for Gas While the pressure is on from oil prices, the implications for natural gas are more interesting to consider. With a 10 percent return assumed, the minimum back to producers and their investors, the implied natural gas price is close to $8 per million Btu (MMBtu). However this only returns a portion of current capex. To return 2014 capex producers would have needed an implied price of more than $13, on average. Much of the incremental gas supply for the U.S. in recent years has come in association with liquids production or where enough ethane is present and can be captured to justify drilling in nonassociated (dry) gas locations. Perhaps as much as 50 percent or more of U.S. gas supply is linked to liquids prices. As a result, oil prices are being watched closely for hints about gas supply and price impacts. Our full report with 2014 data is forthcoming in April $9 $8 $7 $6 $5 $4 $3 $2 $1 $0 $18 $16 $14 $12 $10 $8 $6 $4 $2 $0 10% Return ($/MCFE) Annual Cash Costs per Bbl of Production ($/MCFE) 3-Yr MA FD Costs/3-Yr MA Additions ($/MCFE) Henry Hub Spot Price $ Return of Current Capex ($/MCFE) Annual Cash Costs per Bbl of Production ($/MCFE) 3-Yr MA FD Costs/3-Yr Additions ($/MCFE) Henry Hub Spot Price $ BEG/CEE-UT, 29

30 Bonus: It Takes an Industry An industry leader with an early shift to liquids 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% U.S. NGL Production (MMBOE) U.S. Gas Production (MMBOE) $120 $100 $80 $60 $40 $20 $ EOG Resources U.S. Oil and Liquids Production (MMBOE) U.S. Total Production (MMBOE) Return of Current Capex ($/BOE) Annual Cash Cost ($/BOE) 3-Yr MA FD Costs ($/BOE) 0 Note: Began separating oil and NGLs in % 90% 80% 70% 60% 50% 40% 30% 20% 10% % U.S. NGL Production (MMBOE) U.S. Oil and Liquids Production (MMBOE) $70 $60 $50 $40 $30 $20 $10 $0 A successful gassy player U.S. Gas Production (MMBOE) Range Resources U.S. Total Production (MMBOE) 71 Return of Current Capex ($/BOE) Annual Cash Costs ($/BOE) 3-Yr MA FD Costs ($/BOE) BEG/CEE-UT, 30

31 Comparative View Capex exceeds cash flows Bernstein Research BEG/CEE-UT, 31

32 Comparative View and has done so historically Bernstein Research BEG/CEE-UT, 32

33 Weighted Average NOC Breakeven Costs* ($/BOE) $120 $100 $94 $101 $80 $60 $40 $65 $76 $81 $80 10% ROI Annual Cap. Exp. $20 $ *10% ROI represented 30% of capital expenditures CEE analysis based on company reports BEG/CEE-UT, 33

34 Weighted Average NOC Breakeven Costs ($/BOE) $120 $100 $80 $60 $40 $ $94 $ Annual Cap. Exp. Fiscal Contribution Cash Op. Exp. Find. & Dev. Costs $20 $ CEE analysis based on company reports BEG/CEE-UT, 34

35 NOC Breakeven Costs 2013 ($/BOE) $200 $180 $160 $140 $120 $100 $80 $60 $40 $20 $0 $78 $8 $8 $96 $98 $119 $120 $12 $107 $145 $18 Cap. Exp. Fiscal Contribution Cash Op. Exp. Find. & Dev. Costs *Ecopetrol production taxes included in production costs **CNOOC capital expenditures increased from $12 billion in 2012 to $41 billion CEE analysis based on company reports BEG/CEE-UT, 35

36 DEMAND BEG/CEE-UT, 36

37 World Oil Demand (MBD) Governments are seizing the opportunity to eliminate subsidies North Amwerica Europe & Erasia Central & South America North America Africa & Mid East Asia-Pacific Based on data from EIA BEG/CEE-UT, 37

38 A strong demand stack scenario TCF LNG Exports 2030 = 1.0 (EIA ER = 3.5) Pipe Exports 2030 = 3.9 (EIA ER = 3.4) LNG exports CEE Pipeline exports CEE Power generation CEE Power 2030 = 15.9 (EIA ER = 10.1) CEE assumes all possible EPA actions Industrial 2030 = 8.8 (EIA ER = 8.5) Industrial CEE Other (Res, Comm, Trans) EIA ER Dec 2013 Total demand CEE High Case 5 Other 2030 = 10.8 (residential+ commercial 10.5) Total supply EIA ER Dec 2013 CEE analysis; EIA ER refers to EIA 2014 Early Release, Dec 2013 (reference case) BEG/CEE-UT, 38

39 Industrial Demand: Robust Plans BCFD Steel MTG Hydrogen Chlor-Alkali Methanol Nitrogen fertilizers Propylene Polyethylene Ethylene Base Demand (2012) CEE s industrial projects inventory BEG/CEE-UT, 39

40 Gas Demand by Region, End User BCFD Steel MTG Hydrogen Chlor-Alkali Methanol Nitrogen fertilizers Propylene Polyethylene Ethylene 0 LA TX Rest of US CEE s industrial projects inventory BEG/CEE-UT, 40

41 Investment by Region $billion LA Rest of US TX CEE s industrial projects inventory BEG/CEE-UT, 41

42 Projects by Region Project type LA Rest of US TX Total Chlor-Alkali Ethylene GTL Hydrogen Methanol MTG Nitrogen fertilizers Polyethylene Propylene Steel Grand Total BEG/CEE-UT, 42

43 Drivers: Relative Prices BEG/CEE-UT, 43

44 Drivers: BEG/CEE-UT, 44

45 Power: Competing Views Based on data from EIA AEO 2013 and IHSE BEG/CEE-UT, 45

Announced about 29 GW (2014-2020) BEG/CEE-UT,")

46 Coal Retirements About 50 GW of coal capacity may retire by 2020 Almost 21 GW already retired (mostly older units) Announced about 29 GW ( ) BEG/CEE-UT, 46

47 Nuclear Relicensing? 4 recent announcements, more possible but our modeling does not retire nuclear units 5,500 MW in 3 plants under construction BEG/CEE-UT, 47

48 Resulting Scenario on Gas Use in Power Incorporates a higher, more volatile gas price. BEG/CEE-UT, 48

Value chain integrity supporting infrastructure ( both")

Streamline existing process for long term optionality (exports, imports) Transport modes, risks, policy/regulatory considerations Perception of risk view: less drilling =")

49 Exports: The Crude Oil Debate Is exporting crude oil a problem?? yes no Upstream economics, impacts on wellhead value Regulatory efficiency (political risk of alternative approaches) Value chain integrity supporting infrastructure ( both regulatory process and infrastructure are so 70s ) Enough companies can get exemptions, approvals Revoke EAA or remove all hydrocarbon components (chance of success?) Streamline existing process for long term optionality (exports, imports) Transport modes, risks, policy/regulatory considerations Perception of risk view: less drilling = less production = fewer nuisances and hazards Quick fix to add condensate to CCL (or remove, whichever is correct) BEG/CEE-UT, 49

50 TRADE BEG/CEE-UT, 50

51 O Canada! Getting Their Dander Up Enbridge Eastern Access TransCanada Energy East BEG/CEE-UT, 51

52 Gas Exports: The Future? 2013: U.S. is 29% of Canadian consumption 2013: U.S. is 29% of Mexican consumption ~2x current NA exports by 2020? ~9+ BCFD Map presents a possible gas flow scenario, Foss, Ch. 3 in Pricing Internationally Traded Gas, Oxford, 2012; gas trade data from EIA BEG/CEE-UT, 52

53 LNG: Europe or Asia? Neither? 12 JCC Feb NBP April JKM April Europe Europe Europe Asia Asia Asia Henry Hub Liquefaction Shipping JKM JCC NBP Pertamina, Endesa SA, Iberdrola, EDF, EDP, Gas Natural fenosa, Woodside Energy Trading have signed PSA for $3.50/MMBtu BEG/CEE-UT, 53

54 Is U.S. LNG Competitive? $/MMBtu $10 Japan pre- Fukushima $9-11 NBP Regasification Shipping Liquefaction Field to Terminal Henry Hub Sep 14 NBP $ $14-19 Asia spot The Attraction "Reality" High Cost Delivery to Atlantic Basin High Cost Delivery to Pacific Basin Sep 14 LNG $ Super High Cost Delivery to Pacific Basin mpetitive.pdf BEG/CEE-UT, 54

55 OTHER BEG/CEE-UT, 55

56 Impact of anchoring Dan Ariely, Predictably Irrational, 2009 BEG/CEE-UT, 56

57 Predictable irrationality Anchor prices, arbitrary coherence Herding, self-propelling Perception of value with anchoring Persistence of perception with herding Impact of initial decision on future expectations Price manipulation (by both private market participants and governments) Dan Ariely, Predictably Irrational, 2009 BEG/CEE-UT, 57

58 In short, we re a mess Illusion of truth Confirmation bias Hindsight bias Halo effect Sunk-cost fallacy Loss aversion Self-serving Lady Macbeth effect Framing Availability heuristic We re more likely to believe a familiar statement Tendency to favor information that confirms our beliefs Duh! principle One trait influences others as we make judgments They matter (!), because we are more afraid of incurring losses than acquiring gains, and we ll happily claim responsibility for success more often than failure, but just to be sure Out, damn spot! We have blinders and silos Predict frequency based on how easily an example comes to mind BEG/CEE-UT, 58

59 In love with fear itself Beard/dp/ /ref=sr_1_1?s=books&ie=UTF8&qi d= &sr=1-1&keywords=paranoiaca BEG/CEE-UT, 59

60 Why this stuff matters It is much easier [and] more enjoyable to identify and label the mistakes of others than to recognize our own Most of our judgments and actions are appropriate most of the time We are often confident even when we are wrong In at least some cases, an accurate diagnosis may suggest an intervention to limit the damage that bad judgments and choices often cause BEG/CEE-UT, 60

")

61 unusual (but not unprecedented) Texas Insider; Mulvaney, et.al., BEG/CEE-UT, 61

62 Courtesy Dr. John Christy, NOAA-University of Alabama Huntsville, above as appeared in Wall Street Journal, right as appeared in What s Up with That. BEG/CEE-UT, 62

in the context of natural")

63 Dynamic Earth Sea Surface Temp. Although warming of the northeastern Antarctic Peninsula began around 600 years ago, the high rate of warming over the past century is unusual (but not unprecedented) in the context of natural climate variability over the past two millennia. JRI Ice Core Temp. Mean (black lines are estimates of open water based on sediment cores) BAS Ice Core Temp. Mulvaney, et.al., Nature 11391; SOTU 2014 BEG/CEE-UT, 63

64 The Role of Science BEG/CEE-UT, 64

65 The 6X Gap BEG/CEE-UT, 65

66 An Impact (Scale) 5 Energy GHG (Climate) 4 Energy Security Web Envt (Land, Water) 0 Safety Coal Natural Gas LNG Nuclear Envt (Air) Reliability Hydroelectric Solar, Wind (grid-based) Solar, Distributed Market Friendly BEG/CEE-UT, 66

67 An Energy Web GHG (Climate) Impact (Scale) Energy Security 2 1 Envt (Land, Water) 0 Safety Coal Natural Gas LNG Nuclear Hydroelectric Envt (Air) Reliability Solar, Wind (grid-based) Solar, Distributed Market Friendly BEG/CEE-UT, 67

68 Contact Information All work in progress is located on CEE address - energyecon@beg.utexas.edu BEG/CEE-UT, 68

Major Challenges for Gas: What Can be Expected for Mexico?

Major Challenges for Gas: What Can be Expected for Mexico? Gas Future Forum, Mexico, April 3, 2014 BEG/CEE UT, 1 Overall Observations Resources Reserves Deliverability Deliverability is key Sweet spot

Major Challenges for Gas: What Can be Expected for Mexico? Gas Future Forum, Mexico, April 3, 2014 BEG/CEE UT, 1 Overall Observations Resources Reserves Deliverability Deliverability is key Sweet spot

Five Things You Should Know

Bureau of Economic Geology, Jackson School of Geosciences, The University of Texas at Austin Five Things You Should Know Tx Industries of the Future, March 7, 2013 M.M. Foss, 9/25/2012, BEG/CEE-UT, 1 #1

Bureau of Economic Geology, Jackson School of Geosciences, The University of Texas at Austin Five Things You Should Know Tx Industries of the Future, March 7, 2013 M.M. Foss, 9/25/2012, BEG/CEE-UT, 1 #1

Going through Another Cycle

Global Rig Count Down 5 Since Nov ; Recent Uptick Driven by North America Capital spending cut significantly IEA: $583 billion upstream (25% less than ) IEA: Further 24% drop expected in 216 Going through

Global Rig Count Down 5 Since Nov ; Recent Uptick Driven by North America Capital spending cut significantly IEA: $583 billion upstream (25% less than ) IEA: Further 24% drop expected in 216 Going through

US Energy Independence & Energy Exports

US Energy Independence & Energy Exports Fred C. Beach, Ph.D. Earth Wind & Fire Conference Addison, TX. 4 October, 2014 10/12/2014 1 Global Consumption Trends 2011 Energy Consumption, + 2.5% OEDC, Down

US Energy Independence & Energy Exports Fred C. Beach, Ph.D. Earth Wind & Fire Conference Addison, TX. 4 October, 2014 10/12/2014 1 Global Consumption Trends 2011 Energy Consumption, + 2.5% OEDC, Down

Paradoxically Abundant?

Paradoxically Abundant? Mayer Brown, Houston, April 1, 2014 BEG/CEE UT, 1 200 180 140 120 Simon Erlich Wager Metals & Minerals Non Fuel 160 Energy 100 80 2010=100 120 60 40 20 0 Do cartels succeed? It

Paradoxically Abundant? Mayer Brown, Houston, April 1, 2014 BEG/CEE UT, 1 200 180 140 120 Simon Erlich Wager Metals & Minerals Non Fuel 160 Energy 100 80 2010=100 120 60 40 20 0 Do cartels succeed? It

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

Natural Gas Trends LNG 17 NYC, June 28, 2011

Bureau of Economic Geology, The University of Texas at Austin Natural Gas Trends LNG 17 NYC, June 28, 211 Balancing Our Energy Future What do we want? Safe, clean, affordable, (abundant) energy Reduced

Bureau of Economic Geology, The University of Texas at Austin Natural Gas Trends LNG 17 NYC, June 28, 211 Balancing Our Energy Future What do we want? Safe, clean, affordable, (abundant) energy Reduced

Oil and natural gas: market outlook and drivers

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Trends, Issues and Market Changes for Crude Oil and Natural Gas

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Natural Gas Abundance: The Development of Shale Resource in North America

Natural Gas Abundance: The Development of Shale Resource in North America EBA Brown Bag Luncheon Bracewell & Giuliani Washington, D.C. February 6, 2013 Bruce B. Henning Vice President, Energy Regulatory

Natural Gas Abundance: The Development of Shale Resource in North America EBA Brown Bag Luncheon Bracewell & Giuliani Washington, D.C. February 6, 2013 Bruce B. Henning Vice President, Energy Regulatory

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer.

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2012-13 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2012 Introduction This report presents ICF s

Winter 2012-13 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2012 Introduction This report presents ICF s

Oil and Gas in 2018: Markets, Spending, Projects. Bob Tippee Editor, Oil & Gas Journal Rice Global E&C Forum March 9, 2018

Oil and Gas in 2018: Markets, Spending, Projects Bob Tippee Editor, Oil & Gas Journal Rice Global E&C Forum March 9, 2018 For discussion Oil and gas markets will have a transformative year OPEC wants to

Oil and Gas in 2018: Markets, Spending, Projects Bob Tippee Editor, Oil & Gas Journal Rice Global E&C Forum March 9, 2018 For discussion Oil and gas markets will have a transformative year OPEC wants to

The US shale revolution and its economic impact

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

U.S. Shale Gas in Context

U.S. Shale Gas in Context Overview of U.S. Natural Gas production and trends For National Conference of State Legislatures Natural Gas Policy Institute September 9, 215 Pittsburgh, Pennsylvania By Grant

U.S. Shale Gas in Context Overview of U.S. Natural Gas production and trends For National Conference of State Legislatures Natural Gas Policy Institute September 9, 215 Pittsburgh, Pennsylvania By Grant

What s Going on With Energy? How Unconventional Oil & Gas Development is Impacting Renewables, Efficiency, Power Markets and All That Other Stuff

What s Going on With Energy? How Unconventional Oil & Gas Development is Impacting Renewables, Efficiency, Power Markets and All That Other Stuff Atlanta Economics Club Monthly Meeting December 10, 2012

What s Going on With Energy? How Unconventional Oil & Gas Development is Impacting Renewables, Efficiency, Power Markets and All That Other Stuff Atlanta Economics Club Monthly Meeting December 10, 2012

UNDERSTANDING NATURAL GAS MARKETS. Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015

UNDERSTANDING NATURAL GAS MARKETS Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015 Table of Contents 3 Overview Natural Gas is an Important Source of Energy for the United States.

UNDERSTANDING NATURAL GAS MARKETS Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015 Table of Contents 3 Overview Natural Gas is an Important Source of Energy for the United States.

Global energy markets

For Woodrow Wilson Center Global Energy Forum September 21, 215 Washington, DC by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent

For Woodrow Wilson Center Global Energy Forum September 21, 215 Washington, DC by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent

Energy Prospectus Group

Energy Prospectus Group Founded in 2001 Current Membership is 530 We have members in 38 states and eight countries ~ 60% of our members live in Texas Mission is to help our members make money Luncheons

Energy Prospectus Group Founded in 2001 Current Membership is 530 We have members in 38 states and eight countries ~ 60% of our members live in Texas Mission is to help our members make money Luncheons

Outlook for the Upstream Sector of the Oil and Gas Industry

Outlook for the Upstream Sector of the Oil and Gas Industry VMA Market Outlook Workshop Chicago, IL Spears & Associates Tulsa, OK August 2015 Million bbls/day 3.5 World Oil Demand Growth/US Oil Supply

Outlook for the Upstream Sector of the Oil and Gas Industry VMA Market Outlook Workshop Chicago, IL Spears & Associates Tulsa, OK August 2015 Million bbls/day 3.5 World Oil Demand Growth/US Oil Supply

North American Midstream Infrastructure Through 2035 A Secure Energy Future. Press Briefing June 28, 2011

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

World and U.S. Oil and Gas Production and Price Outlook: To Infinity (or at least 2050) and Beyond

and Beyond") World and U.S. Oil and Gas Production and Price Outlook: To Infinity (or at least 25) and Beyond Energy and Environment Symposium April 18, 218 Rifle, Colorado by Troy Cook, Senior Global Upstream Analyst,

World and U.S. Oil and Gas Production and Price Outlook: To Infinity (or at least 25) and Beyond Energy and Environment Symposium April 18, 218 Rifle, Colorado by Troy Cook, Senior Global Upstream Analyst,

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

Natural Gas. Tuesday, May 1, 2012; 4:00 PM 5:15 PM

Natural Gas Tuesday, May 1, 2012; 4:00 PM 5:15 PM Moderator: Joel Kurtzman, Senior Fellow and Executive Director of the Center for Accelerating Energy Solutions, Milken Institute Speakers: Ralph Eads,

Natural Gas Tuesday, May 1, 2012; 4:00 PM 5:15 PM Moderator: Joel Kurtzman, Senior Fellow and Executive Director of the Center for Accelerating Energy Solutions, Milken Institute Speakers: Ralph Eads,

International gas markets: recent developments and prospects

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves

1 of 5 3/14/2013 11:37 PM U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves With Data for Release Date: August 1, 2012 Next Release Date: March 2013 Previous Issues: Year: Summary Proved reserves

1 of 5 3/14/2013 11:37 PM U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves With Data for Release Date: August 1, 2012 Next Release Date: March 2013 Previous Issues: Year: Summary Proved reserves

API Industry Outlook. Third Quarter R. Dean Foreman, Ph.D. Great Plains and EmPower ND Energy Conference October 8, 2018.

API Industry Outlook Third Quarter 2018 R. Dean Foreman, Ph.D. Chief Economist American Petroleum Institute Great Plains and EmPower ND Energy Conference October 8, 2018 American Updated Petroleum September

API Industry Outlook Third Quarter 2018 R. Dean Foreman, Ph.D. Chief Economist American Petroleum Institute Great Plains and EmPower ND Energy Conference October 8, 2018 American Updated Petroleum September

The New Superpower : Emerging Supplies of Gas Liquids from the United States

The New Superpower : Emerging Supplies of Gas Liquids from the United States Lucian Pugliaresi President Energy Policy Research Foundation, Inc. Washington, DC Energy Policy Research Foundation, Inc. 1031

The New Superpower : Emerging Supplies of Gas Liquids from the United States Lucian Pugliaresi President Energy Policy Research Foundation, Inc. Washington, DC Energy Policy Research Foundation, Inc. 1031

Oil and gas outlook. For New York Energy Forum October 15, 2015 New York, NY. By Adam Sieminski, Administrator. U.S. Energy Information Administration

Oil and gas outlook For New York Energy Forum New York, NY By Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis

Oil and gas outlook For New York Energy Forum New York, NY By Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis

Framing the Challenge A large independent: I can t run a company on single well economics. The whole portfolio has to make sense. Is there a viable bu

U.S. and Global Oil & Gas Dynamics IEEJ, June 23, 2016, Tokyo BEG/CEE-UT, 1 Framing the Challenge A large independent: I can t run a company on single well economics. The whole portfolio has to make sense.

U.S. and Global Oil & Gas Dynamics IEEJ, June 23, 2016, Tokyo BEG/CEE-UT, 1 Framing the Challenge A large independent: I can t run a company on single well economics. The whole portfolio has to make sense.

Short Term Energy Outlook March 2011 March 8, 2011 Release

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

Status and outlook for shale gas and tight oil development in the U.S.

Status and outlook for shale gas and tight oil development in the U.S. for Energy Symposium, University of Oklahoma, Price College Energy Institute Norman, OK by Adam Sieminski, Administrator U.S. Energy

Status and outlook for shale gas and tight oil development in the U.S. for Energy Symposium, University of Oklahoma, Price College Energy Institute Norman, OK by Adam Sieminski, Administrator U.S. Energy

Shale Gas - From the Source Rock to the Market: An Uneven pathway. Tristan Euzen

Shale Gas - From the Source Rock to the Market: An Uneven pathway Tristan Euzen Shale Gas Definition Seal Conventional Oil & Gas Tight Gas Source Rock Reservoir (Shale Gas) Modified from Williams 2013

Shale Gas - From the Source Rock to the Market: An Uneven pathway Tristan Euzen Shale Gas Definition Seal Conventional Oil & Gas Tight Gas Source Rock Reservoir (Shale Gas) Modified from Williams 2013

Annual Energy Outlook 2017

Annual Energy Outlook 217 Valve Manufacturers Association of America VMA Technical Seminar 217 March 2, 217 Nashville, TN By, Director, Office of Integrated and International Energy Analysis U.S. Energy

Annual Energy Outlook 217 Valve Manufacturers Association of America VMA Technical Seminar 217 March 2, 217 Nashville, TN By, Director, Office of Integrated and International Energy Analysis U.S. Energy

Annual Energy Outlook 2015

Annual Energy Outlook 215 for Asia Pacific Energy Research Centre Annual Conference 215 Tokyo, Japan by Sam Napolitano Director of the Office of Integrated and International Energy Analysis U.S. Energy

Annual Energy Outlook 215 for Asia Pacific Energy Research Centre Annual Conference 215 Tokyo, Japan by Sam Napolitano Director of the Office of Integrated and International Energy Analysis U.S. Energy

Gas and Crude Oil Production Outlook

Gas and Crude Oil Production Outlook COQA/CCQTA Joint meeting October 3-31, 214 San Francisco, California By John Powell Office of Petroleum, Natural Gas, and Biofuels Analysis U.S. Energy Information

Gas and Crude Oil Production Outlook COQA/CCQTA Joint meeting October 3-31, 214 San Francisco, California By John Powell Office of Petroleum, Natural Gas, and Biofuels Analysis U.S. Energy Information

North American Natural Gas Market Outlook

North American Natural Gas Market Outlook Energy Trends & Impacts On Gas Infrastructure Prepared For: Gas/Electric Partnership, Conference XVIII Darryl Rogers February 10, 2010 Agenda Introduction to Purvin

North American Natural Gas Market Outlook Energy Trends & Impacts On Gas Infrastructure Prepared For: Gas/Electric Partnership, Conference XVIII Darryl Rogers February 10, 2010 Agenda Introduction to Purvin

ENERGY SLIDESHOW. Federal Reserve Bank of Dallas

ENERGY SLIDESHOW Updated: July 5, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 120 Brent (Jun 29 = $75.24) WTI (Jun 29 = $74.03) 95%

ENERGY SLIDESHOW Updated: July 5, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 120 Brent (Jun 29 = $75.24) WTI (Jun 29 = $74.03) 95%

ENERGY SLIDESHOW. Federal Reserve Bank of Dallas

ENERGY SLIDESHOW Updated: February 14, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 Brent (Feb 9 = $65.50) WTI (Feb 9 = $62.01) 120

ENERGY SLIDESHOW Updated: February 14, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 Brent (Feb 9 = $65.50) WTI (Feb 9 = $62.01) 120

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project June 20, 2008 Barry Pulliam Senior Economist Econ One Research 5th Floor 601 W 5th Street Los Angeles, California 90071 213

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project June 20, 2008 Barry Pulliam Senior Economist Econ One Research 5th Floor 601 W 5th Street Los Angeles, California 90071 213

Outlook for the Oil and Gas Industry

Outlook for the Oil and Gas Industry VMA Market Outlook Workshop Boston, MA Spears& Associates Tulsa, OK August 2017 1 Outlook for the Oil and Gas Industry: Market Drivers Global oil consumption is forecast

Outlook for the Oil and Gas Industry VMA Market Outlook Workshop Boston, MA Spears& Associates Tulsa, OK August 2017 1 Outlook for the Oil and Gas Industry: Market Drivers Global oil consumption is forecast

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

Oil & The Economy: Boom-to-Bust and the Impact to States.

Oil & The Economy: Boom-to-Bust and the Impact to States. Jesse Thompson Business Economist Houston Branch January, 2017 U.S. Oil U.S. Production & Rig Surged Count U.S. crude oil production Million barrels

Oil & The Economy: Boom-to-Bust and the Impact to States. Jesse Thompson Business Economist Houston Branch January, 2017 U.S. Oil U.S. Production & Rig Surged Count U.S. crude oil production Million barrels

Energy Markets. U.S. Energy Information Administration. for. October 29, 2015 Golden, Colorado. by Adam Sieminski, Administrator

Energy Markets for The Payne Institute for Earth Resources at the Colorado School of Mines Golden, Colorado by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information

Energy Markets for The Payne Institute for Earth Resources at the Colorado School of Mines Golden, Colorado by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information

Markets and Opportunities. Paul Burgener March 2015

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Power & Politics Navigating the Changing Vision of Our Energy Future. Rayola Dougher, API Senior Economic Advisor,

Power & Politics Navigating the Changing Vision of Our Energy Future Rayola Dougher, API Senior Economic Advisor, dougherr@api.org U.S. oil and natural gas production is increasing as a result of technological

Power & Politics Navigating the Changing Vision of Our Energy Future Rayola Dougher, API Senior Economic Advisor, dougherr@api.org U.S. oil and natural gas production is increasing as a result of technological

Industry on the Move - What's Next? What will the changes in energy prices mean to industry in South Louisiana?

Industry on the Move - What's Next? What will the changes in energy prices mean to industry in South Louisiana? Event Sponsored by Regions Bank and 1012 Industry Report May 5, 2015 David E. Dismukes, Ph.D.

Industry on the Move - What's Next? What will the changes in energy prices mean to industry in South Louisiana? Event Sponsored by Regions Bank and 1012 Industry Report May 5, 2015 David E. Dismukes, Ph.D.

ENERGY OUTLOOK 2017 FALL/WINTER

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

Energy Markets. U.S. Energy Information Administration. for Center on Global Energy Policy, Columbia University November 20, 2015 New York, New York

Energy Markets for Center on Global Energy Policy, Columbia University New York, New York by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration

Energy Markets for Center on Global Energy Policy, Columbia University New York, New York by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration

Short-Term and Long-Term Outlook for Energy Markets

Short-Term and Long-Term Outlook for Energy Markets Guy Caruso Administrator, Energy Information Administration guy.caruso@eia.doe.gov Fueling the Future: Energy Policy in New England December 2, 25 Boston,

Short-Term and Long-Term Outlook for Energy Markets Guy Caruso Administrator, Energy Information Administration guy.caruso@eia.doe.gov Fueling the Future: Energy Policy in New England December 2, 25 Boston,

U.S. Energy Market Outlook

U.S. Energy Market Outlook for Energy Policy Institute National Governor's Association Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

U.S. Energy Market Outlook for Energy Policy Institute National Governor's Association Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Unconventional Oil & Gas: Reshaping Energy Markets

Unconventional Oil & Gas: Reshaping Energy Markets Guy Caruso Senior Advisor JOGMEC Seminar 7 February 2013 Landscape is Changing Even as We Sit Here Today - US Projected to reach 90% Energy Self-Sufficiency

Unconventional Oil & Gas: Reshaping Energy Markets Guy Caruso Senior Advisor JOGMEC Seminar 7 February 2013 Landscape is Changing Even as We Sit Here Today - US Projected to reach 90% Energy Self-Sufficiency

North, South, Texas and the Rest

North, South, Texas and the Rest CEE Annual Meeting 4 5 December 2013 BEG/CEE UT, 1 Welcome! Agenda highlights and other logistics Introductions Up at Night rules of the game and Chatham House rules for

North, South, Texas and the Rest CEE Annual Meeting 4 5 December 2013 BEG/CEE UT, 1 Welcome! Agenda highlights and other logistics Introductions Up at Night rules of the game and Chatham House rules for

Drilling Deeper: A Reality Check on U.S. Government Forecasts for a Lasting Tight Oil & Shale Gas Boom. Web Briefing December 9, 2014

Drilling Deeper: A Reality Check on U.S. Government Forecasts for a Lasting Tight Oil & Shale Gas Boom Web Briefing December 9, 214 J. David Hughes Post Carbon Institute Global Sustainability Research

Drilling Deeper: A Reality Check on U.S. Government Forecasts for a Lasting Tight Oil & Shale Gas Boom Web Briefing December 9, 214 J. David Hughes Post Carbon Institute Global Sustainability Research

The State of the Energy Markets

The State of the Energy Markets February 2015 The Disclaimer The information within this presentation has been compiled by the Melby Group for general purposes only. Melby Group assumes no responsibility

The State of the Energy Markets February 2015 The Disclaimer The information within this presentation has been compiled by the Melby Group for general purposes only. Melby Group assumes no responsibility

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION ARIZONA CORPORATION COMMISSION APRIL 6, 2017 DALE PROBASCO MANAGING DIRECTOR ROGER SCHIFFMAN DIRECTOR

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION ARIZONA CORPORATION COMMISSION APRIL 6, 2017 DALE PROBASCO MANAGING DIRECTOR ROGER SCHIFFMAN DIRECTOR

Shale Gas as an Alternative Petrochemical Feedstock

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Contemplations about the future of natural gas: the good, the bad and the ugly

Contemplations about the future of natural gas: the good, the bad and the ugly Charles F. Mason H.A. True Chair in Petroleum and Natural Gas Economics Department of Economics Associate Dean, College of

Contemplations about the future of natural gas: the good, the bad and the ugly Charles F. Mason H.A. True Chair in Petroleum and Natural Gas Economics Department of Economics Associate Dean, College of

U.S. Natural Gas Market Dynamics

U.S. Natural Gas Market Dynamics University of Houston Global Energy Management Institute The Future of the Gulf Coast Petrochemical Industry Michael Speltz April 29, 2005 ChevronTexaco 2002 Legal Disclaimer

U.S. Natural Gas Market Dynamics University of Houston Global Energy Management Institute The Future of the Gulf Coast Petrochemical Industry Michael Speltz April 29, 2005 ChevronTexaco 2002 Legal Disclaimer

GLOBAL OIL MARKET TRENDS

GLOBAL OIL MARKET TRENDS Brent timeline and latest forward curve: Prompt prices recovering, back-end more stable ICE Brent crude, historical front month contract price and latest forward curve Our view

GLOBAL OIL MARKET TRENDS Brent timeline and latest forward curve: Prompt prices recovering, back-end more stable ICE Brent crude, historical front month contract price and latest forward curve Our view

Gulf Coast Energy Outlook: Addendum.

Gulf Coast Energy Outlook: Addendum. Addendum accompanying whitepaper. See full whitepaper here. David E. Dismukes, Ph.D. Gregory B. Upton, Jr., Ph.D. Center for Energy Studies Louisiana State University

Gulf Coast Energy Outlook: Addendum. Addendum accompanying whitepaper. See full whitepaper here. David E. Dismukes, Ph.D. Gregory B. Upton, Jr., Ph.D. Center for Energy Studies Louisiana State University

Technologies to recover it were refined as natural gas prices rose to $10 per MMBtu Locations of shale gas were known for decades

Technologies to recover it were refined as natural gas prices rose to $10 per MMBtu Locations of shale gas were known for decades Discovery rates are very high Reduces producer expenses Volume was greatly

Technologies to recover it were refined as natural gas prices rose to $10 per MMBtu Locations of shale gas were known for decades Discovery rates are very high Reduces producer expenses Volume was greatly

Energy markets the short and the long term

Energy markets the short and the long term Christof Rühl, Chief Economist, BP BP 2012 Outline The economy A year of disruptions Long term implications Conclusion Global growth: slow and on life support

Energy markets the short and the long term Christof Rühl, Chief Economist, BP BP 2012 Outline The economy A year of disruptions Long term implications Conclusion Global growth: slow and on life support

North American Gas: A dynamic environment. Josh McCall BP North American Gas and Power November 16, 2011

North American Gas: A dynamic environment Josh McCall BP North American Gas and Power November 16, 2011 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not

North American Gas: A dynamic environment Josh McCall BP North American Gas and Power November 16, 2011 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not

INTERNATIONAL ENERGY AGENCY WORLD ENERGY INVESTMENT OUTLOOK 2003 INSIGHTS

INTERNATIONAL ENERGY AGENCY WORLD ENERGY INVESTMENT OUTLOOK 2003 INSIGHTS Global Strategic Challenges Security of energy supplies Threat of environmental damage caused by energy use Uneven access of the

INTERNATIONAL ENERGY AGENCY WORLD ENERGY INVESTMENT OUTLOOK 2003 INSIGHTS Global Strategic Challenges Security of energy supplies Threat of environmental damage caused by energy use Uneven access of the

Shale Gas and U.S. LNG Exports. Vienna, January 29, 2013 Jean Abiteboul President, Cheniere Supply & Marketing

Shale Gas and U.S. LNG Exports Vienna, January 29, 2013 Jean Abiteboul President, Cheniere Supply & Marketing Forward Looking Statements This presentation contains certain statements that are, or may be

Shale Gas and U.S. LNG Exports Vienna, January 29, 2013 Jean Abiteboul President, Cheniere Supply & Marketing Forward Looking Statements This presentation contains certain statements that are, or may be

By Bob Hugman and Harry Vidas

WHITE PAPER Oklahoma: A Major Player for Future Hydrocarbon Production By Bob Hugman and Harry Vidas Bottom Line 1. Despite sharp drilling activity declines over the past year in most areas of the country,

WHITE PAPER Oklahoma: A Major Player for Future Hydrocarbon Production By Bob Hugman and Harry Vidas Bottom Line 1. Despite sharp drilling activity declines over the past year in most areas of the country,

The Unconventional Reservoirs Revolution and the Rebirth of the U.S. Onshore Oil & Gas Industry

The Unconventional Reservoirs Revolution and the Rebirth of the U.S. Onshore Oil & Gas Industry Feb. 19, 2013 Cautionary Statement The following presentation includes forward-looking statements. These

The Unconventional Reservoirs Revolution and the Rebirth of the U.S. Onshore Oil & Gas Industry Feb. 19, 2013 Cautionary Statement The following presentation includes forward-looking statements. These

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities.

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

OIL AND GAS OUTLOOK: HOW ARE THE ENERGY MARKET AFFECTING METALS? Nicole Leonard, Project Manager, Oil & Gas Consulting Services November 2015

OIL AND GAS OUTLOOK: HOW ARE THE ENERGY MARKET AFFECTING METALS? Nicole Leonard, Project Manager, Oil & Gas Consulting Services November 2015 KEY TAKEAWAYS Macroeconomic outlook: Prices have collapsed

OIL AND GAS OUTLOOK: HOW ARE THE ENERGY MARKET AFFECTING METALS? Nicole Leonard, Project Manager, Oil & Gas Consulting Services November 2015 KEY TAKEAWAYS Macroeconomic outlook: Prices have collapsed

Challenges of Fracking for the MENA Region Martin Bachmann, Member of the Board

Challenges of Fracking for the MENA Region Martin Bachmann, Member of the Board NUMOV German MENA Conference Berlin, 26 January 2017 Simplified Model of Hydrocarbon Deposits Conventional versus Unconventional

Challenges of Fracking for the MENA Region Martin Bachmann, Member of the Board NUMOV German MENA Conference Berlin, 26 January 2017 Simplified Model of Hydrocarbon Deposits Conventional versus Unconventional

A Tale of Two Fuels - Crude Oil and Natural Gas Supply. Private Capital Conference February 24, 2011 Houston, TX

A Tale of Two Fuels - Crude Oil and Natural Gas Supply Private Capital Conference February 24, 2011 Houston, TX Henry Hub Natural Gas vs. WTI Crude $/MMBTU $14 $12 $10 $8 $6 $4 $2 Henry Hub WTI 160 140

A Tale of Two Fuels - Crude Oil and Natural Gas Supply Private Capital Conference February 24, 2011 Houston, TX Henry Hub Natural Gas vs. WTI Crude $/MMBTU $14 $12 $10 $8 $6 $4 $2 Henry Hub WTI 160 140

Perspectives on the Impact of Shale Gas and Tight Oil Production on the Global E&C Industry and Vice Versa

214 RICE GLOBAL E&C ANNUAL FORUM Perspectives on the Impact of Shale Gas and Tight Oil Production on the Global E&C Industry and Vice Versa September 23, 214 www.forum.rice.edu Today s objectives Review

214 RICE GLOBAL E&C ANNUAL FORUM Perspectives on the Impact of Shale Gas and Tight Oil Production on the Global E&C Industry and Vice Versa September 23, 214 www.forum.rice.edu Today s objectives Review

Navigating the Uncertainties in the North American Gas Market

Interesting Times: Navigating the Uncertainties in the North American Gas Market Ed Kelly Vice President North American Gas and Power Wood Mackenzie Risks and Uncertainties On the Supply Side The Resource

Interesting Times: Navigating the Uncertainties in the North American Gas Market Ed Kelly Vice President North American Gas and Power Wood Mackenzie Risks and Uncertainties On the Supply Side The Resource

Natural Gas Outlook and Drivers

Natural Gas Outlook and Drivers November 2012 33% BENTEK Energy 5% 40% Who We Are Based in Evergreen, CO 120 People 400+ Customers Subsidiary of McGraw-Hill/Platts 22% What We Do Collect, Analyze and Distribute

Natural Gas Outlook and Drivers November 2012 33% BENTEK Energy 5% 40% Who We Are Based in Evergreen, CO 120 People 400+ Customers Subsidiary of McGraw-Hill/Platts 22% What We Do Collect, Analyze and Distribute

US LNG Supply into Europe. Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International

US LNG Supply into Europe Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International Forward Looking Statements This presentation contains certain statements that

US LNG Supply into Europe Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International Forward Looking Statements This presentation contains certain statements that

Thoughts on U.S. Unconventional Oil Production and Investment Following the Paris Agreement

Thoughts on U.S. Unconventional Oil Production and Investment Following the Paris Agreement February 16, 2017 KAPSARC/IEF Riyadh, Saudi Arabia Trisha Curtis Co-Founder, PetroNerds, LLC trisha@petronerds.com

Thoughts on U.S. Unconventional Oil Production and Investment Following the Paris Agreement February 16, 2017 KAPSARC/IEF Riyadh, Saudi Arabia Trisha Curtis Co-Founder, PetroNerds, LLC trisha@petronerds.com

Energizing America: Facts for Addressing Energy Policy. Rayola Dougher API Senior Economic Advisor,

Energizing America: Facts for Addressing Energy Policy Rayola Dougher API Senior Economic Advisor, dougherr@api.org 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 1970 1975 1980 1985 1990 1995 2000

Energizing America: Facts for Addressing Energy Policy Rayola Dougher API Senior Economic Advisor, dougherr@api.org 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 1970 1975 1980 1985 1990 1995 2000

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

Impact of Shale Gas on Transmission

Impact of Shale Gas on Transmission February, 08 2012 February, 2012 1 Transco System Overview System Summary 2,000 Mainline Miles from Texas to New York. Approximately 11,000 Miles of Pipeline. Extensive

Impact of Shale Gas on Transmission February, 08 2012 February, 2012 1 Transco System Overview System Summary 2,000 Mainline Miles from Texas to New York. Approximately 11,000 Miles of Pipeline. Extensive

Milken Institute: Center for Accelerating Energy Solutions

Milken Institute: Center for Accelerating Energy Solutions Center for Accelerating Energy Solutions Promotes policy and market mechanisms to build a more stable and sustainable energy future Identifies

Milken Institute: Center for Accelerating Energy Solutions Center for Accelerating Energy Solutions Promotes policy and market mechanisms to build a more stable and sustainable energy future Identifies

Rice Global E&C Forum

Rice Global E&C Forum "Will Shale revolution trigger game changes in Asian Energy Market and LNG?" Tevin Vongvanich President and Chief Executive Officer PTT Exploration and Production Public Company Limited

Rice Global E&C Forum "Will Shale revolution trigger game changes in Asian Energy Market and LNG?" Tevin Vongvanich President and Chief Executive Officer PTT Exploration and Production Public Company Limited

Summary - The Challenge to European Refining Posed by the Rise of US Unconventionals Scottish Oil Club

Summary - The Challenge to European Refining Posed by the Rise of US Unconventionals Scottish Oil Club November 2014 About us We are a global leader in commercial intelligence for the energy, metals and

Summary - The Challenge to European Refining Posed by the Rise of US Unconventionals Scottish Oil Club November 2014 About us We are a global leader in commercial intelligence for the energy, metals and

Energy Macro Review. 3 rd Quarter 2013

Energy Macro Review 3 rd Quarter 2013 Oil Fundamentals 2 $/bbl WTI Oil Prices are Up in 2013 $115 $110 $105 Front Month WTI Prices WTI crude prices are up +11.1% year-to-date. Three factors have driven

Energy Macro Review 3 rd Quarter 2013 Oil Fundamentals 2 $/bbl WTI Oil Prices are Up in 2013 $115 $110 $105 Front Month WTI Prices WTI crude prices are up +11.1% year-to-date. Three factors have driven

Will The Plays Be Commercial? Impact on Natural Gas Price

North American Shale Gas Will The Plays Be Commercial? Impact on Natural Gas Price Arthur E. Berman Slide 1 Natural Gas Prices Natural gas prices will increase over the next 12-24 months to meet the marginal

North American Shale Gas Will The Plays Be Commercial? Impact on Natural Gas Price Arthur E. Berman Slide 1 Natural Gas Prices Natural gas prices will increase over the next 12-24 months to meet the marginal

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond August 14th, 2012 On behalf of: for: 1 BENTEK Energy Market Information Agenda: U.S. Supply, Demand and Storage Outlook Macro

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond August 14th, 2012 On behalf of: for: 1 BENTEK Energy Market Information Agenda: U.S. Supply, Demand and Storage Outlook Macro

Colorado Energy & Environmental Issues. Chris Hansen, PhD Senior Advisor, Janys Analytics Candidate, Colorado House of Representatives

Colorado Energy & Environmental Issues Chris Hansen, PhD Senior Advisor, Janys Analytics Candidate, Colorado House of Representatives Oil 2 Thousand Barrels per Day U.S. Crude Oil Production & Consumption,

Colorado Energy & Environmental Issues Chris Hansen, PhD Senior Advisor, Janys Analytics Candidate, Colorado House of Representatives Oil 2 Thousand Barrels per Day U.S. Crude Oil Production & Consumption,

Wood Mackenzie Gas Market Outlook

Wood Mackenzie Gas Market Outlook Southern Gas Association April 20, 2009 Amber McCullagh Short-Term Outlook 2008 markets were volatile as underlying fundamentals shifted rapidly Three primary phases:

Wood Mackenzie Gas Market Outlook Southern Gas Association April 20, 2009 Amber McCullagh Short-Term Outlook 2008 markets were volatile as underlying fundamentals shifted rapidly Three primary phases:

NEXUS Gas Transmission

NEXUS Gas Transmission Bringing New Supplies to Market Ohio Manufacturers Association - October 2012 Agenda Project Introduction Utica and Marcellus Gas Supply Michigan and Ontario Markets Conclusion &

NEXUS Gas Transmission Bringing New Supplies to Market Ohio Manufacturers Association - October 2012 Agenda Project Introduction Utica and Marcellus Gas Supply Michigan and Ontario Markets Conclusion &

Energy Outlook. Kurt Barrow Vice President, Oil Markets, Midstream and Downstream Insights, IHS Markit

Energy Outlook Kurt Barrow Vice President, Oil Markets, Midstream and Downstream Insights, IHS Markit kurt.barrow@ihsmarkit.com Building a Foundation for Profitable Growth in Uncertain Markets Agenda Short-term

Energy Outlook Kurt Barrow Vice President, Oil Markets, Midstream and Downstream Insights, IHS Markit kurt.barrow@ihsmarkit.com Building a Foundation for Profitable Growth in Uncertain Markets Agenda Short-term

US Oil and Natural Gas Perspective

Presentation to the WEC-Mexican Committee 31 January 2018 US Oil and Natural Gas Perspective Guy Caruso Senior Advisor 1 Source: EIA 2 US Perspective: from Resource Scarcity to. - US is heading towards

Presentation to the WEC-Mexican Committee 31 January 2018 US Oil and Natural Gas Perspective Guy Caruso Senior Advisor 1 Source: EIA 2 US Perspective: from Resource Scarcity to. - US is heading towards

Energy in 2011 disruption and continuity

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Richard de Caux, Refining Analyst, Group Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Richard de Caux, Refining Analyst, Group Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding

U.S. natural gas and LNG exports

U.S. natural gas and LNG exports For Hudson Institute Washington DC April 6, 216 By Victoria Zaretskaya Office of Petroleum, Natural Gas, and Biofuels Analysis U.S. Energy Information Administration Independent

U.S. natural gas and LNG exports For Hudson Institute Washington DC April 6, 216 By Victoria Zaretskaya Office of Petroleum, Natural Gas, and Biofuels Analysis U.S. Energy Information Administration Independent

Global Energy Assessment: Shale Gas and Oil

Global Energy Assessment: Shale Gas and Oil KEEI September, 2014 Yonghun Jung Shale Gas: a new source of energy Shale gas deposits around the world vs. 2009 natural gas consumption (tcf) U.S. 862 22.8

Global Energy Assessment: Shale Gas and Oil KEEI September, 2014 Yonghun Jung Shale Gas: a new source of energy Shale gas deposits around the world vs. 2009 natural gas consumption (tcf) U.S. 862 22.8

U.S. Historical and Projected Shale Gas Production

U.S. Historical and Projected Shale Gas Production Phyllis Martin Phyllis Martin, Senior Energy Analyst Office of Petroleum, Gas and Biofuels Analysis U.S. Energy Information Administration phyllis.martin@eia.doe.gov

U.S. Historical and Projected Shale Gas Production Phyllis Martin Phyllis Martin, Senior Energy Analyst Office of Petroleum, Gas and Biofuels Analysis U.S. Energy Information Administration phyllis.martin@eia.doe.gov

Outlook for the Upstream Sector of the Oil and Gas Industry

Outlook for the Upstream Sector of the Oil and Gas Industry VMA Market Outlook Workshop San Diego, CA Spears& Associates Tulsa, OK August 2016 Oil market fundamentals remain strong World oil demand is

Outlook for the Upstream Sector of the Oil and Gas Industry VMA Market Outlook Workshop San Diego, CA Spears& Associates Tulsa, OK August 2016 Oil market fundamentals remain strong World oil demand is

American Strategy and US Energy Independence

Cordesman: Strategy and Energy Independence 10/21/13 1 American Strategy and US Energy Independence By Anthony H. Cordesman October 21, 2013 Changes in energy technology, and in the way oil and gas reserves

Cordesman: Strategy and Energy Independence 10/21/13 1 American Strategy and US Energy Independence By Anthony H. Cordesman October 21, 2013 Changes in energy technology, and in the way oil and gas reserves

The U.S. Over-Supply of Oil is Ending

The U.S. Over-Supply of Oil is Ending Pay-It-Forward Network Art Berman November 17, 217 Slide 1 The U.S. Over-Supply of Oil is Ending The U.S. Over-Supply of Oil is Ending 11 WTI Price Stocks 239 213

The U.S. Over-Supply of Oil is Ending Pay-It-Forward Network Art Berman November 17, 217 Slide 1 The U.S. Over-Supply of Oil is Ending The U.S. Over-Supply of Oil is Ending 11 WTI Price Stocks 239 213