UNDERSTANDING NATURAL GAS MARKETS. Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015

|

|

|

- Alannah Hunter

- 5 years ago

- Views:

Transcription

1 UNDERSTANDING NATURAL GAS MARKETS Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015

2 Table of Contents

3 3 Overview Natural Gas is an Important Source of Energy for the United States. Natural gas is an attractive fuel because it is clean burning and efficient, and ample supplies of natural gas are available from domestic resources. Reason I The prospect of ample natural gas supplies Reason II continued low prices Reason III the favorable environmental and economic position of natural gas-fired electric generation plants Growing U.S. demand for natural gas, especially in the electric and industrial sectors, and potentially for export as liquefied natural gas (LNG).

4 4

5 5 The important trends now affecting the industry include the following: U.S. natural gas demand is increasingly served by domestic production from unconventional shale gas sources rather than imported natural gas from Canada and other conventional supplies. Natural gas use for electricity generation is poised to increase due to low natural gas prices and expectations that coal-fired power plants will continue to be retired due to environmental regulations. Low natural gas prices are also expected to drive demand growth in the industrial sector. The growth in shale gas production in shifting flows on the U.S. interstate pipeline network. The substantial production increases, and low prices in the U.S. relative to overseas, are leading to the development of both LNG and pipeline export projects. These projects could result in the U.S. becoming a net exporter of natural gas, whereas historically the U.S. was a net importer due to its reliance on Canadian natural gas supplies inmeeting domestic consumption.

6 6 Key points: The shale gas revolution has led to U.S. natural gas supply growth that has exceeded demand growth. As a result, Canadian imports and other conventional supplies have been displaced, prices have fallen substantially and price volatility has declined to some extent. The last large price spike in the summer of 2008 gave way to a substantial price decline as shale gas production increased and the economic recession brought on by the global financial crisis decreased the demand for natural gas. Demand has increased since 2009, domestic shale production has increased even faster. The result has been relatively low prices over the past several years, but not as low as the prices experienced during most of the 1990s.

7 7

8 8 The North American Natural Gas Marketplace Natural gas provides 27% of the marketable energy consumed in the United States. CH4 CH4 CH4 Natural gas use in applications including cooking, residential and commercial heating, industrial process feed stocks, and electricity generation

9 Physical Structure of the U.S. Natural Gas Industry: PHYSICAL FLOW OF NATURAL GAS 9 Exploration and Production Processing Transportation Storage Local Distribution Liquefied Natural Gas

10 10 The U.S. currently imports less than one percent of its natural gas in the form of LNG (compared to a peak of three percent in 2007) primarily from the Everett terminal near Boston and the Elba Island terminal in Georgia, two of eleven existing U.S. LNG import terminals. The growth in shale gas production in the U.S. has resulted in proposals to develop LNG export terminals to liquefy and ship natural gas produced in the U.S. to overseas markets.

11 11 OFFSHORE UNDISCOVERED TECHNICALLY RECOVERABLE FEDERAL OIL AND NATURAL GAS RESOURCES MAP 5 SELECTED U.S.NATURAL GAS PRODUCING REGIONS AND PIPELINE FLOWS 4 87%of federal offshore acreage is off limits to development 4.7 Bbl 37.5 Tcf Source: API primer Offshore Access to Oil and Natural Gas Resources," July Bbl= Billion Barrels Tcf= Trillion Cubic Feet 5,000 4,000 3,000 2,000 1,000 0 Source: Recreated based on graphics from EIA Flow Levels (Billion Cubic =Direction Feet) of the Flow =Bi-directional

12 12 Once natural gas is produced and processed, it is injected into pipelines for transmission to end-use customers and local distribution companies. Transmission and distribution costs are a significant portion of the total cost of delivered natural gas. The rates charged by both natural gas pipelines and local distribution companies are regulated at the federal and state level.

, while transmission and distribution charges have increased from 41% to 72% of the consumer s average heating season cost.")

13 13 In recent years, the cost of the natural gas itself has decreased from 59% in to 28% in of the delivered natural gas cost paid by residential consumers during the heating season (November through March), while transmission and distribution charges have increased from 41% to 72% of the consumer s average heating season cost. See Figure 6

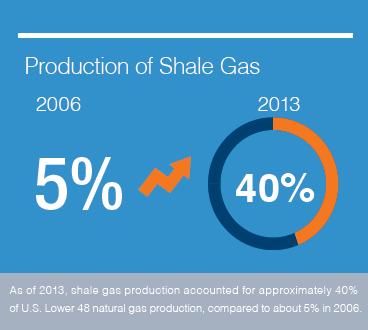

14 14 Natural Gas Supply Shales are fine-grained sedimentary rocks that can be rich sources of petroleum and natural gas. Technically recoverable natural gas resources in the U.S. have been estimated at 2,431 Tcf currently, compared to 1,594 Tcf in 2005 The largest shale production is from the Marcellus (35%), Haynesville (12%), Barnett (14%), and Eagle Ford (12%) shale formations (with all other shales combining to total roughly 27%).

15 15 Figure 7 shows the substantial growth in annual shale gas production from less than 5 Bcf/d in early 2007 to nearly 30 Bcf/d more recently.

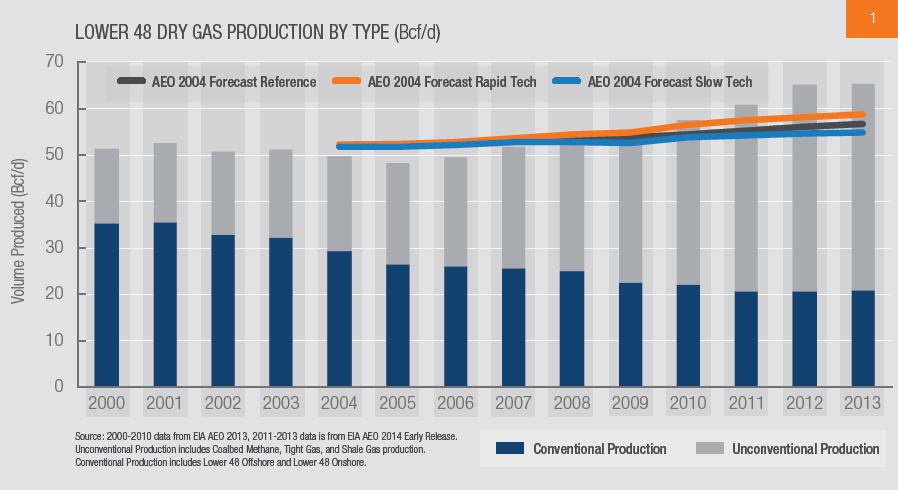

16 16 Figure 8 shows U.S. Lower 48 production of natural gas by source, with shale gas accounting for a significantly increasing proportion of total U.S. Lower 48 natural gas production. Shale gas production is projected to account for over 50% of U.S. Lower 48 natural gas production by 2040, and gas produced by hydraulic fracturing will account for nearly 80% of natural gas production in the future.

17 17 Figure 9 show that total natural gas production has continued to grow even as rigs increasingly have been directed towards oil drilling and away from natural gas.

18 18 An important factor that affects drilling activity in the U.S. is the price of natural gas liquids (NGLs) that are produced in some areas as a byproduct of natural gas production. NGLs are removed from the natural gas stream at natural gas processing and fractionation plants and sold separately. High NGL prices (which typically have followed the trends in oil rather than natural gas prices) make it profitable to separate NGLs from natural gas and sell them as a separate product.

19 19 Figure 10 shows that Recent NGL prices have been high relative to natural gas prices, which has provided a strong incentive for producers to shift their focus from dry gas plays to liquids-rich gas plays.

20 20 Historically, U.S. natural gas consumption exceeded production, and the difference was made up by natural gas imports by pipeline from Canada as well as a relatively small amount of LNG imports from overseas locations. With the growth in domestic shale gas supplies, imports have been declining and forecasts indicate that the U.S. will become a net exporter of natural gas later this decade. These exports will likely include pipeline exports to Mexico, and exports in the form of LNG. Net imports from Canada are likely to continue, but at substantially lower levels than in the past. See Figure 11 & 12

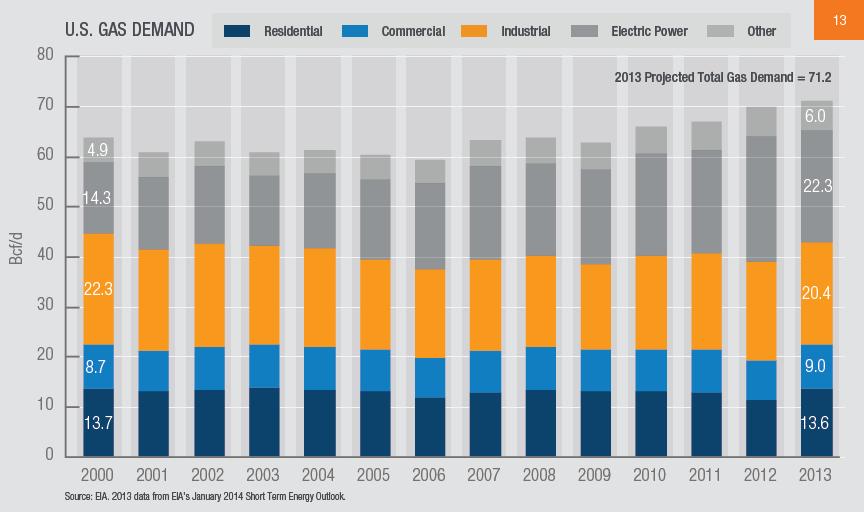

21 21 Natural Gas Demand Recent declines in natural gas prices are also explained by the fact that the demand for natural gas has not grown as rapidly as the growth in supplies. overall consumption was flat or declining between 2000 and 2006, with some demand growth occurring in the period. Residential and commercial use of natural gas has been relatively steady over the period. Industrial natural gas demand generally declined during the period in response to high and volatile gas prices, while natural gas demand for power generation increased during this period, offsetting the declines in industrial demand. In 2012, natural gas use for power generation surged as a result of low natural gas prices. Low prices caused natural gas-fired electricity generating facilities to run more often and in some cases ahead of coal-fired plants. Natural gas demand is highly seasonal in nature, with significant peaks in the winter heating season, as illustrated in Figure 14.

22 22

23 23 Figure 14 shows the pattern of natural gas production and storage. The relatively flat light blue line shows natural gas production and imports into the United States. The figure shows production remains essentially flat throughout the year, but, as the darker blue line shows, consumption rises dramatically in the winter and falls in the spring through the early fall.

24 24 The low natural gas prices are leading many analysts to believe that there will be substantial natural gas demand growth in the future, especially in the electric and industrial sectors

25 25 The effects of the low prices of natural gas: On the Electric side On the industrial side The combination of low natural gas prices and emerging environmental regulations is leading to the retirement of a significant amount of coal-fired generation capacity. The low natural gas prices are also causing a resurgence in industrial activity that may lead to increased natural gas demand there will be substantial natural gas demand growth in the future

26 26 Natural Gas Exports Low natural gas prices in North America are leading to proposals for the development of large LNG export projects. LNG export projects have been announced on the Gulf Coast, East Coast, and West Coast of the United States, as well as in Alaska and British Columbia. How many of LNG export projects advance to the construction phase is uncertain: Uncertainty in how much LNG demand there will be from overseas countries. These projects require substantial capital These projects also require approval from regulatory bodies. Some projects also face certain infrastructure challenges that may put them at a disadvantage. It is expected that the U.S. also will export natural gas to Mexico and Canada

27 27 Figure 16 shows the relationship between U.S. natural gas prices at Henry Hub and oil prices as measured by the Brent benchmark world oil price. Starting around 2009, U.S. natural gas prices began to disconnect substantially from oil prices as a result of the increase in shale gas production.

28 28 How Natural Gas is Traded The natural gas industry in the United States is highly competitive, with literally thousands of producers. Some producers have the ability to market their natural gas and may sell it directly to local distribution companies or to large industrial buyers of natural gas. Other producers sell their gas to marketers who have the ability to aggregate natural gas into quantities that fit the needs of different types of buyers and to transport gas to their buyers. Marketers may be large or small and sell to local distribution companies or to commercial or industrial customers connected directly to pipelines or served by local distribution companies. Marketers and other buyers and sellers of natural gas are able to use financial instruments traded on exchanges to hedge the risks associated with price volatility.

29 29 Figure 17 shows schematically some of the types of natural gas transactions that take place as gas makes its way from the fields where it is produced to end users burner tips.

30 30 Most residential and commercial customers purchase natural gas from a local distribution company. Many industrial customers have the option to purchase natural gas from a marketer or producer instead of from the distribution company. Figure 18 shows some of the points where natural gas for physical delivery is actively traded in the continental United States and Canada.

31 31 Futures and Other Financial Contracts Natural gas derivatives are traded on the New York Mercantile Exchange. A NYMEX natural gas futures contract requires the seller to deliver (and the buyer to take delivery of) natural gas at the contractually agreed price, in a specified future month, at the Henry Hub. Derivatives such as the NYMEX futures contract make it possible for market participants to reduce the risk that results from highly volatile natural gas prices in the physical market.

32 32 Figure 19 shows the number of natural gas contracts traded on the NYMEX each year between 1990 and 2013.

33 33 Figure 20 shows some of the recent movement in natural gas futures prices at different points in time over the past few years. Each line in the figure shows prices for natural gas to be delivered in each of the next 36 months. In June 2008, before shale supplies started coming on line in substantial quantities, the market was expecting relatively high prices with significant peaks during the winter period versus the summer period. More recently, as larger quantities of shale production have come on line, market participants expected lower prices to prevail that have less of a winter peak than was the case historically.

34 34 Conclusion: A New Era For U.S. Natural Gas Markets The U.S. natural gas industry has changed dramatically as a result of technological advancements that have resulted in increasing domestic production, especially from shale resources. These new supplies of natural gas have resulted in lower prices and reduced price volatility, and expectations of increasing demand. Natural gas use for electricity generation is expected to grow, in part due to the expected retirement of some coal-fired generation capacity. Industrial consumption of natural gas is also expected to increase due to a resurgence of petrochemical plants, especially in the U.S. Gulf Coast. Low domestic prices relative to the prices available in world markets are also leading to proposals to export natural gas as LNG. The emergence of shale gas in abundance has profoundly changed the market for natural gas in the U.S. in recent years, and perhaps for the foreseeable future.

35 34 Thanks for your listening

UNDERSTANDING NATURAL GAS MARKETS

UNDERSTANDING NATURAL GAS MARKETS Table of Contents PREVIEW Overview... 2 The North American Natural Gas Marketplace... 4 Natural Gas Supply... 8 Natural Gas Demand... 12 Natural Gas Exports... 15 How

UNDERSTANDING NATURAL GAS MARKETS Table of Contents PREVIEW Overview... 2 The North American Natural Gas Marketplace... 4 Natural Gas Supply... 8 Natural Gas Demand... 12 Natural Gas Exports... 15 How

Natural Gas Abundance: The Development of Shale Resource in North America

Natural Gas Abundance: The Development of Shale Resource in North America EBA Brown Bag Luncheon Bracewell & Giuliani Washington, D.C. February 6, 2013 Bruce B. Henning Vice President, Energy Regulatory

Natural Gas Abundance: The Development of Shale Resource in North America EBA Brown Bag Luncheon Bracewell & Giuliani Washington, D.C. February 6, 2013 Bruce B. Henning Vice President, Energy Regulatory

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Shale Gas - Transforming Natural Gas Flows and Opportunities. Doug Bloom President, Spectra Energy Transmission West October 18, 2011

Fort Nelson Gas Plant, British Columbia Shale Gas - Transforming Natural Gas Flows and Opportunities Doug Bloom President, Spectra Energy Transmission West October 18, 2011 Natural Gas Golden Age Natural

Fort Nelson Gas Plant, British Columbia Shale Gas - Transforming Natural Gas Flows and Opportunities Doug Bloom President, Spectra Energy Transmission West October 18, 2011 Natural Gas Golden Age Natural

ENVIRONMENT AND ENERGY BULLETIN

ENVIRONMENT AND ENERGY BULLETIN Vol. 3 No. 2 June 2011 Editor: Jock A. Finlayson THE NATURAL GAS STORY Both globally and in North America, natural gas is poised to play a bigger role in meeting the energy

ENVIRONMENT AND ENERGY BULLETIN Vol. 3 No. 2 June 2011 Editor: Jock A. Finlayson THE NATURAL GAS STORY Both globally and in North America, natural gas is poised to play a bigger role in meeting the energy

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer.

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

North American Midstream Infrastructure Through 2035 A Secure Energy Future. Press Briefing June 28, 2011

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

The Impact of Developing Energy and Environmental Policy on the Gas Industry Plus Impacts of the Current Economic State

The Impact of Developing Energy and Environmental Policy on the Gas Industry Plus Impacts of the Current Economic State Gas / Electric Partnership Conference XVII Gas Compression from Production thru Transmission

The Impact of Developing Energy and Environmental Policy on the Gas Industry Plus Impacts of the Current Economic State Gas / Electric Partnership Conference XVII Gas Compression from Production thru Transmission

US Oil and Gas Import Dependence: Department of Energy Projections in 2011

1800 K Street, NW Suite 400 Washington, DC 20006 Phone: 1.202.775.3270 Fax: 1.202.775.3199 Email: acordesman@gmail.com Web: www.csis.org/burke/reports US Oil and Gas Import Dependence: Department of Energy

1800 K Street, NW Suite 400 Washington, DC 20006 Phone: 1.202.775.3270 Fax: 1.202.775.3199 Email: acordesman@gmail.com Web: www.csis.org/burke/reports US Oil and Gas Import Dependence: Department of Energy

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

World and U.S. Oil and Gas Production and Price Outlook: To Infinity (or at least 2050) and Beyond

and Beyond") World and U.S. Oil and Gas Production and Price Outlook: To Infinity (or at least 25) and Beyond Energy and Environment Symposium April 18, 218 Rifle, Colorado by Troy Cook, Senior Global Upstream Analyst,

World and U.S. Oil and Gas Production and Price Outlook: To Infinity (or at least 25) and Beyond Energy and Environment Symposium April 18, 218 Rifle, Colorado by Troy Cook, Senior Global Upstream Analyst,

October 23, 2018 Harrisburg, PA

Pennsylvania Public Utility Commission Annual Winter Reliability Assessment Terrance J. Fitzpatrick President & Chief Executive Officer Energy Association of Pennsylvania October 23, 2018 Harrisburg, PA

Pennsylvania Public Utility Commission Annual Winter Reliability Assessment Terrance J. Fitzpatrick President & Chief Executive Officer Energy Association of Pennsylvania October 23, 2018 Harrisburg, PA

The Energy Consortium Recent Developments and the Outlook for Natural Gas in the Northeast. John R. Bitler October 20, 2010

The Energy Consortium Recent Developments and the Outlook for Natural Gas in the Northeast John R. Bitler October 20, 2010 Northeast Overview Traditional Sources of Supply Gulf Coast Western Canada (WCSB)

The Energy Consortium Recent Developments and the Outlook for Natural Gas in the Northeast John R. Bitler October 20, 2010 Northeast Overview Traditional Sources of Supply Gulf Coast Western Canada (WCSB)

U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves

1 of 5 3/14/2013 11:37 PM U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves With Data for Release Date: August 1, 2012 Next Release Date: March 2013 Previous Issues: Year: Summary Proved reserves

1 of 5 3/14/2013 11:37 PM U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves With Data for Release Date: August 1, 2012 Next Release Date: March 2013 Previous Issues: Year: Summary Proved reserves

November 9, 2011 Harrisburg, PA

Pennsylvania Public Utility Commission Annual Winter Reliability Assessment Meeting Remarks by Terrance J. Fitzpatrick President & Chief Executive Officer Energy Association of Pennsylvania November 9,

Pennsylvania Public Utility Commission Annual Winter Reliability Assessment Meeting Remarks by Terrance J. Fitzpatrick President & Chief Executive Officer Energy Association of Pennsylvania November 9,

Short Term Energy Outlook March 2011 March 8, 2011 Release

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

Fortress America. A Resource Rich Island of Stability in a Sea of Turmoil. Presented by Jason Willan Director, Risk Management & Research

Fortress America A Resource Rich Island of Stability in a Sea of Turmoil Presented by Jason Willan Director, Risk Management & Research Disclaimer The data and information contained in this presentation

Fortress America A Resource Rich Island of Stability in a Sea of Turmoil Presented by Jason Willan Director, Risk Management & Research Disclaimer The data and information contained in this presentation

ENERGY OUTLOOK 2017 FALL/WINTER

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

Power & Politics Navigating the Changing Vision of Our Energy Future. Rayola Dougher, API Senior Economic Advisor,

Power & Politics Navigating the Changing Vision of Our Energy Future Rayola Dougher, API Senior Economic Advisor, dougherr@api.org U.S. oil and natural gas production is increasing as a result of technological

Power & Politics Navigating the Changing Vision of Our Energy Future Rayola Dougher, API Senior Economic Advisor, dougherr@api.org U.S. oil and natural gas production is increasing as a result of technological

U.S. Historical and Projected Shale Gas Production

U.S. Historical and Projected Shale Gas Production Phyllis Martin Phyllis Martin, Senior Energy Analyst Office of Petroleum, Gas and Biofuels Analysis U.S. Energy Information Administration phyllis.martin@eia.doe.gov

U.S. Historical and Projected Shale Gas Production Phyllis Martin Phyllis Martin, Senior Energy Analyst Office of Petroleum, Gas and Biofuels Analysis U.S. Energy Information Administration phyllis.martin@eia.doe.gov

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

Annual Energy Outlook 2017

Annual Energy Outlook 217 Valve Manufacturers Association of America VMA Technical Seminar 217 March 2, 217 Nashville, TN By, Director, Office of Integrated and International Energy Analysis U.S. Energy

Annual Energy Outlook 217 Valve Manufacturers Association of America VMA Technical Seminar 217 March 2, 217 Nashville, TN By, Director, Office of Integrated and International Energy Analysis U.S. Energy

DUAL PLENARY SESSION: FUTURE OUTLOOK FOR OIL & GAS PRODUCTION. North American Natural Gas Outlook

DUAL PLENARY SESSION: FUTURE OUTLOOK FOR OIL & GAS PRODUCTION United States Association for Energy Economics North American Natural Gas Outlook November 5, 212 R. Dean Foreman, Ph.D. Chief Economist Talisman

DUAL PLENARY SESSION: FUTURE OUTLOOK FOR OIL & GAS PRODUCTION United States Association for Energy Economics North American Natural Gas Outlook November 5, 212 R. Dean Foreman, Ph.D. Chief Economist Talisman

LNG Exports: A Brief Introduction

LNG Exports: A Brief Introduction Natural gas one of the world s most useful substances is burned to heat homes and run highly-efficient electrical powerplants. It is used as a feedstock in the manufacture

LNG Exports: A Brief Introduction Natural gas one of the world s most useful substances is burned to heat homes and run highly-efficient electrical powerplants. It is used as a feedstock in the manufacture

FROM RAILROAD COMMISSIONER RYAN SITTON

2018 E N E R G Y M A R K E T O U T L O O K FROM RAILROAD COMMISSIONER RYAN SITTON TABLE OF CONTENTS 2018 ENERGY MARKET OUTLOOK Summing up the analysis contained in this report in a few sentences, my prediction

2018 E N E R G Y M A R K E T O U T L O O K FROM RAILROAD COMMISSIONER RYAN SITTON TABLE OF CONTENTS 2018 ENERGY MARKET OUTLOOK Summing up the analysis contained in this report in a few sentences, my prediction

Crude Oil and Natural Gas Trade in North America: Anything New?

Crude Oil and Natural Gas Trade in North America: Anything New? André Plourde Department of Economics Faculty of Public Affairs Carleton University CRUDE OIL All data from US Energy Information Administration

Crude Oil and Natural Gas Trade in North America: Anything New? André Plourde Department of Economics Faculty of Public Affairs Carleton University CRUDE OIL All data from US Energy Information Administration

U.S. Shale Gas in Context

U.S. Shale Gas in Context Overview of U.S. Natural Gas production and trends For National Conference of State Legislatures Natural Gas Policy Institute September 9, 215 Pittsburgh, Pennsylvania By Grant

U.S. Shale Gas in Context Overview of U.S. Natural Gas production and trends For National Conference of State Legislatures Natural Gas Policy Institute September 9, 215 Pittsburgh, Pennsylvania By Grant

International Association for Energy Economics Luncheon Presentation April 21, 2004

International Association for Energy Economics Luncheon Presentation April 21, 2004 Recent Changes in the Natural Gas Market and the Need for More LNG in New England Mike Reimers, Weaver s Cove Energy,

International Association for Energy Economics Luncheon Presentation April 21, 2004 Recent Changes in the Natural Gas Market and the Need for More LNG in New England Mike Reimers, Weaver s Cove Energy,

Overview. Key Energy Issues to Economic Growth

Key Energy Issues to 225 The Energy Information Administration (EIA), in preparing model forecasts for its Annual Energy Outlook 25 (AEO25), evaluated a wide range of current trends and issues that could

Key Energy Issues to 225 The Energy Information Administration (EIA), in preparing model forecasts for its Annual Energy Outlook 25 (AEO25), evaluated a wide range of current trends and issues that could

NEXUS Gas Transmission

NEXUS Gas Transmission Bringing New Supplies to Market Ohio Manufacturers Association - October 2012 Agenda Project Introduction Utica and Marcellus Gas Supply Michigan and Ontario Markets Conclusion &

NEXUS Gas Transmission Bringing New Supplies to Market Ohio Manufacturers Association - October 2012 Agenda Project Introduction Utica and Marcellus Gas Supply Michigan and Ontario Markets Conclusion &

Annual Energy Outlook 2018 with projections to 2050

Annual Energy Outlook 218 with projections to 25 February 218 U.S. Energy Information Administration Office of Energy Analysis U.S. Department of Energy Washington, DC 2585 This publication is on the Web

Annual Energy Outlook 218 with projections to 25 February 218 U.S. Energy Information Administration Office of Energy Analysis U.S. Department of Energy Washington, DC 2585 This publication is on the Web

January 30, 2010 National Conference of State Legislatures Savannah, Georgia. Christopher B. McGill Managing Director, Policy Analysis

January 30, 2010 National Conference of State Legislatures Savannah, Georgia Christopher B. McGill Managing Director, Policy Analysis U.S. Natural Gas Supply and Infrastructure Additions Points of Discussion

January 30, 2010 National Conference of State Legislatures Savannah, Georgia Christopher B. McGill Managing Director, Policy Analysis U.S. Natural Gas Supply and Infrastructure Additions Points of Discussion

Outlook for the Oil and Gas Industry

Outlook for the Oil and Gas Industry VMA Market Outlook Workshop Boston, MA Spears& Associates Tulsa, OK August 2017 1 Outlook for the Oil and Gas Industry: Market Drivers Global oil consumption is forecast

Outlook for the Oil and Gas Industry VMA Market Outlook Workshop Boston, MA Spears& Associates Tulsa, OK August 2017 1 Outlook for the Oil and Gas Industry: Market Drivers Global oil consumption is forecast

Pennsylvania Public Utility Commission Annual Winter Reliability Assessment Meeting

Pennsylvania Public Utility Commission Annual Winter Reliability Assessment Meeting Energy Association of Pennsylvania November 4, 2010 Terrance J. Fitzpatrick President & CEO SUPPLY Winter 2010-2011 (all

Pennsylvania Public Utility Commission Annual Winter Reliability Assessment Meeting Energy Association of Pennsylvania November 4, 2010 Terrance J. Fitzpatrick President & CEO SUPPLY Winter 2010-2011 (all

October U.S. Energy Information Administration Winter Fuels Outlook October

October 2017 Winter Fuels Outlook EIA forecasts that average household expenditures for all major home heating fuels will rise this winter because of expected colder weather and higher energy costs. Average

October 2017 Winter Fuels Outlook EIA forecasts that average household expenditures for all major home heating fuels will rise this winter because of expected colder weather and higher energy costs. Average

ENERGY TRENDS: WHY JOBS, CAPITAL INVESTMENT & TRADE ARE HEATING UP

ENERGY TRENDS: WHY JOBS, CAPITAL INVESTMENT & TRADE ARE HEATING UP Tanya Bodell, Executive Director, Energyzt Once reigning as the King of Coal, the United States is now referred to as the Saudi Arabia

ENERGY TRENDS: WHY JOBS, CAPITAL INVESTMENT & TRADE ARE HEATING UP Tanya Bodell, Executive Director, Energyzt Once reigning as the King of Coal, the United States is now referred to as the Saudi Arabia

Natural Gas Pipeline and Storage Infrastructure Projections Through 2030

Natural Gas Pipeline and Storage Infrastructure Projections Through 2030 October 20, 2009 Submitted to: The INGAA Foundation, Inc. 10 G Street NE Suite 700 Washington, DC 20002 Submitted by: ICF International

Natural Gas Pipeline and Storage Infrastructure Projections Through 2030 October 20, 2009 Submitted to: The INGAA Foundation, Inc. 10 G Street NE Suite 700 Washington, DC 20002 Submitted by: ICF International

North American Gas: A dynamic environment. Josh McCall BP North American Gas and Power November 16, 2011

North American Gas: A dynamic environment Josh McCall BP North American Gas and Power November 16, 2011 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not

North American Gas: A dynamic environment Josh McCall BP North American Gas and Power November 16, 2011 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not

Annual Energy Outlook 2017 with projections to 2050

Annual Energy Outlook 217 with projections to 25 #AEO217 January 5, 217 Table of contents Page Overview/key takeaways 3 Critical drivers and uncertainty 31 Petroleum and other liquids 4 Natural gas 51

Annual Energy Outlook 217 with projections to 25 #AEO217 January 5, 217 Table of contents Page Overview/key takeaways 3 Critical drivers and uncertainty 31 Petroleum and other liquids 4 Natural gas 51

Major Challenges for Gas: What Can be Expected for Mexico?

Major Challenges for Gas: What Can be Expected for Mexico? Gas Future Forum, Mexico, April 3, 2014 BEG/CEE UT, 1 Overall Observations Resources Reserves Deliverability Deliverability is key Sweet spot

Major Challenges for Gas: What Can be Expected for Mexico? Gas Future Forum, Mexico, April 3, 2014 BEG/CEE UT, 1 Overall Observations Resources Reserves Deliverability Deliverability is key Sweet spot

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2012-13 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2012 Introduction This report presents ICF s

Winter 2012-13 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2012 Introduction This report presents ICF s

Technologies to recover it were refined as natural gas prices rose to $10 per MMBtu Locations of shale gas were known for decades

Technologies to recover it were refined as natural gas prices rose to $10 per MMBtu Locations of shale gas were known for decades Discovery rates are very high Reduces producer expenses Volume was greatly

Technologies to recover it were refined as natural gas prices rose to $10 per MMBtu Locations of shale gas were known for decades Discovery rates are very high Reduces producer expenses Volume was greatly

Durability of Eagle Ford Investment: How does the Eagle Ford Compare in North America?

Durability of Eagle Ford Investment: How does the Eagle Ford Compare in North America? March 27, 2013 Unconventional Development Activity North American Shale Plays Source: EIA 2 Converging Consumption

Durability of Eagle Ford Investment: How does the Eagle Ford Compare in North America? March 27, 2013 Unconventional Development Activity North American Shale Plays Source: EIA 2 Converging Consumption

Natural Gas. Smarter Power Today. Perspectives on the Future of Regulatory Policy Illinois State University. Springfield, IL October 25, 2012

Natural Gas Smarter Power Today. Perspectives on the Future of Regulatory Policy Illinois State University Springfield, IL October 25, 2012 ANGA Members 2 ABUNDANCE & PRICE STABILITY The Shale Gas Revolution

Natural Gas Smarter Power Today. Perspectives on the Future of Regulatory Policy Illinois State University Springfield, IL October 25, 2012 ANGA Members 2 ABUNDANCE & PRICE STABILITY The Shale Gas Revolution

Conventional and Unconventional Oil and Gas

Conventional and Unconventional Oil and Gas What is changing in the world? Iain Bartholomew, Subsurface Director Siccar Point Energy Discussion outline 1. Conventional oil and gas - E&P life-cycle - How

Conventional and Unconventional Oil and Gas What is changing in the world? Iain Bartholomew, Subsurface Director Siccar Point Energy Discussion outline 1. Conventional oil and gas - E&P life-cycle - How

Shale Gas and the Outlook for U.S. Natural Gas Markets and Global Gas Resources

Shale Gas and the Outlook for U.S. Natural Gas Markets and Global Gas Resources Organization for Economic Cooperation and Development (OECD) Richard Newell, Administrator June 21, 2011 Paris, France U.S.

Shale Gas and the Outlook for U.S. Natural Gas Markets and Global Gas Resources Organization for Economic Cooperation and Development (OECD) Richard Newell, Administrator June 21, 2011 Paris, France U.S.

Trends, Issues and Market Changes for Crude Oil and Natural Gas

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

U.S. natural gas prices after the shale boom

ENERGY ANALYSIS U.S. natural gas prices after the shale boom Kan Chen / Marcial Nava 9 March 218 Shale production fundamentally altered the relationship between oil and natural gas prices Although most

ENERGY ANALYSIS U.S. natural gas prices after the shale boom Kan Chen / Marcial Nava 9 March 218 Shale production fundamentally altered the relationship between oil and natural gas prices Although most

Shale Gas. A Game Changer for U.S. and Global Gas Markets? Flame European Gas Conference March 2, 2010, Amsterdam. Richard G. Newell, Administrator

Shale Gas A Game Changer for U.S. and Global Gas Markets? Flame European Gas Conference March 2, 2010, Amsterdam Richard G. Newell, Administrator Richard Newell, March SAIS, December 2, 2010 14, 2009 1

Shale Gas A Game Changer for U.S. and Global Gas Markets? Flame European Gas Conference March 2, 2010, Amsterdam Richard G. Newell, Administrator Richard Newell, March SAIS, December 2, 2010 14, 2009 1

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities.

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

North American Natural Gas Market Outlook

North American Natural Gas Market Outlook Energy Trends & Impacts On Gas Infrastructure Prepared For: Gas/Electric Partnership, Conference XVIII Darryl Rogers February 10, 2010 Agenda Introduction to Purvin

North American Natural Gas Market Outlook Energy Trends & Impacts On Gas Infrastructure Prepared For: Gas/Electric Partnership, Conference XVIII Darryl Rogers February 10, 2010 Agenda Introduction to Purvin

Ponzi Scheme Keeps US Market Well Supplied

www.poten.com June 30, 2011 Ponzi Scheme Keeps US Market Well Supplied Conjuring up images of the dot-com bubble of the late-1990s, the industry leveled charges of unprofessional journalism against a story

www.poten.com June 30, 2011 Ponzi Scheme Keeps US Market Well Supplied Conjuring up images of the dot-com bubble of the late-1990s, the industry leveled charges of unprofessional journalism against a story

Markets and Opportunities. Paul Burgener March 2015

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Outlook for Natural Gas Supply and Demand for Winter

Outlook for Natural Gas Supply and Demand for 2013-2014 Winter Energy Ventures Analysis, Inc. (EVA) Executive Summary The outlook for both natural gas supply and demand for the forthcoming winter is very

Outlook for Natural Gas Supply and Demand for 2013-2014 Winter Energy Ventures Analysis, Inc. (EVA) Executive Summary The outlook for both natural gas supply and demand for the forthcoming winter is very

Major Changes in Natural Gas Transportation Capacity,

Major Changes in Natural Gas Transportation, The following presentation was prepared to illustrate graphically the areas of major growth on the national natural gas pipeline transmission network between

Major Changes in Natural Gas Transportation, The following presentation was prepared to illustrate graphically the areas of major growth on the national natural gas pipeline transmission network between

Overview of LNG in the United States

Overview of LNG in the United States Dan McGinnis, Vice President of Gas Infrastructure Tractebel Project Development Inc. Natural Gas Conference Louisiana State University October 27, 2003 What Is Liquefied

Overview of LNG in the United States Dan McGinnis, Vice President of Gas Infrastructure Tractebel Project Development Inc. Natural Gas Conference Louisiana State University October 27, 2003 What Is Liquefied

Steady Wins TORTOISE TALK

Steady Wins TORTOISE TALK October 2014 October 2014 Third quarter 2014: short-term headwinds As 2014 begins to wind to a close, the U.S. energy boom continues, despite challenges that include an intensifying

Steady Wins TORTOISE TALK October 2014 October 2014 Third quarter 2014: short-term headwinds As 2014 begins to wind to a close, the U.S. energy boom continues, despite challenges that include an intensifying

C9-19. Slide 1. markets later in the presentation.

C9-19 Slide 1 Mr. Chairman, Commissioners. Today I am pleased to present the Office of Enforcement's Winter 2011-2012 Energy Market Assessment. The Winter Energy Assessment is staff's opportunity to share

C9-19 Slide 1 Mr. Chairman, Commissioners. Today I am pleased to present the Office of Enforcement's Winter 2011-2012 Energy Market Assessment. The Winter Energy Assessment is staff's opportunity to share

Annual Energy Outlook 2018

Annual Energy Outlook 218 Columbia University, Center on Global Energy Policy February 13, 218 New York, NY John J. Conti, Deputy Administrator U.S. Energy Information Administration U.S. Energy Information

Annual Energy Outlook 218 Columbia University, Center on Global Energy Policy February 13, 218 New York, NY John J. Conti, Deputy Administrator U.S. Energy Information Administration U.S. Energy Information

Greg Hathaway Energy Source Holdings, LLC

Greg Hathaway Energy Source Holdings, LLC WEATHER THE PICTURE TO THE RIGHT SHOWS THE 2015-16 WINTER HAS BEEN MUCH ABOVE NORMAL. SINCE 2008 THE NATIONAL TEMPERATURE HAS BEEN BELOW NORMAL SIX TIMES 2013-14

Greg Hathaway Energy Source Holdings, LLC WEATHER THE PICTURE TO THE RIGHT SHOWS THE 2015-16 WINTER HAS BEEN MUCH ABOVE NORMAL. SINCE 2008 THE NATIONAL TEMPERATURE HAS BEEN BELOW NORMAL SIX TIMES 2013-14

MEMORANDUM. May 6, Subcommittee on Energy and Power Democratic Members and Staff

FRED UPTON, MICHIGAN CHAIRMAN HENRY A. WAXMAN, CALIFORNIA RANKING MEMBER ONE HUNDRED THIRTEENTH CONGRESS Congress of the United States House of Representatives COMMITTEE ON ENERGY AND COMMERCE 2125 RAYBURN

FRED UPTON, MICHIGAN CHAIRMAN HENRY A. WAXMAN, CALIFORNIA RANKING MEMBER ONE HUNDRED THIRTEENTH CONGRESS Congress of the United States House of Representatives COMMITTEE ON ENERGY AND COMMERCE 2125 RAYBURN

OUR CONVERSATION TODAY

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

Atlantic LNG: Has the boat sailed? Is the US out of the LNG trade and what are the implications for Europe?

Atlantic LNG: Has the boat sailed? Is the US out of the LNG trade and what are the implications for Europe? James Osten Principal North American Energy Markets LNG Trade Different for U.S. Than Europe

Atlantic LNG: Has the boat sailed? Is the US out of the LNG trade and what are the implications for Europe? James Osten Principal North American Energy Markets LNG Trade Different for U.S. Than Europe

First Person From Moonbeam Gas to Shale Revolution to What s Next

EPRI JOURNAL September/October 2016 10 First Person From Moonbeam Gas to Shale Revolution to What s Next What Plentiful, Low-Cost Natural Gas Means for the Electric Power Sector The Story in Brief Vello

EPRI JOURNAL September/October 2016 10 First Person From Moonbeam Gas to Shale Revolution to What s Next What Plentiful, Low-Cost Natural Gas Means for the Electric Power Sector The Story in Brief Vello

Global Energy Assessment: Shale Gas and Oil

Global Energy Assessment: Shale Gas and Oil KEEI September, 2014 Yonghun Jung Shale Gas: a new source of energy Shale gas deposits around the world vs. 2009 natural gas consumption (tcf) U.S. 862 22.8

Global Energy Assessment: Shale Gas and Oil KEEI September, 2014 Yonghun Jung Shale Gas: a new source of energy Shale gas deposits around the world vs. 2009 natural gas consumption (tcf) U.S. 862 22.8

Natural Gas Opportunities

Natural Gas Opportunities NAFTANEXT Summit Chicago, IL Erica Bowman, Chief Economist April 25, 2014 U.S. Natural Gas Reserves Source: Potential Gas Committee Abundant Supply Estimates of U.S. Recoverable

Natural Gas Opportunities NAFTANEXT Summit Chicago, IL Erica Bowman, Chief Economist April 25, 2014 U.S. Natural Gas Reserves Source: Potential Gas Committee Abundant Supply Estimates of U.S. Recoverable

Shale Gas as an Alternative Petrochemical Feedstock

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Natural Gas. Tuesday, May 1, 2012; 4:00 PM 5:15 PM

Natural Gas Tuesday, May 1, 2012; 4:00 PM 5:15 PM Moderator: Joel Kurtzman, Senior Fellow and Executive Director of the Center for Accelerating Energy Solutions, Milken Institute Speakers: Ralph Eads,

Natural Gas Tuesday, May 1, 2012; 4:00 PM 5:15 PM Moderator: Joel Kurtzman, Senior Fellow and Executive Director of the Center for Accelerating Energy Solutions, Milken Institute Speakers: Ralph Eads,

Gas s Pipeline to Sustainability:

Gas s Pipeline to Sustainability: An Update on Gas Markets September 28, 2017 An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer

Gas s Pipeline to Sustainability: An Update on Gas Markets September 28, 2017 An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK. Executive Summary.

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK Executive Summary ST98 www.aer.ca EXECUTIVE SUMMARY The Alberta Energy Regulator (AER) ensures the safe, efficient, orderly, and environmentally

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK Executive Summary ST98 www.aer.ca EXECUTIVE SUMMARY The Alberta Energy Regulator (AER) ensures the safe, efficient, orderly, and environmentally

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK. Executive Summary.

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK Executive Summary ST98 www.aer.ca EXECUTIVE SUMMARY The Alberta Energy Regulator (AER) ensures the safe, efficient, orderly, and environmentally

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK Executive Summary ST98 www.aer.ca EXECUTIVE SUMMARY The Alberta Energy Regulator (AER) ensures the safe, efficient, orderly, and environmentally

SHALE DEVELOPMENT TRENDS AND IMPLICATIONS ON VALVE NEEDS JOHN D. SELDENRUST, VICE PRESIDENT-ENGINEERING & CONSTRUCTION

SHALE DEVELOPMENT TRENDS AND IMPLICATIONS ON VALVE NEEDS JOHN D. SELDENRUST, VICE PRESIDENT-ENGINEERING & CONSTRUCTION WHAT IS UNCONVENTIONAL GAS? Gas that is more difficult or less economical to extract

SHALE DEVELOPMENT TRENDS AND IMPLICATIONS ON VALVE NEEDS JOHN D. SELDENRUST, VICE PRESIDENT-ENGINEERING & CONSTRUCTION WHAT IS UNCONVENTIONAL GAS? Gas that is more difficult or less economical to extract

Economic Determinants of the Global Natural Gas Balance*

Economic Determinants of the Global Natural Gas Balance* Kenneth B. Medlock III 1 Search and Discovery Article #70104 (2011) Posted July 26, 2011 *Adapted from oral presentation at AAPG Annual Convention

Economic Determinants of the Global Natural Gas Balance* Kenneth B. Medlock III 1 Search and Discovery Article #70104 (2011) Posted July 26, 2011 *Adapted from oral presentation at AAPG Annual Convention

AEO2005 Overview. Key Energy Issues to Economic Growth

Key Energy Issues to 225 The Energy Information Administration (EIA), in preparing model forecasts for its Annual Energy Outlook 25 (AEO25), evaluated a wide range of current trends and issues that could

Key Energy Issues to 225 The Energy Information Administration (EIA), in preparing model forecasts for its Annual Energy Outlook 25 (AEO25), evaluated a wide range of current trends and issues that could

The Outlook for the Global LPG Market

The Outlook for the Global LPG Market International LP Gas Seminar 213 Ken Otto February 28, 212 Dai-Ichi Hotel Tokyo, Japan 212, IHS Inc. No portion of this presentation may be reproduced, reused, or

The Outlook for the Global LPG Market International LP Gas Seminar 213 Ken Otto February 28, 212 Dai-Ichi Hotel Tokyo, Japan 212, IHS Inc. No portion of this presentation may be reproduced, reused, or

Drilling Deeper: A Reality Check on U.S. Government Forecasts for a Lasting Tight Oil & Shale Gas Boom. Web Briefing December 9, 2014

Drilling Deeper: A Reality Check on U.S. Government Forecasts for a Lasting Tight Oil & Shale Gas Boom Web Briefing December 9, 214 J. David Hughes Post Carbon Institute Global Sustainability Research

Drilling Deeper: A Reality Check on U.S. Government Forecasts for a Lasting Tight Oil & Shale Gas Boom Web Briefing December 9, 214 J. David Hughes Post Carbon Institute Global Sustainability Research

The US shale revolution and its economic impact

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

Regional Gas Market Update

April 26, 2018 Milford, MA Regional Gas Market Update Presentation to: ISO-NE Planning Advisory Committee Tom Kiley Northeast Gas Association 1 Topic Areas Natural gas safety message. Recent market growth,

April 26, 2018 Milford, MA Regional Gas Market Update Presentation to: ISO-NE Planning Advisory Committee Tom Kiley Northeast Gas Association 1 Topic Areas Natural gas safety message. Recent market growth,

Gulf Coast Energy Outlook

Gulf Coast Energy Outlook Gregory B. Upton Jr., Ph.D. Louisiana State University Center for Energy Studies St. James Community Advisory Panel Meeting Gramercy, LA. June 6, 2017 Introduction Consensus Price

Gulf Coast Energy Outlook Gregory B. Upton Jr., Ph.D. Louisiana State University Center for Energy Studies St. James Community Advisory Panel Meeting Gramercy, LA. June 6, 2017 Introduction Consensus Price

The Economic and Budgetary Effects of Producing Oil and Natural Gas From Shale

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 12-2014 The Economic and Budgetary Effects of Producing Oil and Natural Gas From Shale Congressional Budget

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 12-2014 The Economic and Budgetary Effects of Producing Oil and Natural Gas From Shale Congressional Budget

SPECIAL MONTHLY REPORT ON. ENERGY (Aug 2016)

") SPECIAL MONTHLY REPORT ON () PERFORMANCE (July 2016) (% change) NYMEX -13.93-1.37 Natural Gas Crude oil MCX -15.80-2.23-18.00-16.00-14.00-12.00-10.00-8.00-6.00-4.00-2.00 0.00 Source: Reuters & SMC PERFORMANCE

SPECIAL MONTHLY REPORT ON () PERFORMANCE (July 2016) (% change) NYMEX -13.93-1.37 Natural Gas Crude oil MCX -15.80-2.23-18.00-16.00-14.00-12.00-10.00-8.00-6.00-4.00-2.00 0.00 Source: Reuters & SMC PERFORMANCE

U.S. Natural Gas A Decade of Change and the Emergence of the Gas-Centric Future

AIChE Alternative Natural Gas Applications Workshop U.S. Natural Gas A Decade of Change and the Emergence of the Gas-Centric Future Francis O Sullivan October 8 th, 214 1 Natural gas The new unconventional

AIChE Alternative Natural Gas Applications Workshop U.S. Natural Gas A Decade of Change and the Emergence of the Gas-Centric Future Francis O Sullivan October 8 th, 214 1 Natural gas The new unconventional

North American Natural Gas: A Crisis Ahead Or Is Chicken Little Running Around Again?

North American Natural Gas: A Crisis Ahead Or Is Chicken Little Running Around Again? Ron Denhardt Vice President, Natural Gas Services February 2003 Strategic Energy & Economic Research Inc. 781 756 0550

North American Natural Gas: A Crisis Ahead Or Is Chicken Little Running Around Again? Ron Denhardt Vice President, Natural Gas Services February 2003 Strategic Energy & Economic Research Inc. 781 756 0550

The Unconventional Reservoirs Revolution and the Rebirth of the U.S. Onshore Oil & Gas Industry

The Unconventional Reservoirs Revolution and the Rebirth of the U.S. Onshore Oil & Gas Industry Feb. 19, 2013 Cautionary Statement The following presentation includes forward-looking statements. These

The Unconventional Reservoirs Revolution and the Rebirth of the U.S. Onshore Oil & Gas Industry Feb. 19, 2013 Cautionary Statement The following presentation includes forward-looking statements. These

U.S. oil and natural gas outlook

U.S. oil and natural gas outlook New York, NY By Adam Sieminski, EIA Administrator U.S. Energy Information Administration Independent Statistics & Analysis www.eia.go v The U.S. has experienced a rapid

U.S. oil and natural gas outlook New York, NY By Adam Sieminski, EIA Administrator U.S. Energy Information Administration Independent Statistics & Analysis www.eia.go v The U.S. has experienced a rapid

Gulf Coast Energy Outlook

Gulf Coast Energy Outlook Gregory B. Upton Jr., Ph.D. Louisiana State University Center for Energy Studies East Iberville Community Advisory Panel Meeting March 23, 2017 Introduction Consensus Price Outlook

Gulf Coast Energy Outlook Gregory B. Upton Jr., Ph.D. Louisiana State University Center for Energy Studies East Iberville Community Advisory Panel Meeting March 23, 2017 Introduction Consensus Price Outlook

The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports.

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

Natural Gas Outlook and Drivers

Natural Gas Outlook and Drivers November 2012 33% BENTEK Energy 5% 40% Who We Are Based in Evergreen, CO 120 People 400+ Customers Subsidiary of McGraw-Hill/Platts 22% What We Do Collect, Analyze and Distribute

Natural Gas Outlook and Drivers November 2012 33% BENTEK Energy 5% 40% Who We Are Based in Evergreen, CO 120 People 400+ Customers Subsidiary of McGraw-Hill/Platts 22% What We Do Collect, Analyze and Distribute

Gas and Crude Oil Production Outlook

Gas and Crude Oil Production Outlook COQA/CCQTA Joint meeting October 3-31, 214 San Francisco, California By John Powell Office of Petroleum, Natural Gas, and Biofuels Analysis U.S. Energy Information

Gas and Crude Oil Production Outlook COQA/CCQTA Joint meeting October 3-31, 214 San Francisco, California By John Powell Office of Petroleum, Natural Gas, and Biofuels Analysis U.S. Energy Information

CenterPoint Energy Services. Current Market Fundamentals June 27, 2013

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

Shale Gas Report Ed 1, 2011

Market Intelligence Shale Gas Report Ed 1, 2011 Shale gas has been a game changer in the US changing the country from being reliant on imports for the foreseeable future to being able to meet demand from

Market Intelligence Shale Gas Report Ed 1, 2011 Shale gas has been a game changer in the US changing the country from being reliant on imports for the foreseeable future to being able to meet demand from

American Strategy and US Energy Independence

Cordesman: Strategy and Energy Independence 10/21/13 1 American Strategy and US Energy Independence By Anthony H. Cordesman October 21, 2013 Changes in energy technology, and in the way oil and gas reserves

Cordesman: Strategy and Energy Independence 10/21/13 1 American Strategy and US Energy Independence By Anthony H. Cordesman October 21, 2013 Changes in energy technology, and in the way oil and gas reserves

Aspen Energy Orientation Training. Intro to Natural Gas

Aspen Energy Orientation Training Intro to Natural Gas Order 636 (April 8, 1992), required pipelines to "un-bundle" their services and to offer and price these services separately. Order 636 ended the

Aspen Energy Orientation Training Intro to Natural Gas Order 636 (April 8, 1992), required pipelines to "un-bundle" their services and to offer and price these services separately. Order 636 ended the

NARUC. Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

Impacts of Canadian Electricity and Gas Exports in the United States

Impacts of Canadian Electricity and Gas Exports in the United States for Natural Resources Canada Prepared by Ziff Energy 01GC-2021-03 1117 Macleod Trail S.E. Calgary, Alberta T2G 2M8 Tel: (403) 265-0600

Impacts of Canadian Electricity and Gas Exports in the United States for Natural Resources Canada Prepared by Ziff Energy 01GC-2021-03 1117 Macleod Trail S.E. Calgary, Alberta T2G 2M8 Tel: (403) 265-0600

Energy and Economic Update for Louisiana and the Gulf Coast Region

Energy and Economic Update for Louisiana and the Gulf Coast Region Gregory B. Upton Jr., Ph.D. Louisiana State University Center for Energy Studies Kinetica Partners, LLC 2018 Shipper s Meeting Lake Charles,

Energy and Economic Update for Louisiana and the Gulf Coast Region Gregory B. Upton Jr., Ph.D. Louisiana State University Center for Energy Studies Kinetica Partners, LLC 2018 Shipper s Meeting Lake Charles,

U.S. EIA s Liquid Fuels Outlook

U.S. EIA s Liquid Fuels Outlook NCSL 2011 Energy Policy Summit: Fueling Tomorrow s Transportation John Staub, Team Lead August 8, 2011 San Antonio, Texas U.S. Energy Information Administration Independent

U.S. EIA s Liquid Fuels Outlook NCSL 2011 Energy Policy Summit: Fueling Tomorrow s Transportation John Staub, Team Lead August 8, 2011 San Antonio, Texas U.S. Energy Information Administration Independent

Shale Gas - From the Source Rock to the Market: An Uneven pathway. Tristan Euzen

Shale Gas - From the Source Rock to the Market: An Uneven pathway Tristan Euzen Shale Gas Definition Seal Conventional Oil & Gas Tight Gas Source Rock Reservoir (Shale Gas) Modified from Williams 2013

Shale Gas - From the Source Rock to the Market: An Uneven pathway Tristan Euzen Shale Gas Definition Seal Conventional Oil & Gas Tight Gas Source Rock Reservoir (Shale Gas) Modified from Williams 2013